table of contents - · pdf filetable of contents executive suammry ... (spm) and the progress...

TRANSCRIPT

2

Table of Contents

Executive Suammry....................................................................................................................................3

1.1 Introduction...................................................................................................................................4

2.0 The Social Performance Assessment Result...................................................................................5

2.1 Gambia Police Force Cooperative Credit Union (GPFCCU), Banjul...........................................5

2.2 Banjul International Airport Cooperative Credit Union (BIACCU), Kanifing..............................7

2.3 Jambanjelly Community Cooperative Credit Union, West Coast Region..................................9

2.4 Foni Kansala Community Cooperative Credit Union, West Coast Region.................................11

2.5 Fangdema Community Cooperative Credit Union, Kanifing Municipality...............................13

2.6 Sabunima Community Cooperative Credit Union, Bansang.....................................................15

2.7 Dampha Kunda Community Cooperative Credit Union, Basse.................................................17

2.8 Foni Berefet Community Cooperative Credit Union, West Coast region.................................19

2.9 Fandema Kerewan Community Cooperative Credit Union, North Bank Region......................20

2.10 Brufut Badala Kafo Community Cooperative Credit Union....................................................22

2.11 Sofora Community Cooperative Credit Union.......................................................................24

2.12 Jokadu Community Cooperative Credit Union.......................................................................26

2.13 Gambia Ports Authority Cooperative Credit Union...............................................................27

3.0 The Progress Out of Poverty Index (PPI) Result............................................................................30

4.0 Conclusion and

Recommendation.................................................................................................331

3

Executive Summary

The Social Performance Assessment for 13 sampled Credit Unions was completed through the

active support and participation of the Board, staff and members of NACCUG and the Credit

Unions in the institutions and communities visited.

The process included a training on Social Performance Management (SPM) and the Progress

Out of Poverty (PPI) for the staff of NACCUG and all participants at the assessment meetings for

better understanding and appreciation of the process. This was followed by the Social

Performance Assessments of the individual Credit Unions with the use of the ILCUF Assessment

tool developed for the Credit Unions. The PPI form developed for Gambia was also

administered on 101 new members of the sampled Credit Unions in the urban and rural areas.

The assessment result shows that there is limited knowledge on the concept of social

performance and its management across the 13 CUs assessed. This has influenced the low

scores made by the CUs. The report of the individual CUs performance is presented from the

highest to the lowest score for easy flow of reading. The average score of all the CUs overall

Social Performance is 40%. The individual scores starting from the highest is 50% scored by the

Gambia Police Force Cooperative Credit Unions (GPFCCU), followed by Banjul International

Airport Cooperative Credit Union (BIACCU) with 48%; Jambanjelly Community Credit Union with

44%, Foni Kansala Community Credit Union with 43%. Three community credit unions namely,

Fangdema Community Credit Union in Jeshwang, Sambunima Community Credit Union in

Bansang and Dampha Kunda Community Credit in Basse scored 40% each, Foni Berefet and

Fandema in Kerewan scored 38% each, Brufut Badala Kafoo and Sofora Community Credit

Unions scored 37% each, Jokadu Credit Union in Kuntair scored 33% and Gambia Ports

Authority Cooperative Credit Union scored 31%, which is the lowest.

The results of the PPI form administered with a sample of 101 new members reveals that 42%

of them live below the National Poverty Line while 58% live above it. Based on an international

poverty benchmark, 18% of the new members live below the $1.25 per day and 82% live above

it. Furthermore, an analysis on a regional basis (urban and rural) indicates that 28% of the 20

new members in the urban areas live below the national poverty line while 72% of them live

above it. For the 81 new members in the rural areas, 45% of them live below the national

poverty line while 55% of them live above it. Using the international benchmark, 9% of the 20

new members in the urban area live below the $1.25 per day while 91% of them live above it.

For the 81 new rural members, 21% of them live below the $1.25 per day while 79% of them

live above it. This shows that the CUs are reaching the poor within the communities fulfilment

of their social mission of poverty alleviation, although more can be done to expand the

outreach to more poorer people. Recommendations are provided as part of the conclusion

which can improve the social performance management of the CUs in the near future.

4

1.0 Introduction

The National Association of Cooperative Credit Unions of the Gambia (NACCUG) is one of the

beneficiaries of the West Africa Credit Union Project against Poverty (WACUPP) funded by the ACP/EU

Microfinance, identified to participate in the Social Performance Management (SPM) process, one of the

deliverables of the project. The process includes a training of NACCUG staff and Board on SPM, a pilot

SPM assessment of a selected number of CUs across the country using the ILCUF tool developed and a

poverty assessment of a one hundred new clients using the PPI tool developed for Gambia. The Gambia

is yet to develop a PPI as done by other countries, for the purpose of the pilot poverty assessment of the

sampled new CU clients; a PPI was developed for Gambia drawn from the PPI of Senegal and Sierra

Leone and the PAT of Senegal.

The SPM assessment and PPI administration was preceded by the participation of Yaya Colley, NACCUG

Programme Officer and Ndella Faye-Colley, the external facilitator in a SPM training held in Kasoa, at the

Credit Union Training Centre in Ghana from 25th to 29th November 2013. Upon the return of the two

from Ghana, the work plan developed in Ghana was reviewed with NACCUG’s management team and

agreed for implementation within a period of one month from the 10th of December 2013 to the 10th of

January 2014.

1.1 The SPM Assessment Process

The SPM assessment process included a selection of 13 out of 67 Credit Unions drawn from across the

entire country. The number of CUs and total membership by chapter influenced the number of the CUs

selected from each chapter. To give all the CUs an equal chance to be selected as one of the pilot CUs

from all the geographical regions where NACCUG operates, the Random Number Generator was

programmed to randomly select the numbers for CUs chapter by chapter.

The Banjul chapter has 10 CUs with a total membership of 23,050. Two CUs were randomly selected

using a random number generator within the range of 1 to 10. The selected CUs were the Gambia Police

Force and Gambia Ports Authority respectively. The same process was used to select the CUs for the

other chapters. This resulted to three CUs for the KMC chapter including Banjul International Airport,

Fangdema Jeshwang and Sofora respectively, two for the Brikama chapter selected Jambanjelly and

Brufut Badala Kafo; two CUs selected for the Foni chapter were Foni Berefet and Foni Kansala District;

two CUs selected for the North Bank region were Fandema Kerewan and Jokadu District and the two

CUs selected for the Bansang/ Basse chapter were Sabunima in Bansang and Dampha Kunda in Basse.

The SPM assessment process was preceded by a one day training on SPM and the PPI for the NACCUG staff including field officers to enhance their understanding and appreciation of the assessment process. The administration process of the PPI form was also discussed in detail to provide the requisite skills for the field officers for its administration. A simulation exercise was made during the training through the administration of the form with one participant. The process was observed by other participants and comments were shared on how to do it better in the field. The result was also discussed which enhanced the understanding of the interpretation of the results.

5

2.0 The Social Performance Assessment Results

Social Performance as defined by the Social Performance Taskforce is “the effective translation of an institutions mission into practice in line with accepted social values”. Social Performance Management is “the processes an institution uses to translate its mission into practice”. It is agreed that different institutions working in microfinance including the credit union movement has different mission statements that they aim to achieve. Therefore Social performance management is being promoted to support the CUs to achieve their own social missions and goals by putting time and effort alongside the financial goals. The SPM assessment of the selected CUs is aimed to assess the Social Performance Management Status of the Credit Union using the ILCUF assessment tool developed. The assessment tool covers six areas seen as critical for Credit Union and these include: Outreach and Inclusion, Members Benefit and Welfare, Governance, Responsibility to Staff and Volunteer, Community and Environment and Cooperation among Cooperatives. All the assessment processes with the individual CUs were preceded by a presentation on SPM and its importance to the CUs and the PPI as a poverty measurement tool prior to the assessment. This facilitated an understanding and appreciation of the assessment process. The assessments were attended by some board, committees, staff and volunteers of each individual CU. The result for each individual CU is discussed individually and an analysis of the result and recommendations are provided as the conclusion.

2.1 Gambia Police Force Cooperative Credit Union (GPFCCU) GPFCCU is an institutional based credit union which comprised of staff working with the Ministry of Interior. These include the police force, the prison service, the immigration service and the fire and rescue service and the National Drug and Enforcement Agency. It was established in 2003 and has a total membership of 8626. GPFCCUs overall SPM score is 50% as shown in Box 1 which is the highest score among all the 13 CUs assessed. Figure 1 shows the graphic summary of the overall social performance result. Outreach & Inclusion

Its membership is open to all interior staff

The common bond is extended to their wives

It specifically targets the newest recruits who are assumed to be poorer with less income and assets.

It does not use a poverty measurement tool to screen the poverty levels of members and has no poverty outreach goals.

Women reached are estimated to be more than 30% of the membership.

The youth (less than 25yrs) is estimated to be more than 20% based on the large number of new recruits who are younger and targeted by the CU.

Membership data is collected but limited to name, address, next of kin amount to be saved, gender and age is not collected.

6

Figure 1: Overall SPM Result Box 1: Summary of SPM Result

Member Benefit and Welfare

GPFCCU is one of the two CUs among the sampled 13 with a Code of Ethics which is being used.

It has only one standard savings product and an appraisal system for loan process.

There is transparency in the cost of loan which is discussed with members during meetings and during the loan application process. A Loan Analysis form is filled and attached which indicates the cost of the loan.

The interest is 18% which is above the average for the other CUs but less than the other microfinance institution.

Trainings are provided to members on adhoc basis and linkage services are provided on a case by case basis.

Governance

GPFCCU does have a strategic or business plan without explicit social objectives and indicators to measure change in members.

It has an MIS system that captures the limited data collected and there are plans to upgrade it.

It has less women on the board and senior management estimated at less than 20%.

It has a strong democratic control which is demonstrated through regular AGMs with one member one vote principle. It also uses notice board for communication to members.

The board has no awareness on social performance concepts

It has a code of conduct for the board.

Staff and Volunteer

Basic Data on GPFCCU

Year established: 2003

Total membership: 8626

Deposit mobilised (Sept 2013): D73, 436,463.48

Loan Outstanding (Sept 2013): D76, 354,111.88

SPM Dimensions Scores

1) 25% Outreach &Targeting: 9%

2) 25% Member Benefit/Welfare: 9%

3) 20% Governance: 9%

4) 10% Staff & Volunteers: 7%

5) 10% Community & Environment: 7%

6)10% Cooperation among Cooperatives: 10%

Overall SPM Score: 50%

7

GPFCCU has an office with facilities and employed staff.

Staff and volunteers are sent for external trainings organised by the Apex and tertiary institutions in addition to trainings received on the job.

There is no formal staff grievance/feedback system, an informal verbal report is given to the board for redress.

There is no staff appraisal process in place.

Volunteerism is promoted especially in skills development which is manifested through the work of the board and committees.

Community and Environment

GFPCCU promotes community development initiatives and examples of these are provision of dustbins to the police station for environmental cleanliness, logistics support to the Drug Control Squad, construction of the clinic at the Fire and Rescue Services at Churchills Town and refurbished and furnished the police headquarters conference hall.

It prohibits the financing of harmful activities based on the loan policy but does not have a specific policy for it.

It does not include environmental education in trainings provided to members.

Cooperation among Cooperatives

GPFCCU got the 10% score because it is a member to the Apex, fulfils all reporting requirements and always participates in all activities they are invited by the Apex.

It cooperates with other credit unions and provides financial, technical and material support to them such as Sofora, Fangdema and the Banjulanding community study group.

3.2 Banjul International Airport Cooperative Credit Union (BIACCU)

BIACCU is an institutional credit union for staff and others working with the various institutions within the Banjul International Airport. It was established in 1999 and has a total membership of 1205. BIACCU’s overall SPM score is 49% as shown in box 2 which is the second highest score among all the sampled 13 CUs assessed. Figure 2 shows a graphic summary of the overall social performance result. Outreach and Inclusion

The membership is open to all including institutional staff, the airport taxi drivers and the vendors.

The common bond is also extended to the family members and there are indications that the surrounding communities close to the airport are being targeted for outreach.

It does not use a poverty measurement tool to screen the poverty levels of members and no poverty outreach goals.

Membership data is collected but not detail and limited to name, contact address, next of kin and amount to be saved but gender and age is not collected.

The women outreached is estimated to be more than 30% of the membership

This exercise has left some

footprint in our thinking as a

Credit Union,

General Manager, GPFCCU

8

Data on age is not collected but the youth (less than 25yrs) are estimated to be more than 5% but less than 20% among the members.

It is located within the served areas with other financial service providers in place.

Figure 2: Overall SPM Result Box 2: Summary of SPM Scores

Member Benefit and Welfare

BIACCU does not have a code of ethics to safeguard unethical treatment of members

It has only one standard savings product.

There is a standard appraisal procedure used during the loan application process in addition to consultation with employers of loan applicants to check for any liability before approval.

There is transparency in the cost of loans which is discussed with members at meetings and during the loan application process.

The annual interest rate charged on loan is 18% which is above the average for the other CUs but less than the other microfinance institution.

Trainings are provided to members on adhoc basis and linkage/referal services are provided on a case by case basis.

Governance

BIACCU has a draft strategic plan with objectives and indicators to measure but the social goals and indicators are not explicit.

Basic Data on BIACCU

Year established: 1999

Total membership: 1205

Deposit mobilised (Sept 2013): D14,836,155.86

Loan Outstanding (Sept 2013): D13,127,873.55

SPM Dimensions Scores

1) 25% Outreach & Targeting: 7%

2) 25% Member Benefit/Welfare: 14%

3) 20% Governance: 13%

4) 10% Staff & Volunteers: 7%

5) 10% Community & Environment: 0%

6)10% Cooperation among Cooperatives: 7%

Overall SPM Score: 48%

9

No strategy is developed for managing growth, but monthly audit reports are produced for board meetings to review the growth or otherwise of the CU for action.

There is no monitoring of changes in members lives but their savings and loans patterns are monitored.

The salary of staff is more than 5 times but less than 20 times.

The representation of women on the board and senior management is more than 20%.

It has a strong democratic control which is demonstrated through regular AGMs with one member one vote principle.

There is no board awareness on social performance concepts but it is believed that they unconsciously follow a social performance agenda.

There is no code of conduct for the board but the bye-laws are used to guide the work of the board.

Staff and Volunteer

BIACCU has an office with facilities and two employed staff and a volunteer.

The staff is sent for external trainings organised by Apex and tertiary institutions in addition to trainings received on the job.

There is no formal staff grievance/feedback system in place, but feedback is verbally given to the board for redress.

There is no staff appraisal process in place.

Volunteerism is promoted with skills development for the board and the volunteer working with the staff.

Community and Environment

BIACCU has a 0% score on this because it does not initiate or support community development initiatives and is not even aware that this is done by other CUs.

It does not have any policy on the prevention of financing of harmful activities except those based on the loan policy.

It does not include environmental education in trainings provided to members to enhance environmental protection.

Cooperation among Cooperatives

BIACCU is a member to the Apex, fulfils all reporting requirements and always participates in all activities they are invited.

It does not collaborate or work with other CUs.

3.3 Jambanjelly Community Credit Union

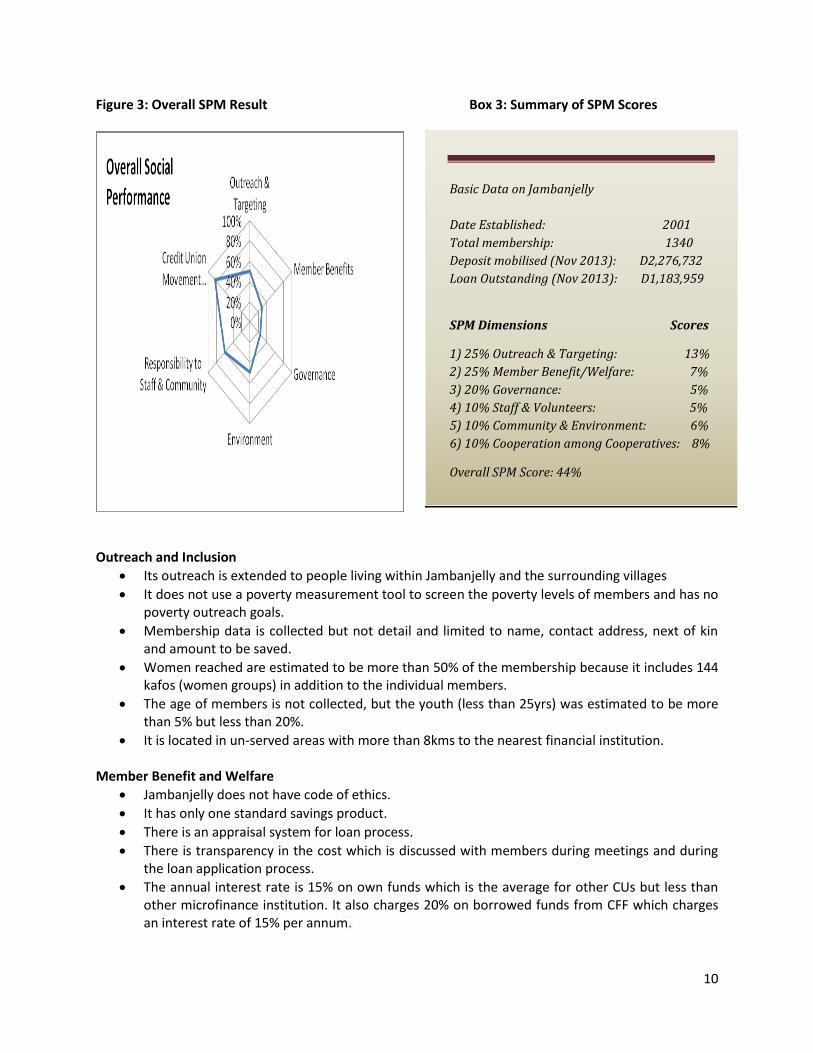

The Jambanjelly Credit Union is a community based credit union located within Jambanjelly in the West Coast Region. It was established in 2001 and has a total membership of 1340. Jambanjelly’s overall SPM score is 44% as shown in Box 3 and is the third highest score among the 13 sample CUs assessed. Figure 3 shows the graphic summary of the overall social performance result.

10

Figure 3: Overall SPM Result Box 3: Summary of SPM Scores

Outreach and Inclusion

Its outreach is extended to people living within Jambanjelly and the surrounding villages

It does not use a poverty measurement tool to screen the poverty levels of members and has no poverty outreach goals.

Membership data is collected but not detail and limited to name, contact address, next of kin and amount to be saved.

Women reached are estimated to be more than 50% of the membership because it includes 144 kafos (women groups) in addition to the individual members.

The age of members is not collected, but the youth (less than 25yrs) was estimated to be more than 5% but less than 20%.

It is located in un-served areas with more than 8kms to the nearest financial institution.

Member Benefit and Welfare

Jambanjelly does not have code of ethics.

It has only one standard savings product.

There is an appraisal system for loan process.

There is transparency in the cost which is discussed with members during meetings and during the loan application process.

The annual interest rate is 15% on own funds which is the average for other CUs but less than other microfinance institution. It also charges 20% on borrowed funds from CFF which charges an interest rate of 15% per annum.

Basic Data on Jambanjelly

Date Established: 2001

Total membership: 1340

Deposit mobilised (Nov 2013): D2,276,732

Loan Outstanding (Nov 2013): D1,183,959

SPM Dimensions Scores

1) 25% Outreach & Targeting: 13%

2) 25% Member Benefit/Welfare: 7%

3) 20% Governance: 5%

4) 10% Staff & Volunteers: 5%

5) 10% Community & Environment: 6%

6) 10% Cooperation among Cooperatives: 8%

Overall SPM Score: 44%

11

Trainings are provided to members on adhoc basis and linkage services are provided on a case by case basis.

Governance

Jambanjelly does not have a strategic or business plan, no social objectives and indicators to measure change in members.

It has more women on the board and senior management which is more than 50%.

It has a strong democratic control with regular AGMs with one member one vote principle.

The board does not have awareness on social performance concepts

It has no code of conduct for the board but uses the bye-laws.

Staff and Volunteer

Jambanjelly CU has an office with basic facilities such as a computer

It has two volunteer staff given monthly allowances.

The volunteer staffs are sent to attend external trainings organised by Apex in addition to trainings provided on the job.

There is no formal staff/volunteer grievance/feedback system but an informal verbal system is used with the board for redress.

There is no staff/volunteer appraisal process in place.

Volunteerism is promoted on the job and for skills development for the volunteer staffs and board.

Community and Environment

Jambanjelly provides advice on community development initiatives and prohibits the financing of harmful activities as indicated on the loan policy.

It provides environmental education to members especially charcoal producers on a case by case basis, but not included in its trainings.

Cooperation among Cooperatives

Jambanjelly is a member to the Apex, fulfils all reporting requirements and always participates in all activities they are invited.

It cooperates with other credit unions in the nearby villages e.g the Manager provides training to other Managers such as the one in Brufut Badala Kafo.

3.4 Foni Kansala Credit Union

Foni Kansala Credit Union is a community based credit union Based in Foni in the West Coast Region in the rural area. It was established in 2001 and has a total membership of 1200. Foni Kansala’s overall SPM score is 43% as shown in Box 4. Figure 4 shows the graphic summary of the overall social performance result. Outreach and Inclusion

Its membership is open to all people living within the Foni Kansala District.

It does not use a poverty screening tool to assess member’s poverty levels and has no poverty outreach goals.

It collects data on members but is limited as the others mentioned before.

12

The women outreach is more than 20%.

Age of members is not taken but the youth outreach is estimated at less than 20%. Figure 4: Overall SPM Result Box 4: Summary of SPM Scores

Member Benefit and Welfare

Foni Kansala does not have a code of ethics for treatment of members.

It has only one standard savings product.

It has an appraisal system for loan process.

There is transparency in the cost, which is discussed with members in meetings and during the loan application process.

The APR is 20% which is above the average charged by most CUs but less than the other microfinance institution.

Trainings are provided to members on adhoc basis but linkage services are not provided to members.

Governance

Foni Kansala does not have strategic or business, no strategy for growth and no indicators to measure changes on members

It has only one staff whose salary is comparable to staff at his level in other CUs.

The board and senior management has more women than men estimated at more than 20%.

It has a strong democratic control which is demonstrated through regular AGMs with one member one vote principle.

Basic Data on Foni Kansala Credit Union

Year Established: 2001

Total membership: 1200

Deposit mobilised (Oct. 2013): D3,644,722

Loan Outstanding (Nov 2013): D1,806,610

SPM Assessment Dimensions Scores

1) 25% Outreach & Targeting: 11%

2) 25% Member Benefit/Welfare: 7%

3) 20% Governance: 5%

4) 10% Staff & Volunteers: 5%

5) 10% Community & Environment: 7%

6)10% Cooperation among Cooperatives: 8%

Overall SPM Score: 43%

13

The board has no awareness on social performance concepts

It has no code of conduct for the board and uses the bye-laws.

Staff and Volunteer

It has an office with basic office facilities like computer, filling cabinet but no internet, photo copier or generator.

It has one employed staff and is sent for external trainings organised by Apex and tertiary institutions in addition to trainings received on the job.

There is no formal staff grievance/feedback system but an informal verbal report is given to the board to address.

There is no staff appraisal process in place.

Volunteerism is actively promoted through the work of the board and committee members. Community and Environment

Foni Kansala support community development initiatives such as community radio station by buying fuel for its operation and contributed to the building of a madrasa (Arabic) school.

It prohibits the financing of harmful activities by funding activities outlined in the loan policy.

It does not include environmental education in trainings provided to members. Cooperation among Cooperatives

Foni Kansala is a member to the Apex, fulfils all reporting requirements and always participates in all activities invited.

It cooperates with other credit union within the Foni Chapter.

3.5 Fangdema Credit Union, Old Jeshwang

Fangdema Credit Union is a community based credit union located in the Kanifing Municipality within the urban area. It was established in 1999 and has a total membership of 243. Fangdema’s overall SPM score is 40% as shown in Box 5. Figure 5 shows the graphic summary of the overall social performance result.. Outreach and Targeting

The membership is open to all people living within Kanifing and surrounding communities.

It does not use a poverty screening tool to assess member’s poverty levels and has no poverty outreach goals.

It collects data on members but is not detailed.

The women outreach is more than 20%.

Age of members is not taken but the youth outreach is estimated at less than 20% because there are more adults than the youth.

Member Benefit and Welfare

Fangdema has a draft code of ethics for treatment of members which is not finalised.

It has only one standard savings product and an appraisal system for loan process.

There is transparency in the cost which is discussed with members in meetings and during the loan application process.

14

The APR is 15% which is the average charged by most CUs and less than the other microfinance institution.

Trainings are provided to members on adhoc basis but linkage services are not provided to members.

Figure 5: Overall SPM Result Box 5: Summary of SPM Scores

Governance

Fangdema has a draft business plan with objectives and indicators to measure changes but social indicators are not clearly specified.

It has an MIS system but does not have indicators to measure changes in members.

It has only one staff whose salary is comparable to staff at his level in other CUs.

The board and senior management has more women than men estimated at more than 50%.

It has a strong democratic control which is demonstrated through regular AGMs with one member one vote principle. Other types of communication written on paper are displaced in the premises.

The board has no awareness on social performance concepts

It has no code of conduct for the board but uses the bye-laws. Staff and Volunteer

It has an office with basic facilities but no internet, photo copier or generator.

Basic Data on Fangdema Credit Union

Year Established: 1999

Total membership: 243

Deposit mobilised (Nov 2013): D1.5Million

Loan Outstanding (Nov 2013): D600,000

SPM Dimensions Scores

1) 25% Outreach & Targeting: 9%

2) 25% Member Benefit/Welfare: 9%

3) 20% Governance: 8%

4) 10% Staff & Volunteers: 5%

5) 10% Community & Environment: 2%

6)10% Cooperation among Cooperatives: 8%

Overall SPM Score: 40%

15

It has one employed staff and is sent for external trainings organised by Apex and tertiary institutions in addition to training received on the job.

There is no formal staff grievance/feedback system but an informal verbal report is given to the board to address.

There is no staff appraisal process in place but a staff handbook which include this is developed and yet to be finalised.

Volunteerism is actively promoted through the work of the board and committee members. Community and Environment

Fangdema does not engage or support community development initiatives.

It prohibits the financing of harmful activities by funding activities outlined in the loan policy.

It does not include environmental education in trainings provided to members.

Cooperation among Cooperatives

Fangdema is a member of the Apex, fulfils all reporting requirements and always participates in all activities invited.

It cooperates with other credit union such as the GPFCCU which provided its electricity cash power system.

3.6 Sabunima Credit Union, Bansang/ Basse Chapter

The Sambunima Credit Union is a community based credit union located in Bansang in the Central River Region. It was established in 1999 and has a total membership of 564 people. Sambunima’s overall SPM score is 40% as shown in Box 6. Figure 6 shows the graphic summary of the overall social performance results. Outreach and Targeting

Its membership is open to people living within Bansang and the surrounding villages.

It does not use a poverty screening tool to assess member’s poverty levels and has no poverty outreach goals.

It collects data on members but is not detailed.

The women outreach is more than 50%.

Age of members is not taken but the youth outreach is estimated at less than 5%. Member Benefit and Welfare

Sabunima does not have a Code of Ethics.

It has only one standard savings product and an appraisal system for loan process.

There is transparency in the cost which is discussed with members during meetings and during the loan application process.

The interest is 20% which is above the average for the other CUs but less than the other microfinance institution.

“The exercise has really opened up

our minds towards our social

directions”

Board Treasurer, Fangdema Credit

Union

16

Trainings are provided to members on adhoc basis and linkage services are provided on a case by case basis.

Figure 6: Overall SPM Result Box 6: Summary of SPM Scores

Governance

Sabunima does not have a strategic or business plan, no plan for growth and no indicators to measure change in members.

It has no staff but a volunteer who is given an allowance

It has more women on the board and senior management estimated to be more than 20%.

There is a strong democratic control which is demonstrated through regular AGMs with one member one vote principle.

There is no board awareness on social performance concepts.

It has no code of conduct for the board Staff and Volunteer

Sabunima has an office with very limited office facilities, no computer and filing cabinet.

It has one volunteer as the general manager given an allowance.

The volunteer receive training on the job.

There is no formal staff grievance/feedback system, issues are reported verbally to the board for redress.

There is no staff/volunteer appraisal process in place.

Volunteerism is promoted especially in skills development which is manifested through the active involvement of the volunteer manager and board members.

Basic Data on Sabunima Credit Union, Bansang

Year Established: 1999

Total membership: 564

Deposit mobilised (Nov 2013): D570,000

Loan Outstanding (Nov 2013): D324,000

SPM Dimensions Scores

1) 25% Outreach & Targeting: 11%

2) 25% Member Benefit/Welfare: 7%

3) 20% Governance: 5%

4) 10% Staff & Volunteers: 4%

5) 10% Community & Environment: 5%

6)10% Cooperation among Cooperatives: 8%

Overall SPM Score: 40%

17

Community and Environment

Sabunima does not engage in community development initiatives, although some members have supported some community work but not under the name of the credit union.

It prohibits the financing of harmful activities based on the loan policy.

It does not include environmental education in trainings provided to members.

Cooperation among Cooperatives

Sabunima is a member to the Apex, fulfil all reporting requirements and always participates in all activities invited.

It does cooperate with other credit unions such as the GPFCCU, Medical and Health CU and attend activities of other CUs in its chapter.

3.7 Dampha Kunda Credit Union, Basse

The Dampha kunda Credit Union is a community based credit union located in Basse in the Upper River Region. It was established in 1997 and has a total membership of 234. The overall SPM score of Dampha Kunda is 40% as shown in table 7. Figure 7 shows the graphic presentation of the overall social performance results. Figure 7: Overall SPM Result Box 7: Summary of SPM Scores

Basic Data on Dampha Kunda, Basse

Year Established: 1997

Total membership: 234

Deposit mobilised (Sept 2013): D147,400

Loan Outstanding (Nov 2013): D131,878

SPM Dimensions Scores

1) 25% Outreach & Targeting: 11%

2) 25% Member Benefit/Welfare: 9%

3) 20% Governance: 5%

4) 10% Staff & Volunteers: 5%

5) 10% Community & Environment: 2%

6)10% Cooperation among Cooperatives: 8%

Overall SPM Score: 40%

18

Outreach and Targeting

The membership is open to all people living within Dampha Kunda in Basse.

It does not use a poverty screening tool to assess member’s poverty levels and no poverty outreach goals.

It collects data on members but is not detailed.

The women outreach is more than 50%.

Age of members is not taken but the youth outreach is estimated at less than 20%.

It is located in an area un-served area except for one located in one of the neighbouring villages. Member Benefit and Welfare

Dampha Kunda does not have a Code of Ethics for treatment of members.

It has only one standard savings product and an appraisal system for loan process.

There is transparency in the cost which is discussed with members during meetings and during the loan application process.

The APR is 10% which is lower than all charges made by most CUs and less than the other microfinance institution.

Trainings are provided to members on adhoc basis but linkage services are not provided to members.

Governance

Dampha Kunda has a draft workplan with objectives and indicators to measure changes but social indicators are not clearly specified.

It has strategy to manage growth through an MIS system but does not have indicators to measure changes in members.

It has a volunteer working as the manager of the CU given an allowance.

The board and senior management has more women than men estimated at more than 20%.

It has a strong democratic control which is demonstrated through regular AGMs with one member one vote principle.

The board has no awareness on social performance concepts and no code of conduct for the board but uses the bye-laws.

Staff and Volunteer

It has an office with basic facilities like computers and a solar system (not currently functional due to inverter problem.

It has volunteer who manages the credit union

He is sent for external trainings organised by Apex in addition to trainings received on the job.

There is no formal staff grievance/feedback system but an informal verbal report is given to the board to address.

There is no staff appraisal process in place and volunteerism is actively promoted through the work of the board and committee members.

Community and Environment

Dampha Kunda does not engage or support community development initiatives.

It prohibits the financing of harmful activities by funding activities outlined in the loan policy.

It does not include environmental education in trainings provided to members.

19

Cooperation among Cooperatives

Dampha Kunda is a member to the Apex, fulfils all reporting requirements and always participates in all activities invited.

It cooperates with other credit union such as Tambasansang, Manneh Kunda and Gambisara within the chapter.

3.8 Foni Berefet, West Coast Region

Foni Berefet credit union is a community based credit union located in the Foni Berefet District. It was established in 1996 and has a total membership of 330 people. It’s overall SPM score is 38% as shown in Table 8. Figure 8 shows the graphic summary of the overall social performance result. Outreach and Targeting

The membership is open to people living within the Foni Berefet District.

It does not use a poverty screening tool to assess member’s poverty levels and no poverty outreach goals.

It collects data on members but is not detailed.

The women outreach is more than 30% but less than 50%.

Age of members is not taken but the youth outreach is estimated to be less than 5%.

It is located in an area un-served by many financial institutions except for one.

Figure 8: Overall SPM Result Box 8: Summary of SPM Scores

Basic Data on Foni Berefet, West Coast Region

Year Established: 1996

Total membership: 330

Deposit mobilised (Nov 2013): D813,725

Loan Outstanding (Nov 2013): D457,597

SPM Dimensions Scores

1) 25% Outreach & Targeting: 7%

2) 25% Member Benefit/Welfare: 9%

3) 20% Governance: 3%

4) 10% Staff & Volunteers: 6%

5) 10% Community & Environment: 5%

6)10% Cooperation among Cooperatives: 8%

Overall SPM Score: 38%

20

Member Benefit and Welfare

Foni Berefet does not have a code of ethics for treatment of members.

It has only one standard savings product and an appraisal system for loan process.

There is transparency in the cost which is discussed with members during meetings and during the loan application process.

The APR is 15% which is the average charged by most CUs and less than the other microfinance institution.

Trainings are provided to members on adhoc basis but linkage services are not provided to members.

Governance

Foni Berefet does not have a strategic or business plan, no strategy for growth and no indicators to measure changes on members.

It has a volunteer who manages the CU and given an allowance.

The board and senior management has women estimated to be more than 20%.

It has a strong democratic control which is demonstrated through regular AGMs with one member one vote principle.

The board has no awareness on social performance concepts and no code of conduct. Staff and Volunteer

It has an office with no facilities except for a table and chair for the Manager.

It has a volunteer who manages the CU and given an allowance.

The volunteer is sent for external trainings organised by Apex in addition to training received on the job.

There is no formal staff grievance/feedback system but an informal verbal report is given to the board to address.

There is no staff appraisal process in place.

Volunteerism is actively promoted through the involvement of the manager and board members.

Community and Environment

Foni Berefet provides advice for community development initiatives.

It prohibits the financing of harmful activities by funding activities outlined in the loan policy.

It provides advice on environmental issues but does not include it in trainings provided to members.

Cooperation among Cooperatives

Foni Berefet is a member to the Apex, fulfils all reporting requirements and always participates in all activities invited.

It cooperates with other credit union through the chapter.

3.9 Fandema Kerewan Credit Union, North Bank Region

Fandema Kerewan credit union is a community based credit union located in the North Bank Region. It was established in 1996 and has a total membership of 197. The overall SPM assessment score is 38% as shown in Table 9. Figure 9 shows the graphic summary of the overall social performance result.

21

Outreach and Targeting

Its membership is open to people living within Kerewan and surrounding villages.

It does not use a poverty screening tool to assess member’s poverty levels and no poverty outreach goals.

It collects data on members but is not detailed.

The women outreach is more than 20%. Age of members is not taken but the youth outreach is estimated at less than 20% because there are more adults than the youth. Figure 9: Overall SPM Result Box 9: Summary of SPM Scores

Member Benefit and Welfare

Fandema Kerewan does not have a Code of Ethics.

It has only one standard savings product and an appraisal system for loan process.

There is transparency in the cost which is discussed with members during meetings and during the loan application process.

Provides fertiliser to members on credit but not cash

Trainings are provided to members on adhoc basis but linkage services are not provided to members.

Governance

Kerewan Fandema does not have a strategic or business plan, no strategy for growth and no indicators to measure changes on members.

It does not have a volunteer who manages the CU, the chairperson manages supported by the field officer.

Basic Data on Kerewan Fandema NBRn

Year Established: 1996

Total membership: 197

Deposit mobilised (Nov 2013): D105,106

Loan Outstanding (Nov 2013): D116,150

SPM Dimensions Scores

1) 25% Outreach & Targeting: 11%

2) 25% Member Benefit/Welfare: 9%

3) 20% Governance: 5%

4) 10% Staff & Volunteers: 0%

5) 10% Community & Environment: 5%

6)10% Cooperation among Cooperatives: 8%

Overall SPM Score: 38%

22

The board and senior management has women estimated to be more than 50% with only two men in the credit union.

It holds frequent meetings with members but elections are not done to change the leadership

The board has no awareness on social performance concepts and no code of conduct. Staff and Volunteer

It has no office and members meet at the chairperson’s home.

It has no volunteer, the work is done by the field officer.

There is no formal staff grievance/feedback system but an informal verbal report is given to the board to address.

There is no staff appraisal process in place.

Volunteerism is not actively promoted because there is no volunteer to manage the CU except board members.

Community and Environment

Fandema Kerewan provides community development initiatives by supporting the “operation no back way” group to weed their rice field.

It prohibits the financing of harmful activities by funding activities outlined in the loan policy.

It provided advice on environmental issues on case by case basis but does not include it in trainings provided to members.

Cooperation among Cooperatives

Fandema is a member to the Apex, fulfils all reporting requirements and always participates in all activities invited.

It cooperates with limited credit union through the chapter.

3.10 Brufut Badala Kafoo Credit Union

Brufut Badala Kafo Credit Union is community based located in the West Coast Region. It was established in 1997 and has a total membership of 132, the smallest number among the 13 CUs assessed. The overall SPM assessment score is 37% as shown in Box 10. Figure 10 shows the graphic summary of the overall score. Outreach and Targeting

Its membership is open to people living within Brufut and the surrounding villages.

It does not use a poverty screening tool to assess member’s poverty levels and no poverty outreach goals.

It collects data on members but is not detailed.

The women outreach is more than 50%.

The youth outreach is estimated at less than 5% because there are more adults than the youth.

It is located in areas served by other financial institutions. Member Benefit and Welfare

Brufut Badala Kafo does not have a Code of Ethics.

It has only one standard savings product and an appraisal system for loan process.

23

There is transparency in the cost which is discussed with members during meetings and during the loan application process.

Its APR is 15% which is the average charged by many CUs

Trainings are provided to members on adhoc basis and provide linkage services on a case by case basis.

Figure 10: Overall SPM Result Box 10: Summary of SPM Scores

Governance

Brufut Badala Kafoo does not have a strategic or business plan, no strategy for growth and no indicators to measure changes on members.

It has a volunteer who manages the CU and is not paid an allowance.

The board and senior management has women estimated to be more than 20%.

It holds frequent meetings with members with election on a one member one vote principle

The board has no awareness on social performance concepts and no code of conduct. Staff and Volunteer

It has no office and members meet at the chairperson’s home.

It has a volunteer who managers the CU without allowance.

The volunteer received training on the job and those organised by the Apex

There is no formal staff grievance/feedback system but an informal verbal report is given to the board to address.

There is no staff appraisal process in place.

Basic Data on Brufut Badala Kafo Credit Union

Year Established: 1997

Total membership: 132

Deposit mobilised (Nov 2013): D105,000

Loan Outstanding (Nov 2013): D14,000

SPM Dimensions Scores

1) 25% Outreach & Targeting: 11%

2) 25% Member Benefit/Welfare: 9%

3) 20% Governance: 5%

4) 10% Staff & Volunteers: 1%

5) 10% Community & Environment: 3%

6)10% Cooperation among Cooperatives: 8%

Overall SPM Score: 37%

24

Volunteerism is actively promoted through the active work of the volunteer manager and board members.

Community and Environment

Brufut Badala Kafo provides advice for community development initiatives in the village.

It prohibits the financing of harmful activities by funding activities outlined in the loan policy.

It does not provide environmental issues on trainings provided to members. Cooperation among Cooperatives

Brufut Badala Kafo is a member to the Apex, fulfils all reporting requirements and always participates in all activities invited.

It cooperates with other credit union such as the Jambanjelly CU and the manager provides training to the Brufut manager.

3.11 Sofora Credit Union, Bundung, Kanifing Municipality

Sofora Credit Union is community based located in the Kanifing Municipality at Six Junction in Bundung. It was established in 2011 and has a total membership of 163. The overall SPM assessment score is 37% as shown in Box 11. Figure 11 shows the graphic presentation of the overall social performance score. Figure 11: Overall SPM Result Box 11: Summary of SPM Scores

Basic Data on Sofora Credit Union, Bundung

Year Established: 2011

Total membership: 163

Deposit mobilised (Nov 2013): over D1million

Loan Outstanding (Nov 2013): D460,000

SPM Dimensions Scores

1) 25% Outreach & Targeting: 11%

2) 25% Member Benefit/Welfare: 7%

3) 20% Governance: 4%

4) 10% Staff & Volunteers: 5%

5) 10% Community & Environment: 2%

6)10% Cooperation among Cooperatives: 8%

Overall SPM Score: 37%

25

Outreach and Targeting

Its membership is open to people living in the Bundung town and beyond.

It does not use a poverty screening tool to assess member’s poverty levels and no poverty outreach goals.

It collects data on members but is not detailed.

The women outreach is more than 50%

The youth outreach is estimated at more than 5% and less than 20%.

It is located in an area served by many financial institutions within the neighbourhood. Member Benefit and Welfare

Sofora Credit Union does not have a Code of Ethics.

It has only one standard savings product and an appraisal system for loan process.

There is transparency in the cost which is discussed with members during meetings and during the loan application process.

Its APR is 15% which is the average charged by many CUs

Trainings are provided to members on adhoc basis and no linkage service is provided to members.

Governance

Sofora does not have a strategic or business plan, no strategy for growth and no indicators to measure changes on members.

It has a volunteer who manages the CU and is paid an allowance.

The board and senior management has women estimated to be more than 20%.

It holds regular AGM and other meetings with members on a one member one vote principle.

The board has no awareness on social performance concepts and no code of conduct.

Staff and Volunteer

Sofora has no office and members meet at the manager’s home.

It has a volunteer who managers the CU and is paid an allowance.

The volunteer received training on the job and those organised by the Apex

There is no formal staff grievance/feedback system but an informal verbal report is given to the board to address.

There is no staff appraisal process in place.

Volunteerism is actively promoted through the active work of the volunteer manager and board members.

Community and Environment

Sofora does not provide advice for community development initiatives in the community.

It prohibits the financing of harmful activities by funding activities outlined in the loan policy.

It does not include environmental issues on trainings provided to members.

“The meeting increased our

knowledge on what we have can do

and are not doing”

Participant, Sofora Credit Union

26

Cooperation among Cooperatives

Sofora is a member to the Apex, fulfils all reporting requirements and always participates in all activities invited.

It cooperates with other credit union such as the GPFCCU, Teacher Credit Union, Jambanjelly etc.

3.12 Jokadu Credit Union, North Bank Region

Jokadu Credit Union is community based located in the Jokadu District in Kuntair Village in the North Bank Region. It was established over 20 years ago and has a total membership of 1984. The overall SPM assessment score is 33% as shown in Box 12. Figure 12 shows the graphic summary of the overall social performance result. Figure 12: Overall SPM Result Box 12: Summary of SPM Scores

Outreach and Inclusion

Its membership is open to people living in villages within the Jokadu District.

It does not use a poverty screening tool to assess member’s poverty levels and no poverty outreach goals.

It collects data on members but is not detailed.

The women outreach is more than 50% and the youth outreach is estimated at less than 5%.

It is located in an un-served area with limited financial institutions.

Basic Data on Jokadu Credit Union, NBR

Year Established: 1984

Membership: 585

Deposit mobilised (Nov 2013): D408,221

Loan Outstanding (Nov 2013): D374,562

SPM Dimensions Scores

1) 25% Outreach & Targeting: 11%

2) 25% Member Benefit/Welfare: 9%

3) 20% Governance: 4%

4) 10% Staff & Volunteers: 1%

5) 10% Community & Environment: 2%

6)10% Cooperation among Cooperatives: 7%

Overall SPM Score: 33%

27

Member Benefit and Welfare

Jokadu Credit Union does not have a Code of Ethics.

It has only one standard savings product and an appraisal system for loan process.

There is transparency in the cost which is discussed with members during meetings and during the loan application process.

Its APR is 15% which is the average charged by many CUs

Trainings are provided to members on adhoc basis and no linkage service is provided to members.

Governance

Jokadu District Credit Union does not have a strategic or business plan, no strategy for growth and no indicators to measure changes on members.

It has no volunteer who manages the CU and this role is played by the field officer.

The board and senior management has women estimated to be more than 20%.

It holds frequent meetings with members with election on a one member one vote principle

The board has no awareness on social performance concepts and no code of conduct.

Staff and Volunteer

It has an office with basic facilities such as a computer and solar system for energy supply, but does not have a toilet facility.

There is no formal staff grievance/feedback system but an informal verbal report is given to the board to address.

There is no staff appraisal process in place.

Volunteerism is not actively promoted except for the board because there is no permanent volunteer to manage the CU.

Community and Environment

The Credit Union does not promote community development initiatives in the village.

It prohibits the financing of harmful activities by funding activities outlined in the loan policy.

It does not provide environmental issues on trainings provided to members. Cooperation among Cooperatives

The CU is a member to the Apex, fulfils all reporting requirements and always participates in all activities invited.

It does not cooperate with other credit union as done by others.

3.13 Gambia Ports Authority Cooperative Credit Union, Banjul The Gambia Ports Authority Credit Union is an institutional credit union for all staff working with at the Gambia Ports Authority. It was established in 2003 and has a total membership of 1066. GPACCU’s overall SPM score is 31% as shown in Box 13, which is the lowest score among the 13 sampled CUs assessed. Figure 13 shows the graphic summary of the overall social performance result.

28

Outreach and Targeting

Its membership is open to all people working under the Ports Authority including the ferry services.

It does not use a poverty screening tool to assess member’s poverty and no poverty outreach goals.

It collects data on members but not detailed

The women outreach is less than 50% and the youth outreach is estimated at less than 5%.

It is located in the capital city Banjul, an area served by many financial institutions.

Figure 13: Overall SPM Result Box 13: Summary of SPM Scores

Member Benefit and Welfare

GPA Credit Union does not have a Code of Ethics.

It has only one standard savings product

It has an appraisal system for loan and also consults the ports authority to check for liability of loan applicant with employer before approval.

There is transparency in the cost which is discussed with members during meetings and during the loan application process.

Its APR is 15% which is the average charged by many CUs

Trainings are provided to members on adhoc basis and no linkage service is provided to members.

Basic Data on Gambia Ports Authority

Cooperative Credit Union, Banjul

Established: 2003

Total membership: 1066

Deposit mobilised (Nov 2013): D12,568,366.74

Loan Outstanding (Nov 2013): D13,610,332.55

SPM Dimensions Scores

1) 25% Outreach & Targeting: 5%

2) 25% Member Benefit/Welfare: 7%

3) 20% Governance: 5%

4) 10% Staff & Volunteers: 5%

5) 10% Community & Environment: 2%

6)10% Cooperation among Cooperatives: 7%

Overall SPM Score: 31%

29

Governance

GPACCU does not have a strategic or business plan, no strategy for growth and no indicators to measure changes on members.

It has employed staff whose salary is based on similar levels with those employed by the authority.

The board and senior management has women estimated to be more than 20%.

It holds frequent meetings with members but has not had an AGM for elections since its inception in 2003.

The board has no awareness on social performance concepts

It has no written code of conduct, but strict policies are applied e.g the allowance of board members are reduced when they are late for meetings.

Staff and Volunteer

It has an office with facilities such as a computer and toilet.

There is no formal staff grievance/feedback system but an informal verbal report is given to the board to address.

There is no staff appraisal process in place.

Volunteerism is actively promoted through the work of the board and a volunteer working with the staff.

Community and Environment

The Credit Union does not promote community development initiatives in the ports or city.

It prohibits the financing of harmful activities by funding activities outlined in the loan policy.

It does not provide environmental issues on trainings provided to members. Cooperation among Cooperatives

The CU is a member to the Apex, fulfils all reporting requirements and always participates in all activities invited.

It does not cooperate with other credit union as done by others, although it was ones proposed but not implemented.

“We have learnt a lot and

hopefully, we will try to implement

some of the issues raised”

Chairman, GPACCU

30

3.0 The PPI Results

The Progress out of Poverty Index (PPI) is a poverty measurement tool used by organisations that have a mission to serve the poor. It is a sound and simple statistical package developed with ten questions and answers about a household characteristics and asset ownership with scores to compute the poverty livelihood of an individual. The score is used with a look up table to know the poverty livelihood value that the household is living below or above the poverty line. The tool helps institutions serving the poor to screen the poverty level of their clients or members to know their poverty outreach, to assess the performance of their services and to be able to track poverty levels over time. The PPI has roots in microfinance and is being promoted for use to improve social performance. As part of the Social performance assessment process, the PPI developed for Gambia was administered to 101 new members of the sampled CUs who joined in 2013 to screen their poverty levels. The PPI scores ranged from 4 points to 89 points, the former being a rural member in Foni Kansala and the latter is an institutional CU member with GPACCU. These scores were reviewed on the look up table to find the livelihood values of each member and the average poverty level for the group. On average, 42% of the 101 sampled new members live below the National Poverty line while 18% of them live below the international benchmark of $1.25 per day as shown in the bar charts below. Figure 14: % by National Poverty Line Figure 15: % by $1.25 per day

A further analysis on a regional level (urban and rural) shows that on average 28% of the 20 sampled new members within the urban areas live below the national poverty line while 72% live above it. In the same vein, 45% of the 81 sampled new members in the rural areas live below the national poverty line and 55% of them live above it. Using the international benchmark, 9% of the 20 sampled urban new members live below the $1.25 per day while the rest (91%) live above it. For the rural areas, 21% of the 81 live below the $1.25 per day while 79% of them live above it. This shows that some percentage of the poor are being reached by the CUs although more could be done to expand the outreach to the poorest. The same group of people could be tracked after two years within the CU membership to check if their poverty status has changed positively, which will be reflected in a change in the percentage rate. The PPI is a good tool to support the CUs to demonstrate that they are serving the poorest among the poor to fulfil their mission for poverty alleviation through the credit union movement.

31

4.0 Conclusion and Recommendation

The assessment process has revealed the successes and weaknesses in the CUs Social Performance management on the critical dimensions necessary to support the achievement of their social goals. In all the assessment meetings, the participants indicated that their CUs were created to fight poverty through the provision of financial services to members at reasonable interest rate, which is a social goal. However, none of them has a tool to screen the poverty levels of the members to facilitate the tracking and reporting of changes in poverty levels. Some of them have indicated that they are aware of some of the benefits of the credit unions to members but these are not documented for evidence. The profile of members captured is very limited due to the limitations on the membership form. This is mainly limited to name, contact address, next of kin and amount to be saved. Gender is mostly not collected but is known based on the names of the people, but this could be misleading as some names are used by both gender. The community CUs which usually includes women’s group were advantaged and had good score on women outreach. Information on age and poverty level is not collected and these were all given based on estimates. The location of the CUs also had a positive influence on the rural CUs and a negative influence for the urban CUs. On the Member benefit dimension, most of the sampled CUs have no code of ethics for treatment of members except for GPFCCU while Fangdema’s own is yet to be finalised. They all have one standard savings product which limits the options available for members. Interestingly, all of them have effective loan appraisal processes in place which include a review of the savings patterns of the individual, credit history, occupation and some (GPACCU and BIACCO) consult with employers to ensure that the capacity to repay is checked before approval. There is adequate education of members by all of them on cost of loans which is shared with members in meetings and during the loan process. The annual interest rate charged by the majority is based on the average (15%) charge by many CUs except for two whose charges are above while one of them (Dampha Kunda) has a lower charge (10%). However, the charges of the sampled CUs are lower than the charges of other financial institutions. None of the CUs has a plan for training of members but are dependent on the trainings organised by the Apex which are done occasionally. Linkage/referral services for members were not regarded as part of the work and not provided by many except few who did occasionally. On the Governance dimension, most of the CUs do not have a strategic or business plan except for GPFCCU whose own is completed and drafts for BIACCU and Fangdema. This is a critical area as its availability will help the CUs to map out the strategies to use to achieve the financial and social goal they aim to achieve. Likewise, there are limited plans for growth management except for the installation of MIS systems and staff training by some CUs. There is no board awareness of social performance, although some of them felt that they were unconsciously working towards social goals. Majority of them have no code of conduct for the board except for the GPFCCU, BIACCU and Fangdema which has a draft, which is yet to be finalised. Staff and volunteer issues are promoted except for two CUs (Fandema Kerewan and Jokadu) who do not have volunteers to manage their CUs. Most of the office facilities are basic while three CUs (Brufut, Sofora and Fangdema Kerewan do not have offices to manage the affairs of the CUs activities and use the homes of either the chairperson or volunteer Managers. There are no staff/volunteer appraisals and feedback/grievance systems in place in all the CUs assessed which are critical to manage staff performance for better outputs.

32

On Community and environment dimension, the sampled CUs have limited knowledge on their responsibility to the community except for the police which has done well in supporting community development initiatives both within the Credit Union movement and within the security system. This gave them a higher score against the others. The others have not done much on this area even though some have supported some community activities as members of their community but not under the auspices of their Credit Union. Lastly, but not the least, the assessment of Cooperation among cooperatives revealed that many of the sampled CUs cooperate with other credit unions and provide financial, material and capacity development support to each other. The GPFCCU is noted to have done very well in this area as it supports many smaller CUs across the country. The only three who do not work with other CUs are GPACCU, BIACCU and Jokadu District. Recommendations Based on the issues discussed above, the following are recommendations for improvement of the social performance management processes of the CUs as revealed by the assessment:

NACCUG should facilitate the use of a poverty assessment tool by CUs to screen the poverty level of members at the start and during membership to study movements on poverty level.

NACCUG should develop a detail membership form and share with the CUs to improve data collection for membership profiling.

The data collected and recorded in the MIS system should be analysed and aggregated to improve reporting e.g the % of youths (less than 25yrs) reached by the Credit Union.

A simplified strategic plan template should be developed by NACCUG and shared with the CUs to develop their plans with both financial and social objectives and indicators.

NACCUG should develop a simple Staff Code of Ethics and Code of Conduct for board and share with all the CUs to adapt to their specific needs.

A simple staff appraisal and feedback/grievance system should be developed by NACCUG and shared with all CUs to adapt and use for staff and volunteer management.

The CUs should be sensitized and encouraged to engage in community development initiatives through financial and non-financial services e.g labour support to community activities.

Cooperation among cooperatives should be promoted among CUs through study tours to share and learn from each other and to strengthen cooperation among them.

NACCUG should organise more trainings on SPM for other CUs within the Banjul and KMC Chapters to enhance knowledge and understanding of SPM for its institutionalisation within the CUs.

Lastly, SPM can be promoted in the CU movement through the award of certificate of merit for good social performance management.

In conclusion, SPM is fairly new in the microfinance industry in the Gambia and the results of the sampled CUs are a good learning point for improvement of systems and processes for better social performance management. One key learning is that the financial status of the CU does not necessarily have a positive effect on their social performance management score as shown by the higher score made by community CUs with lower financial status over others with higher financial status. If the recommendations above are implemented and monitored keenly for effective utilisation, better results will be seen in the future. This will facilitate the availability of the data and evidence to support the advocacy work of the Credit Union movement for appropriate legal and policy framework within the microfinance industry.