swiss code of best practice for corporate governance€¦ · · 2015-07-29“swiss code of best...

TRANSCRIPT

Swiss Code of Best Practice for Corporate Governance Comparison of 2007 and 2014 versions

English Version

“Swiss Code of Best Practice for Corporate Governance” 1

Table of contents

1. Introduction .................................................................................................................. 2

2. Executive summary ....................................................................................................... 3

3. Detailed changes .......................................................................................................... 5

3.1. Preamble and General Principle ................................................................................. 5

3.2. Shareholders ........................................................................................................... 7

3.3. Board of Directors and Executive Board ...................................................................... 9

3.3.1. Duties of the Board of Directors ............................................................................. 9

3.3.2. Composition ...................................................................................................... 10

3.3.3. Independence .................................................................................................... 11

3.3.4. Procedures and Chairmanship of the Board of Directors ......................................... 12

3.3.5. Dealing with conflicts of interest and advance information ..................................... 13

3.3.6. Chairman of the Board of Directors and President of the Executive Board ................ 13

3.3.7. Internal control system, dealing with risk and compliance ...................................... 14

3.3.8. Committees of the Board of Directors ................................................................... 15

3.3.9. Special circumstances ........................................................................................ 17

3.4. Auditing ................................................................................................................ 18

3.5. Disclosure ............................................................................................................. 18

4. Appendix 1 ................................................................................................................. 19

5. Contact ...................................................................................................................... 25

“Swiss Code of Best Practice for Corporate Governance” 2

1. Introduction

Effective corporate governance creates a safer, sounder corporate environment for companies, shareholders and auditors and builds trust and confidence in the capital markets. In order to be effective and gain the confidence of investors, boards and management should be aware of investor priorities and emerging governance practices.

In Switzerland, economiesuisse introduced the Swiss Code of Best Practice for Corporate Governance (Swiss Code) in 2002. Since then the code has strongly influenced the development of corporate governance in Switzerland. It has proven to be an effective instrument for self-regulation as it provides companies with recommendations on the set up of their corporate governance and information that go beyond what is required by law. Companies are able to retain their organizational flexibility and can put their own ideas and different structures into practice (with the new version of the Swiss Code companies have to explain how and why their corporate governance practices deviate from the Swiss Code - “comply or explain”).

As a result of various developments in the past few years, especially the changes to the Federal Constitution (Article 95 [3]), a modification and update were seen as necessary. The new version was published in September 2014. Among other changes, the 2014 version emphasizes the concept of sustainable corporate success as the lodestar of sensible “corporate social responsibility”. It also calls for specific modifications to the composition of the Board of Directors (including representation of women) and to risk management and compliance.

In this document, we have highlighted the changes made and the resulting implications as well as potential action points. In our view, the following action points should be considered:

• Assess the impact of changes on the company;

• Identify and assess new risks;

• Assess the impact of the compensation requirement changes;

• Check whether the company is in line with the new requirements;

• Set up or assess the compliance management system;

• Review or introduce a Code of Conduct based on best practices;

• Develop a sustainability management framework or revise the current framework;

• Revise the company’s current corporate governance framework with a focus on sustainable company interest;

• Support (increased) information and communication actions with shareholders;

• Explain the reasons for deviations (“comply or explain”).

If you like to discuss further, EY also offers balanced insights and data-rich content and analysis which foster alignment and bridges gaps among management, boards of directors and investors.

“Swiss Code of Best Practice for Corporate Governance” 3

2. Executive summary

Since 2002, the Swiss Code of Best Practice for Corporate Governance (Swiss Code) has provided companies in Switzerland with guiding principles for corporate governance. As a result of various developments in the past few years, the Swiss Code has been modified. economiesuisse recently presented a revised version of the Swiss Code. This revised version contains some important changes as listed in the table below.

Main changes • The concept of sustainable corporate development is introduced as the cornerstone to safeguard the company interests in a sustainable perspective.

• The importance of diversity is emphasized with requirements on the composition of the Board of Directors.

• Risk management now also includes reputation-based risks.

• Clear and regular communication between the Board of Directors and shareholders is emphasized with enhanced transparency requirements.

• Additional requirements are introduced relating to compensation and the role of the compensation committee.

• Introduction of the “comply or explain” principle for corporate governance practices that deviate from the recommendations of the Swiss Code.

Implications

• The focus has been shifted from shareholders’ interest toward safeguarding sustainable company interests (short-term versus long-term interests).

• Sustainable corporate development should be the guiding goal for the Board of Directors.

• The Board of Directors is explicitly assigned the task of shaping and implementing the company’s corporate governance.

• The Board of Directors should plan with respect to not only strategy and finances but also risk.

• The aim should be to have dual leadership for the chairmanship of the Board of Directors and the top position of the Executive Board.

• The Board of Directors should consider appropriate diversity and gender equity among its members.

• The term of office for members of the Board of Directors has been reduced to one year.

• With the new principle that companies have to “comply or explain”, compliance gets more importance.

• Shareholders have more rights: they are now entitled to make decisions regarding the compensation paid to the Board of Directors and the Group Executive (Minder Initiative).

• Regarding compensation, concerns are raised related to the different approach Switzerland has taken compared to other countries.

• The compensation policy should take into consideration the company’s strategic goals.

• Golden parachutes are no longer mentioned and it is recommended to have

“Swiss Code of Best Practice for Corporate Governance” 4

Implications (continued)

only fixed elements for the compensation of non-executive members.

• The Compensation Committee should gather specialist knowledge and, where required, contact external (financial) experts.

• The goal of share-based compensation should be to align the interests of senior company representatives and long-term committed shareholders.

• To counter unjustified benefits, or if there has been a lack of compliance, repayment obligations are now possible (“claw backs”).

• The Board of Directors is now responsible for deciding on motions regarding remuneration for the Board of Directors and the Executive Board and for the compilation of the compensation report.

• The members of the Board of Directors are now required to self-evaluate their performance.

• Transparency, clear and regular communication as well as access to information are important preconditions for ensuring informed decision- making and independent voting.

• Independence is now detailed as institutional, financial and personal.

• Reputational risks are now mentioned in the Swiss Code.

• Companies now have to issue a code of conduct, that follows recognized best practice.

Action Points • Assess the impact of changes on the company.

• Identify and assess new risks.

• Assess the impact of the compensation requirement changes.

• Check whether the company is in line with the new requirements.

• Set up or assess the compliance management system.

• Review or introduce a Code of Conduct based on best practices.

• Develop a sustainability management framework or revise the current framework.

• Revise the company’s current corporate governance framework with a focus on sustainable company interest.

• Support (increased) information and communication actions with shareholders.

• Explain the reasons for deviations (“comply or explain”).

“Swiss Code of Best Practice for Corporate Governance” 5

3. Detailed changes

The following tables compares the 2007 version of the “Swiss Code of Best Practice for Corporate Governance” with the new 2014 version. The main changes are highlighted in red in the old version and in green in the new version. Some parts in the 2007 version are not included as they are outdated after the enforcement of the OaEC (Ordinance against Excessive Compensation).

3.1. Preamble and General Principle

Content No. Version 2007 No. Version 2014

Preamble • Recent international development and changes at Swiss level, especially the Revision of Article 95 [3] of the Federal Constitution have led to an updated version of the “Swiss Code”.

• The “Swiss Code” is ultimately a reflection of the fact that Swiss lawmakers have taken a different route with regard to questions of remuneration than is common in other countries.

• The “Swiss Code” is intended as a list of recommendations, using the “comply or explain” principle for Swiss public limited companies.

“Corporate

Governance” as

a guiding

principle

2.2 • Corporate governance encompasses the full range of principles directed towards shareholders’ interest seeking a good balance between direction and control and transparency at the top company level while maintaining decision-making capacity and efficiency.

• Corporate governance encompasses all of the principles aimed at safeguarding sustainable company interests. While maintaining decision-making capability and efficiency at the highest level of a company, these principles are intended to guarantee transparency and a healthy balance of management and control.

The “Swiss Code

of Best Practice

for Corporate

Governance” as

a guideline and

recommendation

2.2 • The “Swiss Code of Best Practice for Corporate Governance” (“Swiss Code”) is intended for public limited companies. Certain provisions are addressed to institutional investors and intermediaries. The purpose of the “Swiss Code” is to set out guidelines and recommendations, but not force Swiss companies into a straightjacket. Each company should retain the possibility of putting its own ideas on structuring and organization into practice.

• The “Swiss Code of Best Practice for Corporate Governance” is intended for Swiss public limited companies. Certain provisions address institutional investors and intermediaries. The purpose of the “Swiss Code” is to set out guidelines and recommendations. However, it should not force Swiss companies into a straitjacket. Every company should retain the option of putting its own ideas on organizing corporate governance into practice. If a company’s corporate governance practices deviate from the recommendations of the “Swiss Code”, it has to provide a suitable explanation (“comply or explain”).

“Swiss Code of Best Practice for Corporate Governance” 6

Implications Action points

• New is the “comply or explain” principle: deviations from the recommended corporate governance practices are still possible, but have now to be explained.

• Compliance gets more importance.

• Focus is shifted from shareholders’ interest towards safeguarding sustainable company interests (short-term vs. long-term interests).

• Regarding compensation, concerns are raised related to the different approach Switzerland has taken compared to other countries.

• Assess the impact of changes on the company.

• Identify and assess new risks.

• Check whether the company is in line with the new requirements.

• Develop a sustainability management framework or revise the current framework.

• Revise the company’s current corporate governance framework with a focus on sustainable company interest.

• Explain the reasons for deviations (“comply or explain”).

“Swiss Code of Best Practice for Corporate Governance” 7

3.2. Shareholders

Content No. Version 2007 No. Version 2014

As investors,

shareholders

have the final

say within the

company.

1 • The powers of the shareholders are defined by statute. They alone are entitled to make decisions with regard to personnel matters at the top company level (electing and granting release to members of the Board of Directors and appointing the company’s auditors), the final approval of accounts (annual and consolidated financial statements) and policy on distributions and shareholders’ equity (dividends, increase in capital or reduction of capital).

1 • The powers of the shareholders are defined by statute. The shareholders alone are entitled to make decisions regarding personnel matters at the top company level (electing and granting release to members of the Board of Directors, electing the Chairman of the Board of Directors and the members of the Compensation Committee, appointing the company’s auditors and the independent voting proxies), the final approval of accounts (annual and consolidated financial statement) and the policy on distributions and shareholders’ equity (dividends, increase in capital or reduction of capital) as well as compensation paid to the Board of Directors and the Group Executive.

New statement:

• Institutional investors, nominees and other intermediaries, including proxy advisors, should take the Guidelines for institutional investors into consideration when exercising their right to vote in public limited companies.

The company

should

endeavour to

facilitate the

exercise of

shareholders’

statutory

rights.

2 • The Articles of Association should be available in writing or in electronic form at any time.

2 • The Articles of Association and at least the main features of the organisational regulations should be available in written or in electronic form at all times. The company should also publish the Articles of Association on their website.

The

organisation of

the General

Shareholders’

Meeting should

enable

shareholders

to make

relevant and

concise

comments on

the agenda

items.

5 New statement

• The Board of Directors should ensure that the shareholders are able to form their opinions in an informed manner and express them clearly.

“Swiss Code of Best Practice for Corporate Governance” 8

Implications Action points

• The shareholders get more rights: they are entitled to make decisions regarding the compensation paid to the Board of Directors and the Group Executive.

• Transparency, clear communication and access to information are important preconditions to ensure informed decision making and independent voting.

• Regular communication with shareholders should ensure that the Board of Directors’ motion is comprehensible and supported.

• Support (increased) information and communication actions with shareholders.

Content No. Version 2007 No. Version 2014

Arrangements

should be made

to ensure that

shareholders’

rights to

information

and inspection

are met.

6 • The minutes of the meeting should be made available to the shareholders as soon as possible but not later than three weeks after the meeting’s date.

6 • The results of the voting should be made available to the shareholders as soon as possible, but no later than one week after the voting takes place.

The will of the

majority should

be clearly and

fairly

expressed in

the General

Shareholders’

Meeting.

7 • The Chairman should implement the voting procedures in such a way that the majority will can be determined in as an unambiguous and efficient a way as possible. In the absence of a clear majority, the Chairman should arrange for voting to take place by written or electronic ballot.

7 • The Chairman should implement the voting procedures in such a way that the will of the majority can be determined as unambiguously and as efficiently as possible. Where possible, the Board of Directors should use tried and tested electronic means.

New statement:

• The Board of Directors should take appropriate measures to ensure that the independent voting representative is able to carry out his function effectively.

The Board of

Directors

should take

steps to

contact the

shareholders

also in between

the General

Shareholders’

Meetings.

8 New statement:

• If a significant proportion of the votes do not support the Board of Directors’ motion, the Board of Directors should improve communication with the shareholders.

“Swiss Code of Best Practice for Corporate Governance” 9

3.3. Board of Directors and Executive Board

3.3.1. Duties of the Board of Directors

Implications Action points

• The Board of Directors is explicitly assigned to shape and implement the company’s corporate governance.

• The Board of Directors should not only plan with respect to strategy and finances but also to risk.

• Sustainable corporate development should be the guiding goal for the Board of Directors.

• The Board of Directors is now responsible to decide on motions regarding remuneration of the Board of Directors and EB and for the compilation of the compensation report.

• Identify and assess new risks.

• Assess the impact of the compensation requirement changes.

• Set up or assess the compliance management system.

• Revise the company’s current corporate governance framework with a focus on sustainable company interest.

• Develop a sustainability management framework or revise the current framework.

Content No. Version 2007 No. Version 2014

The Board of

Directors

elected by the

shareholders is

responsible for

the strategic

direction and

supervision of

the company or

the Group.

9 • In its planning it should ensure the fundamental harmonization of strategy and finances.

9 New statement:

• The Board of Directors should shape the company’s corporate governance and put it into practice.

• In its planning, it should ensure the fundamental harmonisation of strategy, risks and finances.

New statement:

• The Board of Directors should be guided by the goal of sustainable corporate development.

Swiss company

law lays down

the inalienable

and non-

transferable

primary

functions of

the Board of

Directors.

10 Its primary functions are:

New Statement:

• 8. deciding on motions to be submitted to the General Shareholders’ Meeting on the remuneration of the Board of Directors and the Group Executive Board as well as compiling the compensation report.

“Swiss Code of Best Practice for Corporate Governance” 10

3.3.2. Composition

Implications Action points

• Diversity and gender equality are stressed in the new version.

• Independency is discussed in more detail (new Section 14).

• The term of office for members of the Board of Directors is reduced to one year.

• Assess the impact of changes on the company.

• Check whether the company is in line with the new requirements.

Content No. Version 2007 No. Version 2014

The goal should

be well-

balanced

representation

in the Board of

Directors.

12 • Members of the Board of Directors should be persons with the abilities necessary to ensure an independent decision-making process in a critical exchange of ideas with the Executive Management.

• The majority of the Board should, as a rule, be composed of members who do not perform any line management function within the company (non-executive members).

12 • The Board of Directors should be comprised of male and female members. They should have the necessary abilities to ensure an independent decision-making process in a critical exchange of ideas with the Executive Board.

New statement:

• The Board of Directors should guarantee that there is an appropriate diversity among its members.

• The majority of the Board of Directors should be composed of members who are independent within the meaning of Section 14.

The Board of

Directors

should plan for

the succession

of its members

and ensure

that they

receive further

training.

13 • The ordinary term of office for members of the Board of Directors should, as a rule, not exceed four years.

Adequately staggered terms of office are desirable.

13 • The term of office for members of the Board of Directors should be one year.

“Swiss Code of Best Practice for Corporate Governance” 11

3.3.3. Independence (section newly placed in the 2014 version)

Implications Action points

• Independency of the members of the Board of Directors is placed more prominently in the new version.

• Independency is now detailed as institutional, financial or personal.

• Assess the impact of changes on the company.

• Check whether the company is in line with the new requirements.

Content No. Version 2007 No. Version 2014

The

independence

of the

members of

the Board of

Directors is

governed by

particular

principles.

22 • It is recommended that a majority of the members of certain committees be independent. Independent members shall mean non-executive members of the Board of Directors who never were or were more than three years ago a member of the executive management and who have no or comparatively minor business relations with the company.

• Where there is a cross membership in Boards of Directors, the independence of the respective member should be carefully examined case by case.

• The Board of Directors may lay down further criteria of independence.

14 • Independent members shall mean non-executive members of the Board of Directors who have never been a member of the Executive Board, or were members thereof more than three years ago, and who have no or comparatively minor business relations with the company.

• Where there is cross-involvement in other Boards of Directors, the independence of the member in question should be carefully examined on a case-by-case basis.

• The Board of Directors may define further criteria of institutional, financial or personal independence.

“Swiss Code of Best Practice for Corporate Governance” 12

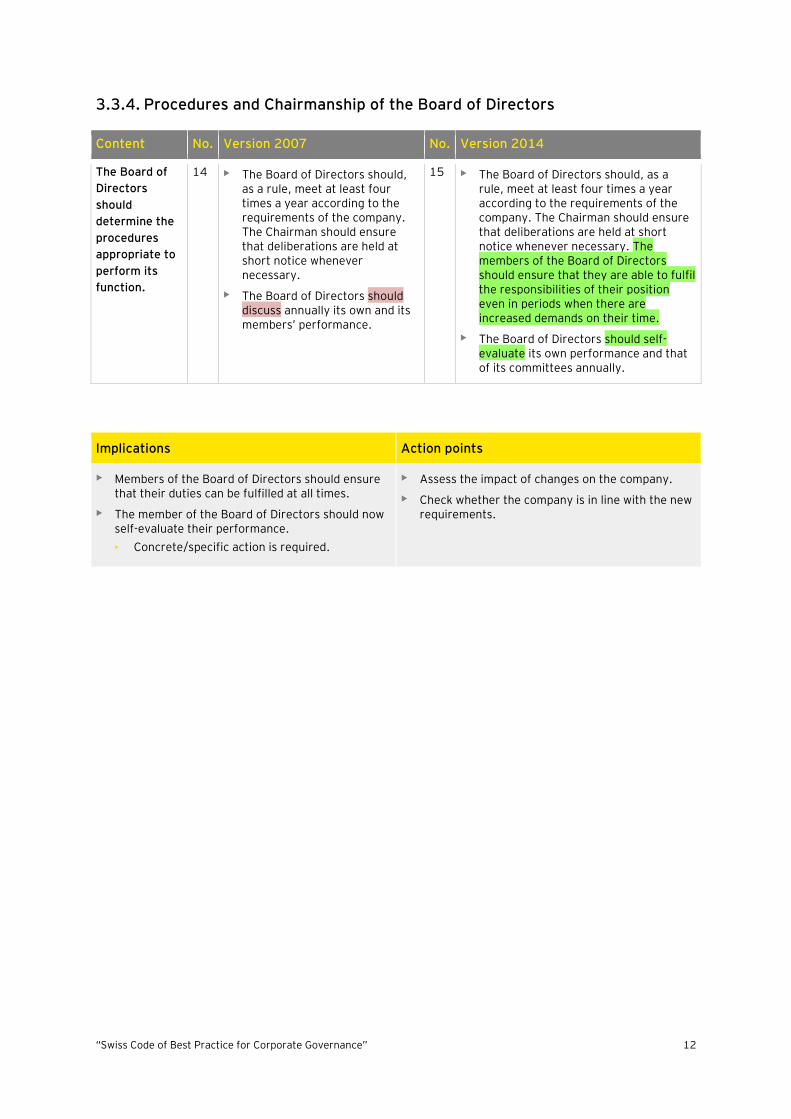

3.3.4. Procedures and Chairmanship of the Board of Directors

Implications Action points

• Members of the Board of Directors should ensure that their duties can be fulfilled at all times.

• The member of the Board of Directors should now self-evaluate their performance.

• Concrete/specific action is required.

• Assess the impact of changes on the company.

• Check whether the company is in line with the new requirements.

Content No. Version 2007 No. Version 2014

The Board of

Directors

should

determine the

procedures

appropriate to

perform its

function.

14 • The Board of Directors should, as a rule, meet at least four times a year according to the requirements of the company. The Chairman should ensure that deliberations are held at short notice whenever necessary.

• The Board of Directors should discuss annually its own and its members’ performance.

15 • The Board of Directors should, as a rule, meet at least four times a year according to the requirements of the company. The Chairman should ensure that deliberations are held at short notice whenever necessary. The members of the Board of Directors should ensure that they are able to fulfil the responsibilities of their position even in periods when there are increased demands on their time.

• The Board of Directors should self-evaluate its own performance and that of its committees annually.

“Swiss Code of Best Practice for Corporate Governance” 13

3.3.5. Dealing with conflicts of interest and advance information

3.3.6. Chairman of the Board of Directors and President of the Executive Board

Implications Action points

• The aim should be to have dual leadership for the chairmanship of the Board of Directors and the top position of the Executive Board.

• Assess the impact of changes on the company.

• Check whether the company is in line with the new requirements.

Content No. Version 2007 No. Version 2014

The Board of

Directors

should regulate

the principles

governing ad

hoc publicity in

greater detail

and take

measures to

prevent

insider-trading

offences.

17 • The Board of Directors should consider in particular whether appropriate action (e.g. “close periods”) should be taken with regard to purchasing and selling securities of the company or other sensitive assets during critical periods, e.g. in connection with take-over projects, before media conferences or prior to announcing corporate results.

18 • The Board of Directors should ensure, in particular, that appropriate action (e.g. “close periods”) is taken with regard to purchasing and selling securities of the company or other sensitive assets during critical periods, e.g. in connection with acquisition projects, before media conferences or prior to announcing corporate figures.

Content No. Version 2007 No. Version 2014

The principle of

maintaining a

balance

between

management

and control

should also

apply to top

management.

18 • The Board of Directors should determine whether a single person (with joint responsibility) or two persons (with separate responsibility) should be appointed to the Chair of the Board of Directors and the top position of the Executive Management (Managing Director, President of the Executive Board or Chief Executive Officer).

19 • The Board of Directors should aim to entrust its chairmanship and the top position on the Executive Board to two people (dual leadership).

“Swiss Code of Best Practice for Corporate Governance” 14

3.3.7. Internal control system, dealing with risk and compliance

Implications Action points

• Reputational risks are now mentioned in the new version.

• Companies now have to issue a code of conduct, which follows recognized best practices.

• Identify and assess new risks.

• Review or introduce a Code of Conduct based on best practices.

Content No. Version 2007 No. Version 2014

The Board of

Directors

should provide

internal control

and risk

management

systems that

are suitable for

the company.

Risk

management

refers to

financial,

operational and

reputation-

based risks.

19 • The internal control system should, depending on the specific nature of the company, also cover risk management. The latter should apply to both financial and operational risks.

20 • The internal control system should, depending on the specific nature of the company, also cover risk management.

The Board of

Directors

should take

measures to

ensure

compliance

with the

applicable

standards.

20 • The Board of Directors should arrange the function of compliance according to the specific nature of the company. It may also allocate compliance to the internal control system.

21 • The Board of Directors should arrange the compliance function according to the specific nature of the company and issue an appropriate code of conduct.

New statement:

• It should follow recognised best practice rules.

“Swiss Code of Best Practice for Corporate Governance” 15

3.3.8. Committees of the Board of Directors

Audit Committee

Implications Action points

• 2014 version defines the need of a financial expert in complex situations.

• Check whether the company is in line with the new requirements.

Compensation Committee

Implications Action points

• Increased focus on the Compensation Committee’s role and requirements of expertise and commitment in the company’s interest.

• Assess the impact of the compensation requirement changes.

Content No. Version 2007 No. Version 2014

The Board of

Directors

should set up

an Audit

Committee.

23 • A majority of members, including the Chairman, should be financially literate.

23 • The majority of the members, including the Chairman, should be experienced in financial and accounting matters. In complex situations, at least one member should be a financial expert (e.g. current or former CEO, CFO or financial auditor).

Content No. Version 2007 No. Version 2014

The Board of Directors should put forward non-executive and independent members at the General Shareholders’ Meeting for election to the Compensation Committee.

25 • The Chairman of the Board respectively the President of the Executive Management should, as a rule, be consulted except when their own remuneration is under review.

• The Compensation Committee should draw up the principles for remuneration of members of the Board of Directors and the Executive Management and submit them to the Board of Directors for approval.

25 New section

• The Compensation Committee has a key role to play in implementing the stipulations of the law and the Articles of Association, and the General Shareholders’ Meeting, which demands expertise and commitment in the interests of the company.

• The Chairman of the Board and the President of the Executive Board may attend the meetings, except when their own remuneration is concerned.

• In all other respects, Appendix 1 shall apply.

“Swiss Code of Best Practice for Corporate Governance” 16

Nomination Committee

Implications Action points

• Requirements on the composition of the Nomination Committee.

• Assess the impact of changes on the company.

Content No. Version 2007 No. Version 2014

The Board of

Directors

should set up a

Nomination

Committee.

26 New statement

• The Nomination Committee should consist predominantly of non-executive and independent members of the Board of Directors.

“Swiss Code of Best Practice for Corporate Governance” 17

3.3.9. Special circumstances

Implications Action points

• Companies can still have a differing set-up, but they have to give suitable explanations why and how their corporate governance deviates from the “Swiss Code” (Principle of “comply or explain”).

• Assess the impact of changes on the company.

• Explain the reasons for deviations (“comply or explain”).

Content No. Version 2007 No. Version 2014

The rules of

the “Swiss

Code” may be

adapted to

actual

circumstances,

depending on

the

shareholder

structure and

the size of the

company.

27 New statement

• For public listed companies, the principle of “comply or explain” remains applicable.

“Swiss Code of Best Practice for Corporate Governance” 18

3.4. Auditing

3.5. Disclosure

Content No. Version 2007 No. Version 2014

The external

audit role

should be

performed by

the audit body

elected by the

shareholders.

29 • Auditors and group auditors should comply with the guidelines on maintaining independence applicable to them.

28 • The audit body shall comply with the guidelines on maintaining independence that are applicable to them.

Content No. Version 2007 No. Version 2014

The company

shall provide

information on

corporate

governance in

its Annual

Report.

30 • The SIX Swiss Exchange Directive on information relating to Corporate Governance is applicable with regard to detailed disclosures.

29 • The SIX Swiss Exchange Directive on information relating to Corporate Governance and the provisions of company law are applicable with regard to individual pieces of information.

“Swiss Code of Best Practice for Corporate Governance” 19

4. Appendix 1

Generally, the Appendix has a new structure in 2014’s version. It clarifies and expands on the provision in Section 25 and gives updated recommendations on the issue of compensation for members of Boards of Directors and Executive Boards. This summary paper is structured following the new version.

Terms like “dealing with these issues responsibly”, “ensure transparent procedures” and “comprehensible” compensation are mentioned in the introduction of both versions.

Role of the General Shareholders’ Meeting

Implications Action points

• Decision-making should be facilitated by providing sufficient information to the shareholders and leading objective debates.

• Support (increased) information and communication actions with shareholders.

Content No. Version 2007 No. Version 2014

The Board of Directors should ensure that the General Shareholders’ Meeting can exercise its powers.

c) 9 The Board of Directors involves the Shareholders’ Meeting in the debate on the compensation system in an appropriate form.

• The Board of Directors decides how to involve the Shareholders’ Meeting in the debate on the compensation system.

30 New Section

• The Board of Directors decides within the framework of the law and the Articles of Association how it will structure and organise the various votes and elections on compensation in the General Shareholders’ Meeting. It should strive for objective debates and efficient decision-making by the General Shareholders’ Meeting.

• The Chairman of the Board of Directors or the Chairman of the Compensation Committee should provide additional information on the compensation report as well as on the remuneration system, and take questions on these topics.

• The Board of Directors should use the resources that it possesses to also facilitate the information retrieval and decision-making of the shareholders in the run-up to the General Shareholders’ Meeting.

“Swiss Code of Best Practice for Corporate Governance” 20

The Role of the Board of Directors and the Compensation Committee

Content No. Version 2007 No. Version 2014

The Board of

Directors

should pass a

resolution on

the design of

the

compensation

system for

members of

top

management,

and

compensation

motions placed

before the

General

Shareholders’

Meeting.

a) 1 • The Board of Directors passes a resolution on the design of the compensation system for members of the Board of Directors and the Executive Board, as well as on guidelines for the design of retirement benefits for the executive members of both bodies.

• Furthermore the Board of Directors sets out the extent to which a Compensation Committee is assigned full resolution authority, the authority to make decisions subject to ratification by the body as a whole, or authority to submit proposals. In doing so the Board of Directors generally reserves the right to approve the overall compensation for the Executive Board and the compensation of the Chief Executive Officer.

31 • Within the framework of the principles set out in the Articles of Association, the Board of Directors should pass a resolution on the company’s compensation policy which takes the strategic goals of the company into consideration, on the fundamental structure of the compensation system for members of the Board of Directors, the Executive Board and if need be for the Advisory Council, as well as on the guidelines for the structure of the occupational pension schemes for the executive members of these bodies.

• The Board of Directors should decide the annual compensation sums to be submitted for approval for the Board of Directors, the Executive Board, and if necessary, the Advisory Council, and justify these in its motion to the shareholders in a comprehensible manner. In doing so, it may also refer to the compensation report.

New statement

• The Board of Directors should comply with the resolutions of the General Shareholders’ Meeting and with the stipulations in the Articles of Association on the division of competence between itself and the Compensation Committee regarding the determination of individual compensation packages. It generally reserves the right to approve the overall compensation for the Executive Board and its Chairman.

The Board of

Directors

should propose

non-executive

and

independent

members for

election to the

Compensation

Committee.

25 • A majority of the Compensation Committee should consist of non-executive and independent members of the Board of Directors.

32 New statement

• The Board of Directors should propose independent members to the General Shareholders’ Meeting for election to the Compensation Committee. If non-independent members are proposed by the shareholders for election, the Board of Directors should inform the General Shareholders’ Meeting of this situation.

“Swiss Code of Best Practice for Corporate Governance” 21

Implications Action points

• The compensation policy should take into consideration the company’s strategic goals.

• The Compensation Committee should gather specialists knowledge and where required involve external consultants.

• Assess the impact of changes on the company.

• Assess the impact of the compensation requirement changes.

• Check whether the company is in line with the new requirements.

Content No. Version 2007 No. Version 2014

The

Compensation

Committee has

a key role to

play in

implementing

the stipulations

of the law, the

Articles of

Association,

and the

General

Shareholders’

Meeting, which

demands

expertise and

dedication in

the interests of

the company.

a) 1 • The Compensation Committee keeps the Board of Directors abreast of its deliberations during the latter’s meetings, and reports to it at least once a year in detail on the development of the compensation process and the Committee’s experience; where necessary it proposes the requisite changes to the compensation system.

33 New statement

• The Compensation Committee should carry out the duties assigned to it in a dedicated manner. It should also only represent the interests of the company in discussions and negotiations on individual compensation packages. It should gather the necessary specialist knowledge to do so where required by bringing in independent external consultants.

• The Compensation Committee should keep the Board of Directors informed about its deliberations during the latter’s meetings and report to it periodically on the development of the remuneration process within the framework of the law, the Articles of Association and relevant resolutions of the General Shareholders’ Meeting. Where necessary, it should propose the requisite changes to the remuneration system.

“Swiss Code of Best Practice for Corporate Governance” 22

Particular features of the compensation system

Content No. Version 2007 No. Version 2014

As a rule, the

compensation

system should

contain both

fixed and

variable

components; it

should reward

performance

aimed at

medium and

long-term

success with

compensation

elements only

available at a

later date.

b) 4 • The Board of Directors determines whether or not share-based compensation is awarded as well. In this case the Board considers the different effects of allocating shares on the one hand and options or similar instruments on the other.

• Where share based compensation is concerned, the Committee ensures the timeliness of such compensation. As a rule, it tailors the immediately available elements of the compensation package to the attainment of short-term targets; elements of the compensation package dependent upon the attainment of medium- or longer-term goals should be vested or blocked for a number of years.

35 New statement

• The compensation system for individuals in non-executive positions should generally only contain fixed elements. In principle, these should consist of payments and share allocations.

• The Board of Directors should determine whether or not share-based compensation is awarded, with the goal of converging the highest company representatives as closely as possible to the interests of long-term committed shareholders. In this case, the Board of Directors should consider the different effects of allocating shares on the one hand and options or similar instruments on the other. During this time, it should take into account experiences and developments within the relevant markets.

• Compensation packages should generally consist of immediately available components for shorter-term, identifiable targets and deferred or blocked components for medium- or longer-term targets. In the event of deferred remunerations which are share-based, the Compensation Committee should respect appropriate performance criteria and a meaningful matching of maturities.

b) 5 • When drawing up employment contracts with members of the Executive Board, any unusually long notice periods or contract durations are to be avoided except in specific situations.

• Options on shares of the company are granted with a strike set at the same level or preferably higher than the average market value in question over a determined number of trading days prior to the day of granting.

36 • In employment contracts with members of the Executive Board, the maximum applicable statutory notice periods and contract terms of twelve months must be observed and no illicit termination benefits may be agreed upon.

New Statement

• No compensation should be paid out in advance. Starting benefits should only be granted when they serve as compensation for recoverable claims lost by the new member of the Board of Directors or Executive Board in question as a result of the change in company.

• To counter non-justified benefits or to sanction a serious lack of compliance, repayment obligations or forfeiture provisions for deferred or blocked compensation can be agreed upon (“claw backs”).

“Swiss Code of Best Practice for Corporate Governance” 23

Implications Action points

• The possibility to get “golden parachutes” is not mentioned anymore.

• Recommended to have only fixed elements for the compensation of non-executive positions.

• The goal of the share-based compensation should be to align the interest of high company representatives and long-term committed shareholders.

• To counter non-justified benefits or if there is a lack of compliance, repayment obligations are possible (“claw backs”).

• Assess the impact of the compensation requirement changes.

“Swiss Code of Best Practice for Corporate Governance” 24

Compensation report and transparency

Implications Action points

• The shareholders hold now a vote on the total compensation (Minder initiative).

• Assess the impact of changes on the company.

• Support (increased) information and communication actions with shareholders.

Content No. Version 2007 No. Version 2014

The Board of

Directors

should produce

an annual

compensation

report and

ensure

transparency

with respect to

the

compensation

given to the

members of the

Board of

Directors and

the Executive

Board.

c) 9 The Board of Directors involves the Shareholders’ Meeting in the debate on the compensation system in an appropriate form.

• The Board of Directors decides how to involve the Shareholders’ Meeting in the debate on the compensation system.

• As a rule, it selects one of the following options:

Option 1

• The compensation report is brought into the discussion during the agenda items.

Option 2

• The Board of Directors puts the compensation report (…) to a consultative vote at the Shareholders’ Meeting.

38 New statements (replace sections c) 9 and d) 10 from 2007’s version)

• The compensation report should also show transparently how the Board of Directors and the Compensation Committee have implemented the compensation decisions of the General Shareholders’ Meeting made in advance in the business year under review.

• If the General Shareholders’ Meeting prospectively approves or authorises the total compensation, the Board of Directors is permitted to present the compensation report to the General Shareholders’ Meeting for consultative voting.

d)10 The Board of Directors ensures transparency with respect to the compensation of the members of the Board of Directors and the Executive Board.

“Swiss Code of Best Practice for Corporate Governance” 25

5. Contact

Roger Müller

Partner FAAS Corporate Governance Services Direct: +41 58 286 33 96

Email: [email protected]

“Swiss Code of Best Practice for Corporate Governance” 26

“Swiss Code of Best Practice for Corporate Governance” 27

EY | Assurance | Tax | Transactions | Advisory About EY

EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

EY’s organization is represented in Switzerland by Ernst & Young Ltd, Basel, with ten offices across Switzerland, and in Liechtenstein by Ernst & Young AG, Vaduz. In this publication, «EY» and «we» refer to Ernst & Young Ltd, Basel, a member firm of Ernst & Young Global Limited. © 2014 Ernst & Young Ltd. All Rights Reserved.

ED None This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com