supreme court of the united states table of authorities—continued page(s) in re roberts, 54 b.r....

TRANSCRIPT

No. 16-1215

WILSON-EPES PRINTING CO., INC. – (202) 789-0096 – WASHINGTON, D. C. 20002

IN THE

Supreme Court of the United States ————

LAMAR, ARCHER & COFRIN, LLP, Petitioner,

v.

R. SCOTT APPLING, Respondent.

————

On Writ of Certiorari to the United States Court of Appeals

for the Eleventh Circuit

————

BRIEF OF AMICI CURIAE THE HONORABLE EUGENE WEDOFF (RET.)

AND A GROUP OF LAW PROFESSORS IN SUPPORT OF RESPONDENT

————

DAVID R. KUNEY Counsel of Record

WHITEFORD, TAYLOR & PRESTON, LLP

1800 M. Street. N.W. Suite 450 North Washington, D.C. 20036 (202) 659-6807 [email protected]

Counsel for Amici Curiae

April 2, 2018

(i)

TABLE OF CONTENTS

Page

TABLE OF AUTHORITIES ................................ iv

INTEREST OF THE AMICI CURIAE ................ 1

SUMMARY OF THE ARGUMENT .................... 7

ARGUMENT ........................................................ 9

I. The availability of a discharge is of critical importance to individual debtors, to the larger economy, and to the proper functioning of the bankruptcy system ..... 9

A. The correct interpretation of 11 U.S.C. § 523(a)(2)(A) should begin with the economic and contextual importance of the bankruptcy discharge for the individual debtor ................................. 9

B. The correct interpretation of 11 U.S.C. § 523(a)(2)(A) should reflect the fiscal and contextual importance of the bankruptcy discharge on the larger economy................................................ 12

C. Chapter 7 debtors frequently lack legal counsel for discharge litigation, which leaves them vulnerable to unwarranted settlement pressure ...... 14

II. Section 523(a)(2)(A) should be inter-preted broadly to mean that the excep-tion to nondischargeability may include an oral statement about a single asset .... 17

ii

TABLE OF CONTENTS—Continued

Page

A. Section 523(a)(2)(A) expressly adopts a broad notion of what is discharge-able by use of the word “respecting” to modify financial condition ................... 17

B. Prior to the adoption of the Code in 1978, most circuit courts generally interpreted “respecting financial con-dition” as applying to more than a formal financial statement .................. 19

C. The meaning of “financial condition” cannot be determined by reliance on the definition of “insolvency” in Code § 101. The definition of equitable insolvency provides a better tool for interpreting “financial condition.” ...... 23

III. The legislative history demonstrates that Congress has been expanding protection against loss of the discharge and that § 523(a)(2)(A) was intended to have a broad meaning .......................................... 25

A. “Financial condition” has been broadly defined since the passage of the Bankruptcy Act in 1898 ...................... 27

B. In 1960 and 1978, Congress added greater debtor protection from loss of the discharge in view of creditor abuse of the discharge provisions .................. 30

CONCLUSION .................................................... 34

iii

TABLE OF CONTENTS—Continued

APPENDIX Page

Bankruptcy Act of 1898, § 14, 30 Stat. 544 ... 1a

Act of February 5, 1903, ch. 487, § 4, 32 Stat. 797 .................................................................. 2a

Amendment of the Bankruptcy Act, S. Rep. No. 61-691 (1910) ........................................... 4a

Establish a Uniform System of Bankruptcy, H. Rep. No. 69-1257 (1926) ............................ 7a

Act of May 27, 1926, § 6, Pub. L. No. 69-301 44 Stat. 662 ..................................................... 10a

Act of June 22, 1938, Pub. L. No. 75-696, § 14, 52 Stat. 850 ............................................ 12a

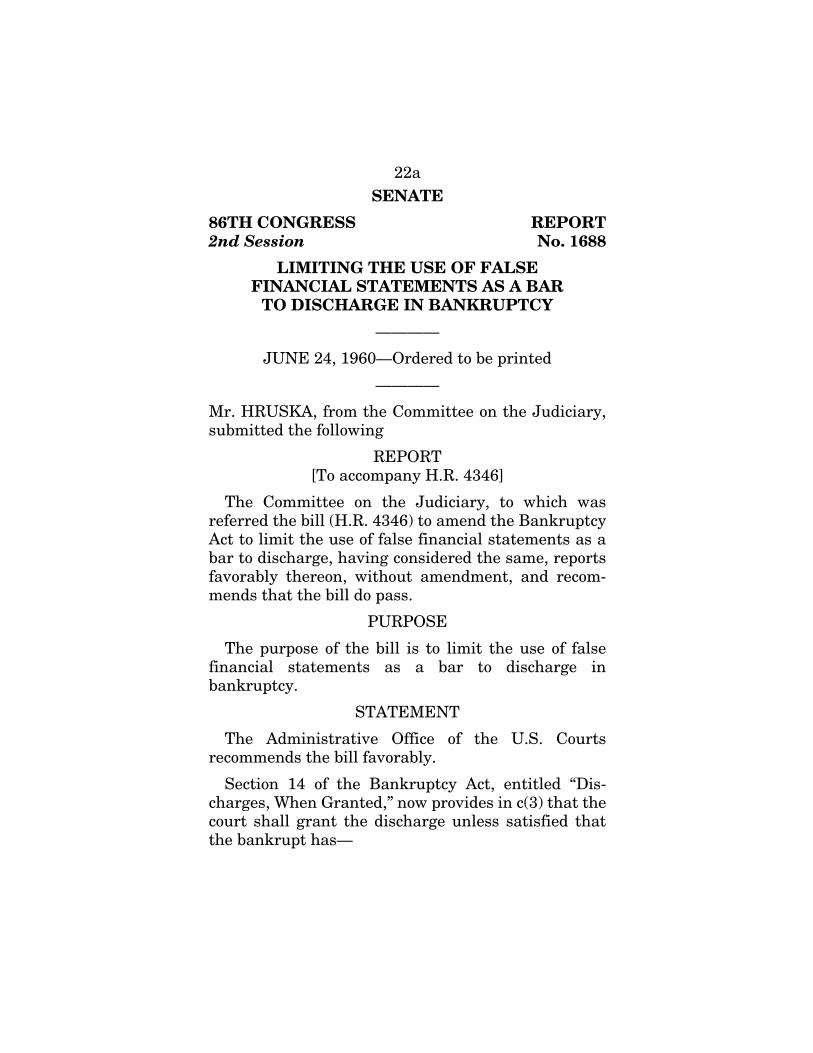

Limiting the Use of False Financial State-ments as a Bar to Discharge in Bankruptcy, H. Rep. No. 86-1111 (1959) ........................... 15a

Limiting the Use of False Financial State-ments as a Bar to Discharge in Bankruptcy, S. Rep. No. 86-1688 (1960) ............................. 22a

Act of July 12, 1960, Pub. L. No. 86-621, 74 Stat. 408 ......................................................... 33a

Bankruptcy Law Revision, H. Rep. No. 95-595 (1977) ....................................................... 35a

Act of November 6, 1978, Pub. L. 96-598, §§ 523-524, 92 Stat. 2590 ............................... 55a

iv

TABLE OF AUTHORITIES

CASES Page(s)

Albinak v. Kuhn, 149 F.2d 108 (6th Cir. 1945) ..................... 20, 21

District of Columbia v. Greater Washington Bd. of Trade, 506 U.S. 125 (1992) ................................... 18

Field v. Mans, 516 U.S. 59 (1995) ................................. 3, 31, 32

Heald v. District of Columbia, 254 U.S. 20 (1920) ..................................... 22

In re C.F. Foods, L.P., 280 B.R. 103 (Bankr. E.D. Penn. 2002) ... 25

In re Cook, 46 B.R. 545 (Bankr. E.D. Va. 1985) ......... 22

In re Dolata, 306 B.R. 97 (Bankr. W.D. Pa. 2004) ......... 24

In re Hyman, 502 F.3d 61 (2d Cir. 2007) ........................ 7

In re Joelson, 427 F.3d 700 (10th Cir. 2005) ................... 3, 24

In re Kanour, No. 09–07030JAD, 2010 WL 8354696 (Bankr. W.D. Pa. July 1, 2010) ................. 24

In re Powell, 423 B.R. 201 (Bankr. N.D. Tex 2010) ... 4, 14, 22

In re Prestridge, 45 B.R. 681 (Bankr. W.D. Tenn. 1985) .... 22

v

TABLE OF AUTHORITIES—Continued

Page(s)

In re Roberts, 54 B.R. 765 (Bankr. D.N.D. 1985) ............ 22

J.W. Ould Co. v. Davis, 246 F. 228 (1917) ................................ 28, 29, 30

Jerman v. Carlisle, McNellie, Rini, Kramer & Ulrich LPA, 559 U.S. 573 (2010) ................................... 22

Key v. Doyle, 434 U.S. 59 (1977) ..................................... 22

Lemon v. Kurtzman, 403 U.S. 602 (1971) ................................... 18

Local Loan Co. v. Hunt, 292 U.S. 234 (1934) ................................... 6

Lockhart v. Edel, 23 F.2d 912 (4th Cir. 1928) ...................... 19

Mau v. Sampsell, 185 F.2d 400 (9th Cir. 1950) ..................... 20

Moody v. Sec. Pac. Bus. Credit, Inc., 971 F.2d 1056 (3d Cir. 1992) .................... 24

Rake v. Wade, 508 U.S. 471 (1993) ................................... 17

Shainman v. Shear’s of Affton, Inc., 387 F.2d 33 (8th Cir. 1967) ....................... 20

Shaw v. Delta Airlines, Inc., 463 U.S. 85 (1983) ..................................... 18

Smith v. United States, 508 U.S. 223 (1993) ................................... 18

vi

TABLE OF AUTHORITIES—Continued

Page(s)

Taltech Ltd. v. Esquel Enterprises Ltd., 410 F. Supp. 2d 977 (W.D. Wash. 2006) .................................... 23

Tenn v. First Hawaiian Bank, 549 F.2d 1356 (9th Cir. 1977) ................... 21

Wright v. Union Cent. Life Ins. Co., 311 U.S. 273 (1940) ................................... 9

STATUTES

11 U.S.C.A. § 32 ............................................ 20

Act of 1898, § 14b(2), 30 Stat. 544-550 ........ 27

Act of Feb. 5, 1903, ch. 487, 32 Stat. 797 (1903) ......................................................... 27

Act of May 27, 1926, Pub. L. 69-301, ch. 406, 44 Stat. 662-63 .................................. 19, 29

Act of July 12, 1960, Pub. L. No. 86-621, 74 Stat. 408-409 ....................................... 19, 31, 32

U.S. Bankruptcy Code, 11 U.S.C. § 101 et. seq. .......................................................passim

§ 101(32) .................................................... 23

§ 523(a)(2) .................................................. 18, 33

§ 523(a)(2)(A) ............................................passim

§ 523(a)(2)(B) ............................................. 22

§ 548(a)(1)(B)(ii) ........................................ 24

§ 548(a)(1)(B)(ii)(III) ................................. 24

vii

TABLE OF AUTHORITIES—Continued

LEGISLATIVE MATERIALS Page(s)

H. Rep. No. 69-1257 (1926) .......................... 19, 29

H. Rep. No. 86-1111 (1959) .......................... 30, 31

H. Rep. No. 95-595 (1977) ...........................passim

S. Rpt. No. 61-691 (1910) ............................. 29

S. Rep. No. 86-1688 (1960) ........................... 14, 31

OTHER AUTHORITIES

Amber J. Moren, Note, Debtor’s Dilemma: The Economic Case for Ride-Through in the Bankruptcy Code, 122 Yale L.J. 1594 (2013) ......................................................... 13

Andrew F. Emerson, So You Want to Buy a Discharge? Revisiting the Sticky Wicket of Settling Denial of Discharge Proceedings in the Chapter 7 Bankruptcy, 92 Am. Bank. L.J. 111 (2018) ................................ 15

Angela Littwin, The Affordability Paradox: How Consumer Bankruptcy’s Greatest Weakness May Account for Its Surprising Success, 52 Wm. & Mary L. Rev. 1933 (2011) ......................................................... 15

Charles Jordan Tabb, The Historical Evolution of the Bankruptcy Discharge, 65 Am. Bankr. L.J. 325 (1991) ................. 13

Jay L. Zagorski & Lois R. Lupica, A Study of Consumers’ Post-Discharge Finances: Struggle, Stasis, or FreshStart? 16 Am. Bankr. Inst. L. Rev. 283 (2008) ................ 11, 12

viii

TABLE OF AUTHORITIES—Continued

Page(s)

John C. McCoid, II, Discharge: The Most Important Development in Bankruptcy History, 70 Am. Bankr. L.J. 163 (1996) ... 5

Katherine Porter & Deborah Thorne, The Failure of Bankruptcy’s Fresh Start, 92 Cornell L. Rev. 67 (2006) .......................... 12

March 2017 Bankruptcy Filings Down 4.7 Percent, United States Courts (Apr. 19, 2017), http://www.uscourts.gov/news/20 17/04/19/march-2017-bankruptcy-filings-down-47-percent [https://perma.cc/LB7B- CAEA] ........................................................ 5

Maurie Backman, This Is the No. 1 Reason Americans File for Bankruptcy, The Motley Fool (May 1, 2017), https://www. fool.com/retirement/2017/05/01/this-is-th e-no-1-reason-americans-file-for-bankrup. aspx [https://perma.cc/M8WA-2WQ8] ....... 10

Michael D. Sousa, The Principle of Con-sumer Utility: A Contemporary Theory of Bankruptcy Discharge, 58 U. Kan. L. Rev. 553 (2010) .......................................... 16

NFIB National Small Business Poll Getting Paid (William J. Dennis, Jr. eds., 2001), http://www.411sbfacts.com/files/gettingpaid[1].pdf [https://perma.cc/CDZ7-PX6T] .... 13, 14

Rafael I. Pardo, An Empirical Examination of Access to Chapter 7 Relief by Pro Se Debtors, 26 Emory Bankr. Dev. J. 5 (2009) ......................................................... 15

ix

TABLE OF AUTHORITIES—Continued

Page(s)

Respecting, Funk & Wagnalls, Standard Encyclopedic Dictionary (1968), www. Funkand Wagnallnalls.com ...................... 17

Respecting, Oxford English Dictionary (3d ed. 2010) .............................................. 17

Robert M. Lawless, et. al., Did Bankruptcy Reform Fail? An Empirical Study of Consumer Debtors, 82 Am. Bankr. L. J. 349 (2008) .................................................. 11

Ronald J. Mann, Bankruptcy and the U.S. Supreme Court (2017) ............................... 32

Teresa A. Sullivan, Elizabeth Warren & Jay Lawrence Westbrook, As We Forgive Our Debtors: Bankruptcy and Consumer Credit in America (1989) .......................... 5, 6

Teresa A. Sullivan, Elizabeth Warren, & Jay Lawrence Westbrook, Consumer Debtors Ten Years Later: A Financial Comparison of Consumer Bankrupts 1981–1991, 68 Am. Bankr. L.J. 121 (1994) ......................................................... 11

Teresa A. Sullivan, Elizabeth Warren & Jay Lawrence Westbrook, Limiting Access to Bankruptcy Discharge: An Analysis of the Creditors’ Data, 1983 Wis. L. Rev. 1091 (1983) ........................... 10

Teresa A. Sullivan, Elizabeth Warren & Jay Lawrence Westbrook, The Fragile Middle Class: Americans in Debt (2000) .............. 10

x

TABLE OF AUTHORITIES—Continued

Page(s)

2 William Blackstone, Commentaries on the Laws of England (1765-1769) ................... 13

William F. Stone, Jr. & Bryan A. Stark, The Treatment of Attorneys’ Fee Retainers in Chapter 7 Bankruptcy and the Problem of Denying Compensation to Debtors’ Attor-neys for Post-Petition Legal Services They Are Obligated to Render, 82 Am. Bankr. L.J. 551 (2008) .......................................... 15-16

INTEREST OF THE AMICI CURIAE1

The amici curiae, whose names are set forth below, include a former bankruptcy judge and law professors at various universities where they teach courses on bankruptcy law, conduct research, and are frequent speakers and lecturers at seminars and conferences on bankruptcy law.

The Honorable Eugene Wedoff (ret.) served as a U.S. Bankruptcy Judge in the Northern District of Illinois in Chicago from 1987-2015 and as Chief Judge from 2002-07. Before his judicial service, Judge Wedoff was a partner and member of the executive committee of the Chicago law firm of Jenner & Block. He served as a member and as the chair of the Advisory Committee on Bankruptcy Rules from 2004 to 2014, and as a governor, secretary, and president of the National Conference of Bankruptcy Judges through 2015. He is currently president of the American Bankruptcy Institute. He is a Fellow of the American College of Bankruptcy and a member of the National Bankruptcy Conference.2

Margaret Howard is the Law Alumni Association Professor of Law, Emerita, at Washington and Lee University School of Law, Lexington, Virginia. She

1 Pursuant to this Court’s Rule 37.3(a), both parties sent a

letter or email granting consent to this amici curiae brief. Pursuant to Rule 37.6, amici affirm that no counsel for a party authored this brief in whole or in part, and that no person other than amici or their counsel contributed any money to fund its preparation or submission.

2 The views set forth herein are the personal views of Judge Wedoff and the named amici and are not necessarily the views of the American Bankruptcy Institute, which has not participated in any way in this appeal.

2 has taught and conducted research on topics in bank-ruptcy law for more than three decades, with an emphasis on discharge issues in consumer bank-ruptcy. She holds a B.A. from Duke University, a J.D. and M.S.W. from Washington University in St. Louis, and an LL.M from Yale University. She has served as the Scholar in Residence at the American Bankruptcy Institute, and as the ABI’s Vice President in charge of the Research Grants Committee. Professor Howard is a fellow of the American College of Bankruptcy and the American Law Institute.

Professor Jack F. Williams is a professor of law at Georgia State University and the Center for Middle East Studies, where he teaches and/or conducts research on bankruptcy and business organizations; mergers and acquisitions; and taxation and statistics. He is the Association of Insolvency and Restructuring Scholar in Residence. He is a fellow in the American College of Bankruptcy. He holds a B.A. in economics from the University of Oklahoma, a J.D. with High Honors from George Washington University National Law Center, and a Ph.D in archaeology from the University of Leicester in Leicester, United Kingdom.

David R. Kuney is an Adjunct Professor at the Georgetown University Law Center where he teaches bankruptcy law. He has taught at American University’s Washington College of Law and at New York Law School. He was formerly a partner at the law firm of Sidley & Austin. He currently serves on the Board of Directors of the American Bankruptcy Institute. He is a fellow in the American College of Bankruptcy.

Your amici are submitting this brief out of a concern that the discharge provisions of the Bankruptcy Code not be interpreted in such a fashion as to cause unwarranted economic injury to individual debtors

3 nor to the larger economy. We write because Petitioner has offered an interpretation of the Code and a view of debtors that we believe is decidedly incorrect and will cause economic harm to many.

The central issue in this case concerns the correct interpretation and application of one of the key discharge provisions in the U.S. Bankruptcy Code,3 namely, 11 U.S.C. § 523(a)(2)(A). This provision states that the Code prohibits the discharge of “any debt . . . for money, property, [or] services . . . to the extent obtained by . . . false pretenses [or] false representa-tion . . . other than a statement respecting the debtor’s . . . financial condition” (emphasis added).

Petitioner argues that the phrase “other than” only excludes from the rule of non-dischargeability a debt obtained by an oral misrepresentation that is tantamount to a “standard” financial statement, e.g., statements that reflect a debtor’s overall assets and liabilities.4 Oral statements about a debtor’s individ-ual assets or debts, large or small, material or not, would potentially bar a discharge, in Petitioner’s view. Debtors would be subject to a discharge challenge based on oral statements, often made many years earlier, for which there is no written evidence and without any showing of reasonable reliance.5

3 11 U.S.C. § 101 et. seq. (the “Code”). 4 See, e.g., In re Joelson, 427 F.3d 700, 707 (10th Cir. 2005)

(describing the limited view that the phrase “statement respect-ing the debtor’s . . . financial condition” as used in § 523(a)(2)(A) means “a debtor's net worth or overall financial condition.”).

5 See Field v. Mans, 516 U.S. 59 (1995) (requiring the lesser showing of “justifiable reliance”).

4 The Eleventh Circuit held the opposite, finding that

an alleged oral misrepresentation concerning even a single asset may still be a statement “respecting” or “related to” one’s financial condition, and hence may not serve as the basis to bar a debtor’s discharge. This view was, until recently, the majority view.6 The Solicitor General, representing the United States as the largest creditor in bankruptcy matters, agrees. S.G. Opp. Br. 21. So do we.

Petitioner’s opening sentence describes Mr. Appling as one who lied to his attorneys and references to lying appear four times in the first paragraph. Pet. Br. 2. Petitioner also argues that the Eleventh Circuit’s ruling would permit a “truck” to be driven through the Code’s discharge provisions. Cert. Pet. 2. Implicit in this opening argument is a view of debtors, collectively, as “can-pay” individuals who will opportunistically seek to game the system when given the chance. Petitioner’s brief is premised on this unflattering view of the population of individual debtors and a notion that Congress has sought to rein in misconduct by ever stricter views of who deserves a discharge.

Petitioner’s view of both debtors collectively and of Congressional response to the discharge issue are decidedly inaccurate. We urge a different view and one widely supported by the existing empirical data, which is missing from Petitioner’s brief. The large body of economic data on the true nature and purpose of the discharge for individual debtors in the bankruptcy system discloses not only a bona fide need

6 See In re Powell, 423 B.R. 201, 210 (Bankr. N.D. Tex 2010) (“Other courts (and the emerging majority of cases) adopt a more liberal view. Those courts have defined the phrase to encompass a much broader class of statements, even those which relate to a single asset or liability.”).

5 for discharge protection, but the macroeconomic value that relieving debt has on the general economy. Congress is aware of this plight and Congressional statements, as well as the legislative movement, over the past 60 years, have sought to broaden protection of the discharge. The Eleventh Circuit correctly perceived this.

The bankruptcy discharge goes to the very heart of bankruptcy law and deeply affects its administration, outcome, and social value. “[T]he introduction of the discharge [into modern bankruptcy law] could well be considered the single most important event in bankruptcy history.” Teresa A. Sullivan, Elizabeth Warren & Jay Lawrence Westbrook, As We Forgive Our Debtors: Bankruptcy and Consumer Credit in America 20 (1989). Indeed, commentators have ob-served that the bankruptcy discharge “ranks ahead in importance of all others in Anglo-American bank-ruptcy history.” John C. McCoid, II, Discharge: The Most Important Development in Bankruptcy History, 70 Am. Bankr. L.J. 163, 164 (1996).

This case has widespread importance to potentially millions of individual Chapter 7 debtors because of its potential to deny a discharge for debtors and to change the law in many jurisdictions.7 Individual debtors who seek bankruptcy relief have been well-studied and their economic plight analyzed with statistical care: “when bankrupt debtors as a group are compared to the general population, their situations are grim.”

7 The number of non-business bankruptcy filings in 2017, 2016, and 2015 was as follows: 770,901, 808,781, and 911,086, respectively. March 2017 Bankruptcy Filings Down 4.7 Percent, United States Courts (Apr. 19, 2017), http://www.uscourts. gov/news/2017/04/19/march-2017-bankruptcy-filings-down-47-pe rcent [https://perma.cc/LB7B-CAEA].

6 Sullivan et al., As We Forgive Our Debtors, supra at 77. The data shows “a segment of America in financial collapse.” Id.

Petitioner’s harsh rule strays far from the underlying principles expressed by this Court over eighty years ago, in which this Court held that bankruptcy discharge is an essential aspect of one’s financial and personal “liberty.” Local Loan Co. v. Hunt, 292 U.S. 234, 245 (1934).

The power of the individual to earn a living for himself and those dependent upon him is in the nature of a personal liberty quite as much as, if not more than, it is a property right. To preserve the free exercise is of the utmost importance, not only because it is a fundamental private necessity, but because it is a matter of great public concern . . . . The new opportunity in life and the clear field for future effort, which it is the purpose of the bankruptcy act to afford the emancipated debtor, would be of little value to the wage earner if he were obliged to face the necessity of devoting the whole or a considerable por-tion of his earnings for an indefinite period of time in the future to the payment of indebt-edness incurred prior to his bankruptcy.

The underlying principles of Local Loan pertain here, as does long-standing practice and the words of the Code. For these reasons set forth below, the Eleventh Circuit’s decision should be affirmed.

7 SUMMARY OF THE ARGUMENT

The Bankruptcy Code, at 11 U.S.C. § 523(a)(2)(A), prohibits a discharge of “any debt . . . for money, property, [or] services . . . to the extent obtained by . . . a false representation . . . other than a statement respecting the debtor’s . . . financial condition.” The question presented in this case is whether the phrase beginning with “other than” should be broadly inter-preted to mean a statement concerning even a single asset or whether it should be narrowly construed to mean only a statement regarding the debtor’s overall financial condition. The better-reasoned rule, and the rule consistent with congressional intent and sound bankruptcy policy, is that § 523(a)(2)(A) may include a statement concerning even one asset where that statement bears on the debtor’s ability to perform or pay the relevant transaction. Accordingly, the decision of the Eleventh Circuit should be affirmed for the following reasons:

First, the proper judicial interpretation of § 523(a)(2)(A) requires consideration of the underlying economic rationale of the bankruptcy discharge, as well as the statutory language used by Congress. One informs the other. The ability of an individual consumer debtor to obtain a discharge in bankruptcy has been said to be a matter of economic life and death. “The consequences to a debtor whose obligations are not discharged are considerable; in many instances, failure to achieve discharge can amount to a financial death sentence.” In re Hyman, 502 F.3d 61, 66 (2d Cir. 2007). Petitioner’s overly narrow view of § 523(a)(2)(A) injures not only individual debtors, but also has a demon-strated harm to the macro economy by discouraging family formation, educational expenditures, and over-all participation in the economy.

8 Second, the statutory language of § 523(a)(2)(A)

fully demonstrates a broader reading of the protection for the discharge. The phrase “respecting financial condition” was first introduced into American bank-ruptcy law in 1926. Virtually every circuit court that interpreted this section prior to adoption of the Code in 1978 held that the phrase was not limited to only a formal financial statement. Petitioner’s reliance on the Code definition of “insolvency” as somehow supply-ing the definition of “financial condition” is unsound and contradicted by other Code-based definitions of insolvency that suggest a different outcome.

Third, the legislative history likewise shows that Congress has been moving steadily toward broader protection of the discharge for individual debtors. The key terminology, such as “financial condition” and “false statement” were untethered to any notion of a formal financial statement. Indeed, when Congress enacted the 1978 Code, the Bankruptcy Commission created to recommend changes to the bankruptcy law was so concerned over creditor abuse of the “financial condition” provision that it “recommended that this exception to discharge be eliminated for consumer debts.” H. Rep. No. 95-595 (1977). App. 47a. While Congress did not eliminate it, Congress did strictly limit the ability to challenge the discharge in new § 523(a)(2)(A). It is inconceivable that the Code should now be read as making the discharge less available when Congress was seeking exactly the opposite outcome.

Accordingly, we urge this Court to affirm the deci-sion of the Eleventh Circuit.

9 ARGUMENT

I. The availability of a discharge is of critical importance to individual debtors, to the larger economy, and to the proper func-tioning of the bankruptcy system.

A. The correct interpretation of 11 U.S.C. § 523(a)(2)(A) should begin with the economic and contextual importance of the bankruptcy discharge for the indi-vidual debtor.

The discharge provisions of the Code were not drafted in a vacuum; they were instead manifestly responsive to perceived economic distress. Thus, a proper interpretation of § 523(a)(2)(A) must reflect the bankruptcy discharge’s impact on the individual debtor, the larger social and economic benefits of the discharge, and Congressional recognition of these values. “[T]he [Bankruptcy] Act must be liberally construed to give the debtor the full measure of the relief afforded by Congress, lest its benefits be frittered away by narrow formalistic interpretations which disregard the spirit and the letter of the Act.” Wright v. Union Cent. Life Ins. Co., 311 U.S. 273, 279 (1940) (internal citations omitted).

Petitioner argues that the rule announced by the Eleventh Circuit undermines the primary operation of § 523(a)(2)(A) “by creating a loophole through which dishonest debtors might relieve themselves, at honest creditors’ expense, of liabilities incurred through fraud.” Cert. Pet. 21. Petitioner argues that the broad rule would permit debtors to “drive a truck” through the intended policy of Congress. Id.

All of these contentions are lacking in any empirical data to support the notion of meaningful debtor abuse.

10 Indeed, Petitioner offers no support for the view that Chapter 7 debtors are in any position to “drive a truck” through Code-based policies nor that such debtors even exist.

Instead, empirical data demonstrates that the typical Chapter 7 debtor seeks bankruptcy protection due to a grim and serious economic plight, rather than misconduct, over-spending, or other non-productive economic conduct. Economic relief in the form of a discharge is of critical importance, and often protects the debtor from health and life-risking choices, such as between medical treatment and food.8 This is important because one in ten Americans has filed for either a Chapter 7 or a Chapter 13 bankruptcy. Teresa A. Sullivan, Elizabeth Warren & Jay Lawrence Westbrook, The Fragile Middle Class: Americans in Debt 22 (2000).

When asked why they filed for bankruptcy 67.5 percent of debtors reported job loss, 19.3 percent cited a medical event, and 22.1 percent listed family concerns (i.e. divorce) as contributing factors that led to their bankruptcy. Id. at 16 fig. 1.2. These Americans file for bankruptcy not because it is “an easy way out,” but because they have run out of options. Teresa A. Sullivan, Elizabeth Warren & Jay Lawrence Westbrook, Limiting Access to Bankruptcy Discharge: An Analysis of the Creditors’ Data, 1983 Wis. L. Rev. 1091, 1138 (1983).

8 One of the largest single causes for the filing of Chapter 7

bankruptcy by individuals is catastrophic medical issues, such as cancer, automobile and industrial accidents, and age-related issues. Maurie Backman, This Is the No. 1 Reason Americans File for Bankruptcy, The Motley Fool (May 1, 2017), https://www. fool.com/retirement/2017/05/01/this-is-the-no-1-reason-americans-file-for-bankrup.aspx [https://perma.cc/M8WA-2WQ8].

11 Debtors who seek bankruptcy protection earn much

less money and owe much more than the average American. Robert M. Lawless, et. al., Did Bankruptcy Reform Fail? An Empirical Study of Consumer Debtors, 82 Am. Bankr. L. J. 349, 371–72 (2008).

[The] median household income for bankrupt debtors in 2007 was about $27,100—statisti-cally indistinguishable from the $27,800 in 2001 and $27,100 back in 1991. Median household income across the United States in 2006 was $48,200. These figures put the income of the median bankrupt household in 2007 a full 45% below the income of the median household in the general U.S. population.

Id. at 363.

Only a small fraction of debtors had any hope of repaying their debt outside of bankruptcy. Even those debtors who voluntarily attempted repayment in Chapter 13 were in terrible shape: at most, only about a third were able to complete their repayment plans, and a significant portion of those debtors were making only minimal repayments. See Teresa A. Sullivan, Elizabeth Warren, & Jay Lawrence Westbrook, Consumer Debtors Ten Years Later: A Financial Comparison of Consumer Bankrupts 1981–1991, 68 Am. Bankr. L.J. 121, 123 (1994).

The discharge provisions have proven to be effective. Debtors who obtain a discharge are generally restored to a productive role in the larger economy. Empirical studies support the concept of fresh start. Indeed, “the average person who files for bankruptcy to relieve financial stress catches up with their peers.” Jay L. Zagorski & Lois R. Lupica, A Study of Consumers’

12 Post-Discharge Finances: Struggle, Stasis, or Fresh-Start? 16 Am. Bankr. Inst. L. Rev. 283, 289 (2008).9 “One study compared bankruptcy filers with non-filers regarding key economic factors such as car ownership and debt, home ownership and debt, savings, credit card ownership, income, and work.” See id. at 296. “None of the data indicate that over time the size of the financial gap between bankruptcy filers and non-filers either gets wider or stays the same; for the most part, the size of the financial gap between these two groups narrows over time.” Id. at 307. Thus, empirical research establishes that the discharge provisions achieve the key goal of restoring individu-als to economic capacity.

B. The correct interpretation of 11 U.S.C. § 523(a)(2)(A) should reflect the fiscal and contextual importance of the bankruptcy discharge on the larger economy.

The bankruptcy discharge benefits the larger econ-omy while aiding the individual. Petitioner incorrectly posits the bankruptcy discharge as a benefit only to the individual debtor, and then, only on a strict condition of “honesty.” This misses much of the point about the importance of the discharge. The discharge also has macro consequences which benefit the larger economy. “The theory is that society as a whole bene-fits when an overburdened debtor is freed from the oppressive weight of accumulated debt. The debtor then is able to resume his or her place as a productive

9 See also Katherine Porter & Deborah Thorne, The Failure of

Bankruptcy’s Fresh Start, 92 Cornell L. Rev. 67, 87 (2006) (“The majority, 65% of families, reported that their financial situations had improved since they filed bankruptcy.”).

13 member of society.” Charles Jordan Tabb, The Historical Evolution of the Bankruptcy Discharge, 65 Am. Bankr. L.J. 325, 364–65 (1991). Essentially, “the bankrupt becomes a clear man again; and, by the assistance of his allowance and his own industry, may become a useful member of the commonwealth.” 2 William Blackstone, Commentaries *484.

Additionally, “it has been noted that the Chapter 7 debt discharge prevents the development of an insol-vent underclass and incentivizes entrepreneurship by offering a mandatory insurance policy for failed business endeavors.” Amber J. Moren, Note, Debtor’s Dilemma: The Economic Case for Ride-Through in the Bankruptcy Code, 122 Yale L.J. 1594, 1618 (2013). This in turn encourages investment and economic stability.

While the discharge has a beneficial effect on the macro economy, the availability of a discharge for individual debtors has no significant impact on small business owners. The notion that the bankruptcy discharge has a significant adverse effect on small businesses is untrue, despite assertions of one amici in this case suggesting that the Eleventh Circuit rule is “fraudster friendly” and will injure small business. See NFIB Br. 17. The lack of bankruptcy harm to small business can be seen in the very polling data that the NFIB cites in its amicus brief, showing that only four percent of small businesses consider bankruptcy a cause of customer non-payment. NFIB National Small Business Poll Getting Paid 3 (William J. Dennis, Jr. eds., 2001), http://www.411sbfacts.com/ files/gettingpaid[1].pdf [https://perma.cc/CDZ7-PX6T]. This was only slightly greater than the “cost of using credit cards” at 2.9%. Id. Ninety-seven percent of all small business owners do not expect to encounter more

14 than one bankruptcy case per year. Id. at 6 (“That means about three percent of the entire small-business population failed to receive payment in five or more bankruptcy cases over the last five years, or one or less [sic] than case per year.”). Indeed, small business owners “benefit more from liberal bank-ruptcy laws than perhaps any other group.” Id.

It is also untrue that the rule in the Eleventh Circuit would create for the first time a rule requiring “mountains of paperwork” or a novel federal statute of frauds. NFIB Br. 3. Until 2010, the majority of courts did in fact follow the very rule urged by the Eleventh Circuit. See In re Powell, 423 B.R. at 210–11. Reversal of the Eleventh Circuit is far more likely to cause disruption in the operation of the bankruptcy system.

C. Chapter 7 debtors frequently lack legal counsel for discharge litigation, which leaves them vulnerable to unwarranted settlement pressure.

The economic distress of the individual debtor, as mentioned above, also means that Chapter 7 debtors frequently lack financial resources to retain legal counsel to defend themselves from discharge chal-lenges, whether well-grounded or not. Beginning in at least 1960, Congress became aware that the discharge provisions were being manipulated by institutional creditors who were able to intimidate honest debtors into surrendering their discharge in order to avoid litigation. It was precisely this threat of intimidation, noted by Congress in 1960 that led to one of the major reforms in discharge legislation. S. Rep. No. 86-1688 (1960). See App. 23a-24a. There is a well-documented history showing that the mere threat of a discharge challenge is often sufficient to provoke an unwar-ranted settlement in which the debtor surrenders his

15 or her discharge. Andrew F. Emerson, So You Want to Buy a Discharge? Revisiting the Sticky Wicket of Settling Denial of Discharge Proceedings in the Chapter 7 Bankruptcy, 92 Am. Bank. L.J. 111, 118–23 (2018).

This intimidation factor is exacerbated by the equally well-documented difficulty in providing legal representation to Chapter 7 debtors who confront discharge litigation. Legal counsel for Chapter 7 debtors frequently “unbundle” their legal services and decline to undertake representation of the debtor in an adversary proceeding challenging the discharge. “Unbundling” allows attorneys to limit the scope of their representation by excluding expensive tasks like adversary proceedings from their general services.

If a creditor challenges the discharge, an adversary proceeding may result. With these services “unbundled,” a Chapter 7 debtor may have to decide whether to pay additional and indeterminate legal fees or simply allow the creditor to collect its known debt in full, thus by-passing the collective process of bankruptcy. Debtors who appear pro se have less favorable outcomes in judicial proceedings.10

The frequent inability to retain legal counsel for discharge litigation makes Petitioner’s view of § 523(a)(2)(A) even more abusive. See William F. Stone, Jr. & Bryan A. Stark, The Treatment of

10 See, e.g., Rafael I. Pardo, An Empirical Examination of Access to Chapter 7 Relief by Pro Se Debtors, 26 Emory Bankr. Dev. J. 5 (2009); Angela Littwin, The Affordability Paradox: How Consumer Bankruptcy's Greatest Weakness May Account for Its Surprising Success, 52 Wm. & Mary L. Rev. 1933, 1957 (2011) (“The percentage of pro se cases rose statistically significantly, especially among lower-income debtors, while the percentage of these cases ending with a discharge of debt declined.”).

16 Attorneys’ Fee Retainers in Chapter 7 Bankruptcy and the Problem of Denying Compensation to Debtors’ Attorneys for Post-Petition Legal Services They Are Obligated to Render, 82 Am. Bankr. L.J. 551, 555 n.25 (2008).

The mere threat of discharge litigation is likely to provoke a settlement and waiver of the discharge, regardless of the merits of the discharge objection. Prior to enacting the 1978 Code, the House Judiciary Committee noted that, “[t]he threat of litigation over this [discharge] exception and its attendant costs are often enough to induce the debtor to settle for a reduced sum, in order to avoid the costs of litigation” even with respect to “marginal cases.” H. Rep. No. 95-595 (1977). App. 47a-48a.

The foundation of Petitioner’s argument is essen-tially empirical. Yet, Petitioner has not remotely shown that there is statistically significant fraud in the discharge area that justifies a narrower view of what is dischargeable. Nothing in the record before this Court, reported case law, or in Petitioner’s brief justifies a harsher interpretation of § 523(a)(2)(A) based on a uniform notion of debtor misconduct and risk of fraud. Mr. Appling is an isolated case.11 His con-duct is hardly the occasion to interpret § 523(a)(2)(A) in a way that produces negative macroeconomic effects by potentially injuring the nearly one million individu-als who seek bankruptcy relief each year.

11 “[T]he consumer bankruptcy system is generally utilized by

American families in grave financial circumstances.” Michael D. Sousa, The Principle of Consumer Utility: A Contemporary Theory of Bankruptcy Discharge, 58 U. Kan. L. Rev. 553, 614 (2010).

17 II. Section 523(a)(2)(A) should be interpreted

broadly to mean that the exception to nondischargeability may include an oral statement about a single asset.

A. Section 523(a)(2)(A) expressly adopts a broad notion of what is dischargeable by use of the word “respecting” to modify financial condition.

The phrase “financial condition” is not defined in the Code. Instead, the Code includes a key modifier, namely, the word “respecting,” which plainly connotes a broad and non-exclusive meaning. Petitioner, how-ever, urges a “narrow” definition which essentially disregards the full import of “respecting.” Pet. Br. 20–21.

Petitioner’s argument that this Court disregard the term “respecting” violates a core rule of statutory construction that requires that each word be given its full meaning.12 The term “respecting” is pivotal. “Respecting” is defined as “with respect to; with reference to; as regards.” Respecting, Oxford English Dictionary (3d ed. 2010). “Respecting” is also defined to mean “[i]n relation to; regarding.” Funk & Wagnalls, Standard Encyclopedic Dictionary, 567 (1968).13 This means that the term “respecting” expands upon subsequent terms in the phrase or sentence.

“Respecting” embraces notions of being “related to.” This Court has interpreted the phrase “relate[d] to”

12 See, e.g., Rake v. Wade, 508 U.S. 471 (1993) (“To avoid

deny[ing] effect to a part of a statute we accord significance and effect to every word.”) (citations omitted).

13 See also, FunkandWagnalls.com (same).

18 as being “deliberately expansive.” District of Columbia v. Greater Washington Bd. of Trade, 506 U.S. 125, 129 (1992) (“We have repeatedly stated that a law ‘relate[s] to’ a covered employee benefit plan for pur-poses of [ERISA] ‘if it has a connection with or reference to such a plan’ . . . and thus gives effect to the ‘deliberately expansive’ language chosen by Congress.”); Shaw v. Delta Airlines, Inc., 463 U.S. 85, 96–97 (1983) (same).14 The same is true within this Court’s constitutional jurisprudence. See Lemon v. Kurtzman, 403 U.S. 602, 612 (1971).

Significantly, in 1987, a House Report described the discharge provision as dealing with a “false state-ment in writing concerning the debtor’s financial condition . . . ” H. Rep. No. 95-595 (1977). App. 44a (emphasis added). This use of “concerning,” much like “respecting,” shows that Congress was looking broadly and well beyond merely formal financial statements.

Petitioner argues that “respecting” is too broad when read to mean “related to,” complaining that “everything is related to everything else.” Pet. Br. 31. But the statute is intended to be broad. The language in § 523(a)(2) was originally an exception to the discharge and was broad; this key point is expressly conceded by Petitioner who notes that the precursor to this section was intended to be “as broad as its authors could do it . . . ” Pet. Br. 9. Further, Petitioner’s argument overlooks the important judicial ability to draw sensible lines within broad language that con-form to congressional purpose. See Lemon, 403 U.S. at 612.

14 This Court also found that the phrase “in relation to” in a

criminal statute clarified that a firearm “must have some purpose or effect” with respect to a drug trafficking crime. See Smith v. United States, 508 U.S. 223, 237 (1993) (citation omitted).

19 B. Prior to the adoption of the Code in

1978, most circuit courts generally interpreted “respecting financial con-dition” as applying to more than a formal financial statement.

The “broad” meaning of the phrase “respecting financial condition” has longstanding roots in settled case law that dates back to 1928. The phrase “respecting financial condition” first appears in H. Rep. No. 69-1257 (1926) (App. 8a) when Congress was in the process of amending what was then § 14b of the Act, which precluded a discharge of all debts for a false statement. See Act of May 27, 1926, § 6, 44 Stat. 663. App. 10a. S.G. Opp. Br. 16. (See Section III below).15

Following the introduction of the phrase “respecting financial condition” in 1926, the circuit courts gener-ally interpreted this phrase broadly as meaning more than a formal financial statement. The Fourth Circuit appears to be the first circuit court to apply it. In Lockhart v. Edel, the Fourth Circuit held that statements made by a brokerage firm that it would purchase stock for the account of its customers upon receipt of a partial payment was false because the brokerage company was insolvent and unable to perform. Lockhart v. Edel, 23 F.2d 912 (4th Cir. 1928). “The representation was that the firm was in a position financially to fulfill the promise held out to its customers . . . when in fact they could not have possibly done so . . .” and hence was a statement with respect to financial condition. Id. at 913.

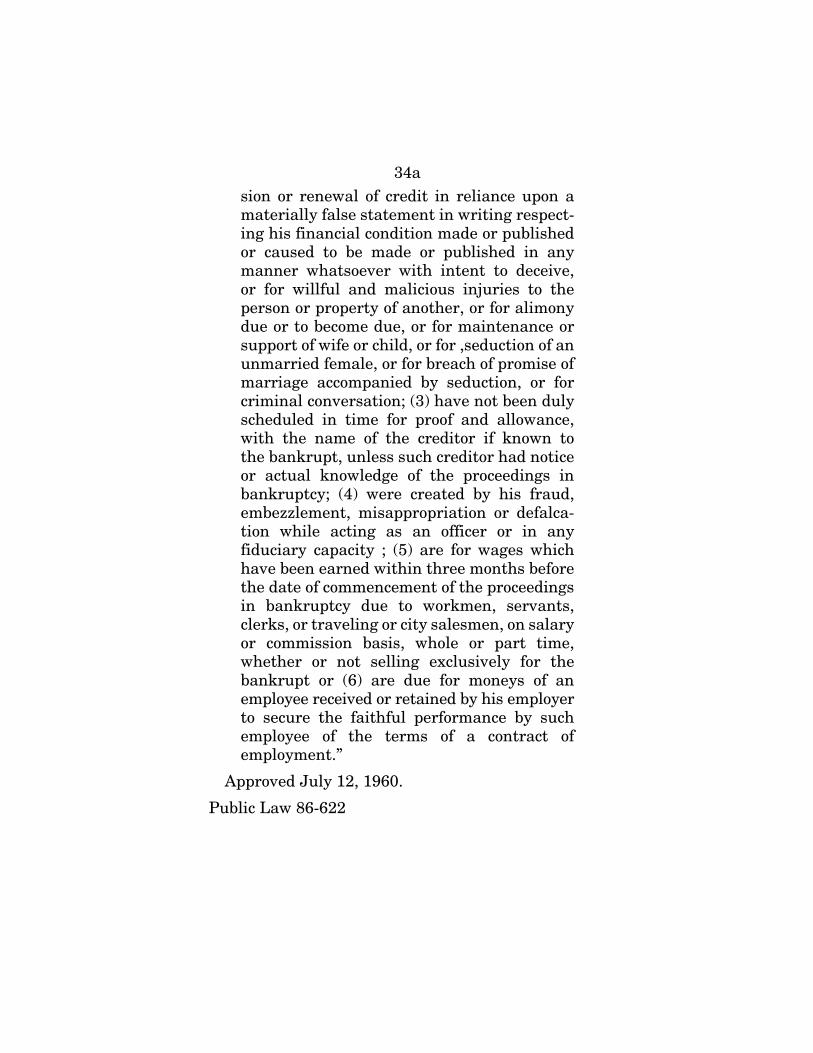

15 The Act was amended in 1960 so that a false statement

respecting financial condition would only bar a discharge of a nonbusiness debtor of the particular debt in question. Act of July 12, 1960, Pub. L. No. 86-621, § 2(a), 74 Stat. 409. App. 33a-34a.

20 In 1945, the issue was given more extensive discus-

sion by the Sixth Circuit. See Albinak v. Kuhn, 149 F.2d 108, 110 (6th Cir. 1945). In Albinak, the argument was first made that the term “financial statement” was a “term of art” that only applied to a “complete statement of assets and liabilities by which the precise financial worth of the person making the statement can be determined.” Id. at 110.16 The Sixth Circuit rejected this narrow view, stating, “No [case] has been found by careful examination, which confines a statement respecting one’s financial condition as limited to a detailed statement of assets and liabilities.” Id.

In 1950, the Ninth Circuit agreed. Mau v. Sampsell, 185 F.2d 400, 400 (9th Cir. 1950) (finding that debtor’s letter “stating that an existing escrow would soon net him cash in excess of the debt” constituted a report of financial status under 11 U.S.C. § 32(c)). In 1967, the Eighth Circuit joined with the Fourth, Sixth, and Ninth Circuits on the meaning of the phrase “respect-ing financial condition.” See Shainman v. Shear’s of Affton, Inc., 387 F.2d 33, 38 (8th Cir. 1967), stating, “A written statement purporting to set forth the true value of a major asset, its inventory, is a statement respecting the financial condition of that corporation.” The court rejected the very argument made in this case by Petitioner: “There is nothing in the language or legislative history of this section of the Act to indicate that it was intended to apply only to complete financial statements in the accounting sense.” Id.

Finally, shortly before the adoption of the Code in 1978, the Ninth Circuit again addressed the issue.

16 The court was then construing Section 14 of Chapter 3 of the

Bankruptcy Act, 11 U.S.C.A § 32.

21 Tenn v. First Hawaiian Bank, 549 F.2d 1356, 1357–58 (9th Cir. 1977) (per curiam). Here, the debtors informed the bank they owned certain real property based on a deed in their favor from their mother. Shortly after the loan was made, they reconveyed the property back to their mother. The Ninth Circuit affirmed the denial of a discharge, finding that “appellants’ recordation of deed . . . for the purpose of obtaining an extension of credit on the basis of [that] asset . . . was a false statement of financial condition.” Id. at 1358.

Petitioner tries to swat away Albinak and First Hawaiian Bank but offers no analysis. Pet. Br. 44. It points to a “mine” of cases contained in a footnote which “involved” a false financial statement. That “involvement” however was not the same as a doctrinal statement within these cases that only a formal financial statement constituted a “statement respecting financial condition” under § 14 of the Act. Pet. Br. 43, n.5. Indeed, none of the cases cited in this “mine” stands for the view that the phrase “respecting financial condition” is to be narrowly interpreted as only a formal financial statement as a matter of law.

Petitioner next argues that because the purpose of the pre-1978 parallel language was to deny discharge, the 1978 reversal to making “statements respecting . . . financial condition” an exception to denying discharge should change the meaning of the phrase. Pet. Br. 45. However, when the 1978 Code was adopted, the view of the circuit courts was that “statements respecting . . . financial condition” did not mean merely a formal financial statement. Congress expressly stated that it did not intend to change the law in this provision. H. Rep. No. 95-595 (1977) App. 50a-51a. Thus, “there is no reason to suppose that Congress

22 disagreed with [pre-1978] interpretation[] when it enacted [the 1978 Code]”. Jerman v. Carlisle, McNellie, Rini, Kramer & Ulrich LPA, 559 U.S. 573, 590 (2010). Prior construction of identical language should continue “in the absence of plain implication to the contrary.” Key v. Doyle, 434 U.S. 59, 76 n.5 (1977) (quoting Heald v. District of Columbia, 254 U.S. 20 (1920)).

Following the adoption of the 1978 Code, courts continued to construe similar language in new § 523(a)(2)(B) to include written statements regarding even a single asset.17 Until recently, the majority rule was consistent with the result reached below by the Eleventh Circuit. See, e.g., In re Powell, 423 B.R. at 210 (construing § 523(a)(2)(B) and holding that the majority view is the broad view).18 Others cases were in accord. See, e.g., In re Cook, 46 B.R. 545, 548–49 (Bankr. E.D. Va. 1985) (list of property owned by debtor to secure a loan is a statement of a debtor’s financial condition); In re Prestridge, 45 B.R. 681, 682 (Bankr. W.D. Tenn. 1985) (in construing § 523(a)(2)(B), the bankruptcy court acknowledged that a statement that one’s assets were not encumbered qualifies as a statement respecting financial condition; “Congress did not speak in terms of financial statements. Instead it referred to a much broader class of statements.”) (citations omitted); In re Roberts, 54 B.R.

17 Cases did not always distinguish between § 523(a)(2)(A) and

§ 523(a)(2)(B). 18 “[T]he emerging majority of cases[ ] adopt a more liberal

view. Those courts have defined the phrase to encompass a much broader class of statements, even those which relate to a single asset or liability.” In re Powell, 423 B.R. 201, 210–11 (Bankr. N.D. Tex. 2010).

23 765, 769–71 (Bankr. D.N.D. 1985) (statement describ-ing collateral pledged to bank is one concerning the debtor’s financial condition).

Thus, while some more recent decisions have dis-agreed with the result reached by the Eleventh Circuit, the meaning of the phrase “respecting finan-cial condition” was well settled by the circuit courts at the time of the adoption of the 1978 Code. Congress has given no indication that it intended to vary from this large body of case law.

C. The meaning of “financial condition” cannot be determined by reliance on the definition of “insolvency” in Code § 101. The definition of equitable insol-vency provides a better tool for interpreting “financial condition.”

Petitioner contends that the meaning of “financial condition” can be found by looking to the Code’s defini-tion of “insolvent,” found in § 101(32). Cert. Pet. 19. Pet. Br. 23. Pet. Add. 12. Section 101(32) defines insolvency as a “financial condition such that” one’s debts are greater than one’s assets. From this they draw the untenable conclusion that since insolvency is one aspect of one’s financial condition, Congress some-how meant to define “financial condition” exclusively as a statement containing all assets and liabilities.

The phrase “such that” by itself indicates that hav-ing liabilities greater than assets is but one example of a financial condition. See Taltech Ltd. v. Esquel Enterprises Ltd., 410 F. Supp. 2d 977, 1003 (W.D. Wash. 2006) (defining “such that” as inclusive, not restrictive; the prior term “creates or results in” the subsequent term). There is nothing to suggest balance sheet insolvency is the Code’s exclusive notion of a

24 “financial condition.” Indeed, not until 2005 did any court ever suggest such an odd linkage, despite the phrase having been part of bankruptcy law since at least 1898; even then the Tenth Circuit said the relationship between the two Code sections was only “tangential.” In re Joelson, 427 F.3d at 705.

However, if this Court determines that the defini-tion of “insolvency” bears on this issue at all, then a far better tool is to employ the other widely-used definition in the Code, namely, equitable insolvency. Equitable insolvency has a long settled meaning of referring to a debtor’s inability to pay debts as they mature. See Moody v. Sec. Pac. Bus. Credit, Inc., 971 F.2d 1056, 1064 (3d Cir. 1992). This concept is incorporated into Code § 548(a)(1)(B)(ii)(III) as part of the trustee’s avoidance powers. For example, a trustee may “avoid” a transfer under Chapter 5 of the Code (e.g., for a fraudulent conveyance) if at the time of the transfer the debtor intended to incur debts that were beyond its ability to pay. This has traditionally been labelled as “equitable insolvency.”

“Insolvency” is a multivalent term as used in bank-ruptcy court. See In re Dolata, 306 B.R. 97, 133 (Bankr. W.D. Pa. 2004) (finding that § 548(a)(1)(B)(ii)(III) was satisfied because “the debtors either intended to incur or believed that they would incur debts that . . . would be beyond their ability to satisfy as such debts matured”); In re Kanour, No. 09–07030JAD, 2010 WL 8354696, at *4 n.6 (Bankr. W.D. Pa. July 1, 2010) (“Section 548(a)(1)(B)(ii) also includes relief . . . if the debtor was rendered “insolvent” in an “equitable” sense. Section 548(a)(1)(B)(ii)(III) states that a debtor may be insolvent . . . if a debtor ‘intended to incur, or believed that the debtor would incur, debts that would be beyond the debtor’s ability to pay as such debts

25 matured’ . . .”). Cf. In re C.F. Foods, L.P., 280 B.R. 103, 117 n.30 (Bankr. E.D. Penn. 2002) (showing how the Bankruptcy Code provides “independent bases for avoiding constructively fraudulent transfers without proving balance sheet insolvency”).

The notion of “insolvency” is not limited to a balance sheet test but may reflect any aspect of financial condition that would give rise to an inability to pay one’s debts. If “insolvency” is to be used as a guide for understanding the phrase “financial condition,” then it is better understood to include any statement that bears on the debtor’s ability to pay or perform the underlying obligation. This could include a statement about a single asset or a combination of assets. This is precisely the argument offered by the Solicitor General, stating that an affirmative representation by a debtor qualifies as a “statement respecting the debtor’s . . . financial condition” where it “relates to a debtor’s financial circumstances and is offered by the debtor as evidence of his ability to pay.” S.G. Opp. Br. 14. We agree.

III. The legislative history demonstrates that Congress has been expanding protection against loss of the discharge and that § 523(a)(2)(A) was intended to have a broad meaning.

The plain meaning of “respecting” and the settled case law that preceded the enactment of the 1978 Code provide this Court with a sufficient basis to affirm the Eleventh Circuit’s ruling. Petitioner, however, urges a different result based on its reading of the legislative history. Pet. Br. 36 et seq. Petitioner focuses on the 1960 amendments to the Bankruptcy Act. It argues that Congress added the “financial condition” excep-tion in 1960, and that it did so only in response to the

26 problem of consumer credit companies attempting to shield their claims from discharge by encouraging debtors to make false financial statements. Cert. Pet. 2. From this, it argues that Congress intended to “tweak” the “general policy” by excepting from non-discharge only a misrepresentation made in a formal financial statement. Id. Hence, the “narrow” rule Petitioner urges here.

Neither argument is correct. The key language that matters in this case (“respecting” and “financial condi-tion”) emerged well before 1960 and was not limited to financial statements that listed all assets and liabilities. The introduction of the phrase “financial condition” in 1898 was, from the outset, given a broad meaning, and not tethered only to formal financial statements. See also, Section II, above.

Nor was Congress merely “tweaking” the Act or the Code when it adopted the various amendments. Congress was responding to specific findings of credi-tor abuse in attempting to block discharges, as well as overly harsh interpretations of the discharge provi-sion. Statements in the legislative history spanning from 1910 to 1978 reflect specific Congressional con-cern that the discharge provisions not be too “harsh,” that they not make “careless” and “general state-ments” the basis for blocking a discharge. Congress saw the need to protect debtors from documented creditor abuse of the discharge provisions by intimi-dating debtors into unwarranted settlements. By 1977 the Bankruptcy Commission would recommend that Congress delete the provision entirely. See App. 47a.

27 A. “Financial condition” has been broadly

defined since the passage of the Bankruptcy Act in 1898.

The Bankruptcy Act of 189819 barred a discharge completely when the debtor acted with fraudulent intent to conceal his or her “true financial condition and in contemplation of bankruptcy, destroyed, concealed or failed to keep books of account or records from which his true condition might be ascertained.” Act of 1898, § 14b(2), 30 Stat. 544, 550. App. 1a. This appears to be the first use of the phrase “financial condition” in American bankruptcy law.

The reference to “true financial condition” and then to “true condition” suggests here, as elsewhere, that the real concern was with the substance of the non-disclosure, and not whether it was embodied in any particular kind of document or whether it pertained to all assets and liabilities. The term “condition” is broadly generic. Non-disclosure of a single asset could well obscure a debtor’s “condition.” The phrase was not limited to a formal financial statement when first used, let alone later. Nor was the phrase tied to “solvency” as Petitioner later argues. Solvency may be a component, or aspect, of a “condition,” but it is hardly the only such component.

The Act was amended in 1903 when Congress added language to § 14b that barred a discharge when the debtor “obtained property on credit . . . upon a materially false statement in writing made . . . for the purpose of obtaining such property . . . ” Act of Feb. 5, 1903, ch. 487, 32 Stat. 797 (1903). App. 2a. Thus, as of 1903, the bar to discharge was not provoked by only false “financial statements” but instead, by any false

19 App. 1a.

28 statement in writing that was “material.” There is no indication that this section only referred to a formal financial statement; then and now, the concern was with the materiality of the non-disclosure.

As early as 1910, however, Congress became aware of overly harsh interpretations of § 14b and deter-mined that debtors needed greater protection from loss of discharge. This legislative history is described by the Fourth Circuit in J.W. Ould Co. v. Davis, 246 F. 228, 231 (1917). That case involved a creditor who sought to block a discharge of a merchant who had provided a false inventory to an independent credit company, which later gave the report to a creditor of the merchant. The court refused to deny the discharge. The Fourth Circuit noted the comments by the Senate Judiciary Committee, in responding to a bill passed by the House in 1910, stating as follows:

Any tendency to make the bankrupt act unduly harsh is to be avoided. It is a sufficient ground of opposition to discharge that the bankrupt has obtained property from a creditor by a materially false statement in writing where that statement was specifically asked for by the creditor or by the creditor's representative. General statements to mer-cantile agencies, not specifically asked for by prospective creditors, ought not to be ground of opposition to discharge; it makes the provision too harsh, in the estimation of your committee. Merchants are likely to make careless general statements where they would be very careful were they making

29 statements to creditors from whom they were at the time asking credit.

Id.20

Ould was not concerned with the form of the statement, but with issues of materiality and reliance. The larger question was whether a discharge could be lost through more typical, “careless” comments made by merchants. What the case recognized was that Congress and the courts did not want to make a debtor’s “careless general statements” be grounds to bar a discharge. It seems unlikely that “careless general statements” were meant to denote something said only in a formal financial statement. Instead, the loss of the discharge should occur only upon a finding of actual reliance and materiality of the statement. This same logic pertains today.

In 1926, the word “respecting” first appears in connection with the discharge exception in a House Conference Report concerning amending § 14b of the Act. H. Rep. No. 69-1257, at 3 (1926) (Conf. Rep.). App. 8a. Section 14b of the Act was then amended to reflect these comments.21 The 1926 amendment changed § 14b to read that a debtor may not receive a discharge of any debt if the debtor has “obtained money or property on credit, or obtained an extension or renewal of credit, by making or publishing, or causing to be made or published, in any manner whatsoever, a materially false statement in writing respecting his financial condition”. App. 10a (emphasis added.)

20 The Court was evidently referring to S. Rpt. No. 61-691

(1910) App. 4a. See similar discussion in H. Rpt. No. 69-1257 (1926). App. 7a.

21 Act of May 27, 1926, Pub. L. 69-301, 44 Stat. 662. App.10a.

30 Petitioner argues the 1926 amendment was added

to close the so-called “loophole” in Ould, and thus was intended only to protect creditors against the dis-charge of a debt where the creditor relied on a false financial statement prepared by a debtor and given to a credit agency. Pet. Br. 8–9. Petitioner thus ignores that while Congress observed the specific problem with credit reporting agencies, its broader concern was with the general problem of creditor abuse by assert-ing fraud based on careless or general statements, as Ould makes clear. One need only look to later House Reports to see that this concern lingered over the next few decades. See H. Rep. No. 86-1111 (1959). App. 15a.

Nothing in the text of the 1926 amendment supports a reading that Congress was now only concerned with formal financial statements. What Congress actually wrote reflects a concern for materially false written statements of any kind and in any manner. The concern was broad and was not limited to formal financial statements. Indeed, Petitioner concedes that this amendment was drafted to be “as broad as [its authors] could do it.” Pet. Br. 9. A materially false statement could be in any kind of document, including but not limited to a full financial statement. This same language remained equally broad once it became the exception to the exception.

B. In 1960 and 1978, Congress added greater debtor protection from loss of the discharge in view of creditor abuse of the discharge provisions.

In 1960 and again in 1978, Congress continued its movement toward protecting the debtor against loss of the discharge. This was largely the result of findings regarding institutional creditor abuse of the discharge provisions. Most broadly, Congress effectively rebalanced

31 its concerns about the “honest debtor” against the well-documented intimidation tactics of the consumer creditor institutions and its concern that “careless” comments become the basis to block a discharge.

By 1959 and 1960, both houses of Congress noted that the discharge provisions were being abused by institutional creditors who sought to intimidate debtors by threatening loss of discharge due to allegedly false statements. See, e.g., S. Rep. No. 86-1688 (1960) App. 22a and H. Rep. No. 86-1111 (1959) App. 15a. Specifically, Congress observed that the consumer credit industry was abusing the discharge provisions by inducing debtors to sign incomplete and hence “fraudulent” financial statements in order to insulate themselves from having their debt discharged. See Field, 516 U.S. at 74–77. “Unscrupulous” lenders “armed with false financial statement[s]” could thus threaten an unwary debtor’s entire discharge unless the debtor agreed to fully pay the lenders’ claims after discharge. S. Rep. No. 86-1688 (1960). App. 23a.

In view of this risk of intimidation by threats of discharge litigation, Congress proposed that the Bankruptcy Act be amended so that only business debtors were subject to the complete bar to discharge due to false statements. S. Rep. No. 86-1688 (1960). App. 22a. “[T]he Committee believes that it is desirable to eliminate the false financial statement as a ground for the complete denial of a discharge insofar as the individual noncommercial bankrupt is con-cerned.” Id. App. 24a. “It is also a penalty which experience has shown is subject to abuse.” Id. App. 23a. Accordingly, the 1960 amendments transferred the language concerning false statements by individuals from § 14 (where it barred any discharge) to § 17a(2) where it now barred only the debt incurred

32 as a result of the false statement. Act of July 12, 1960, Pub. L. 86-621, 74 Stat. 408-409. App. 33a-34a. (See also, Field, 516 U.S. at 65–66, stating that § 17a(2) was the precursor to § 523(a)(2)(A)).

The second key turning point occurred in 1978 when the Bankruptcy Code replaced the Bankruptcy Act. Congress expressly noted its goal of modernizing bankruptcy law and addressing the “second major problem . . . [of] the inadequacy of relief that the Bankruptcy Act provides for consumer debtors.” Id. App 41a. As Professor Ronald Mann noted, one of the central goals of the Bankruptcy Reform Act of 1978 was to provide a “broader discharge for debtors in Chapter 7.” Ronald J. Mann, Bankruptcy and the U.S. Supreme Court 28 (2017).

Congress remained concerned over the abuse of the discharge provision concerning false statements and that an exception to discharge could be sought even where the debtor had no intent to deceive or where the “merits of the case are weak.” Id. App. 47a-48a. Significantly, the House Report described its concern with a “false statement in writing concerning the debtor’s financial condition . . . . ” H. Rep. 95-595. App. 44a. This comment and the use of “concerning,” much like “respecting,” shows that Congress was looking more broadly and well beyond merely formal financial statements.

During the drafting process, Congress created the Commission on the Bankruptcy Laws of the United States to study and recommend changes to the bank-ruptcy laws (the “Bankruptcy Commission”). H. Rep. 95-595 (1977). App. 36a. The Bankruptcy Commission was sufficiently concerned about creditor abuse of the exception to the discharge that it “recommended that the false financial statement exception to discharge be

33 eliminated for consumer debts.” H. Rep. 95-595. App. 47a. Rather than delete the provision, Congress adopted a compromise, but it is inconceivable that in view of the consideration to delete this provision, the upshot was a bill which made the loss of discharge by creditor aggressive conduct more likely rather than less likely.

The legislative history of § 523(a)(2) and its prede-cessors fully reflect that Congress has consistently moved toward greater protection of the discharge. Petitioner’s brief suggests a narrative of Congress moving in the opposite direction and making discharge less available. Yet, Petitioner does not dispute that the legislative history contains a detailed discussion of Congress’ concern over creditor abuse of the discharge provisions. Congress’ response to this abuse was to provide broader protection against loss of the dis-charge, not to re-define the established meaning of “financial condition.” This concern over creditor abuse hardly squares with Petitioner’s conclusion that Congress therefore must have meant to give the very same institutional creditors greater leverage and intimidation opportunities by now making oral statements on “financial condition” the easy prey for a discharge challenge.

34 CONCLUSION

For the foregoing reasons, the decision of the Eleventh Circuit should be affirmed.

Respectfully submitted,

DAVID R. KUNEY Counsel of Record

WHITEFORD, TAYLOR & PRESTON, LLP

1800 M. Street. N.W. Suite 450 North Washington, D.C. 20036 (202) 659-6807 [email protected]

Counsel for Amici Curiae

April 2, 2018

APPENDIX

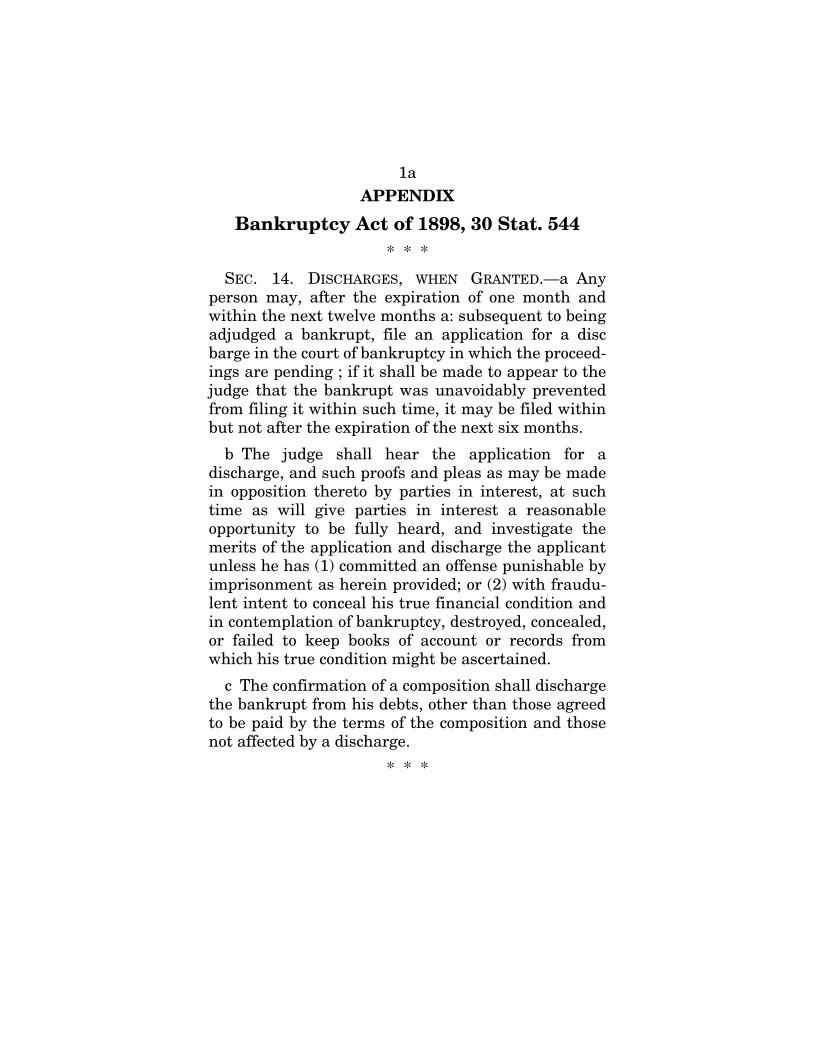

1a

APPENDIX

Bankruptcy Act of 1898, 30 Stat. 544 * * *

SEC. 14. DISCHARGES, WHEN GRANTED.—a Any person may, after the expiration of one month and within the next twelve months a: subsequent to being adjudged a bankrupt, file an application for a disc barge in the court of bankruptcy in which the proceed-ings are pending ; if it shall be made to appear to the judge that the bankrupt was unavoidably prevented from filing it within such time, it may be filed within but not after the expiration of the next six months.

b The judge shall hear the application for a discharge, and such proofs and pleas as may be made in opposition thereto by parties in interest, at such time as will give parties in interest a reasonable opportunity to be fully heard, and investigate the merits of the application and discharge the applicant unless he has (1) committed an offense punishable by imprisonment as herein provided; or (2) with fraudu-lent intent to conceal his true financial condition and in contemplation of bankruptcy, destroyed, concealed, or failed to keep books of account or records from which his true condition might be ascertained.

c The confirmation of a composition shall discharge the bankrupt from his debts, other than those agreed to be paid by the terms of the composition and those not affected by a discharge.

* * *

2a

Act of February 5, 1903, 32 Stat. 797 Approved, February 5, 1903.

CHAP. 487.—An Act To amend an Act entitled “An Act to establish a uniform system of bankruptcy throughout the United States,” approved July first, eighteen – hundred and ninety-eight.

* * *

SEC. 4. That subdivision b of section fourteen of said Act be, and the same is hereby, amended so as to read as follows:

“b The judge shall hear the application for a discharge, and such proofs and pleas as may be made in opposition thereto by parties in interest, at such time as will give parties in interest a reasonable opportunity to he fully heard, and investigate the merits of the application and discharge the applicant unless he has (1) committed an offense punishable by imprisonment as herein provided; or (2) with intent to conceal his financial condition, destroyed, concealed, or failed to keep books of account or records from which such condition might be ascertained; or (3) obtained property on credit from any person upon a materially false statement in writing made to such person for the purpose of obtaining such property on credit; or (4) at any time sub sequent to the first day of the four months immediately preceding the filing of the petition transferred, removed, destroyed, or concealed, or permitted to be removed, destroyed, or concealed any of his property with intent to hinder, delay, or defraud his creditors; or (5) in voluntary proceedings been granted a discharge in bankruptcy within six years; or (8) in the course of the proceedings in bankruptcy ref used to obey any lawful order of or

3a

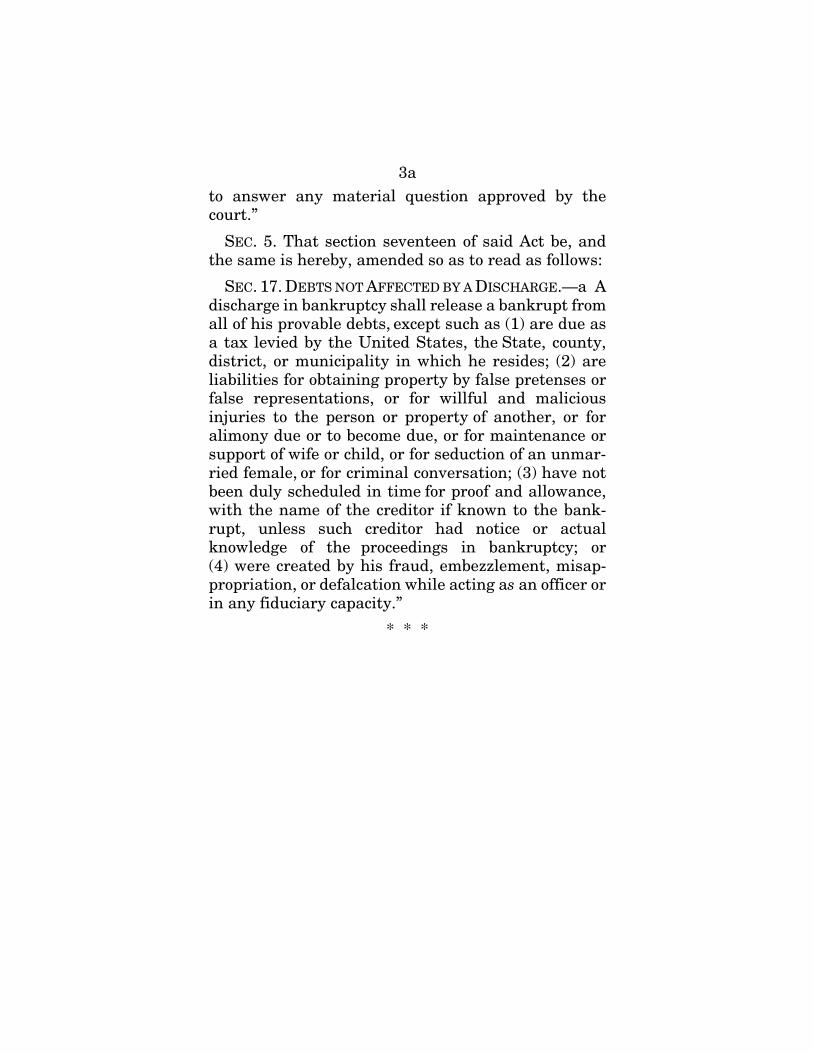

to answer any material question approved by the court.”

SEC. 5. That section seventeen of said Act be, and the same is hereby, amended so as to read as follows:

SEC. 17. DEBTS NOT AFFECTED BY A DISCHARGE.—a A discharge in bankruptcy shall release a bankrupt from all of his provable debts, except such as (1) are due as a tax levied by the United States, the State, county, district, or municipality in which he resides; (2) are liabilities for obtaining property by false pretenses or false representations, or for willful and malicious injuries to the person or property of another, or for alimony due or to become due, or for maintenance or support of wife or child, or for seduction of an unmar-ried female, or for criminal conversation; (3) have not been duly scheduled in time for proof and allowance, with the name of the creditor if known to the bank-rupt, unless such creditor had notice or actual knowledge of the proceedings in bankruptcy; or (4) were created by his fraud, embezzlement, misap-propriation, or defalcation while acting as an officer or in any fiduciary capacity.”

* * *

4a SENATE

61ST CONGRESS REPORT 2d Session No. 691

AMENDMENT OF THE BANKRUPTCY ACT

————

MAY 16, 1910.—Ordered to be printed.

————

Mr. BACON, from the Committee on the Judiciary, submitted the following

REPORT

[To accompany H.R. 20575.]

The Committee on the Judiciary, to whom was referred the bill (H.R. 20575) entitled “An act to amend an act entitled ‘An act to establish a uniform system of bankruptcy throughout the United States,’ approved July 1, 1898, as amended,” etc., have had the same under consideration, and report it back with amendments.

The report of the Judiciary Committee of the House of Representatives on said bill is hereby concurred in with the additions and reservations hereinafter indi-cated and explained in connection with the different sections treated. That report states:

The experience of the seven years elapsing since the amendment of February 5, 1903, in the administration of the bankruptcy law has developed certain defects which seem to the committee to require additional legislation to reconcile conflicting decisions of the courts, to make the law more just to debtor and credi-tor, and also to correct certain faults in its administra-tive features, which, despite the obvious intention of

5a the framers of the present law as well as of those who framed the amendment of 1903, have crept in through loopholes that have developed. Hence the introduction and approval of the bill which this report accompanies. In explanation of this bill the following statement is submitted:

* * * Section 6. The House bill seeks to make three

changes in subdivision–b of section 14 of the present law, relative to opposition to discharge. First, it pro-vides that trustees shall be competent “parties in interest” to object to a discharge; second, that they can so object only when authorized at a meeting of creditors; and, third, that a materially false mercantile statement, if made to the trade and relied on by the creditor, shall be an available objection to the debtor’s discharge.

Your committee concur in the first two of these changes, but do not concur in the last.

The first of these changes, making the trustee a competent party to oppose a bankrupt’s discharge, is a desirable change, as thereby the expense of the proceedings in opposition to discharge will ho spread over all of the creditors, and not be borne by a single creditor who may file objections. Moreover, it lessens the danger of improper oppositions to discharge by single creditors for the purpose of forcing settlements.

The second change, namely, that, the trustee can only oppose discharge when authorized to do so at a meeting of creditors, is also desirable, affording a proper check upon improvident and improper opposi-tion to discharge. In view of the fact that “entry of appearance” in opposition to discharge must be made at the return tune of the ten days’ notice provided

6a by section 58, but that the meeting of creditors for authorizing such opposition also must be upon ten days’ notice—thus preventing creditors meetings being held before the expiration of the time for entering appearance in opposition—it has been found necessary to amend section 58 by providing for thirty days’ notice of the filing of discharge applications in the place of the ten days’ notice at present prescribed, in this way sufficient time being given for the creditors to hold their meeting.

The third change made by the House bill, that which in effect would make the obtaining of property on false written statements to mercantile agencies ground of opposition to discharge, without the creditor whose property has thus been obtained first asking such mercantile agencies to procure him the written state-ment, is not concurred in by your committee. Any tendency to make the bankrupt act unduly harsh is to be avoided. It is a sufficient ground of opposition to discharge that the bankrupt has obtained property from a creditor by a materially false statement in writing where that statement was specifically asked for by the creditor or by the creditor’s representative. General statements to mercantile agencies, not spe-cifically asked for by prospective creditors ought not to be ground of opposition to discharge; it makes the provision too harsh, in the estimation of your our committee. Merchants are likely to make careless general statements where they would be very careful were they making statements to creditors from whom they were at the time asking credit.

Your committee propose a substitute for the House amendment of this ground of opposition to discharge, which is thought to go as far as is proper.

* * *

7a

HOUSE OF REPRESENTATIVES

69TH CONGRESS REPORT 1st Session No. 1257

————

ESTABLISH A UNIFORM SYSTEM OF BANKRUPTCY

————

MAY 19, 1926.—Ordered to be printed

————

Mr. CHRISTOPHERSON, from the committee of conference, submitted the following

CONFERENCE REPORT (To accompany S. 1039]

The committee of conference on the disagreeing votes of the two Houses on the amendment of the House to the bill (S. 1039) entitled, “To amend an act entitled, ‘An act to establish a uniform system of bank-ruptcy throughout the United States’, approved July 1, 1898, and acts amendatory thereof and supplemen-tary thereto, “having met, after full and free confer-ence, have agreed to recommend and do recommend to their respective Houses as follows:

That the Senate recede from its disagreement to the amendment of the House and agree to the same with the following amendments:

In lieu of the matter proposed to be inserted by said amendment insert the following:

* * *

Sec. 6. That section 14 (a) and (b) of said act, as 80 amended, be, and the same hereby is, amended to read as follows:

8a