summary jpx wp_en_no9

TRANSCRIPT

1 1 1 1

Impacts of

Speedup of Market System

on Price Formations

using Artificial Market Simulations

SPARX Asset Management Co., Ltd.

Japan Securities Clearing Corporation

Osaka Exchange, Inc.

The University of Tokyo

CREST, JST

Takanobu Mizuta

Yoshito Noritake

Satoshi Hayakawa

Kiyoshi Izumi

JPX Working Paper 【Summary】

Vol. 9, 31th March 2015

2

This material was compiled based on the results of research and studies by directors, officers,

and/or employees of Japan Exchange Group, Inc., its subsidiaries, and affiliates (hereafter

collectively “the JPX group”) with the intention of seeking comments from a wide range of

persons from academia, research institutions, and market users. The views and opinions in this

material are the writer's own and do not constitute the official view of the JPX group. This

material was prepared solely for the purpose of providing information, and was not intended to

solicit investment or recommend specific issues or securities companies. The JPX group shall

not be responsible or liable for any damages or losses arising from use of this material. This

English translation is intended for reference purposes only. In cases where any differences

occur between the English version and its Japanese original, the Japanese version shall prevail.

This translation is subject to change without notice. The JPX group shall accept no responsibility

or liability for damages or losses caused by any error, inaccuracy, misunderstanding, or changes

with regard to this translation.

3 3 3 3

(1) Introduction

(2) Artificial Market Model

(3) Simulation Results

(4) Empirical Study to Compare

(5) Summary & Future Works

4 4 4 4

(1) Introduction

(2) Artificial Market Model

(3) Simulation Results

(4) Empirical Study to Compare

(5) Summary & Future Works

5 5 5 5

Speedup of Exchange System

How much speedup is best? How much speedup is best?

Increasing liquidity by increasing providing liquidity traders

Increasing cost for systems of Markets and investors

Because of competition between Markets and big investors demands

5

conflicting GOOD

BAD

6 6 6 6

Does Market speed purely effect market efficiency?

Artificial Market Simulation

(Multi-Agent Simulation) 6

What are Mechanisms?

How much enough speedup is Market system?

-> So many factors cause price formation :

An empirical study cannot isolate the pure contribution

-> So many factors cause price formation :

An empirical study cannot isolate the pure contribution

-> Analysis Micro Process: Impossible by empirical study -> Analysis Micro Process: Impossible by empirical study

-> No Market experienced more Speedup:

Impossible by empirical study

-> No Market experienced more Speedup:

Impossible by empirical study

Need Discussions

7 7 7 7

(1) Introduction

(2) Artificial Market Model

(3) Simulation Results

(4) Empirical Study to Compare

(5) Summary & Future Works

8 8 8 8

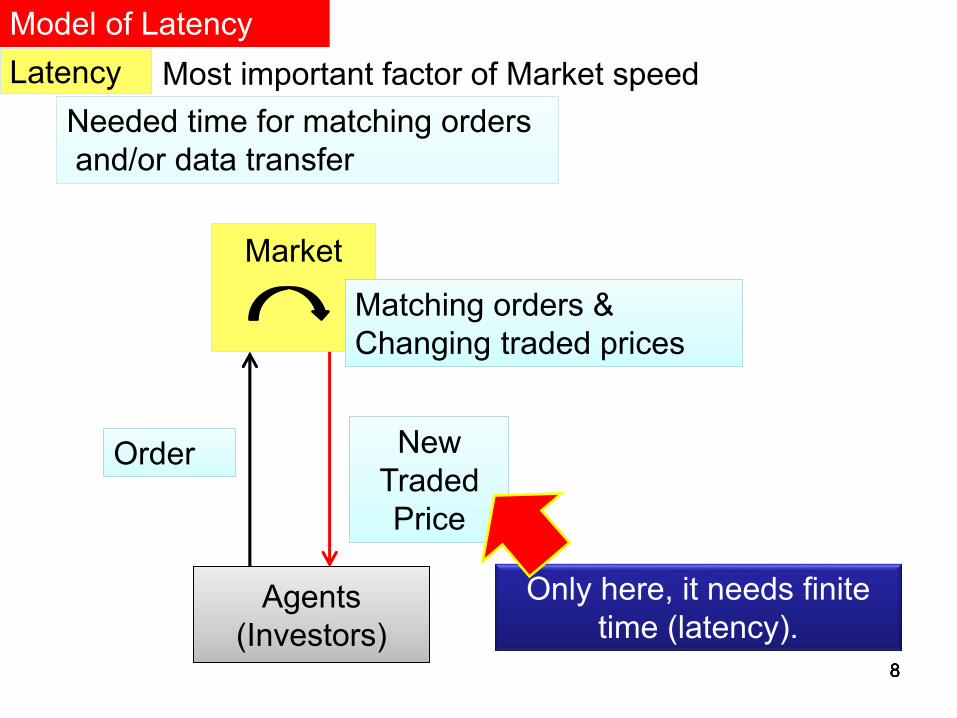

Model of Latency

Agents

(Investors)

Agents

(Investors)

Market

Market

Order Order New

Traded

Price

New

Traded

Price

Matching orders &

Changing traded prices

Matching orders &

Changing traded prices

Only here, it needs finite

time (latency).

Latency Latency

Needed time for matching orders

and/or data transfer

Needed time for matching orders

and/or data transfer

Most important factor of Market speed

Order & Price change

Order & Price change

True Price

Observed

Price

Latency

constant = δl

Order

interval

exponential

random

numbers

Avg. = δo

Difference

Most cases, agents know True Price

True and Observed prices are difference

9

δl / δo > 1 δl / δo > 1

δl / δo ≪ 1 δl / δo ≪ 1

10

* Continuous Double Auction: to implement realistic latency

* Simple Agent model: to avoid arbitrary result

Same Model as JPX Working Paper vol.2; Mizuta et. al. 2013

Agents (Investors) Model

t

jj

t

jhjt

f

j

i ji

t

je urwP

Pw

wr ,,2,1

,

, log1

Fundamental Technical noise

Expected Return ,i jw

Strategy

Weight

↑ Different

for each agent

heterogeneous 1000 agents

Replicate traditional Stylized Facts

and Replicate Micro Structures

Latency has Micro Structure Time Scale, MilliSeconds Latency has Micro Structure Time Scale, MilliSeconds

11 11 11 11

(1) Introduction

(2) Artificial Market Model

(3) Simulation Results

(4) Empirical Study to Compare

(5) Summary & Future Works

12 12 12 δl/δo>1: increasing Volatility, decreasing Kurtosis (flatter fat tail)

⇒ be inefficient?

δl/δo>1: increasing Volatility, decreasing Kurtosis (flatter fat tail)

⇒ be inefficient?

0

5

10

15

20

0.00%

0.01%

0.02%

0.03%

0.04%

0.05%

0.06%

0.0

01

0.0

02

0.0

05

0.0

10

.02

0.0

50

.1

0.2

0.5 1 2 5

10

Ku

rto

sis

Vo

lati

lity

δl / δo

Volatility & Kurtosis(δr/δo=1)

Volatility

Kurtosis

δl/δo: latency / order interval

δr/δo: return calculation period / order interval

δl/δo: latency / order interval

δr/δo: return calculation period / order interval

13 13 13

0

0.5

1

1.5

2

2.5

0.00%

0.02%

0.04%

0.06%

0.08%

0.10%

0.12%

0.0

01

0.0

02

0.0

05

0.0

1

0.0

2

0.0

5

0.1

0.2

0.5 1 2 5

10

Ku

rto

sis

Vo

lati

lity

δl / δo

Volatility & Kurtosis(δr/δo=10)

Volatility

Kurtosis

δl/δo>1:Volatility is flat, Increasing Kurtosis (fatter fat tail)

⇒ be inefficient?

δl/δo>1:Volatility is flat, Increasing Kurtosis (fatter fat tail)

⇒ be inefficient?

We should use the way independent of return calculation period

14 14

We can measure Market Inefficiency Directly,

not estimation in simulation studies.

Market Inefficiency

If Market was perfect efficient, Market prices were exactly same as the fundamental price. This Market Inefficiency is defined actual difference between market and fundamental prices. -> We can not use this definition for an empirical study. Experimental study for human sometimes uses this definition.

Independent of return calculation period

Market Inefficiency =Average of Market Price − Fundamental Price

Fundamental Price

15 15 15

δl / δo > 1 : be Inefficient

0.27%

0.28%

0.29%

0.30%

0.31%

0.32%

0.0

01

0.0

02

0.0

05

0.0

1

0.0

2

0.0

5

0.1

0.2

0.5 1 2 5

10

Mar

ket

Inef

fici

ency

δl / δo

Market Inefficiency

Right side δl / δo = 0.5, Market becomes Inefficient Right side δl / δo = 0.5, Market becomes Inefficient

16 16 16

δl / δo > 1 : Wider Bid Ask Spread δl / δo > 1 : Wider Bid Ask Spread

0.135%

0.140%

0.145%

0.150%

0.0

01

0.0

02

0.0

05

0.0

1

0.0

2

0.0

5

0.1

0.2

0.5 1 2 5

10

Bid

Ask

Sp

read

δl / δo

Bid Ask Spread

17 17 17

δl / δo > 1 : Increasing Execution Rate δl / δo > 1 : Increasing Execution Rate

32.0%

32.2%

32.4%

32.6%

32.8%

0.0

01

0.0

02

0.0

05

0.0

1

0.0

2

0.0

5

0.1

0.2

0.5 1 2 5

10

Exec

uti

on

Rat

e

δl / δo

Execution Rate

18 18 18

Increasing Execution Rate especially

near the fundamental price

Increasing Execution Rate especially

near the fundamental price

29.0%

29.5%

30.0%

30.5%

31.0%

31.5%

32.0%

32.5%

33.0%

9,9

40

9,9

50

9,9

60

9,9

70

9,9

80

9,9

90

10

,00

0

10

,01

0

10

,02

0

10

,03

0

10

,04

0

10

,05

0

10

,06

0

Exe

cuti

on

Rat

e

True Price

Execution Rate for True Prices Fundamental Price = 10,000

δl / δo = 0.001

δl / δo = 10

19 19 19

Observed Price < True Price: More Buy Market Orders: Positive estimated returns Observed Price > True Price: More Sell Market Orders: Negative estimated returns Observed Price < True Price: More Buy Market Orders: Positive estimated returns Observed Price > True Price: More Sell Market Orders: Negative estimated returns

δl / δo

Execution Rate Avg.

Estimated Return of agents

Sum

Buy Market

Sell Limit

Orders

Sell Market

Buy Limit

Orders

10 Observed P. < True P. 32.5% 28.9% 3.5% 0.28%

Observed P. > True P. 32.5% 3.6% 28.9% -0.27%

0.001 --- 31.2% 15.6% 15.6% 0.00%

Unnecessary market following trades Unnecessary market following trades

But, agents cannot change Estimate price, quickly But, agents cannot change Estimate price, quickly

Observed Price > True Price Observed Price < True Price

Too High Estimated P.

⇒ Market Buy order

↑ If agents knew True P.

they did not order.

Too High Estimated P.

⇒ Market Buy order

↑ If agents knew True P.

they did not order.

Observed P.

True P.

Upward trend

Estimated P.

(near Fundamental Price)

Too Low Estimated P.

⇒ Market Sell order

↑ If agents knew True P.

they did not order.

Too Low Estimated P.

⇒ Market Sell order

↑ If agents knew True P.

they did not order.

Stop market trend Stop market trend

21 21 21 21

Stop market trend Stop market trend

Market becomes Inefficient

Expanding Bid Ask Spread Expanding Bid Ask Spread

21

Mechanism of Large Latency(δl/δo>1) making Market Inefficient

Increasing Execution Rate Increasing Execution Rate

Decreasing Limit orders near Market Price, relatively Decreasing Limit orders near Market Price, relatively

But, agents cannot change

Estimate price, quickly

But, agents cannot change

Estimate price, quickly

Unnecessary market

following trades

Unnecessary market

following trades Especially near

Fundamental Price

Especially near

Fundamental Price

Large Latency

22 22 22 22

(1) Introduction

(2) Artificial Market Model

(3) Simulation Results

(4) Empirical Study to Compare

(5) Summary & Future Works

23 23 23

1:Uno, 2012

2~6:In this study

1:Uno, 2012

2~6:In this study

No. Analysis Period arrowhead Order No.

Avg. for day Avg. names

Calculation Period (min)

Avg. δo (ms) = Period (ms) /

Order No.

Latency δl (ms)

δl / δo

1 December 2009 (one month) Before 2,833 270 5,718 3,000 0.525

2 2 August 2010 - 18 November 2011

After

14,621 355 1,457 4.5 0.003

3 21 November 2011 - 26 November 2014 28,974 385 797 4.5 0.006

4 27 October 2014 - 26 November 2014 66,044 385 350 4.5 0.013

5 31 October 2014 (one day) 87,109 385 265 4.5 0.017

6 4 November 2014 (one day) 114,027 385 203 4.5 0.022

Before arrowhead

It is Possible that Market is Chronically Inefficient

After arrowhead

Market is NOT Chronically Inefficient

by the Mechanism we showed

24 24 24

0.000

0.005

0.010

0.015

0.020

0.025

10

/27

10

/28

10

/29

10

/30

10

/31

11

/4

11

/5

11

/6

11

/7

11

/10

11

/11

11

/12

11

/13

11

/14

11

/17

11

/18

11

/19

11

/20

11

/21

11

/25

11

/26

δl /

δo

Month / Day

δl/δo for business day 27 October 2014~26 November 2014

Even though near 31 October 2014, Bank of Japan announced

“Expansion of the Quantitative and Qualitative Monetary Easing”,

Market is NOT Chronically Inefficient by the Mechanism we showed

Even though near 31 October 2014, Bank of Japan announced

“Expansion of the Quantitative and Qualitative Monetary Easing”,

Market is NOT Chronically Inefficient by the Mechanism we showed

25 25 25

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0.14

8:0

0

9:0

0

10

:00

11

:00

12

:00

13

:00

14

:00

15

:00

8:0

0

9:0

0

10

:00

11

:00

12

:00

13

:00

14

:00

15

:00

8:0

0

9:0

0

10

:00

11

:00

12

:00

13

:00

14

:00

15

:00

δl /

δo

δl/δo for 1 minute

31 October 2014~5 November 2014

31 October 4 November 5 November

31 October 2014 at 13:44 Japan time, Bank of Japan announced it.

For a few minutes after the announcement, orders are crowded.

We cannot deny market inefficiency for less than one minute.

Market is NOT Inefficient even for one minute Market is NOT Inefficient even for one minute

Future Works Future Works

26 26 26 26

(1) Introduction

(2) Artificial Market Model

(3) Simulation Results

(4) Empirical Study to Compare

(5) Summary & Future Works

27 27 27 27

Summary

* The ratio (δl/δo) is key parameter,

Latency(δl) per Order Interval (δo)

* Enough fast market system is required δl << δo.

* Stop market trend -> Large Latency

-> agents cannot change Estimate price, quickly

-> Unnecessary market following trades

-> Increasing Execution Rate -> Expanding Bid Ask

Spread

-> Market becomes Inefficient

* Before arrowhead:

It is Possible that Market is Chronically Inefficient

* After arrowhead:

Market is NOT Inefficient even for one minute

28 28 28 28

Future Works

* We should discuss the case of very crowded orders

for less than one minute, for example, at announced

great market impacting information.

-> needed simulation and empirical studies

<- Certainly, such very short time scale event

does not effect to general investors much.

<-> It may effect to High Frequency Trading very much.

* We should discuss it in more kinds of agents.

(For example: High Frequency Trading such as

Market Maker strategy, Arbitrage Strategy, and so on.)

29 29 29 29 29

Appendix

30 30

order

book

sell price buy

84 101

176 100

99 2

98 77

Definition of Market/Limit order In this study

A little difference from actual market

limit

market market limit

market market Exist matching order

Order executed immediately

Exist matching order

Order executed immediately

No matching order

Order not executed immediately

No matching order

Order not executed immediately

buy buy sell sell

Agents decide an order price,

if exist matching order, market order else limit order

Agents decide an order price,

if exist matching order, market order else limit order

All agents decide an order price