study on effects of tax systems on the retention of ... · pdf filemazars was successful in...

TRANSCRIPT

Netherlands Country Report

February 2008

1

CONTRACT SI2.ICNPROCE009493100

IMPLEMENTED BY FOR

DEMOLIN, BRULARD, BARTHELEMY COMMISSION EUROPEENNE - HOCHE - - DG ENTREPRISE AND INDUSTRY -

Study on Effects of Tax Systems on the Retention of Earnings and the Increase of Own Equity

Jean ALBERT Team Leader

- ANNEX 15 - -THE NETHERLANDS - - COUNTRY REPORT -

Submitted by Eric J.H. VERMEULEN Country Expert

February 15, 2008

Netherlands Country Report

February 2008

2

Mazars Paardekooper Hoffman N.V. Eric J.H. Vermeulen Rivium Promenade 200 2909 LM Capelle aan den IJssel The Netherlands Tel 00 31 10 277 1584 INTRODUCTION Mazars was successful in obtaining the European Commission project “Effects of Tax

Systems on the Retention of Earnings and the Increase of Own Equity”. The context of the

Project is SME health, competitiveness and growth. These are hindered by weak own

equity base of many companies in Europe and the difficult access to finance that SMEs

face.

In The Netherlands, the most common manner to run an enterprise is to run it by a

corporation, which run their business with their whole equity. When a corporation will

realise a profit, this company will have to pay 25,5% Corporate Income Tax. After that,

the company might wish to pay out dividend. In case the corporation will pay out

dividend, the business owner (most of the times one shareholder) will have to pay 25%

income tax (in 2007 22%). Distribution of earnings is not advantageous because it will thus

lead to double taxation. Retention of earnings does postpone individual Income tax duty.

Other examples to lower the tax burden in a year are depreciation of assets, making

reservations for provisions and use of valuation rules.

THE NETHERLANDS

Netherlands Country Report

February 2008

3

PART 1 GENERAL QUESTIONS

1. What are the main characteristics of the tax systems applicable on enterprises

and business owners in your Country (corporate income tax, income tax,

capital gains tax, other profit based taxes, capital based taxes, other taxes…)?

Most businesses in The Netherlands are run by corporations, which run their

business with their whole equity. When a corporation will realise a profit, this

company will have to pay 25,5% corporate Income tax. If the company pays out

dividend, the business owner will have to pay 25% income tax (in 2007 22% and 25%

above EUR 250.000) if he holds at least 5% of the shares of the corporation. There

is no specific capital gains tax, capital gains are taxed either with corporate

income tax, otherwise with individual income tax (maximum 52%). Capital gains

will be taxed with corporate income tax when the corporation will realise a capital

gain (as a result of the transfer of business assets). Capital gains will be taxed with

individual income tax when the business owner will transfer his shares in the

corporation (25%) or if he transfers business assets as sole trader or in case of a

partnership (maximum 52%).

Distribution of earnings is not advantageous. Retention of earnings does postpone

individual Income tax duty. Therefore it might be better to wait before to pay out

dividend.

1.1 Corporate Income

1.1.1 What are the general principles for the computation of taxable profits?

For purposes of the corporate income tax, the first thing what should be

determined is whether the company (a Small or Medium sized Enterprise)

has its principal place of business in The Netherlands1. In case the company

has its principal place of business in The Netherlands, the Dutch tax-

administration will tax the company for its results.

Netherlands Country Report

February 2008

4

After the determination that the company has its principal place of

business in The Netherlands, the second thing what should be determined is

which results are subject to corporate income tax. The “Corporate Income

Tax Act 1969” contains a provision in article 8, which refers to the Income

Tax Act 2001. The profit of a company, liable for corporate income tax,

should be determined in accordance with this “Income Tax Act 2001”. As a

result, the amount of the profit should be assessed in accordance with

sound commercial practice. Sound commercial practice is a vague term,

however, the following remarks can be made. The term leaves the

enterprise a high degree of freedom to choose its own system to calculate

its yearly profit. Sound commercial practice requires consistent accounting

principles. The term “sound commercial practice” has been introduced in

1893.2 However, a general definition which includes all descriptions of

“sound commercial practice” and which is applicable at any time, has not

been made.

1.1.2 What are the main differences between tax balance sheet and

commercial balance sheet?

For the determination of the taxable result, the starting point of the tax

balance sheet is the commercial balance sheet. Therefore, in general, the

tax balance sheet and the commercial balance sheet are equal. However,

there are some differences between the balance sheets.

First of all, the valuation of participations is different in the commercial

and the tax balance sheet. Participations are often valuated at the net-

asset value in the commercial balance sheet. In the tax balance sheet,

participations are valuated at cost price, unless the socalled “participation

exemption” is not applicable.

Another difference between the commercial and the tax balance sheet is

that there are provisions to which the company could contribute funds. In

the tax balance sheet, some of these provisions do not exist however or are

1 Article 2, paragraph 1, under a, Corporate Income Tax Act 1969 (=Vpb) 2 J.A. Fray – Weekblad voor Fiscaal Recht 1955/4270

Netherlands Country Report

February 2008

5

part of the fiscal equity. Examples of these provisions are “deferred tax

liabilities”, provisions for maintenance and vacancy.

A difference between the tax balance sheet and the commercial balance

sheet is also that business assets do not have to be valuated in the same

way in the different balance sheets. As a result, business assets can have

different values in the tax balance sheet and in the commercial balance

sheet. For example, the Supreme Court decided already in 1954 that a

business owner does not have to follow the commercial figures for tax

purposes regarding valuation of stocks.3

Finally, the period in which the company depreciates its business assets is

sometimes different according to commercial rules than it is according to

tax rules. This also results in different amounts of the business assets in the

commercial and tax balance sheet.

1.1.3 What are the most important adjustments for the computation of

taxable profits/taxable gains on the base of accounting profits?

The most important adjustments for the computation of taxable

profits/taxable gains on the base of accounting profits are the provisions

that are inserted in the commercial balance sheet and should be eliminated

in the tax balance sheet because they are not admitted for tax purposes.

Examples of such provisions are mentioned under 1.2.

Another important adjustment for the computation of taxable

profits/taxable gains is that the profit and loss account shows an amount of

the corporate income tax due. The profit and loss account for tax purposes

does not show such an amount.

3 HR 17 March 1954, nr 11.681, BNB 1954/128

Netherlands Country Report

February 2008

6

1.2 Income

1.2.1 What are the general principles of income taxation of business owners

on business income, wages, distributed earnings, interest on loans and

capital gain (sale of shares)?

Business owners are generally not taxable for the business income, unless

they are sole traders or the partnership in which they participate is

transparent for tax purposes. In that case the results of the company are

taxable results of the business owner and will be taxed with income tax4. If

the partnership is not transparent or a company drives the business, the

company itself will be taxed for its results5.

If the business owner is receiving a salary from the corporation, this salary

is subject to wage tax. The maximum rate of wage tax is 52%6. Salaries are

deductible from the profits of the corporation.

The treatment of distributed earnings can be described as follows. If the

individual business owner holds a substantial interest in a corporation (5%

or more of the shares)7, and the corporation distributes earnings to the

business owner, the earnings are taxable with 25%8 income tax (Box 2). It

does not matter whether this corporation has its principal place of business

in The Netherlands or in another country. If the interest is less than 5%, the

distributed earnings will not be taxable directly. However, at the end of

the year, the business owner will have to declare the amount of certain of

his assets (including shares, bank savings and the amount of the earnings)

minus certain debts (Box 3). The taxable result of Box 3 is equal to 4%9 of

the average of this amount and the amount of the assets minus debts at the

beginning of the year. The calculated (fictitious) result is taxable at a rate

4 Article 3.2 Income Tax Act 2001 5 Article 2, paragraph 1 under a Corporate Income Tax Act 1969 6 Article 20a Wage Tax Act 1964 7 Article 4.6 Income Tax Act 2001 8 Article 2.12 Income Tax Act 2001 9 Article 5.2 Income Tax Act 2001

Netherlands Country Report

February 2008

7

of 30%10, therefore effectively 1,2% (30% of 4%) of the net wealth has to be

paid annually.

In case the business owner will receive interest on a loan, granted to his

own corporation, the received interest will be taxed progressively in Box

1.11 The maximum rate that is applicable is 52%. The corporation can

deduct the interest paid as costs however.

Capital gains arising from the transfer of shares, held by the business owner

can be treated in two different ways, depending on the percentage of

shares held by the business owner. If the percentage of the shares held by

the business owner is at least 5%, the capital gain realised will be taxed at

25% (Box 2). If the interest held is less than 5%, the capital gain will not be

taxed directly but via the Box 3 system as mentioned before.

1.2.2 Is there a different tax treatment for income from different income

sources?

As of 1 January 2001, The Netherlands has a new tax system with regard to

the individual income tax. The individual income tax (inkomstenbelasting)

is an annual tax imposed under the Individual Income Tax Act 2001 (Wet

inkomstenbelasting 2001, IB). For individuals, the tax year is equal to the

calendar year and the income of an individual should be classified into one

of three boxes. Each type of income in each Box must be calculated

separately. Each Box has a different income calculation and a different tax

rate applies for each Box.

The Individual Income Tax Act 2001 knows three categories (Boxes):

earned income and income from owner-occupied dwellings (belastbaar

inkomen uit werk en woning) - taxed at progressive rates (maximum 52%);

capital gains and other income from a substantial shareholding in a company

(belastbaar inkomen uit aanmerkelijk belang) - taxed at 25%; and

income from savings and investments (belastbaar inkomen uit sparen en

beleggen) –(equal to 4% of the average amount of the assets and debts at

10 Article 2.13 Income Tax Act 2001

Netherlands Country Report

February 2008

8

the beginning and the end of the year. The calculated result is taxable at a

rate of 30%, therefore effectively 1,2% (30% of 4%) of the net wealth.

These abovementioned categories are referred to as Box 1, Box 2 and Box 3

income respectively.

Depending on the source of income, the income will thus be treated

differently for tax purposes.

1.3 Capital

The

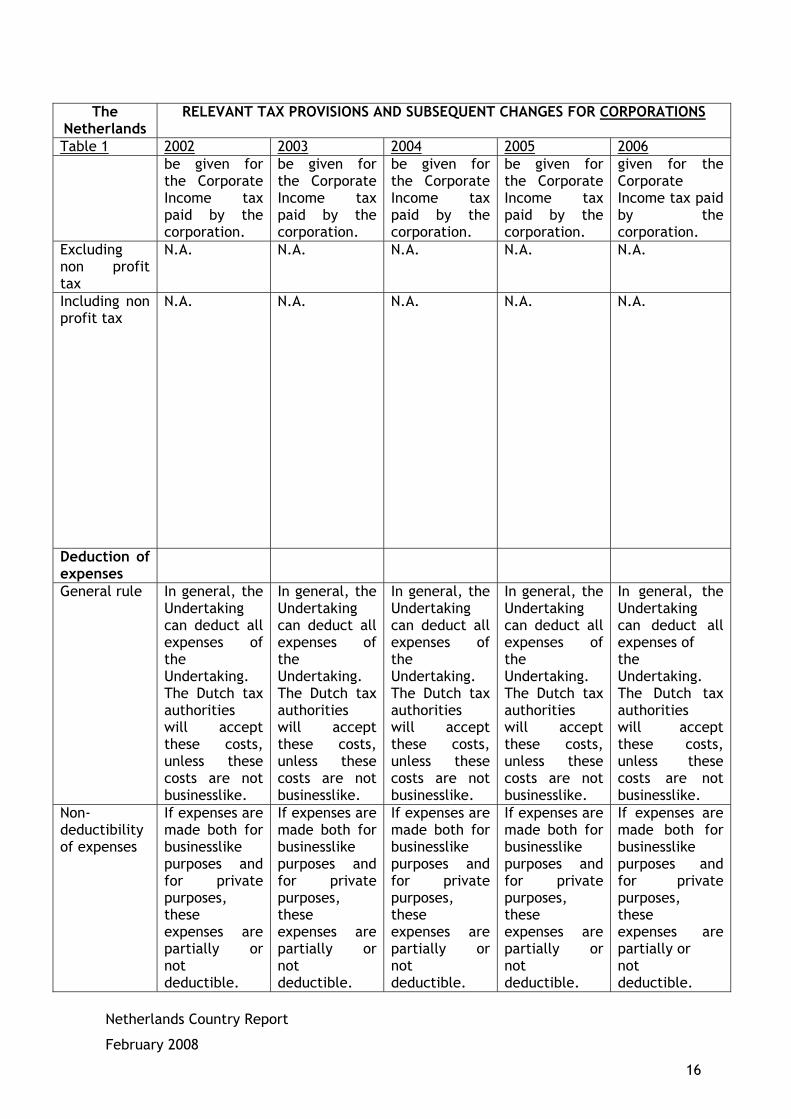

Netherlands RELEVANT TAX PROVISIONS AND SUBSEQUENT CHANGES FOR CORPORATIONS

Table 1 2002 2003 2004 2005 2006 Corporate tax

1. Tax rate Standard 34,5% 34,5% 34,5% 31,5% 29,6 Reduced 29% 29% 29% 27% 25,5% Minimum Tax - - - - - Special Rates Results of

Investment institutions will be taxed at a rate of 0%.

Results of Investment institutions will be taxed at a rate of 0%.

Results of Investment institutions will be taxed at a rate of 0%.

Results of Investment institutions will be taxed at a rate of 0%.

Results of Investment institutions will be taxed at a rate of 0%.

Non profit tax (local tax on corporations, energy tax…)

Municipalities are allowed to levy taxes in accordance with the Municipality law.

Municipalities are allowed to levy taxes in accordance with the Municipality law.

Municipalities are allowed to levy taxes in accordance with the Municipality law.

Municipalities are allowed to levy taxes in accordance with the Municipality law.

Municipalities are allowed to levy taxes in accordance with the Municipality law.

2. Tax accounting rules

Without postponement, an annual return for the corporate income tax should be filed before 1 June of the subsequent year.

Without postponement, an annual return for the corporate income tax should be filed before 1 June of the subsequent year.

Without postponement, an annual return for the corporate income tax should be filed before 1 June of the subsequent year. As of the

Without postponement, an annual return for the corporate income tax should be filed before 1 June of the subsequent year. As of the

Without postponement, an annual return for the corporate income tax should be filed before 1 June of the subsequent year. As of the

11 Article 3.92 Income Tax Act 2001

Netherlands Country Report

February 2008

9

The Netherlands

RELEVANT TAX PROVISIONS AND SUBSEQUENT CHANGES FOR CORPORATIONS

Table 1 2002 2003 2004 2005 2006 tax year 2004, annual returns for corporate income tax should be filed electronically.

tax year 2004, annual returns for corporate income tax should be filed electronically.

tax year 2004, annual returns for corporate income tax should be filed electronically.

3. Depreciation

Basis Cost price Cost price Cost price Cost price Cost price Methods Linear

Degressive Progressive

Linear Degressive Progressive

Linear Degressive Progressive

Linear Degressive Progressive

Linear Degressive Progressive

Rates - - - - - Accounting In accounts In accounts In accounts In accounts In accounts Intangibles Possible,

intangible assets are depreciated linearly most of the times.

Possible, intangible assets are depreciated linearly most of the times.

Possible, intangible assets are depreciated linearly most of the times.

Possible, intangible assets are depreciated linearly most of the times.

Possible, intangible assets are depreciated linearly most of the times.

Non depreciable assets

In general, all business assets are depreciable. An exception is the depreciation of land and portfolio investments.

In general, all business assets are depreciable. An exception is the depreciation of land and portfolio investments.

In general, all business assets are depreciable. An exception is the depreciation of land and portfolio investments.

In general, all business assets are depreciable. An exception is the depreciation of land and portfolio investments.

In general, all business assets are depreciable. An exception is the depreciation of land and portfolio investments.

4. Provisions Risks and futures expenses

The Netherlands Supreme Court has decided in 1998 (Baksteen-case, HR 26 August 1998, BNB 1998/409) that it is possible to allocate funds to a provision for risks and future expenses.

The Netherlands Supreme Court has decided in 1998 (Baksteen-case, HR 26 August 1998, BNB 1998/409) that it is possible to allocate funds to a provision for risks and future expenses.

The Netherlands Supreme Court has decided in 1998 (Baksteen-case, HR 26 August 1998, BNB 1998/409) that it is possible to allocate funds to a provision for risks and future expenses.

The Netherlands Supreme Court has decided in 1998 (Baksteen-case, HR 26 August 1998, BNB 1998/409) that it is possible to allocate funds to a provision for risks and future expenses.

The Netherlands Supreme Court has decided in 1998 (Baksteen-case, HR 26 August 1998, BNB 1998/409) that it is possible to allocate funds to a provision for risks and future expenses.

Bad debts It is not possible to

It is not possible to

It is not possible to

It is not possible to

It is not possible to

Netherlands Country Report

February 2008

10

The Netherlands

RELEVANT TAX PROVISIONS AND SUBSEQUENT CHANGES FOR CORPORATIONS

Table 1 2002 2003 2004 2005 2006 allocate funds to a provision in order to cover bad debts/debtors. However, for tax purposes it is possible to revaluate the amount of “debtors” in the tax balance sheet.

allocate funds to a provision in order to cover bad debts/debtors. However, for tax purposes it is possible to revaluate the amount of “debtors” in the tax balance sheet.

allocate funds to a provision in order to cover bad debts/debtors. However, for tax purposes it is possible to revaluate the amount of “debtors” in the tax balance sheet.

allocate funds to a provision in order to cover bad debts/debtors. However, for tax purposes it is possible to revaluate the amount of “debtors” in the tax balance sheet.

allocate funds to a provision in order to cover bad debts/debtors. However, for tax purposes it is possible to revaluate the amount of “debtors” in the tax balance sheet.

Pensions It is possible for managing directors with a substantial interest in a company to allocate funds to a provision for pension for him/his spouse.

It is possible for managing directors with a substantial interest in a company to allocate funds to a provision for pension for him/his spouse.

It is possible for managing directors with a substantial interest in a company to allocate funds to a provision for pension for him/his spouse.

It is possible for managing directors with a substantial interest in a company to allocate funds to a provision for pension for him/his spouse.

It is possible for managing directors with a substantial interest in a company to allocate funds to a provision for pension for him/his spouse.

Repairs It is possible to allocate funds to a provision for repairs (article 3.53 IB).

It is possible to allocate funds to a provision for repairs (article 3.53 IB).

It is possible to allocate funds to a provision for repairs (article 3.53 IB).

It is possible to allocate funds to a provision for repairs (article 3.53 IB).

It is possible to allocate funds to a provision for repairs (article 3.53 IB).

5. Losses Carry forward

Unlimited in time.

Unlimited in time.

Unlimited in time.

Unlimited in time.

Unlimited in time.12

Carry back Three years. Three years. Three years. Three years. Three years.13 Transfer of losses

Not possible as separate asset. If the interest in an inactive company will change with at least 30% in comparison with the oldest year with a loss, the loss of

Not possible as separate asset. If the interest in an inactive company will change with at least 30% in comparison with the oldest year with a loss, the loss of

Not possible as separate asset. If the interest in an inactive company will change with at least 30% in comparison with the oldest year with a loss, the loss of

Not possible as separate asset. If the interest in an inactive company will change with at least 30% in comparison with the oldest year with a loss, the loss of

Not possible as separate asset. If the interest in an inactive company will change with at least 30% in comparison with the oldest year with a loss, the loss of

12 As of 1 January 2007, the period for carry forward is 9 years. 13 As of 1 January 2007, the period for carry back is 1 year.

Netherlands Country Report

February 2008

11

The Netherlands

RELEVANT TAX PROVISIONS AND SUBSEQUENT CHANGES FOR CORPORATIONS

Table 1 2002 2003 2004 2005 2006 that year can not be set off against future profits.14

that year can not be set off against future profits.15

that year can not be set off against future profits.16

that year can not be set off against future profits.17

that year can not be set off against future profits.18

5. Inventories

Valuation rules

FIFO, LIFO and “Iron Inventories”

FIFO, LIFO and “Iron Inventories”

FIFO, LIFO and “Iron Inventories”

FIFO, LIFO and “Iron Inventories”

FIFO, LIFO and “Iron Inventories”

Allocation methods

FIFO, LIFO and “Iron Inventories”

FIFO, LIFO and “Iron Inventories”

FIFO, LIFO and “Iron Inventories”

FIFO, LIFO and “Iron Inventories”

FIFO, LIFO and “Iron Inventories”

Personal Income tax

Interest Income

Might be taxable in Box 1 at a maximum of 52%, otherwise it will not be taxed.

Might be taxable in Box 1 at a maximum of 52%, otherwise it will not be taxed.

Might be taxable in Box 1 at a maximum of 52%, otherwise it will not be taxed.

Might be taxable in Box 1 at a maximum of 52%, otherwise it will not be taxed.

Might be taxable in Box 1 at a maximum of 52%, otherwise it will not be taxed.

Dividends Taxable at a rate of 25% if the business owner holds a substantial interest in the corporation. Otherwise the dividend will not be taxed directly.

Taxable at a rate of 25% if the business owner holds a substantial interest in the corporation. Otherwise the dividend will not be taxed directly.

Taxable at a rate of 25% if the business owner holds a substantial interest in the corporation. Otherwise the dividend will not be taxed directly.

Taxable at a rate of 25% if the business owner holds a substantial interest in the corporation. Otherwise the dividend will not be taxed directly.

Taxable at a rate of 25% if the business owner holds a substantial interest in the corporation. Otherwise the dividend will not be taxed directly.

Employment income

Employment income is taxable with individual income tax at a maximum rate of 52%.

Employment income is taxable with individual income tax at a maximum rate of 52%.

Employment income is taxable with individual income tax at a maximum rate of 52%.

Employment income is taxable with individual income tax at a maximum rate of 52%.

Employment income is taxable with individual income tax at a maximum rate of 52%.

Capital gains tax

14 Article 20A Corporate Income Tax Act 1969 15 Idem 16 Idem 17 Idem 18 Idem

Netherlands Country Report

February 2008

12

The Netherlands

RELEVANT TAX PROVISIONS AND SUBSEQUENT CHANGES FOR CORPORATIONS

Table 1 2002 2003 2004 2005 2006 Sale of fixed assets

The capital gain will be taxed with regular corporate income tax at a rate of 34,5%19. No special tax is applicable.

The capital gain will be taxed with regular corporate income tax at a rate of 34,5%20. No special tax is applicable.

The capital gain will be taxed with regular corporate income tax at a rate of 34,5%21. No special tax is applicable.

The capital gain will be taxed with regular corporate income tax at a rate of 31,5%22. No special tax is applicable.

The capital gain will be taxed with regular corporate income tax at a rate of 29,6%23. No special tax is applicable.

Timing rules In general the capital gain will be taxed at the moment it comes up, this is the moment of realization of the gain. An exception is when the company will allocate the realised capital gain into a re-investment provision24.

In general the capital gain will be taxed at the moment it comes up, this is the moment of realization of the gain. An exception is when the company will allocate the realised capital gain into a re-investment provision25.

In general the capital gain will be taxed at the moment it comes up, this is the moment of realization of the gain. An exception is when the company will allocate the realised capital gain into a re-investment provision26.

In general the capital gain will be taxed at the moment it comes up, this is the moment of realization of the gain. An exception is when the company will allocate the realised capital gain into a re-investment provision27.

In general the capital gain will be taxed at the moment it comes up, this is the moment of realization of the gain. An exception is when the company will allocate the realised capital gain into a re-investment provision28.

Accounting rules

There are no specific accounting rules for capital gains.

There are no specific accounting rules for capital gains.

There are no specific accounting rules for capital gains.

There are no specific accounting rules for capital gains.

There are no specific accounting rules for capital gains.

Inflation N.A. N.A. N.A. N.A. N.A.

Rates No specific corporate income tax

No specific corporate income tax

No specific corporate income tax

No specific corporate income tax

No specific corporate income tax

19 Article 22 Corporate Income Tax Act 1969 20 Idem 21 Idem 22 Idem 23 Idem 24 Article 3.51 Income Tax Act 2001 25 Idem 26 Idem 27 Idem 28 Idem

Netherlands Country Report

February 2008

13

The Netherlands

RELEVANT TAX PROVISIONS AND SUBSEQUENT CHANGES FOR CORPORATIONS

Table 1 2002 2003 2004 2005 2006 rates apply for capital gains.

rates apply for capital gains.

rates apply for capital gains.

rates apply for capital gains.

rates apply for capital gains.

Exemptions A capital gain realized by a transfer of assets does not have to be taxed immediately. Under certain circumstances it is possible to include the amount of the capital gain in a reserve, maintained for re-investment purposes.

A capital gain realized by a transfer of assets does not have to be taxed immediately. Under certain circumstances it is possible to include the amount of the capital gain in a reserve, maintained for re-investment purposes.

A capital gain realized by a transfer of assets does not have to be taxed immediately. Under certain circumstances it is possible to include the amount of the capital gain in a reserve, maintained for re-investment purposes.

A capital gain realized by a transfer of assets does not have to be taxed immediately. Under certain circumstances it is possible to include the amount of the capital gain in a reserve, maintained for re-investment purposes.

A capital gain realized by a transfer of assets does not have to be taxed immediately. Under certain circumstances it is possible to include the amount of the capital gain in a reserve, maintained for re-investment purposes.

Sale of shares

If the corporation will sell shares in a company in which the corporation has a substantial interest, the capital gain will not be taxed as a result of the applicability of the participation exemption29. If the interest is

If the corporation will sell shares in a company in which the corporation has a substantial interest, the capital gain will not be taxed as a result of the applicability of the participation exemption30. If the interest is

If the corporation will sell shares in a company in which the corporation has a substantial interest, the capital gain will not be taxed as a result of the applicability of the participation exemption31. If the interest is

If the corporation will sell shares in a company in which the corporation has a substantial interest, the capital gain will not be taxed as a result of the applicability of the participation exemption32. If the interest is

If the corporation will sell shares in a company in which the corporation has a substantial interest, the capital gain will not be taxed as a result of the applicability of the participation exemption33. If the interest is

29 Article 13 Corporate Income tax Act 1969 30 Idem 31 Idem 32 Idem 33 Idem

Netherlands Country Report

February 2008

14

The Netherlands

RELEVANT TAX PROVISIONS AND SUBSEQUENT CHANGES FOR CORPORATIONS

Table 1 2002 2003 2004 2005 2006 less than 5%, the capital gain may be taxed at a general rate of 34,5%.

less than 5%, the capital gain may be taxed at a general rate of 34,5%.

less than 5%, the capital gain may be taxed at a general rate of 34,5%.

less than 5%, the capital gain may be taxed at a general rate of 31,5%.

less than 5%, the capital gain may be taxed at a general rate of 29,6%.

Capital loss Fixed assets A loss as a

result of the sale of fixed assets can be set off against positive results of the company. If the company will not have positive results, the company will have a loss in that year.

A loss as a result of the sale of fixed assets can be set off against positive results of the company. If the company will not have positive results, the company will have a loss in that year.

A loss as a result of the sale of fixed assets can be set off against positive results of the company. If the company will not have positive results, the company will have a loss in that year.

A loss as a result of the sale of fixed assets can be set off against positive results of the company. If the company will not have positive results, the company will have a loss in that year.

A loss as a result of the sale of fixed assets can be set off against positive results of the company. If the company will not have positive results, the company will have a loss in that year.

Shares As a result of the participation exemption, losses of a company realised by the transfer of shares held in participations are not deductible unless the participation is liquidated.

As a result of the participation exemption, losses of a company realised by the transfer of shares held in participations are not deductible unless the participation is liquidated.

As a result of the participation exemption, losses of a company realised by the transfer of shares held in participations are not deductible unless the participation is liquidated.

As a result of the participation exemption, losses of a company realised by the transfer of shares held in participations are not deductible unless the participation is liquidated.

As a result of the participation exemption, losses of a company realised by the transfer of shares held in participations are not deductible unless the participation is liquidated.

Wages Average cost to the Undertaking

An employee with a substantial interest in an Undertaking, is deemed to have a fictive salary of at

An employee with a substantial interest in an Undertaking, is deemed to have a fictive salary of at

An employee with a substantial interest in an Undertaking, is deemed to have a fictive salary of at

An employee with a substantial interest in an Undertaking, is deemed to have a fictive salary of at

An employee with a substantial interest in an Undertaking, is deemed to have a fictive salary of at

Netherlands Country Report

February 2008

15

The Netherlands

RELEVANT TAX PROVISIONS AND SUBSEQUENT CHANGES FOR CORPORATIONS

Table 1 2002 2003 2004 2005 2006 least EUR 38.118 a year34. The costs are deductible.

least EUR 38.118 a year35. The costs are deductible.

least EUR 38.118 a year36. The costs are deductible.

least EUR 38.118 a year37. The costs are deductible.

least EUR 39.000 a year38. The costs are deductible.

Average cost to the employee

The wages earned by the employee are taxable in Box 1 at a maximum rate of 52%.

The wages earned by the employee are taxable in Box 1 at a maximum rate of 52%.

The wages earned by the employee are taxable in Box 1 at a maximum rate of 52%.

The wages earned by the employee are taxable in Box 1 at a maximum rate of 52%.

The wages earned by the employee are taxable in Box 1 at a maximum rate of 52%.

Overall tax on distributed earnings or Dividends

Timing At the moment of the distribution of the earnings are put at the disposal of the business owner.

At the moment of the distribution of the earnings are put at the disposal of the business owner.

At the moment of the distribution of the earnings are put at the disposal of the business owner.

At the moment of the distribution of the earnings are put at the disposal of the business owner.

At the moment of the distribution of the earnings are put at the disposal of the business owner.

Tax credit structure

The company will withhold Dividend tax at a rate of 25% which is credited against the personal Income tax. No credit will

The company will withhold Dividend tax at a rate of 25% which is credited against the personal Income tax. No credit will

The company will withhold Dividend tax at a rate of 25% which is credited against the personal Income tax. No credit will

The company will withhold Dividend tax at a rate of 25% which is credited against the personal Income tax. No credit will

The company will withhold Dividend tax at a rate of 25% which is credited against the personal Income tax. No credit will be

34 Wage Tax Act 1964 35 Idem 36 Idem 37 Idem 38 Idem

Netherlands Country Report

February 2008

16

The Netherlands

RELEVANT TAX PROVISIONS AND SUBSEQUENT CHANGES FOR CORPORATIONS

Table 1 2002 2003 2004 2005 2006 be given for the Corporate Income tax paid by the corporation.

be given for the Corporate Income tax paid by the corporation.

be given for the Corporate Income tax paid by the corporation.

be given for the Corporate Income tax paid by the corporation.

given for the Corporate Income tax paid by the corporation.

Excluding non profit tax

N.A. N.A. N.A. N.A. N.A.

Including non profit tax

N.A. N.A. N.A. N.A. N.A.

Deduction of expenses

General rule In general, the Undertaking can deduct all expenses of the Undertaking. The Dutch tax authorities will accept these costs, unless these costs are not businesslike.

In general, the Undertaking can deduct all expenses of the Undertaking. The Dutch tax authorities will accept these costs, unless these costs are not businesslike.

In general, the Undertaking can deduct all expenses of the Undertaking. The Dutch tax authorities will accept these costs, unless these costs are not businesslike.

In general, the Undertaking can deduct all expenses of the Undertaking. The Dutch tax authorities will accept these costs, unless these costs are not businesslike.

In general, the Undertaking can deduct all expenses of the Undertaking. The Dutch tax authorities will accept these costs, unless these costs are not businesslike.

Non-deductibility of expenses

If expenses are made both for businesslike purposes and for private purposes, these expenses are partially or not deductible.

If expenses are made both for businesslike purposes and for private purposes, these expenses are partially or not deductible.

If expenses are made both for businesslike purposes and for private purposes, these expenses are partially or not deductible.

If expenses are made both for businesslike purposes and for private purposes, these expenses are partially or not deductible.

If expenses are made both for businesslike purposes and for private purposes, these expenses are partially or not deductible.

Netherlands Country Report

February 2008

17

The Netherlands

RELEVANT TAX PROVISIONS AND SUBSEQUENT CHANGES FOR CORPORATIONS

Table 1 2002 2003 2004 2005 2006 Thin capitalization

N.A. N.A. As of 2004: Interest paid by a corporation is deductible unless the debt-equity (3:1) ratio is met39.

As of 2004: Interest paid by a corporation is deductible unless the debt-equity (3:1) ratio is met40.

As of 2004: Interest paid by a corporation is deductible unless the debt-equity (3:1) ratio is met41.

Overall corporate tax on Retained earnings

No different tax treatment for distributed earnings in comparison of retained earnings.

No different tax treatment for distributed earnings in comparison of retained earnings.

No different tax treatment for distributed earnings in comparison of retained earnings.

No different tax treatment for distributed earnings in comparison of retained earnings.

No different tax treatment for distributed earnings in comparison of retained earnings.

Excluding non profit tax

N.A. N.A. N.A. N.A. N.A.

Including non profit tax

N.A. N.A. N.A. N.A. N.A.

Debt financing

Interest deductibility

Interest is generally deductible. However, under certain circumstances interest can not be deducted.

Interest is generally deductible. However, under certain circumstances interest can not be deducted.

Interest is generally deductible. However, under certain circumstances interest can not be deducted.

Interest is generally deductible. However, under certain circumstances interest can not be deducted.

Interest is generally deductible. However, under certain circumstances interest can not be deducted.

Limits on interest deductibility

Article 10 Vpb, article 10a Vpb, article 10b and article 15 paragraphs 4 and 5 Vpb.

Article 10 Vpb, article 10a Vpb, article 10b and article 15 AD Vpb.

Article 10 Vpb, article 10a Vpb, article 10b and article 15 AD Vpb.

Article 10 Vpb, article 10a Vpb, article 10b and article 15 AD Vpb.

Article 10 Vpb, article 10a Vpb, article 10b and article 15 AD Vpb.

Interest deductibility on business owner loan to Undertaking

The interest is deductible at the level of the Undertaking but will be taxed at the

The interest is deductible at the level of the Undertaking but will be taxed at the

The interest is deductible at the level of the Undertaking but will be taxed at the

The interest is deductible at the level of the Undertaking but will be taxed at the

The interest is deductible at the level of the Undertaking but will be taxed at the

39 Article 10D Corporate Income Tax 1969 40 Idem 41 Idem

Netherlands Country Report

February 2008

18

The Netherlands

RELEVANT TAX PROVISIONS AND SUBSEQUENT CHANGES FOR CORPORATIONS

Table 1 2002 2003 2004 2005 2006 level of the business owner (maximum 52%).

level of the business owner (maximum 52%).

level of the business owner (maximum 52%).

level of the business owner (maximum 52%).

level of the business owner (maximum 52%).

The Netherlands

RELEVANT TAX PROVISIONS AND SUBSEQUENT CHANGES FOR PARTNERSHIPS

Table 2 2002 2003 2004 2005 2006 Tax applicable to partnerships

1. Tax rate Standard Maximum 52% Maximum 52% Maximum 52% Maximum 52% Maximum 52% Reduced - - - - - Minimum Tax 32,35% 33,15% 33,55% 34,4% 34,15% Special Rates N.A. N.A. N.A. N.A. N.A. Non profit tax (local tax on corporations, energy tax…)

Municipalities are allowed to levy taxes in accordance with the Municipalities Act.

Municipalities are allowed to levy taxes in accordance with the Municipalities Act.

Municipalities are allowed to levy taxes in accordance with the Municipalities Act.

Municipalities are allowed to levy taxes in accordance with the Municipalities Act.

Municipalities are allowed to levy taxes in accordance with the Municipalities Act.

2. Tax accounting rules

Without postponement, an annual return for the individual income tax should be filed

Without postponement, an annual return for the individual income tax should be filed

Without postponement, an annual return for the individual income tax should be filed

Without postponement, an annual return for the individual income tax should be filed

Without postponement, an annual return for the individual income tax should be filed

Netherlands Country Report

February 2008

19

The Netherlands

RELEVANT TAX PROVISIONS AND SUBSEQUENT CHANGES FOR PARTNERSHIPS

Table 2 2002 2003 2004 2005 2006 before 1 April of the subsequent year.

before 1 April of the subsequent year.

before 1 April of the subsequent year. As of the tax year 2004, annual returns for corporate income tax should be filed electronically.

before 1 April of the subsequent year. As of the tax year 2004, annual returns for corporate income tax should be filed electronically.

before 1 April of the subsequent year. As of the tax year 2004, annual returns for corporate income tax should be filed electronically.

3. Depreciation

Basis Cost price Cost price Cost price Cost price Cost price Methods Linear

Degressive Progressive

Linear Degressive Progressive

Linear Degressive Progressive

Linear Degressive Progressive

Linear Degressive Progressive

Rates - - - - - Accounting In accounts In accounts In accounts In accounts In accounts

Intangibles Possible, intangible assets are depreciated linearly most of the times.

Possible, intangible assets are depreciated linearly most of the times.

Possible, intangible assets are depreciated linearly most of the times.

Possible, intangible assets are depreciated linearly most of the times.

Possible, intangible assets are depreciated linearly most of the times.

Non depreciable assets

In general, all business assets are depreciable. An exception is the depreciation of land and portfolio investment.

In general, all business assets are depreciable. An exception is the depreciation of land and portfolio investment.

In general, all business assets are depreciable. An exception is the depreciation of land and portfolio investment.

In general, all business assets are depreciable. An exception is the depreciation of land and portfolio investment.

In general, all business assets are depreciable. An exception is the depreciation of land and portfolio investment.

4. Provisions Risks and futures expenses

The Netherlands Supreme Court has decided in 1998 (Baksteen-case, HR 26 August 1998, BNB 1998/409) that it is possible to allocate funds to a provision for risks and future expenses.

The Netherlands Supreme Court has decided in 1998 (Baksteen-case, HR 26 August 1998, BNB 1998/409) that it is possible to allocate funds to a provision for risks and future expenses.

The Netherlands Supreme Court has decided in 1998 (Baksteen-case, HR 26 August 1998, BNB 1998/409) that it is possible to allocate funds to a provision for risks and future expenses.

The Netherlands Supreme Court has decided in 1998 (Baksteen-case, HR 26 August 1998, BNB 1998/409) that it is possible to allocate funds to a provision for risks and future expenses.

The Netherlands Supreme Court has decided in 1998 (Baksteen-case, HR 26 August 1998, BNB 1998/409) that it is possible to allocate funds to a provision

Netherlands Country Report

February 2008

20

The Netherlands

RELEVANT TAX PROVISIONS AND SUBSEQUENT CHANGES FOR PARTNERSHIPS

Table 2 2002 2003 2004 2005 2006 for risks and future expenses.

Bad debts It is not possible to allocate funds to a provision in order to cover bad debts/debtors. However, for tax purposes it is possible to re-valuate the amount of “debtors” in the tax balance sheet.

It is not possible to allocate funds to a provision in order to cover bad debts/debtors. However, for tax purposes it is possible to re-valuate the amount of “debtors” in the tax balance sheet.

It is not possible to allocate funds to a provision in order to cover bad debts/debtors. However, for tax purposes it is possible to re-valuate the amount of “debtors” in the tax balance sheet.

It is not possible to allocate funds to a provision in order to cover bad debts/debtors. However, for tax purposes it is possible to re-valuate the amount of “debtors” in the tax balance sheet.

It is not possible to allocate funds to a provision in order to cover bad debts/debtors. However, for tax purposes it is possible to re-valuate the amount of “debtors” in the tax balance sheet.

Pensions The business can make contributions for a provision for the self-employed.

The business can make contributions for a provision for the self-employed.

The business can make contributions for a provision for the self-employed.

The business can make contributions for a provision for the self-employed.

The business can make contributions for a provision for the self-employed.

Repairs It is possible to allocate funds to a provision for repairs (article 3.53 IB).

It is possible to allocate funds to a provision for repairs (article 3.53 IB).

It is possible to allocate funds to a provision for repairs (article 3.53 IB).

It is possible to allocate funds to a provision for repairs (article 3.53 IB).

It is possible to allocate funds to a provision for repairs (article 3.53 IB).

5. Losses Carry forward

Losses from entrepreneurship can be carried forward unlimited in time42.

Losses from entrepreneurship can be carried forward unlimited in time43.

Losses from entrepreneurship can be carried forward unlimited in time44.

Losses from entrepreneurship can be carried forward unlimited in time45.

Losses from entrepreneurship can be carried forward unlimited in time46.

Carry back 3 years47 3 years48 3 years49 3 years50 3 years51

42 Article 3.150 Income Tax Act 2001 43 Idem 44 Idem 45 Idem 46 Idem 47 Idem 48 Idem 49 Idem

Netherlands Country Report

February 2008

21

The Netherlands

RELEVANT TAX PROVISIONS AND SUBSEQUENT CHANGES FOR PARTNERSHIPS

Table 2 2002 2003 2004 2005 2006 Transfer of losses

Not possible as losses are strictly connected to the business owner.

Not possible as losses are strictly connected to the business owner.

Not possible as losses are strictly connected to the business owner.

Not possible as losses are strictly connected to the business owner.

Not possible as losses are strictly connected to the business owner.

5. Inventories

Valuation rules

FIFO, LIFO and “Iron Inventories”

FIFO, LIFO and “Iron Inventories”

FIFO, LIFO and “Iron Inventories”

FIFO, LIFO and “Iron Inventories”

FIFO, LIFO and “Iron Inventories”

Allocation methods

FIFO, LIFO and “Iron Inventories”

FIFO, LIFO and “Iron Inventories”

FIFO, LIFO and “Iron Inventories”

FIFO, LIFO and “Iron Inventories”

FIFO, LIFO and “Iron Inventories”

Personal Income tax

Interest Income

N.A. from the business owner´s point of view.

N.A. from the business owner´s point of view.

N.A. from the business owner´s point of view.

N.A. from the business owner´s point of view.

N.A. from the business owner´s point of view.

Dividends N.A. from the business owner´s point of view.

N.A. from the business owner´s point of view.

N.A. from the business owner´s point of view.

N.A. from the business owner´s point of view.

N.A. from the business owner´s point of view.

Employment income

N.A. from the business owner´s point of view.

N.A. from the business owner´s point of view.

N.A. from the business owner´s point of view.

N.A. from the business owner´s point of view.

N.A. from the business owner´s point of view.

Capital gains tax

Sale of fixed assets

The capital gain will be taxed with normal income tax.

The capital gain will be taxed with normal income tax.

The capital gain will be taxed with normal income tax.

The capital gain will be taxed with normal income tax.

The capital gain will be taxed with normal income tax.

Timing rules In general the capital gain will be taxed at the moment it comes up. This is the moment of realization of the gain.

In general the capital gain will be taxed at the moment it comes up. This is the moment of realization of the gain.

In general the capital gain will be taxed at the moment it comes up. This is the moment of realization of the gain.

In general the capital gain will be taxed at the moment it comes up. This is the moment of realization of the gain.

In general the capital gain will be taxed at the moment it comes up. This is the moment of realization of the gain.

Accounting There are no There are no There are no There are no There are no 50 Idem 51 Idem

Netherlands Country Report

February 2008

22

The Netherlands

RELEVANT TAX PROVISIONS AND SUBSEQUENT CHANGES FOR PARTNERSHIPS

Table 2 2002 2003 2004 2005 2006 rules specific

accounting rules for capital gains.

specific accounting rules for capital gains.

specific accounting rules for capital gains.

specific accounting rules for capital gains.

specific accounting rules for capital gains.

Inflation N.A. N.A. N.A. N.A. N.A. Rates The maximum

rate of income tax is 52%. The minimum rate is 32,35%52.

The maximum rate of income tax is 52%. The minimum rate is 33,15%53.

The maximum rate of income tax is 52%. The minimum rate is 33,55%54.

The maximum rate of income tax is 52%. The minimum rate is 34,4%55.

The maximum rate of income tax is 52%.The minimum rate is 34,15%56,

Exemptions A capital gain realised by a transfer of assets does not have to be taxed immediately. Under certain circumstances it is possible to include the amount of the capital gain in a reserve, maintained for re-investment purposes.

A capital gain realised by a transfer of assets does not have to be taxed immediately. Under certain circumstances it is possible to include the amount of the capital gain in a reserve, maintained for re-investment purposes.

A capital gain realised by a transfer of assets does not have to be taxed immediately. Under certain circumstances it is possible to include the amount of the capital gain in a reserve, maintained for re-investment purposes.

A capital gain realised by a transfer of assets does not have to be taxed immediately. Under certain circumstances it is possible to include the amount of the capital gain in a reserve, maintained for re-investment purposes.

A capital gain realised by a transfer of assets does not have to be taxed immediately. Under certain circumstances it is possible to include the amount of the capital gain in a reserve, maintained for re-investment purposes.

Sale of shares

The capital gain will be taxed in Box 2 at a rate of 25%.

The capital gain will be taxed in Box 2 at a rate of 25%.

The capital gain will be taxed in Box 2 at a rate of 25%.

The capital gain will be taxed in Box 2 at a rate of 25%.

The capital gain will be taxed in Box 2 at a rate of 25%.

Capital loss Fixed assets A loss as a result

of the sale of fixed assets can be set off against positive results of the company. If the company will not

A loss as a result of the sale of fixed assets can be set off against positive results of the company. If the company will not

A loss as a result of the sale of fixed assets can be set off against positive results of the company. If the company will not

A loss as a result of the sale of fixed assets can be set off against positive results of the company. If the company will not

A loss as a result of the sale of fixed assets can be set off against positive results of the company. If the

52 Article 2.10 Income Tax Act 2001 53 Idem 54 Idem 55 Idem 56 Idem

Netherlands Country Report

February 2008

23

The Netherlands

RELEVANT TAX PROVISIONS AND SUBSEQUENT CHANGES FOR PARTNERSHIPS

Table 2 2002 2003 2004 2005 2006 have positive results, the company will have a loss in that year.

have positive results, the company will have a loss in that year.

have positive results, the company will have a loss in that year.

have positive results, the company will have a loss in that year.

company will not have positive results, the company will have a loss in that year.

Shares As a result of article 3.150 IB, the loss can be set off against results of the previous three years. The loss can be set off against profits unlimited in future.

As a result of article 3.150 IB, the loss can be set off against results of the previous three years. The loss can be set off against profits unlimited in future.

As a result of article 3.150 IB, the loss can be set off against results of the previous three years. The loss can be set off against profits unlimited in future.

As a result of article 3.150 IB, the loss can be set off against results of the previous three years. The loss can be set off against profits unlimited in future.

As a result of article 3.150 IB, the loss can be set off against results of the previous three years. The loss can be set off against profits unlimited in future.

Wages Average cost to the Undertaking

The costs of the wages paid are deductible.

The costs of the wages paid are deductible.

The costs of the wages paid are deductible.

The costs of the wages paid are deductible.

The costs of the wages paid are deductible.

Average cost to the employee

Income generated is taxable at a maximum rate of 52%

Income generated is taxable at a maximum rate of 52%

Income generated is taxable at a maximum rate of 52%

Income generated is taxable at a maximum rate of 52%

Income generated is taxable at a maximum rate of 52%

Dividends Timing N.A. N.A. N.A. N.A. N.A. Tax credit structure

N.A. N.A. N.A. N.A. N.A.

Deduction of expenses

General rule In general, the Undertaking can deduct all expenses of the Undertaking. The Dutch tax authorities will accept the amounts unless certain costs are not businesslike.

In general, the Undertaking can deduct all expenses of the Undertaking. The Dutch tax authorities will accept the amounts unless certain costs are not businesslike.

In general, the Undertaking can deduct all expenses of the Undertaking. The Dutch tax authorities will accept the amounts unless certain costs are not businesslike.

In general, the Undertaking can deduct all expenses of the Undertaking. The Dutch tax authorities will accept the amounts unless certain costs are not businesslike.

In general, the Undertaking can deduct all expenses of the Undertaking. The Dutch tax authorities will accept the amounts unless certain costs are not businesslike.

Non-deductibility of expenses

If expenses are made both for businesslike

If expenses are made both for businesslike

If expenses are made both for businesslike

If expenses are made both for businesslike

If expenses are made both for businesslike

Netherlands Country Report

February 2008

24

The Netherlands

RELEVANT TAX PROVISIONS AND SUBSEQUENT CHANGES FOR PARTNERSHIPS

Table 2 2002 2003 2004 2005 2006 purposes and for private purposes, these expenses are partially or not deductible.

purposes and for private purposes, these expenses are partially or not deductible.

purposes and for private purposes, these expenses are partially or not deductible.

purposes and for private purposes, these expenses are partially or not deductible.

purposes and for private purposes, these expenses are partially or not deductible.

Thin capitalization

N.A. N.A. N.A. N.A. N.A.

Retained earnings

No special treatment.

No special treatment.

No special treatment.

No special treatment.

No special treatment.

Debt financing

Interest deductibility

Interest paid by the partnership is deductible.

Interest paid by the partnership is deductible.

Interest paid by the partnership is deductible.

Interest paid by the partnership is deductible.

Interest paid by the partnership is deductible.

Limits on interest deductibility

N.A., but the interest should be at arm´s length.

N.A., but the interest should be at arm´s length.

N.A., but the interest should be at arm´s length.

N.A., but the interest should be at arm´s length.

N.A., but the interest should be at arm´s length.

Interest deductibility on business owner loan to Undertaking

Deductible at the level of the Undertaking unless seen as capital.

Deductible at the level of the Undertaking unless seen as capital.

Deductible at the level of the Undertaking unless seen as capital.

Deductible at the level of the Undertaking unless seen as capital.

Deductible at the level of the Undertaking unless seen as capital.

1.3.1 Is there a different tax treatment between distributions of earnings

and capital gains realised by the sale of the business or the shares in

the undertaking?

The tax treatment of distributions of earnings can be described as follows.

Distributed earnings (dividend) from a substantial shareholding (at least 5%)

in a company (belastbaar inkomen uit aanmerkelijk belang) are taxed57 at

a flat rate of 25%58. Apart from that, dividends from a substantial

shareholding in a company are also subject to the dividend withholding tax

(dividendbelasting)59 on distribution to the shareholder at a rate of 15%60

57 Article 4.12 Income Tax Act 2001 58 Article 2.12 Income Tax Act 2001 59 Article 3 paragraph 1 Dividend Tax Act 1965

Netherlands Country Report

February 2008

25

even though the profit of the corporation is taxed with corporate income

tax. Residents can get a credit for this withholding tax. The withholding tax

can be credited against the income tax due on Box 2 or Box 3 income,

whichever is relevant61.

The profit is therefore taxed twice, first at the level of the corporation and

then when distributed at the level of the individual shareholder (the so-

called classical system).

A capital gain realized by a corporation as a result of the sale of the

business will be taxed at a rate of 25,5% corporate income tax. This is the

general rate of corporate income tax62.

Capital gains realised by individuals are in general not taxed unless the

individual is a sole trader.

The most important exception being capital gains realized by individual

shareholders owning a substantial shareholding in a company. These gains

are taxed in Box 2 at a special rate of 25% income tax. If the business

owner does not hold a substantial interest in the company, the capital gain

will not be taxed immediately. However, at the end of the year, the

individual will have to declare the amount of all his belongings. If the

amount of the realised capital gain will be held at a bank-account at that

moment, these funds will be taxed at an effective rate of 1,2% in Box 363.

So, distributed earnings and capital gains are taxed at the same tax rate

(25%) in Box 2 for individual shareholders.

1.3.2 Are there different tax treatments for long-term capital gains and short-

term capital gains?

60 Article 5 Dividend Tax Act 1965 (since 2007 (25% before 2007)) 61 Article 9.2 Income Tax Act 2001 62 Article 22 Corporate Income Tax Act 1969, rate applicable since 2007 for profits above EUR 60.000 63 Article 2.13 Income Tax Act 2001

Netherlands Country Report

February 2008

26

There are no different tax treatments for long-term capital gains and short-

term capital gains: they are treated equally.

1.3.3 Are there different tax treatments for capital gain from SME business

stock and capital gain from larger companies’ business stock?

There are no different tax treatments for capital gains from SME business

stock and capital gains from larger companies´ business stock.

2 What are the main types of business entities and the main differences in

(corporate) income taxation for sole traders, general partnerships, limited

partnerships and corporation and other business entities if relevant?

The main types of business entities in The Netherlands are the corporation, the

limited partnership, the general partnership and the sole trader. In general, most

business owners choose for a corporation to run their business. Corporations can

be subdivided into companies limited by shares and private companies with limited

liability. Most businesses are run by private companies with limited liability (B.V.).

2.1 Are partnerships treated transparent for tax purposes?

Partnerships are generally treated transparent for tax purposes. As a result,

the partnership will not be liable for Income tax, the business owner is

liable for the results of the partnership. In some cases a partnership is not

treated transparent for tax purposes however. A partnership will not be

treated to be transparent in case it is an open limited partnership. A

definition of “open commanditaire vennootschap” (= open limited

partnership) is given in the Algemene Wet inzake rijksbelastingen64.

2.2 Can partnerships opt for corporate income tax?

Partnerships are transparent in case they are not open. There is no

possibility to opt for liability for corporate income tax. There is no

possibility for open partnerships to opt for transparency.

64 Article 2 paragraph 3 under c AWR

Netherlands Country Report

February 2008

27

The only way to switch between transparent or not is to change the

partnership-agreement, which may lead to tax-liability however.

2.3 Once they have opted for a regime is it easy to switch back?

As there is no possibility to opt for liability for corporate income tax, there

is no possibility to switch back to transparency. However, there is a

possibility to switch between transparent or not, by changing the

partnership-agreement, which may lead to tax-liability.

2.4 Is there a difference in this respect between general and limited

partnerships?

General partnerships are always transparent for tax purposes. Limited

partnerships are liable for corporate income tax when the partnership can

be deemed to be open65. Otherwise the limited partnership is transparent

for purposes of (corporate) income tax.

2.5 Can corporations opt to be treated tax transparent?

Corporations can not opt to be treated tax transparent. Therefore,

corporations will always be liable for corporate income tax purposes.

2.6 Once they have opted for a regime is it easy to switch back?

As there is no possibility to opt for transparency, there is no possibility to

switch back to liability for corporate income tax.

65 Article 2, paragraph 1 Corporate Income Tax Act 1969

Netherlands Country Report

February 2008

28

2.7 Are their differences in this respect between the different types of

corporations?

As there is no possibility to switch back to liability for corporate income

tax, no distinction could be made between the various types of

corporations regarding the possibility to switch back.

The Netherlands

RELEVANT TAX PROVISIONS IN 2002 AND SUBSEQUENT CHANGES UP TO 2007

Table 3 General Partnership

Limited Partnership

Corporation Sole Trader

Corporate tax

N.A. (transparant)

N.A., unless the partnership is an open partnership, article 2 paragraph 1 under a Vpb

Yes, article 2 paragraph 1 Vpb.

N.A.

Income tax Yes, article 3.2 IB and further for individuals as partner.

Yes, article 3.2 IB and further if the partnership is not an open partnership.

N.A. Yes, article 3.2 IB and further.

Capital gains tax

No special tax on capital gains. They are taxed with (corporate) income tax.

No special tax on capital gains. They are taxed with (corporate) income tax.

No special tax on capital gains. They are taxed with (corporate) income tax.

No special tax on capital gains. They are taxed with (corporate) income tax.

Option for Transparent treatment

N.A. N.A. N.A. NA.

3. Are there any special tax regimes for SMEs for (corporate) income tax

purposes?

There are no special tax regimes for SMEs for (corporate) income tax purposes.

Netherlands Country Report

February 2008

29

3.1 What are the conditions to be fulfilled in order to benefit from these

special tax regimes?

As there are no special tax regimes, this question does not have to be

answered.

3.2 Are there limits on the length of time during which these special tax

regimes are available, or other limits?

As there are no special tax regimes, this question does not have to be

answered.

4. Are there any special tax incentives, such as (re-)investment reserves or

provisions, special depreciations/capital allowances deductible for (corporate)

income tax purposes?

Dutch law gives several specific tax incentives for (corporate) income tax

purposes.

An example is the reinvestment reserve (herinvesteringsreserve), which may be

created for the replacement or repair of business assets. The reserve is available

upon the alienation, loss or damage of both tangible and intangible assets66. If the

proceeds of alienation or the amount of indemnification exceed the book value of

the asset, the excess may be placed into a reinvestment reserve if, and as long as,

the company intends to reinvest this amount. The amount placed in the reserve

must be reinvested during the year of disposal or the 3 following years, unless

special circumstances justify a longer period. If the reinvestment does not take

place within that period, the reserve must be added to the taxable income.

Other examples are the applicability of the participation exemption67 and the

possibility to request for a fiscal unity68. As a result of the participation

66 Article 3.54 Income Tax Act 2001 and Decree of 6 March 2003, CPP2002/1330 67 Article 13 Corporate Income Tax Act 1969 68 Article 15 Corporate Income Tax Act 1969

Netherlands Country Report

February 2008

30

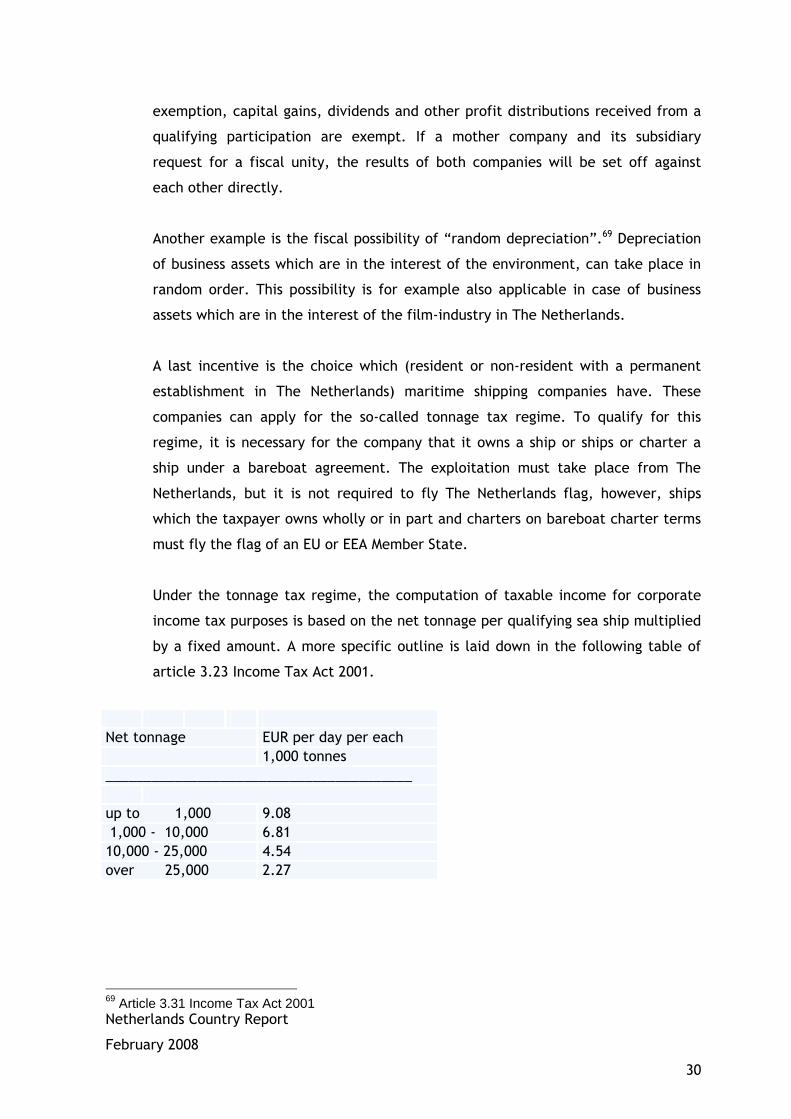

exemption, capital gains, dividends and other profit distributions received from a

qualifying participation are exempt. If a mother company and its subsidiary

request for a fiscal unity, the results of both companies will be set off against

each other directly.

Another example is the fiscal possibility of “random depreciation”.69 Depreciation

of business assets which are in the interest of the environment, can take place in

random order. This possibility is for example also applicable in case of business

assets which are in the interest of the film-industry in The Netherlands.

A last incentive is the choice which (resident or non-resident with a permanent

establishment in The Netherlands) maritime shipping companies have. These

companies can apply for the so-called tonnage tax regime. To qualify for this

regime, it is necessary for the company that it owns a ship or ships or charter a

ship under a bareboat agreement. The exploitation must take place from The

Netherlands, but it is not required to fly The Netherlands flag, however, ships

which the taxpayer owns wholly or in part and charters on bareboat charter terms

must fly the flag of an EU or EEA Member State.

Under the tonnage tax regime, the computation of taxable income for corporate

income tax purposes is based on the net tonnage per qualifying sea ship multiplied

by a fixed amount. A more specific outline is laid down in the following table of

article 3.23 Income Tax Act 2001.

Net tonnage EUR per day per each 1,000 tonnes ________________________________________ up to 1,000 9.08 1,000 - 10,000 6.81 10,000 - 25,000 4.54 over 25,000 2.27

69 Article 3.31 Income Tax Act 2001

Netherlands Country Report

February 2008

31

4.1 Do these elements of internal financing represent an important

alternative to the financing by retained earnings?

An incentive such as reinvestment reserve or the special depreciation-

possibilities does postpone a tax burden for a few years and are therefore

frequently used incentives. Retained earnings financing do not lead to a

postponement of the tax burden. Therefore, the Undertaking might prefer

internal financing to retained earnings financing.

4.2 Are there any compulsory measures in relation to the retention of

earnings (e.g. legal constraints for the distribution of profits and

dividend policy)?

An example of a compulsory measure is that a company may only pay out

dividend when it has enough free reserves70. Another compulsory measure

is that the company can only pay out dividend after the company´s

commercial balance sheet has been adopted (except interim dividends).

5 Are there any differences in the tax treatment of stock and cash dividends71?

Cash dividends will be taxed with 15% Dividend tax and 25% individual Income tax.

When the dividends will be taxed with Dutch individual Income tax, a credit will

be given for the paid Dividend tax. Stock dividends will not be taxed with

individual Income tax.

6 Have there been any changes in the tax regulation in recent years - since 2002

– that have had an important effect on the retention of earnings, the

distribution of earnings or the reinvestment of profits for a particular purpose?

There have not been any changes in the tax regulation since 2001 which had an

effect on the retention of earnings, the distribution of earnings or the

reinvestment of profits for a particular purpose. As of 2007 the Box 2 rate is

70 Article 2:216 Civil Code 71 For the Undertaking stock dividend will lead to an increased amount of share capital and a decreased amount of profit reserves. For the shareholder it means additional shares in the Undertaking which may be taxed with Dividend tax (with full tax credit).

Netherlands Country Report

February 2008

32

decreased to 22% for one year. This will probably have some impact. This year,

more payments of dividend can be expected.

7 Are there any current plans for tax reforms that have as their object to have

an impact on the retention of earnings?

Currently, there are no plans for tax reforms that have as their object to have an

impact on the retention of earnings (besides the Box 2 rate decrease to 22% in

2007 and back to 25% in 2008).

Netherlands Country Report

February 2008

33

PART 2 TAX ASPECTS OF RETAINED EARNINGS VERSUS DISTRUBITED PROFITS AND

WAGES.

8 What is the tax treatment of retained earnings compared to distribution of

earnings on the level of the Undertaking and at a combined level of

Undertaking (corporate) and business owner (individual)?

Retained earnings at the level of the business only, are treated as follows. The

earnings will be taxed with corporate income tax at a rate of 25,5% in the year

they are realised. It does not matter for how long the company will retain these

funds, they will not be taxed as long as they are not distributed.

Distributed earnings at the level of the business only, are treated as follows. The

earnings will be taxed with corporate income tax at a rate of 25,5% at the

company´s level in the year they are realised. When the company distributes these

earnings to shareholders, the company will have to withhold 15% tax (i.e.

Dividendbelasting). The tax should be withheld by the distributing company at the

moment the dividends are put at the disposal of the recipient. The distributing

company must file a tax return and pay the tax withheld to the tax authorities

within 1 month after the distribution. There is no withholding obligation if the

participation exemption regime applies. In case an individual holds the shares, the

participation exemption will of course not be applicable.

Retained earnings at the combined level of the business and the business owner

are treated as follows. The year the earnings are realised, they will be taxed with

corporate income tax. It does not matter for how long the company will retain

these funds, they will not be taxed as long as they are not distributed. In general

this will not have any consequences for the business owner.

If the business owner has a substantial interest in the company, it does not matter

that the company will retain the earnings. If the business owner does not hold at

5% or more of the shares of the company, the retaining of the earnings will have

indirect consequences for the business owner. When the company will retain the

earnings, the value of the shares (held by the business owner) will probably

increase. The business owner will have to file his tax return income tax in the

Netherlands Country Report

February 2008

34

subsequent year. In his tax return he will also have to declare the value of certain

of his possessions (including shares in companies) and liabilities. The average of

the value at the begin and the end of the year will be taxed at an effective rate of

1,2%.

Distributed earnings at the combined level of the business and the business owner

are treated as follows. The year the earnings are realised, they will be taxed with

corporate income tax at a rate of 25,5% at the level of the business. When the

company will distribute the earnings, the company will have to withhold 15%

Dividend tax. The tax should be withheld by the distributing company at the

moment the dividends are put at the disposal of the recipient. The distributing

company must file a tax return and pay the tax withheld to the tax authorities

within 1 month of the distribution. The business owner will be liable for income

tax at a rate of 25% for the dividend received, if he holds a substantial interest in

the corporation. For residents the withholding tax is creditable against the income

tax due on box 2 or box 3 income whichever is relevant.

When the business owner does not have a substantial interest in the business, the

only difference is that the dividend will not be taxed at a rate of 25%, but the net

value of his shares will be taxed effectively at a rate of 1,2%.

8.1 Is there an economic double taxation of distribution of earnings

(taxation of Undertaking income and then taxation on the distribution

of earnings at the Undertaking level or at the business owner level)?

When the company realises a profit, the company will have to pay

corporate income tax. After the distribution of the earning/profit, the

business owner will have to pay individual income tax as well. Therefore,

the distributed earnings are taxed double (the so-called “classical

system”).

Netherlands Country Report

February 2008

35

The Netherlands

Table 4 Undertaking Individual Business owner

Corporate tax

Yes, article 8 Vpb (25,5%)

No

Income tax No Yes, article 4.12 IB

Dividend tax Yes, article 2 DB (15% as of 2007)

No

Dividend credit

No, full credit for the business owner

Yes, article 9.2 IB (full credit)

Capital gains tax

N.A. N.A.

If option for Transparent treatment chosen

N.A. N.A.

Case study (rough figures): I. Profit earned by “corporation”

Profit 100 Corporate income tax (25,5%) 25,5 Result after CIT 74,5 Dividend 74,5 Income tax (25%), normal rate 18,625 Result after taxes 55.875

II. Profit earned by “sole trader”

Profit 100 Exemption 10 Taxable result 90 Income tax (52%) 46,8 Result after Income Tax 43,2

From this case study above follows that the result in case the corporation

will have a result of 100, the result after dividend and taxes which the sole

shareholder is entitled to is 55,875. In case the business owner is a sole

Netherlands Country Report

February 2008

36

trader, the taxes are of an amount of 46,8 (after an exemption of 1072).

Therefore the net-result will be 53,2, which is lower than when the

business was run by a corporation.

9 Please describe the differences in the tax treatment of distribution of earnings

realised as a capital gain in the context of a sale of the shares or of the

business compared to that (i) of retained earnings, (ii) of wages paid to the

business owner and (iii) of a loan granted by the Undertaking to the business

owner?

A capital gain as a result of a sale of shares by the business owner, will be taxed at

a rate of 25%, assumed that the business owner has a substantial interest in the

business. Otherwise the capital gain will be taxed via Box 3.

A capital gain when selling the business by the company itself, will be taxed at a

rate of 25,5%, the current rate for the corporate income tax.

A salary paid by the company to the business owner will be taxed at a maximum