strategy update - talktalk group · strategy update 26 july 2012 1 . chairman 2 . chief executive 3...

TRANSCRIPT

A brighter place for everyone

Strategy Update

26 July 2012

1

Chairman

2

Chief Executive

3

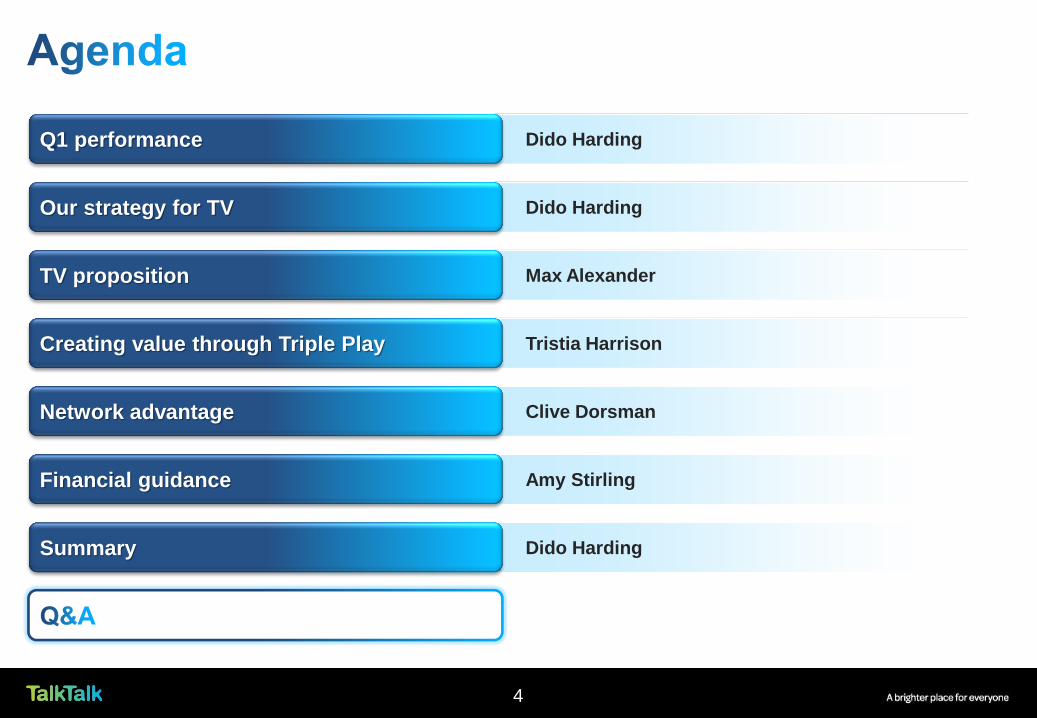

Dido Harding

Dido Harding

Max Alexander

Clive Dorsman

Amy Stirling

Q1 performance

Our strategy for TV

TV proposition

Network advantage

Financial guidance

4

Dido Harding Summary

Tristia Harrison Creating value through Triple Play

10% growth year-on-year in fully unbundled customers

Strong take-up of Plus, +66,000 in Q1, 30% of On-net base

Positive net adds in June; -19,000 in Q1 overall

Continued improvement in On-net churn 1.6% (Q4 FY12 1.7%)

9% growth in On-net revenue; 5% growth in On-net ARPU

Corporate revenue up 4% year on year to £80m

5

13.3

10.6

8.3 8.1

3.8 3.4

H1 11 H2 11 H1 12 H2 12 Q4 12 Q1 13

Call volumes

13,400 14,400

7,900 7,600

3,708 2,671

H1 11 H2 11 H1 12 H2 12 Q4 12 Q1 13

Complaints to Ofcom

1.7% 1.6%

Q4 12 Q1 13

Continued improvement in On-net churn

Churn will to continue to reduce:

• Better customer experience

• Triple Play

• Will report On-net churn quarterly

6

A brighter place for everyone

Our Strategy for TV

7

Low cost

operating model

Network

Advantage Quad-Play

B2B

services

Fibre

future

Expand Margin Grow Revenue

Lower costs

better experience

Expand by

up to 100x

Lower Churn

Higher APRU

Growing revenue

value creating

products

Future proof

service delivery

8

9

Unlimited Broadband and Phone

Unlimited download allowance

Free wireless router

Homesafe + Super safe boost

Unlimited calls to UK landlines

Extraordinary TV

7 day catch up

All your favourite Freeview channels

Huge library of films and shows

Live Sky Sports + Movies - add a month at a time

Source: TalkTalk management data, TalkTalk Omnibus (Pay TV ARPU data), OC&C analysis

10

7.0m Pay TV

Lovers

6.5m Mismatched

3.5m Rejectors

1.5m Dis-

interested

5.0m Pay TV

Wannabees

2.5m Price-

Aware

11

12

Q1 Q2 Q3 Beyond

Simplified

service footprint

Last 12 months

Detailed

process mapping

Developed box

Experienced field

engineering team

Enabled network

Trialing processes

Testing and

de-bugging box

Developing training

Building website

In home trials

Dedicated TV

service team

Pre-registration for Plus

customers only

All customers require

engineers visit

Training of all agents

before selling starts

Start booking install

dates in 6-8 weeks time

Above the line

advertising from

YouView and TalkTalk

Gradual build up

of sales

Self install option

Proposition for

Essentials

Ongoing product

development

BBC, ITV, Channel 4 and Channel 5 content builds confidence in YouView

- a substantial upgrade from Freeview

Comprehensive, flexible pay content gets people started on pay journey

Compelling wholesale agreements with multiple content partners

- Sky, Amazon, UKTV and many others

Network and billing platform provide easy access to customers for

content owners

A market place for content NOT a content rights owner

13

Director of TV

14

15

Sky Virgin Media BT Vision

Freeview,

YouView,

LoveFilm,

Unlimited calls & BB

Sky Entertainment, Sky

Broadband Everyday Lite &

Sky Talk Freetime

30Mb, TV M+,

Talk Weekends,

VHD box

TV Essential + Broadband

and Evening & Weekend

Calls

Inclusive content Freeview, BBC iPlayer, ITV

Player, 4oD, Demand 5

Freesat, Entertainment

Pack (40 channels)

M+ (75 channels,

6 HD channels),

BBC iPlayer, ITV Player,

4oD, Demand 5

Freeview, BBC iPlayer,

ITV Player, 4oD,

Demand 5

Additional functionality Backwards EPG,

Unified search

Anytime+ (VoD)

Sky Go (multiscreen) Anytime+ -

Inclusive TV Hardware YouView PVR Sky+ (PVR) VHD Box Vision+ (PVR)

Downloads Unlimited downloads 2GB Unlimited 10GB

Inclusive calls Anytime Evenings & Weekends Weekend only Evenings & Weekends

Plus

Entry level Triple Play today

16

17

Sky Virgin Media BT Vision

Freeview,

YouView,

LoveFilm,

Unlimited calls & BB

Sky Entertainment, Sky

Broadband Everyday

Lite & Sky Talk Freetime

30Mb, TV M+,

Talk Weekends,

VHD box

TV Essential +

Broadband and Evening

& Weekend Calls

Triple Play price £14.50 £21.50 £20.00 £17.00

Full / Value line rental £9.50 £9.95 £13.90 £10.75

Monthly cost (incl LR )

£24.00 £31.45 £33.90 £27.75

Up front cost £50.00 £2.18 - £46.95

18 months £482.00 £568.28 £610.20 £546.45

Plus

18

19

TV Starter

Boost Kids Boost

Music

Boost

Sky 1

Sky 2

Sky Living

Sky LivingIT

Sky Arts 1

Sky Arts 2

Sky Sports

News

Nickelodeon,

Nick Jnr,

Nick Toons

Cartoon

Network

Disney

Channel

Disney Jnr

Disney XD

Boomerang

Scamp (OD)

The Box

Channels

(x6)

Music OD

MTV Hits

MTV Base

MTV Classic

MTV Music

MTV Rocks

MTV Dance

Entertainment Boost

Sky 1

Sky 2

Sky Living

Sky LivingIT

Sky Arts 1

Sky Arts 2

Sky Sports

News

G.O.L.D

Watch

Alibi

Home

Eden

Blighty

Good Food

Sy-Fy

Universal

FX

E!

Comedy

Central

Comedy

Central Extra

MTV

Discovery

Channel

Nat Geo

Discovery RT

Discovery H &

H

Animal Planet

TCM

Entertainment Extra Boost

Sky 1

Sky 2

Sky Living

Sky LivingIT

Sky Arts 1

Sky Arts 2

Sky Sports News

G.O.L.D

Watch

Alibi

Home

Eden

Blighty

Good Food

The Box x 6

Music OD

MTV Hits

The Box

Channels (x6)

Music OD

MTV Hits

MTV Base

MTV Classic

MTV Music

MTV Rocks

MTV Dance

Sy-Fy

Universal

FX

E!

Comedy Central

Comedy Central

Extra

MTV

Discovery

Channel

Nat Geo

Discovery Real

Time

Discovery H & H

Animal Planet

TCM

Nickleodeon

Nick Jr

Nick Toons

Cartoon Network

Disney Channel

Disney Jnr

Disney XD

Boomerang

Scamp OD

20

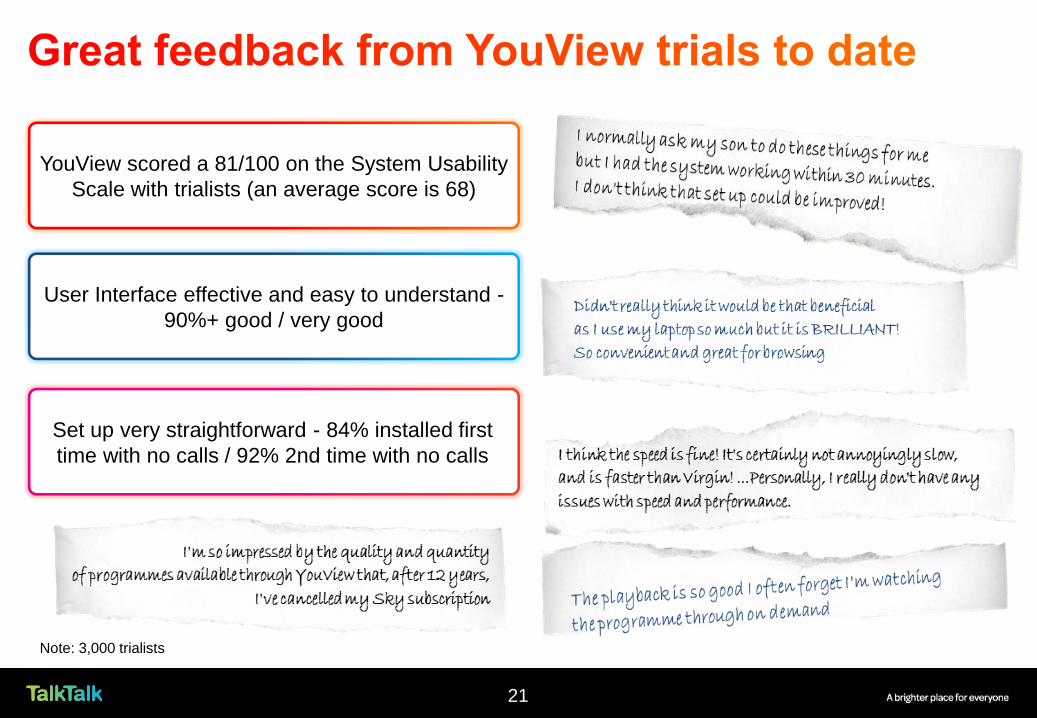

YouView scored a 81/100 on the System Usability

Scale with trialists (an average score is 68)

User Interface effective and easy to understand -

90%+ good / very good

Set up very straightforward - 84% installed first

time with no calls / 92% 2nd time with no calls

Note: 3,000 trialists

21

Consumer Commercial Director

22

23

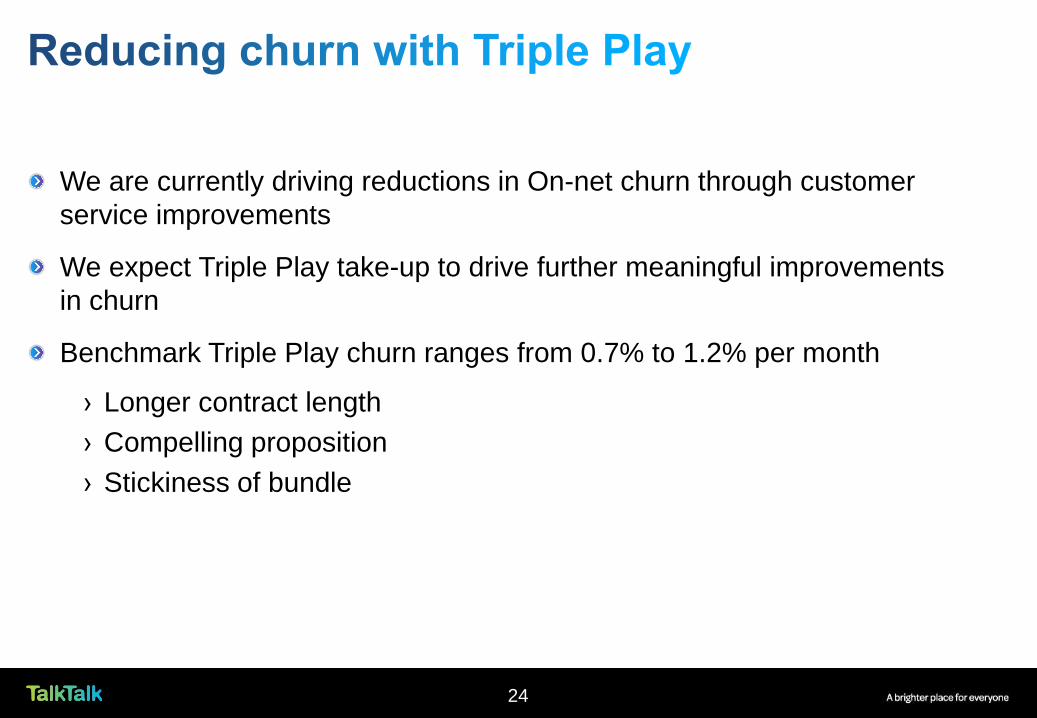

We are currently driving reductions in On-net churn through customer

service improvements

We expect Triple Play take-up to drive further meaningful improvements

in churn

Benchmark Triple Play churn ranges from 0.7% to 1.2% per month

› Longer contract length

› Compelling proposition

› Stickiness of bundle

24

Compelling proposition will drive demand at lower cost

5m homes in the UK currently have no broadband connection

› IPTV will stimulate broadband take-up for access to affordable pay TV

› YouView is expected to drive broadband take-up by 0.5m - 1.0m

› Our unbundled footprint (93% of UK) and compelling value proposition

will allow us to take a disproportionate share of this market

25

Improving Plus mix drives ARPU from launch

Assuming minimal contribution from Pay TV on launch

Our proposition allows customers to explore paid for content

Any take-up of Pay content will be incremental for us

No back-book to defend

Over time TV scale will provide content leverage

26

All customers benefit from lower churn - extends customer life

Essentials to Plus increases monthly contribution by £3 per month

Minimal pay margin assumed in contract payback - value upside

Every Triple Play customer is more valuable than a Dual Play customer

27

Incremental value Contract

length

Incremental

investment

New Triple Play acquisition £140 18 Yes

Essentials to Plus £140 18 Yes

Plus to Plus TV £140 24 Yes

Pay back

in contract

Note: Estimated

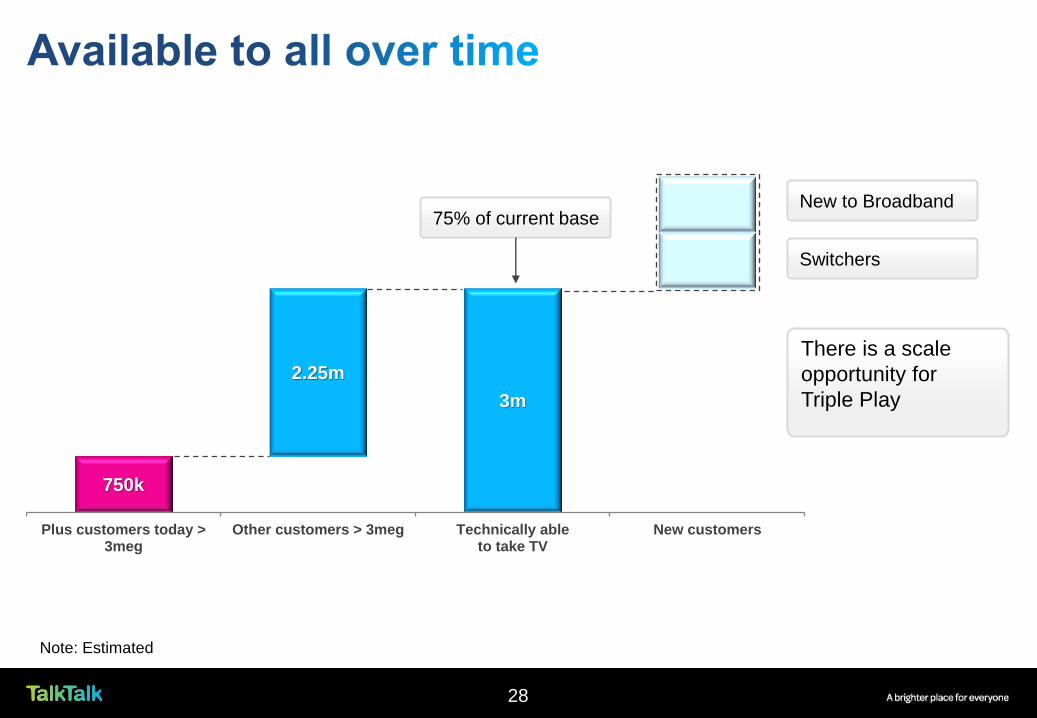

28

750k

3m

2.25m

Plus customers today >3meg

Other customers > 3meg Technically ableto take TV

New customers

There is a scale

opportunity for

Triple Play

New to Broadband

Switchers

75% of current base

Chief Technology Officer

29

30

Collector

Node

Copper

Fibre

Exchange Backhaul

1Gbps optical circuit

supplied by BTOR

or VM

Unbundled Exchange

MSAN & DSLAM

Collector Node to

extend reach

of Core Network

Collector Ring

10Gbps optical circuit or

dark fibre supplied by BTW,

SSE, GEO, VM

and Eirecom

Core Optical Network

2 separate national DWDW

networks with 8Tbps (Huawei) and

1,6Tbps (Infinera) capacity

• 93% of the population

covered provides for

efficient provision

• Dark Fibre in our collector

rings – providing for

unlimited capacity going

forward

• CDN - Delivering content

closer to the edge

(Google, YouTube etc.)

• Traffic prioritisation

(Business, TV, etc.)

• Content Delivery Network

• Allows for flexibility and

rapid growth

• Depth in service portfolio

(Business & Consumer)

• For Consumer;

Broadband, Phone, TV,

Mobile

• For Business; Business

Grade Broadband,

Ethernet, Voice, Managed

Services, ISDN

• Homesafe

31

32

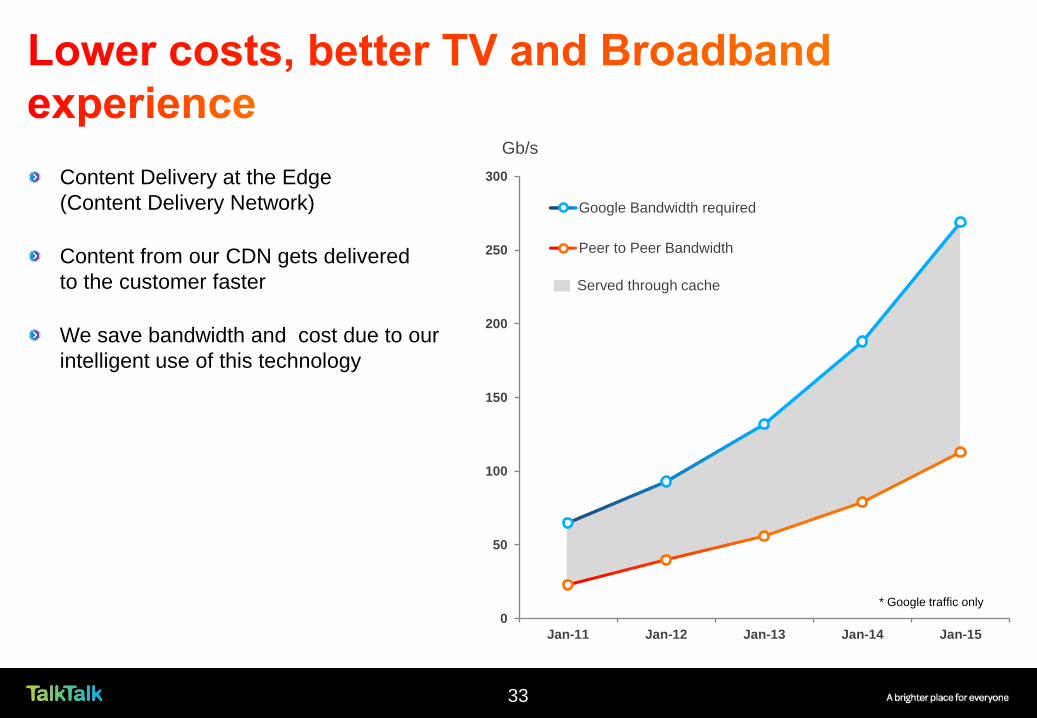

Served through cache

0

50

100

150

200

250

300

Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

Google Bandwidth required

Peer to Peer Bandwidth

Content Delivery at the Edge

(Content Delivery Network)

Content from our CDN gets delivered

to the customer faster

We save bandwidth and cost due to our

intelligent use of this technology

Gb/s

* Google traffic only

33

Over the next 5-10 years, we will

increase our capacity by between

50-100 times within 6% capex ratio

Delivering technology for the future:

solid foundation of Huawei (3.2Tbs)

& Infinera (1.6Tbs).

Trialing next generation of

Transmission (8Tbs with 100gbs

per lambda)

Investing in new Technologies

(Industry's First Programmable 2T

WDM Prototype (Huawei), SDH

replacements, Juniper next gen:

MX 20/20’s, IMS etc.)

0

5,000

10,000

15,000

20,000

25,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Source: Farncombe analysis,

TalkTalk forecasts

Busy Hour Total traffic

(Gbps)

x30

x44

Note: All traffic types are assumed at Access level. Other & Business

traffic for 2015, 2016 are extrapolated based on TalkTalk’s forecasts

x17

x100

34

Chief Financial Officer

35

Dividend growth minimum 15% - confidence in growth and cash generation

Revenue

Operating Expenses

EBITDA margin

Exceptionals

Capex 6% sales

Minimal cash

20 – 21 %

Broadly flat

Return to growth Growth H2 weighted

Network investment

H1 weighted

H2 weighted

Outflow in H1

Inflow in H2

Investment

H2 weighted

H1 / H2 phasing

36

Guidance excludes investment in TV (variable SAC & marketing)

Trial and project costs

Promotional content

Scaling engineers

Above the line marketing

Set top box

Peripherals

Engineer visit

37

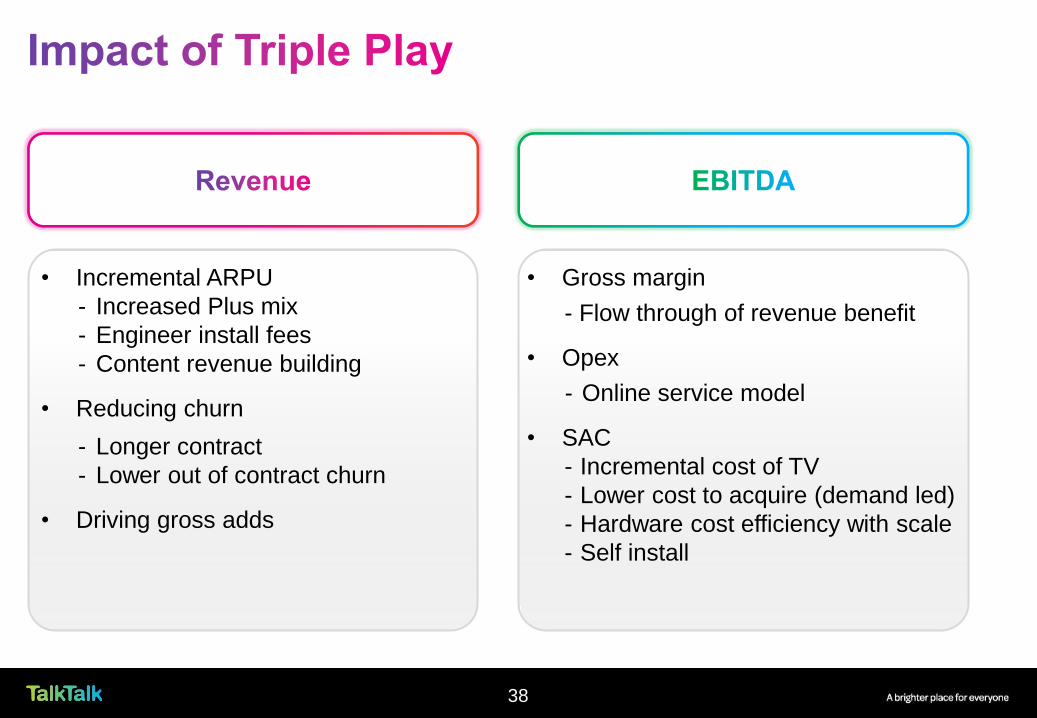

• Incremental ARPU

- Increased Plus mix

- Engineer install fees

- Content revenue building

• Reducing churn

- Longer contract

- Lower out of contract churn

• Driving gross adds

• Gross margin

- Flow through of revenue benefit

• Opex

- Online service model

• SAC

- Incremental cost of TV

- Lower cost to acquire (demand led)

- Hardware cost efficiency with scale

- Self install

38

Chief Executive

39

The best value Triple Play proposition in the market

› Free box, no additional subscription, rich content

Compelling economics

› In-contract payback Incremental contribution

› Significantly lower churn thereafter Lower SAC costs

Longer term growth driver

› ARPU

› Broadband market share

Firmly underpins our medium term targets of 2% CAGR revenue

& 25% EBITDA margin

40

A brighter place for everyone

Q&A

41

A brighter place for everyone

Appendices

42

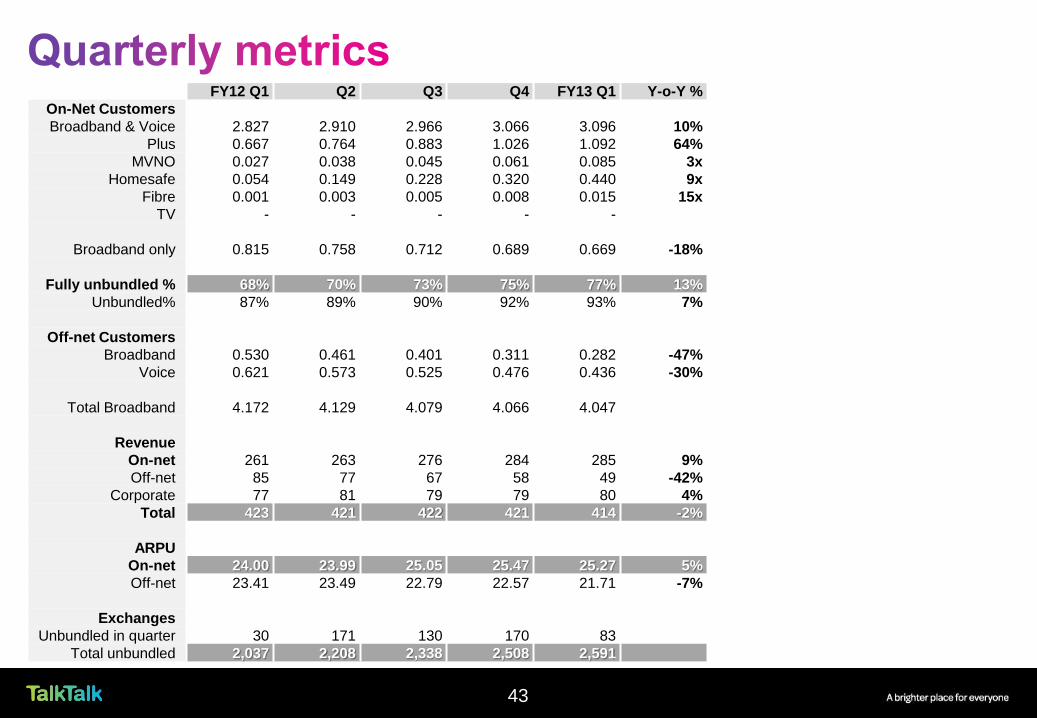

43

FY12 Q1 Q2 Q3 Q4 FY13 Q1 Y-o-Y %

On-Net Customers

Broadband & Voice 2.827 2.910 2.966 3.066 3.096 10%

Plus 0.667 0.764 0.883 1.026 1.092 64%

MVNO 0.027 0.038 0.045 0.061 0.085 3x

Homesafe 0.054 0.149 0.228 0.320 0.440 9x

Fibre 0.001 0.003 0.005 0.008 0.015 15x

TV - - - - -

Broadband only 0.815 0.758 0.712 0.689 0.669 -18%

Fully unbundled % 68% 70% 73% 75% 77% 13%

Unbundled% 87% 89% 90% 92% 93% 7%

Off-net Customers

Broadband 0.530 0.461 0.401 0.311 0.282 -47%

Voice 0.621 0.573 0.525 0.476 0.436 -30%

Total Broadband 4.172 4.129 4.079 4.066 4.047

Revenue

On-net 261 263 276 284 285 9%

Off-net 85 77 67 58 49 -42%

Corporate 77 81 79 79 80 4%

Total 423 421 422 421 414 -2%

ARPU

On-net 24.00 23.99 25.05 25.47 25.27 5%

Off-net 23.41 23.49 22.79 22.57 21.71 -7%

Exchanges

Unbundled in quarter 30 171 130 170 83

Total unbundled 2,037 2,208 2,338 2,508 2,591

A brighter place for everyone

Strategy Update

26 July 2012

44