strategic direction - telenor · pdf filean increasingly global and digital world ......

TRANSCRIPT

STRATEGIC DIRECTION Sigve Brekke, Group CEO

CMD 2017

TELENOR IS COMING FROM A STRONG POSITION

2

• A diversified portfolio with strong market

positions in Europe and Asia

• Strong operations based on quality

networks and mass-market distribution

capabilities

• Majority ownership enabling strong

governance and global scale benefits

• Growth above peers, with solid profitability

in most markets

Scandinavia

Central &

Eastern Europe

Emerging Asia Mature Asia

CUSTOMERS

214 million mobile

subscribers

MARKET POSITION

#1 or #2 in 12 of 13

markets

CMD 2017

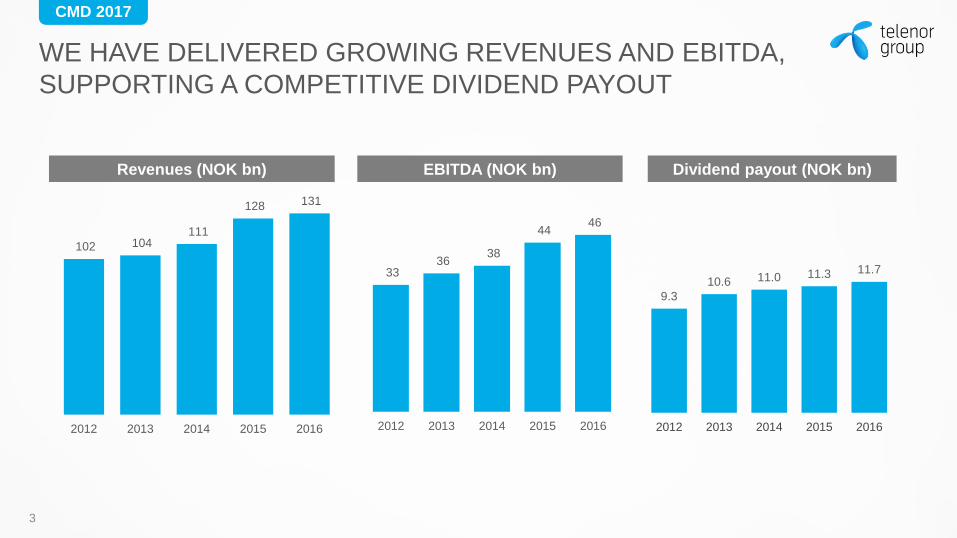

WE HAVE DELIVERED GROWING REVENUES AND EBITDA,

SUPPORTING A COMPETITIVE DIVIDEND PAYOUT

3

Revenues (NOK bn)

102 104 111

128 131

2012 2013 2014 2015 2016

EBITDA (NOK bn)

33 36

38

44 46

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2012 2013 2014 2015 2016

Dividend payout (NOK bn)

9.3

10.6 11.0 11.3 11.7

2012 2013 2014 2015 2016

CMD 2017

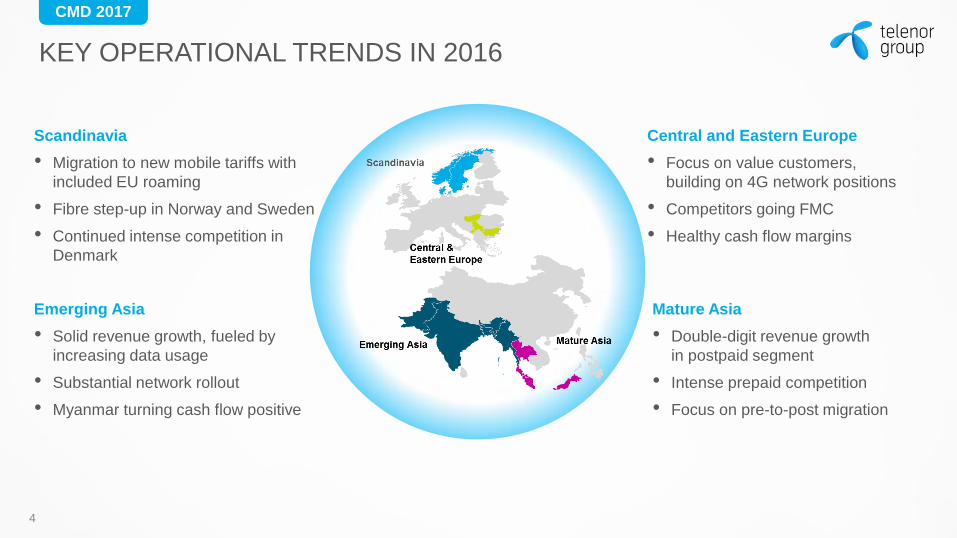

KEY OPERATIONAL TRENDS IN 2016

Scandinavia

• Migration to new mobile tariffs with

included EU roaming

• Fibre step-up in Norway and Sweden

• Continued intense competition in

Denmark

4

Emerging Asia

• Solid revenue growth, fueled by

increasing data usage

• Substantial network rollout

• Myanmar turning cash flow positive

Central and Eastern Europe

• Focus on value customers,

building on 4G network positions

• Competitors going FMC

• Healthy cash flow margins

Mature Asia

• Double-digit revenue growth

in postpaid segment

• Intense prepaid competition

• Focus on pre-to-post migration

CMD 2017

AN INCREASINGLY GLOBAL AND DIGITAL WORLD

REPRESENTS NEW OPPORTUNITIES

5

• Global operating models for products,

network and IT

• Digital customer interactions

• Improved customer insight through

multiple digital touchpoints

• Software defined networks and

cloud-based IT platforms

• Growth opportunities in digital areas

adjacent to core telecom business

MORE SIMILAR THAN DIFFERENT

DIGITAL BEHAVIOR CONNECTED WORLD

CMD 2017

STRATEGIC DIRECTION TOWARDS 2020

Strategic direction

• Capture growth opportunities

• Step up efficiency measures through

digitizing core and leveraging scale

• Ensure a responsible business conduct

Value creation for shareholders

• Focus on cash flow generation

• Prioritization to secure healthy returns

• Year-on-year growth in dividend

6

7

GROWTH EFFICIENCY PRIORITIZATION

KEY DRIVERS FOR VALUE CREATION TOWARDS 2020

8

GROWTH EFFICIENCY PRIORITIZATION

KEY DRIVERS FOR VALUE CREATION TOWARDS 2020

CMD 2017

POTENTIAL FOR CONTINUED MOBILE REVENUE GROWTH

9

Increasing real mobile penetration Increasing data usage More affordable smartphones

230

150

60 40 33

7%

17%

22%

25%

2012 2013 2014 2015 2016

Bangladesh: Smartphone price (USD)

37%

51%

44%

52%

2012 2016

Bangladesh

Pakistan

228 218

244 257

280

61 156

319

503

801

2012 2013 2014 2015 2016

Norway: Domestic ARPU (NOK)Norway: Median usage (MB/month)Bangladesh: Smartphone penetration (%)

CMD 2017

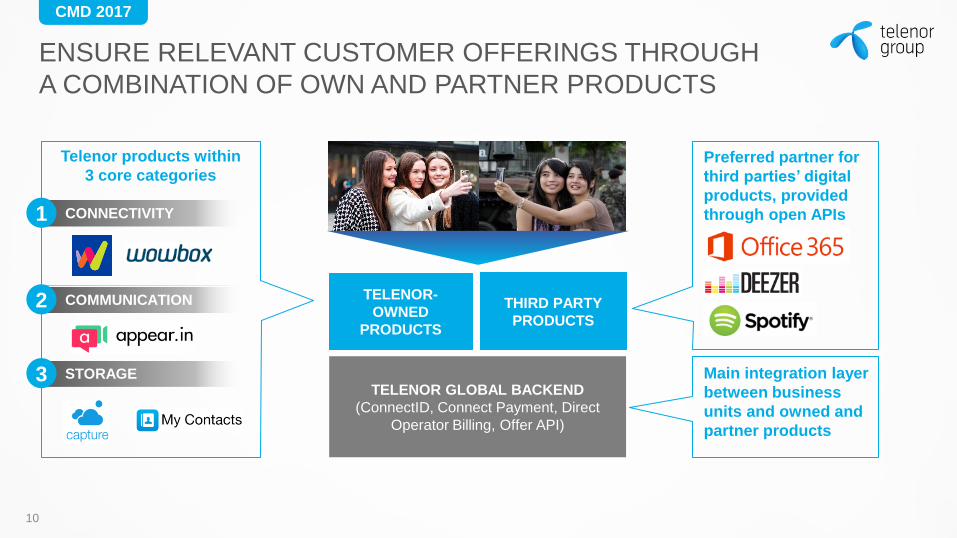

ENSURE RELEVANT CUSTOMER OFFERINGS THROUGH

A COMBINATION OF OWN AND PARTNER PRODUCTS

10

Telenor products within

3 core categories

TELENOR-

OWNED

PRODUCTS

THIRD PARTY

PRODUCTS

CONNECTIVITY

Preferred partner for

third parties’ digital

products, provided

through open APIs

1

Main integration layer

between business

units and owned and

partner products

TELENOR GLOBAL BACKEND

(ConnectID, Connect Payment, Direct

Operator Billing, Offer API)

COMMUNICATION 2

STORAGE 3

STRENGTHEN FIBRE POSITIONS IN NORWAY AND SWEDEN

Fibre footprint (m homes) and market share (%)

0.3

2.0

0.8

2.8

19%

26%

• Rapid growth in fibre in both Norway and

Sweden towards 2020

• Stepping-up fibre rollout to strengthen

market positions

• Solid fibre business cases in both markets,

with 5-6 years payback in both markets

• Exploring FMC opportunities

2016 2020 2020 2016

Telenor Norway Telenor Sweden

11

CMD 2017

EXPLORE EARLY POSITIONS ON FIBRE IN EMERGING ASIA,

UTILIZING EXISTING MOBILE INFRASTRUCTURE

Strong rationale to take early positions:

• Low and fragmented fixed line penetration

• Growing urban middle class

• Leverage on fibre access to buildings for

roof-top base stations

Fibre pilots launched in Myanmar:

• Ambition to roll out in 3 major cities in 2017

and 8 cities by 2020

• Estimated total market size of around USD 250

million in 2020

12

CMD 2017

SELECTED ADJACENT DIGITAL AREAS TO DRIVE GROWTH

AND SUPPORT CORE TELCO BUSINESS

13

• Stand-alone growth area with

churn-prevention effect on core

business

• #1 position in Pakistan through

Easypaisa and Tameer Bank

• Launched services in Myanmar in

2016, aiming for #1 position

• Potential digital sales channel for

mobile services

• Positions in Asia and LatAm

through JVs with Schibsted,

Naspers and SPH

• Aiming to strengthen position in

South East Asia

• Closely linked to core enterprise

segment in Scandinavia

• Building on strong IoT and

enterprise position in Norway

• Telenor Connexion well

positioned within fleet

management and tracking

Relevante bilder til illustrasjon? Relevante bilder til illustrasjon?

Mobile financial services Online classifieds Internet of Things

14

GROWTH EFFICIENCY PRIORITIZATION

KEY DRIVERS FOR VALUE CREATION TOWARDS 2020

CMD 2017

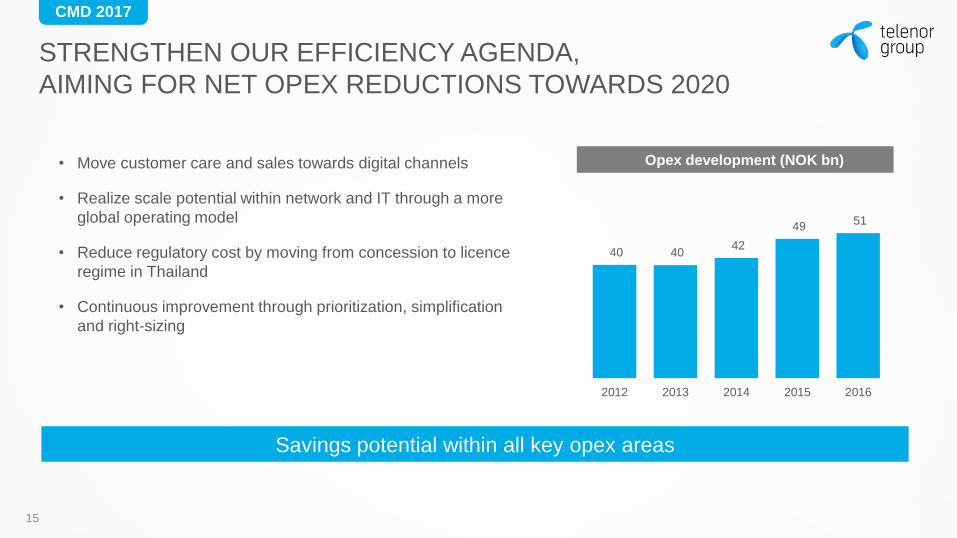

STRENGTHEN OUR EFFICIENCY AGENDA,

AIMING FOR NET OPEX REDUCTIONS TOWARDS 2020

15

• Move customer care and sales towards digital channels

• Realize scale potential within network and IT through a more

global operating model

• Reduce regulatory cost by moving from concession to licence

regime in Thailand

• Continuous improvement through prioritization, simplification

and right-sizing

Opex development (NOK bn)

40 40 42

49 51

2012 2013 2014 2015 2016

Savings potential within all key opex areas

CMD 2017

CUSTOMER CARE AND SALES WILL MOVE TO DIGITAL

CHANNELS, PROVIDING SIGNIFICANT COST EFFICIENCIES

• Shift over 300 million calls to digital self-care,

aiming for 80% reduction in calls by 2020

• Establish the MyTelenor app as the primary digital

care channel in all business units

16

Digital customer care Digital sales and marketing

• Reduce commissions by moving transactions

from physical point-of-sales to digital channels

• Increase efficiency in remaining physical

distribution through digitizing interactions with

retailers and customers

CMD 2017

ADVANCED ANALYTICS WILL BE KEY CAPABILITY TO REACH

GROWTH AND EFFICIENCY AMBITIONS

17

Ow

n &

op

er.

2n

d/3

rd p

art

y

Own digital verticals

Own services

Integrated partner services

Open ad eco-system

Aggregated inventory

Audience creation

Decision modeling Attribution

Media execution

Identity

Aggregated data

CMD 2017

REALIZE SCALE POTENTIAL

WITHIN NETWORK AND IT

18

IT

• Launch global/regional IT operating model in Asia &

Europe

• Standardize and virtualize IT applications

• Establish API gateway in all business units

Network

• Launch global / regional network operating model

• Software defined networks

• Improved asset efficiency through better asset

utilization and adoption of new technologies

• Capex efficiency through standardized,

shared/common solutions

19

GROWTH EFFICIENCY PRIORITIZATION

KEY DRIVERS FOR VALUE CREATION TOWARDS 2020

CMD 2017

TAKING STEPS TOWARDS A MORE

SIMPLIFIED PORTFOLIO

• VimpelCom exit commenced in 2016

• No further capital to be allocated to India

• Review of less strategic assets

• Selective and disciplined M&A, focused on

strengthening core positions and capabilities

20

CMD 2017

STRATEGY AND EXECUTION:

FOCUS ON DIGITIZING CORE BUSINESS

DIGITIZING

THE CORE

PRODUCTS

SUPPORTING

OUR TELCO

OFFERING

NEW DIGITAL

BUSINESSES

21

CMD 2017

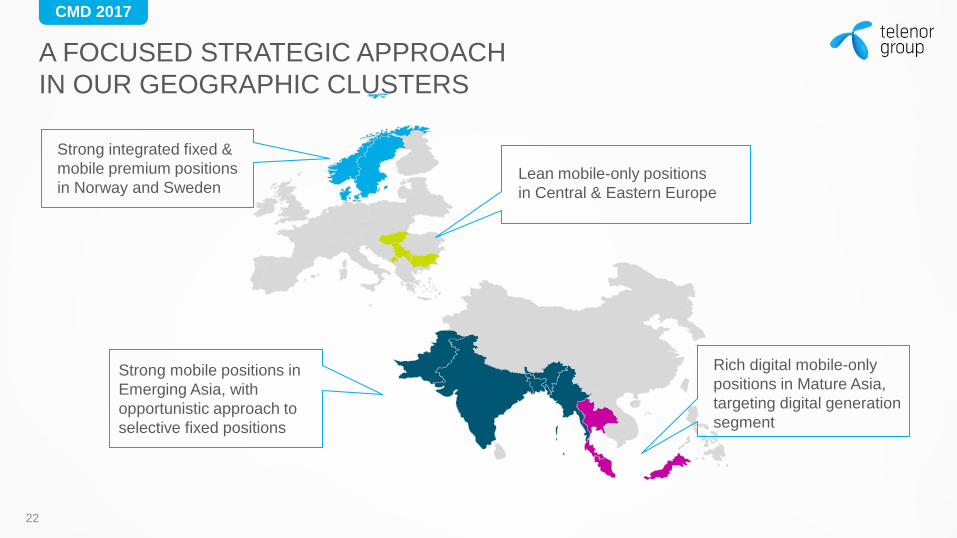

A FOCUSED STRATEGIC APPROACH

IN OUR GEOGRAPHIC CLUSTERS

22

Strong integrated fixed &

mobile premium positions

in Norway and Sweden

Strong mobile positions in

Emerging Asia, with

opportunistic approach to

selective fixed positions

Lean mobile-only positions

in Central & Eastern Europe

Rich digital mobile-only

positions in Mature Asia,

targeting digital generation

segment

CMD 2017

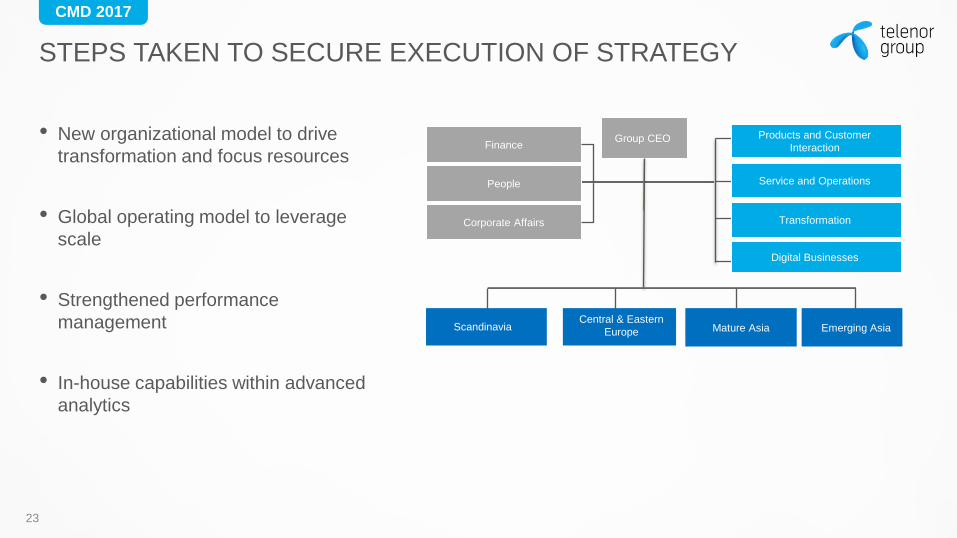

STEPS TAKEN TO SECURE EXECUTION OF STRATEGY

• New organizational model to drive

transformation and focus resources

• Global operating model to leverage

scale

• Strengthened performance

management

• In-house capabilities within advanced

analytics

23

Finance

People

Corporate Affairs

Group CEO

Emerging Asia Mature Asia Central & Eastern

Europe Scandinavia

Service and Operations

Products and Customer

Interaction

Digital Businesses

Transformation

CMD 2017

• Continued revenue growth and increased cost

efficiency, driven by digitizing core business

• Focus on simplification and prioritization of resources

• Building a solid foundation for continued value

creation for our shareholders

24

VALUE CREATION TOWARDS 2020

STRATEGIC DIRECTION Sigve Brekke, Group CEO