strategic analysis and corporate valuation of ic...

TRANSCRIPT

Master thesis

Authors:

MSc. Finance and International Business

Tural Ismayilov

MSc. Finance

Vladlens Proskurovs

Academic supervisor:

Baran Siyahhan

Strategic Analysis and Corporate Valuation

of IC Companys A/S

1st November 2012

Aarhus School of Business and Social Sciences

Aarhus University

Page 2 of 157

Executive summary

In order to make comprehensive corporate valuation of targeted IC Companys A/S in

the first part of the thesis is performed thorough strategic analysis. Then the second part

mainly deals with various corporate valuation theories and models.

IC Companys has been formed in the merger of Carly Gry International A/S and

InWear Group A/S in 2001. Since that the company has been concentrating on being the

best developer of sports and fashion brands in the apparel industry in different markets

worldwide. Through the last 10 years IC Companys has grown mainly relying on

Merger & Acquisitions and the geographical expansion achieved by operating own

shops and franchising. Currently IC Companys has 11various upper-mid and middle

class brands in the apparel market and a successful implementation of the multi-brand

strategy permits the Group to create more value.

The strategic analysis conducted in this paper mainly divided into two groups - external

and internal analyses. External analysis includes PESTEL and Porter’s five forces where

the first defines macro factors that influence the company’s business, and then Porter’s

five forces determines industry criteria and intensity. While external analysis identifies a

company’s threats and opportunities, internal analysis defines the company’s strengths

and weaknesses through the implementation of Porter’s value chain and Core

competences. The sum-up of strengths, weaknesses, opportunities and threats is done in

SWOT analysis.

The second part of the thesis consists of main and supportive valuation tools. The main

valuation model in this paper is considered to be discounted cash flow which is

accompanied with the sensitivity and scenario analyses. As a part of weighted average

cost of capital, cost of equity is calculated according to the CAPM model.

Then in order to verify results that are derived from DCF model, economic profit model

has been applied. Following these models, real option valuation is implemented to

reveal additional value to the company’s underlying assets. In real option valuation

expansion option is used in the Brazilian.

Finally, multiples analysis is applied with the aim to evaluate whether the results

obtained from the DCF and real option valuation are reasonable.

Page 3 of 157

Table of Contents Executive summary ..................................................................................................................... 2

1. Introduction ............................................................................................................................ 6

2. Problem statement ................................................................................................................. 7

3. Delimitations ........................................................................................................................... 8

4. Description of IC Companys ................................................................................................. 8

4.1 Introduction ................................................................................................................... 8

4.2 History ........................................................................................................................... 8

4.3 Merger ........................................................................................................................... 9

4.4 IC Companys A/S .......................................................................................................... 9

4.5 Products ...................................................................................................................... 11

4.6 Distribution channels .................................................................................................. 11

4.7 Markets ........................................................................................................................ 12

5. Strategic analysis .................................................................................................................. 14

5.1 PESTEL Analysis ...................................................................................................... 15

5.1.1 Political and Legal Factors ................................................................................. 15

5.1.2 Economic Factors ............................................................................................... 16

5.1.3 Socio-cultural Factors ......................................................................................... 19

5.1.4 Technological and Environmental Factors ......................................................... 20

5.2 Porter's five forces ..................................................................................................... 22

5.2.1 The threat of the new entrants ............................................................................. 23

5.2.2 Bargaining power of the suppliers ...................................................................... 24

5.2.3 Bargaining power of buyers ................................................................................ 25

5.2.4 Threat of Substitute products and services .......................................................... 26

5.2.5 Competition among the existing rivals ................................................................ 26

5.3 Internal analysis ........................................................................................................ 28

5.3.1 Primary activities ................................................................................................ 30

5.3.2 Supportive activities ............................................................................................ 33

5.4 Core Competencies .................................................................................................... 36

5.5 Growth Strategy ........................................................................................................ 37

5.5.1 Cost leadership .................................................................................................... 38

5.5.2 Differentiation ..................................................................................................... 38

5.5.3 Focus ................................................................................................................... 39

5.6 SWOT analysis .......................................................................................................... 41

Page 4 of 157

5.7 Expansion Strategy ................................................................................................... 43

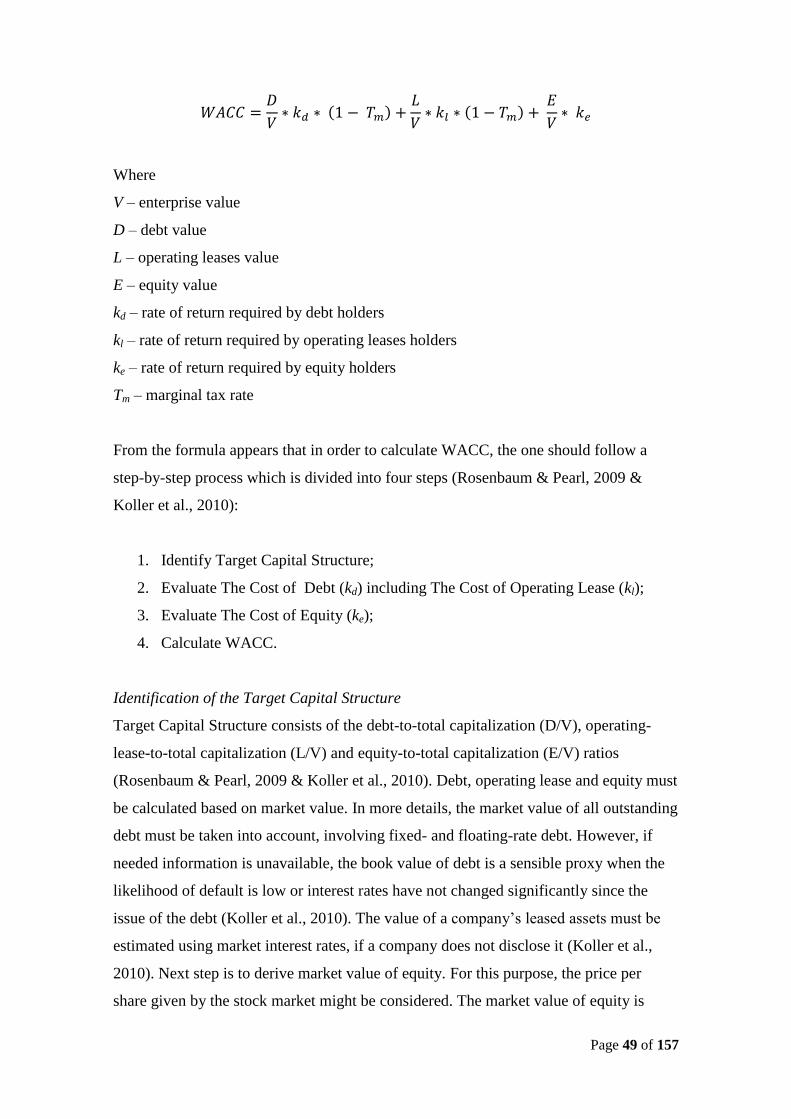

6. Evaluation of the corporate valuation theories ................................................................. 45

6.1 The Discounted Cash Flow (DCF) Method ............................................................. 46

6.1.1 Variables in the DCF Model ............................................................................... 47

6.1.2 The Weighted Average Cost of Capital ............................................................... 48

6.2 Economic profit model .............................................................................................. 56

6.3 Multiples ..................................................................................................................... 58

6.4 Real Option Valuation (ROV) .................................................................................. 61

6.4.1 The Binomial lattice model ................................................................................. 63

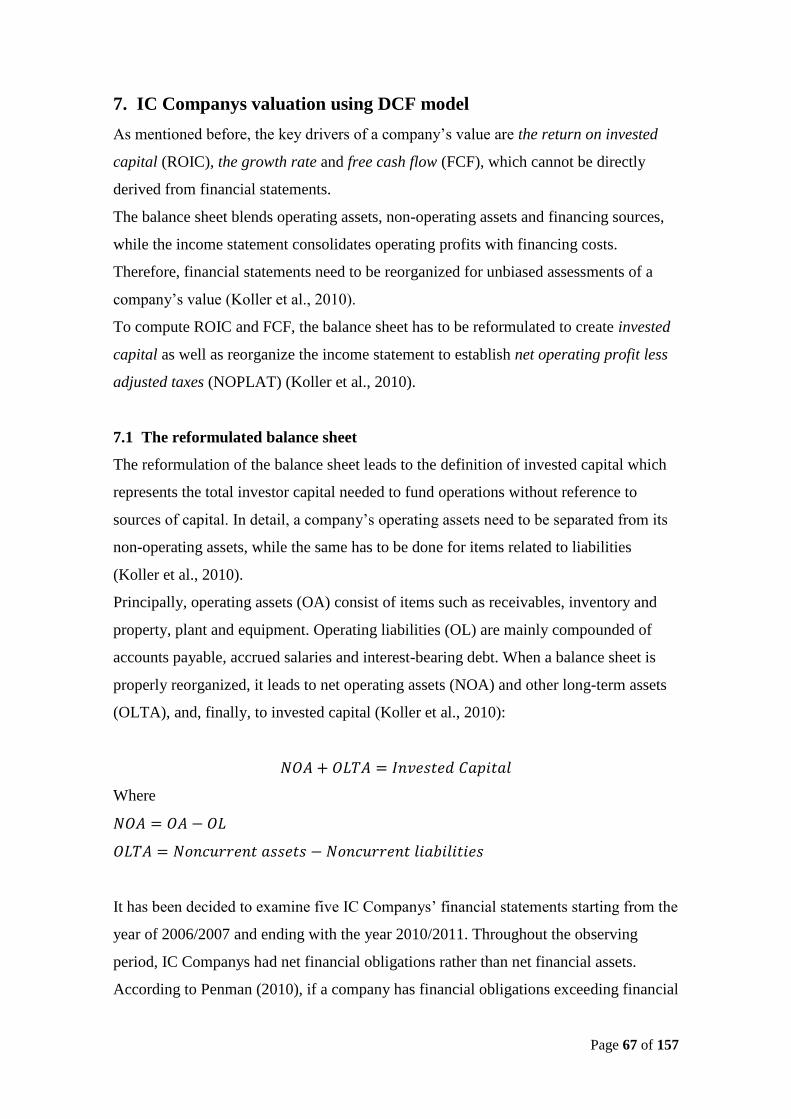

7. IC Companys valuation using DCF model ........................................................................ 67

7.1 The reformulated balance sheet ............................................................................... 67

7.2 The reformulated income statement ........................................................................ 69

7.3 Trend analysis ............................................................................................................ 69

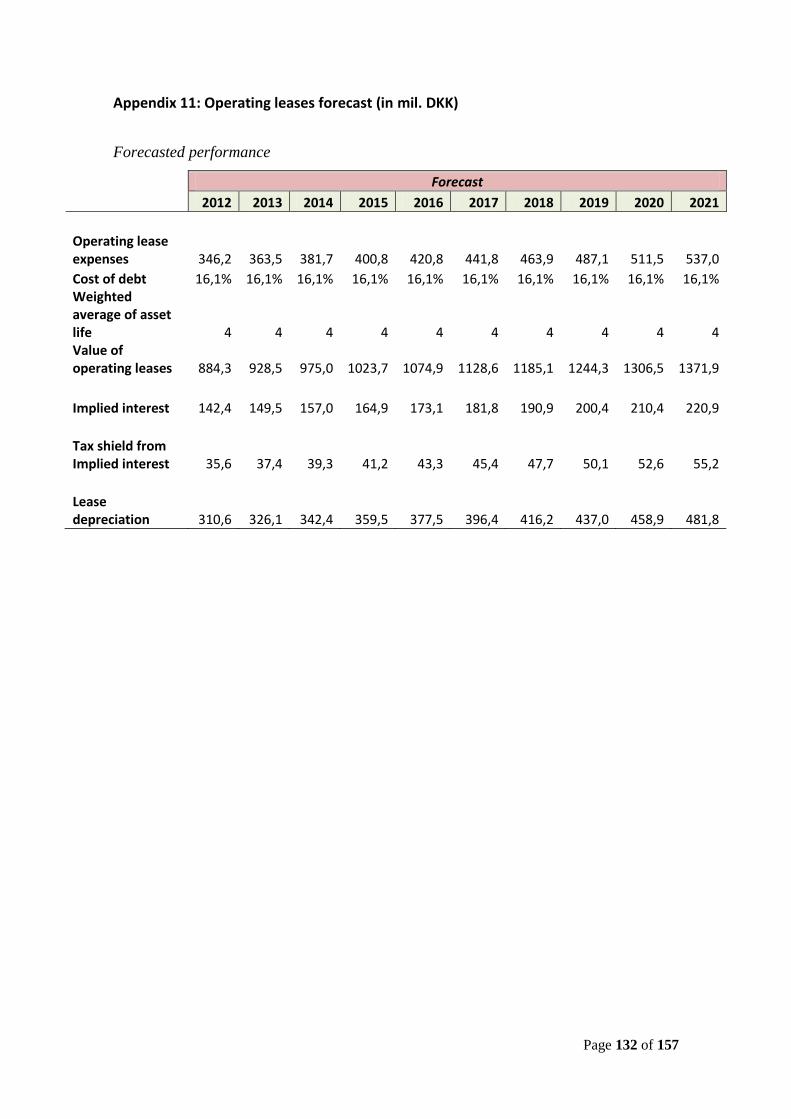

7.4 Operating Leases, Taxes, NOPLAT and Invested Capital .................................... 71

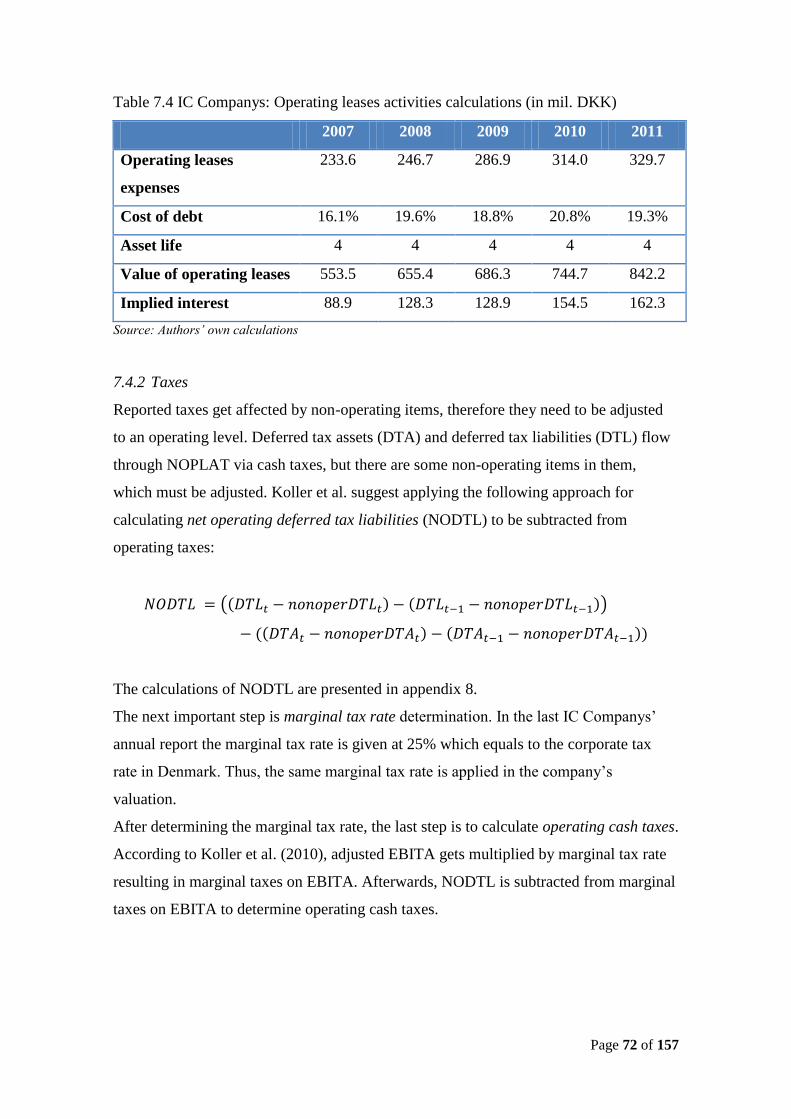

7.4.1 Operating Leases ................................................................................................. 71

7.4.2 Taxes ................................................................................................................... 72

7.4.3 NOPLAT .............................................................................................................. 73

7.4.4 Invested Capital ................................................................................................... 74

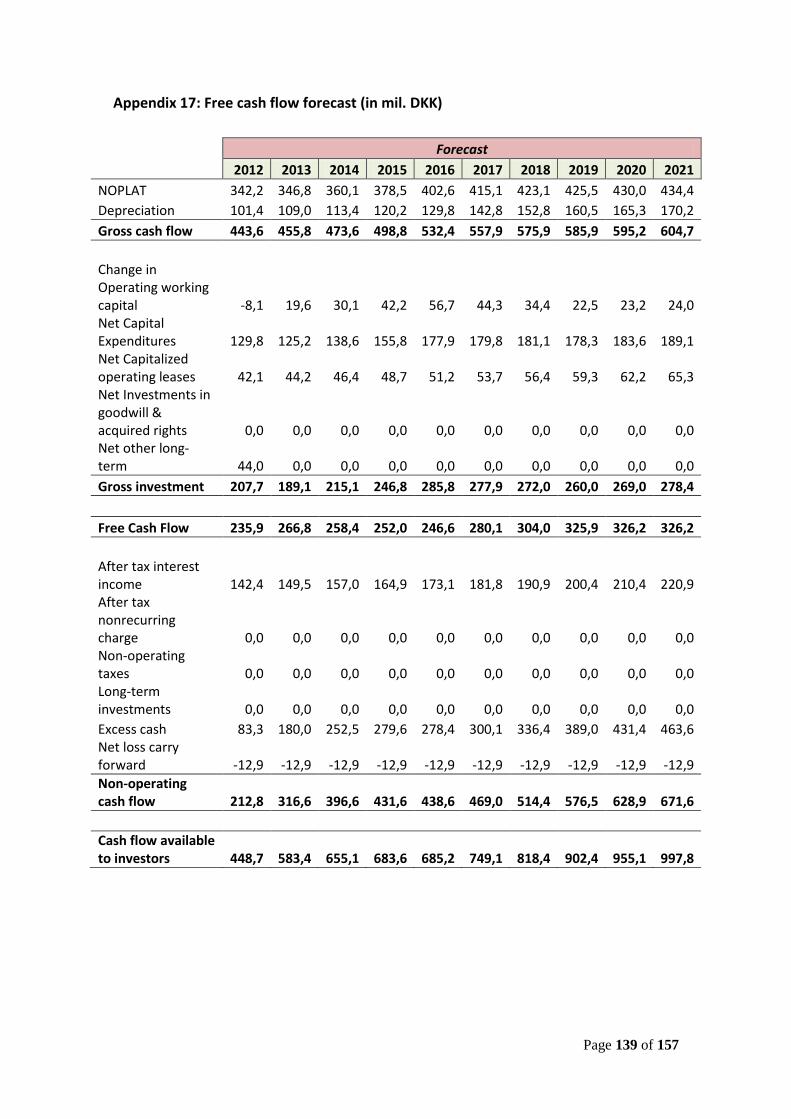

7.5 Free Cash Flow .......................................................................................................... 75

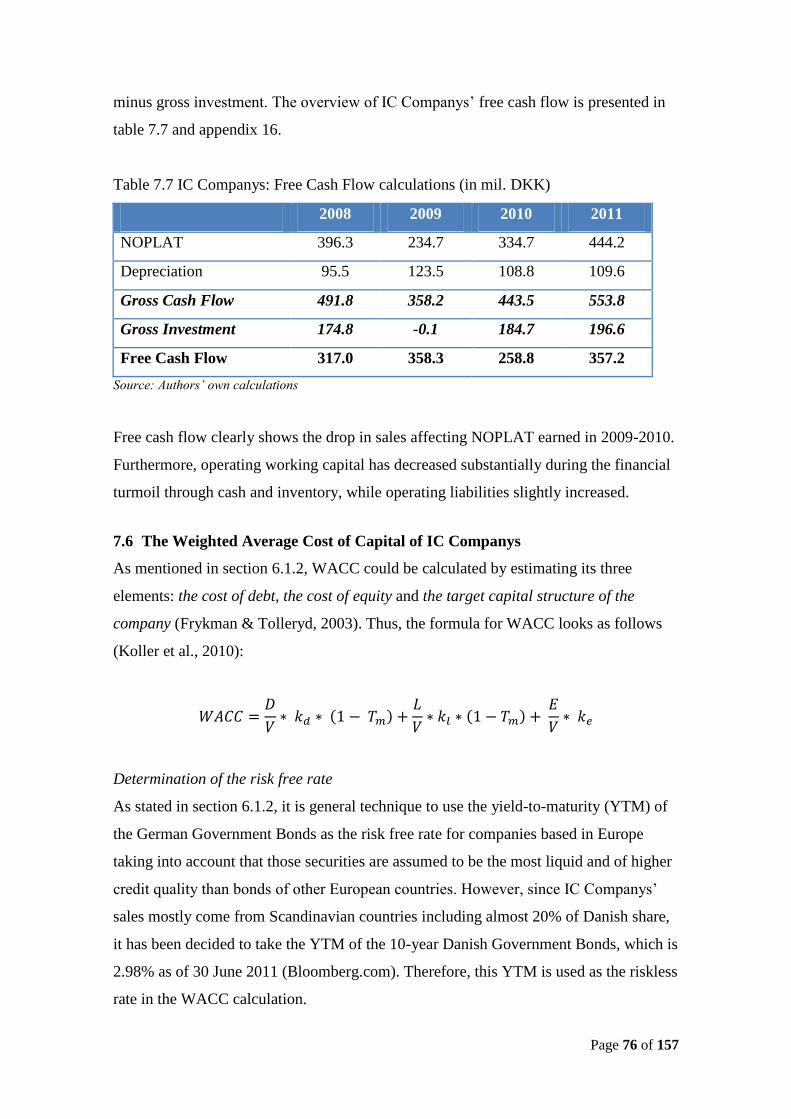

7.6 The Weighted Average Cost of Capital of IC Companys ...................................... 76

7.7 Forecasting of the IC Companys’ free cash flow .................................................... 81

7.8 Calculation of the IC Companys’ continuing value ............................................... 84

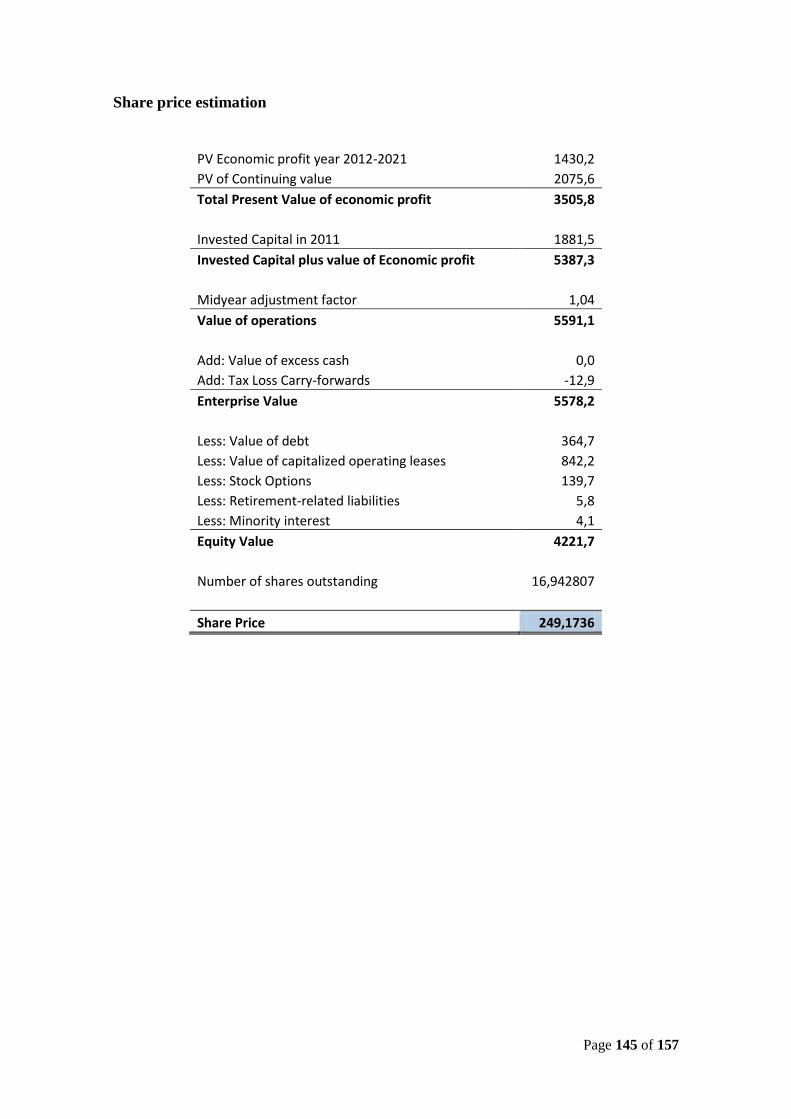

7.9 Calculation of the IC Companys’ share price ......................................................... 85

7.10 Scenario analysis ....................................................................................................... 86

7.11 Sensitivity analysis..................................................................................................... 88

8. IC Companys valuation using Economic Profit Model .................................................... 90

9. Real Options Valuation of IC Companys ........................................................................... 92

9.1 Expansion option ....................................................................................................... 92

9.2 Binomial lattice approach for IC Companys .......................................................... 94

9.2.1 Step 1: Evaluation of IC Companys’ underlying asset without flexibility .......... 94

9.2.2 Step 2: Event tree ................................................................................................ 94

9.2.3 Step 3: Decision tree ........................................................................................... 97

9.2.4 Step 4: Expansion option for IC Companys’ decision tree with flexibility ......... 98

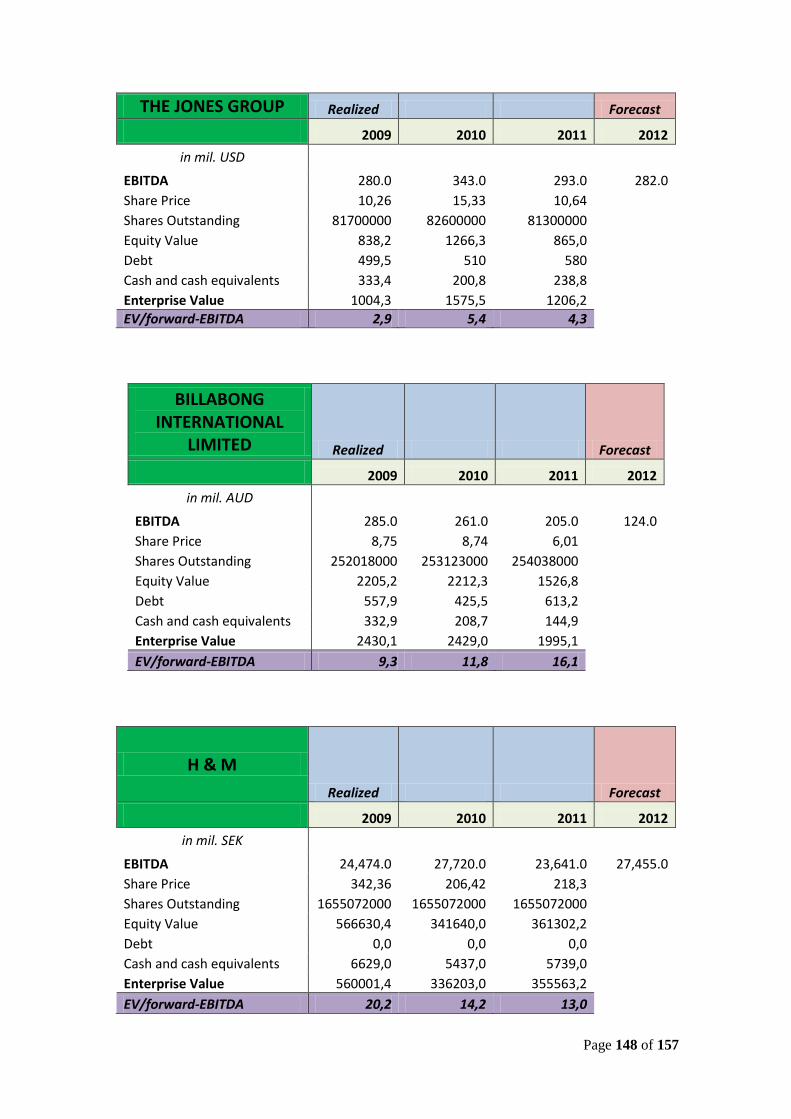

10. Valuation by multiples ....................................................................................................... 100

Page 5 of 157

11. Discussion of the results ..................................................................................................... 102

11.1 DCF analysis ............................................................................................................. 102

11.2 EVA analysis ............................................................................................................. 103

11.3 Real Options valuation .............................................................................................. 103

11.4 Multiples .................................................................................................................... 104

12. Conclusion........................................................................................................................... 104

References ................................................................................................................................ 108

Appendices ............................................................................................................................... 115

Page 6 of 157

1. Introduction

The aim of this paper is to focus on different theories and methods in order to make a

thorough corporate valuation concerning chosen multi-brand apparel enterprise IC

Companys A/S. The theoretical knowledge acquired during Corporate Valuation course

is applied to real life case by using publicly available data such as company’s annual

reports and published articles.

It could be assumed that after the harsh economic crisis in the past 2007/08 that hit

almost all markets and businesses, corporate valuation of different companies becomes

more interesting and challenging due to the recession period.

The main reason of the selection of IC Companys is its multi-brand strategy, where each

brand has separate design and management team. The company’s strong position creates

intensive competition environment for the rivals in the fashion industry. IC Companys

A/S is a Danish fashion and clothing company with relatively short history, but very

colorful and turbulent one. The group was formed on 30 April 2001 by the merger of

two Danish clothing and fashion companies InWear Group A/S and Carly Gry

International A/S. Indeed, newly formed fashion group has experienced some

challenges and difficulties especially within the top management team. As in fact in

2004 it has been realized that in the year 2003/04 company was in turmoil and large

deficit resulted in deposing of CEO and chairman. After some internal changes in the

management team, in the upcoming year of 2004/05 company achieved a surplus and IC

Companys stock price increased from 50 DKK to 400 DKK in spring 2006. This

increase in stock price was indication of positive turnover and IC Companys’ business

in overall. However, it was a temporary rise of stock price, in fact, economic crisis of

2007/08 resulted in turmoil and downturn in almost all kinds of businesses. IC

Company was not an exemption.

Page 7 of 157

Figure 1. IC Companys’ share price in DKK (January 2003 – April 2012)

Source: finance. yahoo.com

2. Problem statement

The purpose of the master thesis is to analyze and answer the following 2 sub-analyze

questions:

1. What are the competitive advantages of IC Company A/S and how the

company exploits them for development?

2. Does a valuation of real options reveal additional value to the company?

Sub-analyze questions lead to the answer of the main question of the master thesis:

Does IC Company A/S stock price reflect a fair market value as of 30th June 2011?

Page 8 of 157

3. Delimitations

The dissertation must be considered to be written for a potential investor of IC

Companys and thus it is based on the publically available information such as

company’s annual reports, websites, newspapers, articles, etc. Due to a selected target

group, interviews of company’s employees are not conducted as it is assumed that, first

of all, they are unable to disclose internal information and, secondly, it is always prevail

the fact that employees’ statements contain bias and therefore are subjective.

The thesis is founded on the application of definite theories and models relevant to the

case company. Strategic analysis models are discussed shortly as the main purpose of

the dissertation is a financial valuation of IC Companys. Financial theories are analyzed

in more details, however, only those which are applied in the thesis.

4. Description of IC Companys

4.1 Introduction

IC Company A/S is a Danish fashion group listed on the OMX Copenhagen Stock

Exchange. IC Companys is one of the major players in the fashion industry operating

across much of the world. IC Companys designs and sells apparel in a Scandinavian

style for conscious and self-confident men and women. The enterprise’s eleven brands

are distributed via two main channels: wholesale and retail. In details, wholesale

segment is compounded of wholesale customers and franchise partners, while retail

distribution channel consists of few types: group’s retail stores, concessions, franchises

and outlet stores and e-commerce (IC Companys’ annual report 2010/2011).

4.2 History

IC Companys was founded by the merger of Carli Gry International A/S and Inwear

Group A/S in 2001 (IC Companys, the history of IC Companys).

Carli Gry International A/S

Carli Gry International A/S was one part of the merger that created the IC Companys

A/S. The company was founded in 1940 and introduced Jackpot for women and

Cottonfield for men. Both brands still operate in the IC Companys brand portfolio and

Jackpot itself enters into the composition of five key brands which generate the major

Page 9 of 157

part of the company’s earnings. Carli Gry was listed in 1996 on the Copenhagen Stock

Exchange. In 1998, the company acquired the Swedish fashion and sports company

Peak Performance, while Carli Gry was also listed on the Stockholm Stock Exchange.

Towards the late 90s the actual results were promising and in 1997 Carli Gry obtained

the largest ever profit before tax of DKK 136 million. The following year the company

experienced growth in revenues, while decreasing profit margins. The development has

been explained by short-sighted focus on margin over long-term focus on IT and

marketing. In order to reverse negative trends, Carli Gry dislocated its sales from

unprofitable stores and increased focus on marketing, branding, logistics and factory

outlets.

Inwear Group A/S

InWear Group A/S was established by Niels Martinsen in 1969, who nowadays is the

major shareholder and chairman of IC Companys. InWear’s primary brands were

InWear focused on young women as the target group, the male counterpart Matinique

and Part Two. InWear and Carli Gry faced some financial troubles before the merger

with deteriorating profit margins in a stressed market. Such difficulties made InWear to

liquidate unprofitable stores and led to further adjustments.

4.3 Merger

Clothing sector experienced the worst times in the late 90s due to a fierce competition.

After evaluation of the strategic and economic considerations of economies of scale, the

merger of Carli Gry and InWear was an obvious decision in order to capture strong

market position, distribution channels, product portfolio and operational synergies. On

12th

March 2001, the companies made the joint announcement where the directors

recommended the merger of Carli Gry and InWear. The merger was approved on 30th

April 2001 with Carli Gry as the continuing corporation under the name of IC

Companys A/S (IC Companys, Fusionsprospekt, 2001).

4.4 IC Companys A/S

After the merger, IC Companys had product portfolio of 13 brands, and in the following

years some additional brands were added to the portfolio. In 2002 IC Companys bought

the Danish company Saint Tropez that was founded in 1993 and specialized in

designing and selling clothes for younger women. At the same year new brand

Page 10 of 157

Designers Remix Collection was introduced. IC Companys has also established the

cooperation with the Danish haute couture designer Isabell Kristensen who has

launched collection "O", but later her designs were launched under the brand name of

Soaked in Luxury.

In 2003 IC Companys also signed a collaboration agreement with the Danish designer

Malene Birger under the brand By Malene Birger. Later that year IC Companys bought

the dominant brand of clothes for young people in Sweden - Sir Tiger Modebolag.

In October 2003 the CEO and the entire board was replaced, with the exception of Niels

Martinsen, due to disappointing results.

In 2006 IC Companys started to expand business in the emerging markets and

Cottonfield that provides clothing for males has been launched in Chinese market. It

must be mentioned that IC Company has already been introduced in China by InWear

brand for few years.

In 2008 IC Companys has experienced the third major change in management in the

company's short history. Due to depressing growth in bottom line, Niels Mikkelsen was

appointed as a new CEO, and Donald Cleemann and Chris Bigler got promoted to fire

director and CFO (RB-Børsen, 2008), respectively. Therefore IC Companys appears as

the company with a relatively short and turbulent history with several changes in

management, but also as a group with a portfolio of brands covering fashion market

today.

Page 11 of 157

4.5 Products

IC Companys follows a multi-brand strategy, thus having the product portfolio of

eleven brands.

Table 4.1 IC Companys’ brands revenues (in mil. DKK)

2010/2011 2009/2010 Growth

Peak Performance 977 915 7%

Tiger of Sweden 563 476 18%

Jackpot 426 398 7%

InWear 404 359 13%

Saint Tropez 320 244 31%

Matinique 289 260 11%

Part Two 272 254 7%

By Malene Birger 264 196 35%

Cottonfield 203 197 3%

Designers Remix 91 74 23%

Soaked in Luxury 74 87 -15%

Total 3,883 3,460 12%

Source: IC Companys Annual Reports 2009/2010 and 2010/2011

The five key brands constitutes for approximately 70% of total company’s revenues,

while Peak Performance is the largest contributor with the share of almost 25%. In

general, it marks the interdependence between how long the brand is presented on the

market and how much revenues it produces. For instance, such brands as By Malene

Birger, Designers Remix and Soaked in Luxury were established in the years of 2003,

2002 and 2005, respectively. In the last financial year, Saint Tropez and By Malene

Birger have experienced a rapid surge largely contributing to the group’s growth, while

only the youngest brand Soaked in Luxury has seen declining sales.

4.6 Distribution channels

The group has two main distribution channels: wholesale and retail.

Wholesale is IC Companys’ initial distribution channel contributing to more than 60%

of total revenues in the financial year of 2010/2011 with the growth of 13%. No

Page 12 of 157

customer accounts for more than 3% of the group’s wholesale revenues, meanwhile the

largest single supplier constitutes for 7% of the total production value (IC Companys’

annual report 2010/2011). Therefore, there is no significant dependence on customers

and supplier.

Retailing is the group’s second major distribution channel which accounts for 1,530.6

mil. DKK in the financial year of 2010/2011 that is equivalent to 40% of total turnover.

As of 30th

June 2011, IC Companys runs 289 retail stores, therefore being presented in

20 countries, primarily in Denmark, Sweden, Benelux countries and Eastern Europe.

Retail revenues experienced an increase of 11% in comparison with the previous

financial year.

The network of outlets is an integral part of the company’s distribution channel as they

allow for more flexibility – any product that cannot be sold through own outlets are sold

to brokers for resale outside the company’s established markets (IC Companys’ annual

report 2009/2010). As of 30th

June 2011, the group runs 28 outlets giving 184 mil. DKK

in total earnings with an increase of 11%.

4.7 Markets

IC Companys’ sales made through its own sales subsidiaries and exports to more than

40 different countries through agents and distributors. Responsibility for the sale is

embedded locally in the respective countries, while in Denmark fire management has an

overall global responsibility. By referring to figure 4.1 it could be calculated that the

group's total turnover is 80% outside Denmark and 45% outside Scandinavia.

Page 13 of 157

Figure 4.1 Geographic segments measured by revenues in 2010/2011 (in mil. DKK)

Source: Annual report 2010/2011

Geographically it could be stated that IC Companys' main markets are concentrated

mostly in the countries of Northern Europe, primarily Scandinavia, Benelux countries,

the UK and Germany. IC Company has achieved significant growth in the financial year

of 2010/2011. Overall the group has achieved essential growth almost in all markets,

exceptions are China, Russia and Benelux countries. Some problems still concern

business in the Chinese market. By referring to the CEO of IC Companys Niels

Mikkelsen, it is hard to determine particular issue, but Group decided to learn more

from the existing Danish fashion companies that successfully operate in the Chinese

market (RB-Børsen, 2008).

Page 14 of 157

5. Strategic analysis

In order to identify state of the company in relation to external and internal drivers it is

decided to conduct main models in strategic analysis. As an external analysis it is

referred to PESTEL model with the aim to identify the macro-environmental factors that

influence IC Companys’ business in all aspects. Additionally, Porter’s five forces model

is applied to conduct an industry analysis.

PESTEL analysis is mainly used to examine 6 different aspects of the macro-

environment which are Political, Economic, Socio-cultural, Technological,

Environmental and Legal.

Main target of Porter's five forces is to identify the overall industry attractiveness and its

aspects of profitability. There are five general points to examine industry conditions and

they are: the competitive rivalry among existing competitors, the bargaining power of

the suppliers, the bargaining power of the customers, the threat of the substitute

products and services, and the threat of new entrants.

Beside the external analysis it has been planned to go through internal analysis with the

aim to examine the chosen company's strengths and weaknesses. That is why Value

Chain analysis, which has been developed by Michael Porter in 1985, is conducted.

Value chain analysis mainly discusses issues concerning generic value-adding activities

of an organization. The primary activities include: inbound logistics,

operations/production, outbound, marketing & sales and service; while supportive

activities consist of infrastructure, human resource management, technology

development and procurement.

In the conclusion results from both external and internal analysis are summarized,

where the output of external analysis allows identifying threats and opportunities, and

internal analysis results determine a company’s strengths and weaknesses.

Both results are combined in the SWOT analysis in order to perform the clear and

objective image of the target company.

Page 15 of 157

5.1 PESTEL Analysis

The purpose of the following analysis is to investigate IC Companys’ macro-economic

aspects that could have an impact on the group’s opportunities and threats as well as its

capability of adjusting to particular environmental factors. PEST analysis reviews the

macro-environment that has the supreme influence on the apparel industry and therefore

on the Group’s strategic position since the clothing industry is considered to be highly

cyclical sector. Specifically, the factors reviewed in this model are Political, Economic,

Socio-cultural, Technological, Environmental and Legal (Kotler & Keller, 2006).

Despite the fact that originally the model reviews each part individually, it is widely

assumed to combine Political and Legal parts of the model in one as well as Technology

and Environment since there have many similarities.

5.1.1 Political and Legal factors

Stability and predictability of a political system any company operates in are vital

requirements for an enterprise to succeed. As IC Companys is an international

company, the Group is highly exposed to political and legal changes in various

countries and thus production, distribution and sales could be extremely influenced by

these factors.

The major part of the company’s sales are conducted in Northern and Western Europe

(IC Companys’ annual report 2010/2011), which are characterized by a steadfast

political environment and relatively similar legal factors. Furthermore, Denmark’s

membership in the EU leads to the uniformity in the legislation. Therefore, it is unlikely

that the Group could face any political and/or legal issues negatively affecting sales.

On the other hand, the major portion of the company’s production is located in China

(including Hong Kong), which accounts for 69%, whereas rest of Asia and Europe

provide 18% and 13%, respectively (IC Companys’ annual report 2010/2011). Thus, the

Group is exposed to risks of political and cultural aspects; meanwhile the main reason

for outsourcing to the Asian region is favorable wage levels and a specialization in

production of clothing. In favor of China says the fact that both Denmark and China are

the members of the World Trade Organization, which actively tries to eliminate trade

barriers among member countries, thereby the EU did not extend the quota system for

goods manufactured in China, which had been introduced in the summer of 2005,

replacing it by a continuous supervision in 2008 (IC Companys’ annual report

2007/2008). Therefore, there are no artificial bureaucratic barriers to Chinese import.

Page 16 of 157

The outsourcing might be exposed to certain commercial risks. One of them is a steadily

increasing wage level in Asian region. Though, it is still lower than in Europe, but it is

just the question of time and the outsourcing to Asian companies might become

deterrent in the foreseeable future.

To sum up, there are not any serious political or legal issues that might affect the Group

negatively.

5.1.2 Economic factors

As it was mentioned before, the garment industry is highly cyclical and primarily

depends on the level of consumer disposable income that in turn follows economic

conditions. In the following part, economic conditions in the company’s main markets

are examined: Scandinavia (Denmark, Sweden and Norway) and two major and growth

potential markets (Russia and China).

Denmark

According to Nordea’s Economic and Market Outlook for May 2012, the Danish

economy is heading to prosper times. Unemployment is decreasing and consumers are

sensing the rise of better things. The Danish economy is expected to expand gradually

throughout 2012, principally driven by higher consumer spending and firm public

investments. In 2013, the growth must accelerate more broadly grounded on a growing

demand from other countries and higher domestic investment activity. Thus, the

economic outlook for GDP is positive: 1.25% and 1.75% in 2012 and 2013,

respectively.

Housing market trends will be crucial for the Danish economy going forward.

Unfortunately, the price declines in the Danish housing market have accelerated again

in recent months. However, there is a strong belief that house prices will stabilize

towards the end of this year converging to the long-term equilibrium level. Thus,

housing market activity looks to make a positive net contribution to growth of the

Danish economy in the coming years.

Macroeconomic situation is kept in proper perspective by the Danish government which

has managed to sustain robust balances in the form of a record-high current account

surplus, low gross public debt and historically large currency reserves. Having the status

of safe haven, Denmark has been taking advantage of this by luring historically cheap

funding of the government debt (Nordea Markets, 2012).

Page 17 of 157

Sweden

Sweden is the major market for IC Company, thus economic conditions there are very

significant. Data in the first couple of months of 2012 give a mixed picture. Export has

increased by 6.8% in 2011 and the unemployment rate declined to 7.5% in 2011

compared to 8.4% in 2010; however, it is still essentially higher than what the Swedish

Central Bank considers normal of about 6.5% (Nordea Markets, 2012).

As export-oriented country, Sweden is highly vulnerable to external economic

conditions and uncertainty concerning international developments negatively affects

further recovery following the financial crisis in 2008-2009. Thereby, the GDP growth

for 2012 is expected at 0.5%, while the forecast for the next year is more optimistic and

GDP is predicted to rise 2.2%.

Due to the weak external environment, the main growth engine might be domestic

demand, in particular, private consumption. Real household disposable income is

forecast to grow 2.0% and 2.1% in 2012 and 2013, respectively, what is a reassuring

factor for consumption sectors and particularly for the Group (Swedbank, 2012).

Norway

In the near future, the Norwegian economy undergoes a modest increase of GDP at

2.7% in 2012 and 2013, respectively. The major contribution comes from private

consumption and petroleum investments.

In recent years, high real wage growth has been supported by strong expansion in terms

of trade and partly also by growing productivity, but going forward these drivers have

been depleting. However, it is projected that annual real wage growth will stay at 4.0%

through 2013 what is below the average level over the last 12 years.

Oil and energy related sectors are booming again mainly driven by high oil prices. It is

expected that in coming years a barrel price stays much higher than 100.0 USD, thus

improving prospects for the Norwegian economy.

The unemployment rate will stay low with moderate rise in coming years, but below

4.0% what is the lowest level in Scandinavia (DnB Nor, 2012).

Russia

The Russian economy is performing satisfactory, but it encounters some difficulties

going forward. In 2011, the economy expanded by 4.3% while the unemployment rate

Page 18 of 157

lowered reaching 6.5% and inflation stayed at surprisingly high level of 8.4% (IMF,

2012).

Amid the global economic slowdown, growth is likely to be somewhat slower in

coming years, but seems to be sustained at reasonable levels backed by still-high oil

prices (OECD, 2012). Slower growth in Europe fighting debt contagion and China

trying to switch to domestic consumption will have a negative impact on the volume of

exports, where about two-thirds of exports consists of energy related goods.

Wage growth has been higher than inflation that also contributed to rising consumer

spending. In addition, a rising value of the currency has played a disinflationary role

boosting consumption. Moreover, fiscal policy has recently been expansionary before

the presidential election. On the one hand, it will contribute to economic growth; on the

other hand, budget deficit will become obvious if oil prices suffer from sharp decline

(Deloitte, 2012).

To sum up, prospects for economic growth remain positive with GDP expansion of

4.0% in 2012 and 3.9% in 2013 and decreasing jobless rate to 6.0% in both 2012 and

2013.

China

In the years following the financial crunch of 2008-2009, China has become the engine

of the world economy contributing the major share to the global growth. Therefore, the

scenario of a sharp tumble in Chinese economic activity is a significant risk, especially

with Europe already in downturn (Royal Bank of Canada, 2012). However, these

prospects are highly unfeasible unless the world economy experiences new turmoil

compared to what happened in 2008-2009.

Growth has continued to ease in emerging Asia largely attributable to weak foreign

demand particularly from advanced countries. China’s first-quarter GDP numbers

(+8.1%) were gently weaker than anticipated due to deteriorating foreign demand, but it

is expected that the Chinese economy has experienced temporary issues and should pick

up in the coming years expanding by 8.2% and 8.8% in 2012 and 2013, respectively

(IMF, 2012).

Meantime, inflation has receded as the result of monetary and lending steps, thus it is

projected to trend down to 3.3% in 2012 and 3.0% in 2013 what is significantly lower

than 5.4% in 2011 (IMF, 2012). Unfortunately, consumer prices have little room to ease

further due to high oil prices (Banco Bilbao Vizcaya Argentaria, 2012).

Page 19 of 157

Summary

The Northern Europe accounts for the major part in IC Companys sales and economic

conditions in this region are of great significance for the company. According to various

prospects, 2012 and 2013 are the years of continuing recovery and the same issues

coming from the Southern Europe. Scandinavian countries which are highly vulnerable

to external sentiment in terms of export volume have been staying a safe haven in times

of extreme turbulence and it seems that necessary adjustments have been made in order

to get back on the growth rails.

Russia and China are two enormous markets with unrealized potential and the Group’s

management has to develop appropriate strategies to succeed there. Meanwhile the

steady growth in China is also a challenge for the company since production expenses

might jump as a result of general wage level increase.

Foreign Currency Exposure and Interest rate risks

IC Companys is exposed to essential exchange rate risks which arise through purchase

of supplies and sale of goods in foreign currencies. The major part of the company’s

purchase of supplies comes from the Far East and denominated in USD and USD-

related currencies while the main share of the sales and capacity expenses are expressed

in DKK, SEK, NOK and EUR. Given currency model causes concerns especially in the

times of financial crises since USD often appreciates and revenue currencies (SEK,

NOK and PLN) depreciate (IC Companys’ annual report 2010/2011).

Therefore, the Group hedges all material transaction risks on a trailing 15-month

horizon, primarily using foreign exchange forwards and/or options (IC Companys’

annual report 2010/2011).

The company’s interest rate risks are related to the Group’s interest-bearing assets and

liabilities. Those risks are managed by acquiring loans with a floating or fixed rate

and/or financial instruments such as forward rate agreement and/or interest rate swaps

with typical neutral maturity of 2 months (IC Companys’ annual report 2010/2011).

5.1.3 Socio-cultural factors

Nowadays, consumer behavior has been changing swiftly; however, it is quite often

occurs that fashion trends recur with some new features. Moreover, boundaries between

male and female fashions have been blurring. Low customer loyalty and allegiance to

brands are common (McKinsey & Company, 2011).

Page 20 of 157

Another trend in the fashion world that proves low customer devotion is mix of

products from different price segments. For instance, depending on consumers’

preferences in the fashion the mix of cheap no-name clothes with high-priced high-end

garment is more frequent.

Therefore, it is vital that the Group persists to concentrate on innovation, diversity and

brand development. The company’s collections change at a minimum of four times a

year. For example, Saint Tropez develops 10 collections a year with ongoing deliveries

and just 3 months from sketch to store rack allowing the design team to respond to the

latest trends (IC Companys’ annual report 2010/2011).

Another positive aspect which plays in favor of IC Companys is its multi-brand

strategy. The following model allows determining various target groups’ needs.

Though, in the fashion industry it could be problematic to focus on a specific target

group as the behavior of specific target groups is not always predictable. Furthermore,

various groups sometimes overlap.

Thus, these aspects have been taken into account by IC Companys while creating its

multi-brand strategy which leads to a brand portfolio correction and managing in regard

to price, consumer taste and behavior.

5.1.4 Technological and Environmental Factors

Technology

In the apparel production, the technological level and thus quality is an essential aspect.

Since the Group’s production primarily occurs in developing countries of Asia and

Eastern Europe, it mainly relies on manual tailoring. In the foreseeable future,

production of high volume will be realized by usage of machinery when workflow

could be facilitated and quality ameliorated.

Moreover, in regard to retail business adapting of next-generation technologies is

almost unlimited and might give a competitive advantage. Such innovations as

electronic shelf labeling, digital promotional displays, self-checkout and sales kiosks

could change how fashion companies relate to their customers (McKinsey & Company,

2011).

IC Companys is technologically dependent on reliable IT systems for the day-to-day

business operations as well as to ensure control of product sourcing and to enhance

efficiency throughout the company’s supply chain. IT support in all aspects of sourcing,

Page 21 of 157

distribution, logistics, administration and sales makes it possible for the individual

brands to focus on the creative and commercial development aspects (IC Companys’

annual report 2010/2011).

The other aspect of technological factor is e-commerce. The idea that the Group’s

websites are used for both sale and demonstration is essential for enhancing company’s

performance. Currently, all company’s eleven brands have their websites where any

customer may get necessary information, compare prices and conduct purchase.

In general, online trade in Denmark has been experiencing two-digit growth in last

couple of years reaching 46 bil. DKK in 2011 (Ekstrabladet.dk, 2012) from 20 bil. DKK

in 2007 (Computerworld.dk, 2008). Thus, e-commerce becomes an essential

distribution channel with massive potential and direct customer contact. Therefore, IC

Companys has been investing substantial amounts of funds in developing IT systems to

enhance its online sales.

Environment

Since August 2011, IC Companys has participated in the United Nation’s Global

Compact working on Corporate Social Responsibility (CSR). It is a voluntary initiative

for private businesses that are committed to dealing with some of the major social and

environmental challenges. Therefore, the Group has been focusing on five areas: human

rights, labor, anti-corruption, animal welfare and environment. The environmental part

implies the company’s policy regarding environment exploiting and supporting of the

prevention of pollution and use of harmful chemicals in products undertaking initiatives

for promoting greater environmental responsibility and encouraging the development

and diffusion of environmentally friendly technologies (IC Companys’ annual report

2010/2011).

Furthermore, IC Companys has decided to undertake a number of comprehensive

measures to ensure that consumers feel safe when wearing company’s garments.

Therefore, the Group performs a set of strict procedures (IC Companys, 2011):

1) Increase of tests number to test whether company’s products have a risk of

increased permitted values of chemical residues. Furthermore, performance of

spot checks on remaining products will be implemented;

2) Transfer of tests to the production countries implying that the products will

never reach the consumers if findings indicate chemical residues above the

Page 22 of 157

permitted values. Until the new procedures have been undertaken in, for

instance, India and China, the test products will be transported to Denmark by

plane to have the tests performed before the product lines leave the production

countries;

3) Enforcement of new stringent requirements on suppliers. The number of

suppliers will be reduced in the nearby future leading to working with only the

most responsible ones enhancing even better quality.

5.2 Porter's five forces

After defining the industry’s boundaries for the target company, above mentioned

Porter’s five forces analysis allows managers to identify competitive advantages in

order to operate more efficiently. By referring to Michael Porter (1980), it could be

stated that if each force intensifies and gets stronger that limits an ability of established

companies to raise prices and increase its earnings. It indicates the fact that if

competitive forces intensify that increases a threat factor for existing companies in an

industry. The power of these forces changes over time by creating new opportunities

and threats which is challenging for managers to formulate relevant strategic planning

with attempt to minimize the threats and to take advantage of the opportunities (Hill &

Jones, 2010). Each of the five forces in relation to the chosen IC Companys and the

industry it operates in are elaborated below.

Page 23 of 157

5.2.1 The threat of the new entrants

There are several requirements for the new entrants to establish their business in the

particular industry. It is assumed to introduce more relevant requirements for the

apparel industry such as investment, brand name, production and distributions

channels. Apparel industry might be assumed as fragmented industry where

standardized fashion is produced in large volume, exclusive collection and high-end

fashion products are produced in low volumes. A barrier overcoming for the new

entrant mainly depends on which end of scale to launch the apparel business from. By

capturing correct trends at the right time, might be possible to enter the market without

having high capital or preferred brand. The ones who want to enter the standardized end

of the apparel market targets a price sensitive customer group that prefers the cheapest

product than expensive high-quality and well-known brand. The existing competitors in

such a segment are those leading in cost leadership, which have expertise in that field

and well-established cheap production facilities. Apparel companies that target price

sensitive customers mostly focus on cost-cutting management and strive to produce

with very low expenses in order to fit into cheap and affordable less expensive products

price interval.

Threat of the new entrants at the low end of apparel industry assumed not to be so

strong in sense of creating high competition since the low end apparel producers

compete not with quality, but with quantity and have already established stable

distribution channels and the cheapest supplies by gaining discounts what might be

complicated for new entrants at the beginning.

On the other end of the apparel industry where prices are too high or mid-upper

segment, existing competitors strive to differentiate their products as differentiation

counts as one of the main barriers for new entrants. By altering its products

manufacturing a company might achieve a premium price and additional cost might

occur if a company has higher quality, better brand or design than its rivals. Indeed,

these factors require significant capital as brand loyalty builds up on customers’

perceptions by investing and using its experience that is earned throughout the years of

satisfaction of customers’ needs and desires. There are already some customer groups

who have defined their preferable brand. It might be assumed that capital is not very

important factor in the high-end price segment since the differentiation and brand image

are more essential.

Page 24 of 157

Concerning the Group, IC Companys mostly operates in the high premium and upper-

mid class segment. Referring to annual reports, IC Companys’ management sets up a

target to be the best developer of sports and fashion brands what means the Group has

decided to focus mostly on building strong brands for high-end customers (IC

Companys’ annual report 2011/2012). It is assumed that the threat of the new entrants

carries less risk for IC Companys since new entrants usually are small businesses or

companies that probably will not be able to compete directly and might capture only a

small market share. However, on the other side, it has to be supposed that the threat

might come from the other bigger competitors who have significant capital and

expertise in the apparel industry. For example, American apparel company, GAP Inc., is

the one of the world's largest apparel retailers that operates four other brands: Banana

Republic, Old Navy, Piperlime and Athleta. Despite the fact that GAP operates

internationally, they have not entered Scandinavian apparel market yet. It might be

assumed that these kinds of potential new entrants are the threat for the IC Companys. It

has to be mentioned that there are few large companies that might be able to capture

significant share in the Scandinavian apparel market.

5.2.2 Bargaining power of the suppliers

In apparel market the bargaining power of the suppliers has been declining due to the

fact that main textile manufactures and producers have been dislocating their businesses

to the emerging markets where production costs are low. China is one of those countries

that lures with lower cost supplier channels. Mentioning IC Companys’ supplier

channels, it could be stated that the major part of supplies comes from IC Companys’

own shared sourcing offices in China, Bangladesh, Vietnam, India and Romania. 69%

of the production belongs to Chinese supply, with 18% to the rest of Asia and just 13%

to European market. By using its own shared sourcing offices IC Companys has made it

possible to handle geographic sourcing options safely and quickly. Indeed, the Group

could easily move its production wherever the combination of price, quality and supply

stability is the best (IC Companys’ annual report 2010/2011). There are usually some

risks of switching suppliers in relation to quality and credibility. In fact, IC Companys’

management stands for credibility of the production in its own shared sourcing offices.

It has to be mentioned that IC Companys has recently implemented a new sourcing

structure of which the object is to reduce the number of suppliers and improve

efficiency and flexibility. The key element of this new structure is the systematization of

Page 25 of 157

the Group's sourcing while at the same time adapting it to the efficiency and flexibility

required by the organization’s new set up (fibre2fashion.com, 2011). But independence

of suppliers has been reducing IC Companys’ power and influence on the suppliers in

terms of volume discounts, improved credit term, etc. Still suppliers’ bargaining power

is very limited. That is why it has been concluded that in the apparel industry, suppliers

have very insignificant influence on the price regulation and thereby has relatively weak

bargaining power.

5.2.3 Bargaining power of buyers

In order to analyze the bargaining power of the buyers it is decided to define customer

segment that IC Companys deals with. That is why, first of all, IC Companys’

distribution channels must be reviewed. There are two distribution channels, wholesale

and retail (franchise, e-commerce, outlets). Wholesale accounts for 61% of revenues in

2011, while retail captures the rest of sales. Both have showed significant growth of

13% and 11%, respectively (IC Companys’ annual report 2010/2011). IC Companys’

customers do not account more than 3% of the wholesale revenue which means total

sales are independent of particular customer as a result of diversity in the strategic

management. As it has already been stated IC Companys belongs to the upper-mid

segment and high premium brands. That is why its target customers also represent

higher or upper-mid class, which is not usually price sensitive comparing with preferred

high-quality and defined brands. It could be assumed that IC Companys’ apparel

belongs to luxury category where buyers usually do not have significant bargaining

power. Buyer might have bargaining power if other rivals in the wholesale market

intensify competition producing similar apparel, but with lower price. By implementing

the multi-brand strategy IC Companys focuses on each brand and educates its

employees to perform high service and expertise relating to each brand. But still there

are some buyers that might switch from preferred brands to other apparel products in

case of personal image changes and design preferences. As it is supposed even though

IC Companys strives to build strong and valuable brands, their buyers are not counted to

be "brand loyal" customers which means that brands from various producers might also

satisfy IC Companys buyers. In that case such buyers will have some degree of the

bargaining power.

Page 26 of 157

5.2.4 Threat of Substitute products and services

As competition intensifies and buyer becomes more price sensitive, the threat of

substitute products and services increases in major markets. By taking into

consideration the existence of such rivals as Inditex, Bestseller, BTX Group, which

produce upper-mid and middle class garments that might substitute products of IC

Companys' respective brands. Indeed, four out of eleven brands (Tiger of Sweden, Peak

Performance, Designers Remix Collection and By Malene Birger) stand for affordable

luxury, where the rest seven brands (Part Two, InWear, Cottonfield, Jackpot, Matinique,

Saint Tropez and Soaked in Luxury) present less expensive modern clothing. On the

high-end the threat of substitute assumed to be less significant as this group of buyers is

not price sensitive, therefore it is unlikely that they could switch to another seller due to

price difference. Indeed, consumers’ needed design and taste might change over time,

thereby influencing a switching from one brand to another. In order to reduce the

switching threat IC Companys educates its labor to focus on premium service that

creates strong brand image among the other competitors’ brands. It might be assumed

that if to consider both middle class and affordable luxury segments, to some extent the

threat of substitutes significantly exists.

5.2.5 Competition among the existing rivals

There are some vital factors that influence behavior of the players in the apparel market.

Industry concentration and growth have direct impact on competition intensity.

Industry concentration

Apparel market is one of the markets characterized by many suppliers with various

market sizes. The global apparel market consists of numerous smaller enterprises

operating internationally and several major companies that operate globally. Owing to

many entities in the apparel industry even the major market participants such as US

GAP, Swedish H&M and Spanish Inditex have relatively low global market shares that

indicates the high industry concentration. High industry concentration intensifies

competition and increases the market attractiveness.

Industry growth

Market growth for the apparel industry could be examined from different aspects.

Through the historical data it could be seen that the global apparel industry had total

Page 27 of 157

revenues of $1,175.4 billion in 2011, representing a compound annual growth rate

(CAGR) of 2.7% between 2007 and 2011. According to forecasts, the global apparel

retail industry is forecasted to earn a value of $1,348.1 billion in 2016 with an

anticipated CAGR of 2.8% for the five-year period (Companiesandmarkets.com, 2012).

The female wear segment was the industry´s most lucrative in 2011, with total revenues

of $600.5 billion, equivalent to 51.1% of the industry´s overall value.

Beside the hard data calculations and historical financial numbers there are many other

external factors that have an impact on the future growth prospects of the whole apparel

industry. Some external influencing drivers which increase uncertainty about positive

outcomes might be political, economic, technological and environmental issues that

have been already described in the PESTEL model. Report, published in Stitch Times in

2011, states that "The apparel industry and market really are at a tipping-point" meaning

that apparel industry has reached a level where the scenarios of stagnation, growth and

recession are quite real.

In order to identify the level of competition among the main rivals of IC Companys it

has to be determined the main target customer groups and respective geographic areas.

As it is stated in the company’s report, IC Companys focuses on the development of

fashion brands and sport apparel, meanwhile 65% of the annual turnover is created from

sales in Scandinavian and Benelux countries. Main competitors in the defined market

sector are Bestseller, Zara from Inditex group, Hennes & Mauritz AB.

Even though each rival strives to add value to its brand portfolio by increasing quality

and concentrating on modern fashion, the target customer groups still are not considered

as loyal customers what means a brand switching and mixing is a normal tendency for

the middle class and affordable luxury class consumers. That is why in order to gain

share in the apparel market through rough competition, the company might use an

expansion strategy and try to operate more new stores in the emerging markets.

There are some issues concerning the Chinese market where IC Companys’ sales have

been decreasing and the company experiences a relatively negative pace of business

development.

It could be concluded that there is harsh competition in the apparel industry and IC

Companys strives to capture market share by using growth strategy in the potential

emerging markets.

Page 28 of 157

5.3 Internal analysis

With the aim to create a clear picture and to better understand the activities through

which IC Companys develops a competitive advantage and creates value to its

shareholders, it is decided to proceed with value chain analysis, which defines a

company's strengths and weaknesses.

In his book "Competitive Advantage" published in 1985, Michael Porter presents

generic value chain model which consists of primary and supportive activities

(Netmba.com)

The figure 5.1 introduces the chain value model.

Figure 5.1 Porter’s chain value model

Source: www.netmba.com

As it is shown in figure 5.1 there are five main activities, namely, Inbound logistic,

Operations, Outbound logistics, Marketing & Sales and Service and four support

activities such as Infrastructure, Human Resource Management, Technology

Development and Procurement. Each activity has been structured to end up with

positive margin that creates value for a company.

In accordance with Michael Porter’s concept of the value chain, primary activities are

described as (learnmarketing.net & netmba.com):

Inbound Logistics: refers to raw materials being obtained from suppliers ready to

be used for producing the end product;

Page 29 of 157

Operations: include processes of transforming raw materials into finished

products and services;

Outbound Logistics: once the products have been manufactured they are ready to

be warehoused and distributed to customers;

Marketing and Sales: identification of needs targeted towards the correct

customer group. Marketing is used to establish an efficient strategy, thus

enhancing the generation of sales;

Service: after the product has been sold, the organization has to offer support

services. They might include such activities as after sales training, warranties

and guarantees.

The supportive activities assist the primary activities in aiding the organization to

achieve its competitive advantage. Aforementioned activities are supported by:

Firm Infrastructure: it is the set of various activities such as organizational

structure, control systems, company culture, etc., to ensure that the entity’s

finances, legal structure and management structure works efficiently enhancing

value creation;

Human Resource Management: in order to succeed in its objectives, the

organization needs to hire, train and develop its employees. Staff has to be

motivated and compensated properly if they are to stay with an organization and

add to it;

Technology Development: technologies are exploited to support value-creating

activities. It is used to reduce cost thus adding value; in research and

development to evolve new products and via the use of the Internet so customers

have access to online facilities;

Procurement: purchasing inputs such as raw materials and equipment obtaining

the best combination of price and quality.

To summarize, the value chain covers the whole entity and focuses on how primary and

supportive activities could cooperate together effectively in helping the organization to

gain an exceptional competitive advantage.

According to the Group’s operational model, it has been decided to adjust its primary

activities with the aim to comply with the steps of the value chain model.

Page 30 of 157

The first modification is the examination of the additional activity taking place before

Inbound Logistics such as Design. The main reason to start with this phase is related to

specific features of the fashion industry. Before placing orders in manufactures, garment

companies have to develop design of new collection.

5.3.1 Primary activities

5.3.1.1 Design

The design process includes designers’ creativity and inspiration coming alongside with

analysis of sales in stores. By examining data from individual stores, designers might

track customers’ preferences observing sales in each individual store. Following this

procedure, designers analyze fashion trends and gather inspiration for implementing

acquired ideas in new collection, therefore, to satisfy consumers’ desires.

5.3.1.2 Inbound Logistics and Operations

Inbound Logistics and Operations combine Outsourcing and Quality Control stages due

to the fact that IC Companys does not have its own production facilities. Instead of it,

the Group employs suppliers through its own shared sourcing offices which conduct

preliminary research with the aim to develop a unique flexibility. It implies the handling

of geographic sourcing alternatives safely and quickly, thereby moving production to

the most beneficial facilities in Eastern Europe and Asian countries.

As the final step just before manufactured apparel leaves production lines, some

examples of apparel have to pass quality tests conducted in Denmark. If apparel meets

quality requirements, it is ready to be delivered.

5.3.1.3 Outbound Logistics

Fashion industry is heavily dependent on delivery of products at the appropriate time

with convenient circumstances. There are two main distribution channels in IC

Companys, wholesale and retail, where the Group is liable by contract to deliver

finished goods from the sourcing countries directly to the wholesale customers within

the determined time range. In a case when demanded products do not reach the store

shelves at the right time, issues arise concerning the returned and surplus products that

create negative impact on sales thereby resulting in write-downs.

Page 31 of 157

Products to be realized through the Group’s retail channels are transported on container

lines to Europe where IC Companys has three large warehouses. Modern warehouse in

Brøndby that deals with the flat packages, a warehouse at Raffinaderivej, which handles

the Group’s hanging products, both located in Denmark, and a warehouse in Lódz,

Poland, responsible for surplus products and marketing material.

In general, the company’s products are handled in two ways: either distributed in flat

packages or hanging. The majority, approximately 90% of goods sourced in Asia, is

transported on container liners to Europe while the rest is sent by air freight. All the

merchandise sourced in Europe is transported by truckage (IC Companys’ annual report

2010/2011).

5.3.1.4 Marketing and Sales

Marketing

As stated before, IC Companys follows the multi-brand strategy when each brand has a

market-oriented management that handles market positioning, product development and

marketing – the activities that are essential to the development of each brand identity

and constitute the decisive factors for the customer’s decision to buy (IC Companys’

annual report 2009/2010).

Needless to say that the multi-brand strategy provides great opportunities, when brand

managers could concentrate on respective brand positioning and development acting in

line with a thoroughly planned brand strategy with a clearly defined fashion position

and market approach in accordance with the company’s business principles which

reduces the total business exposure. Moreover, each brand adds value by being a part of

IC Companys’ portfolio thus delivering financial results to the Group (IC Companys’

annual report 2010/2011).

Brands position themselves differently with respect to consumer groups, price horizon

and quality. In return, the Group covers various parts of the fashion market since brands

supplement each other. Therefore, brands could market themselves into various

segments and price levels thus boosting sales.

With the aim to gain more awareness, IC Companys has created showrooms for all its

eleven brands for displaying new collections to current and potential customers.

Over several years, the Group has been headquartered on Amager, in an area that is now

transforming into a regular fashion district in Copenhagen, where more than 30 different

Page 32 of 157

Danish and international brands are presented in 16 individually designed showrooms

(modebranchen.nu, 2012).

Sales

The key focus for all brands is to achieve sales growth and build equity while

prioritizing investments with respect to return on investment and enforcing tight cost

control (IC Companys’ annual report 2010/2011). The strategy of multi-branding

implies the supplement so that customers associate the individual product with IC

Companys. That gives the company a better position in the fashion market where single

brands do possess a tiny fraction of the total market, but a multi-brand company holds a

substantial market share.

As mentioned above, IC Companys uses two channels of distribution, namely,

wholesale and retail. Wholesale dealers sell other brands apart from the Group’s ones.

As a part of wholesale activities, they include franchise stores which pay to IC

Companys to be under the company’s umbrella. The second type of distribution channel

is retail. It involves own stores, outlet stores and e-commerce.

There are shops that only sell individual brands as well as multi-brand stores selling all

the Group’s brands under shops named “IC Companys”. The network of outlets stores

surplus products and sell them during the year as the main purpose of such stores is to

realize out-of-date apparel from previous collections. Furthermore, any products that

cannot be sold through own outlets are sold to brokers for resale outside the Group’s

established markets (IC Companys’annual report 2010/2011). More hard data regarding

distribution channels are given in the Introduction under Products, Distribution

channels and Markets parts.

5.3.1.5 Service

According to authors’ experience and a short interview with IC Companys’ shop seller

who operates in Fisketorv shopping mall in Copenhagen, it could be stated that products

bought in IC Companys' shops have different service options. For example, in the shop

that operates in Fisketorv, it is possible to return product within 3 days if a receipt is

shown; however, this service does not cover products bought with discount. It also has

to be mentioned that according to the seller, other IC Companys shops have different

obligations and periods for refunding, which might vary from 3 days to 2 weeks. All in

Page 33 of 157

all, it could be concluded that service concerning warranties is different from shop to

shop.

5.3.2 Supportive activities

5.3.2.1 Firm Infrastructure

Despite quite short history, IC Companys has undergone through turbulent periods.

Since the origin of the Group, there were various changes such as the implementation of

the multi-brand strategy, the adjustment of organizational structure and the appointment

of new management team.

After the merger of Inwear Group A/S and Carli Gry International A/S, the newly

created IC Companys has followed centralized form of organization. It implies that the

common company’s management was in charge of all operations both external and

internal ones.

In 2004 the Group has adopted a new multi-brand strategy, with the objective to

maximize the return on a portfolio of independent fashion brands. A market-oriented

management of each brand became responsible for market positioning, product

development and sales. At the same time, there was launched a shared platform for the

brand portfolio which handles and supports all the supply activities that are not relevant

for each particular brand, which included such activities as sourcing, sales, production,

logistics, administration, IT, finance and HR (IC Companys’ annual report 2004/2005).

The starting financial crisis in 2007 had a negative influence on the Group’s

performance as on the whole economy. In such a challenging environment, IC

Companys has failed in cost reduction policy with respect to revenues development.

Therefore, it might be assumed that it was the main reason for the IC Companys to

change its management team.

The new management team has continued the decentralization path what resulted in

giving all 11 brands a full responsibility and power of decision making. It involves full

amenability of entire value chain, including distribution (just-style.com, 2010).

Currently, IC Companys has a two-layer organizational structure: shared service

platform and multi-brand strategy. Figure 5.2 shows separate brand organizations with

full responsibility of own value chain (IC Companys, Corporate presentation, 2012):

Page 34 of 157

Figure 5.2 IC Companys’ organizational structure

Source: IC Companys’ press release

5.3.2.2 Human Resource Management

In the contemporary global markets almost all products follow with services. High

quality service existence creates additional value and supports companies' preferable

brand building.

Therefore, IC Companys has developed a professional HR strategy. The HR department

is in charge of the development and updating of methods and tools assisting in

prioritizing and continuously evaluating the employees’ performance (IC Companys’

annual report 2010/2011).

Beside value benefits, highly managed customer service also helps companies to

differentiate themselves from their rivals. With the aim to provide better services IC

Companys is highly focused on HR management and supports employee training by

providing Retail, Leaders, Sales and Brands Academies. HR chief Morten Linnet states

that Retail Academy has been created with a target to support the company’s business

by developing fantastic service, more sales and better carrier possibilities

(fashionforum.dk, 2010). Moreover, in cooperation with consulting agency Franklin

Covey, IC Companys has created a professional leadership program for the Group’s

many leaders to learn new skills in order to enhance the execution of the multi-brand

strategy (Franklincovey.dk, 2012).

Page 35 of 157

5.3.2.3 Technology Development

Besides the factors mentioned in the PESTEL analysis, such as online sales of apparel

and descriptive websites which refer to each brand, a well-developed IT system ensures

more synchronization in the company’s operations. In fact, IC Companys has been

investing substantial funds in IT systems, specifically in SAP Enterprise Resource

Planning (ERP). The Group’s previous IT architecture consisted of several independent

systems, which were not supportive of business activity and needs for quick and

accurate financial reporting (sap.com, 2011). Thus, the two-phase implementation of

SAP ERP in the years of 2007 and 2008, has allowed IC Companys to gain control of

all economic processes in the Group such as financial management, reporting and

accounting.

As a part of SAP ERP system, IC Companys has implemented SAP Business

Communications Management to improve its customer relationships with business

communications. It implies providing efficient sales service to retail and franchise

partners (ecenta.com, 2009).

5.3.2.4 Procurement

The implementation of the multi-brand strategy led to the shifting of purchasing

function to individual brand managers. As the next step, brand managers make

purchases through the Group’s own shared sourcing offices in China (including Hong

Kong), Bangladesh, Vietnam, India and Romania and to a limited extent by the use of

agents. Therefore, it is no longer a supportive activity, but part of the primary activities

under Inbound and Operations.

More specifically, procurement activities might involve purchasing of commercial

premises, tangible goods and transport services that are related to the shared platform,

however, are not clearly related to the individual brands.

Page 36 of 157

Summary

All activities directly relating to the each brand are under the responsibilities of

respective brand managers, whereas the activities which have no relevance to brand

identity are handled through the shared service platform. Therefore, the multi-brand

strategy allows brand managers to focus on the development of the individual brand.

All in all, authors find IC Companys’ value chain optimal. There cannot be determined

any activities which do not create value and thus should be outsourced. It is reasonable

that the Group has outsourced the manufacturing function and in result could free

additional funds for creating a greater value in the value chain.

However, there is always a room for improvement in already working principles. In

order to succeed in its multi-brand strategy, each brand should overhaul all its value

chain activities. For instance, an individual brand management has to keep track of sales

to determine which products are less attractive to consumers and thus to change next

collection design ideas.

5.4 Core Competencies

According to Prahalad and Hamel, core competencies are defined as (Prahalad &

Hamel, 2009):

“…the company’s collective knowledge about how to coordinate diverse production

skills and technologies… creating unique, integrated systems that reinforce fit among

your firm’s diverse production and technology skills – a systemic advantage your

competitors can’t copy…”

After the examination of the Group’s value chain, authors have found out three core

competencies of the company: sourcing activities, the multi-brand strategy and human

resource management. These three distinguishing features are the pillars of the Group’s

business which create value and help to compete in an intensive apparel market.

Now, authors will briefly introduce each core competence. First of all, there comes the

multi-brand strategy idea to delegate brand-building activities to the individual brand

management. These individual units enjoyed autonomy in design, sales and marketing,

thus forming dedicated brand teams for the respective functions. This was combined

with a shared service platform to gain efficiencies through the joint operations of