stochastic calculus for finance - michigan state...

TRANSCRIPT

Stochastic Calculus for Finance

Albert Cohen

Actuarial Sciences ProgramDepartment of Mathematics

Department of Statistics and ProbabilityA336 Wells Hall

Michigan State UniversityEast Lansing MI

[email protected]@stt.msu.edu

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 1 / 249

Course Information

Syllabus to be posted on class page in first week of classes

Homework assignments will posted there as well

Page can be found athttps://www.stt.msu.edu/Academics/ClassPages/

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 2 / 249

Course Information

Many examples within these slides are used with kind permission ofProf. Dmitry Kramkov, Dept. of Mathematics, Carnegie MellonUniversity.

Course Textbook: Stochastic Calculus for Finance (Springer Finance.)

Some examples here will be similar to those practice questionspublicly released by the SOA. Please note the SOA owns thecopyright to these questions.

This book will be our reference, and some questions for assignmentswill be chosen from it. Copyright for all questions used from this bookbelongs to Springer.

From time to time, we will also follow the format of Marcel Finan’s ADiscussion of Financial Economics in Actuarial Models: A Preparationfor the Actuarial Exam MFE/3F. Some proofs from there will bereferenced as well. Please find these notes here

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 3 / 249

What are financial securities?

Traded Securities - price given by market.

For example:

StocksCommodities

Non-Traded Securities - price remains to be computed.

Is this always true?

We will focus on pricing non-traded securities.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 4 / 249

What are financial securities?

Traded Securities - price given by market.

For example:

StocksCommodities

Non-Traded Securities - price remains to be computed.

Is this always true?

We will focus on pricing non-traded securities.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 4 / 249

What are financial securities?

Traded Securities - price given by market.

For example:

StocksCommodities

Non-Traded Securities - price remains to be computed.

Is this always true?

We will focus on pricing non-traded securities.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 4 / 249

What are financial securities?

Traded Securities - price given by market.

For example:

StocksCommodities

Non-Traded Securities - price remains to be computed.

Is this always true?

We will focus on pricing non-traded securities.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 4 / 249

How does one fairly price non-traded securities?

By eliminating all unfair prices

Unfair prices arise from Arbitrage Strategies

Start with zero capitalEnd with non-zero wealth

We will search for arbitrage-free strategies to replicate the payoff of anon-traded security

This replication is at the heart of the engineering of financial products

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 5 / 249

How does one fairly price non-traded securities?

By eliminating all unfair prices

Unfair prices arise from Arbitrage Strategies

Start with zero capitalEnd with non-zero wealth

We will search for arbitrage-free strategies to replicate the payoff of anon-traded security

This replication is at the heart of the engineering of financial products

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 5 / 249

How does one fairly price non-traded securities?

By eliminating all unfair prices

Unfair prices arise from Arbitrage Strategies

Start with zero capitalEnd with non-zero wealth

We will search for arbitrage-free strategies to replicate the payoff of anon-traded security

This replication is at the heart of the engineering of financial products

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 5 / 249

How does one fairly price non-traded securities?

By eliminating all unfair prices

Unfair prices arise from Arbitrage Strategies

Start with zero capitalEnd with non-zero wealth

We will search for arbitrage-free strategies to replicate the payoff of anon-traded security

This replication is at the heart of the engineering of financial products

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 5 / 249

How does one fairly price non-traded securities?

By eliminating all unfair prices

Unfair prices arise from Arbitrage Strategies

Start with zero capitalEnd with non-zero wealth

We will search for arbitrage-free strategies to replicate the payoff of anon-traded security

This replication is at the heart of the engineering of financial products

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 5 / 249

More Questions

Existence - Does such a fair price always exist?

If not, what is needed of our financial model to guarantee at least onearbitrage-free price?

Uniqueness - are there conditions where exactly one arbitrage-freeprice exists?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 6 / 249

And What About...

Does the replicating strategy and price computed reflect uncertaintyin the market?

Mathematically, if P is a probabilty measure attached to a series ofprice movements in underlying asset, is P used in computing theprice?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 7 / 249

And What About...

Does the replicating strategy and price computed reflect uncertaintyin the market?

Mathematically, if P is a probabilty measure attached to a series ofprice movements in underlying asset, is P used in computing theprice?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 7 / 249

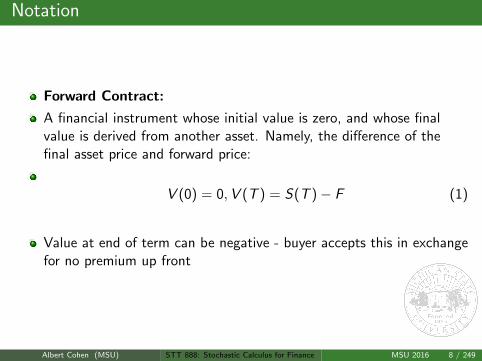

Notation

Forward Contract:

A financial instrument whose initial value is zero, and whose finalvalue is derived from another asset. Namely, the difference of thefinal asset price and forward price:

V (0) = 0,V (T ) = S(T )− F (1)

Value at end of term can be negative - buyer accepts this in exchangefor no premium up front

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 8 / 249

Notation

Forward Contract:

A financial instrument whose initial value is zero, and whose finalvalue is derived from another asset. Namely, the difference of thefinal asset price and forward price:

V (0) = 0,V (T ) = S(T )− F (1)

Value at end of term can be negative - buyer accepts this in exchangefor no premium up front

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 8 / 249

Notation

Forward Contract:

A financial instrument whose initial value is zero, and whose finalvalue is derived from another asset. Namely, the difference of thefinal asset price and forward price:

V (0) = 0,V (T ) = S(T )− F (1)

Value at end of term can be negative - buyer accepts this in exchangefor no premium up front

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 8 / 249

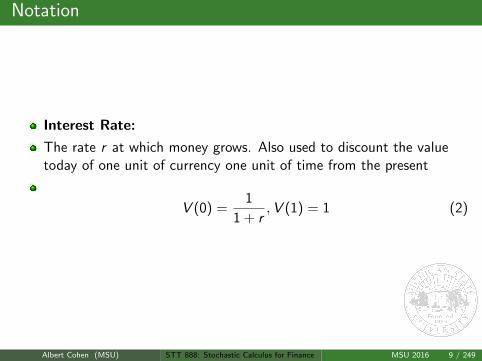

Notation

Interest Rate:

The rate r at which money grows. Also used to discount the valuetoday of one unit of currency one unit of time from the present

V (0) =1

1 + r,V (1) = 1 (2)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 9 / 249

Notation

Interest Rate:

The rate r at which money grows. Also used to discount the valuetoday of one unit of currency one unit of time from the present

V (0) =1

1 + r,V (1) = 1 (2)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 9 / 249

An Example of Replication

Forward Exchange Rate: There are two currencies, foreign anddomestic:

SBA = 4 is the spot exchange rate - one unit of B is worth SB

A of Atoday (time 0)

rA = 0.1 is the domestic borrow/lend rate

rB = 0.2 is the foreign borrow/lend rate

Compute the forward exchange rate FBA . This is the value of one unit

of B in terms of A at time 1.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 10 / 249

An Example of Replication

Forward Exchange Rate: There are two currencies, foreign anddomestic:

SBA = 4 is the spot exchange rate - one unit of B is worth SB

A of Atoday (time 0)

rA = 0.1 is the domestic borrow/lend rate

rB = 0.2 is the foreign borrow/lend rate

Compute the forward exchange rate FBA . This is the value of one unit

of B in terms of A at time 1.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 10 / 249

An Example of Replication

Forward Exchange Rate: There are two currencies, foreign anddomestic:

SBA = 4 is the spot exchange rate - one unit of B is worth SB

A of Atoday (time 0)

rA = 0.1 is the domestic borrow/lend rate

rB = 0.2 is the foreign borrow/lend rate

Compute the forward exchange rate FBA . This is the value of one unit

of B in terms of A at time 1.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 10 / 249

An Example of Replication

Forward Exchange Rate: There are two currencies, foreign anddomestic:

SBA = 4 is the spot exchange rate - one unit of B is worth SB

A of Atoday (time 0)

rA = 0.1 is the domestic borrow/lend rate

rB = 0.2 is the foreign borrow/lend rate

Compute the forward exchange rate FBA . This is the value of one unit

of B in terms of A at time 1.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 10 / 249

An Example of Replication

Forward Exchange Rate: There are two currencies, foreign anddomestic:

SBA = 4 is the spot exchange rate - one unit of B is worth SB

A of Atoday (time 0)

rA = 0.1 is the domestic borrow/lend rate

rB = 0.2 is the foreign borrow/lend rate

Compute the forward exchange rate FBA . This is the value of one unit

of B in terms of A at time 1.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 10 / 249

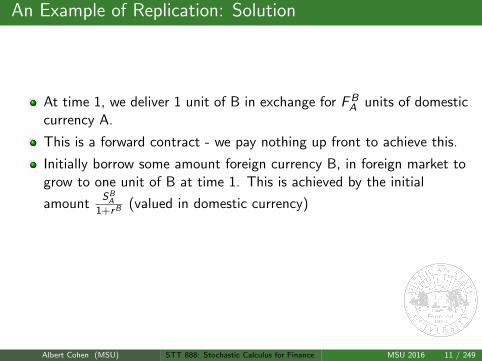

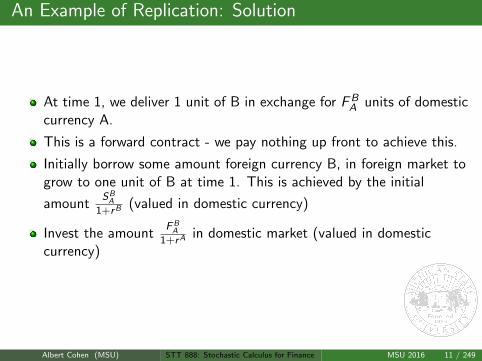

An Example of Replication: Solution

At time 1, we deliver 1 unit of B in exchange for FBA units of domestic

currency A.

This is a forward contract - we pay nothing up front to achieve this.

Initially borrow some amount foreign currency B, in foreign market togrow to one unit of B at time 1. This is achieved by the initial

amountSBA

1+rB(valued in domestic currency)

Invest the amountFBA

1+rAin domestic market (valued in domestic

currency)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 11 / 249

An Example of Replication: Solution

At time 1, we deliver 1 unit of B in exchange for FBA units of domestic

currency A.

This is a forward contract - we pay nothing up front to achieve this.

Initially borrow some amount foreign currency B, in foreign market togrow to one unit of B at time 1. This is achieved by the initial

amountSBA

1+rB(valued in domestic currency)

Invest the amountFBA

1+rAin domestic market (valued in domestic

currency)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 11 / 249

An Example of Replication: Solution

At time 1, we deliver 1 unit of B in exchange for FBA units of domestic

currency A.

This is a forward contract - we pay nothing up front to achieve this.

Initially borrow some amount foreign currency B, in foreign market togrow to one unit of B at time 1. This is achieved by the initial

amountSBA

1+rB(valued in domestic currency)

Invest the amountFBA

1+rAin domestic market (valued in domestic

currency)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 11 / 249

An Example of Replication: Solution

At time 1, we deliver 1 unit of B in exchange for FBA units of domestic

currency A.

This is a forward contract - we pay nothing up front to achieve this.

Initially borrow some amount foreign currency B, in foreign market togrow to one unit of B at time 1. This is achieved by the initial

amountSBA

1+rB(valued in domestic currency)

Invest the amountFBA

1+rAin domestic market (valued in domestic

currency)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 11 / 249

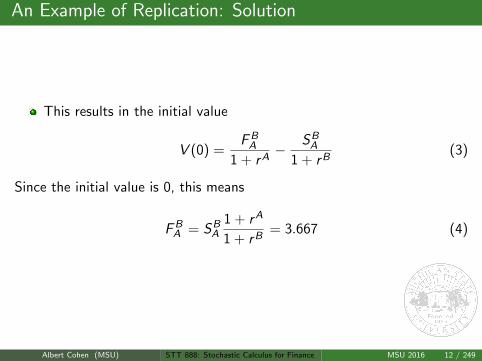

An Example of Replication: Solution

This results in the initial value

V (0) =FBA

1 + rA−

SBA

1 + rB(3)

Since the initial value is 0, this means

FBA = SB

A

1 + rA

1 + rB= 3.667 (4)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 12 / 249

An Example of Replication: Solution

This results in the initial value

V (0) =FBA

1 + rA−

SBA

1 + rB(3)

Since the initial value is 0, this means

FBA = SB

A

1 + rA

1 + rB= 3.667 (4)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 12 / 249

Outline1 Discrete Multiperiod Model

ArbitrageRisk Neutral ProbabilityAmerican OptionsExotic OptionsValuation via Simulation

2 Continuous Model-Ito CalculusBrownian MotionBSMExamplesOptions on FuturesPath Dependent Options

3 Advanced TopicsHeat EquationGeneral Solution of Heat EquationApplication to B-S-M PDE

4 Continuous Model-ProbabilityExpected ValuesApplication of Option GreeksAlbert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 13 / 249

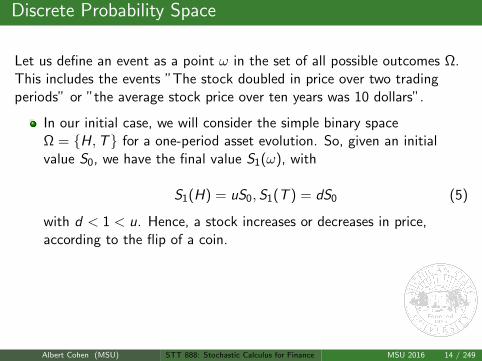

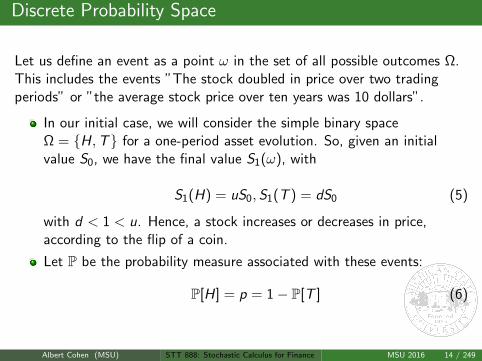

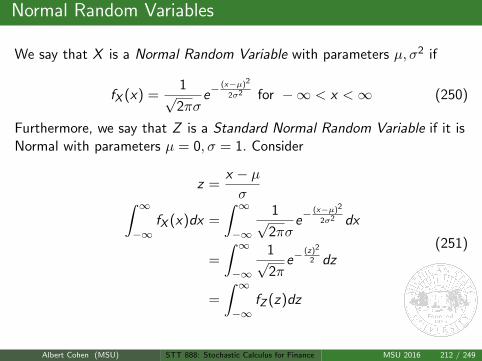

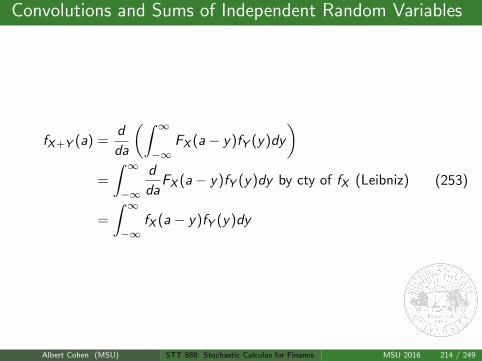

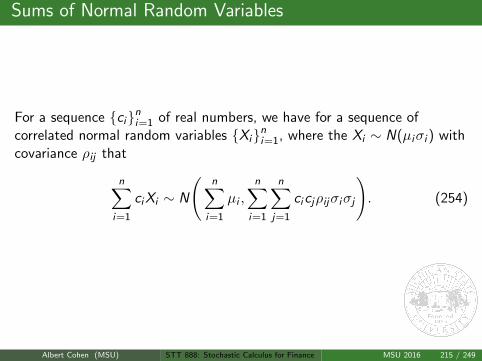

Discrete Probability Space

Let us define an event as a point ω in the set of all possible outcomes Ω.This includes the events ”The stock doubled in price over two tradingperiods” or ”the average stock price over ten years was 10 dollars”.

In our initial case, we will consider the simple binary spaceΩ = H,T for a one-period asset evolution. So, given an initialvalue S0, we have the final value S1(ω), with

S1(H) = uS0,S1(T ) = dS0 (5)

with d < 1 < u. Hence, a stock increases or decreases in price,according to the flip of a coin.

Let P be the probability measure associated with these events:

P[H] = p = 1− P[T ] (6)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 14 / 249

Discrete Probability Space

Let us define an event as a point ω in the set of all possible outcomes Ω.This includes the events ”The stock doubled in price over two tradingperiods” or ”the average stock price over ten years was 10 dollars”.

In our initial case, we will consider the simple binary spaceΩ = H,T for a one-period asset evolution. So, given an initialvalue S0, we have the final value S1(ω), with

S1(H) = uS0,S1(T ) = dS0 (5)

with d < 1 < u. Hence, a stock increases or decreases in price,according to the flip of a coin.

Let P be the probability measure associated with these events:

P[H] = p = 1− P[T ] (6)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 14 / 249

Discrete Probability Space

Let us define an event as a point ω in the set of all possible outcomes Ω.This includes the events ”The stock doubled in price over two tradingperiods” or ”the average stock price over ten years was 10 dollars”.

In our initial case, we will consider the simple binary spaceΩ = H,T for a one-period asset evolution. So, given an initialvalue S0, we have the final value S1(ω), with

S1(H) = uS0,S1(T ) = dS0 (5)

with d < 1 < u. Hence, a stock increases or decreases in price,according to the flip of a coin.

Let P be the probability measure associated with these events:

P[H] = p = 1− P[T ] (6)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 14 / 249

Discrete Probability Space

Let us define an event as a point ω in the set of all possible outcomes Ω.This includes the events ”The stock doubled in price over two tradingperiods” or ”the average stock price over ten years was 10 dollars”.

In our initial case, we will consider the simple binary spaceΩ = H,T for a one-period asset evolution. So, given an initialvalue S0, we have the final value S1(ω), with

S1(H) = uS0,S1(T ) = dS0 (5)

with d < 1 < u. Hence, a stock increases or decreases in price,according to the flip of a coin.

Let P be the probability measure associated with these events:

P[H] = p = 1− P[T ] (6)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 14 / 249

Discrete Probability Space

Let us define an event as a point ω in the set of all possible outcomes Ω.This includes the events ”The stock doubled in price over two tradingperiods” or ”the average stock price over ten years was 10 dollars”.

In our initial case, we will consider the simple binary spaceΩ = H,T for a one-period asset evolution. So, given an initialvalue S0, we have the final value S1(ω), with

S1(H) = uS0,S1(T ) = dS0 (5)

with d < 1 < u. Hence, a stock increases or decreases in price,according to the flip of a coin.

Let P be the probability measure associated with these events:

P[H] = p = 1− P[T ] (6)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 14 / 249

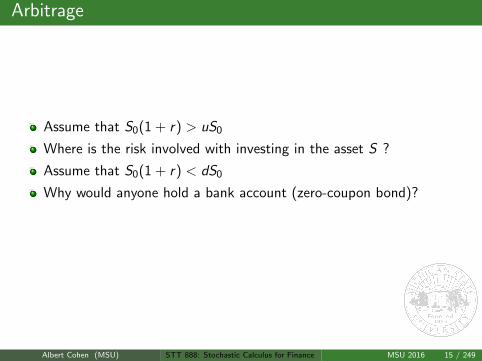

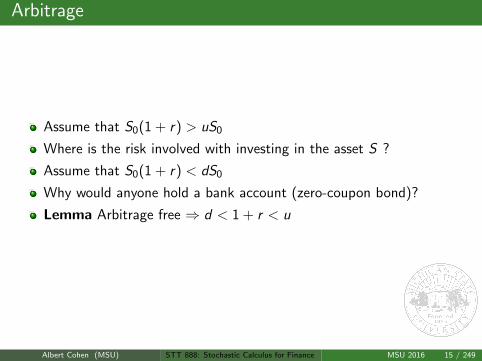

Arbitrage

Assume that S0(1 + r) > uS0

Where is the risk involved with investing in the asset S ?

Assume that S0(1 + r) < dS0

Why would anyone hold a bank account (zero-coupon bond)?

Lemma Arbitrage free ⇒ d < 1 + r < u

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 15 / 249

Arbitrage

Assume that S0(1 + r) > uS0

Where is the risk involved with investing in the asset S ?

Assume that S0(1 + r) < dS0

Why would anyone hold a bank account (zero-coupon bond)?

Lemma Arbitrage free ⇒ d < 1 + r < u

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 15 / 249

Arbitrage

Assume that S0(1 + r) > uS0

Where is the risk involved with investing in the asset S ?

Assume that S0(1 + r) < dS0

Why would anyone hold a bank account (zero-coupon bond)?

Lemma Arbitrage free ⇒ d < 1 + r < u

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 15 / 249

Arbitrage

Assume that S0(1 + r) > uS0

Where is the risk involved with investing in the asset S ?

Assume that S0(1 + r) < dS0

Why would anyone hold a bank account (zero-coupon bond)?

Lemma Arbitrage free ⇒ d < 1 + r < u

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 15 / 249

Arbitrage

Assume that S0(1 + r) > uS0

Where is the risk involved with investing in the asset S ?

Assume that S0(1 + r) < dS0

Why would anyone hold a bank account (zero-coupon bond)?

Lemma Arbitrage free ⇒ d < 1 + r < u

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 15 / 249

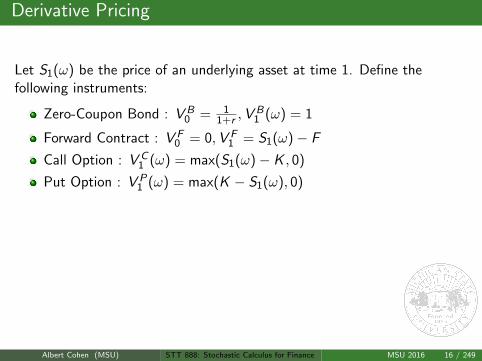

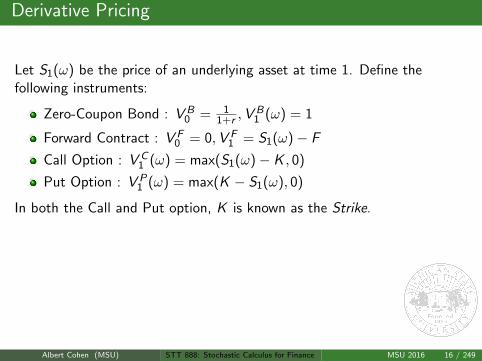

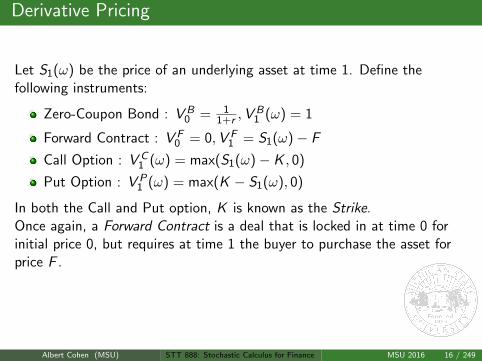

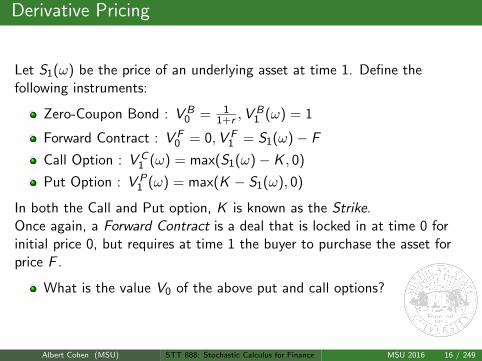

Derivative Pricing

Let S1(ω) be the price of an underlying asset at time 1. Define thefollowing instruments:

Zero-Coupon Bond : V B0 = 1

1+r ,VB1 (ω) = 1

Forward Contract : V F0 = 0,V F

1 = S1(ω)− F

Call Option : V C1 (ω) = max(S1(ω)− K , 0)

Put Option : V P1 (ω) = max(K − S1(ω), 0)

In both the Call and Put option, K is known as the Strike.Once again, a Forward Contract is a deal that is locked in at time 0 forinitial price 0, but requires at time 1 the buyer to purchase the asset forprice F .

What is the value V0 of the above put and call options?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 16 / 249

Derivative Pricing

Let S1(ω) be the price of an underlying asset at time 1. Define thefollowing instruments:

Zero-Coupon Bond : V B0 = 1

1+r ,VB1 (ω) = 1

Forward Contract : V F0 = 0,V F

1 = S1(ω)− F

Call Option : V C1 (ω) = max(S1(ω)− K , 0)

Put Option : V P1 (ω) = max(K − S1(ω), 0)

In both the Call and Put option, K is known as the Strike.Once again, a Forward Contract is a deal that is locked in at time 0 forinitial price 0, but requires at time 1 the buyer to purchase the asset forprice F .

What is the value V0 of the above put and call options?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 16 / 249

Derivative Pricing

Let S1(ω) be the price of an underlying asset at time 1. Define thefollowing instruments:

Zero-Coupon Bond : V B0 = 1

1+r ,VB1 (ω) = 1

Forward Contract : V F0 = 0,V F

1 = S1(ω)− F

Call Option : V C1 (ω) = max(S1(ω)− K , 0)

Put Option : V P1 (ω) = max(K − S1(ω), 0)

In both the Call and Put option, K is known as the Strike.

Once again, a Forward Contract is a deal that is locked in at time 0 forinitial price 0, but requires at time 1 the buyer to purchase the asset forprice F .

What is the value V0 of the above put and call options?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 16 / 249

Derivative Pricing

Let S1(ω) be the price of an underlying asset at time 1. Define thefollowing instruments:

Zero-Coupon Bond : V B0 = 1

1+r ,VB1 (ω) = 1

Forward Contract : V F0 = 0,V F

1 = S1(ω)− F

Call Option : V C1 (ω) = max(S1(ω)− K , 0)

Put Option : V P1 (ω) = max(K − S1(ω), 0)

In both the Call and Put option, K is known as the Strike.Once again, a Forward Contract is a deal that is locked in at time 0 forinitial price 0, but requires at time 1 the buyer to purchase the asset forprice F .

What is the value V0 of the above put and call options?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 16 / 249

Derivative Pricing

Let S1(ω) be the price of an underlying asset at time 1. Define thefollowing instruments:

Zero-Coupon Bond : V B0 = 1

1+r ,VB1 (ω) = 1

Forward Contract : V F0 = 0,V F

1 = S1(ω)− F

Call Option : V C1 (ω) = max(S1(ω)− K , 0)

Put Option : V P1 (ω) = max(K − S1(ω), 0)

In both the Call and Put option, K is known as the Strike.Once again, a Forward Contract is a deal that is locked in at time 0 forinitial price 0, but requires at time 1 the buyer to purchase the asset forprice F .

What is the value V0 of the above put and call options?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 16 / 249

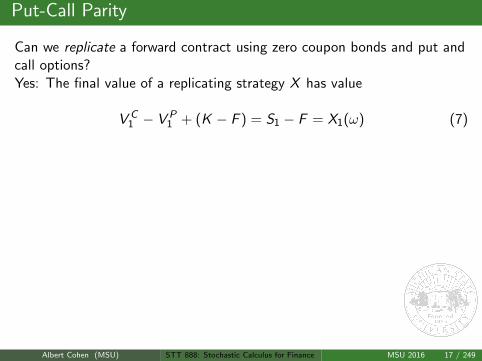

Put-Call Parity

Can we replicate a forward contract using zero coupon bonds and put andcall options?

Yes: The final value of a replicating strategy X has value

V C1 − V P

1 + (K − F ) = S1 − F = X1(ω) (7)

This is achieved (replicated) by

Purchasing one call option

Selling one put option

Purchasing K − F zero coupon bonds with value 1 at maturity.

all at time 0.Since this strategy must have zero initial value, we obtain

V C0 − V P

0 =F − K

1 + r(8)

Question: How would this change in a multi-period model?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 17 / 249

Put-Call Parity

Can we replicate a forward contract using zero coupon bonds and put andcall options?Yes: The final value of a replicating strategy X has value

V C1 − V P

1 + (K − F ) = S1 − F = X1(ω) (7)

This is achieved (replicated) by

Purchasing one call option

Selling one put option

Purchasing K − F zero coupon bonds with value 1 at maturity.

all at time 0.Since this strategy must have zero initial value, we obtain

V C0 − V P

0 =F − K

1 + r(8)

Question: How would this change in a multi-period model?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 17 / 249

Put-Call Parity

Can we replicate a forward contract using zero coupon bonds and put andcall options?Yes: The final value of a replicating strategy X has value

V C1 − V P

1 + (K − F ) = S1 − F = X1(ω) (7)

This is achieved (replicated) by

Purchasing one call option

Selling one put option

Purchasing K − F zero coupon bonds with value 1 at maturity.

all at time 0.Since this strategy must have zero initial value, we obtain

V C0 − V P

0 =F − K

1 + r(8)

Question: How would this change in a multi-period model?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 17 / 249

Put-Call Parity

Can we replicate a forward contract using zero coupon bonds and put andcall options?Yes: The final value of a replicating strategy X has value

V C1 − V P

1 + (K − F ) = S1 − F = X1(ω) (7)

This is achieved (replicated) by

Purchasing one call option

Selling one put option

Purchasing K − F zero coupon bonds with value 1 at maturity.

all at time 0.

Since this strategy must have zero initial value, we obtain

V C0 − V P

0 =F − K

1 + r(8)

Question: How would this change in a multi-period model?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 17 / 249

Put-Call Parity

Can we replicate a forward contract using zero coupon bonds and put andcall options?Yes: The final value of a replicating strategy X has value

V C1 − V P

1 + (K − F ) = S1 − F = X1(ω) (7)

This is achieved (replicated) by

Purchasing one call option

Selling one put option

Purchasing K − F zero coupon bonds with value 1 at maturity.

all at time 0.Since this strategy must have zero initial value, we obtain

V C0 − V P

0 =F − K

1 + r(8)

Question: How would this change in a multi-period model?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 17 / 249

Put-Call Parity

Can we replicate a forward contract using zero coupon bonds and put andcall options?Yes: The final value of a replicating strategy X has value

V C1 − V P

1 + (K − F ) = S1 − F = X1(ω) (7)

This is achieved (replicated) by

Purchasing one call option

Selling one put option

Purchasing K − F zero coupon bonds with value 1 at maturity.

all at time 0.Since this strategy must have zero initial value, we obtain

V C0 − V P

0 =F − K

1 + r(8)

Question: How would this change in a multi-period model?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 17 / 249

General Derivative Pricing -One period model

If we begin with some initial capital X0, then we end with X1(ω). To pricea derivative, we need to match

X1(ω) = V1(ω) ∀ ω ∈ Ω (9)

to have X0 = V0, the price of the derivative we seek.

A strategy by the pair (X0,∆0) wherein

X0 is the initial capital

∆0 is the initial number of shares (units of underlying asset.)

What does the sign of ∆0 indicate?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 18 / 249

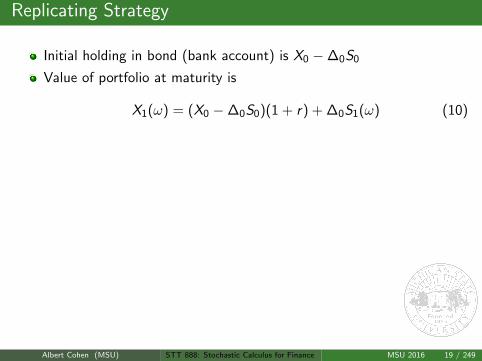

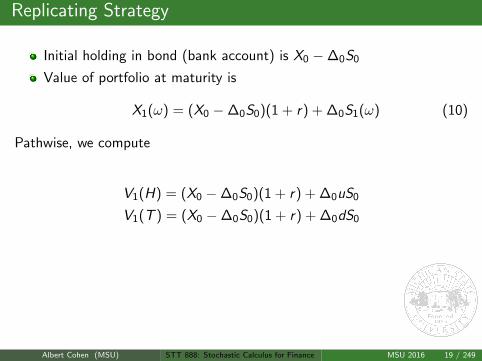

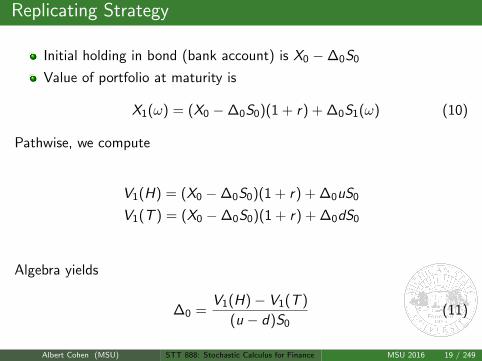

Replicating Strategy

Initial holding in bond (bank account) is X0 −∆0S0

Value of portfolio at maturity is

X1(ω) = (X0 −∆0S0)(1 + r) + ∆0S1(ω) (10)

Pathwise, we compute

V1(H) = (X0 −∆0S0)(1 + r) + ∆0uS0

V1(T ) = (X0 −∆0S0)(1 + r) + ∆0dS0

Algebra yields

∆0 =V1(H)− V1(T )

(u − d)S0(11)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 19 / 249

Replicating Strategy

Initial holding in bond (bank account) is X0 −∆0S0

Value of portfolio at maturity is

X1(ω) = (X0 −∆0S0)(1 + r) + ∆0S1(ω) (10)

Pathwise, we compute

V1(H) = (X0 −∆0S0)(1 + r) + ∆0uS0

V1(T ) = (X0 −∆0S0)(1 + r) + ∆0dS0

Algebra yields

∆0 =V1(H)− V1(T )

(u − d)S0(11)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 19 / 249

Replicating Strategy

Initial holding in bond (bank account) is X0 −∆0S0

Value of portfolio at maturity is

X1(ω) = (X0 −∆0S0)(1 + r) + ∆0S1(ω) (10)

Pathwise, we compute

V1(H) = (X0 −∆0S0)(1 + r) + ∆0uS0

V1(T ) = (X0 −∆0S0)(1 + r) + ∆0dS0

Algebra yields

∆0 =V1(H)− V1(T )

(u − d)S0(11)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 19 / 249

Replicating Strategy

Initial holding in bond (bank account) is X0 −∆0S0

Value of portfolio at maturity is

X1(ω) = (X0 −∆0S0)(1 + r) + ∆0S1(ω) (10)

Pathwise, we compute

V1(H) = (X0 −∆0S0)(1 + r) + ∆0uS0

V1(T ) = (X0 −∆0S0)(1 + r) + ∆0dS0

Algebra yields

∆0 =V1(H)− V1(T )

(u − d)S0(11)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 19 / 249

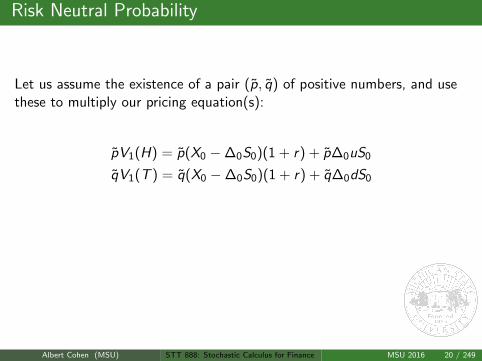

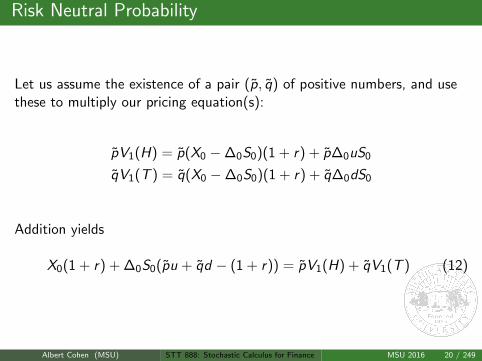

Risk Neutral Probability

Let us assume the existence of a pair (p, q) of positive numbers, and usethese to multiply our pricing equation(s):

pV1(H) = p(X0 −∆0S0)(1 + r) + p∆0uS0

qV1(T ) = q(X0 −∆0S0)(1 + r) + q∆0dS0

Addition yields

X0(1 + r) + ∆0S0(pu + qd − (1 + r)) = pV1(H) + qV1(T ) (12)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 20 / 249

Risk Neutral Probability

Let us assume the existence of a pair (p, q) of positive numbers, and usethese to multiply our pricing equation(s):

pV1(H) = p(X0 −∆0S0)(1 + r) + p∆0uS0

qV1(T ) = q(X0 −∆0S0)(1 + r) + q∆0dS0

Addition yields

X0(1 + r) + ∆0S0(pu + qd − (1 + r)) = pV1(H) + qV1(T ) (12)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 20 / 249

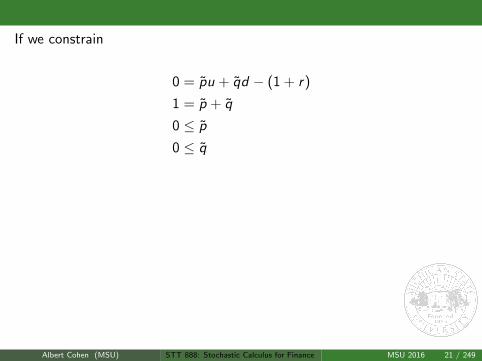

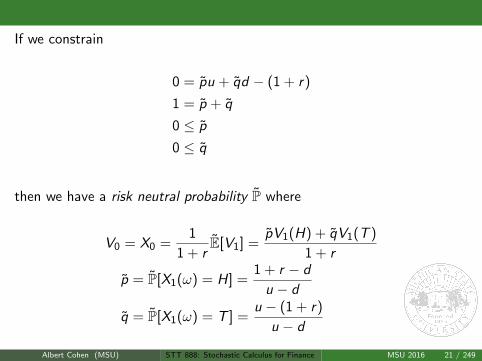

If we constrain

0 = pu + qd − (1 + r)

1 = p + q

0 ≤ p

0 ≤ q

then we have a risk neutral probability P where

V0 = X0 =1

1 + rE[V1] =

pV1(H) + qV1(T )

1 + r

p = P[X1(ω) = H] =1 + r − d

u − d

q = P[X1(ω) = T ] =u − (1 + r)

u − d

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 21 / 249

If we constrain

0 = pu + qd − (1 + r)

1 = p + q

0 ≤ p

0 ≤ q

then we have a risk neutral probability P where

V0 = X0 =1

1 + rE[V1] =

pV1(H) + qV1(T )

1 + r

p = P[X1(ω) = H] =1 + r − d

u − d

q = P[X1(ω) = T ] =u − (1 + r)

u − d

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 21 / 249

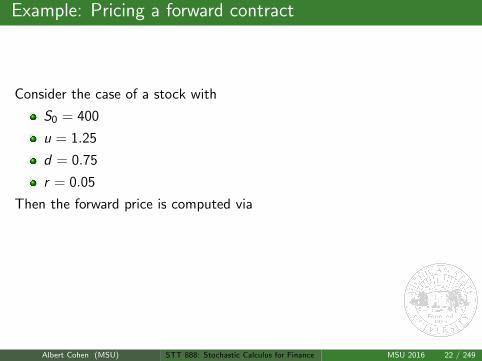

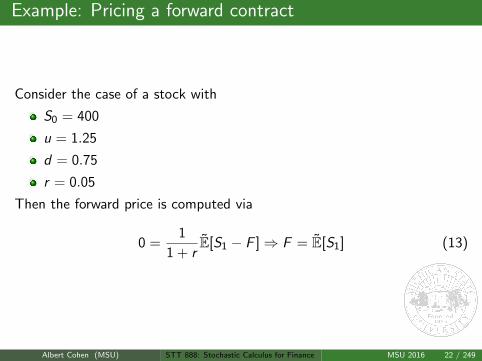

Example: Pricing a forward contract

Consider the case of a stock with

S0 = 400

u = 1.25

d = 0.75

r = 0.05

Then the forward price is computed via

0 =1

1 + rE[S1 − F ]⇒ F = E[S1] (13)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 22 / 249

Example: Pricing a forward contract

Consider the case of a stock with

S0 = 400

u = 1.25

d = 0.75

r = 0.05

Then the forward price is computed via

0 =1

1 + rE[S1 − F ]⇒ F = E[S1] (13)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 22 / 249

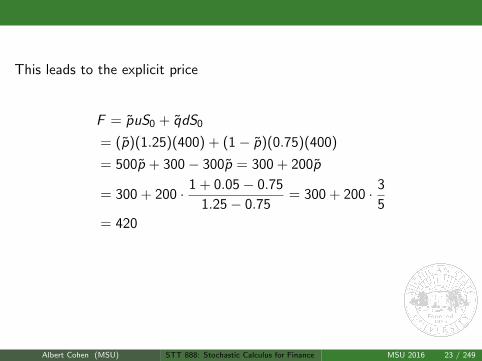

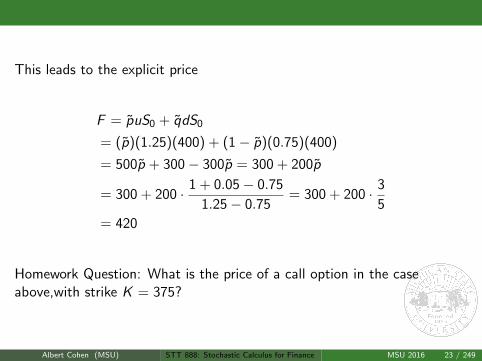

This leads to the explicit price

F = puS0 + qdS0

= (p)(1.25)(400) + (1− p)(0.75)(400)

= 500p + 300− 300p = 300 + 200p

= 300 + 200 · 1 + 0.05− 0.75

1.25− 0.75= 300 + 200 · 3

5

= 420

Homework Question: What is the price of a call option in the caseabove,with strike K = 375?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 23 / 249

This leads to the explicit price

F = puS0 + qdS0

= (p)(1.25)(400) + (1− p)(0.75)(400)

= 500p + 300− 300p = 300 + 200p

= 300 + 200 · 1 + 0.05− 0.75

1.25− 0.75= 300 + 200 · 3

5

= 420

Homework Question: What is the price of a call option in the caseabove,with strike K = 375?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 23 / 249

General one period risk neutral measure

We define a finite set of outcomes Ω ≡ ω1, ω2, ..., ωn and anysubcollection of outcomes A ∈ F1 := 2Ω an event.

Furthermore, we define a probability measure P, not necessarily thephysical measure P to be risk neutral if

P[ω] > 0 ∀ ω ∈ ΩX0 = 1

1+r E[X1]

for all strategies X .

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 24 / 249

General one period risk neutral measure

The measure is indifferent to investing in a zero-coupon bond, or arisky asset X

The same initial capital X0 in both cases produces the same”‘average”’ return after one period.

Not the physical measure attached by observation, experts, etc..

In fact, physical measure has no impact on pricing

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 25 / 249

General one period risk neutral measure

The measure is indifferent to investing in a zero-coupon bond, or arisky asset X

The same initial capital X0 in both cases produces the same”‘average”’ return after one period.

Not the physical measure attached by observation, experts, etc..

In fact, physical measure has no impact on pricing

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 25 / 249

General one period risk neutral measure

The measure is indifferent to investing in a zero-coupon bond, or arisky asset X

The same initial capital X0 in both cases produces the same”‘average”’ return after one period.

Not the physical measure attached by observation, experts, etc..

In fact, physical measure has no impact on pricing

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 25 / 249

General one period risk neutral measure

The measure is indifferent to investing in a zero-coupon bond, or arisky asset X

The same initial capital X0 in both cases produces the same”‘average”’ return after one period.

Not the physical measure attached by observation, experts, etc..

In fact, physical measure has no impact on pricing

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 25 / 249

Example: Risk Neutral measure for trinomial case

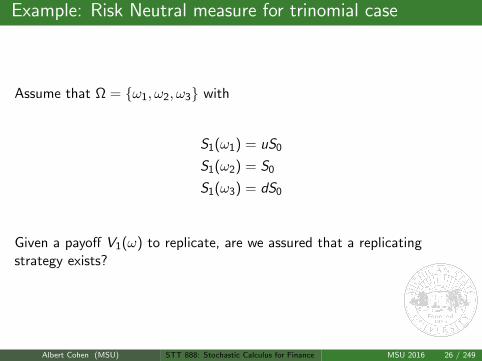

Assume that Ω = ω1, ω2, ω3 with

S1(ω1) = uS0

S1(ω2) = S0

S1(ω3) = dS0

Given a payoff V1(ω) to replicate, are we assured that a replicatingstrategy exists?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 26 / 249

Example: Risk Neutral measure for trinomial case

Assume that Ω = ω1, ω2, ω3 with

S1(ω1) = uS0

S1(ω2) = S0

S1(ω3) = dS0

Given a payoff V1(ω) to replicate, are we assured that a replicatingstrategy exists?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 26 / 249

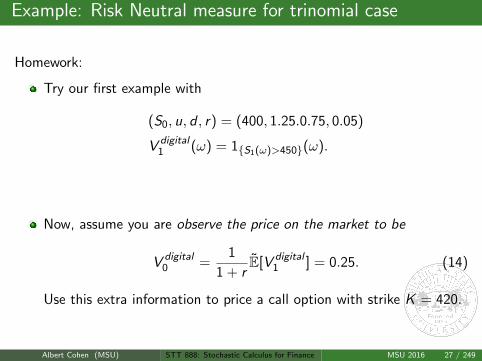

Example: Risk Neutral measure for trinomial case

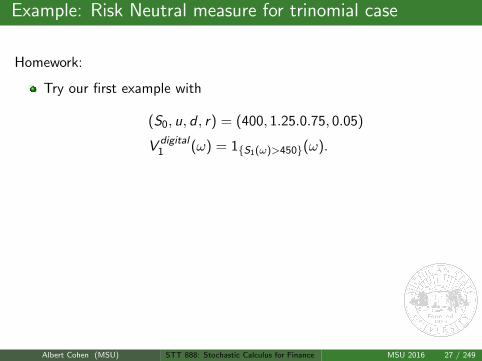

Homework:

Try our first example with

(S0, u, d , r) = (400, 1.25.0.75, 0.05)

V digital1 (ω) = 1S1(ω)>450(ω).

Now, assume you are observe the price on the market to be

V digital0 =

1

1 + rE[V digital

1 ] = 0.25. (14)

Use this extra information to price a call option with strike K = 420.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 27 / 249

Example: Risk Neutral measure for trinomial case

Homework:

Try our first example with

(S0, u, d , r) = (400, 1.25.0.75, 0.05)

V digital1 (ω) = 1S1(ω)>450(ω).

Now, assume you are observe the price on the market to be

V digital0 =

1

1 + rE[V digital

1 ] = 0.25. (14)

Use this extra information to price a call option with strike K = 420.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 27 / 249

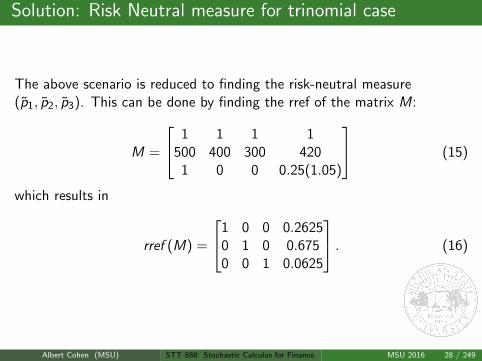

Solution: Risk Neutral measure for trinomial case

The above scenario is reduced to finding the risk-neutral measure(p1, p2, p3). This can be done by finding the rref of the matrix M:

M =

1 1 1 1500 400 300 420

1 0 0 0.25(1.05)

(15)

which results in

rref (M) =

1 0 0 0.26250 1 0 0.6750 0 1 0.0625

. (16)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 28 / 249

Solution: Risk Neutral measure for trinomial case

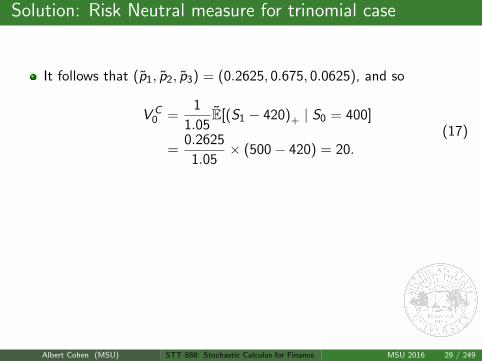

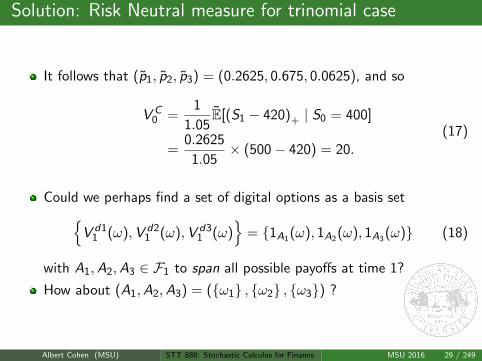

It follows that (p1, p2, p3) = (0.2625, 0.675, 0.0625), and so

V C0 =

1

1.05E[(S1 − 420)+ | S0 = 400]

=0.2625

1.05× (500− 420) = 20.

(17)

Could we perhaps find a set of digital options as a basis setV d1

1 (ω),V d21 (ω),V d3

1 (ω)

= 1A1(ω), 1A2(ω), 1A3(ω) (18)

with A1,A2,A3 ∈ F1 to span all possible payoffs at time 1?

How about (A1,A2,A3) = (ω1 , ω2 , ω3) ?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 29 / 249

Solution: Risk Neutral measure for trinomial case

It follows that (p1, p2, p3) = (0.2625, 0.675, 0.0625), and so

V C0 =

1

1.05E[(S1 − 420)+ | S0 = 400]

=0.2625

1.05× (500− 420) = 20.

(17)

Could we perhaps find a set of digital options as a basis setV d1

1 (ω),V d21 (ω),V d3

1 (ω)

= 1A1(ω), 1A2(ω), 1A3(ω) (18)

with A1,A2,A3 ∈ F1 to span all possible payoffs at time 1?

How about (A1,A2,A3) = (ω1 , ω2 , ω3) ?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 29 / 249

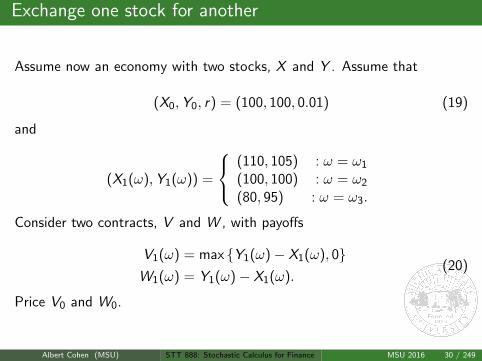

Exchange one stock for another

Assume now an economy with two stocks, X and Y . Assume that

(X0,Y0, r) = (100, 100, 0.01) (19)

and

(X1(ω),Y1(ω)) =

(110, 105) : ω = ω1

(100, 100) : ω = ω2

(80, 95) : ω = ω3.

Consider two contracts, V and W , with payoffs

V1(ω) = max Y1(ω)− X1(ω), 0W1(ω) = Y1(ω)− X1(ω).

(20)

Price V0 and W0.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 30 / 249

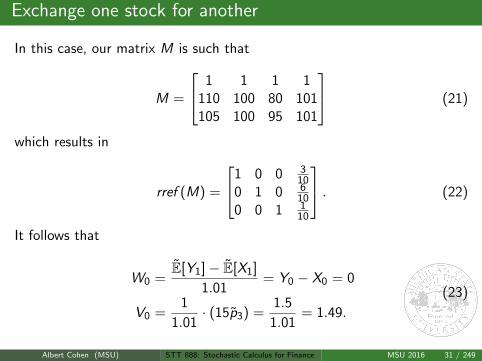

Exchange one stock for another

In this case, our matrix M is such that

M =

1 1 1 1110 100 80 101105 100 95 101

(21)

which results in

rref (M) =

1 0 0 310

0 1 0 610

0 0 1 110

. (22)

It follows that

W0 =E[Y1]− E[X1]

1.01= Y0 − X0 = 0

V0 =1

1.01· (15p3) =

1.5

1.01= 1.49.

(23)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 31 / 249

Existence of Risk Neutral measure

Let P be a probability measure on a finite space Ω. The following areequivalent:

P is a risk neutral measure

For all traded securities S i , S i0 = 1

1+r E[S i

1

]Proof: Homework (Hint: One direction is much easier than others. Also,strategies are linear in the underlying asset.)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 32 / 249

Existence of Risk Neutral measure

Let P be a probability measure on a finite space Ω. The following areequivalent:

P is a risk neutral measure

For all traded securities S i , S i0 = 1

1+r E[S i

1

]Proof: Homework (Hint: One direction is much easier than others. Also,strategies are linear in the underlying asset.)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 32 / 249

Existence of Risk Neutral measure

Let P be a probability measure on a finite space Ω. The following areequivalent:

P is a risk neutral measure

For all traded securities S i , S i0 = 1

1+r E[S i

1

]

Proof: Homework (Hint: One direction is much easier than others. Also,strategies are linear in the underlying asset.)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 32 / 249

Existence of Risk Neutral measure

Let P be a probability measure on a finite space Ω. The following areequivalent:

P is a risk neutral measure

For all traded securities S i , S i0 = 1

1+r E[S i

1

]Proof: Homework (Hint: One direction is much easier than others. Also,strategies are linear in the underlying asset.)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 32 / 249

Complete Markets

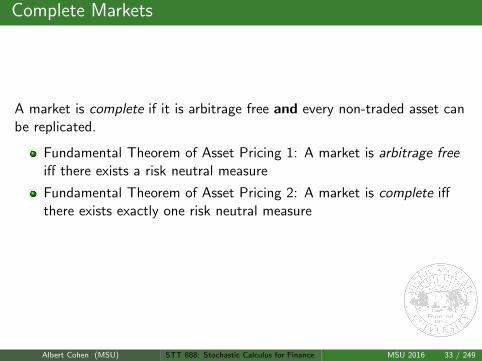

A market is complete if it is arbitrage free and every non-traded asset canbe replicated.

Fundamental Theorem of Asset Pricing 1: A market is arbitrage freeiff there exists a risk neutral measure

Fundamental Theorem of Asset Pricing 2: A market is complete iffthere exists exactly one risk neutral measure

Proof(s): We will go over these in detail later!

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 33 / 249

Complete Markets

A market is complete if it is arbitrage free and every non-traded asset canbe replicated.

Fundamental Theorem of Asset Pricing 1: A market is arbitrage freeiff there exists a risk neutral measure

Fundamental Theorem of Asset Pricing 2: A market is complete iffthere exists exactly one risk neutral measure

Proof(s): We will go over these in detail later!

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 33 / 249

Complete Markets

A market is complete if it is arbitrage free and every non-traded asset canbe replicated.

Fundamental Theorem of Asset Pricing 1: A market is arbitrage freeiff there exists a risk neutral measure

Fundamental Theorem of Asset Pricing 2: A market is complete iffthere exists exactly one risk neutral measure

Proof(s): We will go over these in detail later!

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 33 / 249

Optimal Investment for a Strictly Risk Averse Investor

Assume a complete market, with a unique risk-neutral measure P.

Characterize an investor by her pair (x ,U) of initial capital x ∈ X andutility function U : X → R+.

Assume U ′(x) > 0.

Assume U ′′(x) < 0.

Define the Radon-Nikodym derivative of P to P as the randomvariable

Z (ω) :=P(ω)

P(ω). (24)

Note that Z is used to map expectations under P to expectationsunder P: For any random variable X , it follows that

E[X ] = E[ZX ]. (25)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 34 / 249

Optimal Investment for a Strictly Risk Averse Investor

A strictly risk-averse investor now wishes to maximize her expected utilityof a portfolio at time 1, given initial capital at time 0:

u(x) := maxX1∈Ax

E[U(X1)]

Ax := all portfolio values at time 1 with initial capital x .(26)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 35 / 249

Optimal Investment for a Strictly Risk Averse Investor

Theorem

Define X1 via the relationship

U ′(

X1

):= λZ (27)

where λ sets X1 as a strategy with an average return of r under P:

E[X1] = x(1 + r). (28)

Then X1 is the optimal strategy.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 36 / 249

Optimal Investment for a Strictly Risk Averse Investor

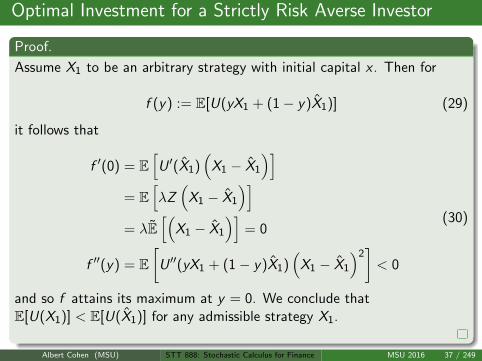

Proof.

Assume X1 to be an arbitrary strategy with initial capital x . Then for

f (y) := E[U(yX1 + (1− y)X1)] (29)

it follows that

f ′(0) = E[U ′(X1)

(X1 − X1

)]= E

[λZ(

X1 − X1

)]= λE

[(X1 − X1

)]= 0

f ′′(y) = E[

U ′′(yX1 + (1− y)X1)(

X1 − X1

)2]< 0

(30)

and so f attains its maximum at y = 0. We conclude thatE[U(X1)] < E[U(X1)] for any admissible strategy X1.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 37 / 249

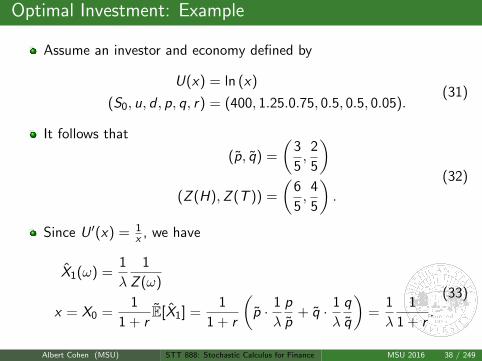

Optimal Investment: Example

Assume an investor and economy defined by

U(x) = ln (x)

(S0, u, d , p, q, r) = (400, 1.25.0.75, 0.5, 0.5, 0.05).(31)

It follows that

(p, q) =

(3

5,

2

5

)(Z (H),Z (T )) =

(6

5,

4

5

).

(32)

Since U ′(x) = 1x , we have

X1(ω) =1

λ

1

Z (ω)

x = X0 =1

1 + rE[X1] =

1

1 + r

(p · 1

λ

p

p+ q · 1

λ

q

q

)=

1

λ

1

1 + r.

(33)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 38 / 249

Optimal Investment: Example

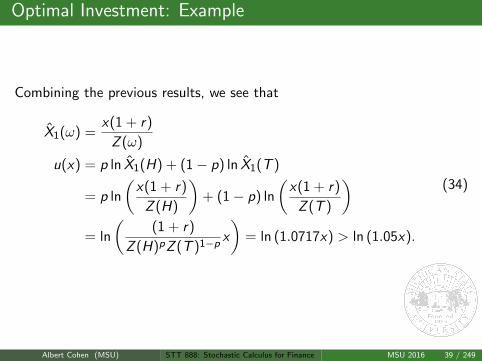

Combining the previous results, we see that

X1(ω) =x(1 + r)

Z (ω)

u(x) = p ln X1(H) + (1− p) ln X1(T )

= p ln

(x(1 + r)

Z (H)

)+ (1− p) ln

(x(1 + r)

Z (T )

)= ln

((1 + r)

Z (H)pZ (T )1−p x

)= ln (1.0717x) > ln (1.05x).

(34)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 39 / 249

Optimal Investment: Example

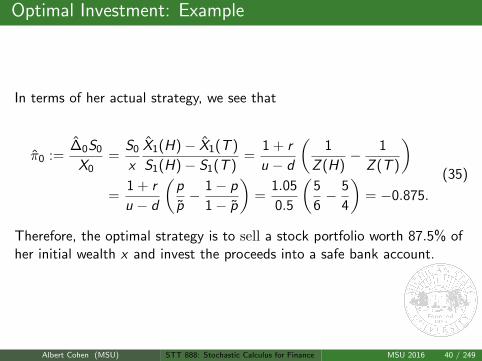

In terms of her actual strategy, we see that

π0 :=∆0S0

X0=

S0

x

X1(H)− X1(T )

S1(H)− S1(T )=

1 + r

u − d

(1

Z (H)− 1

Z (T )

)=

1 + r

u − d

(p

p− 1− p

1− p

)=

1.05

0.5

(5

6− 5

4

)= −0.875.

(35)

Therefore, the optimal strategy is to sell a stock portfolio worth 87.5% ofher initial wealth x and invest the proceeds into a safe bank account.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 40 / 249

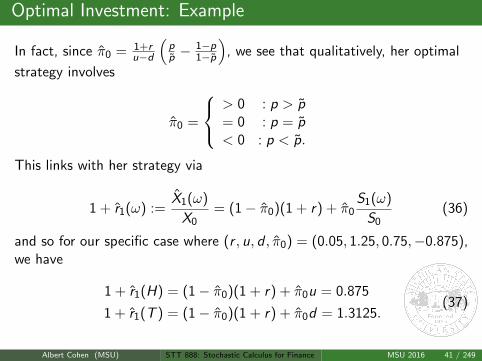

Optimal Investment: Example

In fact, since π0 = 1+ru−d

(pp −

1−p1−p

), we see that qualitatively, her optimal

strategy involves

π0 =

> 0 : p > p= 0 : p = p< 0 : p < p.

This links with her strategy via

1 + r1(ω) :=X1(ω)

X0= (1− π0)(1 + r) + π0

S1(ω)

S0(36)

and so for our specific case where (r , u, d , π0) = (0.05, 1.25, 0.75,−0.875),we have

1 + r1(H) = (1− π0)(1 + r) + π0u = 0.875

1 + r1(T ) = (1− π0)(1 + r) + π0d = 1.3125.(37)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 41 / 249

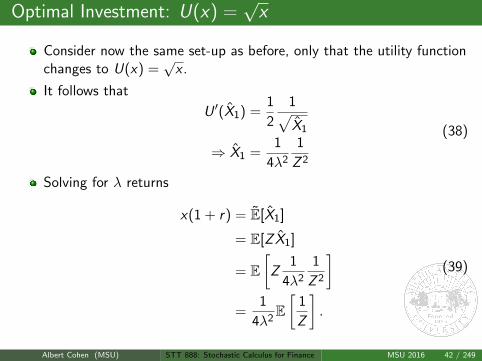

Optimal Investment: U(x) =√x

Consider now the same set-up as before, only that the utility functionchanges to U(x) =

√x .

It follows that

U ′(X1) =1

2

1√X1

⇒ X1 =1

4λ2

1

Z 2

(38)

Solving for λ returns

x(1 + r) = E[X1]

= E[Z X1]

= E[

Z1

4λ2

1

Z 2

]=

1

4λ2E[

1

Z

].

(39)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 42 / 249

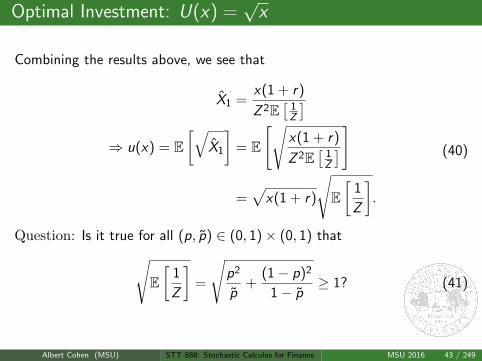

Optimal Investment: U(x) =√x

Combining the results above, we see that

X1 =x(1 + r)

Z 2E[

1Z

]⇒ u(x) = E

[√X1

]= E

[√x(1 + r)

Z 2E[

1Z

]]

=√

x(1 + r)

√E[

1

Z

].

(40)

Question: Is it true for all (p, p) ∈ (0, 1)× (0, 1) that√E[

1

Z

]=

√p2

p+

(1− p)2

1− p≥ 1? (41)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 43 / 249

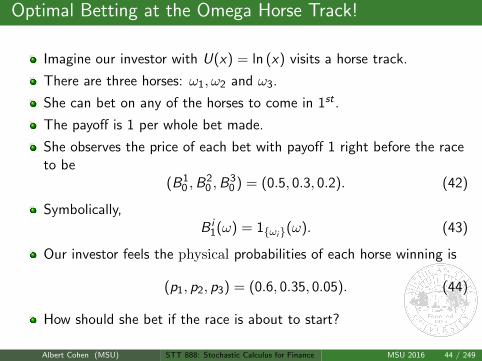

Optimal Betting at the Omega Horse Track!

Imagine our investor with U(x) = ln (x) visits a horse track.

There are three horses: ω1, ω2 and ω3.

She can bet on any of the horses to come in 1st .

The payoff is 1 per whole bet made.

She observes the price of each bet with payoff 1 right before the raceto be

(B10 ,B

20 ,B

30 ) = (0.5, 0.3, 0.2). (42)

Symbolically,B i

1(ω) = 1ωi(ω). (43)

Our investor feels the physical probabilities of each horse winning is

(p1, p2, p3) = (0.6, 0.35, 0.05). (44)

How should she bet if the race is about to start?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 44 / 249

Optimal Betting at the Omega Horse Track!

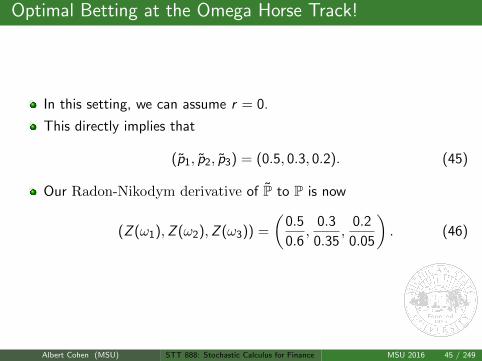

In this setting, we can assume r = 0.

This directly implies that

(p1, p2, p3) = (0.5, 0.3, 0.2). (45)

Our Radon-Nikodym derivative of P to P is now

(Z (ω1),Z (ω2),Z (ω3)) =

(0.5

0.6,

0.3

0.35,

0.2

0.05

). (46)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 45 / 249

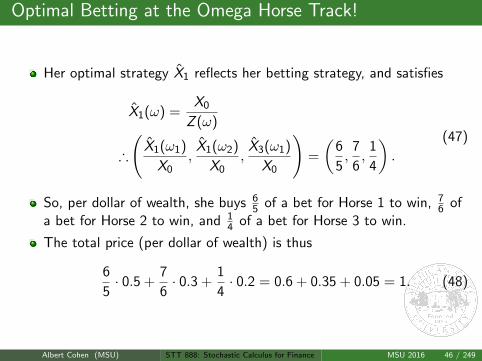

Optimal Betting at the Omega Horse Track!

Her optimal strategy X1 reflects her betting strategy, and satisfies

X1(ω) =X0

Z (ω)

∴

(X1(ω1)

X0,

X1(ω2)

X0,

X3(ω1)

X0

)=

(6

5,

7

6,

1

4

).

(47)

So, per dollar of wealth, she buys 65 of a bet for Horse 1 to win, 7

6 ofa bet for Horse 2 to win, and 1

4 of a bet for Horse 3 to win.

The total price (per dollar of wealth) is thus

6

5· 0.5 +

7

6· 0.3 +

1

4· 0.2 = 0.6 + 0.35 + 0.05 = 1. (48)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 46 / 249

Dividends

What about dividends? How do they affect the risk neutral pricing ofexchange and non-exchange traded assets? What if they are paid atdiscrete times? Continuously paid?

Recall that if dividends are paid continuously at rate δ, then 1 share attime 0 will accumulate to eδT shares upon reinvestment of dividends intothe stock until time T .

It follows that to deliver one share of stock S with initial price S0 at timeT , only e−δT shares are needed. Correspondingly,

Fprepaid = e−δTS0

F = erT e−δTS0 = e(r−δ)TS0.(49)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 47 / 249

Dividends

What about dividends? How do they affect the risk neutral pricing ofexchange and non-exchange traded assets? What if they are paid atdiscrete times? Continuously paid?

Recall that if dividends are paid continuously at rate δ, then 1 share attime 0 will accumulate to eδT shares upon reinvestment of dividends intothe stock until time T .

It follows that to deliver one share of stock S with initial price S0 at timeT , only e−δT shares are needed. Correspondingly,

Fprepaid = e−δTS0

F = erT e−δTS0 = e(r−δ)TS0.(49)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 47 / 249

Dividends

What about dividends? How do they affect the risk neutral pricing ofexchange and non-exchange traded assets? What if they are paid atdiscrete times? Continuously paid?

Recall that if dividends are paid continuously at rate δ, then 1 share attime 0 will accumulate to eδT shares upon reinvestment of dividends intothe stock until time T .

It follows that to deliver one share of stock S with initial price S0 at timeT , only e−δT shares are needed. Correspondingly,

Fprepaid = e−δTS0

F = erT e−δTS0 = e(r−δ)TS0.(49)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 47 / 249

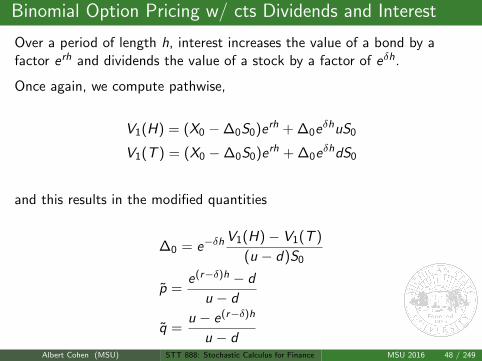

Binomial Option Pricing w/ cts Dividends and Interest

Over a period of length h, interest increases the value of a bond by afactor erh and dividends the value of a stock by a factor of eδh.

Once again, we compute pathwise,

V1(H) = (X0 −∆0S0)erh + ∆0eδhuS0

V1(T ) = (X0 −∆0S0)erh + ∆0eδhdS0

and this results in the modified quantities

∆0 = e−δhV1(H)− V1(T )

(u − d)S0

p =e(r−δ)h − d

u − d

q =u − e(r−δ)h

u − d

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 48 / 249

Binomial Option Pricing w/ cts Dividends and Interest

Over a period of length h, interest increases the value of a bond by afactor erh and dividends the value of a stock by a factor of eδh.

Once again, we compute pathwise,

V1(H) = (X0 −∆0S0)erh + ∆0eδhuS0

V1(T ) = (X0 −∆0S0)erh + ∆0eδhdS0

and this results in the modified quantities

∆0 = e−δhV1(H)− V1(T )

(u − d)S0

p =e(r−δ)h − d

u − d

q =u − e(r−δ)h

u − dAlbert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 48 / 249

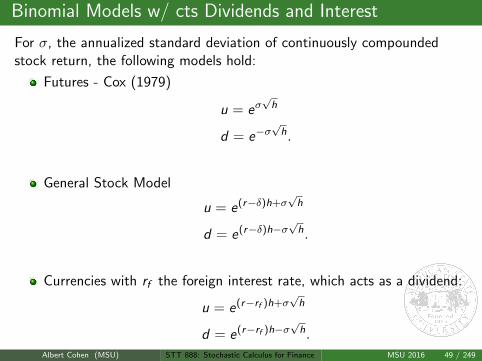

Binomial Models w/ cts Dividends and Interest

For σ, the annualized standard deviation of continuously compoundedstock return, the following models hold:

Futures - Cox (1979)

u = eσ√h

d = e−σ√h.

General Stock Model

u = e(r−δ)h+σ√h

d = e(r−δ)h−σ√h.

Currencies with rf the foreign interest rate, which acts as a dividend:

u = e(r−rf )h+σ√h

d = e(r−rf )h−σ√h.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 49 / 249

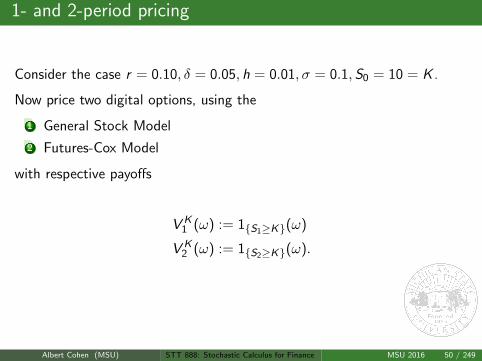

1- and 2-period pricing

Consider the case r = 0.10, δ = 0.05, h = 0.01, σ = 0.1,S0 = 10 = K .

Now price two digital options, using the

1 General Stock Model

2 Futures-Cox Model

with respective payoffs

V K1 (ω) := 1S1≥K(ω)

V K2 (ω) := 1S2≥K(ω).

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 50 / 249

1- and 2-period pricing

Consider the case r = 0.10, δ = 0.05, h = 0.01, σ = 0.1,S0 = 10 = K .

Now price two digital options, using the

1 General Stock Model

2 Futures-Cox Model

with respective payoffs

V K1 (ω) := 1S1≥K(ω)

V K2 (ω) := 1S2≥K(ω).

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 50 / 249

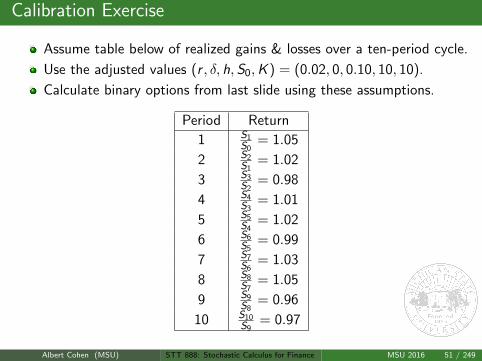

Calibration Exercise

Assume table below of realized gains & losses over a ten-period cycle.

Use the adjusted values (r , δ, h,S0,K ) = (0.02, 0, 0.10, 10, 10).

Calculate binary options from last slide using these assumptions.

Period Return

1 S1S0

= 1.05

2 S2S1

= 1.02

3 S3S2

= 0.98

4 S4S3

= 1.01

5 S5S4

= 1.02

6 S6S5

= 0.99

7 S7S6

= 1.03

8 S8S7

= 1.05

9 S9S8

= 0.96

10 S10S9

= 0.97

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 51 / 249

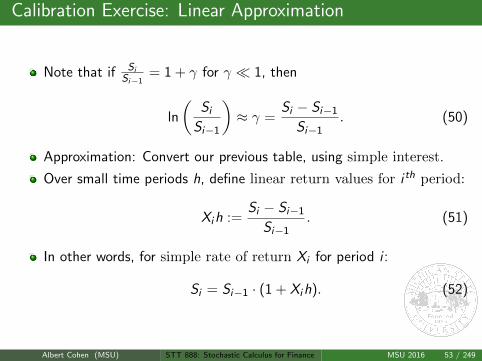

Calibration Exercise: Linear Approximation

We would like to compute σ for the logarithm of returns ln(

SiSi−1

).

Assume the returns per period are all independent.

Q: Can we use a linear (simple) return model instead of a compoundreturn model as an approximation?

If so, then for our observed simple return rate values:

Calculate the sample variance σ2∗.

Estimate that σ ≈ σ∗√h

.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 52 / 249

Calibration Exercise: Linear Approximation

Note that if SiSi−1

= 1 + γ for γ 1, then

ln

(Si

Si−1

)≈ γ =

Si − Si−1

Si−1. (50)

Approximation: Convert our previous table, using simple interest.

Over small time periods h, define linear return values for i th period:

Xih :=Si − Si−1

Si−1. (51)

In other words, for simple rate of return Xi for period i :

Si = Si−1 · (1 + Xih). (52)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 53 / 249

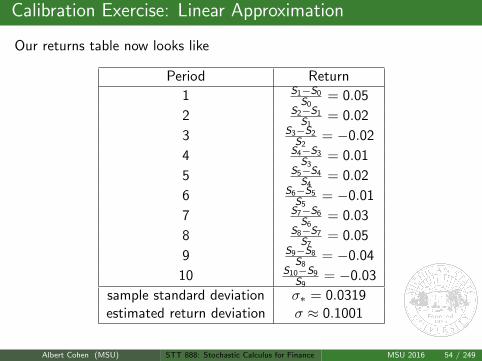

Calibration Exercise: Linear Approximation

Our returns table now looks like

Period Return

1 S1−S0S0

= 0.05

2 S2−S1S1

= 0.02

3 S3−S2S2

= −0.02

4 S4−S3S3

= 0.01

5 S5−S4S4

= 0.02

6 S6−S5S5

= −0.01

7 S7−S6S6

= 0.03

8 S8−S7S7

= 0.05

9 S9−S8S8

= −0.04

10 S10−S9S9

= −0.03

sample standard deviation σ∗ = 0.0319estimated return deviation σ ≈ 0.1001

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 54 / 249

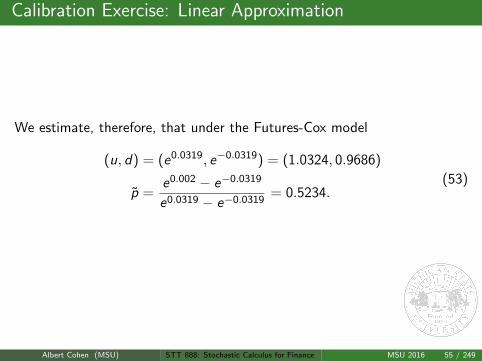

Calibration Exercise: Linear Approximation

We estimate, therefore, that under the Futures-Cox model

(u, d) = (e0.0319, e−0.0319) = (1.0324, 0.9686)

p =e0.002 − e−0.0319

e0.0319 − e−0.0319= 0.5234.

(53)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 55 / 249

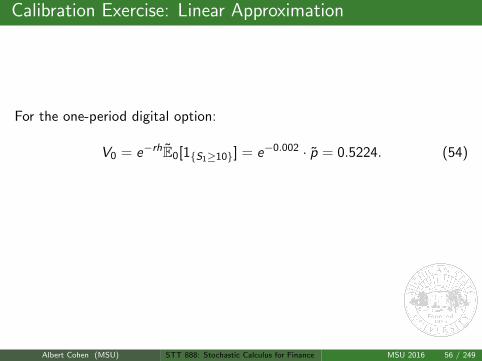

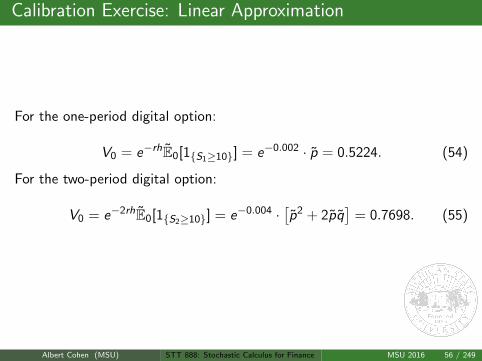

Calibration Exercise: Linear Approximation

For the one-period digital option:

V0 = e−rhE0[1S1≥10] = e−0.002 · p = 0.5224. (54)

For the two-period digital option:

V0 = e−2rhE0[1S2≥10] = e−0.004 ·[p2 + 2pq

]= 0.7698. (55)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 56 / 249

Calibration Exercise: Linear Approximation

For the one-period digital option:

V0 = e−rhE0[1S1≥10] = e−0.002 · p = 0.5224. (54)

For the two-period digital option:

V0 = e−2rhE0[1S2≥10] = e−0.004 ·[p2 + 2pq

]= 0.7698. (55)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 56 / 249

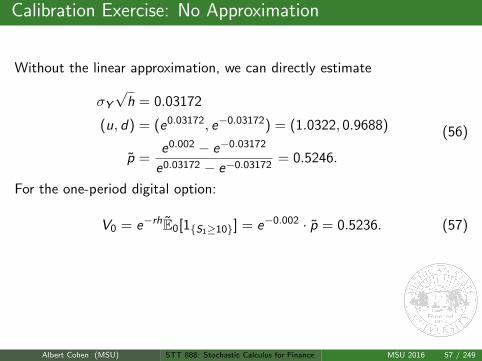

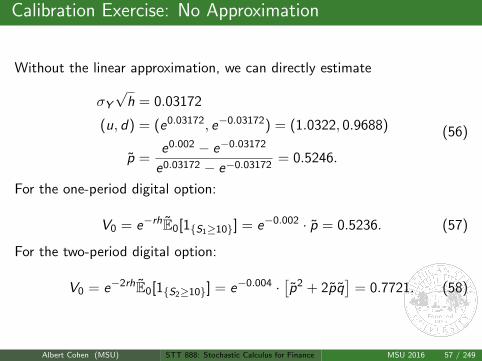

Calibration Exercise: No Approximation

Without the linear approximation, we can directly estimate

σY√

h = 0.03172

(u, d) = (e0.03172, e−0.03172) = (1.0322, 0.9688)

p =e0.002 − e−0.03172

e0.03172 − e−0.03172= 0.5246.

(56)

For the one-period digital option:

V0 = e−rhE0[1S1≥10] = e−0.002 · p = 0.5236. (57)

For the two-period digital option:

V0 = e−2rhE0[1S2≥10] = e−0.004 ·[p2 + 2pq

]= 0.7721. (58)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 57 / 249

Calibration Exercise: No Approximation

Without the linear approximation, we can directly estimate

σY√

h = 0.03172

(u, d) = (e0.03172, e−0.03172) = (1.0322, 0.9688)

p =e0.002 − e−0.03172

e0.03172 − e−0.03172= 0.5246.

(56)

For the one-period digital option:

V0 = e−rhE0[1S1≥10] = e−0.002 · p = 0.5236. (57)

For the two-period digital option:

V0 = e−2rhE0[1S2≥10] = e−0.004 ·[p2 + 2pq

]= 0.7721. (58)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 57 / 249

1- and 2-period pricing

We can solve for 2-period problems

on a case-by-case basis, or

by developing a general theory for multi-period asset pricing.

In the latter method, we need a general framework to carry out ourcomputations

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 58 / 249

1- and 2-period pricing

We can solve for 2-period problems

on a case-by-case basis, or

by developing a general theory for multi-period asset pricing.

In the latter method, we need a general framework to carry out ourcomputations

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 58 / 249

1- and 2-period pricing

We can solve for 2-period problems

on a case-by-case basis, or

by developing a general theory for multi-period asset pricing.

In the latter method, we need a general framework to carry out ourcomputations

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 58 / 249

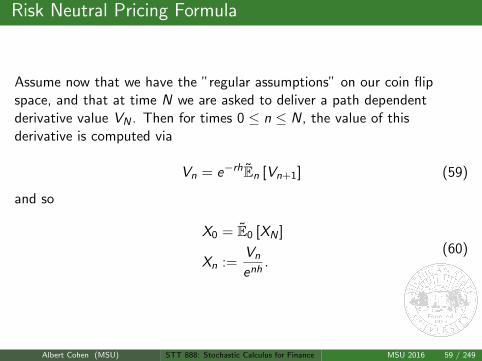

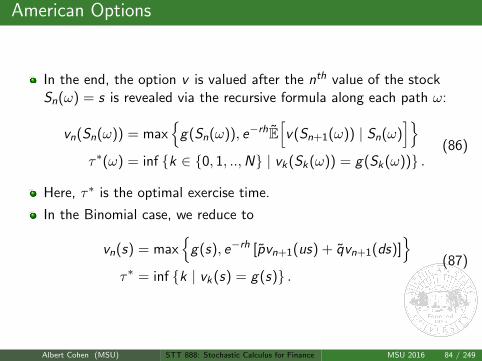

Risk Neutral Pricing Formula

Assume now that we have the ”regular assumptions” on our coin flipspace, and that at time N we are asked to deliver a path dependentderivative value VN . Then for times 0 ≤ n ≤ N, the value of thisderivative is computed via

Vn = e−rhEn [Vn+1] (59)

and so

X0 = E0 [XN ]

Xn :=Vn

enh.

(60)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 59 / 249

Risk Neutral Pricing Formula

Assume now that we have the ”regular assumptions” on our coin flipspace, and that at time N we are asked to deliver a path dependentderivative value VN . Then for times 0 ≤ n ≤ N, the value of thisderivative is computed via

Vn = e−rhEn [Vn+1] (59)

and so

X0 = E0 [XN ]

Xn :=Vn

enh.

(60)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 59 / 249

Risk Neutral Pricing Formula

Assume now that we have the ”regular assumptions” on our coin flipspace, and that at time N we are asked to deliver a path dependentderivative value VN . Then for times 0 ≤ n ≤ N, the value of thisderivative is computed via

Vn = e−rhEn [Vn+1] (59)

and so

X0 = E0 [XN ]

Xn :=Vn

enh.

(60)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 59 / 249

Risk Neutral Pricing Formula

Assume now that we have the ”regular assumptions” on our coin flipspace, and that at time N we are asked to deliver a path dependentderivative value VN . Then for times 0 ≤ n ≤ N, the value of thisderivative is computed via

Vn = e−rhEn [Vn+1] (59)

and so

X0 = E0 [XN ]

Xn :=Vn

enh.

(60)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 59 / 249

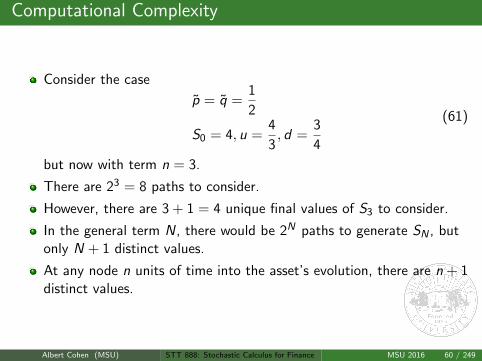

Computational Complexity

Consider the case

p = q =1

2

S0 = 4, u =4

3, d =

3

4

(61)

but now with term n = 3.

There are 23 = 8 paths to consider.

However, there are 3 + 1 = 4 unique final values of S3 to consider.

In the general term N, there would be 2N paths to generate SN , butonly N + 1 distinct values.

At any node n units of time into the asset’s evolution, there are n + 1distinct values.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 60 / 249

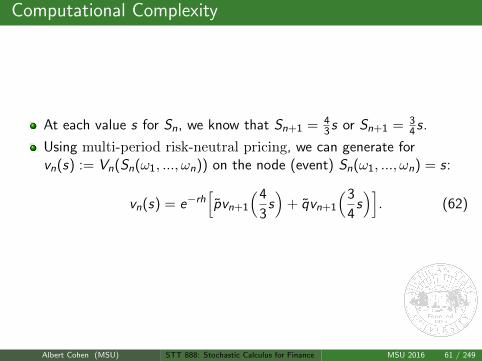

Computational Complexity

At each value s for Sn, we know that Sn+1 = 43 s or Sn+1 = 3

4 s.

Using multi-period risk-neutral pricing, we can generate forvn(s) := Vn(Sn(ω1, ..., ωn)) on the node (event) Sn(ω1, ..., ωn) = s:

vn(s) = e−rh[pvn+1

(4

3s)

+ qvn+1

(3

4s)]. (62)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 61 / 249

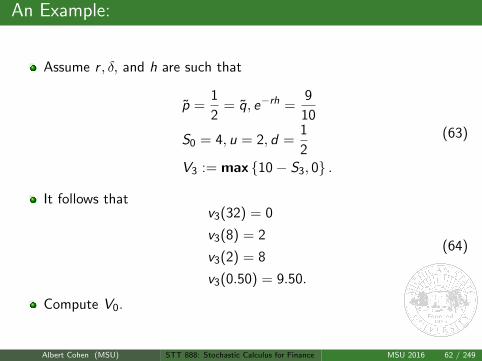

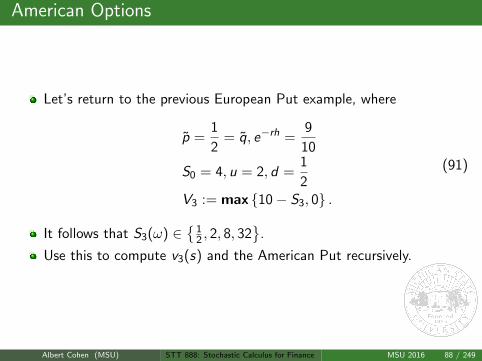

An Example:

Assume r , δ, and h are such that

p =1

2= q, e−rh =

9

10

S0 = 4, u = 2, d =1

2V3 := max 10− S3, 0 .

(63)

It follows thatv3(32) = 0

v3(8) = 2

v3(2) = 8

v3(0.50) = 9.50.

(64)

Compute V0.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 62 / 249

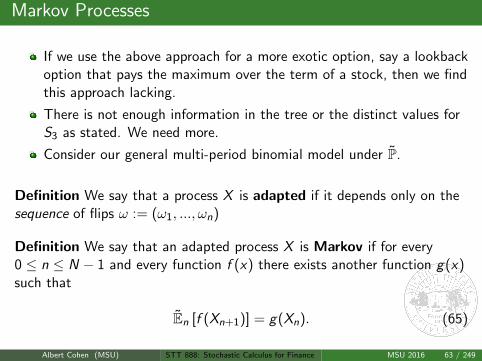

Markov Processes

If we use the above approach for a more exotic option, say a lookbackoption that pays the maximum over the term of a stock, then we findthis approach lacking.

There is not enough information in the tree or the distinct values forS3 as stated. We need more.

Consider our general multi-period binomial model under P.

Definition We say that a process X is adapted if it depends only on thesequence of flips ω := (ω1, ..., ωn)

Definition We say that an adapted process X is Markov if for every0 ≤ n ≤ N − 1 and every function f (x) there exists another function g(x)such that

En [f (Xn+1)] = g(Xn). (65)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 63 / 249

Markov Processes

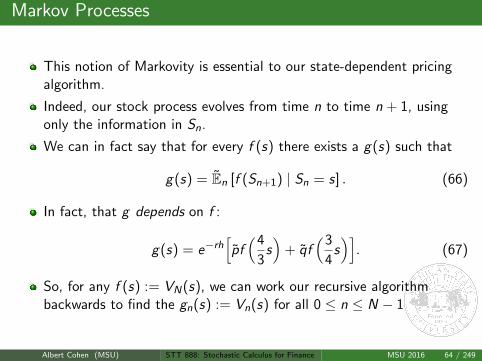

This notion of Markovity is essential to our state-dependent pricingalgorithm.

Indeed, our stock process evolves from time n to time n + 1, usingonly the information in Sn.

We can in fact say that for every f (s) there exists a g(s) such that

g(s) = En [f (Sn+1) | Sn = s] . (66)

In fact, that g depends on f :

g(s) = e−rh[pf(4

3s)

+ qf(3

4s)]. (67)

So, for any f (s) := VN(s), we can work our recursive algorithmbackwards to find the gn(s) := Vn(s) for all 0 ≤ n ≤ N − 1

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 64 / 249

Markov Processes

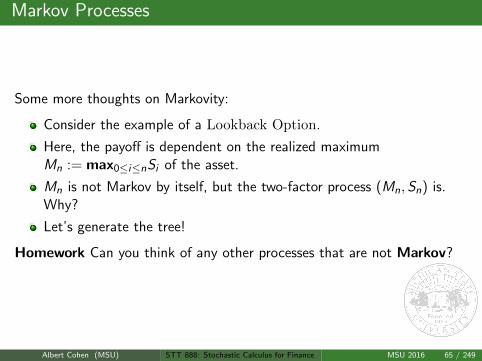

Some more thoughts on Markovity:

Consider the example of a Lookback Option.

Here, the payoff is dependent on the realized maximumMn := max0≤i≤nSi of the asset.

Mn is not Markov by itself, but the two-factor process (Mn, Sn) is.Why?

Let’s generate the tree!

Homework Can you think of any other processes that are not Markov?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 65 / 249

Call Options on Zero-Coupon Bonds

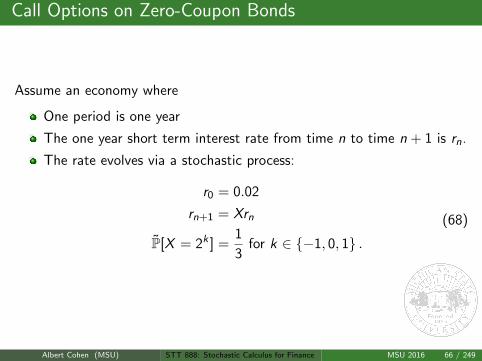

Assume an economy where

One period is one year

The one year short term interest rate from time n to time n + 1 is rn.

The rate evolves via a stochastic process:

r0 = 0.02

rn+1 = Xrn

P[X = 2k ] =1

3for k ∈ −1, 0, 1 .

(68)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 66 / 249

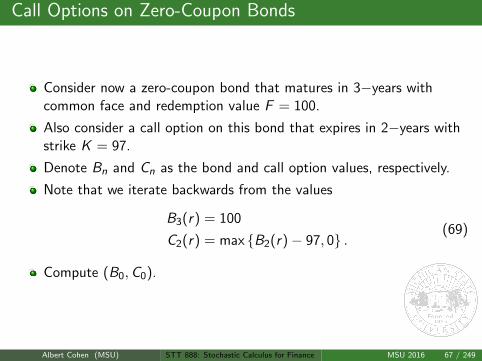

Call Options on Zero-Coupon Bonds

Consider now a zero-coupon bond that matures in 3−years withcommon face and redemption value F = 100.

Also consider a call option on this bond that expires in 2−years withstrike K = 97.

Denote Bn and Cn as the bond and call option values, respectively.

Note that we iterate backwards from the values

B3(r) = 100

C2(r) = max B2(r)− 97, 0 .(69)

Compute (B0,C0).

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 67 / 249

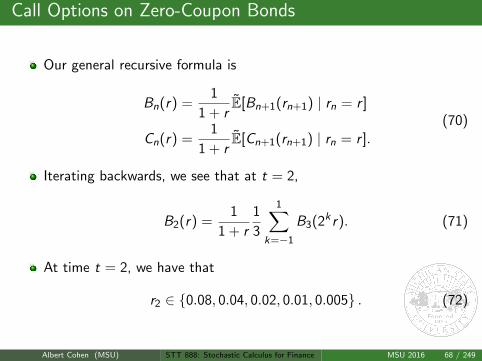

Call Options on Zero-Coupon Bonds

Our general recursive formula is

Bn(r) =1

1 + rE[Bn+1(rn+1) | rn = r ]

Cn(r) =1

1 + rE[Cn+1(rn+1) | rn = r ].

(70)

Iterating backwards, we see that at t = 2,

B2(r) =1

1 + r

1

3

1∑k=−1

B3(2k r). (71)

At time t = 2, we have that

r2 ∈ 0.08, 0.04, 0.02, 0.01, 0.005 . (72)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 68 / 249

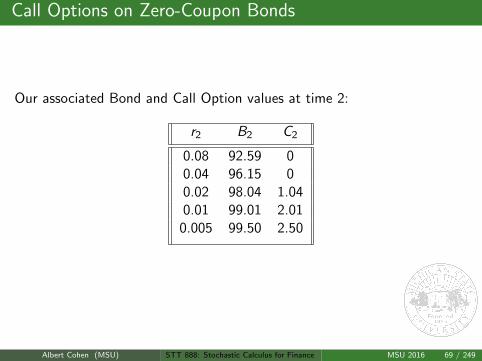

Call Options on Zero-Coupon Bonds

Our associated Bond and Call Option values at time 2:

r2 B2 C2

0.08 92.59 00.04 96.15 00.02 98.04 1.040.01 99.01 2.01

0.005 99.50 2.50

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 69 / 249

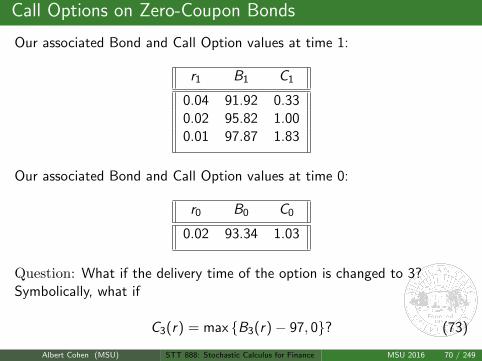

Call Options on Zero-Coupon Bonds

Our associated Bond and Call Option values at time 1:

r1 B1 C1

0.04 91.92 0.330.02 95.82 1.000.01 97.87 1.83

Our associated Bond and Call Option values at time 0:

r0 B0 C0

0.02 93.34 1.03

Question: What if the delivery time of the option is changed to 3?Symbolically, what if

C3(r) = max B3(r)− 97, 0? (73)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 70 / 249

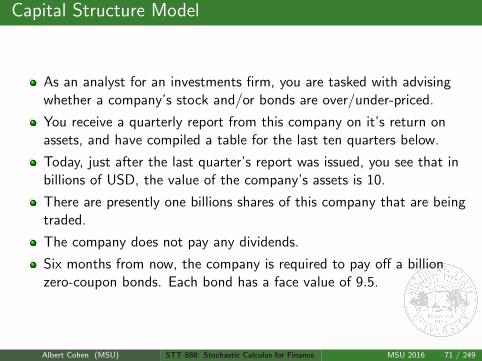

Capital Structure Model

As an analyst for an investments firm, you are tasked with advisingwhether a company’s stock and/or bonds are over/under-priced.

You receive a quarterly report from this company on it’s return onassets, and have compiled a table for the last ten quarters below.

Today, just after the last quarter’s report was issued, you see that inbillions of USD, the value of the company’s assets is 10.

There are presently one billions shares of this company that are beingtraded.

The company does not pay any dividends.

Six months from now, the company is required to pay off a billionzero-coupon bonds. Each bond has a face value of 9.5.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 71 / 249

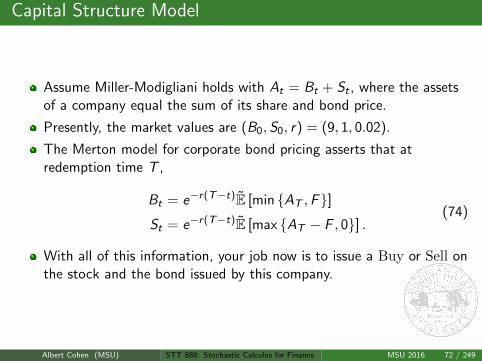

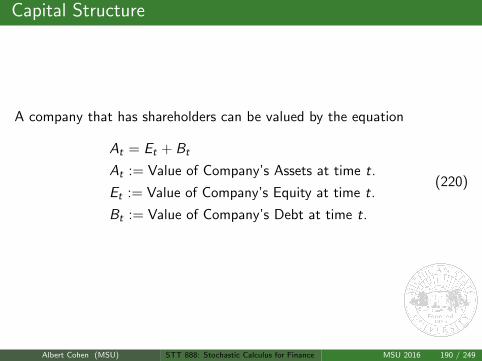

Capital Structure Model

Assume Miller-Modigliani holds with At = Bt + St , where the assetsof a company equal the sum of its share and bond price.

Presently, the market values are (B0, S0, r) = (9, 1, 0.02).

The Merton model for corporate bond pricing asserts that atredemption time T ,

Bt = e−r(T−t)E [min AT ,F]St = e−r(T−t)E [max AT − F , 0] .

(74)

With all of this information, your job now is to issue a Buy or Sell onthe stock and the bond issued by this company.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 72 / 249

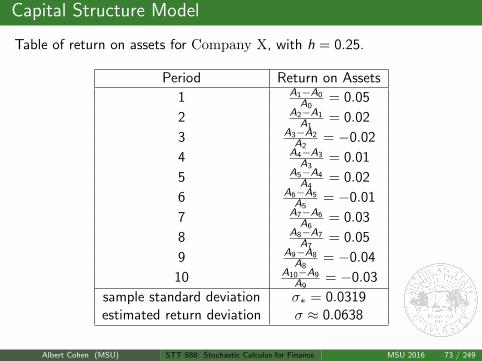

Capital Structure Model

Table of return on assets for Company X, with h = 0.25.

Period Return on Assets

1 A1−A0A0

= 0.05

2 A2−A1A1

= 0.02

3 A3−A2A2

= −0.02

4 A4−A3A3

= 0.01

5 A5−A4A4

= 0.02

6 A6−A5A5

= −0.01

7 A7−A6A6

= 0.03

8 A8−A7A7

= 0.05

9 A9−A8A8

= −0.04

10 A10−A9A9

= −0.03

sample standard deviation σ∗ = 0.0319estimated return deviation σ ≈ 0.0638

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 73 / 249

Capital Structure Model

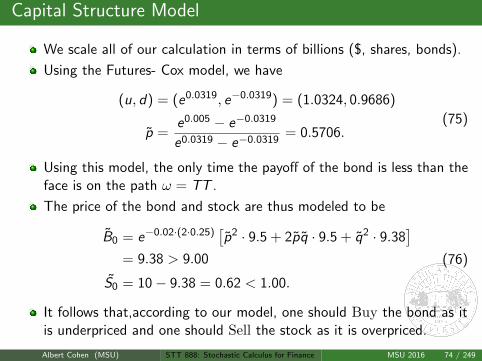

We scale all of our calculation in terms of billions ($, shares, bonds).

Using the Futures- Cox model, we have

(u, d) = (e0.0319, e−0.0319) = (1.0324, 0.9686)

p =e0.005 − e−0.0319

e0.0319 − e−0.0319= 0.5706.

(75)

Using this model, the only time the payoff of the bond is less than theface is on the path ω = TT .

The price of the bond and stock are thus modeled to be

B0 = e−0.02·(2·0.25)[p2 · 9.5 + 2pq · 9.5 + q2 · 9.38

]= 9.38 > 9.00

S0 = 10− 9.38 = 0.62 < 1.00.

(76)

It follows that,according to our model, one should Buy the bond as itis underpriced and one should Sell the stock as it is overpriced.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 74 / 249

The Interview Process

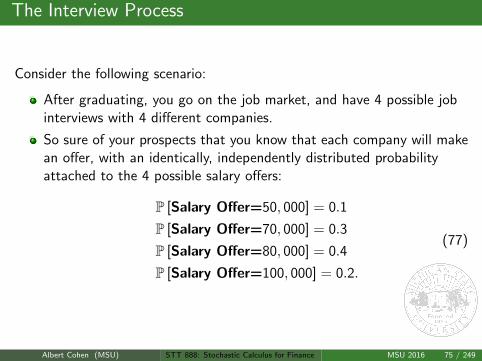

Consider the following scenario:

After graduating, you go on the job market, and have 4 possible jobinterviews with 4 different companies.

So sure of your prospects that you know that each company will makean offer, with an identically, independently distributed probabilityattached to the 4 possible salary offers:

P [Salary Offer=50, 000] = 0.1

P [Salary Offer=70, 000] = 0.3

P [Salary Offer=80, 000] = 0.4

P [Salary Offer=100, 000] = 0.2.

(77)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 75 / 249

The Interview Process

Questions:

How should you interview?

Specifically, when should you accept an offer and cancel theremaining interviews?

How does your strategy change if you can interview as many times asyou like, but the distribution of offers remains the same as above?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 76 / 249

The Interview Process

Questions:

How should you interview?

Specifically, when should you accept an offer and cancel theremaining interviews?

How does your strategy change if you can interview as many times asyou like, but the distribution of offers remains the same as above?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 76 / 249

The Interview Process

Questions:

How should you interview?

Specifically, when should you accept an offer and cancel theremaining interviews?

How does your strategy change if you can interview as many times asyou like, but the distribution of offers remains the same as above?

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 76 / 249

The Interview Process: Strategy

Some more thoughts...

At any time the student will know only one offer, which she can eitheraccept or reject.

Of course, if the student rejects the first three offers, than she has toaccept the last one.

So, compute the maximal expected salary for the student after thegraduation and the corresponding optimal strategy.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 77 / 249

The Interview Process: Optimal Strategy

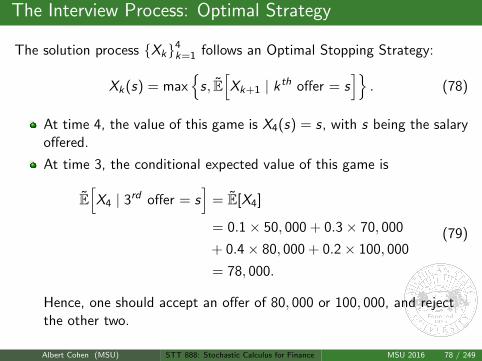

The solution process Xk4k=1 follows an Optimal Stopping Strategy:

Xk(s) = max

s, E[Xk+1 | kth offer = s

]. (78)

At time 4, the value of this game is X4(s) = s, with s being the salaryoffered.

At time 3, the conditional expected value of this game is

E[X4 | 3rd offer = s

]= E[X4]

= 0.1× 50, 000 + 0.3× 70, 000

+ 0.4× 80, 000 + 0.2× 100, 000

= 78, 000.

(79)

Hence, one should accept an offer of 80, 000 or 100, 000, and rejectthe other two.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 78 / 249

The Interview Process: Optimal Strategy

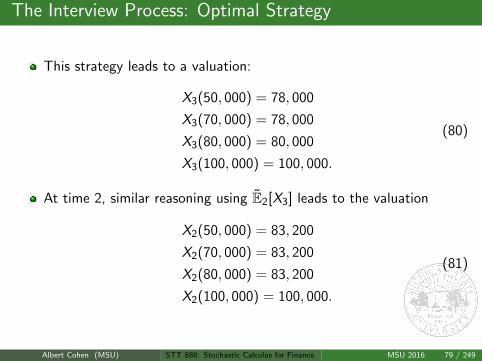

This strategy leads to a valuation:

X3(50, 000) = 78, 000

X3(70, 000) = 78, 000

X3(80, 000) = 80, 000

X3(100, 000) = 100, 000.

(80)

At time 2, similar reasoning using E2[X3] leads to the valuation

X2(50, 000) = 83, 200

X2(70, 000) = 83, 200

X2(80, 000) = 83, 200

X2(100, 000) = 100, 000.

(81)

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 79 / 249

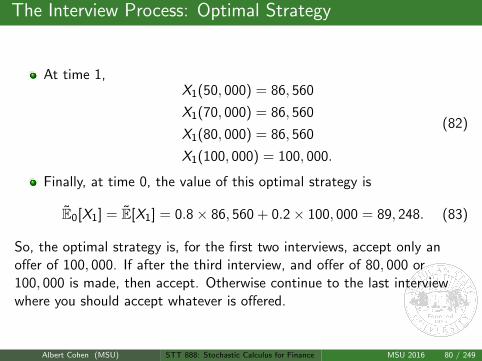

The Interview Process: Optimal Strategy

At time 1,X1(50, 000) = 86, 560

X1(70, 000) = 86, 560

X1(80, 000) = 86, 560

X1(100, 000) = 100, 000.

(82)

Finally, at time 0, the value of this optimal strategy is

E0[X1] = E[X1] = 0.8× 86, 560 + 0.2× 100, 000 = 89, 248. (83)

So, the optimal strategy is, for the first two interviews, accept only anoffer of 100, 000. If after the third interview, and offer of 80, 000 or100, 000 is made, then accept. Otherwise continue to the last interviewwhere you should accept whatever is offered.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 80 / 249

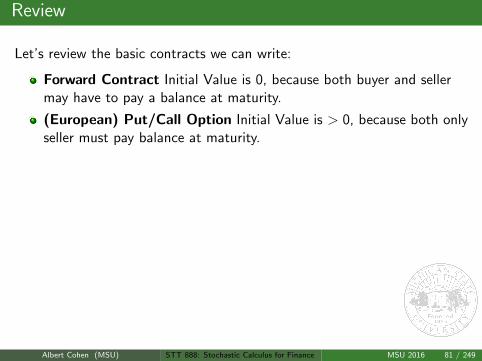

Review

Let’s review the basic contracts we can write:

Forward Contract Initial Value is 0, because both buyer and sellermay have to pay a balance at maturity.

(European) Put/Call Option Initial Value is > 0, because both onlyseller must pay balance at maturity.

(European) ”Exotic” Option Initial Value is > 0, because both onlyseller must pay balance at maturity.

During the term of the contract, can the value of the contract ever fallbelow the intrinsic value of the payoff? Symbolically, does it ever occurthat

vn(s) < g(s) (84)

where g(s) is of the form of g(S) := max S − K , 0, in the case of a Calloption, for example.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 81 / 249

Review

Let’s review the basic contracts we can write:

Forward Contract Initial Value is 0, because both buyer and sellermay have to pay a balance at maturity.

(European) Put/Call Option Initial Value is > 0, because both onlyseller must pay balance at maturity.

(European) ”Exotic” Option Initial Value is > 0, because both onlyseller must pay balance at maturity.

During the term of the contract, can the value of the contract ever fallbelow the intrinsic value of the payoff? Symbolically, does it ever occurthat

vn(s) < g(s) (84)

where g(s) is of the form of g(S) := max S − K , 0, in the case of a Calloption, for example.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 81 / 249

Review

Let’s review the basic contracts we can write:

Forward Contract Initial Value is 0, because both buyer and sellermay have to pay a balance at maturity.

(European) Put/Call Option Initial Value is > 0, because both onlyseller must pay balance at maturity.

(European) ”Exotic” Option Initial Value is > 0, because both onlyseller must pay balance at maturity.

During the term of the contract, can the value of the contract ever fallbelow the intrinsic value of the payoff? Symbolically, does it ever occurthat

vn(s) < g(s) (84)

where g(s) is of the form of g(S) := max S − K , 0, in the case of a Calloption, for example.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 81 / 249

Review

Let’s review the basic contracts we can write:

Forward Contract Initial Value is 0, because both buyer and sellermay have to pay a balance at maturity.

(European) Put/Call Option Initial Value is > 0, because both onlyseller must pay balance at maturity.

(European) ”Exotic” Option Initial Value is > 0, because both onlyseller must pay balance at maturity.

During the term of the contract, can the value of the contract ever fallbelow the intrinsic value of the payoff? Symbolically, does it ever occurthat

vn(s) < g(s) (84)

where g(s) is of the form of g(S) := max S − K , 0, in the case of a Calloption, for example.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 81 / 249

Review

Let’s review the basic contracts we can write:

Forward Contract Initial Value is 0, because both buyer and sellermay have to pay a balance at maturity.

(European) Put/Call Option Initial Value is > 0, because both onlyseller must pay balance at maturity.

(European) ”Exotic” Option Initial Value is > 0, because both onlyseller must pay balance at maturity.

During the term of the contract, can the value of the contract ever fallbelow the intrinsic value of the payoff? Symbolically, does it ever occurthat

vn(s) < g(s) (84)

where g(s) is of the form of g(S) := max S − K , 0, in the case of a Calloption, for example.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 81 / 249

Review

Let’s review the basic contracts we can write:

Forward Contract Initial Value is 0, because both buyer and sellermay have to pay a balance at maturity.

(European) Put/Call Option Initial Value is > 0, because both onlyseller must pay balance at maturity.

(European) ”Exotic” Option Initial Value is > 0, because both onlyseller must pay balance at maturity.

During the term of the contract, can the value of the contract ever fallbelow the intrinsic value of the payoff? Symbolically, does it ever occurthat

vn(s) < g(s) (84)

where g(s) is of the form of g(S) := max S − K , 0, in the case of a Calloption, for example.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 81 / 249

Review

Let’s review the basic contracts we can write:

Forward Contract Initial Value is 0, because both buyer and sellermay have to pay a balance at maturity.

(European) Put/Call Option Initial Value is > 0, because both onlyseller must pay balance at maturity.

(European) ”Exotic” Option Initial Value is > 0, because both onlyseller must pay balance at maturity.

During the term of the contract, can the value of the contract ever fallbelow the intrinsic value of the payoff? Symbolically, does it ever occurthat

vn(s) < g(s) (84)

where g(s) is of the form of g(S) := max S − K , 0, in the case of a Calloption, for example.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 81 / 249

Early Exercise

If σ = 0, and so uncertainty vanishes, then an investor would seek toexercise early if

rK > δS . (85)

If σ > 0, then the situation involves deeper analysis.

Whether solving a free boundary problem or analyzing a binomialtree, it is likely that a computer will be involved in helping theinvestor to determine the optimal exercise time.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 82 / 249

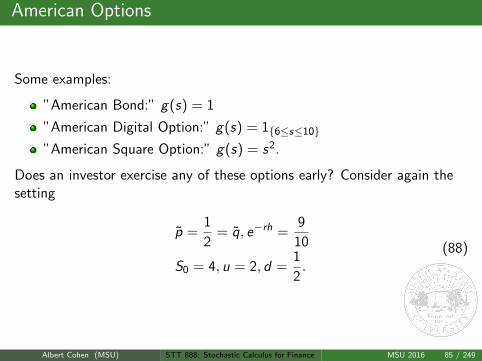

For Freedom! (we must charge extra...)

What happens if we write a contract that allows the purchaser to exercisethe contract whenever she feels it to be in her advantage? By allowing thisextra freedom, we must

Charge more than we would for a European contract that is exercisedonly at the term N.

Hedge our replicating strategy X differently, to allow for thepossibility of early exercise.

Albert Cohen (MSU) STT 888: Stochastic Calculus for Finance MSU 2016 83 / 249

For Freedom! (we must charge extra...)