staying competitive: the changing ltl...

TRANSCRIPT

All rights reserved by CarrierDirect, LLC, 2014

Staying Competitive: The Changing LTL Environment

July 30, 2014

@CarrierDirect

CarrierDirect

Listen To Recording

Legal Disclaimer

2All rights reserved by CarrierDirect, LLC, 2014

CarrierDirect and its affiliates are in the business of providing, among other things, consulting and marketing services to carriers

and third-party logistics companies. In their role they are entrusted with information, some of which may be confidential and

proprietary, regarding market strategies and operations, technology and route-to-market tactics. All information provided herein

is based upon public information shared in publicly disclosed documents, industry events and company-sponsored

presentations. CarrierDirect may be currently, may have in the past or may in the future provide services to certain of the

companies referenced in this presentation.

For more information, contact us at www.carrierdirect.co.

Staying Competitive: The Changing LTL Environment

3All rights reserved by CarrierDirect, LLC, 2014

Introducing CarrierDirect

From The Great Recession To Today

Strategically Engaging Carriers For Partnership

What We’re About At CarrierDirect

4All rights reserved by CarrierDirect, LLC, 2014

Bringing fresh perspectives to the

transportation and logistics industry.

A Brief History of CarrierDirect

5All rights reserved by CarrierDirect, LLC, 2014

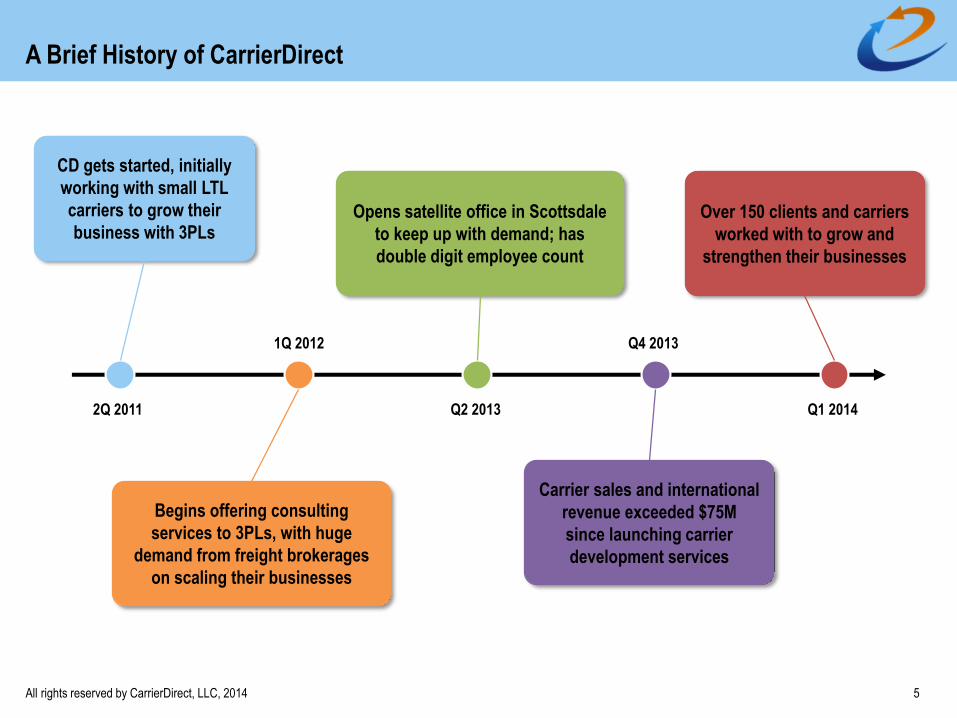

CD gets started, initially

working with small LTL

carriers to grow their

business with 3PLs

2Q 2011

Begins offering consulting

services to 3PLs, with huge

demand from freight brokerages

on scaling their businesses

1Q 2012

Opens satellite office in Scottsdale

to keep up with demand; has

double digit employee count

Q2 2013

Carrier sales and international

revenue exceeded $75M

since launching carrier

development services

Q4 2013

Over 150 clients and carriers

worked with to grow and

strengthen their businesses

Q1 2014

What We Do At CarrierDirect

6All rights reserved by CarrierDirect, LLC, 2014

3PL

3PL

3PL

3PL

3PL

3PL

3PL

3PL

3PL

3PL

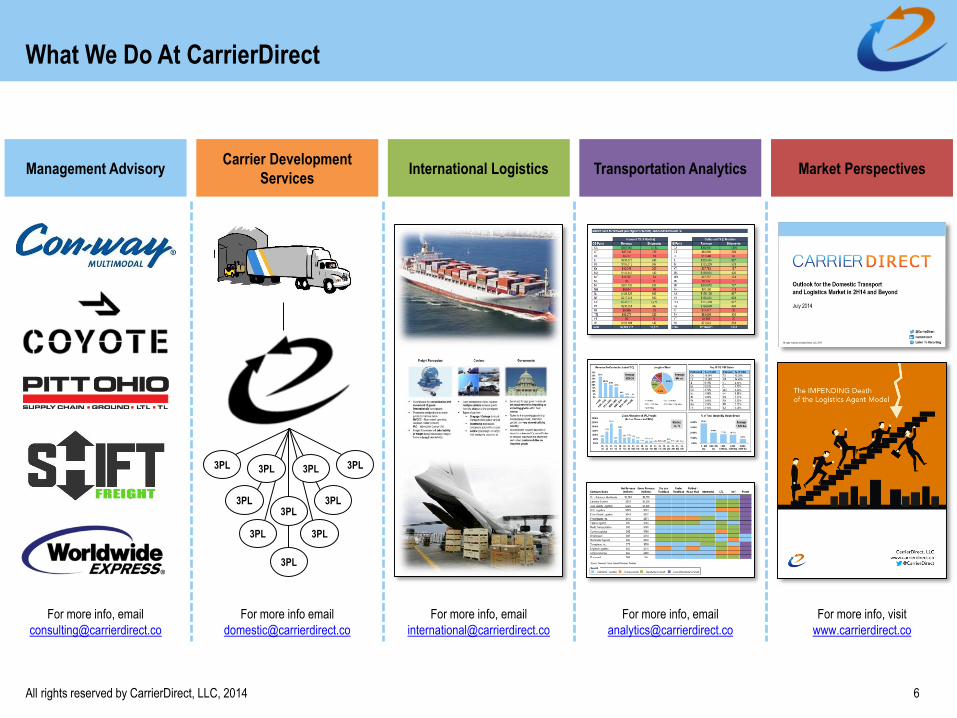

Management AdvisoryCarrier Development

ServicesInternational Logistics Transportation Analytics Market Perspectives

For more info, email

For more info email

For more info, email

For more info, email

For more info, visit

www.carrierdirect.co

Staying Competitive: The Changing LTL Environment

7All rights reserved by CarrierDirect, LLC, 2014

Introducing CarrierDirect

From The Great Recession To Today

Strategically Engaging Carriers For Partnership

M&A Continues At A Rapid Pace In The Logistics Sector

8All rights reserved by CarrierDirect, LLC, 2014

Source: Company Filings, Internal CD Analysis, CapIQ

Date Target

Announced Buyer Transaction Notes

5/13/2014 One Stop Logistics Echo Global Logistics acquires One Stop Logistics, a leading LTL brokerage based in California for

Echo Global $37.3 million, representing an 8.7x EBITDA multiple

3/31/2014 Access America Transport Coyote and Access America complete their merger for a combined revenue of $2+ billion, helping to

Coyote Logistics diversify Coyote's service offerings and strengthen its presence in the LTL arena

3/14/2014 Unitrans International Corporation Roadrunner acquires Unitrans International, a leading provider of international logistics, for $55 million;

Roadrunner Transportation Unitrans generated a TTM total revenue of $84 million at the time of acquisition

2/26/2014 Comcar Logistics Echo Global Logistics acquires Comcar Logistics, a non-asset based truckload brokerage based in

Echo Global Jacksonville, FL; Comcar has approximately $15 million in TTM revenue at the time of acquisition

2/24/2014 Rich Logistics / Everett Transportation Roadrunner acquires Rich Logistics and Everett Transportation for a total transaction value of $48 million

Roadrunner Transportation to strengthen Roadrunner's truckload capacity to/from Mexico; TTM revenue from Rich was $113 million

1/6/2014 Pacer International Pacer, the 3rd largest intermodal provider in America, agrees to be acquired by XPO for an Enterprise

XPO Logistics Value of $296 million; Pacer generated a TTM total revenue of $1.0 billion at the time of announcement

12/10/2013 Landstar SCS XPO Logistics purchased Landstar's Supply Chain Solutions group for $87M at a 7.5X EBITDA multiple

XPO Logistics

7/12/2013 3PD XPO Logistics purchased 3PD, a last mile delivery 3PL for $365 million

XPO Logistics

3/19/2013 Open Mile Echo Global acquired Open Mile, an East Coast TL brokerage for $2M

Echo Global Logistics

Echo and Coyote acquisitions increase the

already well-established dominance of

Chicago’s brokerage market

As XPO integrates its numerous

acquisitions the industry holds

its breath to see what’s next

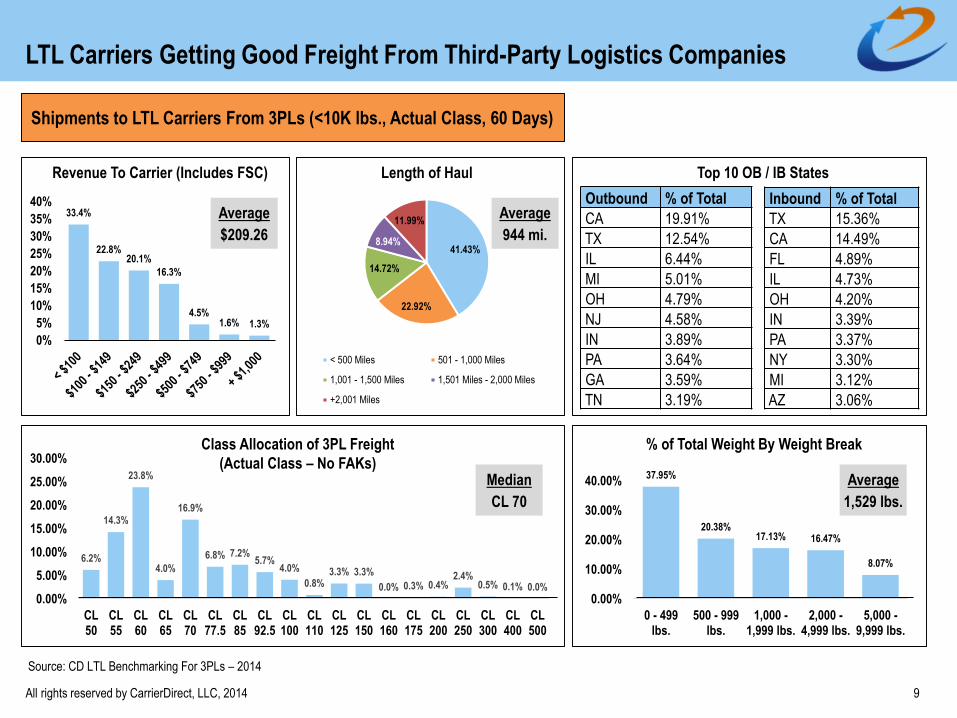

LTL Carriers Getting Good Freight From Third-Party Logistics Companies

9All rights reserved by CarrierDirect, LLC, 2014

Source: CD LTL Benchmarking For 3PLs – 2014

Inbound % of Total

TX 15.36%

CA 14.49%

FL 4.89%

IL 4.73%

OH 4.20%

IN 3.39%

PA 3.37%

NY 3.30%

MI 3.12%

AZ 3.06%

6.2%

14.3%

23.8%

4.0%

16.9%

6.8% 7.2%5.7%

4.0%

0.8%3.3% 3.3%

0.0% 0.3% 0.4%2.4%

0.5% 0.1% 0.0%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

CL50

CL55

CL60

CL65

CL70

CL77.5

CL85

CL92.5

CL100

CL110

CL125

CL150

CL160

CL175

CL200

CL250

CL300

CL400

CL500

37.95%

20.38%17.13% 16.47%

8.07%

0.00%

10.00%

20.00%

30.00%

40.00%

0 - 499lbs.

500 - 999lbs.

1,000 -1,999 lbs.

2,000 -4,999 lbs.

5,000 -9,999 lbs.

41.43%

22.92%

14.72%

8.94%

11.99%

< 500 Miles 501 - 1,000 Miles

1,001 - 1,500 Miles 1,501 Miles - 2,000 Miles

+2,001 Miles

Outbound % of Total

CA 19.91%

TX 12.54%

IL 6.44%

MI 5.01%

OH 4.79%

NJ 4.58%

IN 3.89%

PA 3.64%

GA 3.59%

TN 3.19%

Top 10 OB / IB States

% of Total Weight By Weight Break

33.4%

22.8%20.1%

16.3%

4.5%1.6% 1.3%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Revenue To Carrier (Includes FSC) Length of Haul

Average

$209.26

Average

944 mi.

Average

1,529 lbs.

Median

CL 70

Class Allocation of 3PL Freight

(Actual Class – No FAKs)

Shipments to LTL Carriers From 3PLs (<10K lbs., Actual Class, 60 Days)

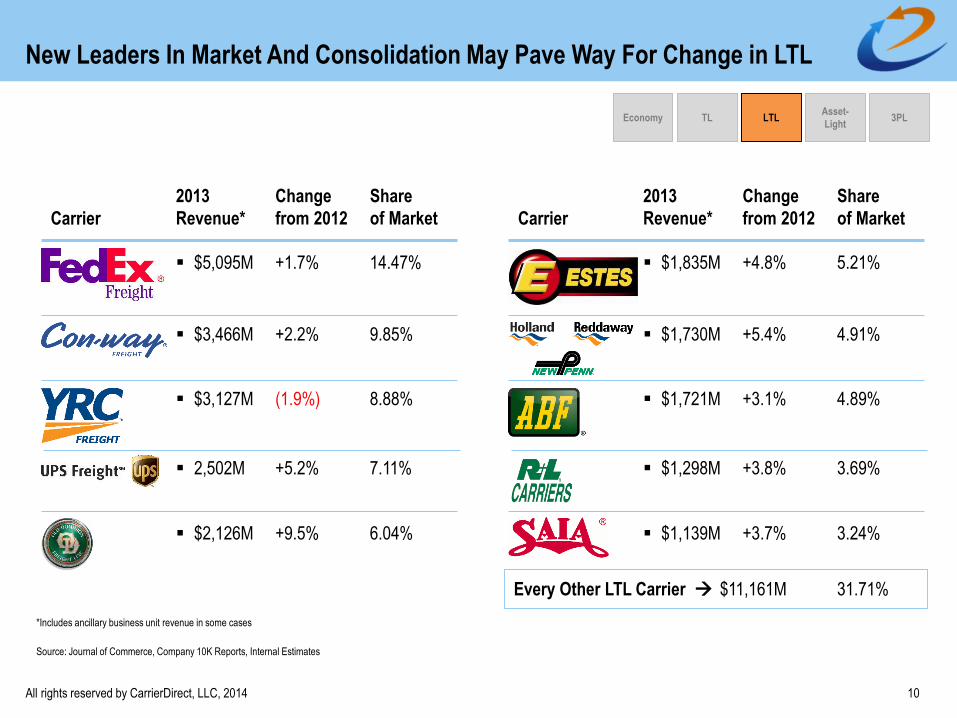

New Leaders In Market And Consolidation May Pave Way For Change in LTL

10All rights reserved by CarrierDirect, LLC, 2014

Carrier

2013

Revenue*

Share

of Market

$5,095M

$3,466M

$3,127M

2,502M

$2,126M

14.47%

9.85%

8.88%

7.11%

6.04%

Source: Journal of Commerce, Company 10K Reports, Internal Estimates

Change

from 2012

+1.7%

+2.2%

(1.9%)

+5.2%

+9.5%

Carrier

2013

Revenue*

Share

of Market

$1,835M

$1,730M

$1,721M

$1,298M

$1,139M

5.21%

4.91%

4.89%

3.69%

3.24%

Change

from 2012

+4.8%

+5.4%

+3.1%

+3.8%

+3.7%

$11,161M 31.71%Every Other LTL Carrier

*Includes ancillary business unit revenue in some cases

TLAsset-

LightLTL 3PLEconomy

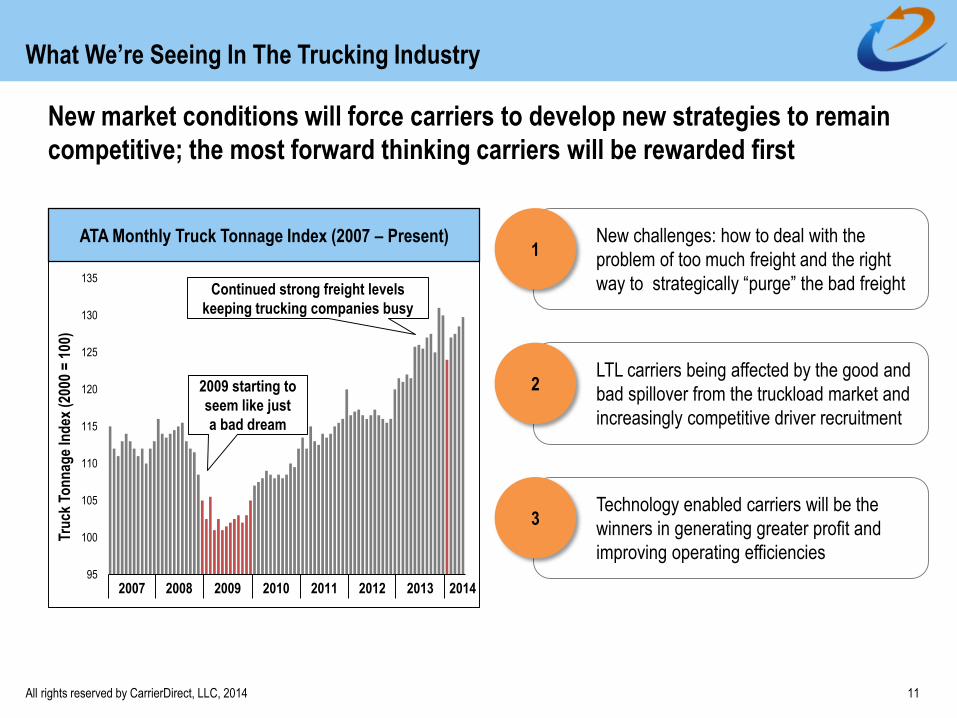

What We’re Seeing In The Trucking Industry

11All rights reserved by CarrierDirect, LLC, 2014

ATA Monthly Truck Tonnage Index (2007 – Present)

95

100

105

110

115

120

125

130

135

2007 2008 2009 2010 2011 2012 2013 2014

Tru

ck T

on

nag

e In

dex

(20

00 =

100

)

Continued strong freight levels

keeping trucking companies busy

2009 starting to

seem like just

a bad dream

New market conditions will force carriers to develop new strategies to remain

competitive; the most forward thinking carriers will be rewarded first

New challenges: how to deal with the

problem of too much freight and the right

way to strategically “purge” the bad freight

1

LTL carriers being affected by the good and

bad spillover from the truckload market and

increasingly competitive driver recruitment

2

Technology enabled carriers will be the

winners in generating greater profit and

improving operating efficiencies

3

“Pushed” Into 3PLs and Shipper Systems

We’re Standing On The Edge Of Big Pricing Changes For LTL Sector

12All rights reserved by CarrierDirect, LLC, 2014

Web Services

Connections

Dimensional

Pricing

Dynamic

Pricing

Real-Time

Information

Gathering

Pay for space taken up in trailer

vs. confusing class-based system

FedEx/UPS goes first, then the industry

Pricing based on needs of carrier’s network

Ability to set future discounts to guide freight

shipments to days that are typically light

Driver / sales rep pricing using

handheld “dimensioners”

LH planning before freight hits dock

Output From Carriers’ Operating System

Getting Paid For What’s

Moved vs. Hoping For Best

Ability to Standardize / Tier

Pricing For Different 3PLs

Immediate Change Of Freight

Mix vs. Long Tariff Changes

Source: CD Internal Perspective

It’s been talked about since de-regulation, but we are truly on the cusp of some pretty significant changes

in the LTL industry that will let carriers better manage their businesses and run more efficient networks

Staying Competitive: The Changing LTL Environment

13All rights reserved by CarrierDirect, LLC, 2014

Introducing CarrierDirect

From The Great Recession To Today

Strategically Engaging Carriers For Partnership

Carriers’ Goal for Using Third-Party Logistics Providers

14All rights reserved by CarrierDirect, LLC, 2014

Add Your Book Of Business With Their Current

Volume That Brings Better Utilization To Their

Assets And More Profit

Carriers Will Start Using 3PLs As An Extension Of Their Sales Channel

15All rights reserved by CarrierDirect, LLC, 2014

A smaller handful of 3PLs will start to be considered a legitimate extension of the carrier’s sales force (and

not thought of as a competitor) that can be used to extend the reach of the carrier without the sales costs

Carrier

Head of Sales

National Account ManagersRegional Key Account ManagersValue-Added Resellers

Carrier 3PL

Whose Employee

A small sub-set of 3PLs that meet

the carrier’s rules of engagement

Tiered pricing that is well thought

out by the carrier to meet goals

Offer business to carriers that is

“scaled” and meets needs of

carrier’s network

Deployed in local markets across

different regions in carrier’s

footprint

Tasked with directives to build out

local sales presence targeting

specific kinds of accounts

(of a size or growth potential)

Located at carrier’s headquarters

Works closely with pricing and

operations teams to build account

and implement new initiatives

Focus on large accounts that

span multiple-regions with

centralized decision-making

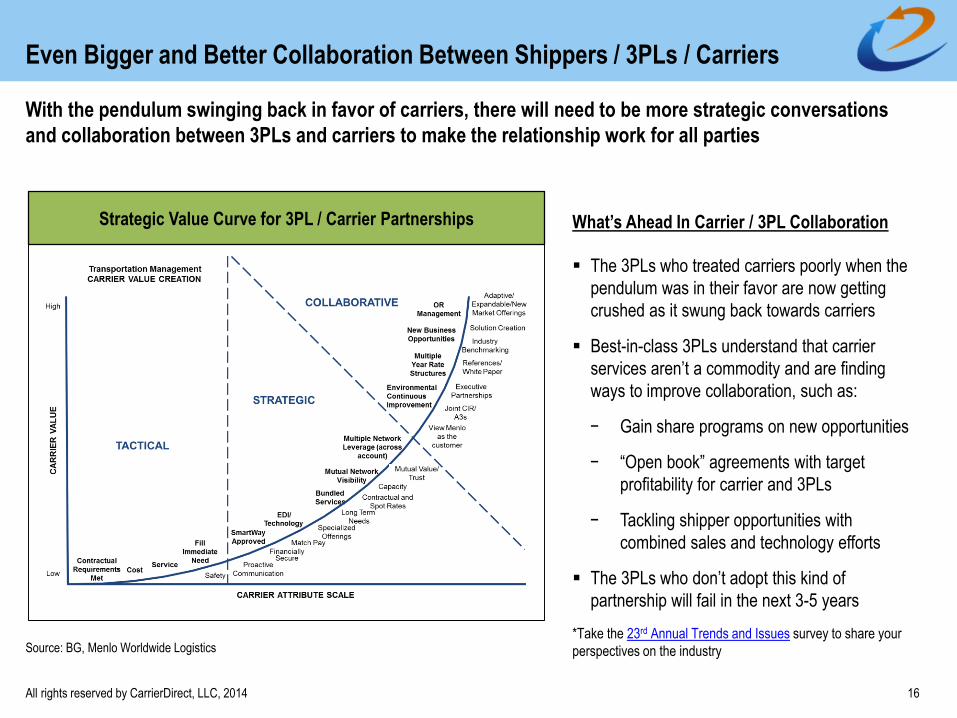

Even Bigger and Better Collaboration Between Shippers / 3PLs / Carriers

16All rights reserved by CarrierDirect, LLC, 2014

Strategic Value Curve for 3PL / Carrier Partnerships

Source: BG, Menlo Worldwide Logistics

What’s Ahead In Carrier / 3PL Collaboration

The 3PLs who treated carriers poorly when the

pendulum was in their favor are now getting

crushed as it swung back towards carriers

Best-in-class 3PLs understand that carrier

services aren’t a commodity and are finding

ways to improve collaboration, such as:

− Gain share programs on new opportunities

− “Open book” agreements with target

profitability for carrier and 3PLs

− Tackling shipper opportunities with

combined sales and technology efforts

The 3PLs who don’t adopt this kind of

partnership will fail in the next 3-5 years

*Take the 23rd Annual Trends and Issues survey to share your

perspectives on the industry

With the pendulum swinging back in favor of carriers, there will need to be more strategic conversations

and collaboration between 3PLs and carriers to make the relationship work for all parties

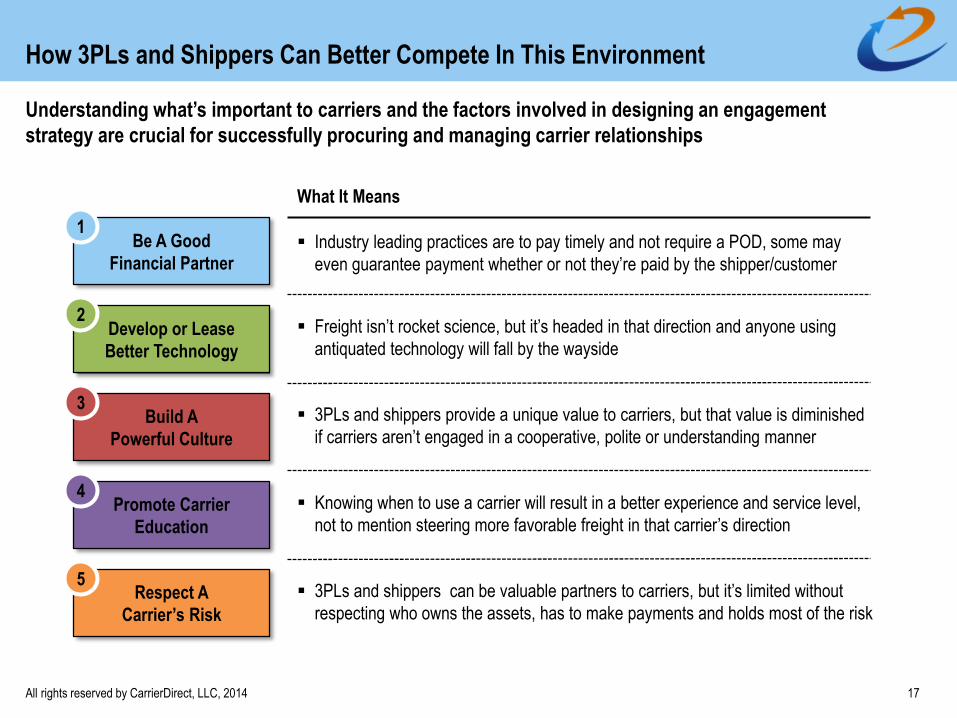

How 3PLs and Shippers Can Better Compete In This Environment

17All rights reserved by CarrierDirect, LLC, 2014

Understanding what’s important to carriers and the factors involved in designing an engagement

strategy are crucial for successfully procuring and managing carrier relationships

Build A

Powerful Culture

Develop or Lease

Better Technology

Be A Good

Financial Partner

1

2

3

Industry leading practices are to pay timely and not require a POD, some may

even guarantee payment whether or not they’re paid by the shipper/customer

Freight isn’t rocket science, but it’s headed in that direction and anyone using

antiquated technology will fall by the wayside

3PLs and shippers provide a unique value to carriers, but that value is diminished

if carriers aren’t engaged in a cooperative, polite or understanding manner

What It Means

Respect A

Carrier’s Risk

Promote Carrier

Education

4

5

Knowing when to use a carrier will result in a better experience and service level,

not to mention steering more favorable freight in that carrier’s direction

3PLs and shippers can be valuable partners to carriers, but it’s limited without

respecting who owns the assets, has to make payments and holds most of the risk

CarrierDirect

All rights reserved by CarrierDirect, LLC, 2014 18

Erik Malin

Director of Strategy

(312) 546-3022

Erik Malin

CarrierDirect, LLC

105 West Adams, Suite 3010

Chicago, IL 60603

@CarrierDirect

CarrierDirect

Listen to Webinar Presentation

www.carrierdirect.co