statewide meetings february 2015 02.02.15 version league of arizona cities and towns: psprs pension...

TRANSCRIPT

Statewide Meetings

February 2015

0 2 . 0 2 . 1 5 v e r s i o n

LEAGUE OF ARIZONA CITIES AND TOWNS:

PSPRS PENSION TASK FORCE

2

Formed in June, 2014 Partnership with ACMA and GFOAz 15 Members Review all aspects of PSPRS,

identify areas of improvement, and reform recommendations

TASK FORCE

3

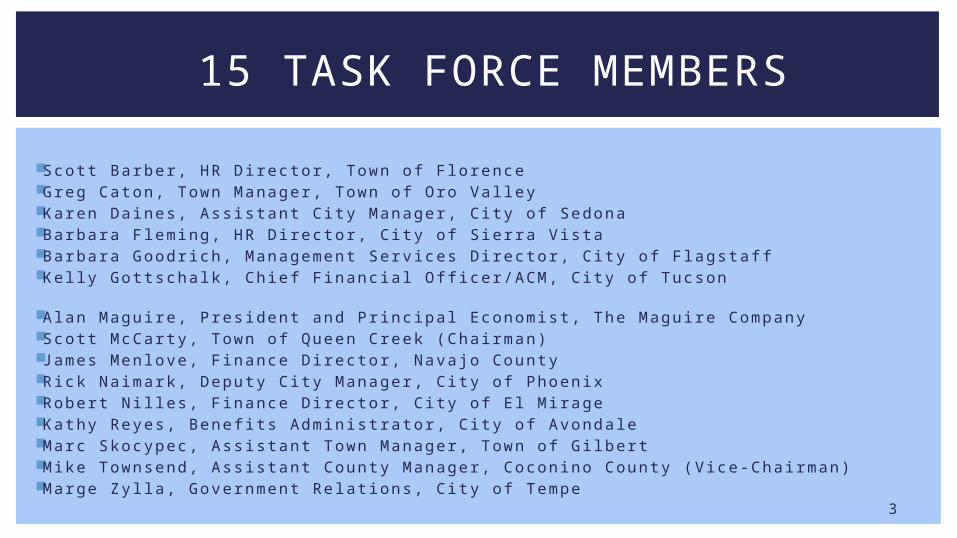

Scott Barber, HR Director , Town of F lorence Greg Caton, Town Manager, Town of Oro Val ley Karen Daines, Assistant Ci ty Manager, C i ty of Sedona Barbara F leming, HR Director , C i ty of S ierra Vista Barbara Goodr ich, Management Services Director , C i ty of F lagstaff Kel ly Gottschalk, Chief Financia l Offi cer/ACM, City of Tucson

Alan Maguire, President and Pr incipal Economist , The Maguire Company Scott McCarty, Town of Queen Creek (Chairman) James Menlove, Finance Director , Navajo County Rick Naimark, Deputy City Manager, C i ty of Phoenix Robert Ni l les, Finance Director , C i ty of E l Mirage Kathy Reyes, Benefi ts Administrator , C i ty of Avondale Marc Skocypec, Assistant Town Manager, Town of Gi lbert Mike Townsend, Assistant County Manager, Coconino County (Vice-Chairman) Marge Zyl la , Government Relat ions, C i ty of Tempe

15 TASK FORCE MEMBERS

4

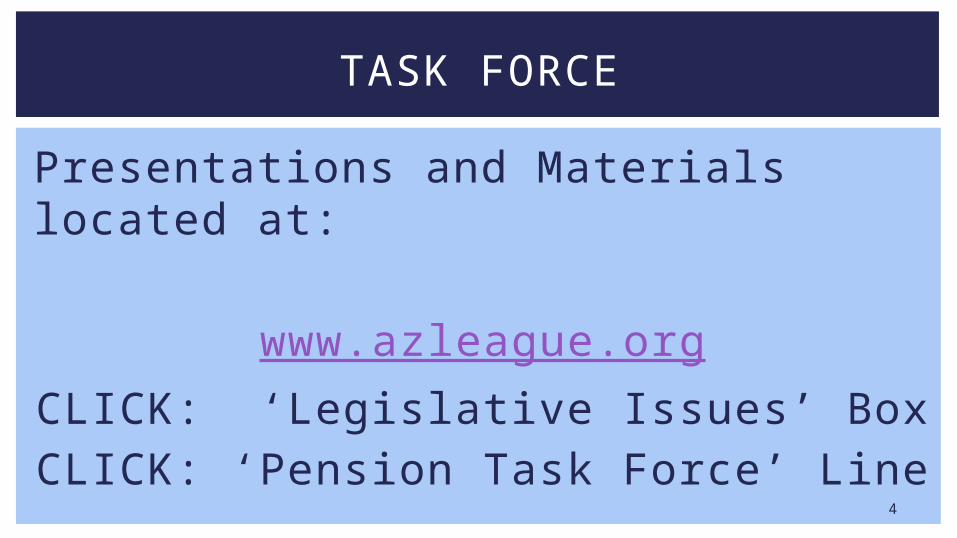

Presentations and Materials located at:

www.azleague.orgCLICK: ‘Legislative Issues’ BoxCLICK: ‘Pension Task Force’ Line

TASK FORCE

5

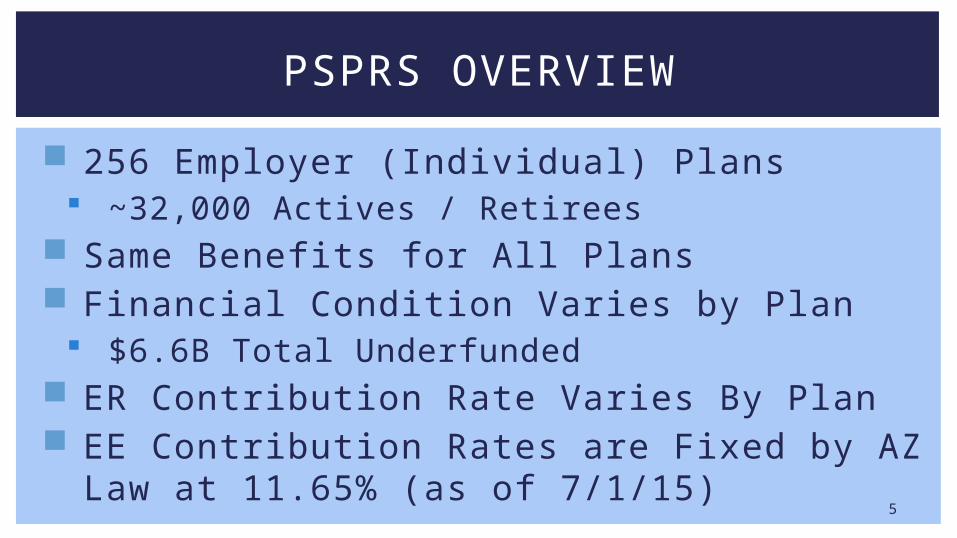

256 Employer (Individual) Plans ~32,000 Actives / Retirees

Same Benefits for All Plans Financial Condition Varies by Plan

$6.6B Total Underfunded ER Contribution Rate Varies By Plan EE Contribution Rates are Fixed by AZ

Law at 11.65% (as of 7/1/15)

PSPRS OVERVIEW

6

Phase 1 Information and EducationPhase 2 Employer Recommended PracticesPhase 3 Yardstick: Characteristics of a Well-

Designed Plan

TASK FORCE APPROACH

7

Phase 1

8

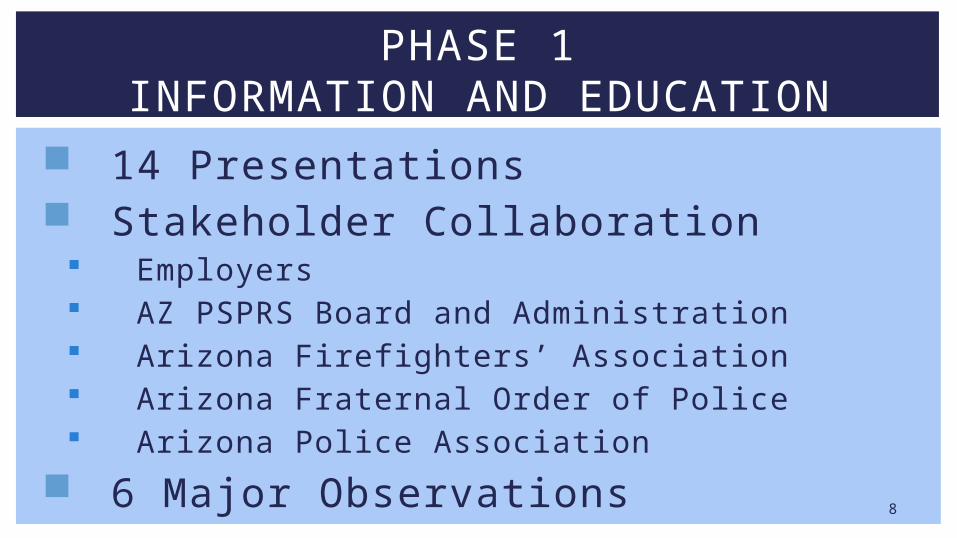

14 Presentations Stakeholder Collaboration

Employers AZ PSPRS Board and Administration Arizona Firefighters’ Association Arizona Fraternal Order of Police Arizona Police Association

6 Major Observations

PHASE 1INFORMATION AND EDUCATION

9

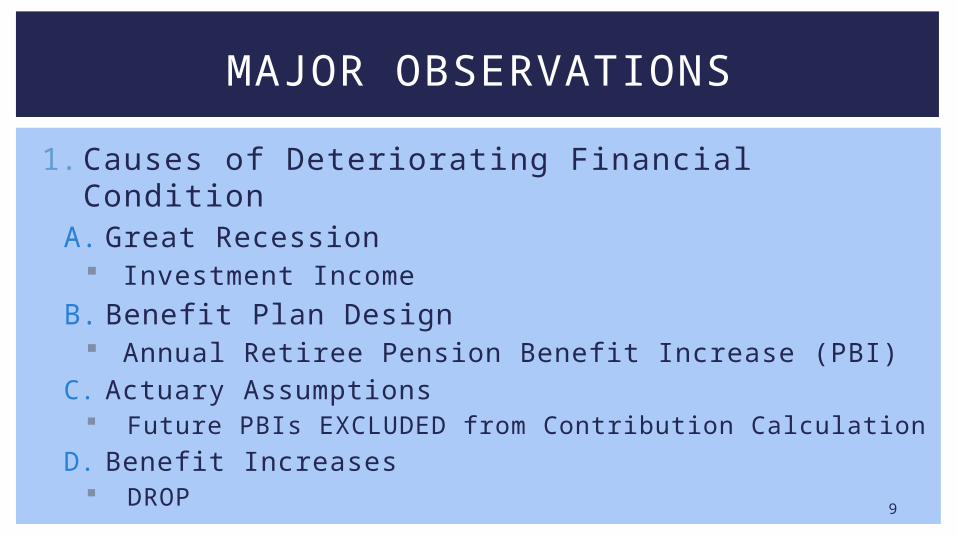

1. Causes of Deteriorating Financial Condition A. Great Recession

Investment Income

B. Benefit Plan Design Annual Retiree Pension Benefit Increase (PBI)

C. Actuary Assumptions Future PBIs EXCLUDED from Contribution Calculation

D. Benefit Increases DROP

MAJOR OBSERVATIONS

10

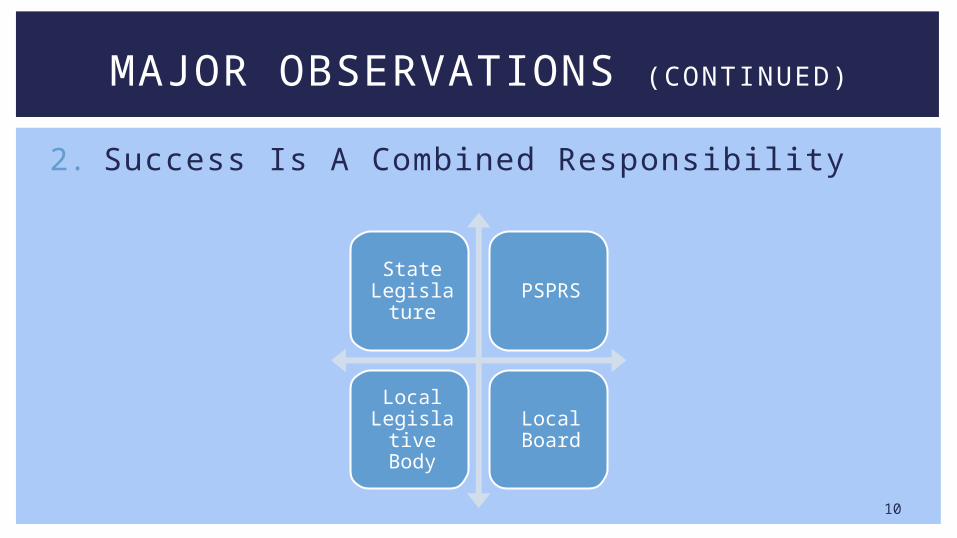

2. Success Is A Combined Responsibility

MAJOR OBSERVATIONS (CONTINUED)

State Legislatu

rePSPRS

Local Legislativ

e Body

Local Board

11

3. PSPRS Employers are Managing…or Not Managing…a Pension Plan

PSPRS in Not ASRS Assumptions Used vs. Local Reality

Fiduciary Responsibility Exists Legislative Body and Local Board

MAJOR OBSERVATIONS (CONTINUED)

12

4. “Know Your Numbers” Normal Cost vs. Unfunded Liability Focus on Dollar Amounts, Not Rates Don’t be Fooled by Low Contributions

Today, They Will Increase Plan Maturity / Demographics Retiree Annual PBI

MAJOR OBSERVATIONS (CONTINUED)

13

5. Improve Employer Engagement Task Force

Clearing House for Concerns and Thoughts Presentations to Councils, Organizations

MAJOR OBSERVATIONS (CONTINUED)

14

6. Plan Changes that Effect Existing Members or Retirees are Not Possible (Legally Challengeable)

Fields’ Case (Decided-$375 million impact)

Restored PBI Formula for Retirees as of 6/1/11

Hall Case (Pending) Restore PBI formula Active Members Reduce EE Contributions Back to 7.65%

MAJOR OBSERVATIONS (CONCLUDED)

15

Phase 2

16

Employers Can Improve Their Plan’s Financial Condition Today Without Waiting for Resolution of Pending Litigation or Legislative Changes

See Separate Section of Presentation for Detailed Discussion

PHASE 2 EMPLOYER RECOMMENDED

PRACTICES

17

Phase 3

18

PHASE 3DESIGN A WELL-STRUCTURED PLAN (A

YARDSTICK)Goal

Principles

Plan Design Elements

19

What should the Employee, Retiree, Employer, and Taxpayer get out of the System?

How is this Accomplished? Type of Plan, Cost Sharing, Annual

Pension Increase (PBI), etc.

KEY QUESTIONS

20

1. Adequate and Affordable2. Financially Solvent3. Transparent and Accountable

GUIDING PRINCIPLES

21

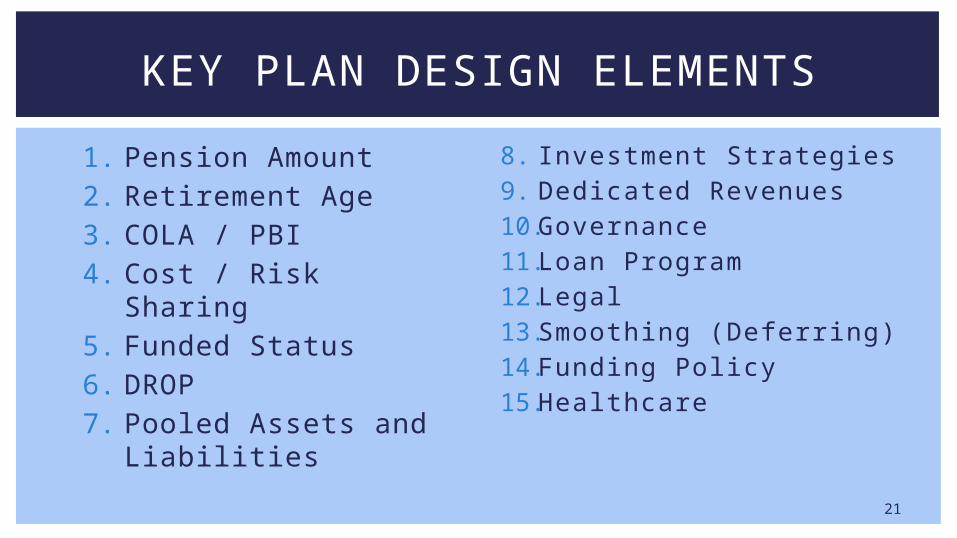

1. Pension Amount2. Retirement Age3. COLA / PBI4. Cost / Risk Sharing5. Funded Status6. DROP7. Pooled Assets and

Liabilities

8. Investment Strategies9. Dedicated Revenues10.Governance11.Loan Program12.Legal13.Smoothing (Deferring)14.Funding Policy15.Healthcare

KEY PLAN DESIGN ELEMENTS

22

Recommendation to League’s Executive Committee

Tool to Evaluate Reform Proposals

THE YARDSTICK

23

Employer Recommended

Practices

24

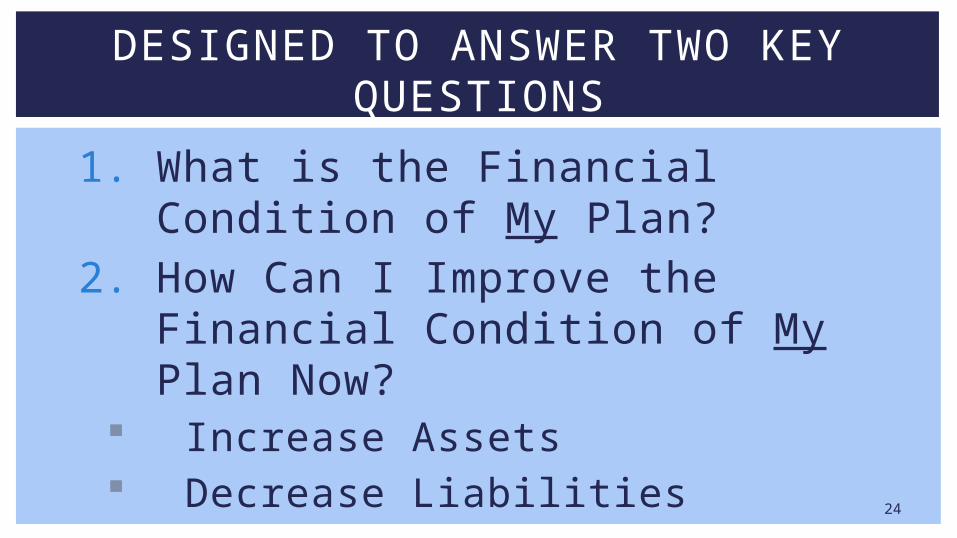

1. What is the Financial Condition of My Plan?

2. How Can I Improve the Financial Condition of My Plan Now?

Increase Assets Decrease Liabilities

DESIGNED TO ANSWER TWO KEY QUESTIONS

25

1. Unfunded Liability2. Funded Status (Funded Ratio)3. Pension Funding Formula

ACTUARY 101

26

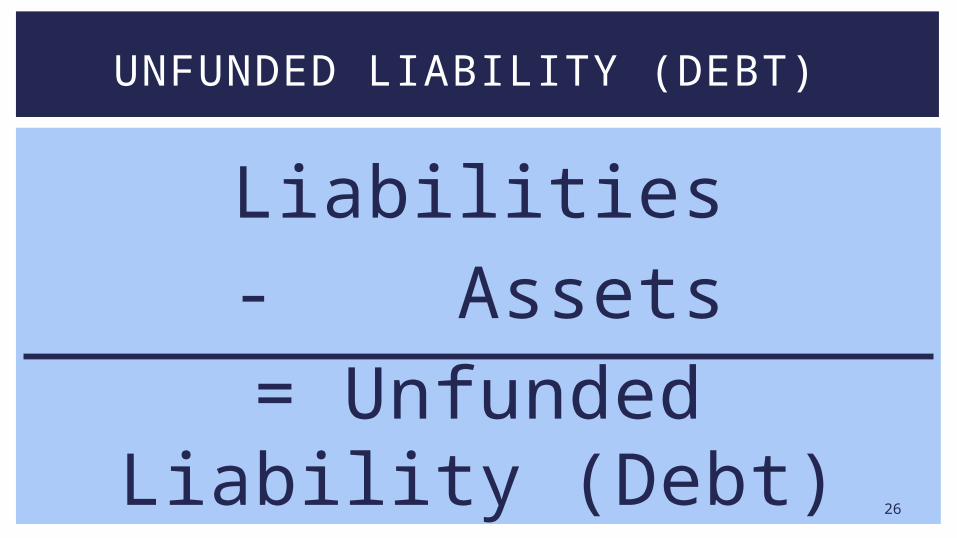

UNFUNDED LIABILITY (DEBT)

Liabilities- Assets

= Unfunded Liability (Debt)

27

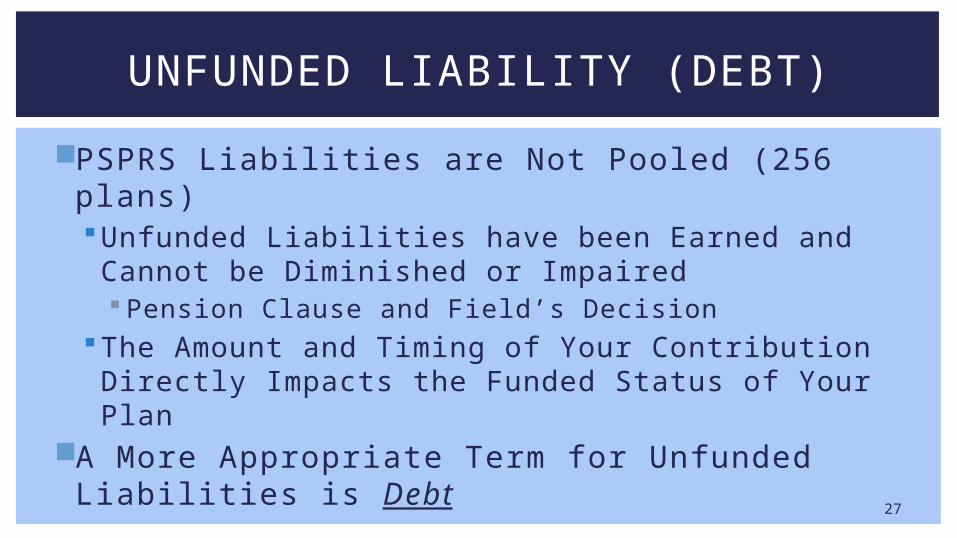

PSPRS Liabilities are Not Pooled (256 plans)Unfunded Liabilities have been Earned and Cannot be Diminished or Impaired Pension Clause and Field’s Decision

The Amount and Timing of Your Contribution Directly Impacts the Funded Status of Your Plan

A More Appropriate Term for Unfunded Liabilities is Debt

UNFUNDED LIABILITY (DEBT)

28

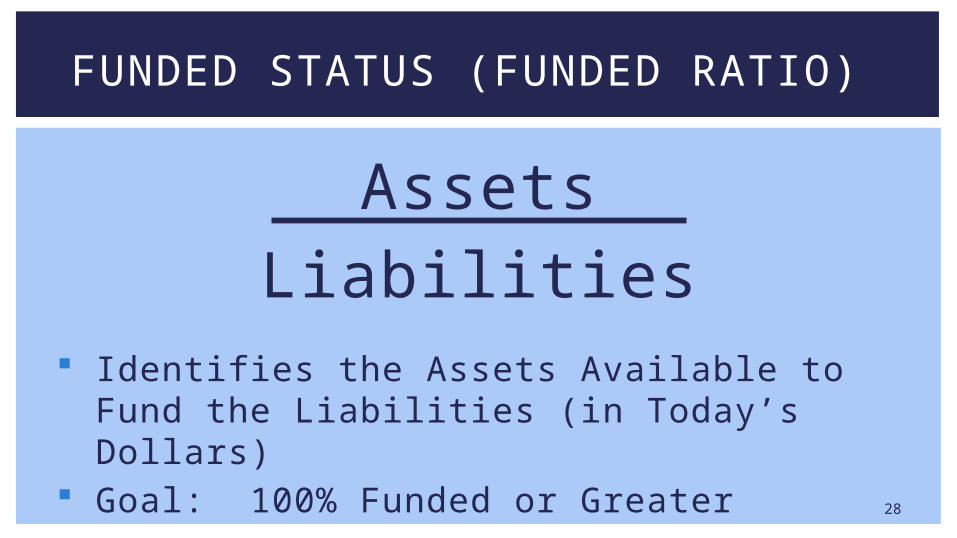

Identifies the Assets Available to Fund the Liabilities (in Today’s Dollars)

Goal: 100% Funded or Greater

FUNDED STATUS (FUNDED RATIO)

AssetsLiabilities

29

Total

Accrued Liability $28.8M

Total Assets $7.6M

Unfunded Liability $21.2M

Assets as a % of Liabilities (Funded Status)

26%

Unfunded Liability Per Capita $1,630

PARADISE VALLEY’S UNFUNDED LIABILITY AT 6/30/14

30

C + I = B + EContributions Interest Benefits Expenses

PENSION FUNDING EQUATION

31

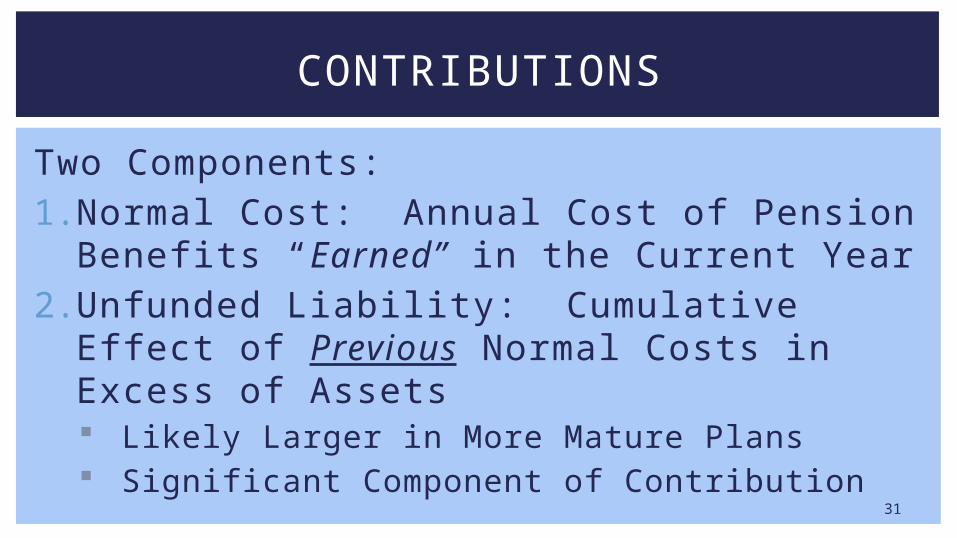

Two Components:1. Normal Cost: Annual Cost of Pension

Benefits “Earned” in the Current Year2. Unfunded Liability: Cumulative Effect of

Previous Normal Costs in Excess of Assets Likely Larger in More Mature Plans Significant Component of Contribution

CONTRIBUTIONS

32

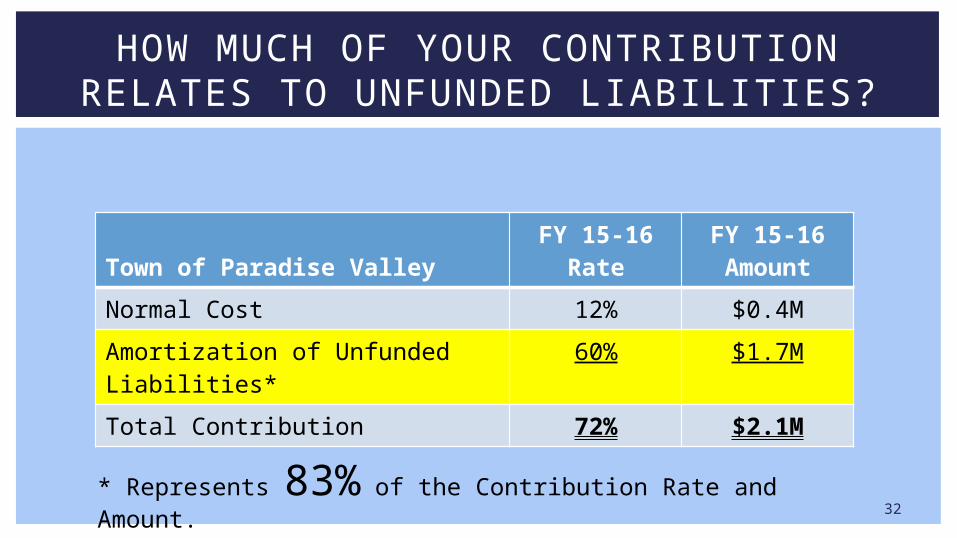

Town of Paradise ValleyFY 15-16

RateFY 15-16Amount

Normal Cost 12% $0.4M

Amortization of Unfunded Liabilities*

60% $1.7M

Total Contribution 72% $2.1M

HOW MUCH OF YOUR CONTRIBUTION RELATES TO UNFUNDED LIABILITIES?

* Represents 83% of the Contribution Rate and Amount.

33

The Employer Recommended

Practices Are . . .

34

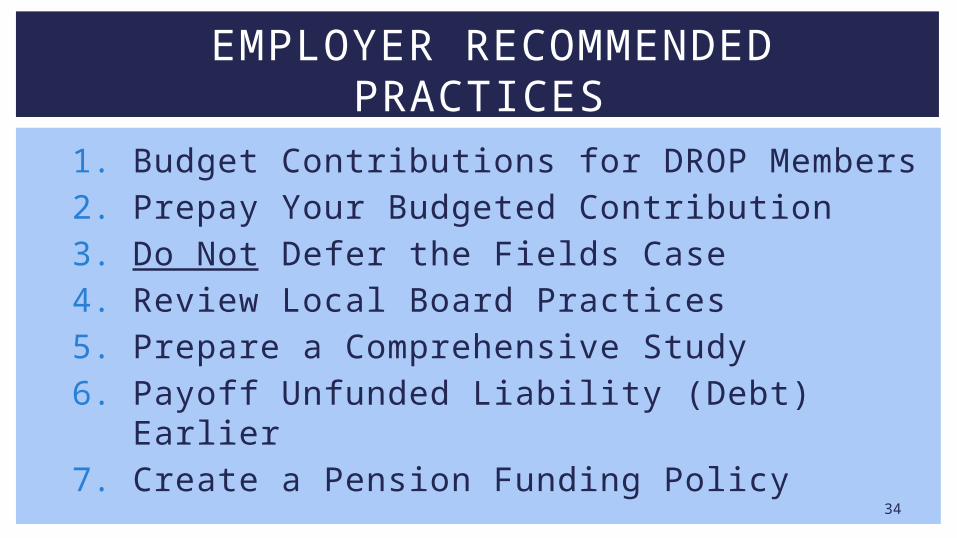

1. Budget Contributions for DROP Members

2. Prepay Your Budgeted Contribution3. Do Not Defer the Fields Case4. Review Local Board Practices5. Prepare a Comprehensive Study6. Payoff Unfunded Liability (Debt) Earlier7. Create a Pension Funding Policy

EMPLOYER RECOMMENDED PRACTICES

35

DROP Has A Cost Even Though ER Contributions are Not Required

ER Contributions Have Been Budgeted Since Hire and Get Put Back In to Budget Once Replacement EE is Hired

Avoids Future Budget Increase

1. BUDGET CONTRIBUTIONS FOR DROP MEMBERS

36

Results in Two Outcomes1. Increases Your Investment Income2. Reduces Your Unfunded Liability

2. PREPAY YOUR BUDGETED CONTRIBUTION

37

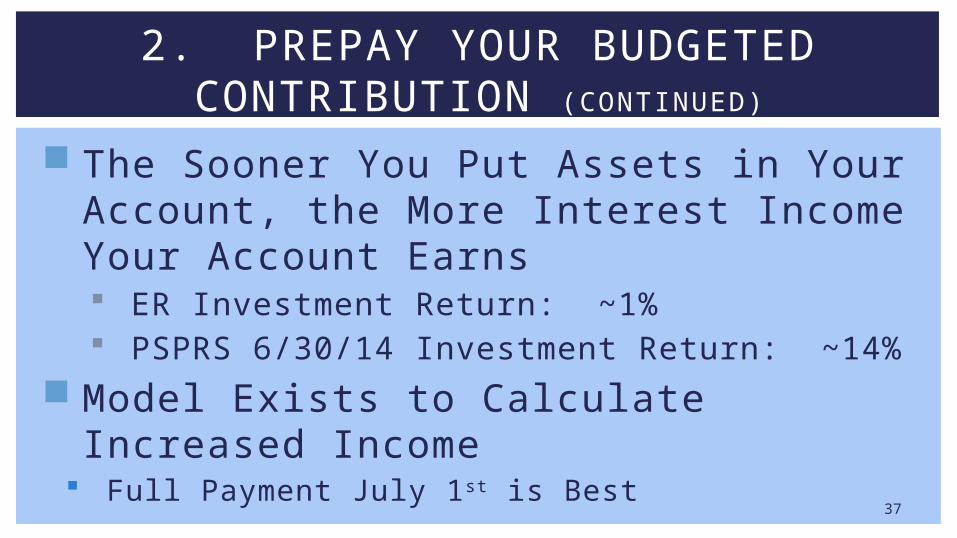

The Sooner You Put Assets in Your Account, the More Interest Income Your Account Earns ER Investment Return: ~1% PSPRS 6/30/14 Investment Return: ~14%

Model Exists to Calculate Increased Income

Full Payment July 1st is Best

2. PREPAY YOUR BUDGETED CONTRIBUTION (CONTINUED)

38

The Actuary Amount is Only an Estimate – The Minimum Amount

Any Amount is Excess of the Minimum Reduces the Unfunded Liability

2. PREPAY YOUR BUDGETED CONTRIBUTION (CONTINUED)

39

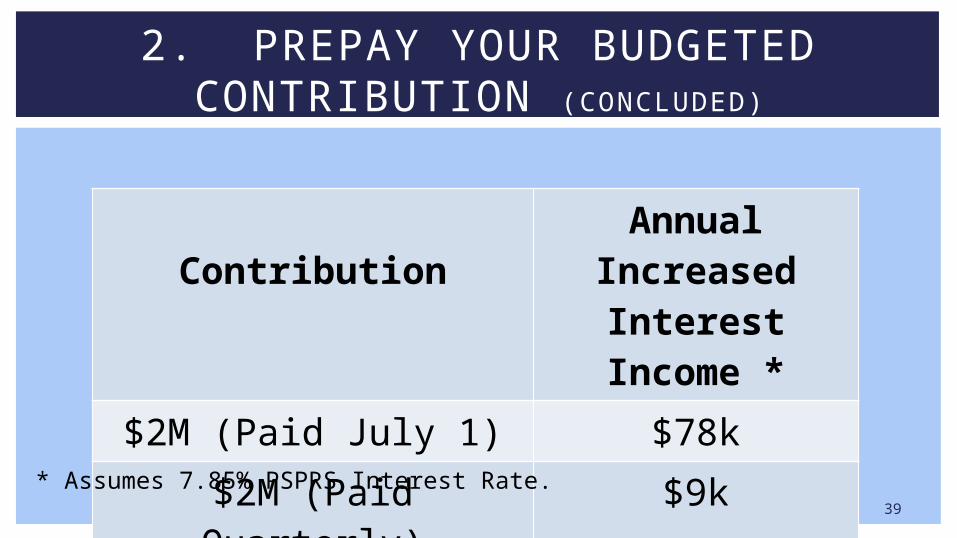

2. PREPAY YOUR BUDGETED CONTRIBUTION (CONCLUDED)

ContributionAnnual

IncreasedInterest Income *

$2M (Paid July 1) $78k$2M (Paid Quarterly) $9k

* Assumes 7.85% PSPRS Interest Rate.

40

PSPRS Board Adopted a Policy to Allow for a 3-Year Deferral Due to the Potential Financial Impact on Employers

Your Decision is Due by 3/1/15 Deferral Will Cost More over Next 22 Years

Model Created to Calculate Cost of Deferral Available on PSPRS and League’s Website

3. DO NOT DEFER THE FIELDS CASE

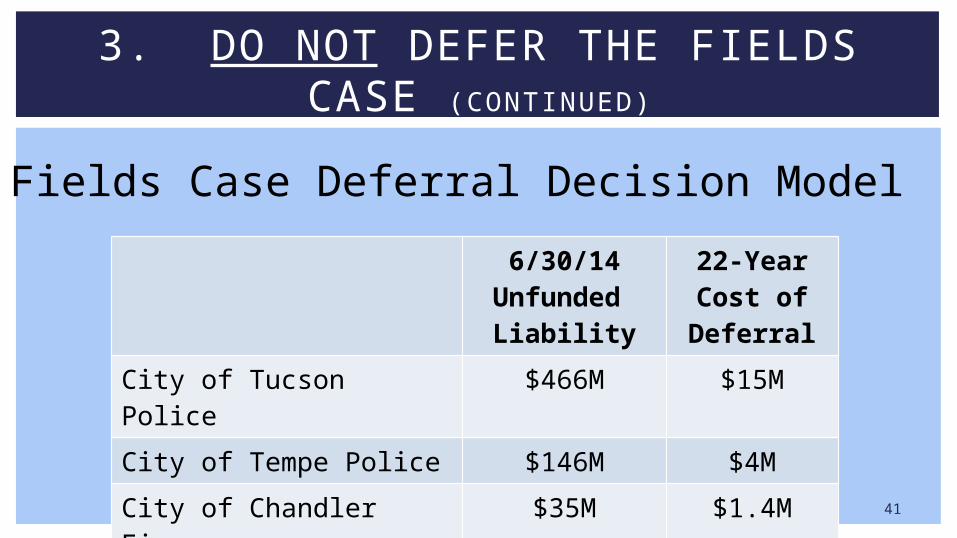

41

6/30/14Unfunded Liability

22-YearCost of Deferral

City of Tucson Police $466M $15M

City of Tempe Police $146M $4M

City of Chandler Fire $35M $1.4M

3. DO NOT DEFER THE FIELDS CASE (CONTINUED)

Fields Case Deferral Decision Model

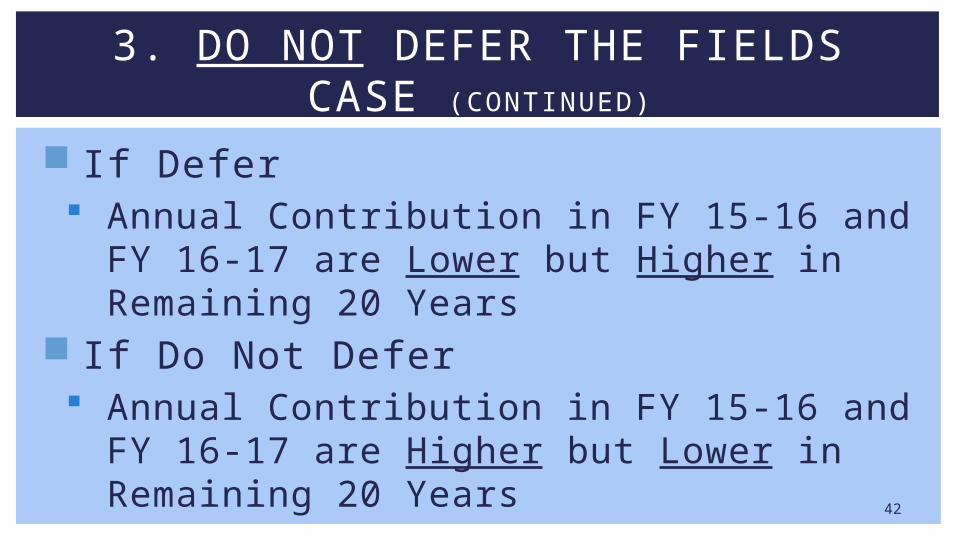

42

If Defer Annual Contribution in FY 15-16 and FY

16-17 are Lower but Higher in Remaining 20 Years

If Do Not Defer Annual Contribution in FY 15-16 and FY

16-17 are Higher but Lower in Remaining 20 Years

3. DO NOT DEFER THE FIELDS CASE (CONTINUED)

43

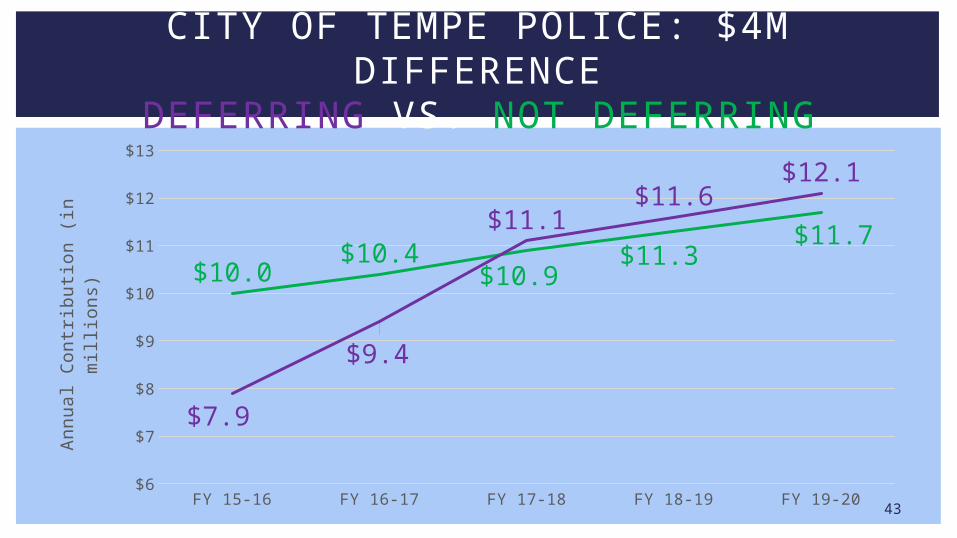

CITY OF TEMPE POLICE: $4M DIFFERENCE

DEFERRING VS. NOT DEFERRING

FY 15-16 FY 16-17 FY 17-18 FY 18-19 FY 19-20$6

$7

$8

$9

$10

$11

$12

$13

$10.0$10.4

$10.9$11.3

$11.7

$7.9

$9.4

$11.1$11.6

$12.1

Annual C

ontr

ibuti

on (

in m

illio

ns)

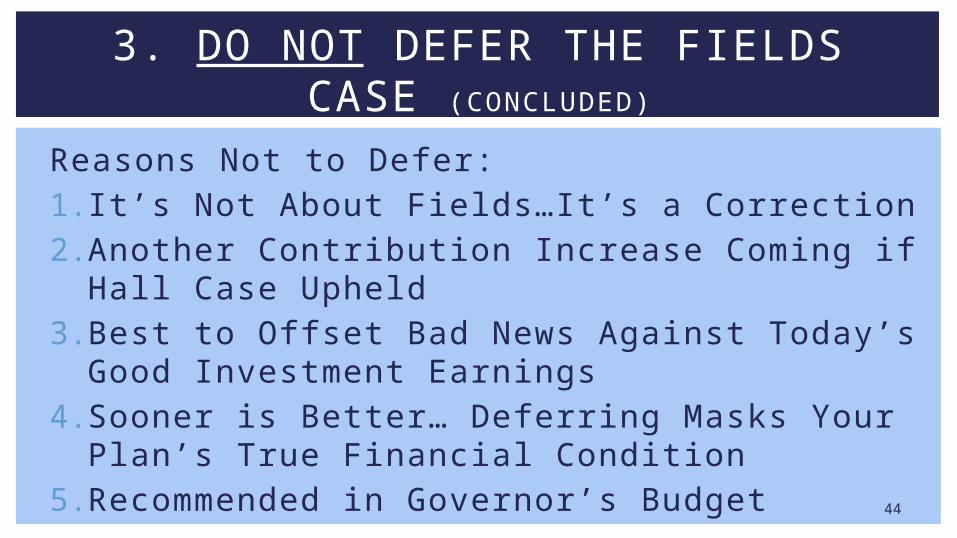

44

Reasons Not to Defer:1. It’s Not About Fields…It’s a Correction2. Another Contribution Increase Coming if Hall

Case Upheld3. Best to Offset Bad News Against Today’s

Good Investment Earnings4. Sooner is Better… Deferring Masks Your

Plan’s True Financial Condition5. Recommended in Governor’s Budget

3. DO NOT DEFER THE FIELDS CASE (CONCLUDED)

45

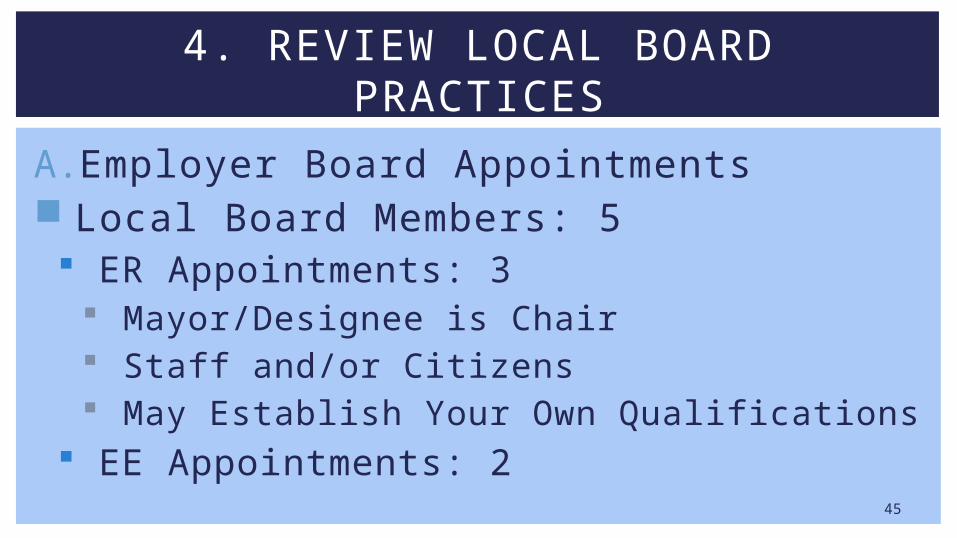

A. Employer Board Appointments Local Board Members: 5

ER Appointments: 3 Mayor/Designee is Chair Staff and/or Citizens May Establish Your Own Qualifications

EE Appointments: 2

4. REVIEW LOCAL BOARD PRACTICES

46

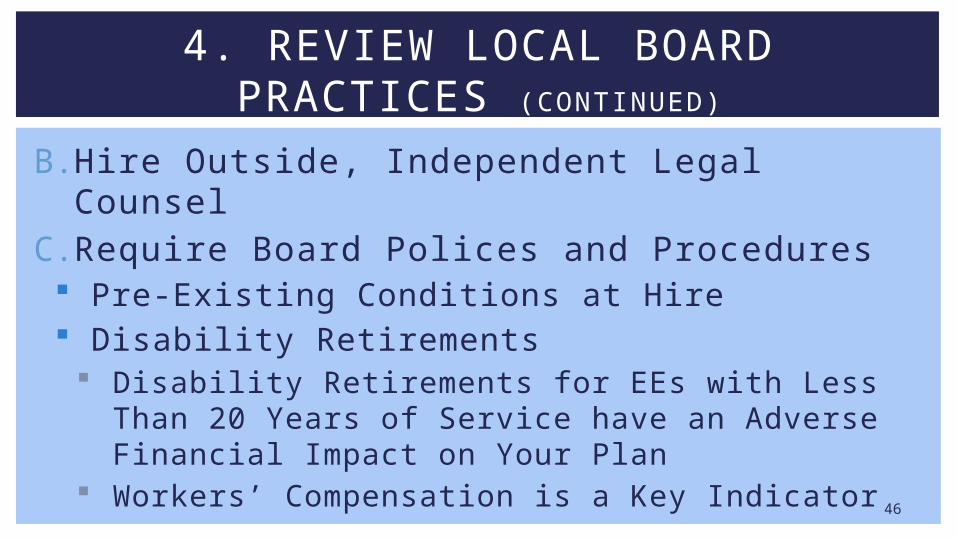

B. Hire Outside, Independent Legal CounselC. Require Board Polices and Procedures

Pre-Existing Conditions at Hire Disability Retirements

Disability Retirements for EEs with Less Than 20 Years of Service have an Adverse Financial Impact on Your Plan

Workers’ Compensation is a Key Indicator

4. REVIEW LOCAL BOARD PRACTICES (CONTINUED)

47

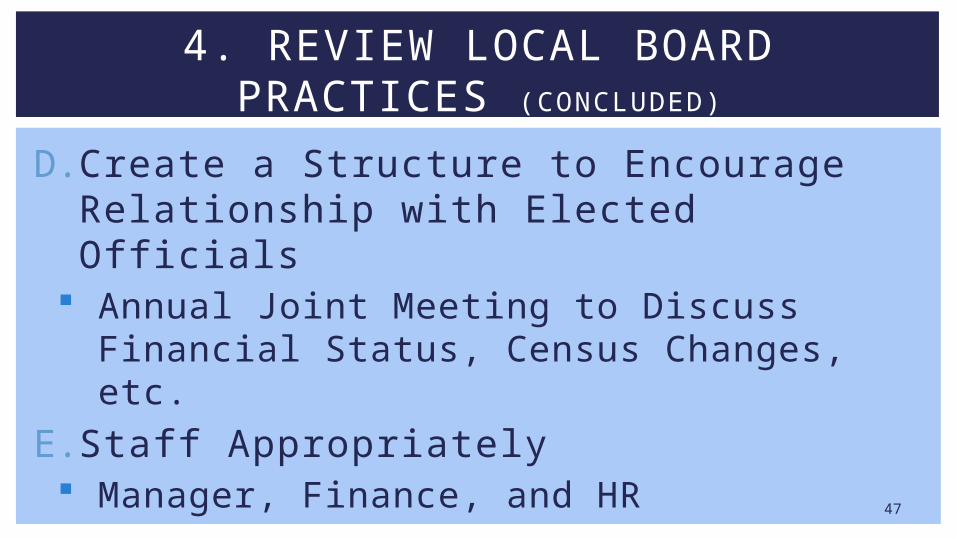

D.Create a Structure to Encourage Relationship with Elected Officials

Annual Joint Meeting to Discuss Financial Status, Census Changes, etc.

E. Staff Appropriately Manager, Finance, and HR

4. REVIEW LOCAL BOARD PRACTICES (CONCLUDED)

48

“A Movie”: Establishes a Baseline Annual Valuation Report is a “Picture” Where are You in the Pension Life

Cycle? Young Today, Mature Tomorrow…

Reconstructs Your Current Financial Condition

5. PREPARE A COMPREHENSIVE STUDY

49

Provides Census Information Ratio of Actives to Retirees Turnover Rates given DROP, Staffing

Levels Identifies ER Specific Practices Final Salary Components (e.g. Spiking) Impact of Lateral Hires

5. PREPARE A COMPREHENSIVE STUDY (CONCLUDED)

50

Sooner Is Fairer Currently Being Paid Off Over 22 Years at 7.85%

Interest Rate in Your Contribution Amount PV: $21M Unfunded Now; $49M Final Cost

Treat and Manage as Any Other Debt What is the Impact to Your Operating Budget? What is the Best Way to Reduce or Eliminate

this Debt?

6. PAYOFF UNFUNDED LIABILITY (DEBT) EARLIER

51

Options to Reduce or Eliminate:1. Use Positive Variances from Operating

Budget2. Use Reserves3. Issue Debt for Projects You Were Planning

to Pay Cash For4. Add a New Line Item to Your Budget to

Make a Direct Payment Against It

6. PAYOFF UNFUNDED LIABILITY (DEBT) EARLIER (CONCLUDED)

52

A Comprehensive Document with the Objective of Ensuring Financial Resources Exist to Fund Pension Obligations

Accounting Standard Requirement Engages Elected Officials Avoids or Fixes “Kicking the Can Down the

Road” “If that, then this…”

7. CREATE A PENSION FUNDING POLICY

53

Policy Components Defines Funded Status Goal

EXAMPLE: Not Less Than 80% Defines Annual Contribution Amount

EXAMPLE: Contribution Not Greater Than 10% of Operating Revenues

Defines Actuary Assumptions Identifies Roles and Responsibilities

7. CREATE A PENSION FUNDING POLICY (CONCLUDED)

54

Paradise Valley Completed Comprehensive Analysis Developing Pension Funding Policy

Sierra Vista, Apache Junction Developing Comprehensive Report

Youngtown Considering Payoff of Entire Unfunded

Liability

WHAT ARE OTHER EMPLOYERS DOING?

55

Education and Collaboration Employer Engagement Employer Recommended Practices Yardstick Legislative Solutions Will Take

Time

TASK FORCE SUMMARY

56

WE NEED YOU

FINAL THOUGHT

57

Questionsand

Comments