state of the retail q4 2011

TRANSCRIPT

February 2012

State of the U.S. Online Retail Economy in Q4 2011

Gian Fulgoni, Chairman, comScore, Inc.

Andrew Lipsman, VP Industry Analysis, comScore, Inc.

Note: A copy of this presentation will be sent to all attendees within 24 hours of today’s webinar

2 © comScore, Inc. Proprietary and Confidential.

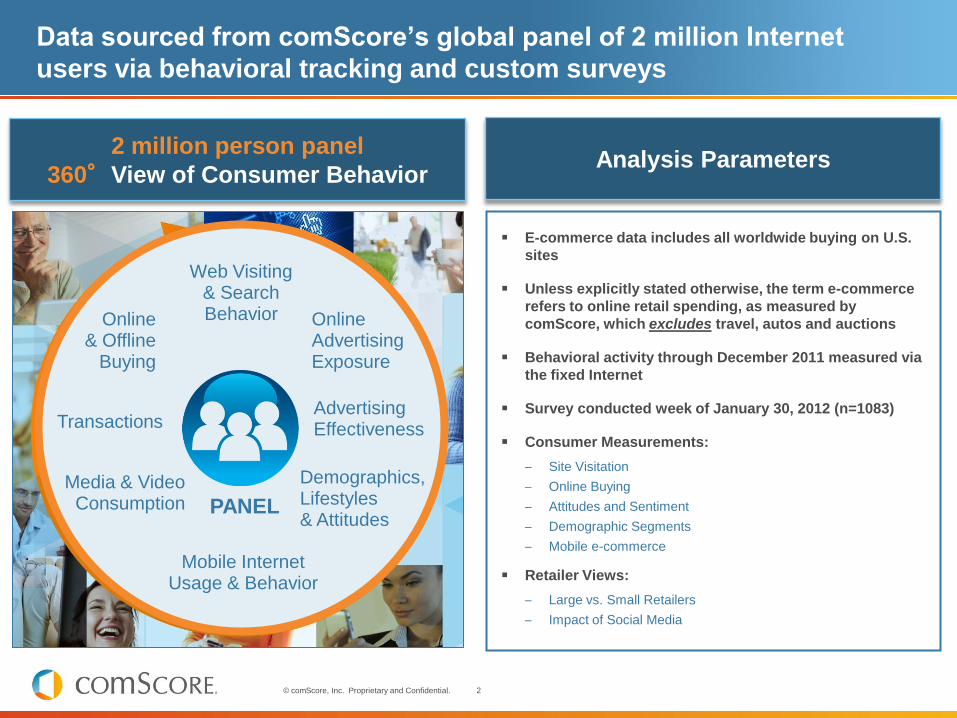

Data sourced from comScore‟s global panel of 2 million Internet

users via behavioral tracking and custom surveys

E-commerce data includes all worldwide buying on U.S.

sites

Unless explicitly stated otherwise, the term e-commerce

refers to online retail spending, as measured by

comScore, which excludes travel, autos and auctions

Behavioral activity through December 2011 measured via

the fixed Internet

Survey conducted week of January 30, 2012 (n=1083)

Consumer Measurements:

– Site Visitation

– Online Buying

– Attitudes and Sentiment

– Demographic Segments

– Mobile e-commerce

Retailer Views:

– Large vs. Small Retailers

– Impact of Social Media

2 million person panel

360°View of Consumer Behavior Analysis Parameters

Web Visiting & Search Behavior Online

Advertising Exposure

Advertising Effectiveness

Demographics, Lifestyles & Attitudes

Media & Video Consumption

Transactions

Online & Offline

Buying

Mobile Internet Usage & Behavior

PANEL

3 © comScore, Inc. Proprietary and Confidential.

-10%

0%

10%

20%

30%

40%

50%

2005 - Q1

2005 - Q2

2005 - Q3

2005 - Q4

2006 - Q1

2006 - Q2

2006 - Q3

2006 - Q4

2007 - Q1

2007 - Q2

2007 - Q3

2007 - Q4

2008 - Q1

2008 - Q2

2008 - Q3

2008 - Q4

2009 - Q1

2009 - Q2

2009 - Q3

2009 - Q4

2010 - Q1

2010 - Q2

2010 - Q3

2010 - Q4

2011 - Q1

2011 - Q2

2011 - Q3

Validation of comScore Sales Data:

Comparison of comScore data to U.S. Department of Commerce

Quarterly U.S. e-Commerce Growth* vs. YA Source: comScore & U.S. Department of Commerce (DOC)

% G

row

th v

s. Y

A

Dept. of Commerce (DOC) comScore Estimate of DOC

Correlation: 0.96

*Note: To be consistent with DOC, comScore estimate excludes

travel and event tickets but includes auction fees and autos.

4 © comScore, Inc. Proprietary and Confidential.

State of the Economy

A Review of Key Macroeconomic Trends

5 © comScore, Inc. Proprietary and Confidential.

$42 $53 $67 $82 $102

$123 $130 $130 $142 $162

$30 $40

$51 $61

$69

$77 $84 $80

$85

$94

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

$72 $93

$117 $143

Retail

Travel

+26%

+33%

+26%

+28%

+20%

+24% +24%

+13%

$171 $200

+20%

+12%

+6%

+9%

Total e-Commerce spending continues to recover strongly from the

recession, posting a +12% gain Y/Y in 2011. Retail e-Commerce up 14%

$214

0%

-5%

$209

U.S. e-Commerce Dollar Sales Growth ($ Billions) Source: comScore e-Commerce Measurement

+10%

+6%

$228

+14%

+11%

$256

+29%

+26%

+22%

+19%

+17%

+7% -2%

+9%

+12%

6 © comScore, Inc. Proprietary and Confidential.

17%

23% 23%

19%

11%

13%

6% -3% 0% -1% -2%

3%

10%

9% 9%

11% 12% 14%

13%

14%

Q1 2007

Q2 2007

Q3 2007

Q4 2007

Q1 2008

Q2 2008

Q3 2008

Q4 2008

Q1 2009

Q2 2009

Q3 2009

Q4 2009

Q1 2010

Q2 2010

Q3 2010

Q4 2010

Q1 2011

Q2 2011

Q3 2011

Q4 2011

Channel shift accelerating: e-Commerce growth shows significant gains,

nearly triple the growth rate of total retail in Q4 2011

Quarterly e-Commerce Sales Growth vs. YA Source: comScore e-Commerce Measurement

Quarterly Retail & Food Services Sales Growth* vs. YA

Source: U.S. Department of Commerce (DOC)

*Note: The U.S. Department of Commerce calculation includes total

retail and food service sales, which also includes motor vehicles and

parts dealers.

4% 4% 3% 5%

4% 2%

1%

-8% -10% -9%

-7%

2%

6% 7%

5%

8%

7% 7% 7% 5%

Q1 2007

Q2 2007

Q3 2007

Q4 2007

Q1 2008

Q2 2008

Q3 2008

Q4 2008

Q1 2009

Q2 2009

Q3 2009

Q4 2009

Q1 2010

Q2 2010

Q3 2010

Q4 2010

Q1 2011

Q2 2011

Q3 2011

Q4 2011

When excluding autos, gas and

food/beverage, Q4 2011 retail growth

is up only +3% versus 2010

7 © comScore, Inc. Proprietary and Confidential.

4.3%

3.7% 4.0%

4.6%

5.1%

4.3% 4.5%

5.3%

5.9%

5.0%

5.3%

6.4% 6.7%

5.9%

6.3%

7.4% 7.3%

6.5% 6.6%

7.6% 7.7%

6.8% 6.9%

7.7% 8.1%

7.1% 7.1%

8.0%

8.6%

7.7% 7.6%

8.9%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

e-Commerce share of all consumer sales continues to grow, with

almost one in every ten discretionary dollars spent online

*Note: e-Commerce share is shown as a percent of DOC’s Total Retail Sales excluding Food

Service & Drinking, Food & Bev. Stores, Motor Vehicles & Parts, Gasoline Stations and Health &

Personal Care Stores.

e-Commerce Share of Corresponding Consumer Spending* Source: comScore for e-Commerce & U.S. Department of Commerce (DOC) for Retail

e-C

om

me

rce S

hare

e-Commerce share peaks in

colder seasons (Q4 & Q1)

8 © comScore, Inc. Proprietary and Confidential.

Q1 '08 Q2 '08 Q3 '08 Q4 '08 Q1 '09 Q2 '09 Q3 '09 Q4 '09 Q1 '10 Q2 '10 Q3 '10 Q4 '10 Q1 '11 Q2 '11 Q3 '11 Q4 '11

Overall e-Commerce dollar sales posted double-digit gains in every

quarter in 2011, reaching almost $50 billion in Q4

Bil

lio

ns

($

)

e-Commerce Dollar Sales ($ Billions) Source: comScore e-Commerce Measurement

+11% +13% +6% -3% 0% -1% -2% +3% +10% +9% +9% +11% +12% +14% +13% +14%

% Chg vs.YA

$31.2 $30.6 $30.3

$38.1

$31.0 $30.2 $29.6

$39.0

$33.9 $32.9 $32.1

$43.4

$38.0 $37.5 $36.3

$49.7

9 © comScore, Inc. Proprietary and Confidential.

$15.1

$12.4

$13.5

$12.1

$17.5

Q4 '10 Q1 '11 Q2 '11 Q3 '11 Q4 '11

+9% +7% +12% +15% +16% +6% +2% +8% +3% +9%

$10.0 $10.3 $9.4

$8.9

$12.2

Q4 '10 Q1 '11 Q2 '11 Q3 '11 Q4 '11

+26% +39% +28% +31% +22%

Consumers earning $100k+ showed double-digit e-commerce growth rates for the

third consecutive quarter, while the middle class also grew at the best rate in more

than a year

$50K - $99K

(43% of Total)

Under $50K

(23% of Total)

$100K or more

(34% of Total)

e-Commerce Sales by Income Segment ($ Billions)

Growth vs. YA Source: comScore e-Commerce Measurement

$18.3

$15.3 $14.6

$15.4

$20.0

Q4 '10 Q1 '11 Q2 '11 Q3 '11 Q4 '11

10 © comScore, Inc. Proprietary and Confidential.

Overall consumer sentiment has improved, with 54% stating the

economy is in „poor‟ condition (2nd lowest percentage since 2009)

Percent of Consumers Who View The Economy as Poor

Q. How would you rate economic conditions today? Source: comScore Surveys

77% 68% 66%

61% 61% 59% 62% 61% 52%

59% 60% 62% 60% 54%

Jan-09 Apr-09 Jul-09 Oct-09 Jan-10 Apr-10 Jul-10 Oct-10 Jan-11 Apr-11 Jul-11 Aug-11 Oct-11 Jan-12

11 © comScore, Inc. Proprietary and Confidential.

Consumer concern over unemployment dropped to 31% in January

Percent of Respondents Citing Their One Most Important Issue

46%

40% 42%

50%

42% 44% 45%

36%

27%

37% 38%

31% 28%

32% 32%

29%

33%

30%

29%

42%

54%

37% 37%

43%

15% 13% 13%

9% 10%

13%

9% 7% 7%

12% 12%

10% 8% 8% 8%

7% 9%

8%

10% 11%

7%

8% 9%

10%

Apr-09 Jul-09 Oct-09 Jan-10 Apr-10 Jul-10 Oct-10 Jan-11 Apr-11 Jul-11 Oct-11 Jan-12

Unemployment / Job Security

Rising Prices

Financial Markets

Real Estate / Home Values

Q. Based on your current situation, which one of the following economic conditions most concerns you? Source: comScore Surveys

12 © comScore, Inc. Proprietary and Confidential.

Retailer and Product Category Overview

13 © comScore, Inc. Proprietary and Confidential.

Most categories show strong growth in Q4 2011 versus Q4 2010

Q3 2011 e-Commerce Sales Growth vs. YA by Retail Category Source: comScore e-Commerce Measurement

Q4 growth rates of 15% or

higher

Q4 growth rates of 5% to 9%

Product Category Relative Chg

Growth Rate Q4

2011 vs. Q3 2011

Q4 2011

Growth

vs. YA

Digital Content and Subscriptions Very Strong

Jewelry & Watches Very Strong

Consumer Electronics (x PC Peripherals) Very Strong

Sport & Fitness Very Strong

Computers/Peripherals/PDAs Very Strong

Apparel & Accessories Very Strong

Event Tickets Strong

Flowers, Greetings & Misc. Gifts Strong

Books & Magazines Strong

Video Games, Consoles & Accessories Strong

Furniture, Appliances & Equipment Strong

Consumer Packaged Goods Strong

Office Supplies Moderate

Home & Garden Moderate

Q4 growth rates of 10-14%

14 © comScore, Inc. Proprietary and Confidential.

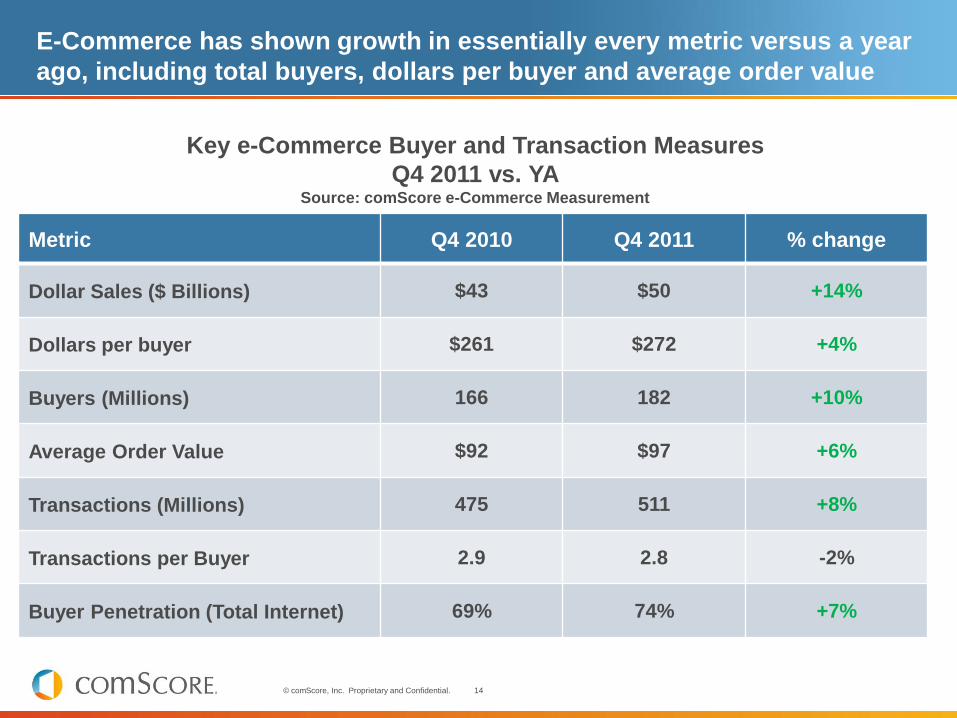

E-Commerce has shown growth in essentially every metric versus a year

ago, including total buyers, dollars per buyer and average order value

Metric Q4 2010 Q4 2011 % change

Dollar Sales ($ Billions) $43 $50 +14%

Dollars per buyer $261 $272 +4%

Buyers (Millions) 166 182 +10%

Average Order Value $92 $97 +6%

Transactions (Millions) 475 511 +8%

Transactions per Buyer 2.9 2.8 -2%

Buyer Penetration (Total Internet) 69% 74% +7%

Key e-Commerce Buyer and Transaction Measures

Q4 2011 vs. YA Source: comScore e-Commerce Measurement

15 © comScore, Inc. Proprietary and Confidential.

Compared to 2010, smaller retailers gained share of quarterly e-

Commerce sales versus the top-25 retailers

67.7% 69.9% 68.8% 67.7% 66.4% 67.9% 67.6%

32.3% 30.1% 31.2% 32.3% 33.6% 32.1% 32.4%

Q2-2010 Q3-2010 Q4-2010 Q1-2011 Q2-2011 Q3-2011 Q4-2011

All Other Retailers

Top 25 Retailers

Top-25 Retailers vs. All Other Retailers: Share of Quarterly

U.S. e-Commerce Sales Source: comScore e-Commerce Measurement

16 © comScore, Inc. Proprietary and Confidential.

Over half of all online transactions included free shipping in Q4 2011,

the highest level ever seen

42% 44% 39% 40% 41% 49% 47% 43% 40%

52%

58% 56% 61% 60% 59% 51% 53% 57% 60%

48%

Q3 09 Q4 09 Q1 '10 Q2 '10 Q3 '10 Q4 '10 Q1 '11 Q2 '11 Q3 '11 Q4 '11

% Transactions with Free Shipping

% Transactions with Paid Shipping

Percentage of e-Commerce Transactions with

Free Shipping Source: comScore e-Commerce Measurement

54% of consumers stated in a recent survey* that if they reached the end of an e-Commerce

transaction and free shipping was not offered, they would cancel their purchase

*comScore survey – Jan 2012

17 © comScore, Inc. Proprietary and Confidential.

Amazon sites continue to break their own records, reaching 111

Million UVs in Q4, a 31% increase from 2010

Avg. Monthly UVs (MM) on Select Retail Sites in Q4 2011 Source: comScore Media Metrix U.S. Data

+31% vs. Q4 2010

+11% vs. Q3 2011

16.5

17.3

17.8

25.6

29.7

30.7

34.9

50.6

53.2

111.5

Macy's Inc.

JCPenney Sites

Sears.com

Hewlett Packard

Netflix.com

Best Buy Sites

Target Corporation

Apple.com

Wal-Mart

Amazon Sites

18 © comScore, Inc. Proprietary and Confidential.

The overall popularity of flash-sale sites continues to grow, with

several sites showing triple-digit growth versus a year ago

U.S. Unique Visitors (000) to Leading U.S. Flash Sales Sites Source: comScore Media Metrix, U.S., December 2011

Kids clothing site Totsy.com has exploded on the Flash Sale scene,

reaching 520,000 UVs in Dec-2011, vs. just 6,000 in Dec-2010

+62%

+115%

+153%

+30%

N/A

+40%

+206%

+36%

+8,306%

N/A

Y/Y Growth

487

520

590

716

925

1,163

1,186

1,655

1,701

2,428

EBay Fashion Vault

Totsy.com

RueLaLa.com

OneKingsLane.com

Ideeli.com

MyHabit.com

Gilt Groupe

Zulily.com

HauteLook.com

Woot.com

19 © comScore, Inc. Proprietary and Confidential.

Online Retail Advertising in 2011

20 © comScore, Inc. Proprietary and Confidential.

Internet advertising spending surged in 2011, reaching $7.9 Billion in Q3,

up 22% vs YA -- a growth rate about 6X faster than all media spending

$-

$1

$2

$3

$4

$5

$6

$7

$8

Q3 2011 $7.9 B

+22% vs YA

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Source: IAB Internet Advertising Revenue Report, Q1 2000 - Q3 2011 IAB &

PricewaterhouseCoopers

Quarterly Revenue Trend ($ Billions)

2000 - 2011

$0

21 © comScore, Inc. Proprietary and Confidential.

Netflix and eBay were the top retail advertisers in 2011, serving 37

billion and 28 billion total impressions, respectively

37.0

28.0

11.2

9.8

8.2

6.2

5.9

5.1

5.0

4.8

4.5

Netflix

eBay

QuiBids

JustFabulous

Amazon.com

Sears

Apple Inc.

Wal-Mart

ShoeDazzle.com

Target

RadioShack

Total Advertising Impressions (Billions) Served Across the Internet in 2011 – Top Retailers Source: comScore Ad Metrix

22 © comScore, Inc. Proprietary and Confidential.

0

500

1,000

1,500

2,000

2,500

3,000

Amazon.com

Walmart.com

Ad impressions delivered on Amazon.com (not including Amazon‟s

own ads) are up 81% versus a year ago

Impressions Delivered (in Millions) & Selected Leading Creatives on Amazon & Walmart Source: comScore Ad Metrix, U.S., Jul-2010 to Dec-2011

+81% vs. Dec ‟10

+12% vs. Nov „11

Amazon.com

Walmart.com

23 © comScore, Inc. Proprietary and Confidential.

$994

$9,905

$1,263

$11,550

Online Offline

Unexposed Exposed

Dollar Sales Lift Among Households

Exposed to Online Advertising

% Lift: 17%

% Lift: 27%

Despite click rates of only 0.1%, comScore research has shown that

display ads can lift retailer sales – both online and offline

Source: “Whither the Click?” 139 comScore studies in the

June 2009 Journal of Advertising Research

Exposure to display ads

doesn‟t just impact online

sales – it lifts in-store

sales as well

The absolute dollar lift

in offline sales is 5x higher

than the lift in e-commerce

sales

The click is misleading

as a measure of campaign

effectiveness

Conclusions

24 © comScore, Inc. Proprietary and Confidential.

Making Measurement Make Sense (3MS) Mission:

Reduce costs of doing business due to

complexity of digital advertising ecosystem

„Single Tag‟ solution to reduce complexity

Improve reporting of ad exposure

Bolster confidence that ads delivered are

actually visible

25 © comScore, Inc. Proprietary and Confidential.

Billions of impressions are being delivered – how can retailers ensure

the right consumers are seeing the messaging?

26 © comScore, Inc. Proprietary and Confidential.

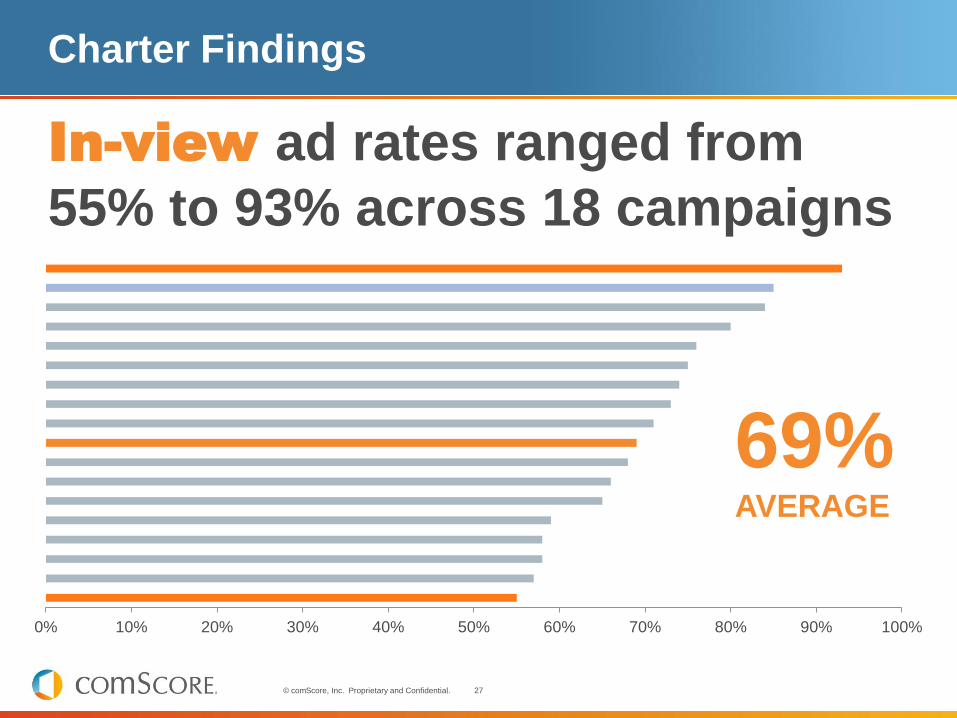

vCE Charter Study

18 campaigns

2 billion impressions

400k sites

Allstate

27 © comScore, Inc. Proprietary and Confidential.

Charter Findings

In-view ad rates ranged from

55% to 93% across 18 campaigns

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

69% AVERAGE

28 © comScore, Inc. Proprietary and Confidential.

Mobile Retail Trends

29 © comScore, Inc. Proprietary and Confidential.

2011: The Rise of Mobile & Tablet Commerce

9% 8%

6% 5%

3% 3%

2%

Q4 2011

Q3 2011

Q2 2011

Q1 2011

Q4 2010

Q3 2010

Q2 2010

Percentage of Total e-Commerce Dollars Spent via Mobile or Tablet Device Source: comScore Mobile Measurements

Spike in percentage of

e-commerce sales via

mobile coincides with

surge in tablet ownership

30 © comScore, Inc. Proprietary and Confidential.

6.5 million new smartphones were activated in Dec 2011, the highest month

of activations on record; almost 100 million people now own smartphones

+1.1 +1.3 +1.3

+1.9

+3.3

+2.7

+1.3 +1.3 +1.0

+2.1 +2.3 +2.3

+2.9

+2.0

+0.7

+1.8

+2.7

+3.6

+2.9

+2.1 +2.2

+1.6

+3.8

+2.2

+3.1

+2.5

+1.4

+6.5

+0.0

+1.0

+2.0

+3.0

+4.0

+5.0

+6.0

+7.0

0

20,000

40,000

60,000

80,000

100,000

120,000

New Smartphone Acquisitions (In Millions)

Total Smartphone Subscriber Base (In Thousands)

Acquisition Trend for Smartphone Subscriber Base and

Total Smartphone Subscriber Base Source: comScore MobiLens, 3 Mo. Avg. Sep-2009 to Dec-2011

31 © comScore, Inc. Proprietary and Confidential.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Classifieds Online Retail

Real Estate Listings

E-Payments Auction Sites

Credit Cards

Shopping Guides

Bank Accounts

Restaurant Info

Travel Service

Dec-2010 Dec-2011

Mobile retail activities are surging as smartphone adoption approaches 100

million people in the U.S.

Retail Content Categories Are Among the Fastest Growing for Mobile

+116% +123%

+115%

+112% +104% +96%

+93%

+76%

+89%

+69%

Content Categories Consumed by Mobile Phone Owners (000) & Growth vs. YA Source: comScore Mobilens, Dec-2011, U.S.

32 © comScore, Inc. Proprietary and Confidential.

1 in 3 smartphone owners have used a phone to find a store location,

while about 20% compared product prices or features

33%

21% 20% 19% 17% 17%

16%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Found store location

Compared product prices

Researched product features

Found coupons or

deals

Made shopping lists

Checked product

availability

Used deal-a-day

To

tal A

ud

ien

ce

(00

0)

Retail Activities by Smartphone Users (000) and % of Audience Source: comScore Mobilens, Dec-2011

33 © comScore, Inc. Proprietary and Confidential.

While in a brick-and-mortar retail store, 12% of smartphone owners

compared prices and 10% searched for information on product features

Activities Performed on Mobile While in a Retail Store, % of Smartphone Audience Source: comScore Mobilens, Dec-2011, U.S.

22% 21%

18% 17%

13% 12%

10% 9%

6%

Took picture of a product

Texted or called

friends/family about a product

Scanned a product barcode

Sent picture of product to

family/friends

Found store location

Compared product prices

Found coupons or

deals

Researched product features

Checked product

availability

34 © comScore, Inc. Proprietary and Confidential.

2011 Holiday Shopping Season

e-Commerce Wrap-Up and Key Findings

35 © comScore, Inc. Proprietary and Confidential.

$19.6

$24.6

$29.2 $28.0

$29.1

$32.6

$37.2

+26%

+19%

-4%

+4%

+12% +15%**

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

$35.0

$40.0

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Holiday Season $ in Billions Y/Y Growth Rates

The 2011 U.S. e-Commerce holiday season surpassed all previous

years in sales and grew 15% versus year ago

* Holiday Season includes November and December

**Percentage change includes seasonal adjustment to account for unequal

number of weekdays and weekend days in 2010 and 2011

Holiday Season* Retail e-Commerce Sales ($ Billions)

Growth vs. YA Source: comScore e-Commerce Measurement

2005 2006 2007 2008 2009 2010 2011

36 © comScore, Inc. Proprietary and Confidential.

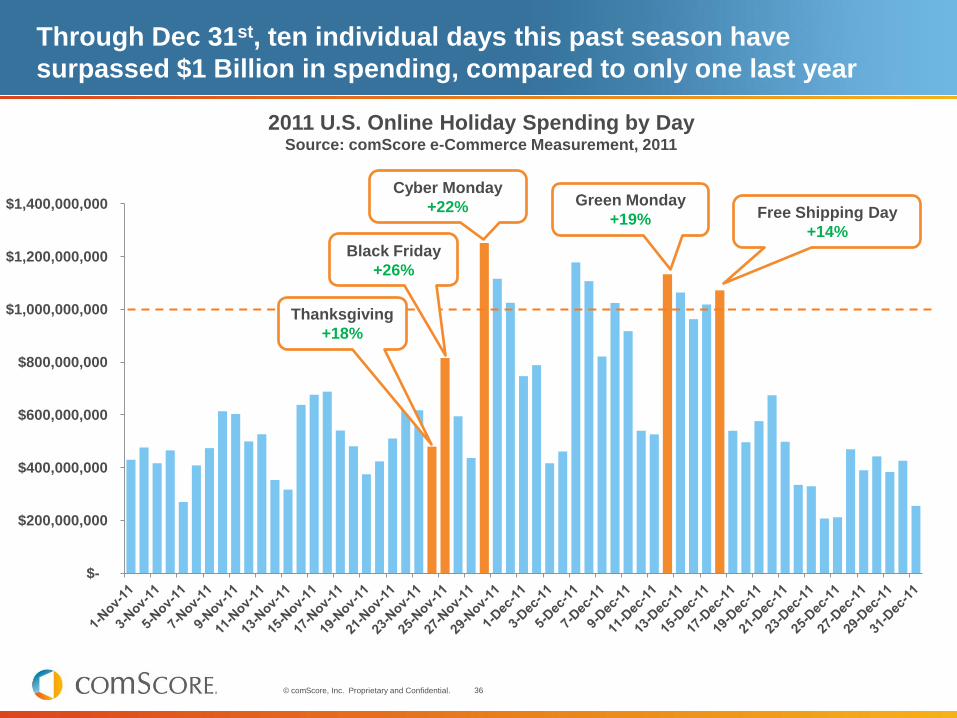

Through Dec 31st, ten individual days this past season have

surpassed $1 Billion in spending, compared to only one last year

$-

$200,000,000

$400,000,000

$600,000,000

$800,000,000

$1,000,000,000

$1,200,000,000

$1,400,000,000

2011 U.S. Online Holiday Spending by Day Source: comScore e-Commerce Measurement, 2011

Black Friday

+26%

Cyber Monday

+22% Green Monday

+19% Free Shipping Day

+14%

Thanksgiving

+18%

37 © comScore, Inc. Proprietary and Confidential.

$484

$608

$733

$846 $887

$1,028

$1,251

2005 2006 2007 2008 2009 2010 2011

For the second consecutive year, Cyber Monday was the highest

spending day throughout the holiday season

Cyber Monday U.S. Online Spending in

Millions (% growth vs. YA) Source: comScore E-commerce Measurement, 2005-2011

+16%

+5% +15%

+21%

+26%

+22%

8

12

9

3

2

1 1

0

2

4

6

8

10

12

14

2005 2006 2007 2008 2009 2010 2011

Sp

en

din

g D

ay R

an

k

Cyber Monday - Spending Day Rank

Cyber Monday - Spending Day Rank Source: comScore E-commerce Measurement. 2005-2011

38 © comScore, Inc. Proprietary and Confidential.

Cyber Monday 2011 activity saw a relatively higher percentage of sales occur

in the early morning as consumers sought out early deals and in the evening

hours as retailers continued to push promotions throughout the day

3% 12%

29%

32%

44% 22%

24% 34%

2010 2011

5pm - 9pm

1pm - 5pm

9am - 1pm

Before 9am

Cyber Monday Spending by Time of Day Source: comScore, Inc.

Time of Day:

39 © comScore, Inc. Proprietary and Confidential.

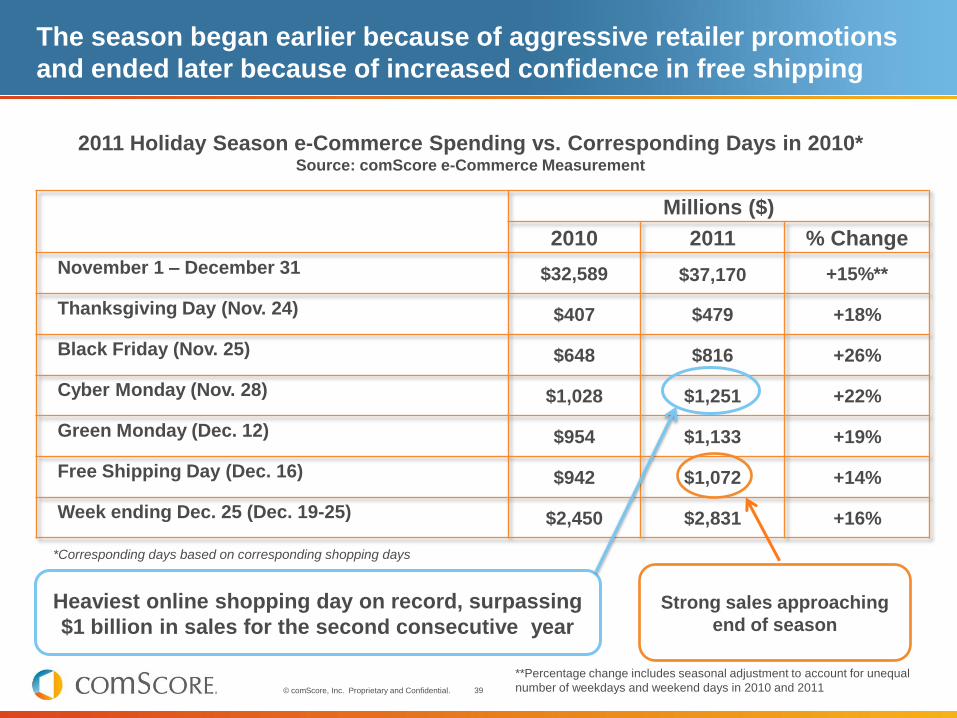

The season began earlier because of aggressive retailer promotions

and ended later because of increased confidence in free shipping

Millions ($)

2010 2011 % Change

November 1 – December 31 $32,589 $37,170 +15%**

Thanksgiving Day (Nov. 24) $407 $479 +18%

Black Friday (Nov. 25) $648 $816 +26%

Cyber Monday (Nov. 28) $1,028 $1,251 +22%

Green Monday (Dec. 12) $954 $1,133 +19%

Free Shipping Day (Dec. 16) $942 $1,072 +14%

Week ending Dec. 25 (Dec. 19-25) $2,450 $2,831 +16%

2011 Holiday Season e-Commerce Spending vs. Corresponding Days in 2010* Source: comScore e-Commerce Measurement

*Corresponding days based on corresponding shopping days

Heaviest online shopping day on record, surpassing

$1 billion in sales for the second consecutive year

Strong sales approaching

end of season

**Percentage change includes seasonal adjustment to account for unequal

number of weekdays and weekend days in 2010 and 2011

40 © comScore, Inc. Proprietary and Confidential.

41%

47%

50%

46% 44% 45%

40%

44%

41% 42%

45%

50%

55% 51%

52%

52% 54%

50%

52% 51%

56%

64%

59%

53%

59% 56% 56%

30%

35%

40%

45%

50%

55%

60%

65%

70% 2009 2010 2011

Percentage of E-commerce Transactions with Free Shipping Source: comScore e-Commerce Measurement

Free shipping in the week leading up to Cyber Monday 2011 reached

a record 64% of total transactions

Average Order Value on free shipping purchases was $95 during the 2011

holiday season. For non-free shipping purchases, it was $87.

41 © comScore, Inc. Proprietary and Confidential.

Nearly 1 in 4 consumers purchased a gift via a deal-of-the-day site

this holiday season

8%

13%

11% 10%

13% 12%

5%

12%

10%

Yes, I purchased gifts via deal of the day vouchers I had already purchased but not

used

Yes, I purchased a new deal this holiday season & used it to buy a gift

Yes, I purchased a deal of the day as a gift (i.e. gave the voucher itself as a gift)

All consumers Men Women

Daily Deals As Holiday Gifts

Q. When thinking of this past holiday season, did you purchase any gifts via deal-of-the-day sites?

(Please select all that apply) Source: comScore Survey – January 2012

Overall, 27% of men and 21% of women bought gifts via

deal-of-the-day sites this season

42 © comScore, Inc. Proprietary and Confidential.

Promotions targeted to Fans can significantly expand the viral impact

of social media to Friends of Fans

0.31 0.34 0.50 0.45

0.67

0.92

1.76

1.53

Amazon Best Buy Target Walmart

Week Ending Oct. 19 Week Ending Nov. 30

2011 Holiday Retail Promotion Analysis Ratio of Friends of Fans Reached to Fans Reached for Leading U.S. Retailers

Source: comScore Social Essentials, U.S., November 2011

Viral Lift from

Promotions

2.2x

2.7x

3.5x 3.4x

43 © comScore, Inc. Proprietary and Confidential.

For most retailers, a significantly higher percentage of Fans &

Friends of Fans visited the retailer‟s website

27%

8% 9% 14%

36%

13% 12%

22%

64%

18% 12%

21%

Amazon Best Buy Target Walmart

Total Internet Friend of Fan Fan

2011 Holiday Retail Promotion Impact Analysis: Week Ending Nov. 30 Percentage of Brand-Exposed Fans & Friends of Fans Who Visited Retailer Website

Source: comScore Social Essentials, U.S., November 2011

Fans of Amazon were more than twice

as likely to have visited the brand’s site

than the general Internet user

44 © comScore, Inc. Proprietary and Confidential.

Key Takeaways

45 © comScore, Inc. Proprietary and Confidential.

Key Takeaways

Quarterly e-Commerce sales have increased by double digits Y/Y for five

straight quarters

– Online growth now nearly triple total retail sales, which means that $1 in every $10 of

discretionary spending will soon be spent online

– Channel shift to online has accelerated in 2011

Overall consumer perception of the economy improving, albeit slowly, but

remains negative with unemployment and high prices top concerns.

Smartphone adoption continues to explode: 6.5 million new phones activated in

Dec 2011, and overall 98 million people now use smartphones

– Smartphones & tablets used to buy and research competitive price / product features

while in-store, now accounting for 9% of Q4 dollars spent online

Strong holiday e-commerce sales exceeded $37 billion, up 15% vs YA

Free shipping growing in importance, far surpassing 50% of all transactions in

holiday season

– Has it become a cost of doing business?

– Negative impact on retailer profit margins?

46 © comScore, Inc. Proprietary and Confidential.

QUESTIONS?

Please contact us at [email protected] if

you have any additional questions or comments.

Thank You!

Note: A copy of this presentation will be sent to all attendees within 24

hours of today‟s webinar.