state of the audit profession virginia accounting & auditing conference presented by chuck...

TRANSCRIPT

State of the State of the Audit Audit

ProfessionProfession

Virginia Accounting & Auditing Virginia Accounting & Auditing ConferenceConference

Presented byPresented by

Chuck Landes, CPAChuck Landes, CPA

AgendaAgenda

► How did we get to where we are today?How did we get to where we are today?► The provisions and implications of The provisions and implications of

Sarbanes-OxleySarbanes-Oxley► The cascade effect – what’s the next The cascade effect – what’s the next

front?front?► Honoring our heritage and moving Honoring our heritage and moving

forwardforward► Overview of significant assurance Overview of significant assurance

initiativesinitiatives

What went wrong – corporate What went wrong – corporate culture and reporting modelculture and reporting model

►Simple greed or arroganceSimple greed or arrogance►Market pressure on short term earnings Market pressure on short term earnings ►Lack of transparency or timely Lack of transparency or timely

disclosures in the reporting modeldisclosures in the reporting model►Lack of mandated disclosures on Lack of mandated disclosures on

management’s accounting policiesmanagement’s accounting policies►Too many rules leading to connect the Too many rules leading to connect the

dots accounting and auditingdots accounting and auditing

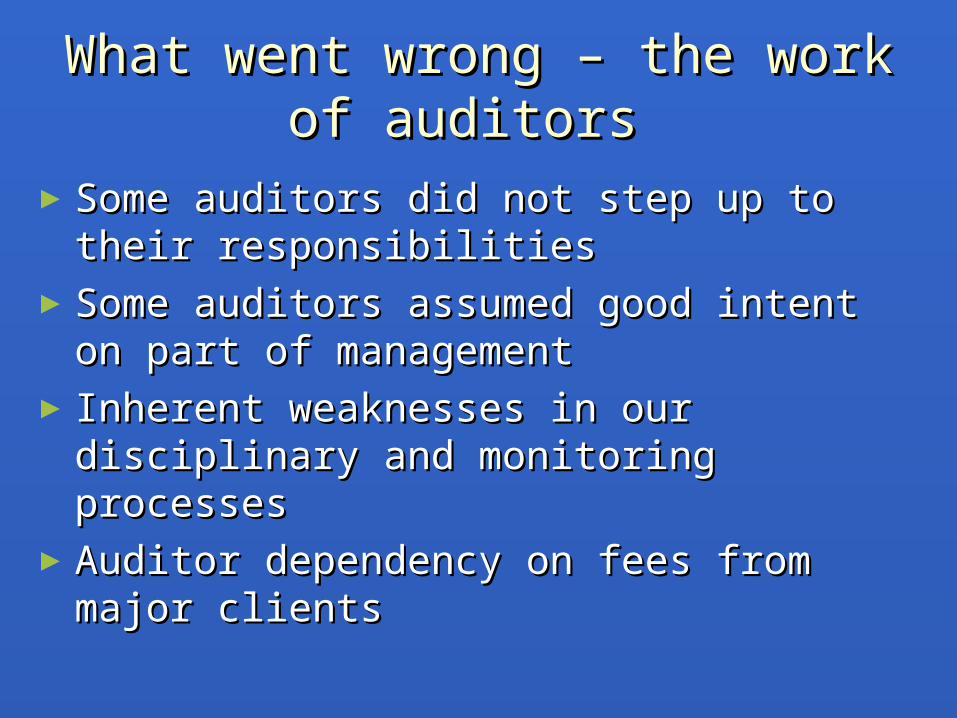

What went wrong – the work of What went wrong – the work of auditors auditors

►Some auditors did not step up to their Some auditors did not step up to their responsibilitiesresponsibilities

►Some auditors assumed good intent on Some auditors assumed good intent on part of management part of management

► Inherent weaknesses in our Inherent weaknesses in our disciplinary and monitoring processesdisciplinary and monitoring processes

►Auditor dependency on fees from Auditor dependency on fees from major clientsmajor clients

What was the What was the response of response of Congress?Congress?

The Sarbanes - Oxley Act:The Sarbanes - Oxley Act:Oversight BoardOversight Board

►New Public Company Accounting New Public Company Accounting Oversight Board (PCAOB)Oversight Board (PCAOB)

►Requires 2 CPAs (but only 2) to serveRequires 2 CPAs (but only 2) to serve►Power to set auditing rules, inspect Power to set auditing rules, inspect

firms and discipline wrongdoersfirms and discipline wrongdoers►Funding from accounting firms and Funding from accounting firms and

registrantsregistrants

The Sarbanes - Oxley Act:The Sarbanes - Oxley Act:Standards SettingStandards Setting

►PCAOB has authority to “adopt, PCAOB has authority to “adopt, amend, modify, repeal or reject” amend, modify, repeal or reject” standardsstandards

► Includes provisions for SEC oversight, Includes provisions for SEC oversight, governance and funding of FASBgovernance and funding of FASB

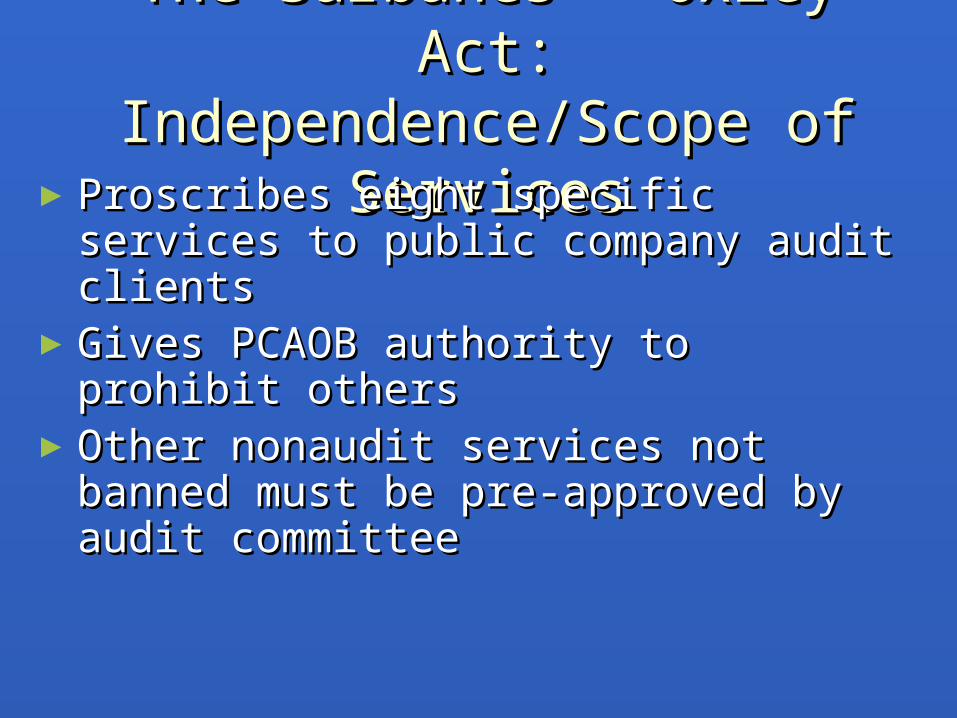

The Sarbanes - Oxley Act:The Sarbanes - Oxley Act:Independence/Scope of Independence/Scope of

ServicesServices►Proscribes eight specific services to Proscribes eight specific services to

public company audit clientspublic company audit clients►Gives PCAOB authority to prohibit Gives PCAOB authority to prohibit

othersothers►Other nonaudit services not banned Other nonaudit services not banned

must be pre-approved by audit must be pre-approved by audit committeecommittee

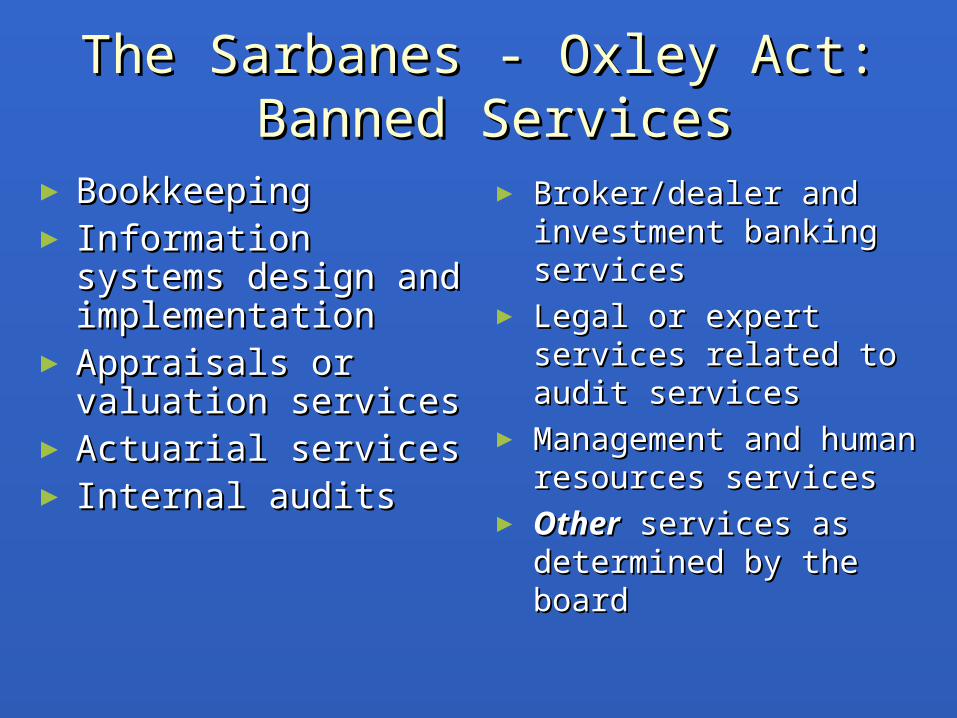

The Sarbanes - Oxley Act:The Sarbanes - Oxley Act: Banned Services Banned Services

► BookkeepingBookkeeping► Information systems Information systems

design and design and implementationimplementation

► Appraisals or Appraisals or valuation servicesvaluation services

► Actuarial servicesActuarial services► Internal auditsInternal audits

► Broker/dealer and Broker/dealer and investment banking investment banking servicesservices

► Legal or expert services Legal or expert services related to audit servicesrelated to audit services

► Management and Management and human resources human resources servicesservices

► OtherOther services as services as determined by the determined by the board board

The Sarbanes - Oxley Act:The Sarbanes - Oxley Act:Liability ConcernsLiability Concerns

►Statute of limitations extended to 5 Statute of limitations extended to 5 years from occurrence or 2 from years from occurrence or 2 from discoverydiscovery

►No specific language on non-preclusive No specific language on non-preclusive effecteffect

The Sarbanes - Oxley Act:The Sarbanes - Oxley Act:Report on Internal ControlsReport on Internal Controls

►Requires auditor report on internal Requires auditor report on internal controls assertionscontrols assertions

►Must be part of audit - not separate Must be part of audit - not separate engagementengagement

The Sarbanes - Oxley Act:The Sarbanes - Oxley Act:Corporate GovernanceCorporate Governance

►Mandates audit committee oversight Mandates audit committee oversight of auditsof audits

►Requires CEO/CFO certification of Requires CEO/CFO certification of reportsreports

►Prison terms of up to 10 years for Prison terms of up to 10 years for senior executivessenior executives

The Sarbanes - Oxley Act:The Sarbanes - Oxley Act:Workpaper RetentionWorkpaper Retention

►Auditors to retain documents in Auditors to retain documents in support of report for 7 years.support of report for 7 years.

►5 yr retention requirement under 5 yr retention requirement under “criminal fraud accountability”“criminal fraud accountability”

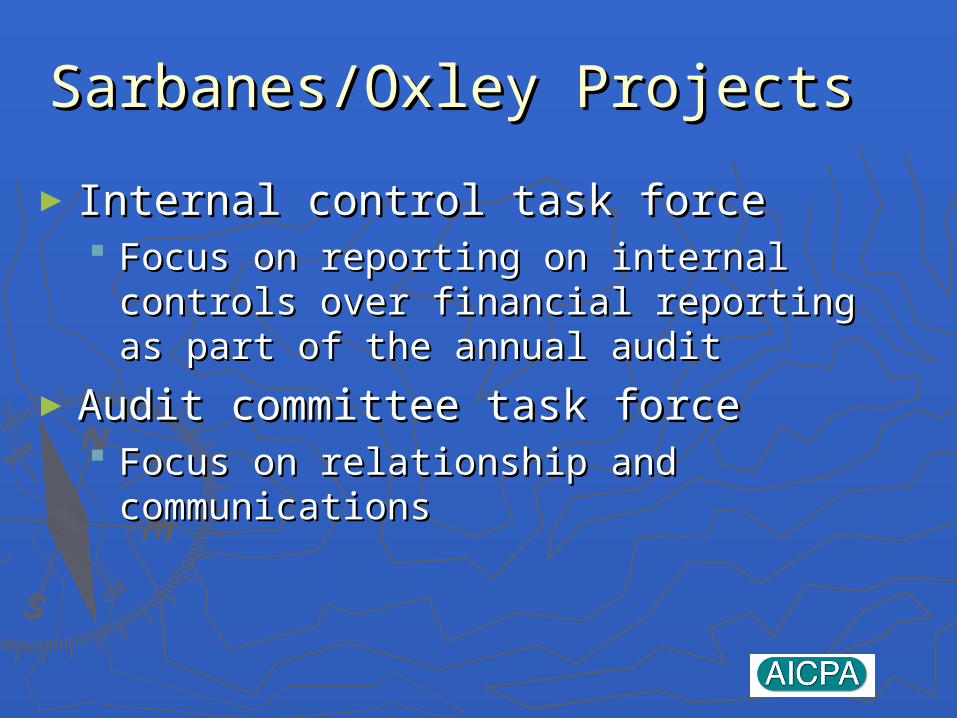

Sarbanes/Oxley ProjectsSarbanes/Oxley Projects

► Internal control task forceInternal control task force Focus on reporting on internal controls Focus on reporting on internal controls

over financial reporting as part of the over financial reporting as part of the annual auditannual audit

►Audit committee task forceAudit committee task force Focus on relationship and Focus on relationship and

communicationscommunications

Sarbanes/Oxley ProjectsSarbanes/Oxley Projects

►Omnibus task forceOmnibus task force Documentation retentionDocumentation retention Concurring partner reviewConcurring partner review Foreign affiliate issuesForeign affiliate issues Representation and attorney letter Representation and attorney letter

amendmentsamendments►Q.C. Task ForceQ.C. Task Force

Focus on inspection/monitoring guidanceFocus on inspection/monitoring guidance Audit partner rotationAudit partner rotation Objectivity issuesObjectivity issues

Possible Cascade at Federal Possible Cascade at Federal LevelLevel

►DOL rules for ERISA AuditsDOL rules for ERISA Audits►Banking Regulators Banking Regulators ►Future Action from the GAOFuture Action from the GAO►Public Interest Entity – A concept that Public Interest Entity – A concept that

may be comingmay be coming

Senate’s Attempt to Address Senate’s Attempt to Address State IssueState Issue

►The bill says that state regulators:The bill says that state regulators: “ “Should make an independent Should make an independent

determination of the proper standards determination of the proper standards applicable” in supervising nonregistered applicable” in supervising nonregistered accounting firms.accounting firms.

►Standards applied by the Board Standards applied by the Board “should not be presumed to be “should not be presumed to be applicable” for small and medium applicable” for small and medium sized firmssized firms

Overview of the Potential Overview of the Potential ImpactImpact

►New rules New rules couldcould require mandatory require mandatory rotation of rotation of allall partners on audit partners on audit engagements.engagements.

►New auditor responsibility for “testing” New auditor responsibility for “testing” issuers’ compliance with laws and issuers’ compliance with laws and reporting on “potential” violations.reporting on “potential” violations.

►The new Board The new Board couldcould have the authority to have the authority to enforce securities laws, duplicating SEC’s enforce securities laws, duplicating SEC’s powers.powers.

►State legislative/regulatory proposals State legislative/regulatory proposals couldcould “pile on” and/or conflict with Federal laws. “pile on” and/or conflict with Federal laws.

Honoring our Honoring our Heritage and Moving Heritage and Moving

Forward…..Forward…..

A Revitalized Accounting A Revitalized Accounting CultureCulture

►What is needed is not just legislation What is needed is not just legislation but a revitalized accounting culturebut a revitalized accounting culture

►Build upon the profession’s Build upon the profession’s traditional valuestraditional values A rigorous commitment to integrityA rigorous commitment to integrity A passion for getting it rightA passion for getting it right A commitment to rules and a zeal for A commitment to rules and a zeal for

applying themapplying them Zero tolerance for those who break Zero tolerance for those who break

themthem

Getting the Right AnswerGetting the Right Answer

►We are at a serious juncture in the history of We are at a serious juncture in the history of our financial markets and our professionour financial markets and our profession

► Anyone who deceives investors must be held Anyone who deceives investors must be held accountableaccountable

► Regulators should have all the resources they Regulators should have all the resources they need to police the capital markets and enforce need to police the capital markets and enforce the lawthe law

► Investors must have information that is Investors must have information that is accurate, clear, timely and relevantaccurate, clear, timely and relevant

► The reputation of the CPA profession must be The reputation of the CPA profession must be restored and our proud heritage honoredrestored and our proud heritage honored

Honoring our heritage and Honoring our heritage and moving forwardmoving forward

►We need to reaffirm our basic We need to reaffirm our basic commitment to professionalismcommitment to professionalism

►Auditors must be willing to say Auditors must be willing to say NONO Every day, auditors everywhere are telling Every day, auditors everywhere are telling

a corporate exec what must be disclosed, a corporate exec what must be disclosed, why a transaction can’t be treated in a why a transaction can’t be treated in a certain fashion and why certain activity certain fashion and why certain activity must be reflected on the balance sheetmust be reflected on the balance sheet

““Trust, but verify,”Trust, but verify,” this is the true spirit of this is the true spirit of the professionthe profession

What saying NO meansWhat saying NO means

►Rejecting unsound corporate Rejecting unsound corporate accounting practicesaccounting practices

►Reducing the risk of deceit and fraud Reducing the risk of deceit and fraud through diligent inquirythrough diligent inquiry

►Ensuring that audited statements are Ensuring that audited statements are not just accurate, but illuminatingnot just accurate, but illuminating

►Questioning management, challenging Questioning management, challenging managementmanagement

►When justified – rejecting When justified – rejecting management’s accounting decisionsmanagement’s accounting decisions

Overview of Other Overview of Other Significant Significant

Professional Professional DevelopmentsDevelopments

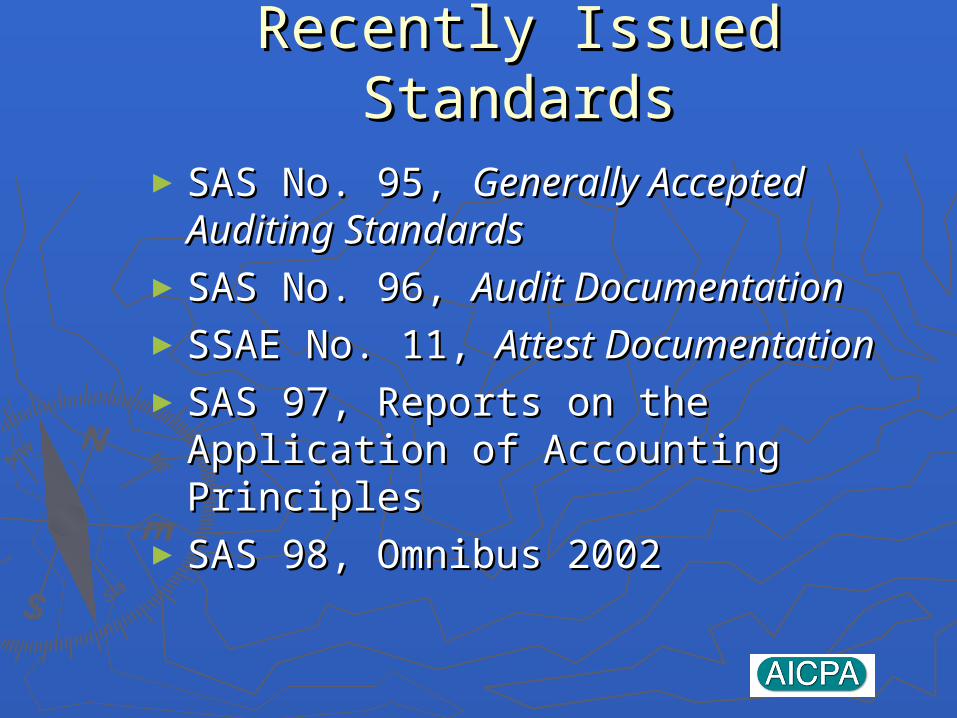

Recently Issued StandardsRecently Issued Standards

►SAS No. 95, SAS No. 95, Generally Accepted Generally Accepted Auditing StandardsAuditing Standards

►SAS No. 96, SAS No. 96, Audit DocumentationAudit Documentation►SSAE No. 11, SSAE No. 11, Attest DocumentationAttest Documentation►SAS 97, Reports on the Application SAS 97, Reports on the Application

of Accounting Principlesof Accounting Principles►SAS 98, Omnibus 2002SAS 98, Omnibus 2002

The ASB’s Current AgendaThe ASB’s Current Agenda

►FraudFraud►Risk AssessmentsRisk Assessments►Fair ValueFair Value►SAS No. 71(Quarterly Reviews of SAS No. 71(Quarterly Reviews of

SEC Entities)SEC Entities)► Joint Task Force on Quality ControlJoint Task Force on Quality Control►Sarbanes/Oxley related projectsSarbanes/Oxley related projects►Horizons IIHorizons II

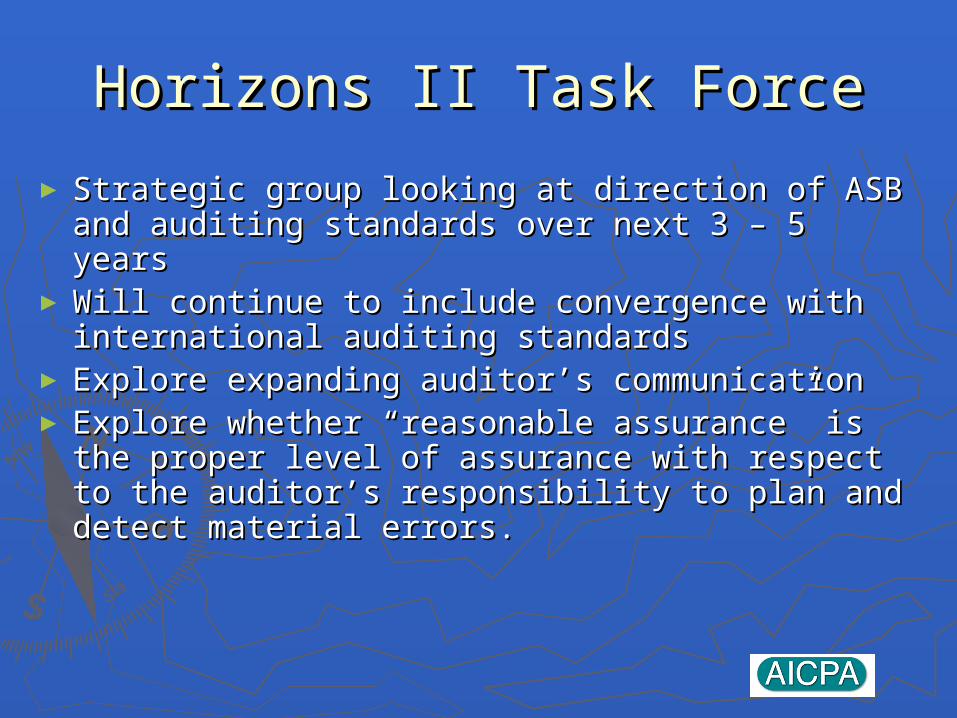

Horizons II Task ForceHorizons II Task Force

► Strategic group looking at direction of ASB Strategic group looking at direction of ASB and auditing standards over next 3 – 5 yearsand auditing standards over next 3 – 5 years

►Will continue to include convergence with Will continue to include convergence with international auditing standardsinternational auditing standards

► Explore expanding auditor’s communicationExplore expanding auditor’s communication► Explore whether “reasonable assurance” is Explore whether “reasonable assurance” is

the proper level of assurance with respect to the proper level of assurance with respect to the auditor’s responsibility to plan and detect the auditor’s responsibility to plan and detect material errors.material errors.

Where do we go from Where do we go from here?here?

Working with Corporate Working with Corporate AmericaAmerica

►AICPA to convene anti-fraud summit AICPA to convene anti-fraud summit with corporate leaders, accountants with corporate leaders, accountants and market professionalsand market professionals

►Will partner with corporations to Will partner with corporations to design and establish anti-fraud design and establish anti-fraud controls and programs.controls and programs.

►Will created enhanced attestation Will created enhanced attestation standards for CPAs to report on standards for CPAs to report on corporate anti-fraud programscorporate anti-fraud programs

ResearchResearch

►AICPA to sponsor academic research AICPA to sponsor academic research into the who, what, when, where & into the who, what, when, where & why of fraudwhy of fraud

►AICPA will establish an Institute for AICPA will establish an Institute for Fraud Studies with the University of Fraud Studies with the University of Texas and Association of Certified Texas and Association of Certified Fraud ExaminersFraud Examiners

Education & TrainingEducation & Training

►AICPA will develop training programs AICPA will develop training programs to prevent fraudto prevent fraud

►AICPA to work with academia on anti-AICPA to work with academia on anti-fraud curricula and materialsfraud curricula and materials

►AICPA calling for members to more AICPA calling for members to more anti-fraud CPEanti-fraud CPE

►AICPA urges stock exchanges to AICPA urges stock exchanges to mandate anti-fraud education for mandate anti-fraud education for corporate managers and directorscorporate managers and directors

Advancing Financial Advancing Financial ReportingReporting

► AICPA to initiate a dialogue on differentiating AICPA to initiate a dialogue on differentiating reporting needs of private vs. public companiesreporting needs of private vs. public companies

►Will work with FASB on more timely and better Will work with FASB on more timely and better quality reporting – particularly for off balance quality reporting – particularly for off balance sheet, intangibles & liquiditysheet, intangibles & liquidity

► AICPA is co-sponsoring Value Measurement & AICPA is co-sponsoring Value Measurement & Reporting CollaborativeReporting Collaborative

► AICPA supports more disclosure of accounting AICPA supports more disclosure of accounting policies and estimates and reporting in policies and estimates and reporting in Management’s Discussion and AnalysisManagement’s Discussion and Analysis

Corporate GovernanceCorporate Governance

►AICPA calls for revision of auditing AICPA calls for revision of auditing standards to provide public notice of standards to provide public notice of internal control weaknessesinternal control weaknesses

►Reportable conditions to include: Reportable conditions to include: One person as Chair and as CEOOne person as Chair and as CEO Audit committee that is not fulfilling its Audit committee that is not fulfilling its

mission.mission. It may include lack of mandatory anti-fraud It may include lack of mandatory anti-fraud

education, or lack of a Code of Conducteducation, or lack of a Code of Conduct

Conclusion -- Moving ForwardConclusion -- Moving Forward

►Core values and traditional areas.Core values and traditional areas.►Building on what we do best and what Building on what we do best and what

the public needs us to do.the public needs us to do.►Wrestle with such key issues as Wrestle with such key issues as

reporting measures, transparency, reporting measures, transparency, fraud responsibility, dependency, etc.fraud responsibility, dependency, etc.

►Address state issuesAddress state issues►Enhance the public’s perception of our Enhance the public’s perception of our

professionprofession

What the AICPA Will DoWhat the AICPA Will Do

►Continue to communicate with youContinue to communicate with you►Work to keep the profession togetherWork to keep the profession together►Work to assist with the Work to assist with the

implementation of this new regulatory implementation of this new regulatory structurestructure

►Provide you with the assistance to deal Provide you with the assistance to deal with the Legislative/Regulatory issues with the Legislative/Regulatory issues in your Statein your State

Questions?Questions?