state and local business tax policy trends for 2018 - ey.com · 2018 gubernatorial and...

TRANSCRIPT

State and local business tax policy trends for 2018

Page 1 EY Domestic Tax Conference

Disclaimer

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited,

each of which is a separate legal entity. Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited

operating in the US.

This presentation is © 2018 Ernst & Young LLP. All Rights Reserved. No part of this document may be reproduced,

transmitted or otherwise distributed in any form or by any means, electronic or mechanical, including by photocopying,

facsimile transmission, recording, rekeying, or using any information storage and retrieval system, without written permission

from Ernst & Young LLP. Any reproduction, transmission or distribution of this form or any of the material herein is prohibited

and is in violation of US and international law. Ernst & Young LLP expressly disclaims any liability in connection with use of

this presentation or its contents by any third party.

Views expressed in this presentation are those of the speakers and do not necessarily represent the views of

Ernst & Young LLP.

This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax advice to

any taxpayer because it does not take into account any specific taxpayer’s facts and circumstances.

These slides are for educational purposes only and are not intended, and should not be relied upon, as accounting advice.

Page 2 EY Domestic Tax Conference

Today’s presenters

Steven WlodychakPrincipal and State and Local Tax Leader, Ernst & Young LLP Center for Tax Policy, Washington, DC

Daniel Mullins, Ph.D.Executive Director, Ernst & Young LLP Quantitative and Statistical Services, Washington, DC

Scott Roberti Executive Director, Ernst & Young LLP Indirect Tax, State & Local Tax Policy, Stamford, CT

Joseph CrosbyCEO, MultiState Associates, Alexandria, VA

Page 3 EY Domestic Tax Conference

State policy and political environment – 2018

Page 4 EY Domestic Tax Conference

State policy environment

► 2018–2019 could be one of the most active state tax legislative periods ever:

► State considerations in conforming to federal changes:

► Economic development impact/opportunity

► Challenges in states facing budget shortfalls

► Balanced budget requirements

► Tax relief versus need for funding state services and infrastructure improvements

► 2018 gubernatorial and congressional midterm elections

► Impact of federal individual $10,000 cap on state and local tax paid deduction … relief?

► Gubernatorial responses:

► Blue states:

► NY Governor Cuomo press conf: “Missiles fired from Washington toward NY.”

► CT Governor Malloy budget address: “The corporations have received a very large reduction in corporate taxes

as part of the federal plan, and so we’ve adjusted that.’’

► Red states:

► GA Governor Deal slashes state tax windfall by 75%. “R” Gubernatorial candidates vowing bigger tax reductions.

► MI Republicans call for deeper tax cuts to return windfall from federal reform to taxpayers.

Page 5 EY Domestic Tax Conference

2018 partisan control of state houses

2018 gubernatorial map by party 2018 partisan control of state legislatures

2018 states with

complete one-party

control

HI

NY

KY

WA

OR

VA

ME

PAOH

IN

MIWI

MT

AL

CO

IA

FL

ND

SD

KS

OKTN

GASC

NCAZ

UT

ID

WY

CA

NM

LA

AR

MS

ILWV

MO

MN

NENV

AK TXHI

NY

KY

WA

OR

VA

ME

PAOH

IN

MIWI

MT

AL

CO

IA

FL

ND

SD

KS

OKTN

GASC

NCAZ

UT

ID

WY

CA

NM

LA

AR

MS

ILWV

MO

MN

NENV

AK TX

HI

NY

KY

WA

OR

VA

ME

PAOH

IN

MIWI

MT

AL

CO

IA

FL

ND

SD

KS

OKTN

GASC

NCAZ

UT

ID

WY

CA

NM

LA

AR

MS

ILWV

MO

MN

NENV

AK TX

Democrat governor

Republican governor

Other

Democrat control of both houses

Republican control of both houses

Each party controls one house

Complete Democratic control

Complete Republican control

Split partisan control

VT NH

CT MA

NJ

DE

RI

MD

DC

VT NH

CT MA

NJ

DE

RI

MD

DC

VT NH

CT MA

NJ

DE

RI

MD

DC

Page 6 EY Domestic Tax Conference

2018 state gubernatorial elections map

HI

NY

KY

WA

OR

VA

ME

PA

OHIN

MI

WI

MT

AL

CO

IA

FL

ND

SD

KS

OKTN

GA

SC

NCAZ

UT

ID

WY

CA

NM

LA

AR

MS

IL

WV

MO

MN

NENV

AK TX

VT NH

CT MA

NJ

DE

RI

MD

DC

Source: 270 to Win webpage, 2018 battleground states pro forecast Larry Sabato

https://www.270towin.com/2018-governor-election/(last accessed April 6, 2018)

36 gubernatorial elections in 2018

7 Democrats

and

7 Republicans

do not face a

2018 election.

Projected results

Democratic control

Republican control

Toss-up

No election

Page 7 EY Domestic Tax Conference

State reaction and fiscal impact to federal tax reform

Page 8 EY Domestic Tax Conference

State reaction to the Tax Cuts and Jobs Act (TCJA) Trends and new ideas

Proposal States

Revenue department analysis CA, DC, IL, ME, NY

Employer payroll tax Proposed NY

New entity-level tax on PTE’s pass-through entities (PTEs) Proposed CA, CT, (NY gov. proposed)

Conformity update bills Enacted GA, IA, MI, VA, WV

Foreign provisions – IRC Section 245A (future foreign

dividends received deduction (DRD)), Section 250 (foreign-

derived intangible income (FDII)/global intangible low-taxed

income (GILTI) deduction), Section 951A (GILTI), Section 965

(transition tax on accumulated foreign earnings)

Enacted ID (IRC Section 965),

GA (IRC Sections 250, 951A, 965);

(ID, NY, OR – proposed)

30% business interest expense limitation Enacted GA (decoupled)

PTE deduction Proposed OR

Bonus depreciation Proposed CT, NY, PA

Charitable contribution in lieu of tax Proposed CA, CT, DC, MD, NJ, NY, OR, WA

Carried interest fee (compensating state tax rate equal to Fed

ordinary income rate)

Proposed CA, IL, NJ, NY, RI

Page 9 EY Domestic Tax Conference

Quantifying the impacts of TCJA on state corporate taxes

► New EY/COST study (March 5, 2018) provides estimates

of the impacts of TCJA on state corporate tax bases.

► Study examines the impact of all states updating their

corporate tax codes to the TCJA but remaining coupled to

specific provisions as they have in the past:

► Not what will happen, not what the states will do but what

could happen if the states conform to federal tax law changes

as they have in the past

► The estimated percentage change in the state corporate

tax base from TCJA is about 12% over the first 10 years

(2018–27), with significant variation among the states.

Page 10 EY Domestic Tax Conference

Estimated percentage change in state corporate tax base from TCJA by state (2018–27)

* State starts with IRS Form 1120 line 28. To the extent

IRC Section 250 deductions not allowed, this impact

would be higher by 4%.

** There may be a California impact relating to cash

repatriation for waters’-edge filers once the deemed

repatriated earnings have been actually distributed as

dividends to US corporate shareholders. California

Franchise Tax Board has estimated this amount at

approximately $350m.

State % increase in state corporate tax base State % increase in state corporate tax base

Alabama 11% Nebraska 11%

Alaska* 12% Nevada n/a

Arizona 14% New Hampshire* 13%

Arkansas 12% New Jersey* 12%

California** 12% New Mexico* 11%

Colorado 12% New York* 12%

Connecticut* 12% North Carolina 12%

Delaware 10% North Dakota 10%

Florida 13% Ohio n/a

Georgia 12% Oklahoma 13%

Hawaii* 13% Oregon* 10%

Idaho 9% Pennsylvania* 14%

Illinois 9% Rhode Island* 11%

Indiana* 12% South Carolina 12%

Iowa 13% South Dakota n/a

Kansas 11% Tennessee* 12%

Kentucky* 12% Texas n/a

Louisiana 12% Utah* 12%

Maine 12% Vermont 14%

Maryland* 12% Virginia 13%

Massachusetts* 12% Washington n/a

Michigan 9% West Virginia 9%

Minnesota* 12% Wisconsin* 9%

Mississippi* 4% Wyoming n/a

Missouri 11% District of Columbia 12%

Montana* 9% Overall change 12%

Page 11 EY Domestic Tax Conference

Sales tax remote seller nexus expansion

Page 12 EY Domestic Tax Conference

States expand sales tax nexus for remote sellers

Page 13 EY Domestic Tax Conference

US Supreme Court hears remote seller nexus case

► South Dakota v. Wayfair (U.S. S.Ct. Dkt.17-494):

► Heard by US Supreme Court on April 17, 2018

► Ruling expected by June 2018

► 2017 – South Dakota legislature enacts SB 106:

► Remote seller nexus:

► Physical presence not required; nexus if:

► $100,000 of South Dakota sales or 200 transactions

► What could the Court do?

► Overturn Quill v. North Dakota (1992):

► (Holding: Dormant Commerce Clause requires physical presence.)

► Uphold Quill, strike down SB 106

► Remand back to South Dakota courts on procedural issue (no case in controversy!)

► What will the states do? Will Congress respond?

Page 14 EY Domestic Tax Conference

Wayfair scorecard from questions on oral argument

Kill Quill –

Three Justices

Not sure

Two Justices

For affirmance –

Four Justices

J. Thomas: As usual, didn’t say a word in oral argument

(never does), but he has been a consistent opponent of

“dormant Commerce Clause” (it’s nontextual … it’s not in the

Constitution.)

J. Gorsuch: Telegraphed his opinion in DMA v. Brohl when

he was on the 10th Cir. – concurring opinion – Quill/Bellas

Hess is “precedential island” which “will wash away with the

tides of time.”

C.J. Roberts: Court really isn’t in the role of telling Congress

what to do. “It would be very strange for [this Court] to tell

Congress it ought to do something ... just a thought.” Congress

was working on solution until Court took the case.

J. Kagen: She has concerns about stare decisis, leave to

Congress, fundamental role of the Court. Author of Kimble v.

Marvel Entertainment. It is a bit ironic to overturn Quill to benefit

the very companies that benefited from it.

J. Breyer: protect the mandolin seller; costs of compliance; he is

very concerned about US SG’s position that one sale was

enough!

J. Kennedy: Concurring opinion in DMA v. Brohl “inviting” a

challenge to Quill – Wrongly decided then. No other Justice

joined him.

J. Ginsburg: She had pointed questions about role of Court

versus Congress, but has been a long proponent of state action

(dissented in Wynne) – concern about retroactive taxation.

J. Sotomayor: She has raised concerns about retroactive

impact of overturning Quill.

J. Alito: He is a current champion of Commerce Clause. Won’t

the states go crazy and grab all they can? Double taxation?

Page 15 EY Domestic Tax Conference

State and local government finance in 2018

Page 16 EY Domestic Tax Conference

State and local government spending, billions of nominal dollars

Source: State and Local Government Finance, US Census, billions of nominal dollars; Centers of Medicare and Medicaid Services

0%

30%

60%

90%

120%

2001 2003 2004 2005 2006 2008 2009 2010 2011 2012 2013 2014 2015

Spending growth, relative to 2001

$0

$500

$1,000

$1,500

$2,000

$2,500

'01 '03 '04 '05 '06 '08 '09 '10 '11 '12 '13 '14 '15

State and local spending

12%

14%

16%

18%

$0

$200

$400

$600

'95'96'97'98'99'00'01'02'03'04'05'06'07'08'09'10'11'12'13'14'15'16

Medicaid

Federal

State and local

Medicaid as % of national health

expenditure

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

'01 '03 '04 '05 '06 '08 '09 '10 '11 '12 '13 '14 '15

State and local government finance

Total expenditure

Total revenue

14.0%

14.5%

15.0%

15.5%

16.0%

16.5%

17.0%

17.5%

'95'96'97'98'99'00'01'02'03'04'05'06'07'08'09'10'11'12'13'14'15'16

Medicaid share of total health care expenditures Federal, state and local spending

ACA passed

Transportation+19%

Everything else+29%

0%

10%

20%

30%

'05 '06 '08 '09 '10 '11 '12 '13 '14 '15

Per capita state and local transportation expenditures Relative to 2005 (capital and operating)

Page 17 EY Domestic Tax Conference

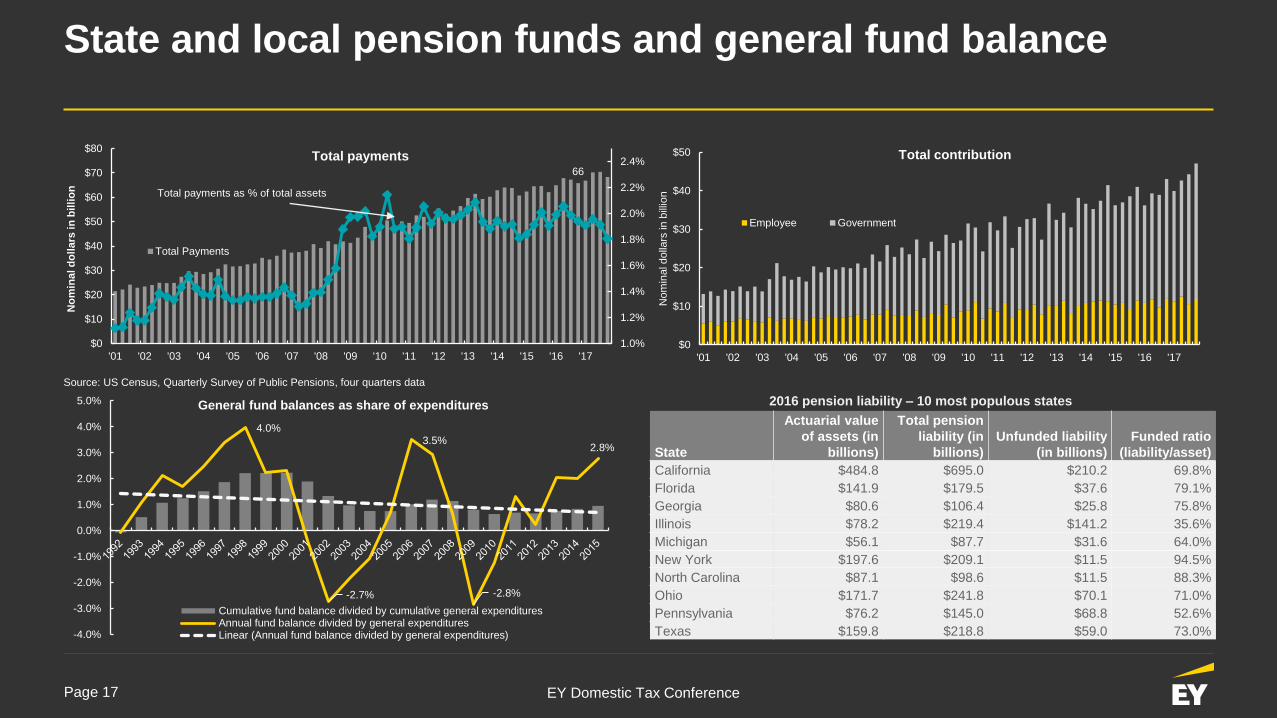

State and local pension funds and general fund balance

Source: US Census, Quarterly Survey of Public Pensions, four quarters data

66

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

2.2%

2.4%

$0

$10

$20

$30

$40

$50

$60

$70

$80

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

No

min

al d

oll

ars

in

bil

lio

n

Total Payments

Total payments as % of total assets

$0

$10

$20

$30

$40

$50

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

Nom

inal dolla

rs in

bill

ion

Employee Government

Total contributionTotal payments

State

Actuarial value

of assets (in

billions)

Total pension

liability (in

billions)

Unfunded liability

(in billions)

Funded ratio

(liability/asset)

California $484.8 $695.0 $210.2 69.8%

Florida $141.9 $179.5 $37.6 79.1%

Georgia $80.6 $106.4 $25.8 75.8%

Illinois $78.2 $219.4 $141.2 35.6%

Michigan $56.1 $87.7 $31.6 64.0%

New York $197.6 $209.1 $11.5 94.5%

North Carolina $87.1 $98.6 $11.5 88.3%

Ohio $171.7 $241.8 $70.1 71.0%

Pennsylvania $76.2 $145.0 $68.8 52.6%

Texas $159.8 $218.8 $59.0 73.0%

2016 pension liability – 10 most populous states

4.0%

-2.7%

3.5%

-2.8%

2.8%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0% General fund balances as share of expenditures

Cumulative fund balance divided by cumulative general expendituresAnnual fund balance divided by general expendituresLinear (Annual fund balance divided by general expenditures)

Page 18 EY Domestic Tax Conference

Revenue performance of the state and local sector

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50% Major taxes as a portion of total state and local tax revenue

Property

General sales and gross receipts

Individual income

Corporation net income

-8%

26%

-25%

-6%

16%

-30%

-20%

-10%

0%

10%

20%

30%

2007 2008 2009 2010 2011 2012 2013 2014

Major state and local tax growth rates since 2007

Individual incomeCorporation net incomeGeneral sales and gross receipts

150,000

200,000

250,000

300,000

350,000

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

Annualized state and local tax collections, by quarter ($2009)

Total_a Ind_inc_a Sales_G_GR_a All Other

0.015

0.017

0.019

0.021

0.023

0.025

0.027

0.029

-0.005

0.005

0.015

0.025

0.035

0.045

0.055

0.065

0.075

Incom

e, sale

s a

nd o

ther

To

tal ta

x c

olle

ctio

ns

Annualized state and local tax collections, by quarterly as a portion of annualized personal income

Total_a Ind_inc_a Sales_G_GR_a All Other

2015

Page 19 EY Domestic Tax Conference

2018–19 shaping up to be one of the busiest state tax legislative sessions ever!

Page 20 EY Domestic Tax Conference

Q&A

Page 21 EY Domestic Tax Conference

#EYDTC

Thank you!

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory

services. The insights and quality services we deliver help build trust

and confidence in the capital markets and in economies the world

over. We develop outstanding leaders who team to deliver on our

promises to all of our stakeholders. In so doing, we play a critical role

in building a better working world for our people, for our clients and

for our communities.

EY refers to the global organization, and may refer to one

or more, of the member firms of Ernst & Young Global Limited, each

of which is a separate legal entity. Ernst & Young

Global Limited, a UK company limited by guarantee, does not

provide services to clients. For more information about our

organization, please visit ey.com.

Ernst & Young LLP is a client-serving member firm of

Ernst & Young Global Limited operating in the US.

© 2018 Ernst & Young LLP.

All Rights Reserved.

1801-2575548

ED None

This material has been prepared for general informational purposes

only and is not intended to be relied upon as accounting, tax or other

professional advice. Please refer to your advisors for specific advice.

ey.com