startup financing 101

TRANSCRIPT

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l

Asia Pacific Trends and Intelligence

July 2013 Will Matthews

Start-Up Financing 101

Adrian Vanzyl

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 2

• Headquartered in Bangkok, offices in Singapore

• Not a traditional fund – no carry, no management fee, no fixed size or lifespan

• Focus on ecommerce companies, B2C and platforms supporting commerce

• Invest only across Southeast Asia

• And only where management team is in SEA

• And only where primary customer base is in SEA

• Venture side of Ardent

– Seed and early stage

– 5 investments so far, including into E27

• Labs side of Ardent

– We build a company inside of Ardent

– aCommerce as example – full backend logistics and fulfillment, 80 staff in our Bangkok

office

• Founded by the entrepreneurs behind Ensogo (sold to LivingSocial), Admax (sold to

Komli) and NewmediaEdge (sold to STW)

• Investors include founding team, plus Japanese investors (Recruit.co.jp and GMO-

vp.com), US investors (Siemervc.com), and several regional angels.

About Ardent Capital

We are an Operator Venture Capital Firm

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 3

• Educated in Australia

• AU 1995, CTO of Sausage Software (HotDog), IPO on ASX

• USA 1997, CTO of LookSmart, IPO on Nasdaq

• USA 1999, VP Bizdev LinkExhange, sold to Microsoft

• USA 2000 onwards, CTO Blumberg Capital, $100M early stage VC in SF

– CEO of two portfolio companies

– Over 70 investments, including Hootsuite, Nutanix

• Thailand, end 2011 onwards, CEO Ardent Capital

• MD by training (Monash University, MB BS)

• I love technology, the internet, entrepreneurs, investing and building stuff.

• Have personally invested in about 30 companies

About Adrian Vanzyl

CEO and co-founder of Ardent

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 4

• Debt Financing

– You borrow the money and agree to pay it back in a particular time frame at a

set interest rate

– You owe the money whether your start-up succeeds or not

• Equity Financing

– You sell partial ownership of your company in exchange for cash

• Equity = Stock or any other security representing an ownership interest

– The investors assume all (or most) of the risk

• If the company fails, the investors lose their money

• If the company succeeds, the investors typically make much greater return

on their investment than interest rate (“higher risk higher returns”)

– Because investors take on a much higher risk than lenders, they are typically

far more involved in your company

How to Fund Your Start-Up?

There are essentially two different types of business financing

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 5

Which Type of Financing is Best?

There are many types of investment vehicles depending on your

objectives and the stages which your start-up is in

Debt (e.g. Bank

Loans)

Convertible Debt

Convertible Equity

Founder Equity/Shares

Preferred Shares

Common Shares/ Equity

Equity Debt

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 6

• Common shares should be contrasted with Founder Shares and Preference shares

• Also known as "ordinary shares“

• Can be “voting” or “non-voting”

– A voting share is a share of stock with the right to vote on certain corporate

policies

– Complex cap table situations (hundred small shareholders is a problem)

• Common stockholders have a residual claim to the income and assets of the

business

– In the event of liquidation, common shareholders have rights to a company's

assets only after bondholders, preferred shareholders and other debt holders

have been paid in full

Common Stock/Common Shares

Common Stock is a form of equity ownership and gives the right to its

owner to share in the profits of the company

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 7

• Founder Equity or Founder Shares are simply common stock

– Typically allocated and committed, but not really issued until the time of startup

incorporation

– Usually follow a vesting schedule but may start vesting before the issuance of

founders’ stock or even prior to the date of incorporation of the company

– This vesting is balanced by investors’ desire to keep the founders committed to

the company over the long term

– Investors typically insist on a 3-4 year vesting period, in equal monthly

increments. This is to reduce the risk of a founder leaving early.

Founder Equity/ Founder Shares

Even before seeking outside financing, founders must agree on how to

split initial ownership

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 8

• It is an option to buy, not an actual share

• Employees get options “for free”

• Critical to motivate and retain staff

• Cliff – typically one year

• Vesting schedule – 3 to 4 years

• 15-30% of the company. Why so much

• Separate from Founders shares, but Founders shares can also vest

• Strike price

• Exercise

• Acceleration

• Can make your employees rich

• Critical for building the ecosystem

ESOP

Employee Stock Options

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 9

• Preferred stock is a class of stock that provides certain rights, privileges, and

preferences to investors

– Examples of such preferential rights include

• dividend payment preferences

• liquidation preferences

• redemption rights

• voting rights

• Preferred stock entitle the holders to certain rights senior to those of common

stockholders

• Senior to the common stock in the event of a sale of the business

– Preferred equity holders get paid at least their money back before the common

shareholders (downside protection)

• This is one way in which the investors can protect their interests

Preferred Shares

Venture capitalists and other early stage investors typically invest in

startups through preferred shares

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 10

• Typically the way the debt will be converted into shares is specified at the time the

loan is made

• Converts on a ‘Qualified Financing’

• Converts into same class of shares as the preference investors

• Usually there is compensation in the form of a discount

– Discussed next

• Sometimes there is a cap on the valuation at which the debt will convert. This is to

protect the investors from a massive increase in valuation

• Ability to raise funds while allowing founders to avoid pricing until valuations can be

made on firmer ground

– Advantageous particularly for Friends & Family round

• Less dilutive if the company believes its equity will be worth more at a later date

• Typically faster than raising a priced round from an institutional venture capital firm

that typically seeks a minimum ownership level

• Lower transaction costs (mostly legal fees) when issuing debt vs. equity

Convertible Debt, or Convertible Note

Why Use Convertible Debt?

A type of debt that the holder can convert into a specified number of

shares of common stock in the issuing company

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 11

Discount - Amount of reduction in price the convertible debt holders will get when

they convert in the next round (expressed in terms of a percentage, usually 20% - 25%)

It can also increase over time (eg start at 10%, grow at 2% per month)

Example

• An investor invests $100,000 in a startup as a convertible debt

• The terms of the note are a 20% discount and automatic conversion after a qualified

financing of $1,000,000.

• Assuming the shares were priced at $1.00, the investor can convert the $100,000 debt

to shares at the discount rate of $.80 each (20% discount) instead of the $1.00 price

that other participants in the current funding round will have to pay

• That gives the initial investor 125,000 shares for the price of $100,000

• Caps can also be added to convertible debt, setting a limit for how much the startup

can raise before the shares stop getting diluted

• If the pre-money cap was $5,000,000, you would still get a discount of 20% up to that

amount. If the startup raised at a valuation over $5,000,000, then the investor will

convert at $5M no matter what the actual valuation is

Convertible Debt

Sometimes a discount is offered as a compensation to convertible debt

holders

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 12

• Essentially, Convertible Equity removes the repayment at maturity and interest

provisions of Convertible Debt

• Startups can avoid complex interest-rate calculations and payments that come with

convertible debt

• Startups don’t have to worry about investors calling for the debt if the maturity date

rolls around and there has not been a Series A Round

• Companies don’t have to artificially carry debt on their books, a potential liability

when seeking a line of credit from a supplier or closing a deal with a large

corporation

Convertible Equity

Convertible Equity retains the most popular features of Convertible Debt

but does not saddle startups with debt

Why Use Convertible Equity?

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 13

• An investor buys shares directly from a founder

• The money does NOT go into the company

• It only goes to the founder

• Founder positives

– Gets some money out

– Reduces day to day stress (can I afford to pay my rent)

• Company negatives

– Money doesn’t go into company to help it grow

– If too much can demotivate the Founder

Selling Founders Shares

Buy out some of the Founders’ holding

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 14

• Bootstrapping

• Angels

• Friends & Family

• Incubators

• Accelerators

The different stages of equity financing

A typical start up go through multiple rounds of financing, but the

number and type of stages may change based on start up performance

and market conditions

Idea Stage Seed StageEarly Stage

Round

Growth/Late Stage

• Angel Investors

• Incubators

• Accelerators

• Seed Funds

• Institutional

Funding

– Series A

• Institutional

Funding

– Series B

– Series C

• IPO

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 15

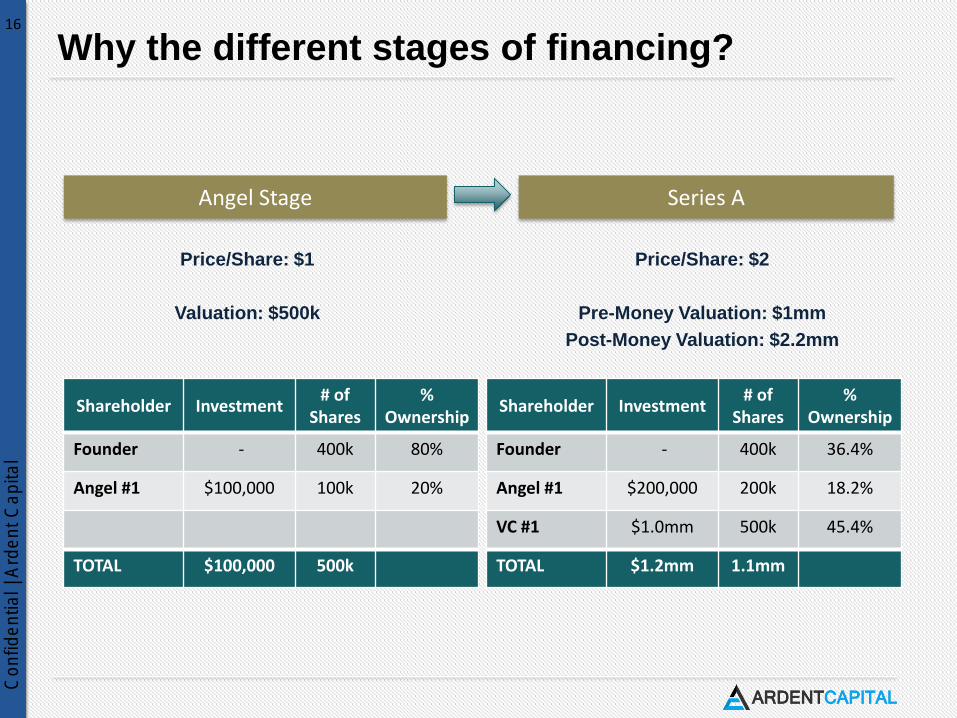

• Before each equity financing round, there is a valuation of the company

• Each round is priced independently and involves a new term sheet specifying the

characteristics of the investment

Why the different stages of financing?

Entrepreneurs often raise capital in multiple rounds of financing so that

they can take advantage of higher pre-money valuations at each

subsequent round

Post Money Valuation

Pre Money Valuation

Investment= +

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 16

Why the different stages of financing?

Price/Share: $1

Valuation: $500k

Angel Stage Series A

Price/Share: $2

Pre-Money Valuation: $1mm

Post-Money Valuation: $2.2mm

Shareholder Investment# of

Shares%

Ownership

Founder - 400k 80%

Angel #1 $100,000 100k 20%

TOTAL $100,000 500k

Shareholder Investment# of

Shares%

Ownership

Founder - 400k 36.4%

Angel #1 $200,000 200k 18.2%

VC #1 $1.0mm 500k 45.4%

TOTAL $1.2mm 1.1mm

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 17

• Key provisions include

– Board of Director Composition/ Appointment

– Veto Rights

– Right of First Refusal

– Pre-Emptive Rights

– Drag Along/ Tag Along Rights

– Liquidation Preference & Participation Rights

Shareholders’ Agreement

A shareholders’ agreement (or SHA) is an arrangement among the

company's shareholders describing how the company should be

operated and the shareholders' rights and obligations

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 18

• The shareholder agreement sets out the size of the board and the manner in which

board members will be elected

• As part of the investment negotiation, an investor can demand the right to appoint a

director to the company’s board

– The investor will have the right to appoint and remove its representation

• In addition, an investor may negotiate to appoint an observer to the board

– The observer shall be entitled to attend any Board meeting

– But does not have the same legal responsibility

• Typical board composition

– Odd number of members

– Chairman

– Example – two insiders (including CEO), two investors, one independent

• Board structure is critical!

Board Composition/ Appointment

Some investors are entitled to representation on the company’s board of

directors

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 19

Some examples include:

• Decision on Financial Interests/Affairs

– Incurrence of any capital expenditure above a defined amount in a single year

– Any decisions regarding the making of an IPO• Risk is forcing a sale, or blocking a sale

– The sale, transfer, lease, mortgage, or pledge of any assets of the Company of a

value in excess of a defined amount

– Any change in the nature and/or scope of the of the Company

– Any increase, reduction or alteration to the issued share capital of the Company

– The winding up, dissolution or liquidation of the Company, including any filings in

respect of any of the foregoing

• Decisions on Corporate Governance

– The appointment, remuneration and dismissal of any Director

– The appointment, remuneration and dismissal of the auditors of the Company

– The appointment, and the terms of appointment and dismissal, of any member of

the Management Team and Key Employees (this means YOU!!!)

Veto Rights

Investors can also negotiate specific veto rights so that they have

decision-making over certain issues deemed important to them

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 20

• For example, if Shareholder A wishes to sell shares to a third party, but Shareholder

B has the right of first refusal, shareholder B has to right to acquire the shares

before A can transfer shares to the third party.

• If B decides to acquire all the shares, then the third party will not even have the

chance to acquire any shares from A

• This is to avoid unwanted (from the Shareholder/Investor’s point of view) new

shareholders (eg a competitor) from owning part of the company

• Makes negotiating with a new buyer complicated, as they know at the end of it all,

they may still not get their shares

Right of First Refusal

The Right of First Refusal is the right to acquire shares before shares

are transferred to a third party

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 21

• For example, if the company decides to issue new shares to potential Series B

investors, Series A investors will have the right to acquire shares up to its pro rata

shareholding

– This helps ensure that Series A investors can prevent its shareholding from

being diluted from future rounds of financing

Pre-Emptive Rights

Pre-Emptive Rights give the existing shareholders the right to acquire

new shares issued by the company

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 22

Drag Along Right

• Gives the majority shareholder the right to force other investor(s) to sell his

stake should the majority shareholder exit

• Protects majority shareholders

• Standard terms in a stock purchase agreement

• Typically terminate upon an initial public offering

• Important esp when lots of little shareholders (tracking them down can be

impossible)

Tag Along Right

• Gives the minority shareholder(s) the right to join in the exit should the

majority shareholder sells his stake

• Minority holders have the right to sell their stake at the same terms and

conditions as would apply to the majority shareholder

• Protects minority shareholders

Drag Along/Tag Along Rights

Drag Along and Tag Along Rights exist to protect majority and minority

shareholders respectively

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 23

• Liquidation Preference specify how money is returned to a particular series of the

company’s stock ahead of other series of stock

Example

• Liquidation Preference: In the event of any liquidation or winding up of the

Company, the holders of the Series A Preferred shall be entitled to receive in

preference to the holders of the Common Stock a per share amount equal to [x] the

Original Purchase Price plus any declared but unpaid dividends (the Liquidation

Preference)

• In this case, a certain multiple (x) of the original investment per share is returned to

the investor before the common stock receives any consideration

Liquidation Preference

The liquidation preference determines how the pie is shared in a

liquidity event

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 24

• Fully-Participating stock will share in the sale proceeds on a pro rata basis with

common after payment of the liquidation preference

• Capped Participation indicates that the stock will share in the sale proceeds on a

pro rata basis until a certain multiple return is reached

• Non-Participating This liquidation preference is most favorable to the company as

the stock will not share in the sale proceeds beyond the payment of the liquidation

preference

Participation Rights

After the payment of the liquidation preference, the next thing to

consider is whether or not the investor shares are participating

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 25

• Assuming that both classes of preferred (Series A & B) are straight preferred with

no multiple or dividends with Series B senior to the Series A

Liquidation Preferences in Different Scenarios

Depending on the sale price, liquidation preference can lead to

drastically different outcomes for founders

ShareholderCommon

SharesSeries A Shares

Series A Cost

Series B Shares

Series B Cost

Total Shares

Total CostOwnership

(Fully Diluted)

Founder 1,000,000 45.4%

VC # 1 - 400,000 $1,000,000 200,000 $1,000,000 600,000 $2,000,000 27.3%

VC # 2 - 600,000 $3,000,000 600,000 $3,000,000 27.3%

Shareholding Total SharesSharePrice

CostLiquidationPreference

Ownership %

Series B 800,000 $5.00 $4,000,000 $4,000,000 36.4%

Series A 400,000 $2.50 $1,000,000 $1,000,000 18.2%

Common Shares 1,000,000 45.4%

Options 0%

TOTAL 2,200,000 100%

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 26

• Sale Price = $3.0mm

Scenario 1: Low Exits

If the sale price is low enough, founders can sell the company and not

get the fully diluted ownership percentage of the proceeds because

some or all of the preferred shareholders will choose to take their

liquidation preference instead of their percentage of the company

Liquidation Preference Proceeds % of Total Proceeds% of Pre-Sale Ownership

Series B $3,000,000 100.0% 36.4%

Series A $0 0% 18.2%

Common Shares $0 0% 45.4%

Shareholder % Series B Total Proceeds% of Total Proceeds

VC # 1 25% $750,000 25%

VC # 2 75% $2.25mm 75%

Founder 0% $0 0%

Total 100% $3.0mm

% of Pre-Sale Ownership

45.4%

27.3%

27.3%

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 27

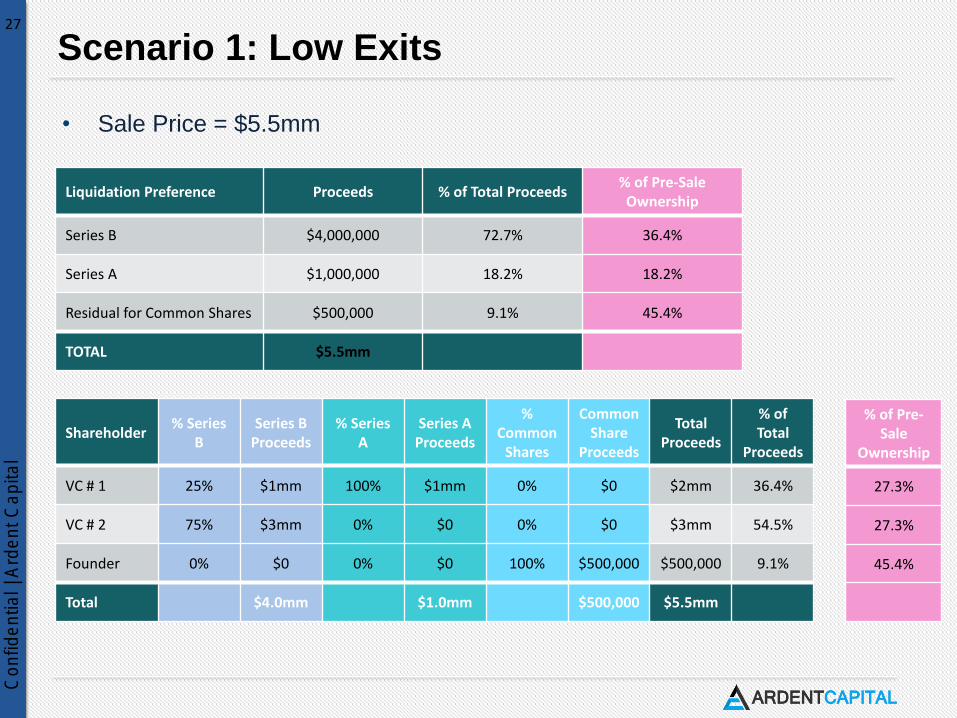

• Sale Price = $5.5mm

Scenario 1: Low Exits

Liquidation Preference Proceeds % of Total Proceeds% of Pre-Sale Ownership

Series B $4,000,000 72.7% 36.4%

Series A $1,000,000 18.2% 18.2%

Residual for Common Shares $500,000 9.1% 45.4%

TOTAL $5.5mm

Shareholder% Series

BSeries B

Proceeds% Series

ASeries A

Proceeds

%Common

Shares

Common Share

Proceeds

TotalProceeds

% of Total

Proceeds

VC # 1 25% $1mm 100% $1mm 0% $0 $2mm 36.4%

VC # 2 75% $3mm 0% $0 0% $0 $3mm 54.5%

Founder 0% $0 0% $0 100% $500,000 $500,000 9.1%

Total $4.0mm $1.0mm $500,000 $5.5mm

% of Pre-Sale

Ownership

27.3%

27.3%

45.4%

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 28

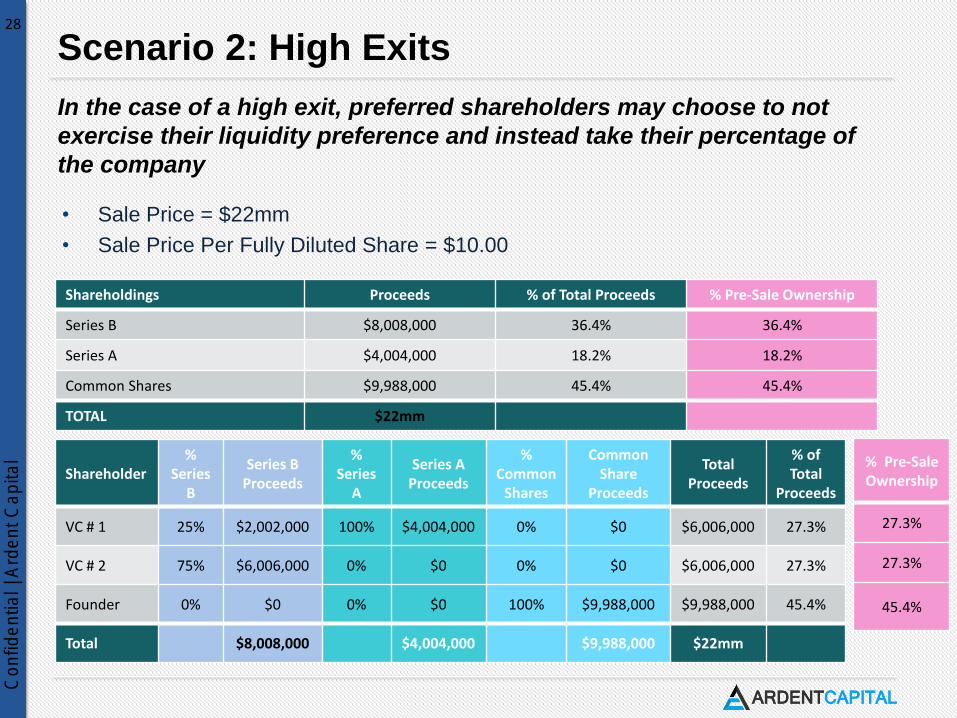

• Sale Price = $22mm

• Sale Price Per Fully Diluted Share = $10.00

Scenario 2: High Exits

Shareholder%

Series B

Series B Proceeds

%Series

A

Series A Proceeds

%Common

Shares

Common Share

Proceeds

TotalProceeds

% of Total

Proceeds

VC # 1 25% $2,002,000 100% $4,004,000 0% $0 $6,006,000 27.3%

VC # 2 75% $6,006,000 0% $0 0% $0 $6,006,000 27.3%

Founder 0% $0 0% $0 100% $9,988,000 $9,988,000 45.4%

Total $8,008,000 $4,004,000 $9,988,000 $22mm

% Pre-Sale Ownership

27.3%

27.3%

45.4%

In the case of a high exit, preferred shareholders may choose to not

exercise their liquidity preference and instead take their percentage of

the company

Shareholdings Proceeds % of Total Proceeds % Pre-Sale Ownership

Series B $8,008,000 36.4% 36.4%

Series A $4,004,000 18.2% 18.2%

Common Shares $9,988,000 45.4% 45.4%

TOTAL $22mm

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 29

• Sale Price = $22mm

• Sale Price Per Fully Diluted Share = $10.00

• c

Scenario 3: High Exits with Participation

ShareholdingsLiquidationPreference

ParticipationParticipation

ProceedsTotal Proceeds

% TotalProceeds

% Pre-Sale Ownership

Series B $4mm 36.4% $6,188,000 $10,188,000 46.3% 36.4%

Series A $1mm 18.2% $3,094,000 $4,094,000 18.6% 18.2%

Common Shares $0 45.4% $7,718,000 $7,718,000 35.1% 45.4%

TOTAL $5mm $17mm $22mm

Share-holder

%Series

B

Liquid Pref

Series B Participation

Proceeds

%Series

A

Liquid Pref

Series A Proceeds

%Common

Shares

Common Share

Proceeds

TotalProceeds

% of Total

Proceeds

% Pre-Sale

Ownership

VC # 1 25% $1mm $1.547mm 100% $1mm $3.094mm 0% $0 $6.641mm 30.2% 27.3%

VC # 2 75% $3mm $4.641mm 0% $0 $0 0% $0 $7.641mm 34.7% 27.3%

Founder 0% $0 $0 0% $0 $0 100% $7.718mm $7.718mm 35.1% 45.4%

Total $4mm $6.188 $1mm $3.094mm $7.718mm $22mm

In the case of a high exit with both liquidation preference and full

participation, the preferred shareholders get to “double dip” in the total

proceeds

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 30

Angels

Friends & Family

Incubators

• JFDI

• FF&F

• Self fund

Start Up Funding Landscape

Idea Stage Seed StageEarly Stage (Series A)

Growth/ Late Stage

Seed Funds

• Ardent Capital

• Golden Gate

Ventures

• Jungle Ventures

• Crystal Horse

NRF

• 15% invested by

qualified VCs and

85% Follow Up by

NRF

• CyberAgent

• SingTel Innov8

• Recruit

• Rakuten

• Gree

• SingTel

• Tiger Global

• Sequoia

• Macquarie

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 31

• Positives

– $500K of funding

– Relatively easy and fast

– Lots of NRF funds operating in Singapore

– Provide incubation support at low cost

– Good valuations

• Negatives

– Must do everything in SG – Incorporate, IP, books in SG$

– Key execs must be in SG

– Small market

– Expensive staff costs

– For a Thai team:

• Away from your home base, home team, home customers

• Insufficient follow on funding – Series A crunch

• Lots of competition

NRF Funding in Singapore

Very big positives and negatives

Co

nfid

en

tia

l | A

rde

nt C

ap

ita

l C

on

fid

en

tia

l | A

rde

nt C

ap

ita

l 32

THANK YOU