s&p industry surveys: insurance - life & health

TRANSCRIPT

September 13, 2007

Industry SurveysInsurance: Life & Health

THIS ISSUE REPLACES THE ONE DATED DECEMBER 7 , 2006 .THE NEXT UPDATE OF THIS SURVEY IS SCHEDULED FOR MARCH 2008 .

CCoonnttaaccttss::

Inquiries &Client [email protected]

MediaMichael [email protected]

Replacement copies800.852.1641

Tanjila ShafiLife & Health Insurance Analyst

CURRENT ENVIRONMENT..................................................................1Earnings gain in 2006

Annuities: variable products still dominate Equity-indexed annuities hit a bump Variable universal life sales pick up A challenging interest rate environment Industry consolidation focuses on scale and scope An evolving regulatory environment S&P Ratings Services View:

Credit quality will depend more on risk management Life settlement segment draws scrutiny

INDUSTRY PROFILE...............................................................................9Large, well-known companies dominate a mature industry

INDUSTRY TRENDS .................................................................................9Changing demographics create new opportunities Distribution channels have been shifting M&A activity focuses on scale and scope The demutualization trend takes a pause Capital market activity may slow Legislative changes impact wealth products Federal regulation for life products appears unlikely

HOW THE INDUSTRY OPERATES .............................................................15Ownership structures differ Types of assets Finding funds for investment Two accounting methods Types of products Distribution Regulating the industry

KEY INDUSTRY RATIOS AND STATISTICS ...................................................23HOW TO ANALYZE A LIFE INSURER ........................................................23

Macroeconomic indicators Profitability S&P Ratings Services View:

Evaluating a life insurance company’s creditworthinessLiquidity Leverage Operating and GAAP earnings

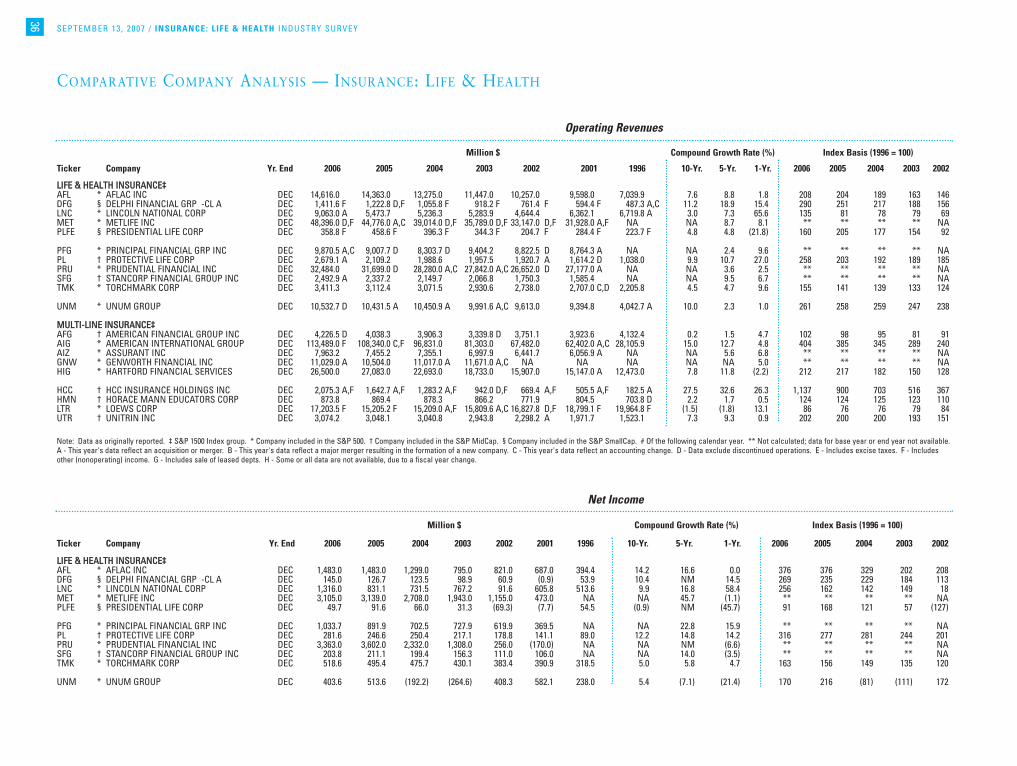

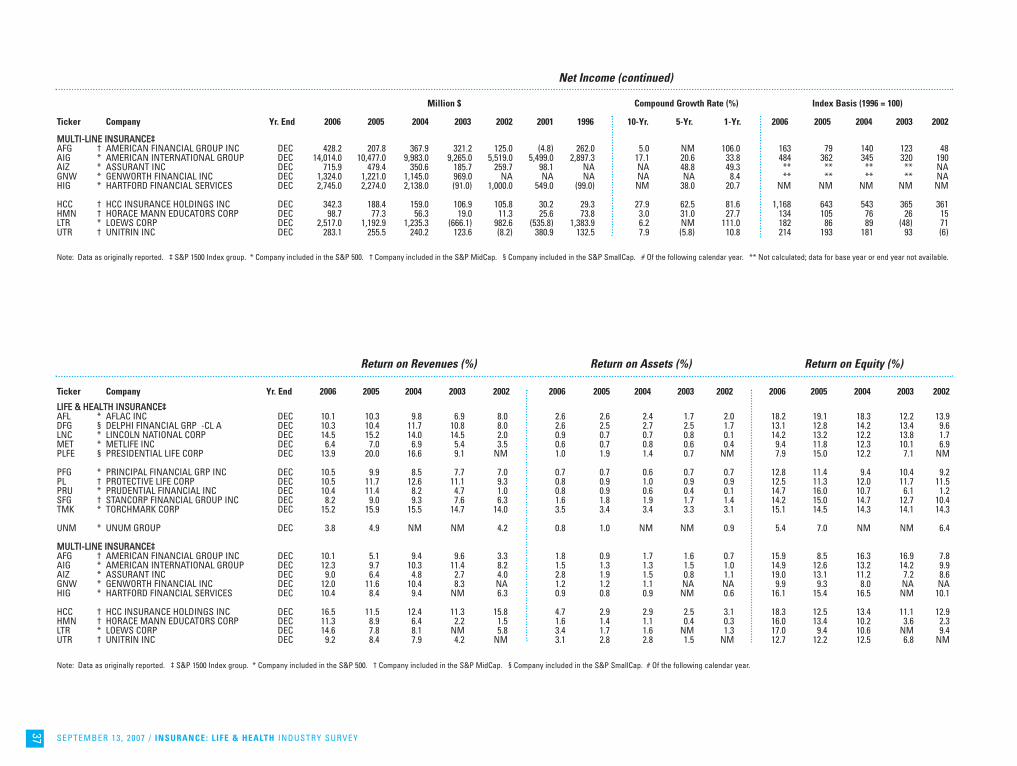

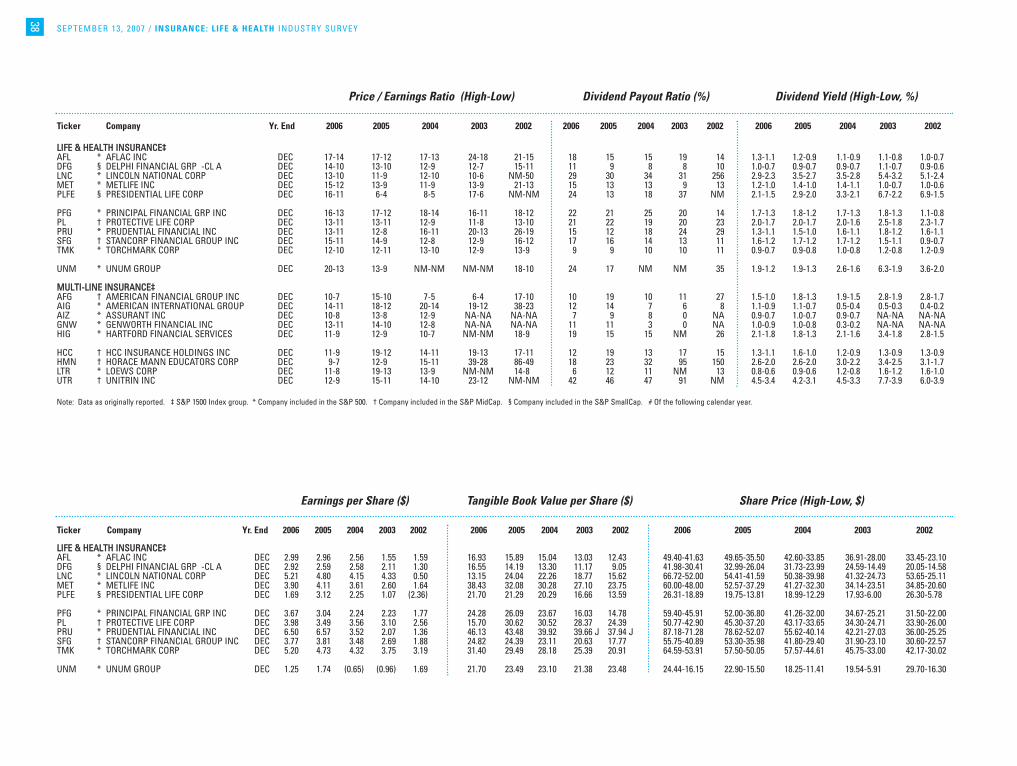

GLOSSARY .............................................................................................29INDUSTRY REFERENCES.....................................................................33COMPARATIVE COMPANY ANALYSIS ..............................................36

Executive Editor: Eileen M. Bossong-MartinesAssociate Editor: Joseph M. CodaCopy Editor: Brandon WilkersonProduction: GraphMediaStatistician: Sally Kathryn NuttallJunior Designer: Paulette Dixon

Client Support: 1-800-523-4534Copyright © 2007 by Standard & Poor’sAll rights reserved.ISSN 0196-4666USPS No. 517-780Visit the Standard & Poor’s Web site:http://www.standardandpoors.com

STANDARD & POOR’S INDUSTRY SURVEYS is published weekly. Annualsubscription: $10,500. Please call for special pricing: 1-800-523-4534,option 2. Reproduction in whole or in part (including inputting into acomputer) prohibited except by permission of Standard & Poor’s.Executive and Editorial Office: Standard & Poor’s, 55 Water Street, NewYork, NY 10041. Standard & Poor’s is a division of The McGraw-HillCompanies. Officers of The McGraw-Hill Companies, Inc.: Harold McGrawIII, Chairman, President, and Chief Executive Officer; Kenneth M. Vittor,Executive Vice President and General Counsel; Robert J. Bahash,Executive Vice President and Chief Financial Officer; John Weisenseel,Senior Vice President, Treasury Operations. Periodicals postage paid atNew York, NY 10004 and additional mailing offices. POSTMASTER: Sendaddress changes to Standard & Poor’s, INDUSTRY SURVEYS, Attn: MailPrep, 55 Water Street, New York, NY 10041. Information has beenobtained by Standard & Poor’s INDUSTRY SURVEYS from sourcesbelieved to be reliable. However, because of the possibility of human ormechanical error by our sources, INDUSTRY SURVEYS, or others,INDUSTRY SURVEYS does not guarantee the accuracy, adequacy, orcompleteness of any information and is not responsible for any errors oromissions or for the results obtained from the use of such information.

VOLUME 175, NO. 37, SECTION 2 THIS ISSUE OF INDUSTRY SURVEYS INCLUDES 3 SECTIONS.

Standard & Poor’s Industry Surveys

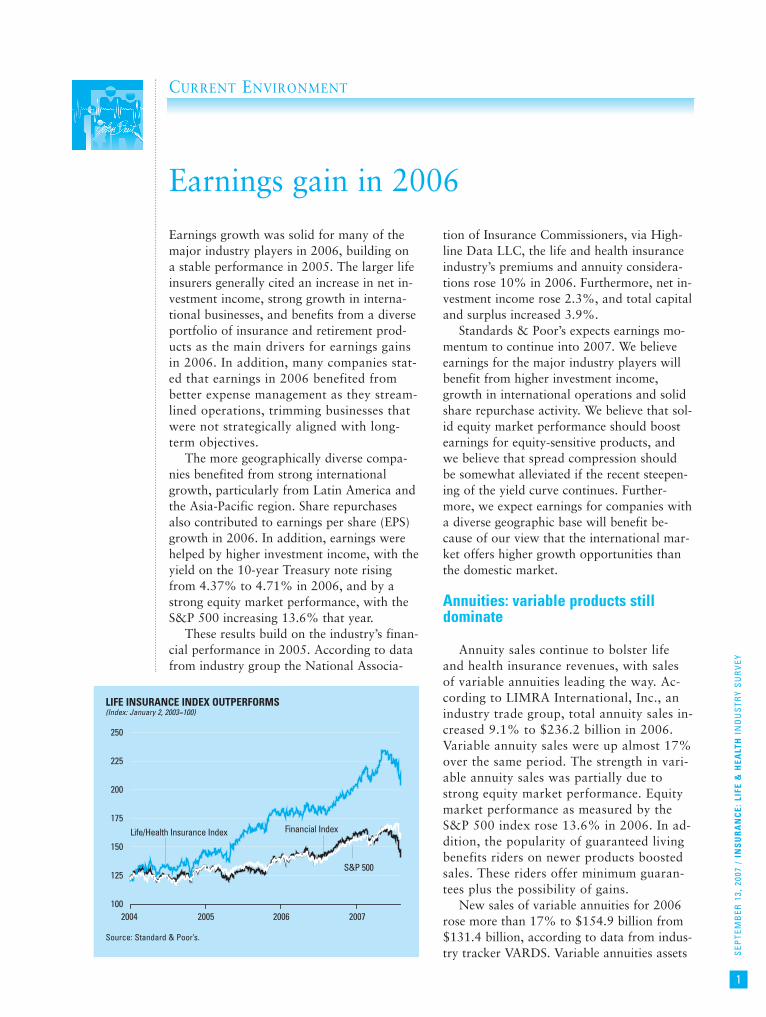

Earnings growth was solid for many of themajor industry players in 2006, building ona stable performance in 2005. The larger lifeinsurers generally cited an increase in net in-vestment income, strong growth in interna-tional businesses, and benefits from a diverseportfolio of insurance and retirement prod-ucts as the main drivers for earnings gainsin 2006. In addition, many companies stat-ed that earnings in 2006 benefited frombetter expense management as they stream-lined operations, trimming businesses thatwere not strategically aligned with long-term objectives.

The more geographically diverse compa-nies benefited from strong internationalgrowth, particularly from Latin America andthe Asia-Pacific region. Share repurchasesalso contributed to earnings per share (EPS)growth in 2006. In addition, earnings werehelped by higher investment income, with theyield on the 10-year Treasury note risingfrom 4.37% to 4.71% in 2006, and by astrong equity market performance, with theS&P 500 increasing 13.6% that year.

These results build on the industry’s finan-cial performance in 2005. According to datafrom industry group the National Associa-

tion of Insurance Commissioners, via High-line Data LLC, the life and health insuranceindustry’s premiums and annuity considera-tions rose 10% in 2006. Furthermore, net in-vestment income rose 2.3%, and total capitaland surplus increased 3.9%.

Standards & Poor’s expects earnings mo-mentum to continue into 2007. We believeearnings for the major industry players willbenefit from higher investment income,growth in international operations and solidshare repurchase activity. We believe that sol-id equity market performance should boostearnings for equity-sensitive products, andwe believe that spread compression shouldbe somewhat alleviated if the recent steepen-ing of the yield curve continues. Further-more, we expect earnings for companies witha diverse geographic base will benefit be-cause of our view that the international mar-ket offers higher growth opportunities thanthe domestic market.

Annuities: variable products stilldominate

Annuity sales continue to bolster lifeand health insurance revenues, with salesof variable annuities leading the way. Ac-cording to LIMRA International, Inc., anindustry trade group, total annuity sales in-creased 9.1% to $236.2 billion in 2006.Variable annuity sales were up almost 17%over the same period. The strength in vari-able annuity sales was partially due tostrong equity market performance. Equitymarket performance as measured by theS&P 500 index rose 13.6% in 2006. In ad-dition, the popularity of guaranteed livingbenefits riders on newer products boostedsales. These riders offer minimum guaran-tees plus the possibility of gains.

New sales of variable annuities for 2006rose more than 17% to $154.9 billion from$131.4 billion, according to data from indus-try tracker VARDS. Variable annuities assets

CURRENT ENVIRONMENT

Earnings gain in 2006

SEP

TEM

BER

13,

200

7 /

INS

UR

AN

CE:

LIF

E &

HEA

LTH

IN

DU

STR

Y S

UR

VEY

1

LIFE INSURANCE INDEX OUTPERFORMS(Index: January 2, 2003=100)

Source: Standard & Poor’s.

Life/Health Insurance Index

250

225

200

175

150

125

1002004 2005 2006 2007

Financial Index

S&P 500

SEP

TEM

BER

13,

200

7 /

INS

UR

AN

CE:

LIF

E &

HEA

LTH

IN

DU

STR

Y S

UR

VEY

2

climbed 14.3% to $1.36 trillion as of De-cember 31, 2006, according to VARDS.

According to LIMRA, sales of fixed annu-ities declined 4.2% to $75.6 billion in 2006.Part of the decline was due to the rise of short-term interest rates, which led to increased com-petition from bank certificates of deposit.

Equity-indexed annuities hit a bump

Sales of equity-indexed annuities (EIAs) de-clined 7.2% to $25.3 billion in 2006, accord-ing to data from industry tracker AdvantageCompendium. Sales of EIAs were hurt by high-er bank interest rates and negative attentionsurrounding the National Association of Secu-rities Dealers’ Notice to Members 05-50, whichaddresses the responsibility of broker-dealerfirms to supervise the sale of EIAs, whichcurrently are not registered under the federalsecurities laws. (This issue is discussed fur-ther under “Annuities remain under scruti-ny” toward the end of this section.)

Equity-indexed annuities have beenamong the industry’s more popular products:sales rose 18% in 2005, and EIAs accountedfor 40% of all fixed deferred annuity sales.EIAs are linked to a stock market index,such as the S&P 500 Composite Stock index.

Investors get a guaranteed return, tax-deferred, as they would through a fixed an-nuity, but the return rises if the underlyingequity index performs well.

Sales of equity-indexed annuitiesreached $27 billion in 2005, according toAdvantage Compendium, up from $23 bil-lion in 2004 and $14 billion in 2003. Afterincreasing for 11 consecutive years, sales ofEIAs declined in 2006.

The growth in equity-indexed annuitieshelped to boost profits at a number of life in-surers. EIAs are lucrative for the industry:commissions average 8.5% to 9%, but theygo as high as 10%, compared with a com-mission rate of 2% to 3% on traditional mu-tual funds. Allianz Life Insurance Co. ofNorth America, a unit of German financialservices giant Allianz SE, is the US leader inindex annuity sales. Solid sales growth andhigh commission rates have made the marketmore competitive as other life insurers enterand chip away at Allianz’s dominant 19.6%market share position.

Variable universal life sales pick up

According to LIMRA, individual life in-surance sales increased 7% in 2006, thelargest increase since 2000. The total faceamount increased by 4%, but the number ofnew policies sold decreased by 1%. Further-more, variable universal life sales increasedby 9% in 2006, the first increase in six years.The increase in variable universal life salesmay be attributable to innovative productfeatures such as death benefit guarantees, aswell as to marketing efforts from broker gen-eral agents and wirehouses, distributors whotraditionally have not been major marketersof the product.

A challenging interest rateenvironment

Investment income saw improvement in2006 as interest rates increased. At the be-ginning of 2006, the 10-year Treasury noteyielded 4.37% and peaked in June 28th,reaching 5.24%. By year-end, the yield haddeclined to 4.71%. Overall, the 10-yearTreasury note rose 34 basis points in 2006,which boosted investment income, an impor-tant source of revenues for life insurers. In-terest rates continued to rise in 2007. In the

TOP 20 WRITERS OF GROUP LIFE INSURANCE — 2006(Ranked by net premiums written)

PREMIUMSCOMPANY (MIL. $)

1. Metropolitan Group 7,746 2. Prudential of America 6,696 3. Hartford Fire and Casualty 1,949 4. CIGNA 1,375 5. New York Life 1,297 6. Aetna Life and Casualty 1,163 7. Minnesota Mutual 1,162 8. Nationwide Corporation 1,033 9. ING America 984

10. Sun Life Assurance 92211. UnumProvident Life 802 12. Mass Mutual Life 729 13. Stancorp Financial 656 14. American International 504 15. HCSC 499 16. Assurant Group 439 17. Forethought Financial 427 18. Lincoln National 412 19. AEGON USA 408 20. Wellpoint Group 331

Source: National Association of Insurance Commissioners,via Highline Data, LLC

SEP

TEM

BER

13,

200

7 /

INS

UR

AN

CE:

LIF

E &

HEA

LTH

IN

DU

STR

Y S

UR

VEY

3

first half of 2007, the 10-year Treasury noteincreased 34 basis points to yield 5.03%. Al-though still at relatively low levels, the high-er yield provided a boost to investmentincome and, thus, operating income.

However, despite 17 increases in the tar-get for the federal funds rate between June2004 and June 2006 — for a total increaseof 425 basis points — the yield on the 10-year Treasury note has actually fallen sincemid-2006. As of July, 16th, 2007, the 10-year Treasury yielded approximately 5.04%.Improving bond default experience compli-cated matters further for life insurers byleading to tighter yield spreads betweenTreasury and investment-grade corporatebonds, which make up a large part of lifeinsurers’ investments.

As a result, new money inflows and pro-ceeds from maturing or liquidated portfolioassets have generally been invested by life in-surers at rates of return near or lower thanexisting investments, putting pressure onportfolio yields. With portfolio yields declin-ing, spreads on deposit-type funds and con-tracts have narrowed, as many policies havebeen reaching their minimum crediting rates.Moreover, rising short-term interest ratesmay keep life insurers from aggressively

lowering minimum crediting rates (i.e., theinterest rate offered) on new policies andcould encourage higher surrender activityon existing policies already at minimumcrediting rates.

This spread compression could lead tomore problems as multiyear guarantee an-nuities begin to mature. These products,which offered three- to 10-year guarantees,sold heavily between 2001 and 2003. Asthey mature, money could be withdrawn,unless the industry has adequate alterna-tives to offer. The tight interest ratespreads make it more difficult to offer at-tractive alternatives. However, the yieldcurve has recently begun to steepen, whichwill help alleviate spread compression,boosting investment income.

Earnings outlook becomes less certainThe current interest rate environment, rel-

atively flat yield curve, and increasing salescompetition may make it more difficult forthe life insurance industry to continue topost the kind of strong earnings growth itenjoyed during 2006.

Those life insurers with more pronouncedexposure to spread-based products (includingfixed annuities and universal life insurance)might be hurt more by the challenging inter-est rate environment. Standard & Poor’s be-lieves that sales of fixed annuity policies havesuffered, as low crediting rates have madethe products less attractive relative to otherinvestment choices.

Net investment income is also likely to behurt by the relatively low yields seen in2006. As mentioned earlier, new money in-flows and proceeds from maturing or liqui-dated portfolio assets have generally beeninvested by life insurers at rates of returnnear or lower than existing investments,putting pressure on portfolio yields.

Stocks hit by subprime concernsAfter seeing stock market returns of 20%

or more in each of the past three years, theS&P US Life and Health Insurance indexrecorded a 15.0% gain in 2006. The gain inthe index compares with a 16.2% gain for thebroader S&P Financials index and a 13.6%gain for the S&P 500 during that year. Inour view, the life and health insurancegroup’s outperformance versus the S&P 500index in 2006 resulted from favorable com-

TOP 20 WRITER OF ORDINARY LIFE INSURANCE — 2006(Ranked by net premiums written)

PREMIUMSCOMPANY (MIL. $)

1. American International 18,055 2. Northwestern Mutual 9,911 3. Metropolitan Group 7,784 4. New York Life 6,616 5. Prudential of America 4,011 6. Mass Mutual Life Insurance 3,820 7. Lincoln National 3,634 8. State Farm 3,373 9. AXA Insurance 3,107

10. AEGON USA 3,093 11. Swiss Reinsurance 2,647 12. Guardian Life Insurance 2,524 13. Pacific Life 1,817 14. John Hancock 1,785 15. Hartford Fire and Casualty 1,762 16. Allstate Insurance 1,717 17. Nationwide Corporation 1,594 18. Sun Life Assurance 1,564 19. Citigroup 1,436 20. ING America 1,353

Source: National Association of Insurance Commissioners,via Highline Data, LLC

SEP

TEM

BER

13,

200

7 /

INS

UR

AN

CE:

LIF

E &

HEA

LTH

IN

DU

STR

Y S

UR

VEY

4

pany-specific M&A developments, businessrestructurings, and turnaround stories.

However, whether the share price gainsfor the Life and Health Insurance indexcan continue in 2007 remains uncertain. Aweakening housing market, credit qualityconcerns, and especially subprime issueshave plagued life and health insurancestocks recently. Through August 17, 2007,the S&P Life and Health Insurance indexrose 5.7%, year to date, versus a 6.9% de-cline in the broader S&P Financial indexand 1.9% increase in the S&P 500 index.However, looking at just the first twoquarters of 2007, the S&P Life and HealthInsurance index had risen 9.9%, comparedwith a 2.0% decline for the S&P Financialindex and a 6.0% gain for the S&P 500during that same period. The decline inshare performance for the Life and HealthInsurance index is attributable to the mar-ket’s concern regarding the credit qualityof the life and health insurance companies’subprime holdings, in our view.

We are concerned that the market’s fo-cus on subprime exposure specifically andthe housing market and credit quality ingeneral will cause headline risk which willlead to excess volatility in share price per-formance for the life and health insurancecompanies. Our greater concern is that theweakening housing market will spread tothe overall economy. A downturn in theeconomy could result in a deterioration ofcorporate credit. Insurance companies tendto hold the bulk of the investment portfo-lio in corporate bonds, so an accelerationof corporate bond default rates, in ourview, could erode the value of their invest-ment portfolios significantly.

Industry consolidation focuses onscale and scope

Consolidation has been a continuing themein the life insurance industry. Over the past fewyears, a handful of large insurers merged,putting pressure on mid-tier players to seek outpartners in order to build additional economiesof scale, to better compete with their biggerand more heavily capitalized rivals.

In June 2006, AXA announced plans to ac-quire Winterthur Swiss Insurance Co. fromCredit Suisse Group for approximately 12.3billion Swiss francs. The deal, which closed in

December 2006, should add some diversifica-tion in Switzerland, and in Central and EasternEurope, where Winterthur has a strong pres-ence. Standard & Poor’s expects cost savingsto come from overlapping operations. Wethink AXA will benefit from Winterthur’snetwork of agents and access to Credit SuisseGroup’s retail network.

On July 3, 2006, Protective Life and Annu-ity Insurance Co. acquired Chase InsuranceGroup, the insurance and annuity operationsunit of JPMorgan Chase & Co., in a deal val-ued at $1.2 billion. Through a series of reinsur-ance agreements entered into immediately afterthe acquisition, approximately 42% of thebusiness of the Chase Insurance Group, exclud-ing the variable annuity business, has beenreinsured to insurance subsidiaries of WiltonRe Holdings Ltd. All of the variable annuitybusiness has been reinsured to Allmerica Finan-cial Life Insurance and Annuity Co., a sub-sidiary of The Goldman Sachs Group, Inc.

In order to better compete with larger rivals(such as MetLife, Inc., Manulife FinancialCorp., and Prudential Financial, Inc.), LincolnNational Corp. and Jefferson-Pilot Corp.struck a merger deal in October 2005 worth$7.6 billion. The deal, completed on April 3,2006, created the fourth largest US life insurer,with $151.3 billion in assets.

In January 2005, Citigroup Inc. exitedthe insurance business, agreeing to sell itslife insurance and annuities business, Trav-elers Life and Annuity Co., to MetLife for$11.5 billion. That deal followed Man-ulife’s $10.8 billion purchase of John Han-cock Life Insurance Co. in 2003.

These deals have created more formidablecompetitors in the life insurance industry andhave ushered in another wave of consolidation.During 2005, there were 28 mergers in the lifeand health insurance sector, with a total valueof $21.8 billion, according to data from finan-cial services analyst SNL Financial. This com-pares with 31 merger deals ($3.5 billion) in2004 and 35 mergers ($14.5 billion) in 2003.

While generating economies of scale tomatch their rivals’ larger geographical foot-prints and product offerings is one rationalefor industry mergers, the current interestrate environment provides another. With arelatively flat yield curve, insurers have notbeen able to profit much on the interest ratespread between what they can earn in thebond market and the interest rates that they

SEP

TEM

BER

13,

200

7 /

INS

UR

AN

CE:

LIF

E &

HEA

LTH

IN

DU

STR

Y S

UR

VEY

5

pay to buyers of their life insurance and an-nuity products. As higher yielding securitiesmature, insurers have been unable to re-place them with anything other than lower-yielding bonds. The cost synergies thatcome from increased size will enable thecompanies to better weather this challengingoperating environment.

M&A trend set to continueConsolidation is likely to remain a theme in

the life and health insurance industry, as manylife insurers are awash with excess capital. Ac-cording to industry trade group, the AmericanCouncil of Life Insurers (ACLI), the industry’srisk-based capital ratio improved to 409% atyear-end 2005 from 390% at year-end 2004,which has left some companies with billionsof dollars that could be put to use in corpo-rate expansions.

The mergers between larger industryplayers since 2003, and the more recentcombination of Jefferson-Pilot and LincolnNational, may force a number of other lifeinsurance firms to use this excess capital toseek out partners as a way to expand theirgeographical coverage and product offer-ings, in order to compete more effectively.

Standard & Poor’s also believes that somebroader financial services companies withrelatively small life insurance operationscould decide to exit these businesses and turntheir attention to their core businesses, lead-ing to more M&A activity as these business-es are divested.

An evolving regulatory environment

Regulation is a major part of the insur-ance industry, and the group faces a numberof ongoing issues. A spate of investigationsat the state level into company practices —including market timing, brokerage commis-sions, and accounting irregularities — con-tinues to hang over the industry. Additionally,states are cracking down on annuity salespractices that they feel are improper.

Ongoing regulatory investigationsThe insurance industry came under fire

from a host of regulatory agencies starting in2002. Although many of those investigationsand lawsuits finally have been settled or arewinding down, there could be more scrutiny instore for the industry over the coming months.

The market-timing scandals that hit themutual fund industry in 2004 resulted inincreased scrutiny of the variable life andannuity products sold by many life insurancecompanies. So far, the fines for market-timing activities have been imposed ononly a few companies. Still, other insurershave increased their reserves to cover po-tential fines and penalties as these investi-gations continue. Companies that haveseen their fair share of scrutiny — includ-ing Conseco Inc., UnumProvident Corp.,Marsh & McLennan Cos. Inc., and Ameri-can International Group Inc. — are hopingthat the worst of the scandals are over.

In August 2006, Prudential Equity Groupreached a settlement with several regulatoryagencies in connection with their investiga-tions into market timing activities involvingthe broker-dealer business at Prudential Secu-rities. Many companies within the insuranceindustry have changed their policies andpractices to avoid any hint of wrongdoing:many of the large insurance brokers haveeliminated contingent commissions, equity-indexed annuity providers are improvingsuitability procedures, and many health in-surers are correcting claims practices.

Annuities remain under scrutinyState and federal regulators are investigating

the annuity market, with the government tak-ing a hard look at the marketing of both vari-able annuities and equity-indexed annuities.

◆ Variable annuities. A number of stateattorneys general have the marketing of vari-able annuities in their crosshairs, as they goafter firms for marketing abuses. Attorneysgeneral Eliot L. Spitzer of New York andRichard Blumenthal of Connecticut began in-vestigating The Hartford Financial ServicesGroup in June 2005. In May 2006, Hartfordagreed to pay $20 million to settle chargesthat it secretly paid brokers to steer pensionfunds to the insurer’s annuities even thoughthey may not have been the best choice. Cali-fornia, Kansas, Missouri, and New York alsoare investigating the industry and looking atnew marketing and suitability rules.

Ultimately, the federal government couldget involved. In late 2004, the NASD (thenknown as the National Association of Se-curities Dealers), a private-sector providerof financial regulatory services, asked the

SEP

TEM

BER

13,

200

7 /

INS

UR

AN

CE:

LIF

E &

HEA

LTH

IN

DU

STR

Y S

UR

VEY

6

Securities and Exchange Commission (SEC)to approve a proposed regulation layingdown suitability standards. The life insur-ance industry opposes such a plan, sayingthat it is unfair to apply suitability stan-dards to variable products only.

◆ Equity-indexed annuities. Regulatorsalso are probing suitability issues in rela-tion to EIAs, which may eventually be la-beled as securities. In August 2005, theSEC asked a number of insurance compa-nies for information on their top-selling

EIAs and any unregistered products thatmay return less than 90% of total premi-ums.

The SEC is scrutinizing the evolvingcharacteristics of these products and mayeventually move to have them registeredwith the SEC in the same manner as othersecurities, such as stocks. In August 2005,the NASD issued a Notice to Members 05-50, which recommended that broker-dealers adopt special procedures in han-dling equity-indexed annuities, due to un-certainty over their classification.

Credit quality will depend more onrisk management

The next 12 months present some sizable chal-lenges for the US life insurance sector. Among the is-sues the industry faces are the likelihood ofcontinued flatness in the yield curve, more mergersand acquisitions, and a weak environment for salesof individual life insurance products. In addition, risklevels are rising in the credit markets, which have be-gun to show some weakening, and will make thecoming year even more difficult for insurers.

Still, as of mid-August 2007, Standard & Poor’sRating Services’ outlook for the US life insurancesector remained stable; that is, we expected pos-itive and negative rating movements to be aboutequal for the next six to 12 months. Our outlookreflects company-specific circumstances rather thanmacroeconomic or sector-wide factors.

Over the next three years, we expect revenuegrowth in the ultra-competitive market for traditionallife insurance products (including whole, term, anduniversal life) to be about 2% to 4%, in line with pro-jected increases in US gross domestic product (GDP).Furthermore, if the yield curve remains flat, higherprofits will be harder to achieve.

To offset these pressures, companies have beenseeking growth in dicey ways, mostly on the liabilityside: creating higher-risk products; making acquisi-tions that could strain operations, financially and/ormanagerially; and engaging in more aggressive prac-tices, such as underwriting with narrower built-inprofit margins.

We believe the default rate cycle for speculative-grade bonds (those rated ‘BB+’ and below) hastroughed and that defaults will start increasing. Inaddition, the life insurance industry continues to feel

the ripples of the potential deterioration of sub-prime mortgage-related assets (primarily residen-tial mortgage-backed securities). Although insurersmay experience some credit losses in the comingyear, Standard & Poor’s believes that in general, theindustry can absorb the impact through the improve-ments it has made since the last credit cycle down-turn, including better risk management and higherrelative capitalization.

Flat interest rates could cap incomeIf long-term interest rates continue to stagnate at

current levels, life insurers’ 2007 income could beconstrained. The 10-year Treasury note has been rel-atively flat since January 2007, with rates now about4.6%, down from more than 5% in 2006. We expecta low, relatively stable interest rate environment thisyear, with 10-year Treasuries projected to yield 4.8%by year-end. We are beginning to observe creditspreads widening as a result of the subprime mort-gage spillover effect, and we expect the yield curve’sshape to stay relatively flat.

To compensate for these flat interest rates, largeinsurers have been chasing yield, using alternativeinstruments, especially private equity, for their in-vestment strategies. For these insurers, strong divi-dend distributions from private equity securities haveenhanced profitability. The overall rate of earningsgrowth for life insurers this year will be less thanin 2006, however, due to the low interest rate en-vironment and the likely decline in the level of pri-vate equity distributions.

Is sales growth sustainable? We expect a return to more historical growth

rates (in the low single digits) for individual life in-surance in 2007. The 7% uptick seen in 2006 individ-

S&P Ratings Services View:

SEP

TEM

BER

13,

200

7 /

INS

UR

AN

CE:

LIF

E &

HEA

LTH

IN

DU

STR

Y S

UR

VEY

7

In much the same way that it is going af-ter the marketing of variable annuities, theNASD is cracking down on EIA marketingabuses. The NASD is looking at the indus-try’s aggressive efforts to move customersinto these instruments, even in cases whereEIAs may be unsuitable for them. Specifical-ly, the NASD is concerned about firms thathave engaged in “switching” campaigns,where customers were moved from variableannuity-type instruments into EIAs, whichhave higher commission rates and higher sur-render fees.

TRIA extension passes without group lifeA reauthorization and two-year extension of

the Terrorism Risk Insurance Act of 2002(TRIA) was passed by Congress in December2005, just before the original law was set toexpire. The original TRIA was passed after theterrorist attacks of September 11, 2001, andprovided federal property-casualty reinsurancefor future terrorist events. Some proposedversions of the December extension includedfederal reinsurance for group life; this, how-ever, was not in the original law and waseventually excluded from the final version.

ual life sales may not be sustainable, as much of itcame from large sales of investor-owned life insur-ance (IOLI), which is a new twist on life settlements.

Variable annuity growth, driven by living benefitguarantees, has more than offset the impact of theflat yield curve, which has plagued sales of fixed de-ferred annuities compared with the certificates ofdeposit with which they compete. Net flows in fixedannuities have been negative because of higher sur-renders resulting from the expiration of surrendercharges on multiyear guarantee annuities.

Is M&A the answer? Some US life insurers are turning to mergers and

international expansion to satisfy shareholders’ de-sire for greater financial returns. Historically, M&Ahas been a high-risk strategy that often destroyedshareholder value due to exorbitant purchase prices,culture clashes between acquirer and acquiree, andpoor operational execution of the merger.

Recent transactions, however, have fared better. Forone thing, recent acquisition prices are more rationalthan they were in the late 1990s. That’s partially be-cause the marketplace is more transparent and due dili-gence has improved, and partially because enterpriserisk management (ERM) is becoming more effective asit increases in importance. Finally, more reasonable pur-chase prices mean recent deals have involved less debtfinancing than in the past.

Because the US life insurance sector remainsfragmented, Standard & Poor’s expects the pace ofconsolidation to continue, with most M&A through2007 and into 2008 coming from sales of large booksof business and divestiture of noncore books.

Enterprise risk management: the ratingdifferentiator

Standard & Poor’s continues to expand the num-ber of enterprise risk management evaluations for

life insurance companies. We see solid ERM disci-pline as key to profitable growth with lower volatili-ty, and we believe it will continue to be an importantrating differentiator for life insurers, especially as itrelates to product risk.

Improved ERM means most insurers are now bet-ter prepared for the expected reversal in the creditcycle. For instance, many have repositioned theirportfolios by taking advantage of the relative value ofcorporate credit securities and by increasing theirholdings of higher-grade issues in anticipation of theexpected downgrade in corporate credit.

Factors that will determine ratings trendsShort-term trends in the US life insurance sec-

tor are relatively benign, so it is long-term trendsthat are shaping the ratings environment. For theremainder of 2007 and into 2008, upgrades anddowngrades are likely to be balanced. The deter-mining factors in rating trends over the long termwill be the strength and sustainability of a compa-ny’s competitive position and its operating perfor-mance, especially with regard to using ERMcapabilities to manage emerging product risk andthe impending negative credit cycle.

Life insurers that can optimize advantages in dis-tribution, product innovation, and risk managementwill see their fortunes increase. Those that lackthese key strengths will see their competitive andcapitalization positions increasingly compromised. Insuch a challenging environment, prudent ERM will beall the more important to assuring long-term stabili-ty and financial strength in the face of another diffi-cult business cycle. ■

— Kevin Ahern Credit Ratings Analyst, Life Insurance

SEP

TEM

BER

13,

200

7 /

INS

UR

AN

CE:

LIF

E &

HEA

LTH

IN

DU

STR

Y S

UR

VEY

8

The TRIA extension raised the property-casualty industry’s retention level from 15% to17.5% in 2006 and to 20% in 2007. The newlaw also raised the program trigger from $5million in insured losses to $50 million in in-sured losses in 2006 and $100 million in 2007.

The Bush administration, along withsome prominent members of Congress, hadopposed the reauthorization of TRIA un-less it was significantly scaled back. Somein Congress argued that private industry —not the US government — ultimately bearsthe burden of insuring terrorist risks. Someindustry groups remain skeptical thatenough private capital could be raised tocover terrorism risk, while others believethat, in the wake of Hurricane Katrina inSeptember 2005, the reinsurance industryhas become much more risk-averse andwill not step up to provide protection with-out some form of federal guarantees.

Life settlement segment drawsscrutiny

On March 8, 2006, National FinancialPartners Corp. stated in its 10-K that it re-ceived a subpoena from the office of NewYork Attorney General Eliot Spitzer, “seek-ing information regarding life settlementtransactions.” It was unclear, from the in-formation given, the exact nature of thesubpoena. Although no direct action hasbeen taken on National Financial Partnersto date, on October 26, 2006, Spitzer fileda civil complaint in State Supreme Court inManhattan alleging that Coventry FirstLLC, a provider of life settlements based inPhiladelphia, Pennsylvania, made secretpayments, dubbed “co-brokering fees,” tolife settlement brokers. The suit allegesthat, in exchange for these payments, thebrokers suppressed competitive bids fromother life settlement companies.

Life settlements, also known as viaticalsettlements in some instances, have been aslowly growing and evolving segment of theUS life insurance industry since the mid-1980s. At that time, the spread of acquiredimmunodeficiency syndrome (AIDS) helpedto create a market of terminally ill individu-als with short life expectancies looking toliquidate their life insurance policies beforedeath. This practice got a bad name in the1990s, when a number of firms were accused

of taking unfair advantage of the infirm.While the initial focus of the life settlementsegment was the terminally ill, the practicehas expanded and now includes purchases oflife insurance policies held by older individu-als with longer life expectancies.

As the segment has evolved, new intermedi-aries have developed as well. Viatical settle-ment brokers negotiate among competingsettlement companies on behalf of the insured.State regulation of the life settlement segmenthas slowly evolved in parallel, following nu-merous reports of unethical and fraudulentpractices within the segment. Many viatical set-tlement providers also have been hurt by drugtreatment breakthroughs that have extendedthe lifetimes of some terminally ill patients be-yond initial assumptions. ■

The US life insurance industry is large, rela-tively mature, and led by a number of big,well-known companies. Based on data fromindustry group the National Association ofInsurance Commissioners, via Highline DataLLC, the life and health insurance industry’sassets totaled $4.7 trillion at December 31,2006, with a three-year compound annualgrowth rate (CAGR) of 7.5%; the industry’scapital and surplus reached $253 billion atthat date, with a three-year CAGR of 4.2%.

According to the data from the NationalAssociation of Insurance Commissioners, to-tal premiums and annuity considerations forthe life and health industry totaled $584 bil-lion in 2006, or roughly 4.4% of US grossdomestic product, compared to 4.2% in 2005.Life insurance in force in the United States atyear-end 2006 reached $34.3 trillion, up 6.0%from $32.3 trillion a year earlier, and up

36.4% over the previous five years. (Life insur-ance in force is the aggregate face value of in-surers’ portfolios. Ongoing changes in theuniverse of companies and certain restatementsmean that year-to-year numbers may not al-ways be strictly comparable.)

We estimate that there were roughly onethousand life insurance companies operatingin the United States during 2006. However,the 20 largest life insurance companies ac-counted for nearly 73% of the industry’s totaladmitted assets as of year-end 2006. In addi-tion, according to A.M. Best Co., a globalinsurance-rating and information agency, the10 largest life insurance groups accounted formore than 51% of the industry’s admitted as-sets as of year-end 2006. The country’s threelargest insurance groups — MetLife, Inc., Pru-dential Financial, Inc., and American Interna-tional Group, Inc. — accounted for more than24% of total admitted assets.

INDUSTRY TRENDS

Although the percentage of the US popu-lation covered by life insurance has beentrending downward overall since the 1970s,the face amount of life in force has grownsteadily. According to the American Councilof Life Insurers (ACLI), an industry trade as-sociation, individual life insurance protectionin the United States totaled $10.0 trillion atthe end of 2005, and it had grown at an av-erage annual rate of 5.5% since 1995. Thesame study indicated that the average size ofa new individual life policy increased to$158,000 in 2005 up from $83,000 in 1995.The number of individual policies purchasedfell 1% in 2005. According to LIMRA Inter-national, a trade group, 68% of US adultsare covered by life insurance, about the sameas 20 years ago. Furthermore, 44% of all UShouseholds either don’t own life insurance

INDUSTRY PROFILE

Large, well-known companiesdominate a mature industry

SEP

TEM

BER

13,

200

7 /

INS

UR

AN

CE:

LIF

E &

HEA

LTH

IN

DU

STR

Y S

UR

VEY

9

TOP 20 LIFE-HEALTH COMPANIES — 2006(Ranked by year-end assets)

ASSETSCOMPANY (MIL. $)

1. Metropolitan Life 445,926 2. Prudential of America 368,595 3. AIG Life 350,283 4. Hartford Life 238,475 5. Manulife 200,789 6. TIAA Group 186,565 7. AEGON USA 178,702 8. New York Life 178,471 9. ING USA Life 173,421

10. AXA Financial Group 148,682 11. Northwestern Mutual 145,121 12. Lincoln Financial 144,166 13. Principal Life Insurance 125,532 14. MassMutual Financial Group 122,180 15. Nationwide Life Group 110,869 16. Allstate Financial 91,004 17. Pacific Life 87,629 18. Ameriprise Financial Group 79,109 19. Jackson National Group 69,407 20. Genworth Financial Group 69,049

Source: A.M. Best.

SEP

TEM

BER

13,

200

7 /

INS

UR

AN

CE:

LIF

E &

HEA

LTH

IN

DU

STR

Y S

UR

VEY

10

and believe they should, or do own life insur-ance and believe they need more. Amongthose that already own some life insurance,40% believe they do not have enough.

Changing demographics create newopportunities

The forces shaping the life insurance in-dustry today stem from a number of demo-graphic changes, as well as from structuralchanges within the financial services market-place. According to the US Census Bureau,the segment of the general population of re-tirement age (aged 65 or older) is expected toincrease from 12.4% in 2000 to 13.0% in2010, 16.3% in 2020, and 19.6% in 2030.Conversely, while the segment of working-aged people (ages 20 to 64) in the generalpopulation is expected to increase from59.0% in 2000 to 60.0% in 2010, the per-centage is then projected to decrease sharplyto 57.2% in 2020 and 54.2% in 2030.

The overall aging of the population isturning insurers’ attention gradually awayfrom income-protection financial productstowards retirement-oriented financial prod-ucts. In addition, increasing longevity is alsohaving an influence on insurers, as longer

lives will bolster the need for greater retire-ment wealth. For more traditional life insur-ance products, rising longevity has helped toreduce mortality rates, which can aid insurerprofitability in these product lines.

Mortality tables revisedIn 2004, a new set of mortality tables,

CSO 2001, was adopted by a majority ofstates and became the prevailing mortalitytables used by the Internal Revenue Serviceand the life insurance industry, replacing thedecades-old CSO 1980 set of tables. Mortali-ty rates under the new tables are expected toimprove for most population classes, general-ly leading to lower reserving requirements. Inaddition, the maximum age under the tableswill extend from 100 years to 120 years.

Through 2009, the National Associationof Insurance Commissioners (NAIC), an or-ganization of insurance regulators, is allow-ing insurance companies to implement thetables in states where it has been adopted.The new mortality tables, which are used forproduct reserving, apply only to new sales oflife insurance products. Given the lower re-serve requirements and changes in actuarialassumptions, the revisions could affect pre-mium levels, product guarantees, cash values,and the need for reinsurance.

Baby boomers generate new demands...Longer life expectancies and concerns

about the financial safety net of Social Secu-rity have given baby boomers a heightenedawareness of the need to save for retirement.(Baby boomers are the approximately 77million Americans born between 1946 and1964.) Moreover, a shift in pension trends —from defined benefit plans to defined contri-bution plans, such as 401(k) plans — hasgiven many Americans a greater sense of fi-nancial empowerment. Standard & Poor’sbelieves variable annuities will also play animportant role in meeting the retirementneeds of baby boomers.

Many people now use technology, such asthe Internet, to filter the vast array of infor-mation available to them as they plan theirfinancial futures. Furthermore, the break-down of the barriers that once separated thevarious sectors of the financial services in-dustry is having an effect on consumer be-havior. Banks and brokerage houses now sellmore annuities than do life insurance agents.

TOP 20 WRITERS OF INDIVIDUAL ANNUITIES — 2006(Ranked by net premiums written)

PREMIUMSCOMPANY (MIL. $)

1. Metropolitan Group 16,537 2. Hartford Fire and Casualty 13,330 3. American International 12,508 4. Lincoln National 11,370 5. Ameriprise Financial Group 10,346 6. Allianz Insurance 10,219 7. Pacific Life Ins 8,713 8. Jackson National 8,548 9. TIAA Group 7,201

10. Prudential of America 6,229 11. New York Life 6,213 12. ING America 5,812 13. Nationwide Corporation 5,258 14. Allstate Insurance 5,170 15. Genworth Financial Group 3,841 16. AXA Financial 3,770 17. AEGON USA 3,527 18. Aviva Group 2,836 19. John Hancock 2,579 20. Principal Financial 2,401

Source: National Association of Insurance Commissioners,via Highline Data, LLC

SEP

TEM

BER

13,

200

7 /

INS

UR

AN

CE:

LIF

E &

HEA

LTH

IN

DU

STR

Y S

UR

VEY

11

Life insurance agents, in turn, now sellinvestment-oriented products, includingmutual funds. These factors have greatlychanged the selling process and probably willcontinue to chip away at the old maxim that“life insurance is sold, not bought.”

...and the industry respondsAlthough life insurance remains a mature,

relatively slow-growth business, new challengeshave sparked some dynamic changes in the in-dustry. Many insurers have undertaken majorrestructuring programs in an attempt to re-shape their market image. A number of insur-ers have launched aggressive variable annuitysales programs and new wealth product guar-antees in an effort to ramp up growth; this fol-lows several years of declining equity markets(following the technology bubble), whichdampened enthusiasm for equity-linked prod-ucts, such as variable annuities and variablelife. Insurers also are refining their risk man-agement, borrowing techniques that have beenpopular in the banking industry for spread-based products, such as fixed annuities.

While consumer acceptance for new prod-uct guarantees, such as guaranteed minimumwithdrawal and income benefits, has beenencouraging, the new features are not with-out their downsides. Most insurers use com-plex market-hedging strategies for theguarantees that can be difficult and expen-sive to implement. Since the guarantees arerelatively new, most insurers do not havemuch historical data on which to rely whenpricing these features. Furthermore, the lackof historical data and an incomplete under-standing of the risks associated with theguarantees have resulted in a scarcity of rein-surance for these new product features. In-surers also must contend with recent andpending accounting changes that require in-surers to post reserves for new componentsof their wealth products. Accordingly, Stan-dard & Poor’s believes that insurers likelywill continue to reassess and reengineer theirwealth products to meet consumer needs andnew regulatory challenges.

Distribution channels have beenshifting

Faced with growing competition from otherfinancial services firms and the imperative toboost revenue growth and profit margins,

many insurers have reevaluated their distribu-tion channels and are revamping the way theydeliver products to consumers. In particular,banks and other financial services firms havegenerated an increasing share of insuranceproduct sales, especially for annuities.

Historically, life insurers were essentiallythe sole source of life insurance products andprospered by selling policies through anagency system. Establishing an agency net-work was costly, but necessary; the conven-tional wisdom was that life insurance wassold, not bought; and consumers had to beeducated on products and convinced thatthey needed life insurance. Today, the repealof the Glass-Steagall Act has allowed otherfinancial services firms, such as banks andbrokerages, to offer insurance products.Many have widespread and efficient distribu-tion networks through their branch systemsor broker networks. Moreover, these distrib-utors have recognized that most life insur-ance is a commodity, and, as such, it must bemarketed primarily on price. Therefore,those companies that deliver these productsto consumers in the most cost-effective man-ner will thrive in the long term.

Work site marketing gaining importanceWork site marketing is the process where-

by an insurer offers its products or servicesto employees at their place of work. Typical-ly, these solicitations are made via the clientcompany’s Web site and/or through directmailings sent to employees, either at theirhome or office. Direct, face-to-face solicita-tion of employees is not typical in this kindof situation; however, follow-up contacts —either to administer a policy or conduct pre-screening tests — are possible.

A broad array of products is offered, includ-ing homeowners’ and auto insurance, dentalcoverage, long-term care, and supplemental lifeinsurance. Savings and retirement products alsomay be offered. According to a MetLife surveycommissioned in 2005, 40% of all employeespurchase more financial products (e.g., insur-ance, mortgages, long-term care insurance, 529plans, and securities) through the workplacethan outside of work.

For the client company, this kind of mar-keting enables it to “offer” these choices toits employees. There is an appearance of anenhanced benefit package without addedbenefit costs for the employer. By offering

SEP

TEM

BER

13,

200

7 /

INS

UR

AN

CE:

LIF

E &

HEA

LTH

IN

DU

STR

Y S

UR

VEY

12

these services, the employer also is able tohelp its employees to juggle work/life issues.For the employee, there is an element of con-venience with being able to purchase theseproducts and services at work, often withoutsitting through a presentation by an insur-ance sales representative. Moreover, there isan implied endorsement being provided bythe client company that may give the em-ployee an added sense of comfort. In essence,some of the screening has already been done.

For insurance companies, this kind ofmarketing is a very productive use of re-sources. Marketing through this channel of-fers an insurer the potential to achieve quickeconomies of scale and, in some cases, a fa-vorable mix of underwriting risk by insuring(presumably) younger, healthier workers.

M&A activity focuses on scale andscope

The US life insurance industry has beenin a period of consolidation since the1990s. According to the ACLI, the numberof US life insurers operating in the UnitedStates peaked at 2,343 in 1988. At year-end 2005, there were only 1,119 US life in-surers, down from 1,650 at the end of1995 — a 10-year compound annual de-cline of 3.8%. Standard & Poor’s believesthat, in the long term, consolidation in thelife insurance industry will continue to bedriven by the need to offset slowing rev-enue growth, compete in a converging fi-nancial services marketplace, cut costs, andachieve economies of scale.

During 2005, a stable economic environ-ment, stronger balance sheets, and an increasedappetite for growth helped fuel further mergerand acquisition (M&A) activity in the life in-surance sector. According to data obtainedfrom SNL Securities, a financial services orga-nization, 28 deals — valued at a total of $21.8billion — were announced in the life insurancesector in 2005. This contrasted sharply withthe M&A environment that existed in 2004,when 31 deals valued at $3.5 billion wereannounced. Results in 2005 were affectedby several large transactions, includingMetLife’s acquisition (in January 2005) ofTravelers Life & Annuity, valued at $11.5billion, and Lincoln National Corp.’s ac-quisition (in October 2005) of Jefferson-Pilot, valued at $7.6 billion. In 2003, the

overall level of M&A activity included 35deals valued at $14.5 billion. (For more infor-mation on current M&A trends, see the “Cur-rent Environment” section of this Survey.)

Standard & Poor’s expects this pace oftransactions to continue. The significant num-ber of smaller life insurance companies pro-vides numerous M&A candidates for the largerinsurance companies. Furthermore, many in-surers are reassessing their current businessmix, with some choosing to sell off smallerlines or underperforming books of business inan effort to improve profits and focus on theircore competencies. Indeed, a fair amount ofM&A activity going forward may be in theform of restructurings: companies selling offparts of their operations that no longer fit withtheir long-term strategic initiatives.

Standard & Poor’s believes that many lifeinsurance companies will acquire smallercompanies or blocks of businesses to im-prove their scale and scope. Some firms aregrowing almost entirely through acquisitions,figuring that it is more cost-efficient to ac-quire blocks of existing in-force policies thanto build critical mass through a start-up ef-fort. Other buyers are looking to offset slow-er growth in their core business with newlines, such as retirement savings, to expanddistribution or gain a presence in the USmarketplace, or simply to acquire a franchiseor brand that increases their overall presencein the marketplace.

The demutualization trend takes apause

Today, most of the major life insurancecarriers that were mutually owned have al-ready demutualized (converted to stockhold-er ownership). The few notable exceptionsinclude Massachusetts Mutual Life InsuranceCo., New York Life Insurance Co., and theNorthwestern Mutual Life Insurance Co.Mutual insurance companies are owned bytheir policyholders, so their main focus is toprovide low-cost policies and high-qualityservice to their policyholder owners. In con-trast, stockholder-owned insurance compa-nies must juggle the often-conflictinginterests of their policyholder clients andshareholder owners.

According to the ACLI, there were only135 mutual life insurers doing business in theUnited States during 2005, down from 228

SEP

TEM

BER

13,

200

7 /

INS

UR

AN

CE:

LIF

E &

HEA

LTH

IN

DU

STR

Y S

UR

VEY

13

in 1995. Furthermore, according to A.M.Best’s Aggregates & Averages, mutual com-panies accounted for only 16% of the lifeinsurance industry’s admitted assets in 2005,down from 39% in 1995. Previously, two ofthe largest life insurers in the United States —Prudential Financial Inc. and MetLife — wereboth mutual life insurers. MetLife demutual-ized in April 2000, and Prudential completedits demutualization in late December 2001.Other notable demutualizations occurringaround the same time included John Han-cock, Principal Financial Group Inc., and thePhoenix Companies Inc.

Insurers involved in the last round of de-mutualizations benefited from a rising stockmarket that permitted companies to raisecapital at a favorable price, while also pro-viding management with a publicly tradedstock that could be used for currency in fu-ture acquisitions. Both prospects were partic-ularly appealing to mutual insurers, whofaced new competitive threats and opportu-nities following repeal of the Glass-SteagallAct and believed that stock ownership wouldallow them the flexibility to adapt and profitin this new environment.

Of course, transformation to stockholder-owned status does not happen overnight.Prudential’s demutualization process took al-most four years from the time the companyfirst announced its intention to convert tothe completion of its initial public stock of-fering. Central to the process are regulatoryapprovals and the arduous task of estimatingwhat the policyholders’ shares are worth.Typically, policyholders are offered the op-tion of exchanging their interest for cash,stock in the new company, or an increasedlevel of insurance benefits.

M&A could spur sponsored demutualizationsMany of the remaining mutual insurers

are currently generating healthy levels of cap-ital through their internal operations. Withthe passage of the Sarbanes-Oxley Act of2002, which requires additional and costlyoverhead expenses for those mutual compa-nies choosing to demutualize and issue apublic stock, Standard & Poor’s believes thatthe next wave of demutualization could bedifferent and may take the form of spon-sored demutualizations.

A sponsored demutualization is a processof demutualization under which a mutual in-

surer converts to a stock company ownershipstructure in order to be acquired by anotherstockholder-owned company. For example,in September 2002, shareholders of Nation-wide Financial Services Inc., a diversified in-surer and financial services firm based inColumbus, Ohio, approved a plan underwhich Nationwide would acquire ProvidentMutual Life Insurance Co., of Berwyn, Penn-sylvania, for about $1.5 billion. As part ofthe transaction, Provident simultaneouslyconverted to a stockholder-owned company.Nationwide completed its sponsored demutu-alization of Provident on October 1, 2002.

Despite its attractions, demutualizing isnot a panacea. While it affords the insureraccess to capital markets, demutualizationcan lead to complications. After operating ina mutual environment, where the goals ofthe insurer are to serve only the needs of pol-icyholders, many mutual insurance execu-tives may be ill prepared for the heightenedscrutiny and proactive ownership base of astockholder-based company. In addition, thestock market constantly grades the financialperformance of publicly owned insurers andexacts a heavy toll from stock prices of com-panies that do not perform up to par.

Capital market activity may slow

Life insurers have extremely large invest-ment portfolios that can be affected by large-scale bankruptcy or credit downgrades.Despite the credit issues experienced by FordMotor Co. and General Motors Corp. in2005 and 2006, most life insurers were re-porting favorable bond credit trends andrenewed balance sheet strength. Moreover,80% of all life companies rated by Stan-dard & Poor’s had a stable outlook as ofMay 2007. Standard & Poor’s believes thatmost publicly traded life insurance compa-nies will have little need to raise additionalfunds in the capital markets in order tomaintain their financial strength ratings. Infact, many life insurance companies havebeen building excess capital. The averagerisk-based capital (RBC) ratio increased to409% in 2005, compared to 290% in 1997.As calculated by the National Association ofInsurance Commissioners model law, theRBC ratio measures the minimum amount ofcapital an insurance company needs to pre-vent triggering regulatory action.

SEP

TEM

BER

13,

200

7 /

INS

UR

AN

CE:

LIF

E &

HEA

LTH

IN

DU

STR

Y S

UR

VEY

14

Standard & Poor’s expects many pub-licly traded life insurance companies tocontinue raising dividends and buying backstock. Excess capital may also be used topay for strategic acquisitions. These com-panies’ strong internal cash flow will alsosupport a prudent, measured approach togrowing the business internally. However,as guarantee features for wealth productscontinue to evolve, some life insurers maydecide to access the capital markets andraise reserves for these guarantees, espe-cially given the lack of adequate reinsur-ance for many of these features.

Legislative changes impact wealthproducts

On August 17, 2006, President Bushsigned the Pension Protection Act of 2006.One of the key provisions of the new law isthat new employees are automatically en-rolled in the company’s 401(k) plan, whichwill help young employees get an early starton saving for retirement. Standard & Poor’sbelieves that the bill’s automatic provisionwill increase 401(k) participation rates andact as a boon to companies that provide re-tirement benefits. In addition, the new lawallows annuities to be an investment optionin a company’s 401(k) plan. The bill also al-lows investment providers to offer profes-

sional investment advice to plan participants.The bill further codifies the tax-free treat-ment of death benefits and codifies insuranceindustry “best practices” relating to the useof company-owned life insurance (COLI).COLI is an insurance product used by em-ployers both to protect against the financialcost of losing a key employee and to providemeans to fund employee and retiree benefits.

Life insurers often have sold survivor-ship or “second-to-die” life insurance poli-cies to be used in estate planning purposesfor the payment of estate taxes. In 2001,President Bush signed into law the Eco-nomic Growth and Tax Relief Reconcilia-tion Act (EGTRRA), which, among otherthings, increased federal tax deductions formany retirement savings plans, includingindividual retirement accounts (IRAs) and401(k) plans, and reduced or repealed fed-eral estate taxes from 2001 to 2010. As aresult of this new legislation, the demandfor survivorship policies may have de-creased, and IRA and 401(k) accountscould accept additional funds that other-wise might be invested in tax-advantagedwealth products offered by life insurers,such as annuities.

In 2003, President Bush signed into law theJobs and Growth Tax Relief Reconciliation Act(JGTRRA), which, among other things, cut thefederal income tax rate on stock dividends andcapital gains. This increased the attractivenessof common stock for income-oriented in-vestors, providing additional competition forlife insurance wealth products.

Federal regulation for life productsappears unlikely

For years, life insurance companies havebeen lobbying Congress to give insurers theoption to be regulated at the federal levelrather than the current state regulatoryregime, whereby insurers must work withregulators in each individual state wherethey conduct business. Life insurers claimthat the state regulatory system is morecostly and time-consuming than a proposedfederal system, and that insurers often havedifficulty creating products that can be eas-ily altered to meet the differing require-ments of individual state regulators.Furthermore, they say that banks, whichcan be federally chartered and regulated,

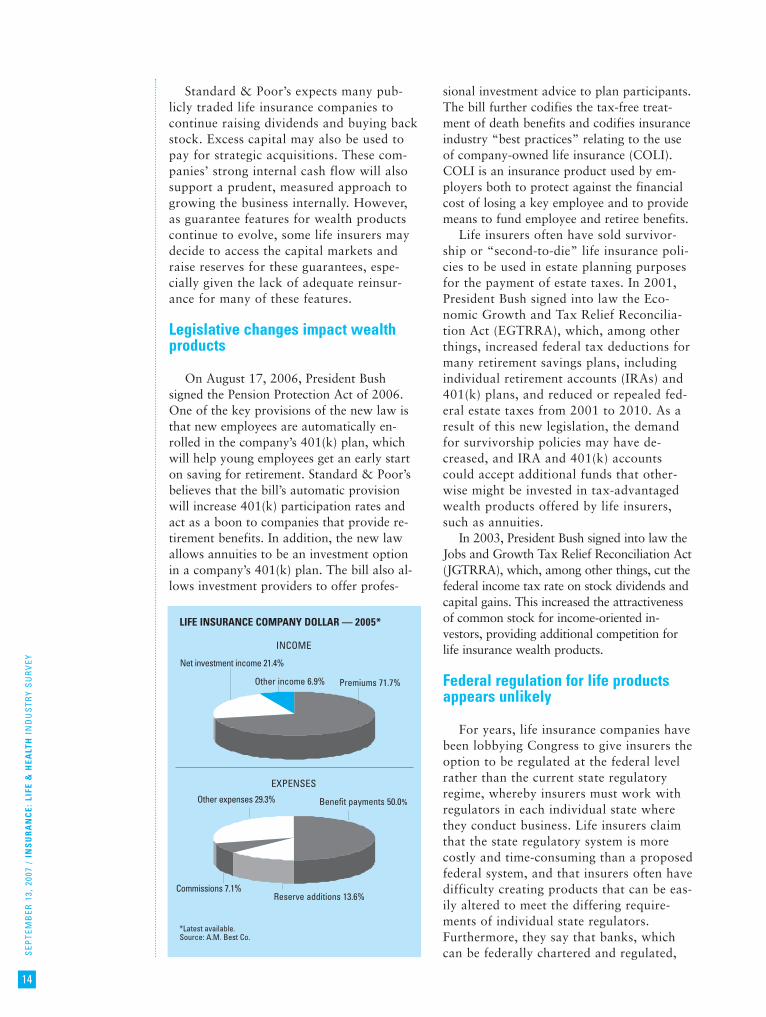

LIFE INSURANCE COMPANY DOLLAR — 2005*

*Latest available.Source: A.M. Best Co.

Reserve additions 13.6%

Net investment income 21.4%

Premiums 71.7% Other income 6.9%

Benefit payments 50.0%Other expenses 29.3%

INCOME

EXPENSES

Commissions 7.1%

SEP

TEM

BER

13,

200

7 /

INS

UR

AN

CE:

LIF

E &

HEA

LTH

IN

DU

STR

Y S

UR

VEY

15

do not have to deal with individual stateregulators — and thus have an unfair com-petitive advantage. According to a studyconducted in 2004 by the ACLI and con-sulting firm Computer Sciences Corp., asingle federal regulatory regime would re-duce the cost of regulation by more than$2.5 billion annually.

Standard & Poor’s believes that federal reg-ulation for life insurers is unlikely in the nearfuture. One problem is that many property-casualty insurance associations are lobbyingnot for federal regulation, but for better stateregulation. These insurance associations con-tend that, because property-casualty coverageneeds can vary from state to state, the currentregulatory system is more appropriate.

The National Association of Mutual In-surance Companies, the National Associationof Professional Insurance Agents, and the In-dependent Insurance Agents and Brokers ofAmerica are among the associations thatoppose the plan. State regulators and con-sumer groups also do not support a federalregulatory framework.

HOW THE INDUSTRY OPERATES

The life insurance industry is being trans-formed by ongoing competitive pressure frombanks and other financial intermediaries, aswell as by regulation changes. In the past, lifeinsurers provided only one thing: financial re-muneration in the event of a policyholder’sdeath. Today, they provide an array of financialproducts and play an integral role in manypeople’s financial planning, including servicesin such complex areas as tax, retirement, andestate planning.

In its simplest form, however, life insur-ance is still a business of shared risk. Insurerscollect premiums from policyholders, investthose premiums, and share some of that in-come with policyholders (in the form of apolicy dividend or income from an annuity,or through a policy’s cash value). Eventually,insurers give policyholders some sort of fi-nancial reimbursement, either upon the poli-cyholder’s death or when a policy or anannuity matures.

In the following section, we discuss variouskinds of ownership structures, assets, account-ing methods, products, and other key informa-tion pertinent to how the industry operates.

Ownership structures differ

Generally, a life insurance company’s own-ership can take one of two basic forms: that ofa stock insurance company, or that of a mutualinsurance company. In addition, a companycan be structured as a hybrid, known as a mu-tual holding company (MHC).

Stock insurance companiesStock insurance companies, as their name

implies, are owned by shareholders. Theownership capital of a stock insurance com-pany is called shareholders’ equity. Stock in-surance companies that are publicly held arerequired to file quarterly financial reportswith the Securities and Exchange Commis-sion (SEC). As a result, obtaining timely fi-nancial information about these companies isrelatively easy.

Mutual insurance companiesA mutual insurance company is owned by

its policyholders, and its ownership capital iscalled policyholders’ surplus. Because thesecompanies are not publicly held, they are notrequired to disclose financial information tothe SEC. Although mutual insurers provide in-formation to state regulators, and some distrib-ute financial information to policyholders,obtaining timely financial information aboutmutual life insurers can be difficult for analystsand other interested parties.

This used to create problems for those an-alyzing the industry when mutual companiesdominated the upper echelons of the life in-surance industry. However, in the wake ofnumerous high-profile demutualizations —including those by Metropolitan Life Insur-ance Co., Nationwide Financial Services Inc.,and Prudential Financial Inc. — the numberof large mutual companies has declined.Only two of the top 10 US life insurers by ad-mitted assets — TIAA Group and New YorkLife Group — were mutual companies at theend of 2005, according to the latest figuresfrom A.M. Best Co., a global insurance-ratingand information agency.

Mutual holding companiesIn some instances, life insurers have

formed Mutual holding companies (MHCs)to combine the benefits of a mutual owner-ship with those of stock ownership. In thiscase, the insurance operations are conducted

SEP

TEM

BER

13,

200

7 /

INS

UR

AN

CE:

LIF

E &

HEA

LTH

IN

DU

STR

Y S

UR

VEY

16

by a stock company formally owned by theholding company, which in turn remains incontrol of the policyholders.

A benefit to this ownership structure is thatshares in the life insurance subsidiary can besold to the public to raise capital for expansionor for use as currency for acquisitions. Howev-er, such an arrangement may lead to conflictingpriorities as management seeks to please poli-cyholders, who prefer that the company remainfiscally sound and able to pay benefits, whilealso trying to satisfy outside shareholders, whoprefer growth and dividends. As a result, manyinsurers looking to demutualize have opted forfull demutualization, which is a more stream-lined process than a partial demutualization.

Types of assets

There are three main ways of classifyingthe assets owned by life insurance compa-nies: admitted assets, separate account assets,and troublesome assets.

Admitted assetsAdmitted assets are those assets that state

insurance regulators include when determin-ing an insurer’s financial condition or abilityto pay policyholders’ claims. Accordingly,they are usually those with a high degree ofliquidity or that can be easily converted intocash. Items such as office equipment andpast-due accounts receivable are examples ofassets that would be excluded from an insur-er’s tally of admitted assets.

In order to maintain an adequate financialcondition, life insurers keep the vast majorityof their assets in higher-quality investments

with a high degree of liquidity. As a result,invested assets constitute the largest portionof an insurer’s asset base. Invested assets ofthe life insurance industry equaled about$2.9 trillion at December 31, 2005, or morethan 64% of total admitted assets. This fig-ure showed a 3.6% increase from year-end2004 invested assets and a 7.4% five-yearcompound annual growth rate (CAGR). Incomparison, the five-year CAGR for admit-ted assets was 6.6%.

Because life insurance products are generallylong-term in nature, most of life insurers’ in-vested assets have longer maturities and arehigher yielding, such as multiyear bonds andloans. Of the invested asset total at year-end2005, bonds constituted 77%, followed bymortgage loans and real estate (11%), contractloans (4%), stock (3%), and cash and short-term investments (2%). The remaining 3% wasin other kinds of investments.

Separate account assetsAs their name implies, separate account as-

sets are held apart from other assets in the in-surer’s investment portfolio. These accounts areestablished by insurers primarily to fund cer-tain annuity and investment-oriented life insur-ance accounts where the policyholder orannuity holder (annuitant) directs the invest-ment process and bears most of the investmentrisk. By segregating these assets, an insurer isnot restricted by state laws that mandate howthe assets in an insurer’s general account areinvested. As a result, a particular insurer’sseparate account portfolio may be over-weighted with common stocks or real estatecompared with the overall industry standard.

Since they first came into existence in the1960s (when life insurers used them to fundpension accounts), separate account assets havegrown more rapidly than the overall life insur-ance industry’s total admitted assets. Accordingto statistics from A.M. Best, the CAGR for lifeinsurers’ separate account assets was 17.7%for the period from 1985 to 1995, versus9.7% for total admitted assets. However, withthe bear stock market from 2001 to 2003, thefive-year CAGR for separate accounts from1999 to 2003 slowed to 5.0%. For insurers,there has been a tradeoff for the rapid growthof separate account products: namely, a nar-rowing of profit margins, because most of theupside potential from these investments ispassed along to the consumer.

DISTRIBUTION OF ASSETS — 2005*

*Latest available.Source: A.M. Best Co.

US government bonds 3.3%

Special revenue bonds 6.7%

Other bonds 11.2%

Common stocks 1.6%Preferred stocks 0.8%

Mortgages & real estate 6.8%

Other assets 8.5 %

Industrial bonds 28.1%Separate account

assets 33.0%

SEP

TEM

BER

13,

200

7 /

INS

UR

AN

CE:

LIF

E &

HEA

LTH

IN

DU

STR

Y S

UR

VEY

17

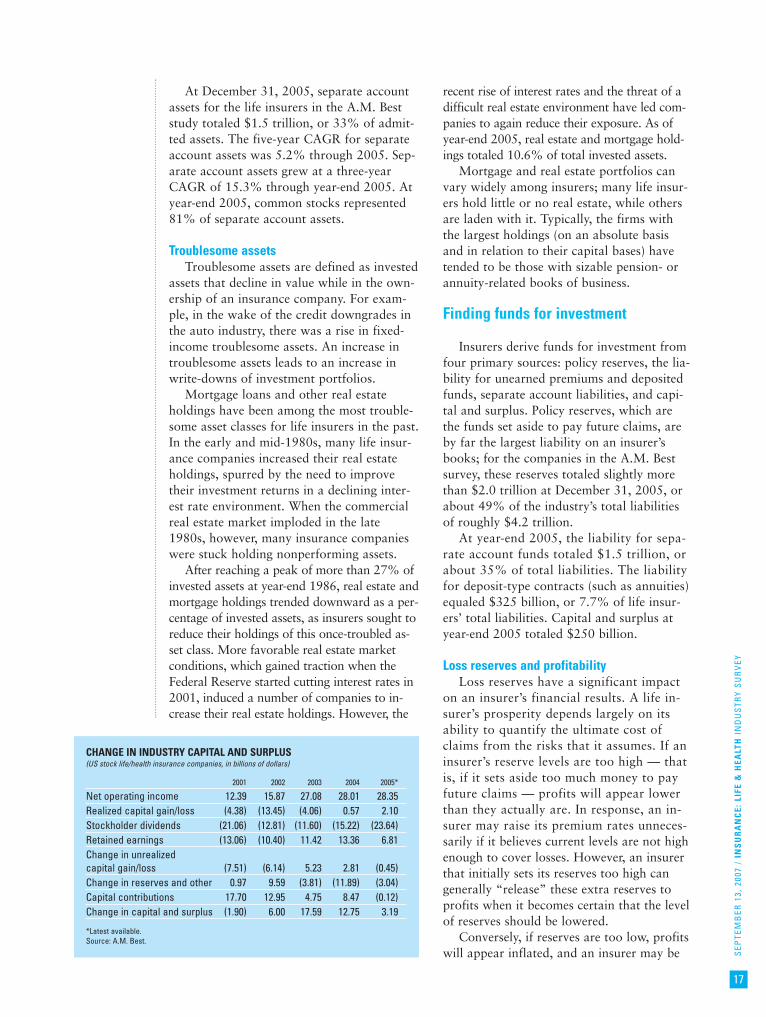

At December 31, 2005, separate accountassets for the life insurers in the A.M. Beststudy totaled $1.5 trillion, or 33% of admit-ted assets. The five-year CAGR for separateaccount assets was 5.2% through 2005. Sep-arate account assets grew at a three-yearCAGR of 15.3% through year-end 2005. Atyear-end 2005, common stocks represented81% of separate account assets.

Troublesome assetsTroublesome assets are defined as invested

assets that decline in value while in the own-ership of an insurance company. For exam-ple, in the wake of the credit downgrades inthe auto industry, there was a rise in fixed-income troublesome assets. An increase introublesome assets leads to an increase inwrite-downs of investment portfolios.

Mortgage loans and other real estateholdings have been among the most trouble-some asset classes for life insurers in the past.In the early and mid-1980s, many life insur-ance companies increased their real estateholdings, spurred by the need to improvetheir investment returns in a declining inter-est rate environment. When the commercialreal estate market imploded in the late1980s, however, many insurance companieswere stuck holding nonperforming assets.

After reaching a peak of more than 27% ofinvested assets at year-end 1986, real estate andmortgage holdings trended downward as a per-centage of invested assets, as insurers sought toreduce their holdings of this once-troubled as-set class. More favorable real estate marketconditions, which gained traction when theFederal Reserve started cutting interest rates in2001, induced a number of companies to in-crease their real estate holdings. However, the

recent rise of interest rates and the threat of adifficult real estate environment have led com-panies to again reduce their exposure. As ofyear-end 2005, real estate and mortgage hold-ings totaled 10.6% of total invested assets.

Mortgage and real estate portfolios canvary widely among insurers; many life insur-ers hold little or no real estate, while othersare laden with it. Typically, the firms withthe largest holdings (on an absolute basisand in relation to their capital bases) havetended to be those with sizable pension- orannuity-related books of business.

Finding funds for investment

Insurers derive funds for investment fromfour primary sources: policy reserves, the lia-bility for unearned premiums and depositedfunds, separate account liabilities, and capi-tal and surplus. Policy reserves, which arethe funds set aside to pay future claims, areby far the largest liability on an insurer’sbooks; for the companies in the A.M. Bestsurvey, these reserves totaled slightly morethan $2.0 trillion at December 31, 2005, orabout 49% of the industry’s total liabilitiesof roughly $4.2 trillion.

At year-end 2005, the liability for sepa-rate account funds totaled $1.5 trillion, orabout 35% of total liabilities. The liabilityfor deposit-type contracts (such as annuities)equaled $325 billion, or 7.7% of life insur-ers’ total liabilities. Capital and surplus atyear-end 2005 totaled $250 billion.

Loss reserves and profitabilityLoss reserves have a significant impact

on an insurer’s financial results. A life in-surer’s prosperity depends largely on itsability to quantify the ultimate cost ofclaims from the risks that it assumes. If aninsurer’s reserve levels are too high — thatis, if it sets aside too much money to payfuture claims — profits will appear lowerthan they actually are. In response, an in-surer may raise its premium rates unneces-sarily if it believes current levels are not highenough to cover losses. However, an insurerthat initially sets its reserves too high cangenerally “release” these extra reserves toprofits when it becomes certain that the levelof reserves should be lowered.

Conversely, if reserves are too low, profitswill appear inflated, and an insurer may be

CHANGE IN INDUSTRY CAPITAL AND SURPLUS(US stock life/health insurance companies, in billions of dollars)

2001 2002 2003 2004 2005*

Net operating income 12.39 15.87 27.08 28.01 28.35 Realized capital gain/loss (4.38) (13.45) (4.06) 0.57 2.10 Stockholder dividends (21.06) (12.81) (11.60) (15.22) (23.64)Retained earnings (13.06) (10.40) 11.42 13.36 6.81 Change in unrealized capital gain/loss (7.51) (6.14) 5.23 2.81 (0.45)Change in reserves and other 0.97 9.59 (3.81) (11.89) (3.04)Capital contributions 17.70 12.95 4.75 8.47 (0.12)Change in capital and surplus (1.90) 6.00 17.59 12.75 3.19

*Latest available.Source: A.M. Best.

SEP

TEM

BER

13,

200

7 /

INS

UR

AN

CE:

LIF

E &

HEA

LTH

IN

DU

STR

Y S

UR

VEY

18

inclined to lower its rates. Moreover, inaccu-rate reserve levels ultimately will have to beadjusted once losses develop. These account-ing adjustments may make the insurer’s fi-nancial position seem erratic and unstable.Reserving for losses and setting premium lev-els involve estimating the ultimate value offuture claims. This actuarial process, howev-er, is extremely difficult. Forecasts of futurelosses are subject to a number of variables,including but not limited to mortality rates,real economic growth, inflation, interestrates, lapse rates, and sociopolitical events,including judicial rulings.

Two accounting methods

Many insurers report their financial re-sults using two kinds of accounting princi-ples. For results submitted to regulators,insurers use statutory accounting principles(SAP). For results given to investors, they usegenerally accepted accounting principles(GAAP). However, many financial analystsalso use SAP financial statements when eval-uating an insurer.

The primary difference between the twoaccounting systems lies in a concept knownas the matching principle. Under GAAP, ex-penses are charged (matched) to the periodin which they were used to generate revenuesand provide services, also known as accrual-based accounting. Under SAP, expenses arerecognized as incurred, also known as cash-based accounting.

This means that, under SAP, expenses as-sociated with writing an insurance policy —such as commissions and other underwritingexpenses — are immediately expensed anddeducted from income. Under GAAP, thesesame costs are treated as assets (referred toas a policy’s deferred acquisition costs, orDAC) and are amortized as expenses overthe insurance policy’s life, which is the periodover which the insurer provides its servicesto the policyholder. Since a policyholder canchoose to terminate a policy at a future date,the insurer must estimate (for DAC amorti-zation purposes) lapse rates and the lifetimeof a policy. Changes in these estimates cancause an insurer to accelerate or decelerateDAC amortization over time.