sound currency: the czech experience - cnb.cz · pdf filesinger – czech republic: can...

TRANSCRIPT

M. Singer – Sound currency: The Czech experience 1M. Singer – Sound money: Czech experience 1M. Singer – Czech Republic: Current Situation and Outlook 1M. Singer – Inside or Outside the Euro Area 1M. Singer – Recent Developments in the Czech Economy, Risks and Outlook 1M. Singer – Macroeconomic developments, monetary policy and financial sector 1M. Singer – The Czech economy and crisis in Eurozone: CNB view 1M. Singer – Czech economy and development in Europe: Outlook and Challenges 1M. Singer – Czech Republic: Can record low rates be sustained? 1M. Singer – Czech Republic: Future challenges and opportunities 1M. Singer – Present Conditions, Monetary Policy and Outlook in Czech Republic 1M. Singer - Czech Republic: Staying Ahead of the Curve with Regard to Monetary Policy 1M. Singer: The economic and financial crisis from the point of view of the Czech banks 1M. Singer: Financial Crisis: Impacts on the CR and Lessons for the Supervisors 1M. Singer: Financial Crisis: Likely Impacts on the CR and Lessons for the SupervisorsM. Singer: Present Conditions, Monetary Policy and Outlook for CR 1M. Singer: Consumer protection in financial services: CNB approach 1

Sound Sound currencycurrency: : The Czech experienceThe Czech experience

Mont Pelerin Society for Czech Academia & BusinessPrague, 6 September 2012

MiroslavMiroslav SingerSingerGovernor, Czech National BankGovernor, Czech National Bank

M. Singer – Sound currency: The Czech experience 2

IntroductionIntroduction

•

The Czech economy has experienced four shocks (1990–1993, 1996–1998, 2001–2002 and 2008–2009)

•

Common feature of 1996–1998 and 2001–2002 shocks: mistakes made by main domestic economic policymakers

•

In this presentation, I will focus on twin (currency and banking sector) crisis of 1996–1998 and on assessing present stability of Czech currency

•

Methodological starting point: sound currency is result of:

1) appropriate monetary policy framework

2) correctly implemented macroeconomic policies

3) appropriate regulation and careful supervision of financial sector

M. Singer – Sound currency: The Czech experience 3

•

Strong demand

High wage growth (much higher than productivity growth)

High growth of private and public investment (infrastructure)

Strong credit growth

Strong capital inflow (high interest rate differential) •

Weak supply side

(underdeveloped markets, badly defined property

rights, malfunctioning legal and institutional framework, etc.) Emergence of external imbalance

•

Situation also complicated by errors in main statistical series (GDP, foreign trade, current account) preventing correct assessment of state of Czech economyIn 1996 the overheating proved to be unsustainable: the situation required adjustment and appropriate policy responses

Causes of twin crisis I: Causes of twin crisis I: Macroeconomic developmentsMacroeconomic developments

M. Singer – Sound currency: The Czech experience 4

Real wages and labour productivityReal wages and labour productivity

The wage-productivity mismatch peaked in 1995 (at 12 pp) and was still significant in 1996

-4

-2

0

2

4

6

8

10

12

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

y-o-

y ch

ange

s in

%

Real wages

Labour productivity

Source: CZSO

M. Singer – Sound currency: The Czech experience 5

External imbalance External imbalance

The external imbalance was widest in 1996

Source: CZSO

-10

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

As

% o

f GD

P

Trade balance/GDP

Current account/GDP

M. Singer – Sound currency: The Czech experience 6

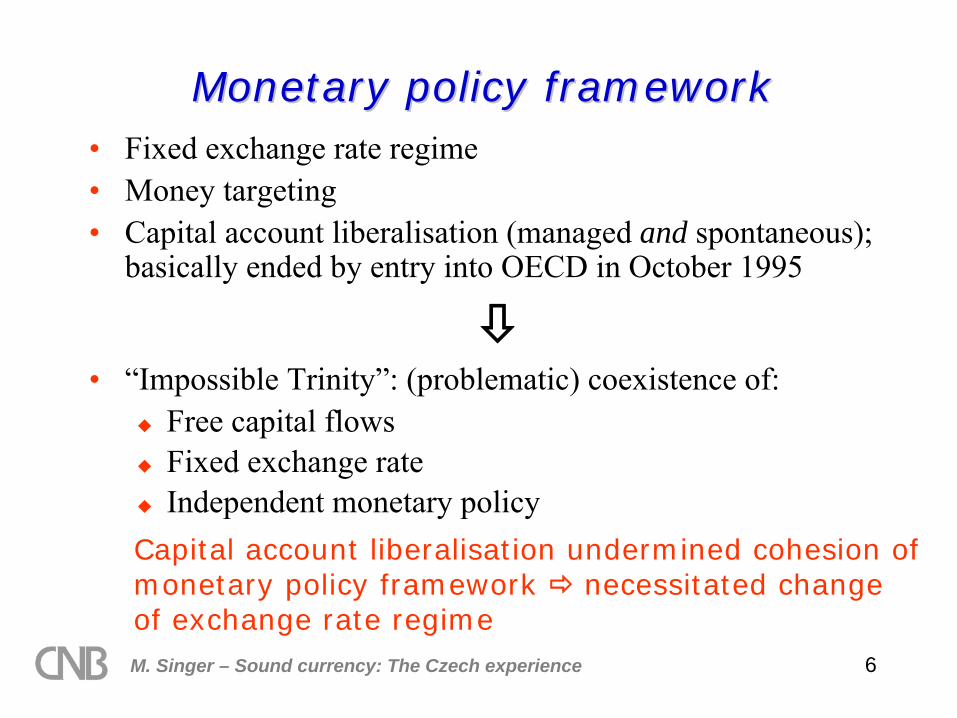

Monetary policy frameworkMonetary policy framework•

Fixed exchange rate regime

•

Money targeting•

Capital account liberalisation (managed and spontaneous); basically ended by entry into OECD in October 1995

•

“Impossible Trinity”:

(problematic) coexistence of:

Free capital flows

Fixed exchange rate

Independent monetary policy Capital account liberalisation undermined cohesion of monetary policy framework

necessitated change

of exchange rate regime

M. Singer – Sound currency: The Czech experience 7

•

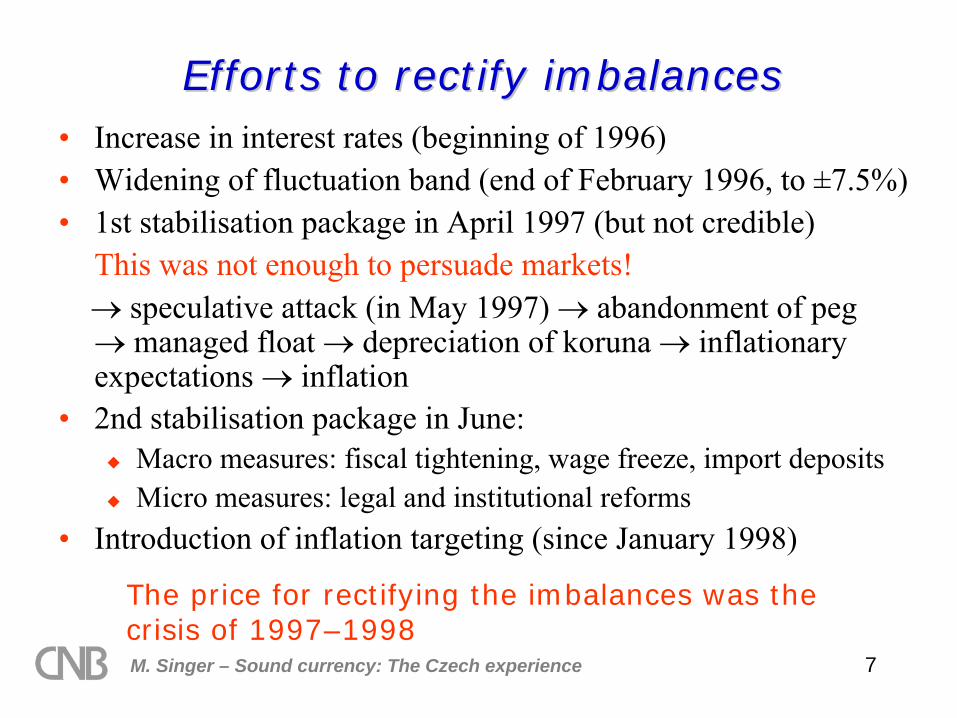

Increase in interest rates (beginning of 1996) •

Widening of fluctuation band (end of February 1996, to ±7.5%)

•

1st stabilisation package in April 1997 (but not credible) This was not enough to persuade markets! speculative attack (in May 1997) abandonment of peg managed float depreciation of koruna inflationary expectations inflation

•

2nd stabilisation package in June:

Macro measures: fiscal tightening, wage freeze, import deposits

Micro measures: legal and institutional reforms•

Introduction of inflation targeting (since January 1998)

Efforts to rectify imbalancesEfforts to rectify imbalances

The price for rectifying the imbalances was the crisis of 1997–1998

M. Singer – Sound currency: The Czech experience 8

-6

-4

-2

0

2

4

6

8

95/I II III IV 96/I II III IV 97/I II III IV 98/I II III IV 99/I II III IV

y-o-

y ch

ange

in %

Data from 4Q/98Data from 4Q/99

Deceleration was steeper

Depression instead of growth

Actual growth was faster

Comparison of two GDP time seriesComparison of two GDP time series

More accurate and timely information on the cyclical position of the economy could have led to less restrictive policies

Source: CZSO

M. Singer – Sound currency: The Czech experience 9

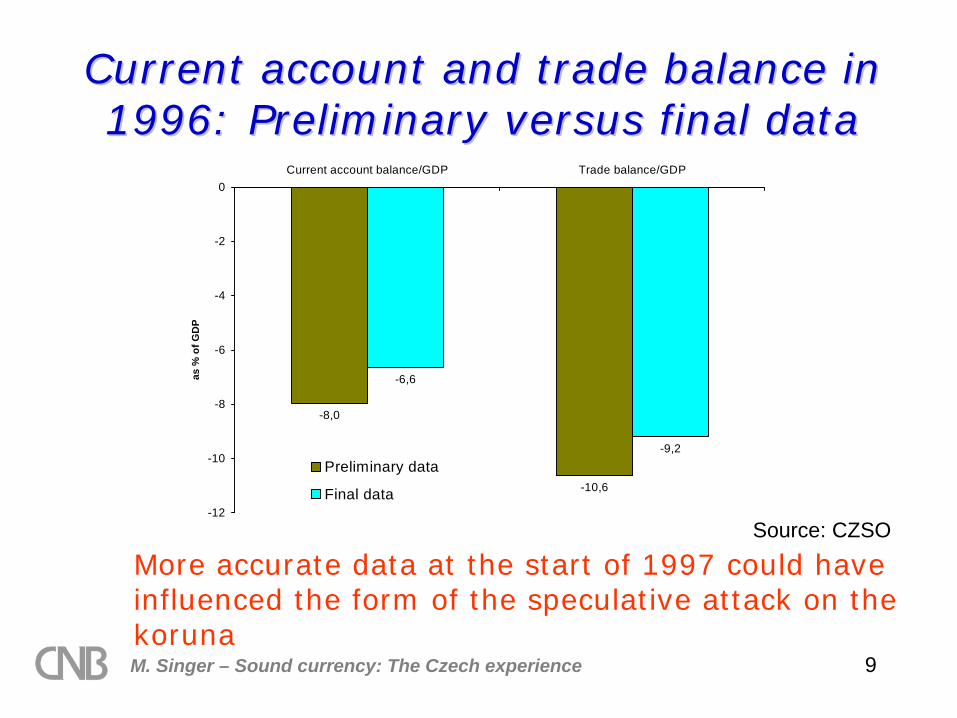

Current account and trade balance in Current account and trade balance in 1996: Preliminary versus final data1996: Preliminary versus final data

More accurate data at the start of 1997 could have influenced the form of the speculative attack on the koruna

-8,0

-10,6

-6,6

-9,2

-12

-10

-8

-6

-4

-2

0Current account balance/GDP Trade balance/GDP

as %

of G

DP

Preliminary data

Final data

Source: CZSO

M. Singer – Sound currency: The Czech experience 10

Causes of twin crisis II:Causes of twin crisis II: Banking sector developmentsBanking sector developments 1/21/2

•

Banking sector started from zero in 1990•

Division of “monobank”

(1990) two-tier system

•

Inherited problems (undercapitalisation, inherited bad loans, lack of long-term funds, lack of experienced and skilled managers)

•

Consolidation Programme I

(clean-up of balance sheets of banks KB, ČS and IPB; foundation of Konsolidační

Banka

in 1991) (total costs: around 7% of annual GDP of 1995)•

Entry of small banks (13 in 1990, 13 in 1991, 17 in 1992, 10 in 1993 and 4 in 1994) (undercapitalised, risky business policies)

M. Singer – Sound currency: The Czech experience 11

•

Consolidation Programme II

(1996) (aim: to prevent domino effect in small bank subsector; 15 out of 18 small banks participated) (costs: similar to CP I)

•

Stabilisation Programme (1996) (intended for 13 small banks; 5 out of 6 banks that participated were excluded; program

proved unsuccessful)•

Four state-owned banks:

inadequate management, low

profitability and competitiveness, wrong signals for resource allocation, major drain on public funds

The banking sector, and in particular the failure to privatise large banks in the more favourable pre-1998 period, started to hamper the incipient market system to an increasing extent

Causes of twin crisis II:Causes of twin crisis II: Banking sector developments Banking sector developments 2/22/2

M. Singer – Sound currency: The Czech experience 12

Anatomy of banking sector crisisAnatomy of banking sector crisis

Accumulation of bad loans

Capital inflow Non-market factors

Inadequate banking

supervision

Property and capital market

bubbles

Fraudulent behaviour

Rapid credit growth

Inadequate risk assessment

Rapid growth in bad loans became the main source of future difficulties in the banking sector

M. Singer – Sound currency: The Czech experience 13

Twin crisis Twin crisis •

Until first third of 1997, macroeconomic imbalances and banks’

problems developed more or less in parallel•

Sharp depreciation + dramatic interest rate increase + fiscal restrictions shock to banking sector of magnitude not usually simulated in bank stress tests

•

Outbreak of currency crisis and slide into recession caused two crises to merge into one –

twin crisis

•

Twin crisis was caused solely by bad policies:

Underestimation of symptoms of overheating and external imbalances; underestimation of Impossible Trinity and late exit from fixed exchange rate regime

Deferral of privatisation of large banks in 1994–1995

The twin crisis was an unforced crisis of domestic origin

M. Singer – Sound currency: The Czech experience 14

•

Banking sector:

Major state-funded clear-out of bad loans from banks’ balance sheets

Sale of large banks to private foreign owners•

Macroeconomic policies:

Macroeconomic restrictions (monetary and fiscal)

Introduction of consistent framework (inflation targeting + freely floating exchange rate)

The measures adopted as a result of the twin crisis put the economy on a long-term equilibrium path

Way out of crisisWay out of crisis

M. Singer – Sound currency: The Czech experience 15

Bank profitability and bad loans Bank profitability and bad loans

The clean-up and privatisation of large banks led to a big improvement in the characteristics of the banking sector

Source: CNB

-600

-400

-200

0

200

400

600

800

1 000

1 200

1 400

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 05H1

in 1

000

CZK

0

5

10

15

20

25

30

in %

Net profit per emloyee (left axis)Non-performing loans (as % of all loans) (right axis)

M. Singer – Sound currency: The Czech experience 16

•

Increased volatility of output, exchange rates and inflation during crisis + growth in general uncertainty negative impact on investment decision-making

•

Cumulative gap between potential and actual output paths in 1997–1998 could have reached around 4–5% of annual GDP (could have been even larger had gap not been closed in 1999)

•

Macroeconomic policy response (restriction) was in textbook contradiction with current (also textbook) consensus on macroeconomic policy response to current shocks to financial systems in advanced countries

The twin crisis was a costly lesson for the Czech economy

Costs of twin crisisCosts of twin crisis

M. Singer – Sound currency: The Czech experience 17

GDP in CZ 1997 Q1GDP in CZ 1997 Q1––2012 Q12012 Q1 quarterly quarterly yy--oo--yy; seasonally adjusted; seasonally adjusted

The decline in 1997–1998 was followed by a period of rapid growth ending with the financial crisis in 2008

-8

-6

-4

-2

0

2

4

6

8

10

1997

Q119

97Q4

1998

Q319

99Q2

2000

Q120

00Q4

2001

Q320

02Q2

2003

Q120

03Q4

2004

Q320

05Q2

2006

Q120

06Q4

2007

Q320

08Q2

2009

Q120

09Q4

2010

Q320

11Q2

2012

Q1

Source: Eurostat

M. Singer – Sound currency: The Czech experience 18

Consumer price index in CZConsumer price index in CZ ((yy--oo--yy changes in %)changes in %)

After the switch to inflation targeting (1998) inflation fell from 9–10% to a level regarded as price stability; the volatility was due mostly to exogenous shocks (VAT, crude oil, food, etc.)

-2

0

2

4

6

8

10

12

14

16

1/96 8 3 10 5

12/9 7 2 9 4 11 6

1/03 8 3 10 5

12/0 7 2 9 4 11 6

1/10 8 3 10 5

12/1

y-o-

y ch

ange

s in

%

Source: CZSO

M. Singer – Sound currency: The Czech experience 19

Equilibrium and nominal exchange Equilibrium and nominal exchange rate of koruna rate of koruna (CZK/EUR)(CZK/EUR)

The exchange rate of the koruna has been close to its equilibrium values since 1997

Source: Komárek L., Motl M. (2012)Note: Equilibrium

band based

on BEER (Behavioral

Equilibrium

Exchange Rate) and

FEER (Fundamental

Equilibrium

Exchange Rate)

22

24

26

28

30

32

34

36

38

40

42

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 1222

24

26

28

30

32

34

36

38

40

42

Equilibrium band Nominal CZK/EUR

M. Singer – Sound currency: The Czech experience 20

““Magic triangleMagic triangle””

The vertices of the triangle and the relationships between them all contribute to stability/instability of the economy

Financial sector

Macroeconomic and exchange rate

frameworkEnterprises

M. Singer – Sound currency: The Czech experience 21

““Magic triangleMagic triangle””: Then and now: Then and now•

Banking sector:

1997: was not stabilised, banks were inefficient, toxic assets accumulated

2012: is well capitalised, highly profitable and resilient to shocks•

Macroeconomic framework:

1997: growing inconsistency source of sys. instability and shocks

2012: is not internally inconsistent; is anchor for economy and buffer against external shocks (current crisis); however, exchange rate

can

be source of short-term shocks in the event of monetary policy mistakes (e.g. 2001–2002)

•

Enterprise sector:

1997: had only just come into being and was vulnerable

2012: is competitive and much more resilient

The entire triangle is now in infinitely better shape than during the 1996–1998 crisis

M. Singer – Sound currency: The Czech experience 22

Role of supervision: Then and nowRole of supervision: Then and now•

Factors formerly weakening role of banking supervision:

Limited circle of people, who inevitably knew each other

State representatives sitting “on other side of table”

(in banks)

“No time”

for standard supervisory procedures (only choice available in some phases: bail it out or close it down)

•

Role of supervision now:

No major or systemic sources of risk in banking sector

Integration of supervision (2006) was big step forward in safeguarding financial sector stability (closer relationship with monetary policy)

Foreign ownership of sector reduces conflict of interests of supervisory staff

•

Main risk: shift of supervision to supranational level Domestic financial market supervision conditions are better now than they were then

M. Singer – Sound currency: The Czech experience 23

Macroeconomic stability: Macroeconomic stability: Then and now Then and now

•

First half of 1990s: period of stability and transformation

Currency peg (despite relatively high inflation) was anchor for economy undergoing systemic changes

•

1996–1998: period of instability (home-made) •

1999–2008: period of stability and growth

Consistent monetary policy framework; nominal appreciation; disinflation and attainment of price stability; rapid growth

•

2008–2012: financial and debt crisis (external)

Main negative impacts: via foreign trade

Pre-crisis policies proved fully effective The former problem areas are now acting as buffers against the crisis

M. Singer – Sound currency: The Czech experience 24

SummarySummary

•

Twin crisis (1997–1998) was caused by domestic factors and inappropriate domestic policies (too long-lasting fixed exchange rate strategy and deferred privatisation of banks)

•

Rectification of domestic mistakes kicked off period of rapid growth

•

Former sources of shocks (monetary policy framework and financial sector) turned into absorbers of external shocks

•

Transfer of financial market supervision to supranational level will pose risk to financial stabilityIn the 1990s the risks of instability were mostly of a domestic nature, whereas external risks now predominate and will continue to do so

M. Singer – Sound currency: The Czech experience 25

Thank youThank you

Miroslav

[email protected]: +420 224 412 000

Česká

národní

banka Na Příkopě

28

115 03 Praha

1