sonoma county employer advisory council

TRANSCRIPT

SONOMA COUNTY EMPLOYER ADVISORY COUNCILEMPLOYER ADVISORY COUNCIL2012 Employment Law Update

INTRODUCTION

$70 Per Year, Per Company

Mission

2013 Seminars

Annual Update

Bruce MatlockBruce Matlock

Board MembersRecords Retention – Get Your Ducks In A Row ● Social

Media & Beyond – Exploring Boundaries for the Workplace ● Balancing Accommodation and Leaves of Absence ● Employment Law Update ● Management Absence ● Employment Law Update ● Management

Hotline ● What To Do When The State Comes Knocking

I Feel Your Pain

AGENDA/OVERVIEW

Agendag

Employment Law UpdateEmployment Law UpdateLegislative Law Update408b 2 Regulations408b-2 RegulationsQuestion & Answer Session with Senior Deputy Labor Commissioner Roxanne CornejoLabor Commissioner Roxanne Cornejo

A Time To Reflect

There’s A New Sheriff In Town

There Are New Sheriffs In Town

Social Media – Pushing Boundariesg

Promises, Promises, Promises, ,

EMPLOYMENT LAW UPDATE

Nicholas Laboratories v. Chen

Reimbursement for Legal Fees under Labor Code 2802

Nicholas sued its former employee Chen for, among other things, breach of contract and conversion

Chen cross complained for indemnity underChen cross-complained for indemnity under

Labor Code 2802 for the costs of defending

the suit

Court found in favor of Chen on complaint

and Nicholas on cross-complaint

Legislature did not intend to provide indemnification for first party disputes between employer and employee

“American Rule” applies – each party to a lawsuit must ordinarily pay his own attorneys’ fees

Robles v. Employment Development D t tDepartment

Employee used company money intended for safety purchases to buy shoes for a friendEmployer terminated him for misconductEmployee appealed the denial of unemployment benefitsSection 1256 states in part: “An individual is disqualified for unemployment compensation benefits if the director finds that he or she . . . has been discharged for misconduct connected with his or her most recent work.”Benefits … granted.

Paratransit, Inc. v. Unemployment I A l B dInsurance Appeals Board

Employee refuses to sign a p y gdisciplinary noticeEmployer terminates the employee f i b di ifor insubordinationSection 1256 states in part: “An individual is disqualified for individual is disqualified for unemployment compensation benefits if the director finds that he or she . . . h b di h d f i d t has been discharged for misconduct connected with his or her most recent work.”Benefits … denied.

Fillpoint LLC v. Massp

Multiple non-compete provisionsp p p

Sale of a business exemptionp

Stock purchase agreement/ employment agreement

Enforceable?

Arnold v. Mutual Of Omaha

Nonexclusive insurance agent for Mutual of Omaha

Licensed activity

Provided with assistance, training, software, conference rooms

Multiple clients

Contract defining relationship as “independent contractor”

Mutual understanding

Plenty of freedom

“At Will” provisionp

Independent Contractor or Employee?

LeFiell Manufacturing Co. v. Superior C tCourt

Wage Theft Prevention Act (1)g ( )

Labor Code 2810.5

Provides employees notice of basic employment information

Notice must be given to all new non-exempt hires in private sectorf C AUnnecessary if CBA

Notice of change must be within 7 days (wage statement is ok)

Wage Theft Prevention Act (2)g ( )

Labor Commissioner Guidancehttp://www.dir.ca.gov/dlse/Governor_signs_Wage_Theft_Protection_Act_of_2011.html

Template (revised 5/4/12)

FAQ’ l FAQ’s examples: #6 – Don’t have to use DLSE’s template

#7 – Must be a stand alone document

#8 – Can’t be waived

#9 – All hourly and piece rates must be on notice

#10 – Employee signature not required, but note it#10 Employee signature not required, but note it

#18 – “Pay” = wages on notice & must include all compensation including commissions

#25 – No annual requirement#25 – No annual requirement

Wage Theft Prevention Act (3)g ( )

Brinker – Meal

Provide unpaid 30-minute meal break to employees who work more than five hours in a day

Duty-free (no work expected)

Free to leave premises Free to leave premises

Must start before the end of the fifth hour of worke.g., 8:00 am – 4:00 pm shift, must start lunch by 12:59 pm

Early lunch ok, late lunch not ok

Work through lunch? Employer choice = penaltyEmployer choice = penalty

Employee choice = straight pay

Brinker – Rest

Authorize and permit paid 10-minute rest period for every four hours worked or major fraction thereoffraction thereof

3.5 hrs – 6 hrs = one 10 minute break

6 hrs – 10 hrs = two 10 minute breaks

10 hrs – 14 hrs = three 10 minute breaks

Take in the middle of each work period to the Take in the middle of each work period to the extent practicable to do so

Commission Agreementsg

Just the teaserJust the teaserAll Commission Agreements in writingSetting forth method of computation and paymentSetting forth method of computation and paymentSigned copy to and from each employeeE i d h ffExceptions and other stuffJanuary 1, 2013

Deleon v. Verizon Wireless, LLC,

Advanced commissionsAdvanced commissionsVesting process/chargeback periodSensible explicit planSensible, explicit plan“Can you hear me now?”

Harris v. Superior Courtp

Administrative Exemption to Overtime

Work is “administrative” when it is directly related to management policies or general business operations

To be directly related, the work must be:

1. Qualitative (white collar work such as advising management, planning, negotiating and representing the company)

2. Quantitative (substantial importance to management policy or general business operations)

Case involved qualitative prong only – BUT court found them non-exempt even though they spent majority of time doing qualitative work

Take away:

Whether position exempt is always fact-specific

Exemptions are narrowly construedp y

To qualify as exempt the job duties must be more than the day-to-day operations of the company

Christopher v. Smithkline Beechamp

Ph ti l l / d t ilPharmaceutical sales reps / detailers

Outside sales exemption

Selling v. promoting

CA v. DOL

Aleman v. Airtouch

Reporting-Time Pay Split-Shift Compensation

Muldrow v. Surrex Solutions C tiCorporation

Commissioned Employees Exemption/Inside Sales Commissioned Employees Exemption/Inside Sales ExemptionEmployed “principally in selling a product or p y p p y g pservice”Commissions were “sufficiently related to price”Compensation systemwas a “bona fide

i i t ”commission system”

Touchstone Television Productions v. Ni l tt Sh idNicolette Sheridan

Labor Code Section 6310(b): Any employee who is discharged, threatened with discharge, demoted, suspended, or in any other manner discriminated against in the terms and conditions of employment by his or her employer because the employee has made a bona fide oral or written complaint to the division other governmental agencies having written complaint to the division, other governmental agencies having statutory responsibility for or assisting the division with reference to employee safety or health, his or her employer, or his or her

representative, of unsafe working p , gconditions, or work practices, in his or her employment or place of employment, or has participated in an

l l ti l h lth employer-employee occupational health and safety committee, shall be entitled to reinstatement and reimbursement for lost wages and work benefits caused by lost wages and work benefits caused by the acts of the employer.

Johnson v. Board Of Trustees (9th Cir.)( )

Special education teacher allowed certification to lapse

Employer terminated her employment without stepping in

Employee sued for wrongful termination, claiming disabilities contributed to the lapse

“A ‘ lifi d i di id l i h “A ‘qualified individual with a disability’ is one ‘who satisfies the requisite skills, experience, education and other job related requirements of j qthe employment position such individual holds or desires, and who, with or without reasonable accommodation, can perform the essential f nctions of can perform the essential functions of such position.’”

Samper v. Providence St. Vincent M di l C t (9th Ci )Medical Center (9th Cir.)

N l ff d f Neo-natal nurse suffered from FibromyalgiaTerminated for poor attendancepBrought suit for wrongful termination“The common-sense notion that on-

l dsite regular attendance is an essential job function could hardly be more illustrative than in the context of a neo-natal nurse. This at-risk patient population cries out for constant vigilance, team g ,coordination and continuity.”

Reyes v. Liberman Broadcastingy g

Wage and hour class action complaintWage and hour class action complaintValid arbitration agreementNo waiver of right to arbitrationNo waiver of right to arbitration

Wisdom v. Accentcare

Arbitration Agreement in gemployment applicationStructural deficiencies in agreement

One WayAAA Rules Referenced but AAA Rules Referenced but not attachedNo Explanation of “Binding Arbitration”Contract of Adhesion

Unlawful as written

D.R. Horton, Inc. (NLRB), ( )

Arbitration Agreement with class action waiver

“Employers may not compel employees to waive their NLRA right to collectively pursue litigation of employment claims in all forums, arbitral and judicial. So long as the employer leaves open a judicial as the employer leaves open a judicial forum for class and collective claims, employees’ NLRA rights are preserved without requiring the availability of without requiring the availability of classwide arbitration. Employers remain free to insist that arbitral proceedings be conducted on an individual basis.”

The State Of Arbitration

James v. Costa Mesa

QUESTION & ANSWERQUESTION & ANSWER

LEGISLATIVE UPDATE

Agendag

New laws and potential impact

Commission AgreementsCommission Agreements

Questions

New Employment Lawsp y

AB 2386 – Breastfeeding = “Sex” Under FEHAG C d §12926( )(1) (A d d)Government Code §12926(q)(1) (Amended)

Adds “Breastfeeding or medical conditions related Adds Breastfeeding or medical conditions related to breastfeeding” to the definition of “sex.”This change is a declaration of existing law, not a This change is a declaration of existing law, not a change of law.This should have no impact on employers.This should have no impact on employers.

AB 1964 – Religious Dress Or Grooming Practice Government Code §12926(p) (Amended)Government Code §12926(p) (Amended)

Adds religious dress or grooming practice as a Adds religious dress or grooming practice as a “belief or observance” that needs to be accommodated under FEHA.Interpreted broadly.Not required to accommodate religious dress or Not required to accommodate religious dress or grooming practice if it would:

Segregate an employee from the public or other employees.Result in the violation of specified laws protecting civil rights.Cause an undue hardship.

AB 1450 – Discrimination Against The UnemployedLabor Code §1045- §1048 (New)Labor Code §1045 §1048 (New)

Cannot advertise current employment is a p yrequirement or that the employer will only accept applications from currently employed individuals.

Can:Advertise for legitimate job requirements including education and experience.Get dates of employment & reasons for separation.Have knowledge of a person’s employment status. Consider the employment history and underlying reasons for employment status.Refuse to offer employment because of reasons underlying an individual’s employment status.

AB 2103 – Explicit Mutual Wage Agreements Labor Code §515 (Amended)Labor Code §515 (Amended)

This law is intended to overturn the case of Archiga v. Dolores Press (2011) 192 Cal.App.4th567.

Employer and employee can agree on l k f a set salary per week for non-exempt

employees but it cannot encompass overtime.overtime.

Overtime must be paid and tracked Overtime must be paid and tracked separately.

AB 889 – Domestic Worker OvertimeLabor Code §1450 (New)Labor Code §1450 (New)

Department of Industrial Relations must adopt p pwage orders reflecting that domestic workers are entitled to overtime.Domestic Workers include:

Nannies, housekeepers, caregivers for children, persons with disabilities and the elderly.persons with disabilities and the elderly.

Exclusions apply. Check with legal counsel if you have domestic workers to confirm if the law applies to your employees.

AB 1744 – Temporary Agencies To Include More Information On Wage TemplateLabor Code § 2810.5(a)(3) (Amended)

Adds a requirement that the temporary agency Adds a requirement that the temporary agency provide information on the Wage Template about the legal entity for whom the employee g y p ywill perform work:

NamePh i l dd f h i ffiPhysical address of the main officeMailing address if different from main officeTelephone numberAnything else the Labor Commissioner deems material and necessary

AB 1744 – Temporary Agencies To Included More Information On Wage StatementsLabor Code § 226(a)(9) and § 226.1 (Amended)

Also requires that on or after July 1, 2013temporary agencies will need to show on each

l ’ t t temployee’s wage statement:

R f d l h Rate of pay and total hours worked for each assignment

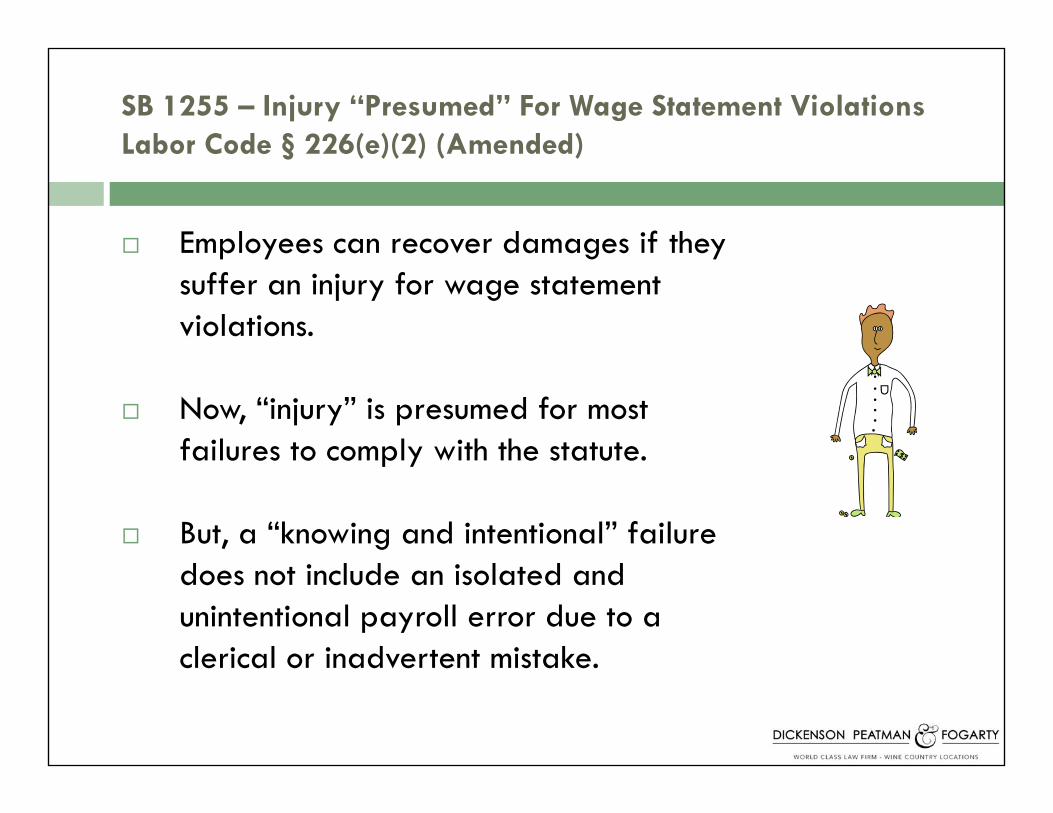

SB 1255 – Injury “Presumed” For Wage Statement Violations Labor Code § 226(e)(2) (Amended)Labor Code § 226(e)(2) (Amended)

Employees can recover damages if they p oyees ca ecove da ages ey suffer an injury for wage statement violations.

Now, “injury” is presumed for most failures to comply with the statute.failures to comply with the statute.

But, a “knowing and intentional” failure does not include an isolated and unintentional payroll error due to a clerical or inadvertent mistakeclerical or inadvertent mistake.

AB 2674 – Right To Inspect Employment RecordsLabor Code § 226 (Amended)Labor Code § 226 (Amended)

Wage StatementsWage StatementsEmployers required to keep copies of itemized wage statements for 3 years.

Copy can be a duplicate or computer-generated record that shows all of the information that shows all of the information that existing law requires to be in the itemized statement.

AB 2674 – Right To Inspect Employment RecordsLabor Code § 1198.5 (Amended)Labor Code § 1198.5 (Amended)

Personnel RecordsPersonnel Records

Current law requires employers to provide employees access to personnel files at reasonable intervals and at reasonable timesat reasonable times

This law would require employers to provide a current or former employee, or his/her representative, an opportunity to inspect and receive a copy of personnel opportunity to inspect and receive a copy of personnel records within 30 calendar days from the date the employer receives a written request

These provisions do not apply if the employee has These provisions do not apply if the employee has filed a lawsuit against employer

SB 1234 – Retirement Savings Plans For Private Employers The California Secure Choice Retirement Savings Trust ActGovernment Code §100000 (New)

Mandates private employers offer payroll deposit retirement savings arrangement to employeesEmployees required to deposit a specified p y q p ppercentage of their annual salary or wages in the California secure Choice Retirement Savings TrustOpt-out optionEDD to assess penalties against employers who fail to make program availablep gWill not happen if law is found to violate ERISA or if plan does not qualify as a tax exempt IRAexempt IRA

AB 1844 – Employer Use Of Social MediaLabor Code §980 (New)Labor Code §980 (New)

Employers cannot require or request an employee or applicant to:

Disclose a username or password or access personal social media in the presence of the

lemployer.

Employers can:Request username and password to investigate allegations of employee misconduct or employee violation of applicable laws and regulationsapplicable laws and regulations.Request username and password to access employer-issued electronic deviceTerminate or discipline employees for reasons Terminate or discipline employees for reasons otherwise permitted by law

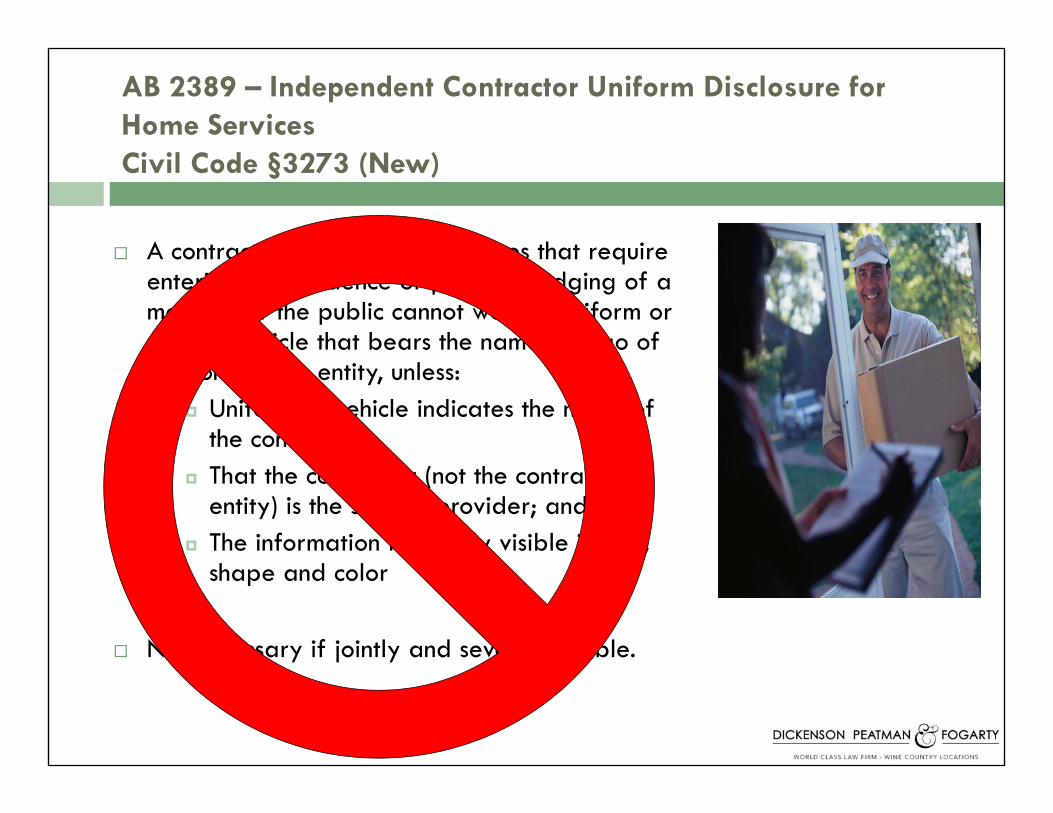

AB 2389 – Independent Contractor Uniform Disclosure for Home ServicesCivil Code §3273 (New)

A contractor that provides services that require A contractor that provides services that require entering the residence or place of lodging of a member of the public cannot wear a uniform or drive a vehicle that bears the name or logo of the contracting entity, unless:

Uniform or vehicle indicates the name of the contractor;That the contractor (not the contracting entity) is the service provider; andThe information is readily visible in size, shape and color

Not necessary if jointly and severally liable.

AB 1817 – Commercial Computer Technicians Mandated Reports For Child Abuse Penal Code § 11165.7(a)(41) (Amended)

Commercial computer technicians now mandated reporters of child abuse.

Commercial Computer Technician means a person p pwho works for a company that is in the business of repairing, installing, or otherwise servicing computer or computer components for a fee.

Companies can designate one employee to be the “mandated reporter” to whom all other employees must provide the information.

Employers must provide employees with knowledge p y p p y gof their mandated reporter status. Employers are encouraged (but not required) to provide training.

AB 1675 – Farm Labor Contractors License – Civil PenaltyLabor Code §1683 (Amended)Labor Code §1683 (Amended)

E i ti l i f l b Existing law requires farm labor contractors to receive a license from the Labor Commissioner If unlicensed the Labor Commissioner. If unlicensed it is a misdemeanor punishable by fines and up to 6 months in jailes a d up o 6 o s ja

This law provides civil penalties in This law provides civil penalties in addition.

AB 2346 – Heat Related Illness – Private Right Of ActionFarm Worker Safety Act Of 2012Labor Code § 6720 et seq. (New)

Agricultural employer must certify by January 31 of each year that the employer Agricultural employer must certify by January 31 of each year that the employer has adopted written procedures for complying with heat protective measures.In addition to any other available causes of action for failure to comply with heat protective measures, an employee may bring a civil action against a repeat offender offender. Acts of omissions of the employer are imputed on the Farm Operator.Farm Operator means:

Land owner unless land leased and owner is not gaining anything of benefit other than Land owner unless land leased and owner is not gaining anything of benefit other than rent; andPerson who leases the property used in the farming operation.

AB 2676 – Heat Related Illness – CrimeHumane Treatment Of Farm Workers ActPenal Code §338 (New)

A person is guilty of a misdemeanor if he/she p g y /directs an agricultural employee to perform or supervises an agricultural employee in the

f f td k ith t idi performance of outdoor work without providing employee with:

Continuous ready access to an area of yshade sufficient to allow body to coolPotable water suitably cool; orE h bl ll l Enough potable water to allow employee one quart per hour throughout shift

SB 863 – Workers’ Compensation Reform

In the past two years the costs of workers’ p ycompensation insurance has risen from $14.8 billion to $19 billion with an estimated 12.6% increase projected in the near future..6% c ease p ojec ed e ea u u e.Reforms are projected to save businesses $1 billion in 2013, increase payments to di bl d k b 30% d i th disabled workers by 30% and improve the delivery of worker benefits.Examples of changes:

Workers benefits are to increase 30%Creates an alternative dispute resolution programprogram

COMMISSION AGREEMENTSCOMMISSION AGREEMENTS

Labor Code §2751W itt C i i A t J 1 2013Written Commission Agreements – January 1, 2013

All commission agreements must be in writingg gSigned copy must be given to the employeeEmployer must obtain a receipt indicating employee has copyIf employee continues to work under the terms of an expired contract, the contract will continue until a new agreement is signed or the employment is terminatedg p y

Here Is What Should Be In Your C i i A tCommission Agreements

1. The term of the agreement and expiration date, if any2. How base pay, if any, is calculated (annual salary, hourly wage,

advance draw, etc.)3. The method of calculating the employee’s commission4. When that commission is earned and when it is paid to the

employee5. What conditions must be met to earn the commission6 Wh h id d / d i i h h 6. What happens to unpaid and or/unearned commissions when the

employment is terminatedThe object of the law is to make it crystal clear what the employee will be earning and when it will be paidwill be earning and when it will be paidDepending on type of position there could be other information that should be includedYou should review with your legal counsel before implementingYou should review with your legal counsel before implementing

“Commission” Defined:

Commission wages are compensation paid to any Commission wages are compensation paid to any person for services rendered in the sale of such employer’s property or services and based p y p p yproportionately upon the amount or value thereof

“Commission” Does Not Include:AB 2675 L b C d 2751( )AB 2675 – Labor Code 2751(c)

Short term productivity bonuses such as are paid to retail clerks.

Temporary, variable incentive payments that increase, but do not decrease, payment under the written contract., p y

Bonus or profit-sharing plans unless there has been an offer by the employer to pay a fixed percentage of sales or profits as employer to pay a fixed percentage of sales or profits as compensation for work to be performed

The law is not intended to change California’s view on bonuses which is The law is not intended to change California s view on bonuses, which is defined by DLSE as “Money promised to an employee in addition to the monthly salary, hourly wage, commission or piece rate usually due as compensation”p

Consequences For Not Having Written C i i A t?Commission Agreement?

There are no penalties for noncompliance, but p p ,employers could face potential claims under the following statutes:

PAGA (Private Attorney General Act)Unfair competition claims under Business and Professions Code §17200

Exempt or Non-Exempt Salesperson?p p p

Good time to review the exempt status of positionsp p

Must meet federal and California sales/commissions /exemptions

Recommended discussing exemption questions with your legal counsel

QUESTION & ANSWERQUESTION & ANSWER

408b-2 REGULATIONS

E l R ti t I S it A tEmployee Retirement Income Security Act

29 CFR § 2550.408b-2(c)

Effective July 1, 2012

Elizabeth R. Palmer

A duty to acty

People who exercise authority over the management p y g

or the assets of retirement plans have an over arching

obligation (duty) to act in the best interest ofobligation (duty) to act in the best interest of

retirement plan participants.

What is the duty?y

To avoid prohibited transactions

“Prohibited Transaction”Prohibited Transaction

1. Transaction between plan and party in interest

2 T i b l d fid i2. Transaction between plan and fiduciary

3 Transaction in which property (real or personal)3. Transaction in which property (real or personal) is transferred from a partying interest to a plan

ERISA § 406ERISA § 406

Today’s focus

Transactions between

l d t i i t ta plan and a party in interest

“Fiduciary”y

(i) exercises discretionary authority of control regarding the management of the plan; or exercises any authority or control

A person who

management of the plan; or exercises any authority or control regarding the management or disposition of the plan’s assets,

(ii) renders investment advice for a fee or other compensation regarding any money of property of a plan, or

(iii) has any discretionary authority or responsibility in the administration of the plan.

ERISA §3 (21)

Today’s focus

Transactions between

l fid i d t i i t ta plan fiduciary and a party in interest

“Party in interest”y

With respect to a retirement plan:With respect to a retirement plan:A person providing services to a plan

ERISA § 3(14)(B)

Examples of persons providing services

Investment advisorsInvestment advisorsRecord keepers

AttorneysAttorneys

Includes

Relatives of a CSP

A corporation, partnership, trust or estate controlled by a CSP

An employee, officer, director or 10% owner of a CSP

General rule of § 406§

If a plan fiduciary allows a party in interest toIf a plan fiduciary allows a party in interest to

provide services to the Plan, the provision of

services is a prohibited transaction.

Exceptionp

Contracting or making reasonable arrangements with a

party in interest for office space, legal or accounting or p y p , g g

other services necessary for the establishment or

operation of the plan is not a prohibited transaction if nooperation of the plan is not a prohibited transaction, if no

more than reasonable compensation is paid therefor.

ERISA § 408(b)(2)

What’s Reasonable?

The new regulation is intended to ensure that

fiduciaries get the information they need to

determine whether the compensation the plandetermine whether the compensation the plan

is paying is “reasonable.”

New Regulation

No contract or arrangement for service between a

covered plan and a covered service provider is p p

reasonable (for purposes of 408(b)(2)) unless the

service provider discloses certain information inservice provider discloses certain information in

writing to a plan fiduciary.

29 CFR 2550.408b-2(c)

“Covered Plans”

ERISA d d fi d b fit dERISA-covered defined benefit and

defined contribution plansdefined contribution plans.

ERISA 480b-2(c)(ii)

Not Covered

Simplified employee pension plans (SEPs)

SIMPLE retirement accounts

IRAs and certain annuity contracts and custodial yaccounts described in IRC §403(b)

ERISA 480b-2(c)(ii)

“Covered Service Provider”

Expects > $1,000

ERISA fiduciary service providersERISA fiduciary service providers

Investment Advisors

Record keepers or brokers offering designated investment alternatives (e.g., a platform provider)provider).

ERISA 480b-2(c)(iii)

“Covered Service Provider”

Providers of other services who receive “indirect compensation” in connection with the services:

A ti InsuranceAccountingAuditingActuarial

InsuranceInvestment advisoryLegalR dk iBanking

ConsultingCustodial

RecordkeepingSecurities brokerageThird party administration or valuation Custodial p yservices to the plan or the CSP

ERISA 480b-2(c)(iii)

Initial Disclosure Requirements

In writing to a responsible plan fiduciary:In writing to a responsible plan fiduciary:

- Describe services and compensation (direct & indirect) to be received by CSP, its affiliates and/or subcontractorsy ,

- Allocate compensation between related parties

Ex. of transaction based: commissions, referral or finder’s fees, other incentive compensation.

Ex. Rule 12b-1 fees, charged against plan assets and reflected in the net value of the investment.

ERISA 480b-2(c)(iv)

Initial Disclosure Requirements

D ib th l ti hi b t CSP d- Describe the relationship between CSP and any source of indirect compensation (to identify potential conflicts of interest).)

- Attribute compensation to recordkeeping, even if there is no explicit charge.

If recordkeeping services are subject to a rebate or offset

with an affiliated party, the CSP must provide a reasonable

good faith estimate of the value of the services.

ERISA 480b-2(c)(iv)

Initial Disclosure Requirements

CSPs acting as fiduciaries must disclose compensation

that is charged directly against an investment and must

disclose an investment’s annual operating expenses. For

ppt. directed individual account plans, disclosure mustppt. directed individual account plans, disclosure must

include “total annual operating expenses” as required

under the ppt level disclosure regulation at 29 CFRunder the ppt. level disclosure regulation at 29 CFR

2550.404a-5.

ERISA 480b-2(c)(iv)

Initial Disclosure Requirements

CSPs that are record keepers or brokers may “pass

through” disclosures from an unaffiliated issuer, provided

the issuer is a registered investment company.t e ssue s a eg ste ed est e t co pa y

ERISA 480b-2(c)(iv)

Initial Disclosure Requirements

Disclosures may be made electronically, via

website or other medium readily accessible to

the responsible fiduciary.

ERISA 480b-2(c)(iv)

Timing of Disclosuresg

Initial Disclosures:Initial Disclosures:

No later than August 30, 2012; thereafter, reasonably in

advance of date contract begins, is extended or renewed.

Changes to Disclosures g

CSP: asap but no later than 60 days after change

Investment-related information: at least annually

Also

Upon request of a responsible fiduciary

Reasonably in advance of reporting date

Summary or Guide to Initial DisclosuresInitial Disclosures

EBSA “strongly encourages” CSPs to offer a guide, summary or similar tool to assist fiduciaries in identifying all required disclosures particularly when service arrangements aredisclosures, particularly when service arrangements are complex and information is in multiple documents.

Sample guide in binder

EBSA may issue a rule in the near future requiring this.

Disclosure Errors by CSPy

No contract or arrangement will fail to be

“ bl ” d thi l ti l l b“reasonable” under this regulation solely because

the CSP acting in good faith provided inaccurate

information, provided the CSP corrects the error as

soon as practicable but not later than 30 days after

discovering the error.

ERISA 480b-2(c)(vii)

Exemption for Responsible Plan FiduciaryPlan Fiduciary

The excise tax and liability rules will not apply to a fiduciaryThe excise tax and liability rules will not apply to a fiduciary because a CSP fails to provide disclosures as long as

The fiduciary did not know of the failure and believed the CSP had provided the required information;

The fiduciary promptly requests the information, and;

If the CSP does not provide the information within 90If the CSP does not provide the information within 90 days, the fiduciary notifies the DOL of the failure.

ERISA 480b-2(c)(ix)

Impact on Participant-Level Disclosures

For calendar year plans, the initial annual disclosure of

information (including fees and expenses) should have been

furnished by August 30, 2012 (60 days after July 1).

The first quarterly statements due no later November 14, 2012

(45 days after the end of the third qtr (July-Sept))

Q t l t t t d l fl t th f dQuarterly statement need only reflect the fees and expenses

actually deducted from the participant’s or beneficiary’s account

during the quarter (i e July September)during the quarter (i.e., July – September).

29 CFR 2550.404a-5

Q&A WITH SENIOR DEPUTY Q&A WITH SENIOR DEPUTY LABOR COMMISSIONER O COMM SS ON

ROXANNE CORNEJO

Q&A WITH SENIOR DEPUTY LABOR COMMISSIONER ROXANNE CORNEJOROXANNE CORNEJO

Roxanne Cornejo is the Senior Deputy of the Santa Rosa LaborCommissioner’s office with responsibility for adjudicating wage claims inMarin, Sonoma, Mendocino, Lake, Napa and Solano Counties. Prior toh L b C i i ’ ffi M C j k d i i fthe Labor Commissioner’s office, Ms. Cornejo worked in various areas ofworkers’ compensation from State Compensation Insurance Fund to theWorkers’ Compensation Appeals Board. And, before working for theState Ms Cornejo was employed by some of the largest insuranceState, Ms. Cornejo was employed by some of the largest insurancecompanies heading up a training department and as a productdeveloper.

Ms. Cornejo holds a BA from University of California, San Diego and anMBA from University of San Diego.

QUESTIONS?

About Your Presenters

Elizabeth began her legal career with the SanFrancisco commercial litigation firm Rice, Fowler,

Greg is an avid fan of the Rose Bowl ChampionOregon Ducks. He and his family live in Sebastopol.

JENNIFER D. PHILLIPS is a senior associateprimarily in the firm's labor and employment

GREGORY J. WALSH is the Co-ManagingDirector of Dickenson, Peatman & Fogarty and thelead Director in the firm's Labor and EmploymentGroup. Greg’s practice encompasses all aspects oflabor and employment law including advising g

Booth & Banning, LLP representing clients in arange of business and trade related matters. In1994, she chose the Sonoma County lifestyle andjoined the Santa Rosa law firm Merrill, Arnone &Jones, LLP, shifting her practice to transactionaland tax-related matters for clients in businesses

primarily in the firm s labor and employmentdepartment. She has been a lawyer for over 15years. During this time she has worked for bothlarge and small firms gaining valuable experiencein both litigation and counseling. She has extensiveexperience in all manner of employment issuesi l di d h di i i ti bl

labor and employment law, including advisingemployers on how to prevent issues before theyarise, and developing workable solutions to thosethat do. Greg is also a member of the firm’s WineLaw and Litigation groups, representing clients inadministrative and court proceedings.

and tax related matters for clients in businessesranging from healthcare, goods and services,construction and real estate development totourism, wine/agriculture, government entities,equine-related industries and non-profitorganizations. At DP&F, Elizabeth continues herbusiness and tax practice with an emphasis on

including wage and hour, discrimination, reasonableaccommodation, leaves of absence, andimplementing state and federal regulations. Sheoften analyzes legal risks associated with hiring,disciplining and firing in order to counsel clients withthese employment decisions. Although counseling is

' f

A native Californian, Greg began his legal careerpracticing labor and general business law inBoston. He later returned to the Bay Area, wherehe continued developing his practice with one ofthe nation's largest labor and employment firms,

business and tax practice with an emphasis onwine industry related services.

Prior to attending law school, Elizabeth spent sixyears with the accounting firm of Coppers &Lybrand (now PricewaterhouseCoopers) as adefined contribution plan consultant in the firm’s

the key to DP&F's employment practice, Jennifer is atrained and experienced litigator who protects herclients' interests when litigation becomes necessary.

Jennifer is an extensive world traveler and nativeCalifornian. She enjoys all that Sonoma County has

representing union and non-union employers. In2004, Greg’s love of the wine country brought himnorth, where he now uses his range of experienceto solve problems for North Bay employers,businesses and individuals. The North Bay BusinessJournal recently named Greg as a "Forty Under

defined contribution plan consultant in the firm’sActuarial, Benefits and Compensation Group.

Elizabeth is on the board of the American RedCross, Sonoma, Mendocino and Lake CountiesChapter and is vice-president of the Wild Horse

d B S l d i Sh C

to offer and resides in Santa Rosa with her husbandand two young children.

ELIZABETH R. PALMER joined DP&F's businessgroup in 2011 and is the senior business lawyer inthe firm's Santa Rosa office. Elizabeth's experience

40" award recipient.

Greg received his B.S. while double-majoring inJournalism and Sociology at the University ofOregon. He earned his law degree fromUniversity of California, Hastings College of the

and Burro Sanctuary, located in Shasta County,California. She is an avid horseperson anddressage enthusiast. When Elizabeth is not at thebarn, she and her husband Mike enjoy winetasting and taking their dog to the beach.

pcovers a broad range of business matters involvingmergers and acquisitions, partnerships, joint ventures,entity formation, financing, purchases, sales,employment, pensions and benefits, including thetaxation implications of those matters.

y g gLaw, where he served as Senior Executive Editor ofthe Communications And Entertainment LawJournal. Greg is admitted to practice in California,Massachusetts, and several federal jurisdictions.

About The Firm

Dickenson, Peatman & Fogarty provides a level ofrepresentation ordinarily associated with legal practices in

Napa Countyrepresentation ordinarily associated with legal practices inmajor metropolitan centers. Our attorneys are routinelyrecognized in legal rankings and surveys as some of thebest in their fields, and the firm is involved regularly with

tt f l l d ti l i t F f t

1455 First Street Suite 301

Napa, CA 94559matters of local and national import. For over forty yearsDP&F lawyers have practiced law with the “get to knowyou” culture that has engendered significant client loyalty.

d h f N d S &

T: 707.252.7122F: 707.255.6876

Rooted in the wine regions of Napa and Sonoma, DP&Fprovides full service legal representation to all manner ofbusinesses and individuals throughout California, the UnitedStates and abroad. The Firm’s major practice areas

Sonoma Countyj p

include alcohol beverage law, business and corporatedealings, land use matters, labor and employment, civillitigation, intellectual property, real property transactions,as well as estate planning and probate. With offices in

50 Old Courthouse Sq. Suite 200

Santa Rosa, CA 95404as well as estate planning and probate. With offices inthe major wine valleys of Napa and Sonoma, the firm isintimately familiar with, and has extensive experience, inboth the wine and hospitality industries.

T: 707.524.7000F: 707.546.6800

THANK YOU!THANK YOU!

Sonoma County EAC 2012 Employment Law Update