some perspectives of the norwegian oil and gas clusters. jacob sannes director, statoil do brasil...

TRANSCRIPT

Some Perspectives of the Norwegian Oil and Gas Clusters.Some Perspectives of the Norwegian Oil and Gas Clusters.

Jacob Sannes

Director, Statoil do Brasil Ltda.

Some Norwegian experiences that could be applicable in Brazil.

Jacob Sannes

Director, Statoil do Brasil Ltda.

Some Norwegian experiences that could be applicable in Brazil.

NOT AN OFFICIAL UNCTAD RECORD

What is a cluster.

Clusters were not ”invented” by Michael Porter but his work in the early 90-ies established the term for common use.

Porter defined clusters as a location where Cost and quality of inputs Nature and intensity of local competition Sophistication of local customers, and Presence of related industries

interact to create dynamics which innovate, boost productivity and attract new industry to that location.

Porter stated that success is greatest where competition is strongest and peer companies compete to be best but also have constructive co-operation.

Some examples.

Italian shoes

Hollywood films

Broadway and London Theatres

Detroit cars

Silicon Valley IT

Madison Avenue advertising agencies

Houston and Norwegian Oil and Gas Industry.

Clusters must develop

Productivity and technology may out-compete the advantages of a cluster

Heavy shipbuilding moved from Europe and USA to take advantage of higher productivity in Japan

Steel production moved from proximity to iron and coal in Europe and USA as combination of productivity and new technologyin Japan plus cheaper bulk transport developed

In some cases, new clusters develop from the ruins

Specialist shipbuilding in Europe but not USA Specialist quality steel production

Norway’s goals and strategies -

The petroleum resourcesbelong to the nation

Development of the resources must benefit the society as a whole

The goals and strategies:

National involvement

Resource management

Technology and competence

Transforming the societyDeveloping the necessary knowledge

Build competence Adapting the education

system Focusing on training and

developing employees Stimulating students

Transform existing industries Maritime Mining Process

Maintain a balance between oil and non-oil sectors

Strengthening the competitivenessof the energy service industry

Structure projectsaccording to national capabilities

Develop technologyin joint projects

Inform

Educate

De-brief

Help with advice

Balancing Competition and Co-operation

Successful clusters are invigorated by strong competition, very often ”personal” and driven by strong individual’s desire to show who is best.

Inside successful clusters there is recognition that some issues are best solved through collective actions.

The Norwegian society traditionally works towards solving issues through co-operation, and this has helped in establishing the Norwegian Oil and Gas cluster.

To sustain any cluster its members must develop a mode of co-operation whilst maintaining competition.

The Norwegian co-operation model

Govern-ment and

Authorities

Oil companies

Contracting and supply

industry

Employees and Labour

Unions

Oil and Gas Production1980-2020, thousands barrels o.e. per day

0

1000

2000

3000

4000

5000

6000

1980 1985 1990 1995 2000 2005 2010 2015 2020

Oil Gas NGL

A large oil and gas producerNorway has celebrated 30 years of production

A large producer – and exporter –of oil and gas

Oil and gas revenues represents 20% of Norway’s GDP

A strong and capable domestic support industry – now going international

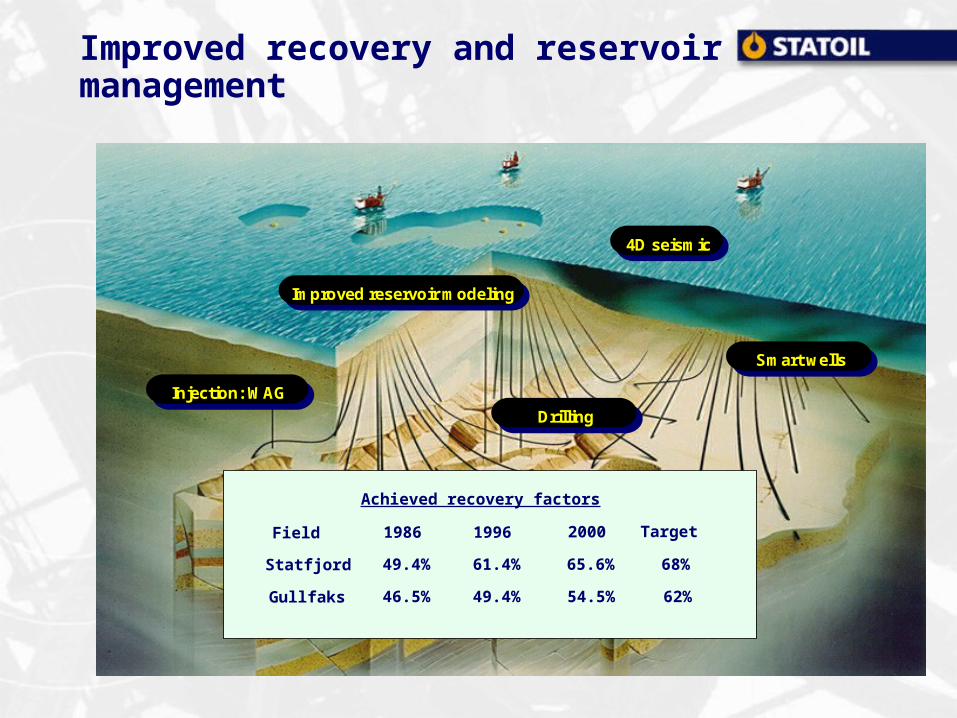

Improved recovery and reservoir management

Improved reservoir modeling

4D seismic

Injection: WAG

Smart wells

Field 1996 2000 Target

Statfjord

Gullfaks

Achieved recovery factors

1986

61.4% 65.6% 70%

49.4% 54.5% 62%

49.4%

46.5%

Drilling

Field 1996 2000 Target

Statfjord

Gullfaks

Achieved recovery factors

1986

61.4% 65.6% 68%

49.4% 54.5% 62%

49.4%

46.5%

Supplier Development Programme

STATOIL

NEWPRODUCT

Commercial

Royalties

User profit

activities

LUP

LSupplier industy GOALS1. Bring new technology to market2. Establish new possibilities for the

industry3. Availability of new products, giving

Statoil reduced cost, environmental profit, and increased safety

STATOILS CONTRIBUTION1. Define user

requirements2. Technical competence3. Project control4. Establish contacts5. Advising

PROJECT STATUS LUP - 2000

2%

18%

9%5%

66%

0

10

20

30

40

50

60

CommersialLimited commersial successStopped. Commersial goals not achivedStoppedBankrupt

Principles applied in the Development of a Norwegian Oil & Gas Industry

Focus on development of a supply industry sustainable on a long term basis

Contractors to be selected on a transparent, non-discriminatory manner, securing best value for money

Technical solutions and contract management structure that accommodates domestic supply industry

A proactive information policy towards domestic supply industry

Norwegian Oil & Gas “World-Class” ClustersAround 80.000 directly employed in sector

OilCompanies

MainContractors

SystemIntegrators

ProductSuppliers

ServiceCompanies

TYPE OFCOMPANY

Reservoir/Seismic

OffshoreDrilling

Drillingequipment

Down-holeand WellServices

Subsea Platforms/fixed/floaters Decomis-sioning

Field oper-ations andtransporta-tion

SubseaDown-holeand WellServices

Drillingequipment

Equipmentand

Models

Reservoirand

SeismicDrilling

Designand

ProjectManage-

ment

E, I&T

MarineEquipment

MMO,Transpor-

tation Offshore

Supply

Operator/Duty

holderDecom

Emerging Clusters Established Clusters

Su

pp

ly C

hai

n

Value Chain

A sustainable future for Norway?

Fewer discoveries and developments in Norway will shift industry focus towards operational challenges and internationalisation

Many Norwegian companies already co-operate with local industry in other countries, using their capital and technology to develop competitive local companies

Statoil strongly believes that supporting local industry to become competent and competitive will bring benefits to Statoil, the oil and gas industry and the host country later

And for Brazil?

Brazil already has a nucleus of an oil and gas cluster in Rio/Niteroi and a number of competent companies in related areas

Brazil has strong universities offering higher education in all relevant areas

Brazil has strong industry associations and are used to establishing industry-wide development programs

Brazil has a strong national champion for the development of a competitive national industry

Going forward

I believe Brazil is in a unique position to develop a national oil and gas cluster

But this will require a long-term view from all engaged Federal and State government and authorities Financing institutions Employees and unions Contractors and service industries Oil and gas companies

which must all understand the potential benefits from co-operating whilst being internationally competitive.

I hope Statoil may be part of this challenging development