solar ready northwest indiana

TRANSCRIPT

SOLAR READY NORTHWEST

INDIANA Kathy Luther

Northwestern Indiana Regional Planning Commission

February 28, 2014

U.S Department Of Energy SunShot Initiative Rooftop Solar Challenge

U.S Department of Energy SunShot Initiative

•The U.S. Department of Energy SunShot Initiative is a collaborative national effort that aggressively drives innovation to make solar energy fully cost-competitive with traditional energy sources before the end of the decade. Through SunShot, DOE supports efforts by private companies, academia, and national laboratories to drive down the cost of solar electricity to $0.06 per kilowatt-hour.

U.S. Department of Energy SunShot Initiative Rooftop Solar Challenge

The U.S. Department of Energy SunShot Initiative Rooftop Solar Challenge incentivizes regional awardee teams to make it easier and more affordable for Americans to go solar. By streamlining permit processes, updating planning and zoning codes, improving standards for connecting solar power to the electric grid, and increasing access to financing, teams will clear a path for rapid expansion of solar energy and serve as models for other communities across the nation.

Solar Ready II

•Partnering with Mid-America Regional Council (MARC), National Association of Regional Councils (NARC), Meister Consultants Group (MCG), and Council of State Governments (CSG).

•Goals are to implement solar best management practices, training materials and methods, and other proven implementation strategies previously established by MARC’s 2012 Solar Ready KC Initiative.

•Ultimately will result in more streamlined and standardized solar practices, and will achieve measurable improvements in solar market conditions and access for ten million people across the US.

Goals of the Solar Ready II (SRII) Program

7

Reduce costs through

regulatory reform

Increase access to financing

Promote solar adoption

Grant Details Major Goals Streamline the permitting process

Update planning and zoning codes

Reduce overall barriers to solar implementation

Funding Amount $90,000 ($75,000 plus $15,000 if goals are met)

Timeframe 18 to 30 months (depending on accomplishments met)

8

Grant Details National Partners •Mid-America Regional Council (MARC) •National Association of Regional Councils (NARC) •Meister Consultants Group •Council of State Governments

9

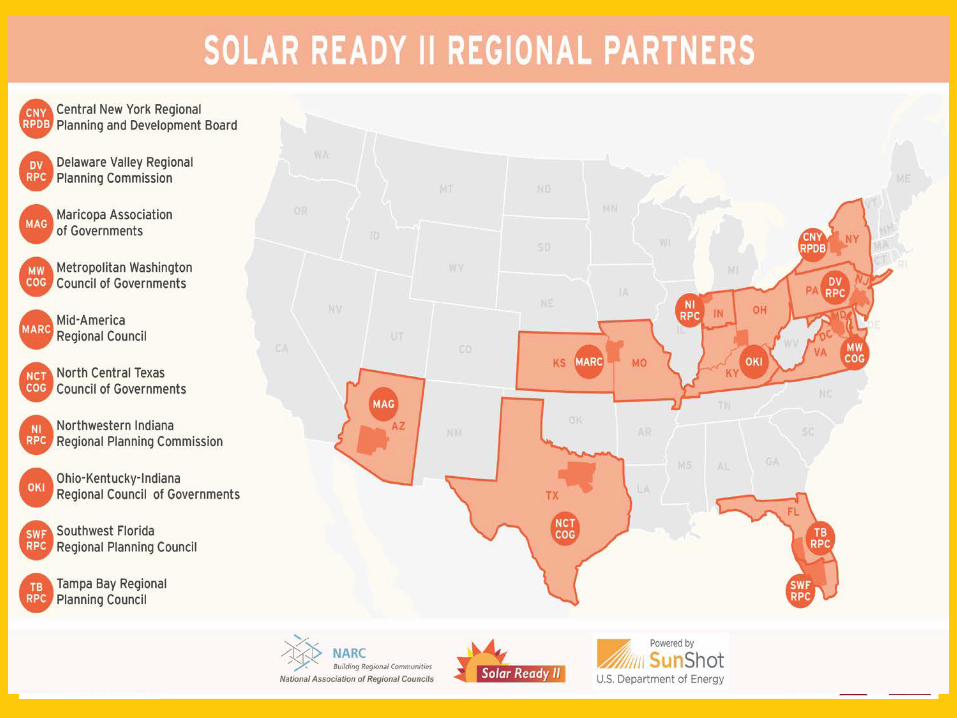

Grant Details Regional Participants •Central New York Regional Planning & Development Board (CNYRPDB) •Delaware Valley Regional Planning Commission (DVRPC) •Maricopa Association of Governments (MAG) •Metropolitan Washington Council of Governments (MWCOG) •North Central Texas Council of Governments (NCTCOG) •Northwester Indiana Regional Planning Commission (NIRPC) •Ohio Kentucky Indiana Regional Council of Governments (OKI) •Southwestern Florida Regional Planning Commission (SWFRPC) •Tampa Bay Regional Planning Commission (TBRPC) 10

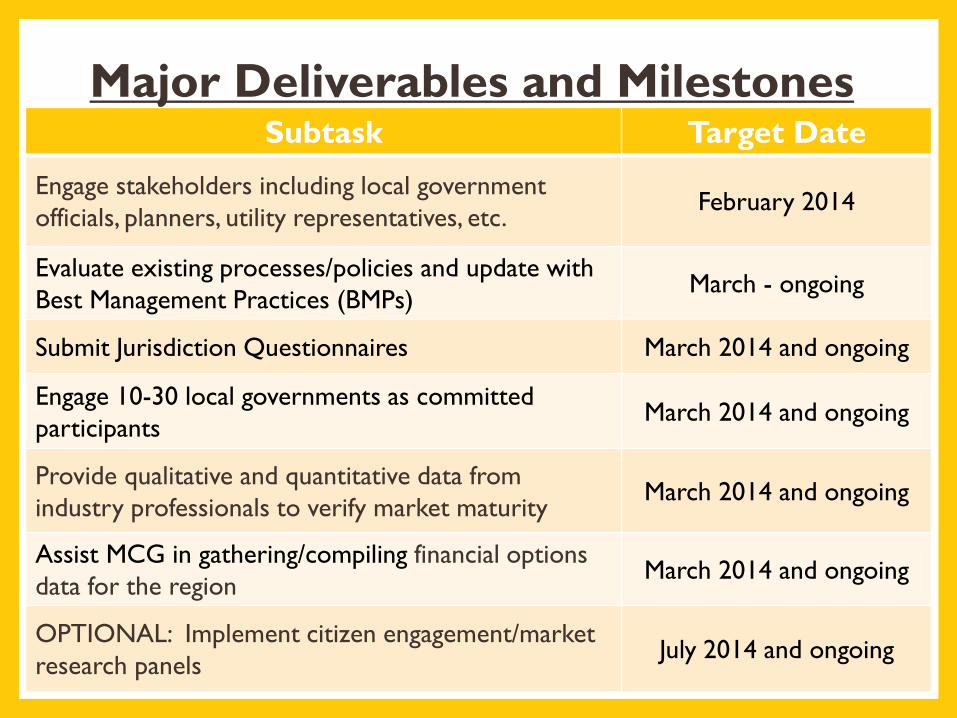

Major Deliverables and Milestones

11

Subtask Target Date

Engage stakeholders including local government officials, planners, utility representatives, etc. February 2014

Evaluate existing processes/policies and update with Best Management Practices (BMPs) March - ongoing

Submit Jurisdiction Questionnaires March 2014 and ongoing

Engage 10-30 local governments as committed participants March 2014 and ongoing

Provide qualitative and quantitative data from industry professionals to verify market maturity March 2014 and ongoing

Assist MCG in gathering/compiling financial options data for the region March 2014 and ongoing

OPTIONAL: Implement citizen engagement/market research panels July 2014 and ongoing

Kathy Luther Director of Environmental Programs

NIRPC

[email protected] (219) 763-6060 x 127

www.nirpc.org/environment/solar

Mia Colson National Contact

National Association of Regional Councils

[email protected] (202) 986-1032, x218

www.narc.org/solarready

Acknowledgment: This material is based upon work supported by the U.S. Department of Energy under Award Number DE-EE0006310 Disclaimer: This presentation was prepared as an account of work sponsored by an agency of the United States Government. Neither the United Sates Government nor any agency thereof, nor any of their employees, makes any warranty, express or implied, or assumes any legal liability or responsibility for the accuracy, completeness, or usefulness of any information, apparatus, product, or process disclosed, or represents that its use would not infringe privately owned rights. Reference herein to any specific commercial product, process, or service by trade name, trademark, manufacturer, or otherwise does not necessarily constitute or imply its endorsement, recommendation, or favoring by the United States Government or any agency thereof. The views and opinions of authors expressed herein do not necessarily state or reflect those of the United States Government or any agency thereof.

http://www.eere.energy.gov/solarchallenge/index.html

Benefits and Barriers to Solar

Adoption in Your Region

Who Are We?

2

100 Consultants

7 offices worldwide

U.S. HQ in Boston

15 years experience

Using global best practices

to inform local decisions

Meister Consultants Group

(617) 209 -1986

Chad LaurentMeister Consultants Group

(617) 209 -1990

Jayson Uppal

Stakeholders

Elected

Officials

Local

Constituents

Business &

IndustryRegional

Utilities

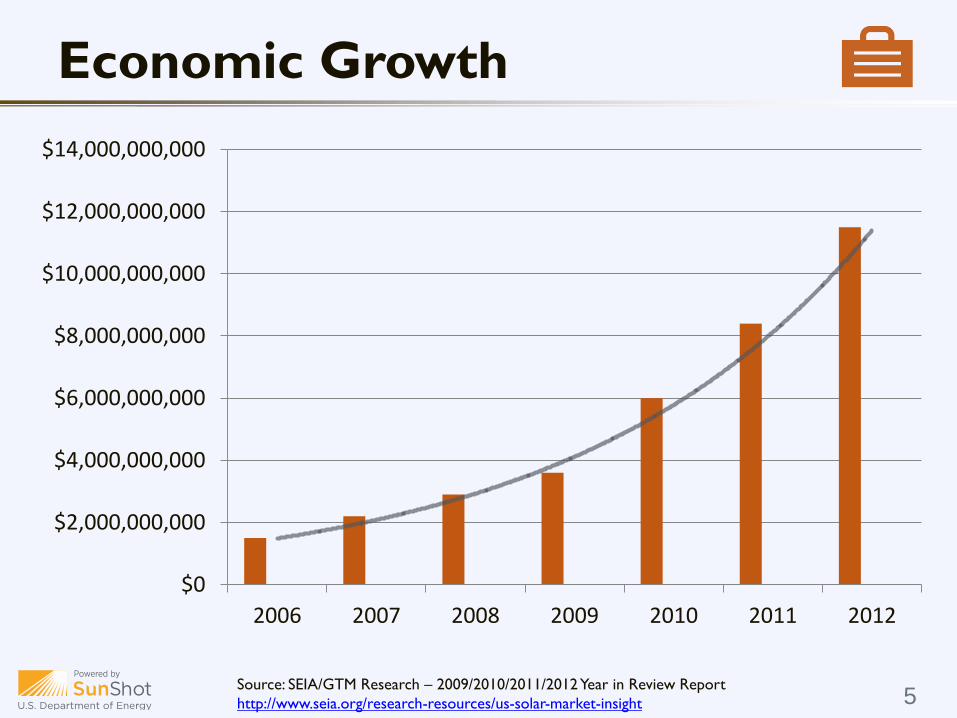

Economic Growth

Source: SEIA/GTM Research – 2009/2010/2011/2012 Year in Review Report

http://www.seia.org/research-resources/us-solar-market-insight 5

$0

$2,000,000,000

$4,000,000,000

$6,000,000,000

$8,000,000,000

$10,000,000,000

$12,000,000,000

$14,000,000,000

2006 2007 2008 2009 2010 2011 2012

Job Creation

Source: SEIA Estimates (2006-2009), The Solar Foundation’s National Solar Jobs Census 2010

(2010), The Solar Foundation’s National Solar Jobs Census 2012 (2011-2012). 6

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2006 2007 2008 2009 2010 2011 2012 2013

Solar Job Growth in the US

SEIA

Estimates

The Solar

Foundation

Job Creation

Sources: Interstate Renewable Energy Council, The Solar Foundation, Meister Consultants Group 7

0

10,000

20,000

30,000

40,000

50,000

0 500 1000 1500 2000 2500 3000

Num

ber

of So

lar

Jobs

Cumulative Installed Capacity (MW)

Correlation of Market Size & Jobs in Each State

90%

Correlatio

n

Price Stability

Source: ISO New England, Inc. 8

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

180.00

Mar

-03

Jul-

03

No

v-0

3

Mar

-04

Jul-

04

No

v-0

4

Mar

-05

Jul-

05

No

v-0

5

Mar

-06

Jul-

06

No

v-0

6

Mar

-07

Jul-

07

No

v-0

7

Mar

-08

Jul-

08

No

v-0

8

Mar

-09

Jul-

09

No

v-0

9

Mar

-10

Jul-

10

No

v-1

0

Mar

-11

Jul-

11

No

v-1

1

Mar

-12

Jul-

12

No

v-1

2

Mar

-13

Jul-

13

No

v-1

3

$/M

Wh

Date

Historical Avg. Real-Time Wholesale Prices (Boston)

.

Solar homes sold

20% fasterand for

17% morethan the equivalent non-solar homes

in surveyed California subdivisions

Smart Investment for Homes

Source: http://www.nrel.gov/docs/fy07osti/38304-01.pdf 9

From NREL:

Smart Investment for Business

Source: Solar Energy Industries Association

0 20 40 60 80 100

Walmart

Costco

Kohl's

Apple

Ikea

Macy's

Johnson and Johnson

McGraw Hill

Staples

Campbell's Soup

U.S. Foods

Bed Bath and Beyond

Kaiser Permanente

Volkswagen

Walgreen's

Target

Safeway

FedEx

Intel

L'Oreal

General Motors

Toys 'R' Us

White Rose Foods

Dow Jones and Co

Solar Capacity (MW)

Top 20 Companies by Solar Capacity

445 megawatts

deployed as of

August 2013 –

enough to power

73,400 homes

Smart Investment for Gov’t

Source: Borrego Solar 11

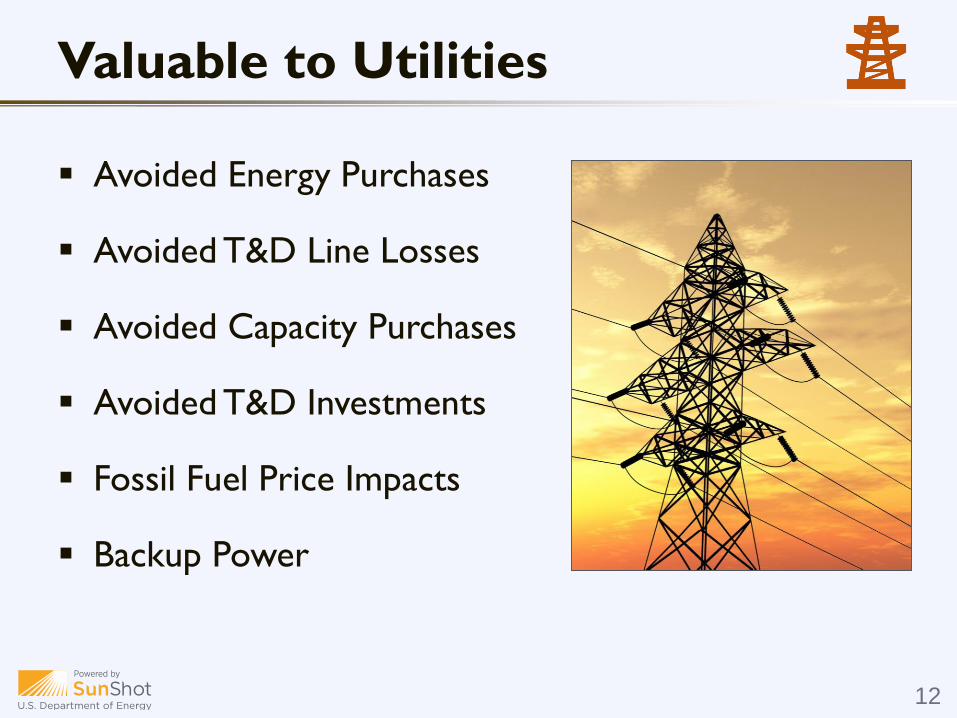

Avoided Energy Purchases

Avoided T&D Line Losses

Avoided Capacity Purchases

Avoided T&D Investments

Fossil Fuel Price Impacts

Backup Power

Valuable to Utilities

12

Valuable to Utilities

Source: Renewable Energy World

2008

2012

Quantified Value

Source: Clean Power Research http://mseia.net/site/wp-content/uploads/2012/05/MSEIA-Final-

Benefits-of-Solar-Report-2012-11-01.pdf

LevelizedValue of Solar ($/MWh) in PA and NJ

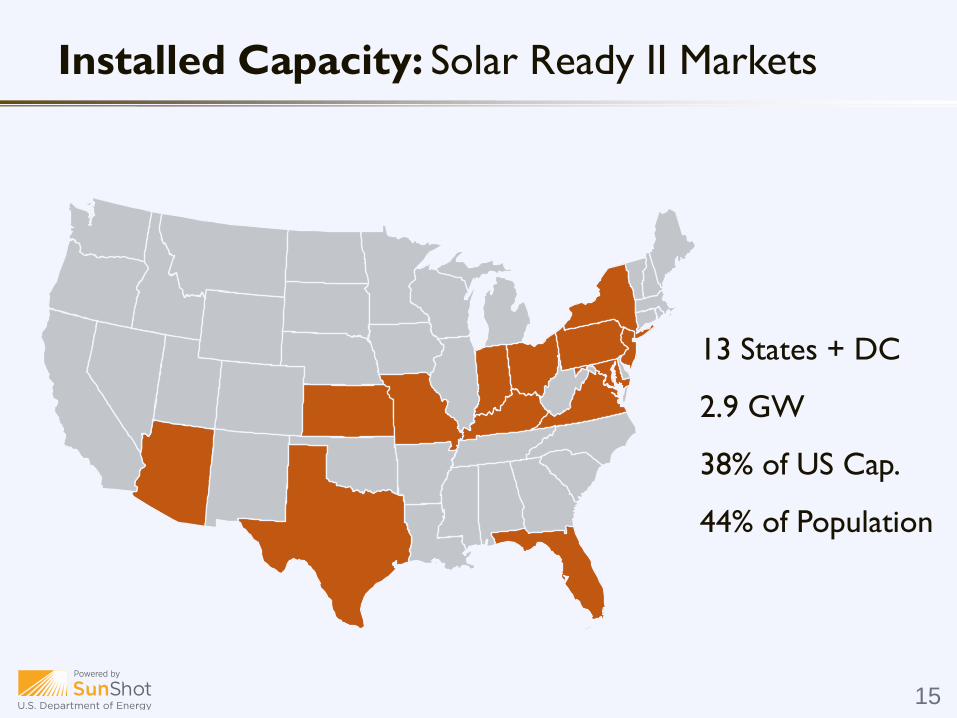

Installed Capacity: Solar Ready II Markets

15

13 States + DC

2.9 GW

38% of US Cap.

44% of Population

Installed Capacity: Solar Ready II Markets

16

0

200

400

600

800

1000

1200

Inst

alled

Cap

acit

y (

MW

)

Cumulative Installed Capacity (2011 - 2012)

Cumulative Installed Capacity 2012

Cumulative Installed Capcaity 2011

Global Installed Capacity

Source: REN 21

Top 5 Countries Solar Operating Capacity (2012)

Germany

Italy

USA

China

Japan

Rest of World

Germany

32 %

USA

7.2%

Global Installed Capacity per Capita

Source: REN 21, World Bank, Interstate Renewable Energy Council

0

50

100

150

200

250

300

350

400

450

Watt

s p

er

Cap

ita

400 Watts

Per Person

23 Watts

Per Person0.67 Watts

Per Person

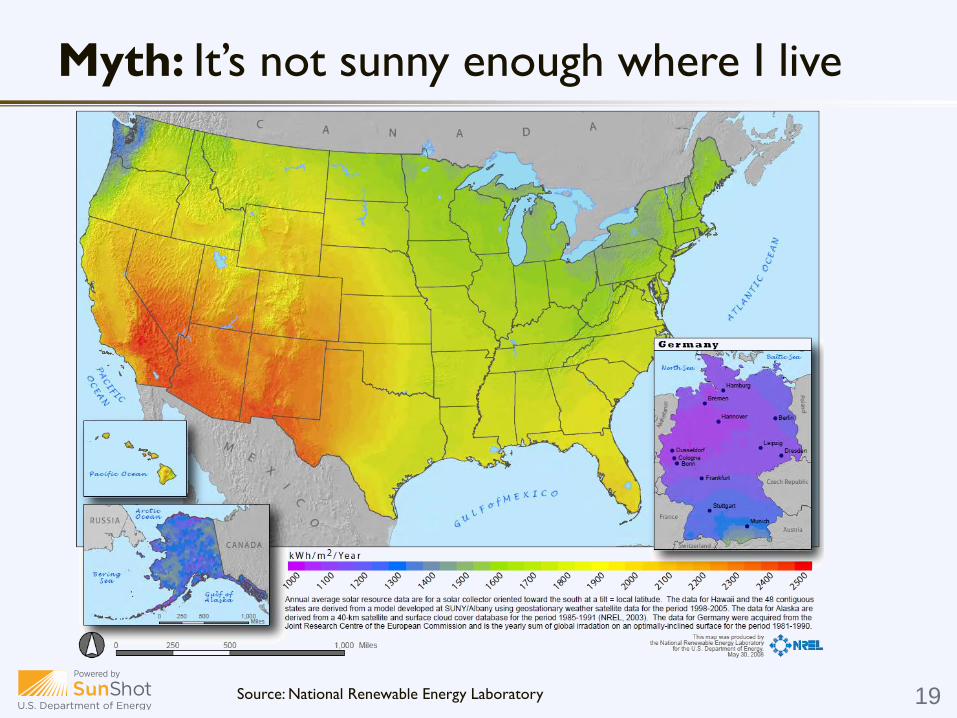

Myth: It’s not sunny enough where I live

Source: National Renewable Energy Laboratory 19

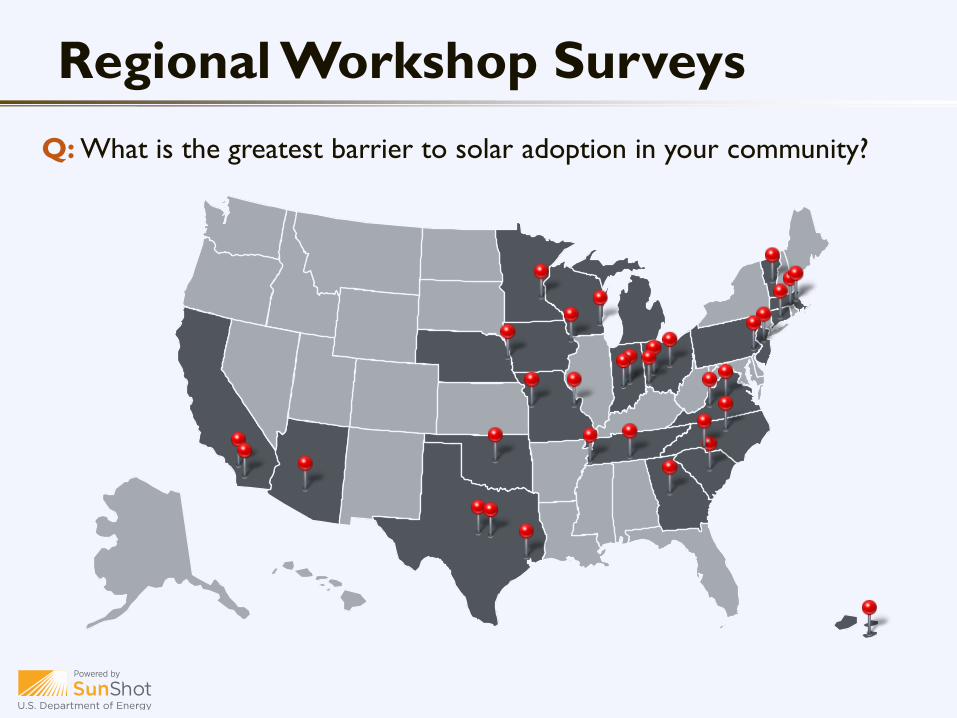

Regional Workshop Surveys

Q: What is the greatest barrier to solar adoption in your community?

Survey Results: Barriers

0 50 100 150 200 250 300 350

High Upfront Cost & Low ROI

Lack of Information & Education

Unfriendly Policy Environment & Lack of Incentives

Local Zoning & Permitting

Utility Support

Aesthetics & Historic Preservation

Lack of Support from HOAs

Reliability Concerns

Environmental Impact

Other

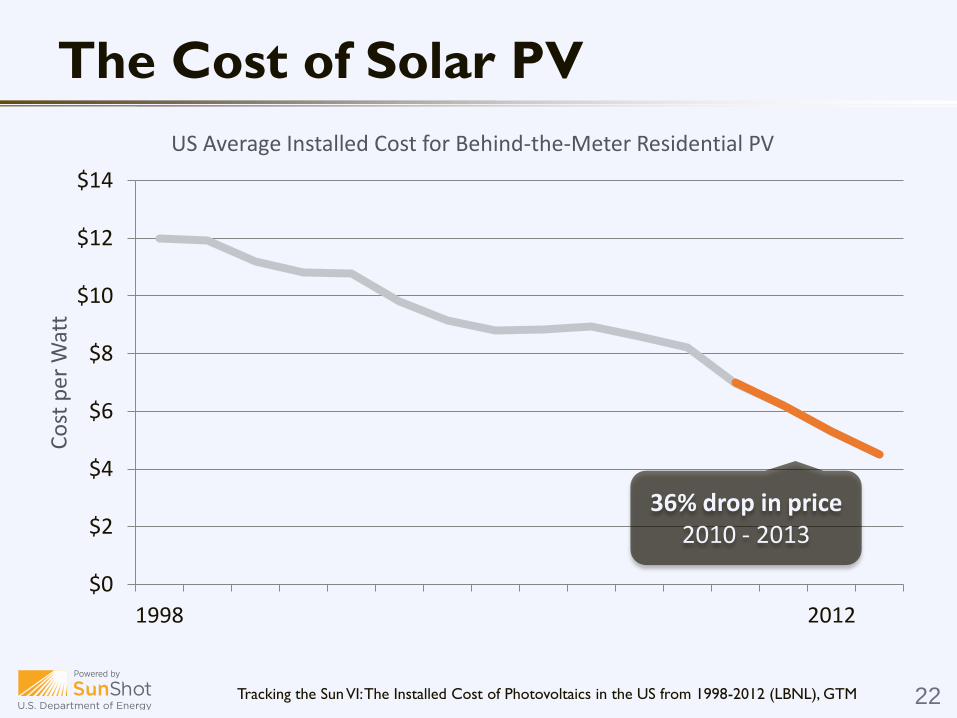

The Cost of Solar PV

Tracking the Sun VI: The Installed Cost of Photovoltaics in the US from 1998-2012 (LBNL), GTM 22

$0

$2

$4

$6

$8

$10

$12

$14

1998 2012

Co

st p

er W

att

US Average Installed Cost for Behind-the-Meter Residential PV

36% drop in price2010 - 2013

The Cost of Solar in the US

Source: Solar Electric Power Association

Co

st o

f El

ect

rici

ty

Time

Solar Price

Retail Price

Wholesale Price

Stage 1

Today

Stage 2 Stage 3

Subsidies and Support

Source: Management Information Services, Inc. October 2011. 60 Years of Energy Incentives: Analysis of

Federal Expenditures for Energy Development; SEIA, May 1, 2012. Federal Energy Incentives Report. 24

0 50 100 150 200 250 300 350 400

Solar

Nuclear

Coal

Natural Gas

Oil

Value of Subsidies and Support ($ billions)

Subsidies for Conventional and Solar Energy, 1950-2010

$104 Billion

$73 Billion

$17 Billion

$369 Billion

$121 Billion

The Cost of Solar in the US

Source: NREL (http://www.nrel.gov/docs/fy14osti/60412.pdf)

LBNL (http://emp.lbl.gov/sites/all/files/lbnl-6350e.pdf)(http://www1.eere.energy.gov/solar/pdfs/sunshot_webinar_20130226.pdf )

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

US Solar Cost German Solar Cost

$ p

er

Watt

Comparison of US and German Solar Costs

Non-Hardware Cost

Total Installed Cost

The Cost of Solar in the US

Source: NREL (http://www.nrel.gov/docs/fy14osti/60412.pdf)

LBNL (http://emp.lbl.gov/sites/all/files/lbnl-6350e.pdf)(http://www1.eere.energy.gov/solar/pdfs/sunshot_webinar_20130226.pdf )

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

US Solar Cost German Solar Cost

$ p

er

Watt

Comparison of US and German Solar Costs

Non-Hardware Cost

Hardware Cost

The Cost of Solar in the US

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

US Solar Cost German Solar Cost

$ p

er

Watt

Comparison of US and German Solar Costs

Non-Hardware Cost

Hardware Cost

Source: NREL (http://www.nrel.gov/docs/fy14osti/60412.pdf)

LBNL (http://emp.lbl.gov/sites/all/files/lbnl-6350e.pdf)(http://www1.eere.energy.gov/solar/pdfs/sunshot_webinar_20130226.pdf )

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

US Solar Cost German Solar Cost

$ p

er

Watt

Comparison of US and German Solar Costs

Column1

Non-Hardware Cost

Hardware Cost

The Cost of Solar in the US

Profits, Taxes, &

Overhead

Source: NREL (http://www.nrel.gov/docs/fy14osti/60412.pdf)

LBNL (http://emp.lbl.gov/sites/all/files/lbnl-6350e.pdf)(http://www1.eere.energy.gov/solar/pdfs/sunshot_webinar_20130226.pdf )

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

US Solar Cost German Solar Cost

$ p

er

Watt

Comparison of US and German Solar Costs

Column1

Non-Hardware Cost

Hardware Cost

The Cost of Solar in the US

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

$ p

er

Wat

t

Other Paperwork

Permitting & Inspection

Financing Costs

Customer Acquisition

Installation Labor

Solar Soft Costs

Source: NREL (http://www.nrel.gov/docs/fy14osti/60412.pdf)

LBNL (http://emp.lbl.gov/sites/all/files/lbnl-6350e.pdf)(http://www1.eere.energy.gov/solar/pdfs/sunshot_webinar_20130226.pdf )

Challenge: Installation Time

Photon Magazine

8 daysfrom inception to completion

Germany

Today

New York City’s

Goal 100 daysfrom inception to completion

0

2

4

6

8

10

12

14

16

18

US Germany

Ho

urs

Average Time to Permit a Solar Installation

Time to Installation

Source: NREL, LBNL

7.2x more man-hours

needed in the US

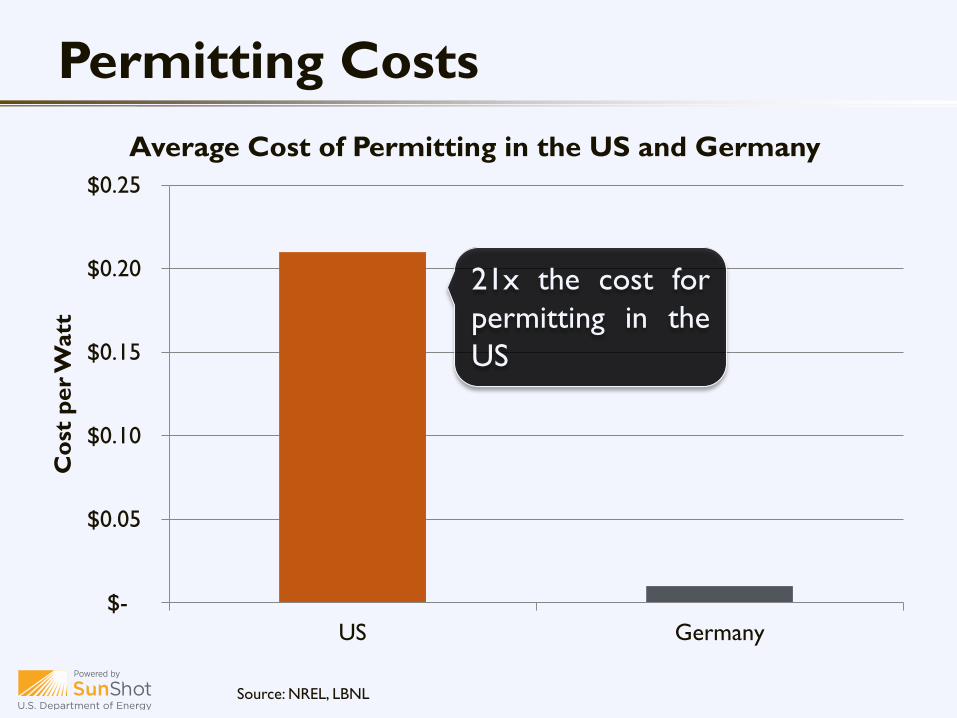

Permitting Costs

Source: NREL, LBNL

$-

$0.05

$0.10

$0.15

$0.20

$0.25

US Germany

Co

st p

er

Watt

Average Cost of Permitting in the US and Germany

21x the cost for

permitting in the

US

Consistency and Transparency

through

Standardized Processes

Germany’s Success

The Cost of Solar in the US

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

2010 2012 2014 2016 2018 2020

$/w

att

Change in Soft Costs and Hardware Costs Over Time

Soft Costs

Hardware Costs

$3.3

2

$3.3

2

$3.2

8

$1.9

0

No change in soft

costs between

2010 and 2012

Enable local governments to replicate

successful solar practices to reduce soft

costs and expand local adoption of solar

energy

Program Goal

Solar Ready Roadmap

36

PlanningZoning Code Improvements

Enable Solar Access

Building Code Improvements

ProcessPermitting Process

ImprovementsPermit Fees

Prequalify Installers

Financing & Solar

Adoption

Distribute Cost Survey to Installers

Engage Local Lenders

Enact a Solarize Program

Step 1 Step 2 Step 3