solar and semiconductor solutions - amtech · pdf file•ald al 2 o 3 solar taking...

TRANSCRIPT

Solar and Semiconductor Solutions

This Presentation may contain certain statements or information that constitute “forward-looking statements” (as defined in

Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as

amended). In some but not all cases, forward-looking statements can be identified by terminology such as, for example,

“may,” “will,” “should,” “would,” “expects,” “plans,” “anticipates,” “intends,” “believes,” “estimates,” “predicts,” “potential,”

“continue,” or the negative of these terms or other comparable terminology. Examples of forward-looking statements include

statements regarding Amtech System, Inc.’s (the “Company”) future financial results, operating results, business strategies,

projected costs, products under development, competitive positions and plans and objectives of the Company and its

management for future operations. Such forward-looking statements and information are provided by the Company based

on current expectations of the Company and reflect various assumptions of management concerning the future

performance of the Company, and are subject to significant business, economic and competitive risks, uncertainties and

contingencies, many of which are beyond the control of the Company. Accordingly, there can be no guarantee that such

forward-looking statements or information will be realized. Actual results may vary from any anticipated results included in

such forward-looking statements and information and such variations may be material. No representations or warranties are

made as to the accuracy or reasonableness of any expectations or assumptions or the forward-looking statements or

information based thereon. Only those representations and warranties that are made in a definitive written agreement

relating to a transaction, when and if executed, and subject to any limitations and restrictions as may be specified in such

definitive agreement, shall have any effect, legal or otherwise. Each recipient of forward-looking statements should make

an independent assessment of the merits of and should consult its own professional advisors. Except as required by law,

we undertake no obligation to publicly update forward-looking statements, whether as a result of new information, future

events, or otherwise.

Safe Harbor Statement

2

Investment Highlights

3

▪ Market leader in developing and producing key manufacturing equipment used in the production of solar, semiconductor and electronics components

▪ Focused on manufacturing innovation in three end markets:

▪ Solar: equipment addresses over 50% of cell manufacturing process, with advanced and next generation solutions

− Successful development of solar PECVD, high density diffusion systems, n-PERT and PERC cell solutions, and next generation solar N-type cell technologies

▪ Semiconductors and Electronics: equipment used in key thermal processes for packaging and assembly of chips

− Successful development of new generation reflow equipment / technologies

− Successful development of 300mm Analog/Power Chip diffusion furnace

▪ LEDs: equipment used in polishing and lapping

▪ Large and growing end markets; Technology driven upgrade cycle underway

▪ Solar: Multi-year technology driven capacity upgrade cycle in solar

− China is driving the technology expansion driven by government policies and subsidies favoring high efficiency

▪ Semiconductors and Electronics: steady global base growth with potential upside from Chinese buildout

▪ Strong financials and order momentum

▪ Four consecutive quarters of bookings and backlog growth

− F3Q’17 record backlog/bookings of $126mn (up 44% Q/Q and 97% Y/Y) / $79.9mn (up 17% Q/Q and 166% YoY)

− Amtech is seeing order strength for both its tools and "turn-key" lines; its largest “turn-key” customer is undergoing a 1GW expansion, of which only half has been booked to date

▪ Book-to-bill ratio of 1.7x in F3Q’17

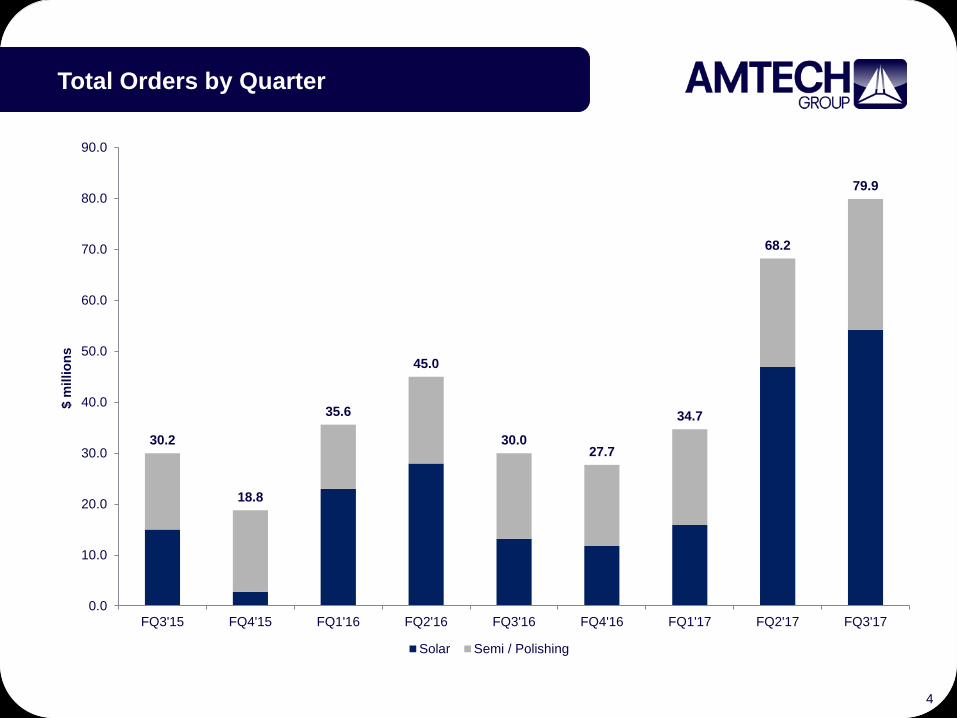

Total Orders by Quarter

30.2

18.8

35.6

45.0

30.027.7

34.7

68.2

79.9

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

FQ3'15 FQ4'15 FQ1'16 FQ2'16 FQ3'16 FQ4'16 FQ1'17 FQ2'17 FQ3'17

$ m

illio

ns

Solar Semi / Polishing

4

46.9

34.6

42.9

67.363.8

48.651.5

87.4

125.7

0.0

20.0

40.0

60.0

80.0

100.0

120.0

FQ3'15 FQ4'15 FQ1'16 FQ2'16 FQ3'16 FQ4'16 FQ1'17 FQ2'17 FQ3'17

$ m

illio

ns

Solar Semi / Polishing

Total Backlog by Quarter

* Backlog includes deferred revenue and customer orders that are expected to ship within the next 12 months5

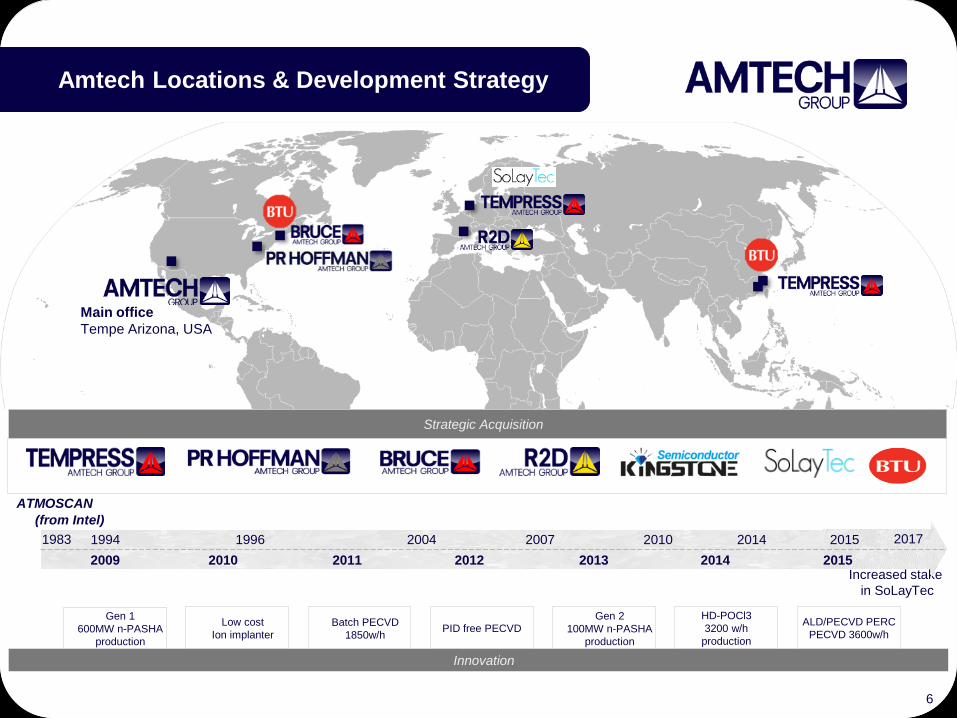

Amtech Locations & Development Strategy

Main office

Tempe Arizona, USA

Increased stake

in SoLayTec

Strategic Acquisition

2009 2012 2013 2014 20152010 2011

HD-POCl3

3200 w/h

production

Gen 1

600MW n-PASHA

production

Batch PECVD

1850w/h

Gen 2

100MW n-PASHA

production

ALD/PECVD PERC

PECVD 3600w/hPID free PECVD

Low cost

Ion implanter

1994 2007 2010 2014 20151996 2004

ATMOSCAN

(from Intel)

1983 2017

Innovation

6

Electronics | LEDSolar

Spatial ALD for PERC

Amtech Markets

LED templates and carriers

High Temp

Custom and Belt SystemsN-PERT / PERC Diffusion

and PECVD Systems

Semiconductor

Furnace & Automation

Reflow Products

Semi Packaging & SMT

7

Solar Value Chain – Integrated Offering

Solar CellSilicon Ingot / Wafer Module

Cleaning

Texturing

Diffusion

Screen Printing

Metallization

Edge Isolation

Testing Sorting

PSG Etching Removal

PECVD (anti-reflective)

Coating

AMTECH GROUP

Products

Integrated Offering

Partnerships

Te

ch

no

log

y

ALD - AL2O3

Passivation (n-type)

8

In solar, Amtech supplies

equipment into 3 key areas

= Quantum

Amtech Brand

= InPassion

= Spectrum

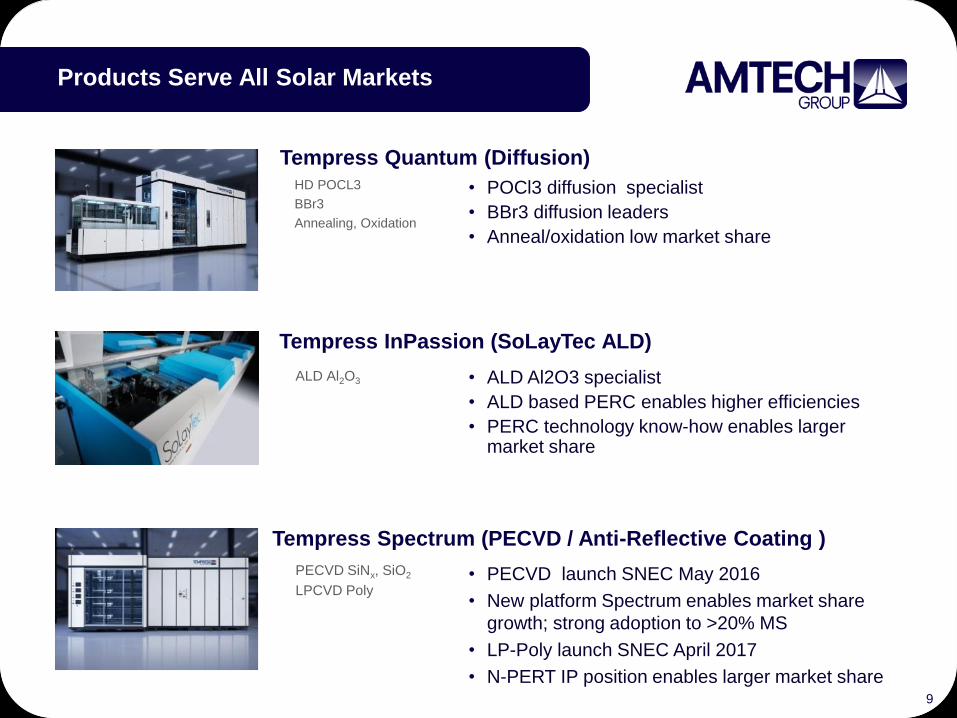

Tempress Quantum (Diffusion)

Tempress Spectrum (PECVD / Anti-Reflective Coating )

PECVD SiNx, SiO2

LPCVD Poly

HD POCL3

BBr3

Annealing, Oxidation

Tempress InPassion (SoLayTec ALD)

ALD Al2O3

Products Serve All Solar Markets

9

• PECVD launch SNEC May 2016

• New platform Spectrum enables market share

growth; strong adoption to >20% MS

• LP-Poly launch SNEC April 2017

• N-PERT IP position enables larger market share

• POCl3 diffusion specialist

• BBr3 diffusion leaders

• Anneal/oxidation low market share

• ALD Al2O3 specialist

• ALD based PERC enables higher efficiencies

• PERC technology know-how enables larger market share

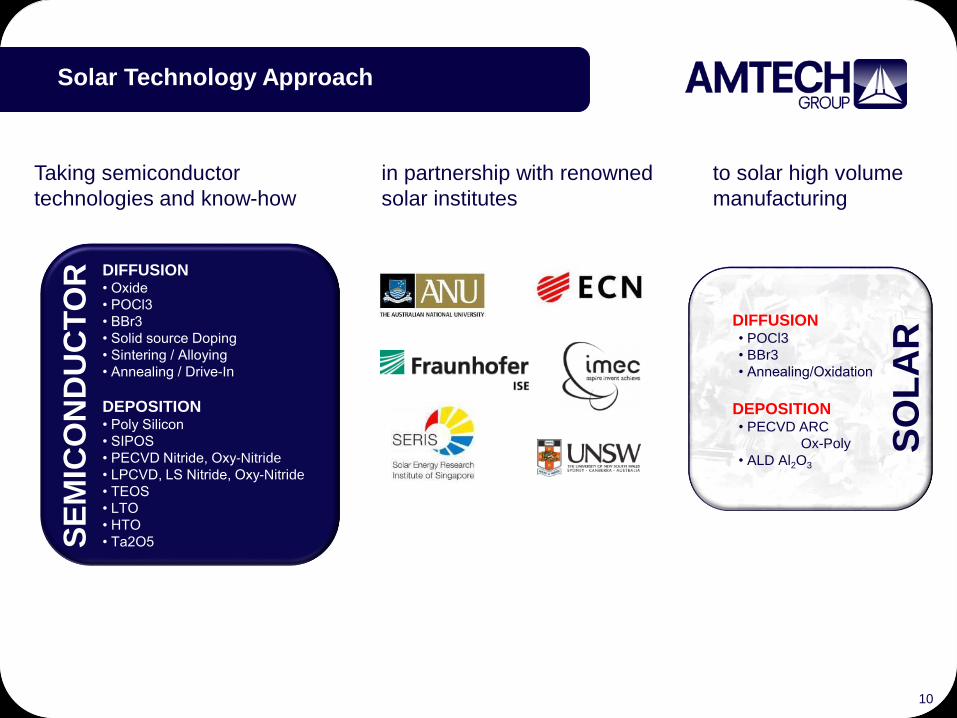

Solar Technology Approach

DIFFUSION• POCl3

• BBr3

• Annealing/Oxidation

DEPOSITION• PECVD ARC

Ox-Poly

• ALD Al2O3

SO

LA

R

Taking semiconductor

technologies and know-how

10

in partnership with renowned

solar institutes

to solar high volume

manufacturing

DIFFUSION• Oxide

• POCl3

• BBr3

• Solid source Doping

• Sintering / Alloying

• Annealing / Drive-In

DEPOSITION• Poly Silicon

• SIPOS

• PECVD Nitride, Oxy-Nitride

• LPCVD, LS Nitride, Oxy-Nitride

• TEOS

• LTO

• HTO

• Ta2O5SE

MIC

ON

DU

CT

OR

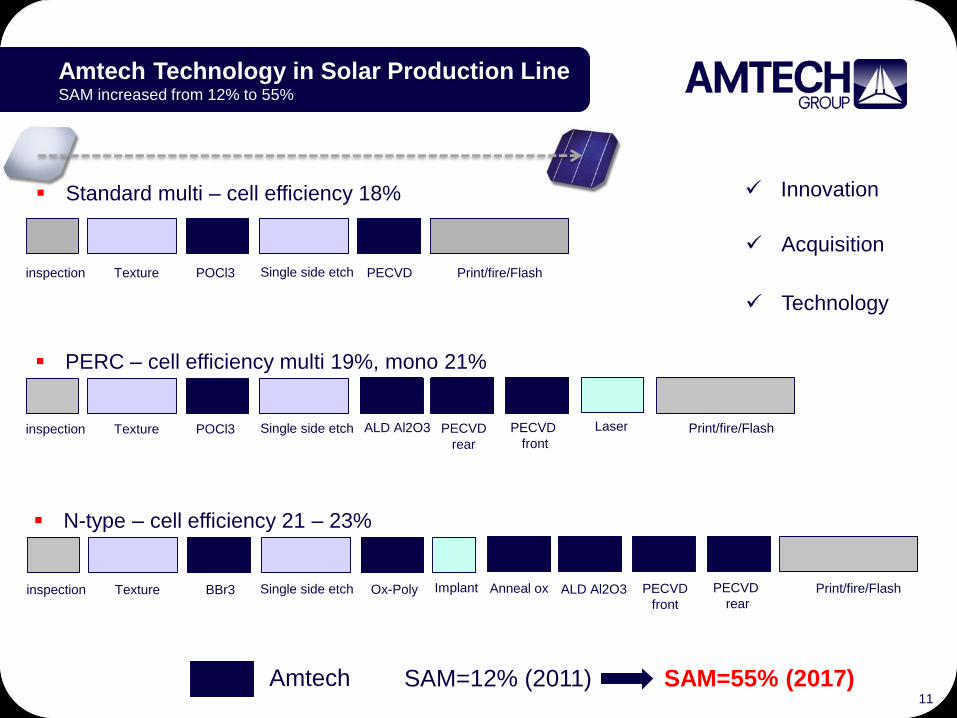

Amtech Technology in Solar Production LineSAM increased from 12% to 55%

▪ Standard multi – cell efficiency 18%

inspection Texture POCl3 Single side etch PECVD Print/fire/Flash

▪ PERC – cell efficiency multi 19%, mono 21%

inspection Texture POCl3 Single side etch PECVD

rear

Print/fire/FlashALD Al2O3 PECVD

front

Laser

✓ Innovation

✓ Acquisition

✓ Technology

▪ N-type – cell efficiency 21 – 23%

inspection Texture BBr3 Single side etch PECVD

front

Print/fire/FlashImplant PECVD

rearALD Al2O3Anneal ox

Amtech SAM=12% (2011) SAM=55% (2017)

▪ N-type – cell efficiency 21 – 23%

inspection Texture BBr3 Single side etch PECVD

front

Print/fire/FlashImplant PECVD

rearALD Al2O3Anneal oxOx-Poly

11

Wafer Market Share

12Source: ITRPV 8th edition 2017 – report release and key findings

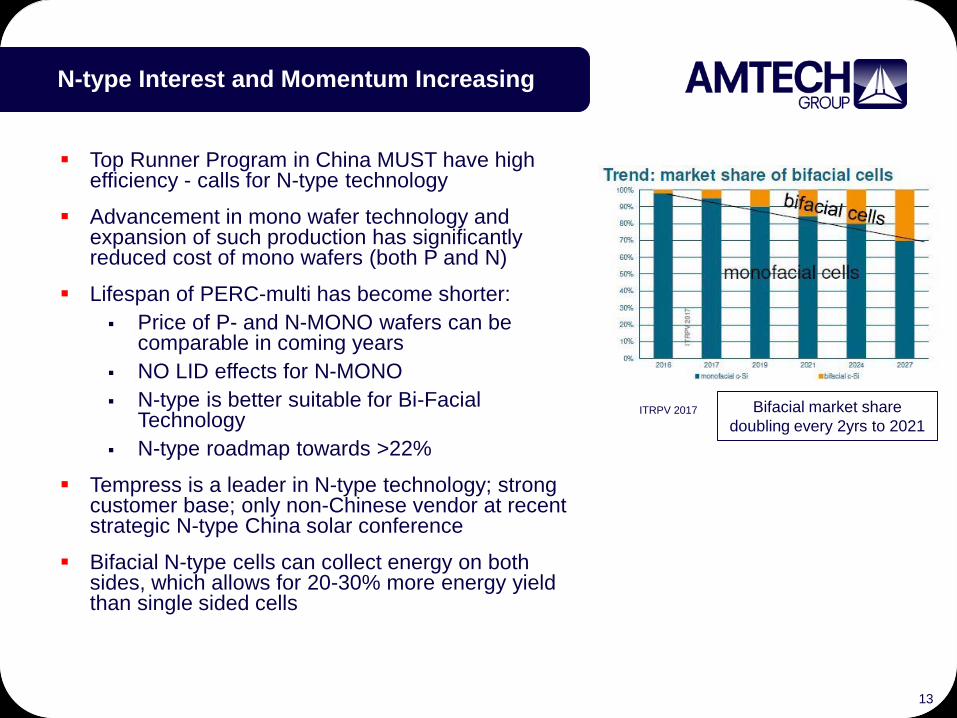

N-type Interest and Momentum Increasing

▪ Top Runner Program in China MUST have high efficiency - calls for N-type technology

▪ Advancement in mono wafer technology and expansion of such production has significantly reduced cost of mono wafers (both P and N)

▪ Lifespan of PERC-multi has become shorter:

▪ Price of P- and N-MONO wafers can be comparable in coming years

▪ NO LID effects for N-MONO

▪ N-type is better suitable for Bi-Facial Technology

▪ N-type roadmap towards >22%

▪ Tempress is a leader in N-type technology; strong customer base; only non-Chinese vendor at recent strategic N-type China solar conference

▪ Bifacial N-type cells can collect energy on both sides, which allows for 20-30% more energy yield than single sided cells

Bifacial market share

doubling every 2yrs to 2021ITRPV 2017

13

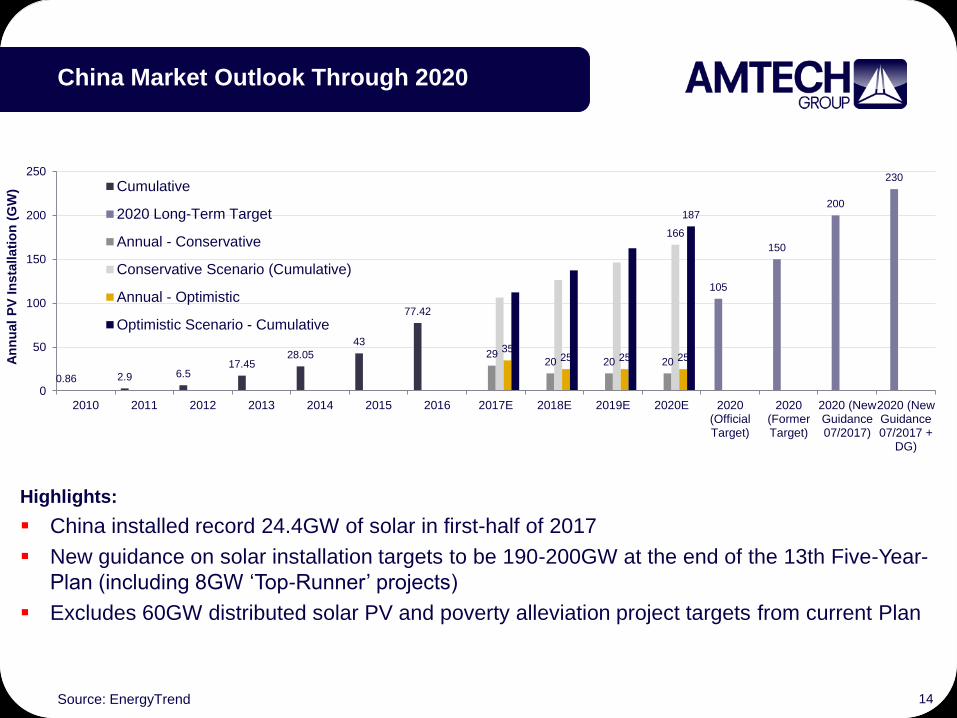

China Market Outlook Through 2020

14

Highlights:

▪ China installed record 24.4GW of solar in first-half of 2017

▪ New guidance on solar installation targets to be 190-200GW at the end of the 13th Five-Year-

Plan (including 8GW ‘Top-Runner’ projects)

▪ Excludes 60GW distributed solar PV and poverty alleviation project targets from current Plan

Source: EnergyTrend

0.86 2.9 6.517.45

28.05

43

77.42

105

150

200

230

2920 20 20

166

35 25 25 25

187

0

50

100

150

200

250

2010 2011 2012 2013 2014 2015 2016 2017E 2018E 2019E 2020E 2020(OfficialTarget)

2020(FormerTarget)

2020 (NewGuidance07/2017)

2020 (NewGuidance07/2017 +

DG)

An

nu

al

PV

In

sta

llati

on

(G

W) Cumulative

2020 Long-Term Target

Annual - Conservative

Conservative Scenario (Cumulative)

Annual - Optimistic

Optimistic Scenario - Cumulative

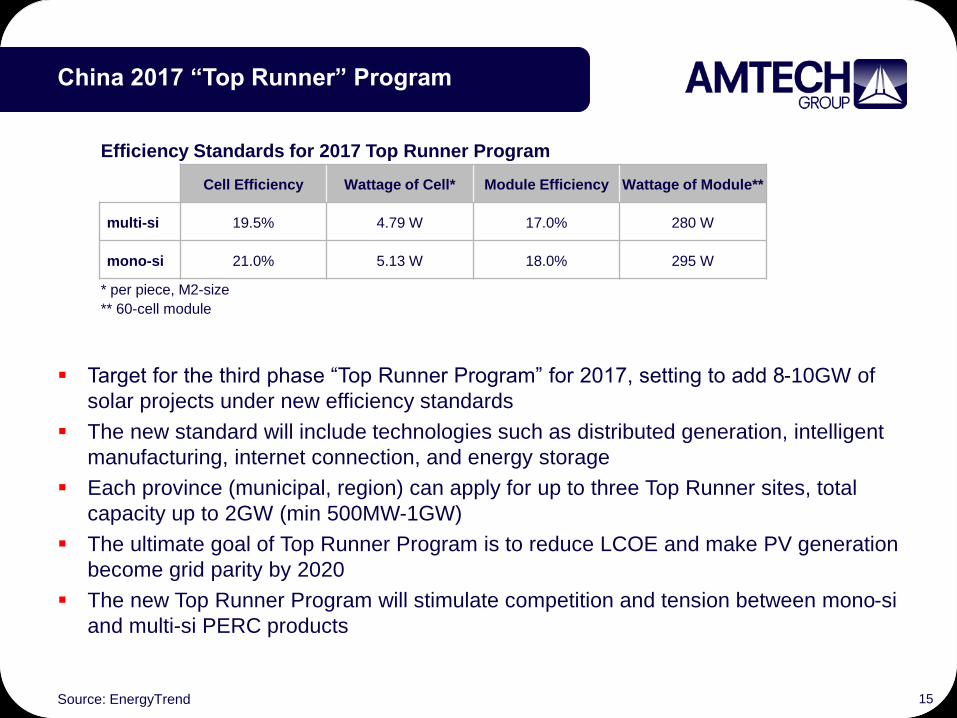

China 2017 “Top Runner” Program

15

▪ Target for the third phase “Top Runner Program” for 2017, setting to add 8-10GW of

solar projects under new efficiency standards

▪ The new standard will include technologies such as distributed generation, intelligent

manufacturing, internet connection, and energy storage

▪ Each province (municipal, region) can apply for up to three Top Runner sites, total

capacity up to 2GW (min 500MW-1GW)

▪ The ultimate goal of Top Runner Program is to reduce LCOE and make PV generation

become grid parity by 2020

▪ The new Top Runner Program will stimulate competition and tension between mono-si

and multi-si PERC products

Source: EnergyTrend

Efficiency Standards for 2017 Top Runner Program

Cell Efficiency Wattage of Cell* Module Efficiency Wattage of Module**

multi-si 19.5% 4.79 W 17.0% 280 W

mono-si 21.0% 5.13 W 18.0% 295 W

* per piece, M2-size

** 60-cell module

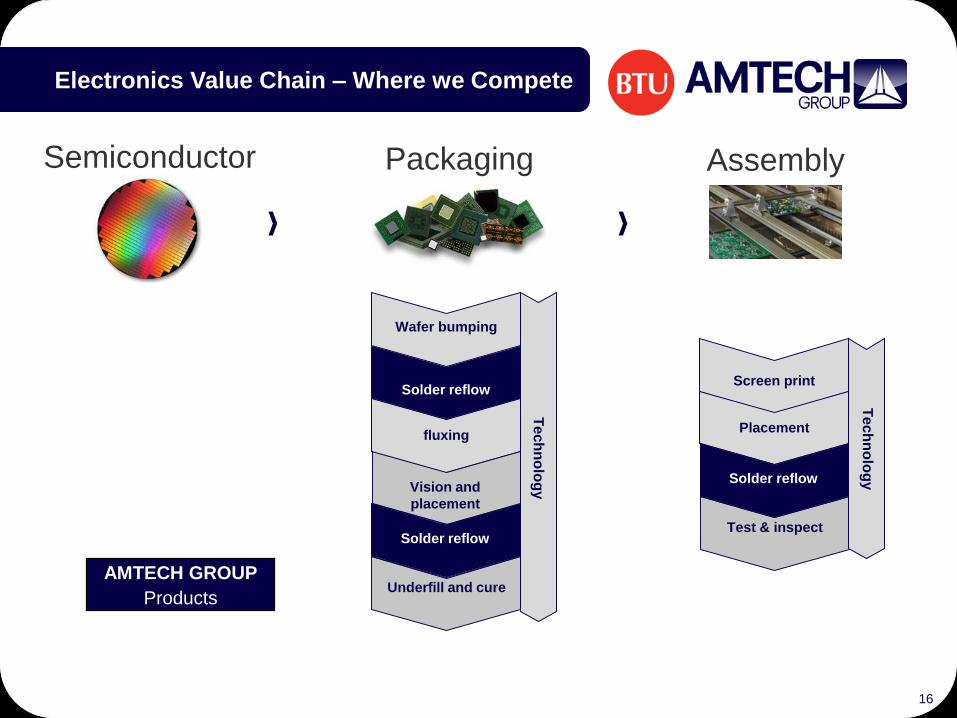

Electronics Value Chain – Where we Compete

AssemblyPackagingSemiconductor

16

Wafer bumping

Solder reflow

Underfill and cure

fluxing

Solder reflow

Te

ch

no

log

yVision and

placement

Screen print

Test & inspect

Placement

Solder reflow

Te

ch

no

log

y

AMTECH GROUP

Products

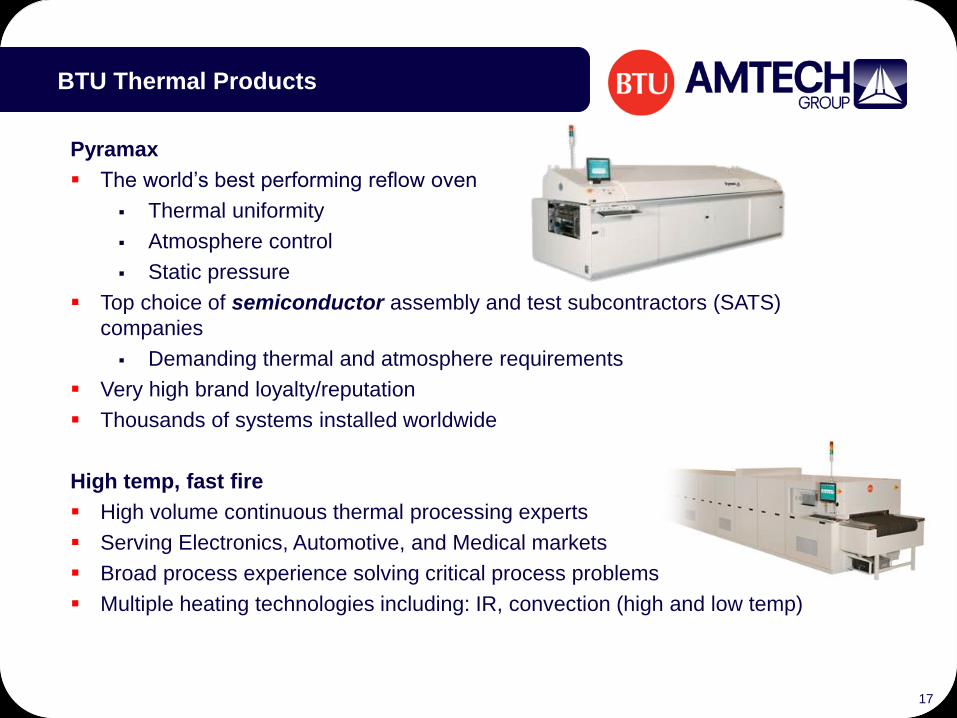

BTU Thermal Products

17

Pyramax

▪ The world’s best performing reflow oven

▪ Thermal uniformity

▪ Atmosphere control

▪ Static pressure

▪ Top choice of semiconductor assembly and test subcontractors (SATS)

companies

▪ Demanding thermal and atmosphere requirements

▪ Very high brand loyalty/reputation

▪ Thousands of systems installed worldwide

High temp, fast fire

▪ High volume continuous thermal processing experts

▪ Serving Electronics, Automotive, and Medical markets

▪ Broad process experience solving critical process problems

▪ Multiple heating technologies including: IR, convection (high and low temp)

BTU’s Diverse Customer Base

18

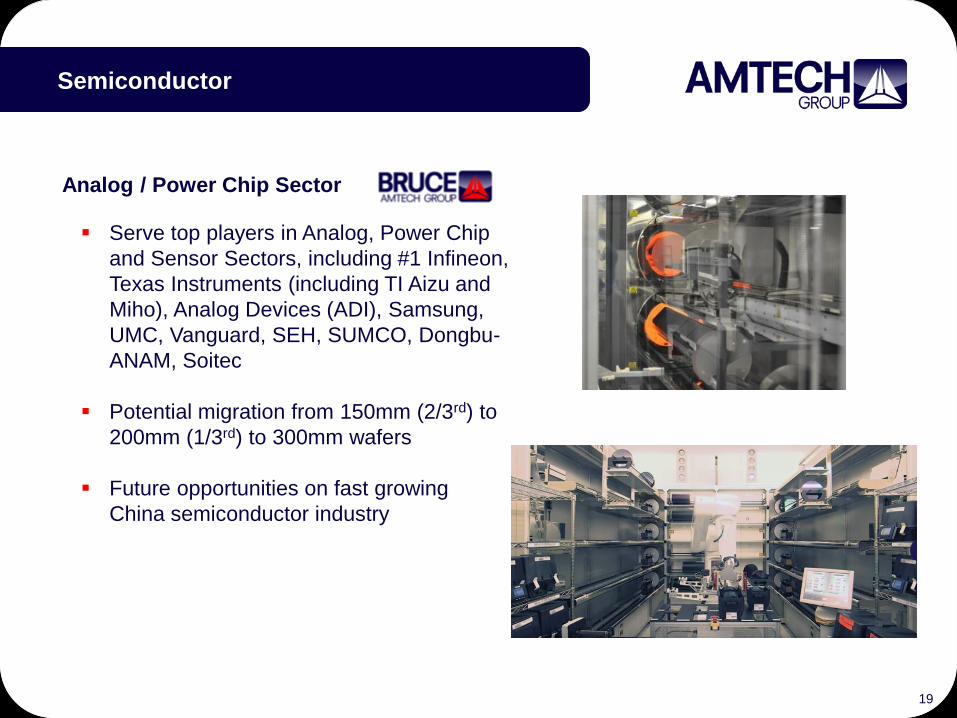

Analog / Power Chip Sector

▪ Serve top players in Analog, Power Chip

and Sensor Sectors, including #1 Infineon,

Texas Instruments (including TI Aizu and

Miho), Analog Devices (ADI), Samsung,

UMC, Vanguard, SEH, SUMCO, Dongbu-

ANAM, Soitec

▪ Potential migration from 150mm (2/3rd) to

200mm (1/3rd) to 300mm wafers

▪ Future opportunities on fast growing

China semiconductor industry

Semiconductor

19

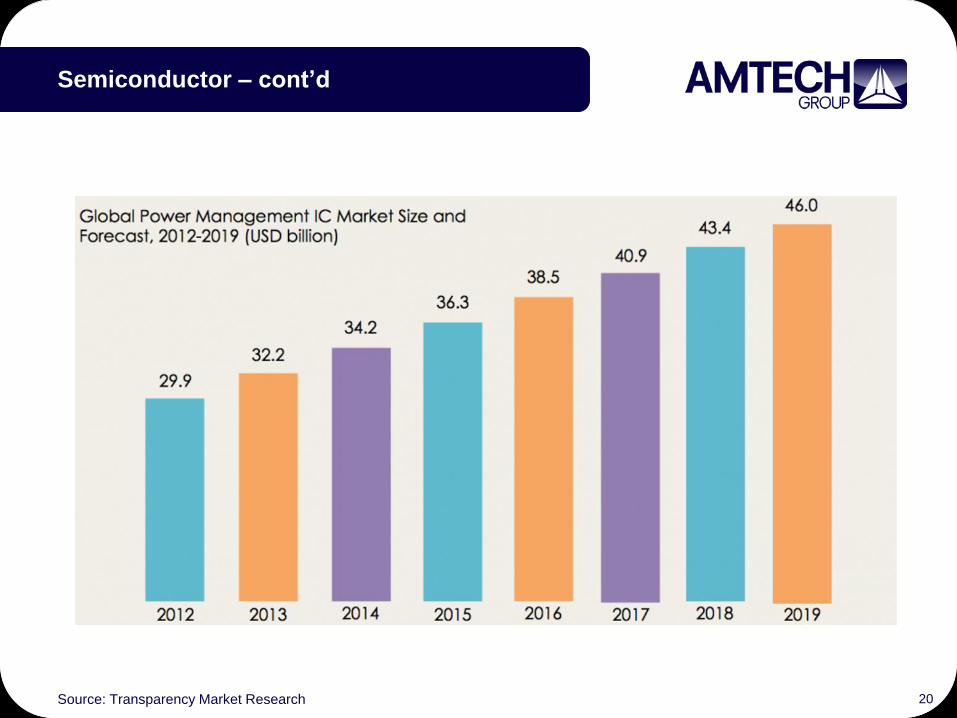

Semiconductor – cont’d

20Source: Transparency Market Research

LED & Optics Highlights

▪ Premier global brand since 1938

▪ Market leader in LED and SEMI polishing

and lapping

▪ LED consumable growth

▪ LED and Optics equipment opportunities

LED

21

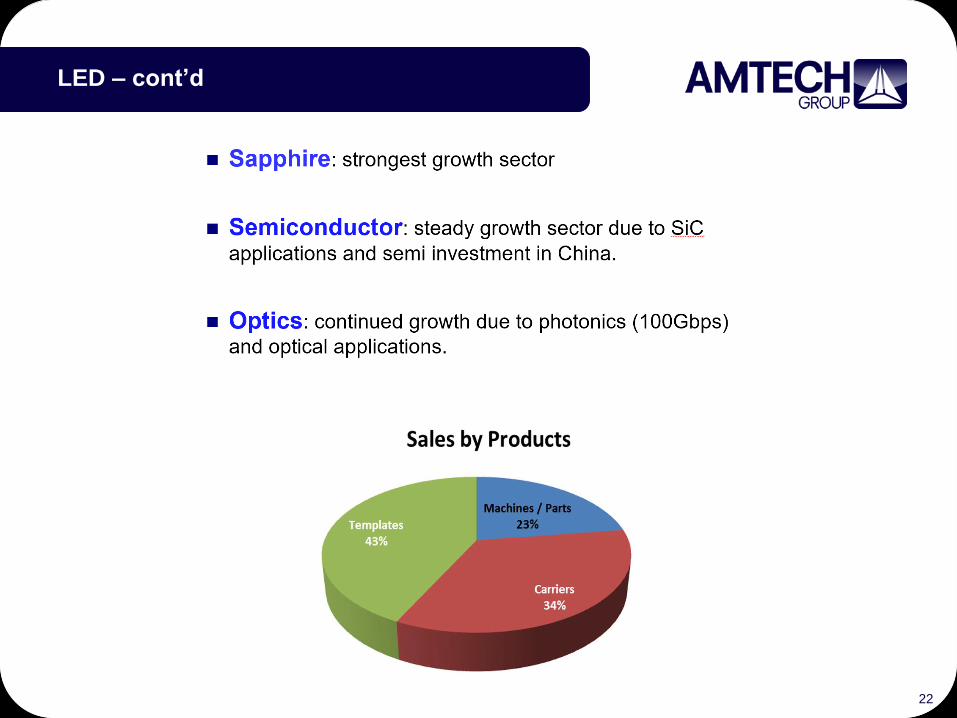

LED – cont’d

22

Financial Overview

23

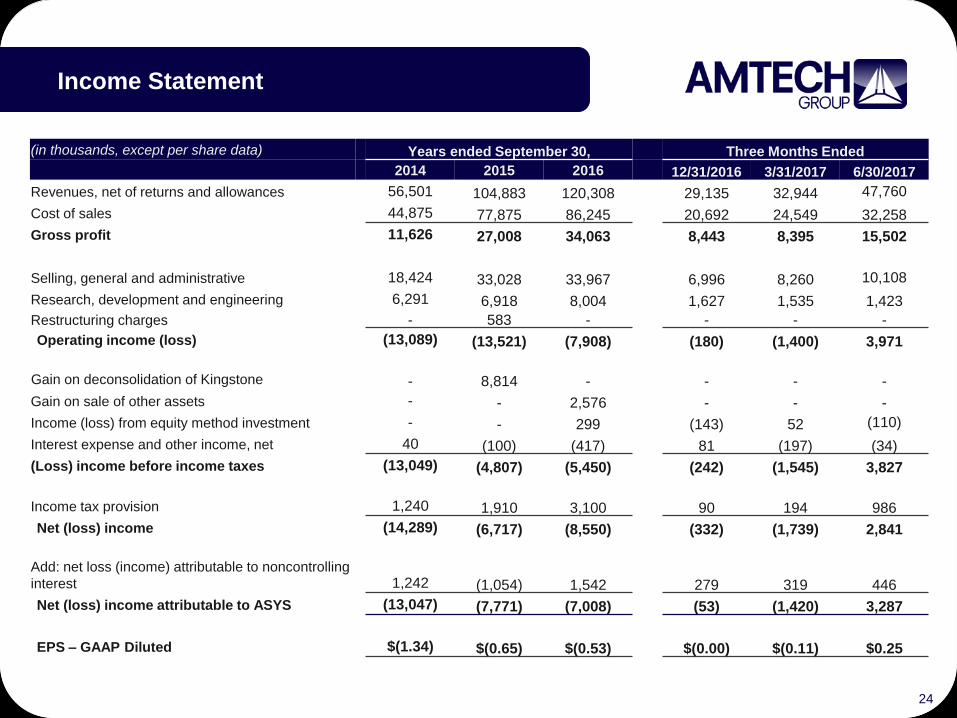

Income Statement

(in thousands, except per share data) Years ended September 30, Three Months Ended

2014 2015 2016 12/31/2016 3/31/2017 6/30/2017

Revenues, net of returns and allowances 56,501 104,883 120,308 29,135 32,944 47,760

Cost of sales 44,875 77,875 86,245 20,692 24,549 32,258

Gross profit 11,626 27,008 34,063 8,443 8,395 15,502

Selling, general and administrative 18,424 33,028 33,967 6,996 8,260 10,108

Research, development and engineering 6,291 6,918 8,004 1,627 1,535 1,423

Restructuring charges - 583 - - - -

Operating income (loss) (13,089) (13,521) (7,908) (180) (1,400) 3,971

Gain on deconsolidation of Kingstone - 8,814 - - - -

Gain on sale of other assets - - 2,576 - - -

Income (loss) from equity method investment - - 299 (143) 52 (110)

Interest expense and other income, net 40 (100) (417) 81 (197) (34)

(Loss) income before income taxes (13,049) (4,807) (5,450) (242) (1,545) 3,827

Income tax provision 1,240 1,910 3,100 90 194 986

Net (loss) income (14,289) (6,717) (8,550) (332) (1,739) 2,841

Add: net loss (income) attributable to noncontrolling

interest 1,242 (1,054) 1,542 279 319 446

Net (loss) income attributable to ASYS (13,047) (7,771) (7,008) (53) (1,420) 3,287

EPS – GAAP Diluted $(1.34) $(0.65) $(0.53) $(0.00) $(0.11) $0.25

24

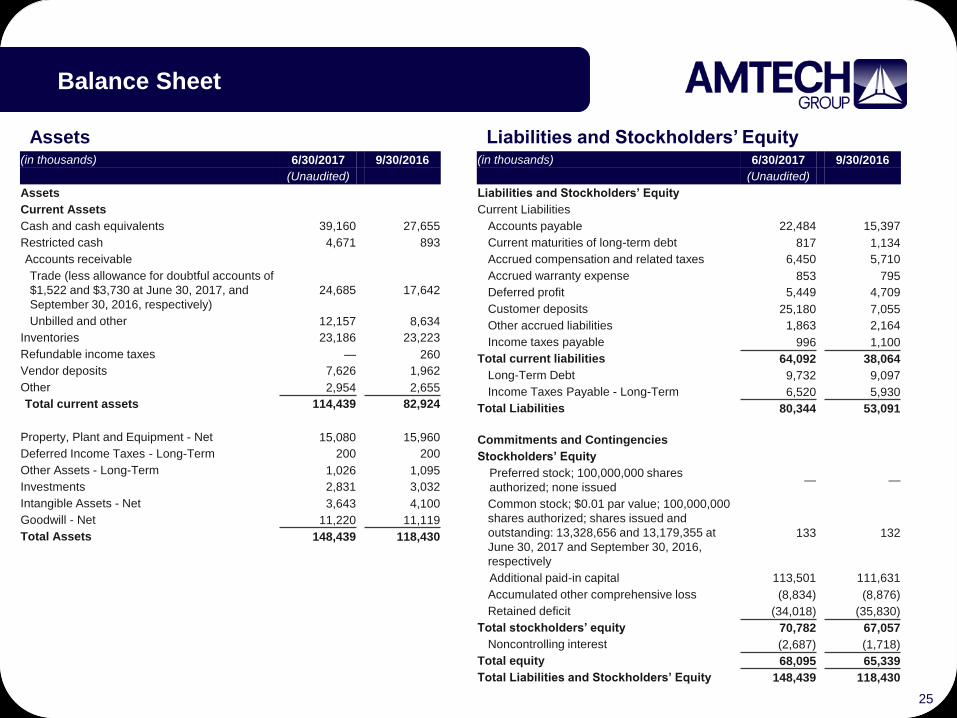

Balance Sheet

(in thousands) 6/30/2017 9/30/2016

(Unaudited)

Assets

Current Assets

Cash and cash equivalents 39,160 27,655

Restricted cash 4,671 893

Accounts receivable

Trade (less allowance for doubtful accounts of

$1,522 and $3,730 at June 30, 2017, and

September 30, 2016, respectively)

24,685 17,642

Unbilled and other 12,157 8,634

Inventories 23,186 23,223

Refundable income taxes — 260

Vendor deposits 7,626 1,962

Other 2,954 2,655

Total current assets 114,439 82,924

Property, Plant and Equipment - Net 15,080 15,960

Deferred Income Taxes - Long-Term 200 200

Other Assets - Long-Term 1,026 1,095

Investments 2,831 3,032

Intangible Assets - Net 3,643 4,100

Goodwill - Net 11,220 11,119

Total Assets 148,439 118,430

(in thousands) 6/30/2017 9/30/2016

(Unaudited)

Liabilities and Stockholders’ Equity

Current Liabilities

Accounts payable 22,484 15,397

Current maturities of long-term debt 817 1,134

Accrued compensation and related taxes 6,450 5,710

Accrued warranty expense 853 795

Deferred profit 5,449 4,709

Customer deposits 25,180 7,055

Other accrued liabilities 1,863 2,164

Income taxes payable 996 1,100

Total current liabilities 64,092 38,064

Long-Term Debt 9,732 9,097

Income Taxes Payable - Long-Term 6,520 5,930

Total Liabilities 80,344 53,091

Commitments and Contingencies

Stockholders’ Equity

Preferred stock; 100,000,000 shares

authorized; none issued— —

Common stock; $0.01 par value; 100,000,000

shares authorized; shares issued and

outstanding: 13,328,656 and 13,179,355 at

June 30, 2017 and September 30, 2016,

respectively

133 132

Additional paid-in capital 113,501 111,631

Accumulated other comprehensive loss (8,834) (8,876)

Retained deficit (34,018) (35,830)

Total stockholders’ equity 70,782 67,057

Noncontrolling interest (2,687) (1,718)

Total equity 68,095 65,339

Total Liabilities and Stockholders’ Equity 148,439 118,430

Assets Liabilities and Stockholders’ Equity

25

Investment Highlights

26

▪ Market leader in developing and producing key manufacturing equipment used in the production of solar, semiconductor and electronics components

▪ Focused on manufacturing innovation in three end markets:

▪ Solar: equipment addresses over 50% of cell manufacturing process, with advanced and next generation solutions

− Successful development of solar PECVD, high density diffusion systems, n-PERT and PERC cell solutions, and next generation solar N-type cell technologies

▪ Semiconductors and Electronics: equipment used in key thermal processes for packaging and assembly of chips

− Successful development of new generation reflow equipment / technologies

− Successful development of 300mm Analog/Power Chip diffusion furnace

▪ LEDs: equipment used in polishing and lapping

▪ Large and growing end markets; Technology driven upgrade cycle underway

▪ Solar: Multi-year technology driven capacity upgrade cycle in solar

− China is driving the technology expansion driven by government policies and subsidies favoring high efficiency

▪ Semiconductors and Electronics: steady global base growth with potential upside from Chinese buildout

▪ Strong financials and order momentum

▪ Four consecutive quarters of bookings and backlog growth

− F3Q’17 record backlog/bookings of $126mn (up 44% Q/Q and 97% Y/Y) / $79.9mn (up 17% Q/Q and 166% YoY)

− Amtech is seeing order strength for both its tools and "turn-key" lines; its largest “turn-key” customer is undergoing a 1GW expansion, of which only half has been booked to date

▪ Book-to-bill ratio of 1.7x in F3Q’17