smb automation software

TRANSCRIPT

1

1

SMB Automation

Sector Introduction and Thesis

Patrick Montague

2

2

Table of Contents

Summary – Reasons for Interest

3-5 Market Size, Fragmentation, Refresh Rate

6, 7 Innovation/Procurement Cycle

8 Macro Tailwinds: SaaS flexibility, internet distribution, bottom up scaling

9 Precedent Cases

10 Investor Landscape

Industry Map

12 Lifecycle of an SMB

13-16 Business Formation Tools

ERP, Legal, Website/Hosting, Productivity/Communication

17-19 Growth and Customer Acquisition Tools

Sales/CRM, Marketing, Commerce/POS

20-23 Business Management Tools

HCM, Finance, Supply Chain/Product Development, BI/IT

Exit Activity & Incumbent Landscape

25 Current Incumbents

26 Acquisition Activity

3

3

Market Size, Fragmentation, Refresh Rate

United Sates

Sources: SMB Group, US Census Bureau Data, World Bank Estimates (www.smb-gr.com/company/smb-market)

Worldwide

Small Office/Home Office (SoHo)1 – 4 Employees

(No commercial location)

Small Businesses5-99 FTE

Medium Businesses100-999 FTE

&Upper Mid-Market

1,000-2,500 FTE

Enterprise 2,500+ FTE

16.5mm firms (72%)21mm FTE (16%)8% total IT spend(6-7% spend growth)

6.3mm firms (28%)55mm FTE (41%)27% IT spend(7-8% spend growth)

100k firms (0.4%)25mm FTE (20%)19% IT spend(6-7% spend growth)

9,000 firms (0.04%)33mm FTE (23%)46% IT spend(3-4% spend growth)

137mm firms (68%)250mm FTE (18%)10% Total IT spend(7-9% spend growth)

65mm firms (32%)700mm FTE (52%)31% IT spend(8-10% spend gr.)

705k firms (0.3%)225mm FTE (17%)21% IT spend(7-9% spend growth)

52,000k firms (0.03%)200mm FTE (13%)38% IT spend(3-4% spend growth)

4

4

Ind

ust

ry R

isk

Market Size, Fragmentation, Refresh Rate

SMB

Lif

esp

an

1 Year Survival Rate

2 Year Survival Rate

5 Year Survival Rate

10 Year Survival Rate

Annual Turnover

Riskiest Industries

Least Risky Industries

Financing Needs

- ~80%

- 69%

- 49%

- 34%

- 10 – 12% (~550,000 – 650,000 firms)

- Transportation, Apparel, Restaurants/Bars, Communication, Travel Agencies

- Real Estate, Insurance, Health Care, Law (i.e. Professional Services and/or Licensed Trades)

- $80k/year average (mostly self-funded and bank credit)

Sources: US Department of Labor, Bureau of Labor Statistics; US Small Business Administration, Office of Advocacy; Fair Isaac Corporation

5

5

Market Size, Fragmentation, Refresh Rate

Source: Profit from the Cloud, 2013 Parallels Global SMB Cloud Insights

6

6

Market Velocity1

Constant Contact:~605k cumulative active

customers (2% Q/Q growth)~50k new customers each

quarter (~40k churn)

Yelp:~74k active business

accounts (13% Q/Q growth)~35% new reviews from

mobile (57mm cumulative reviews)

Innovation/Procurement Cycle

Source: 1. Company filings

Rapidly growing and changing market Willingness to try innovative solutions

0

100

200

300

400

500

600

700

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2012 2013 2014

YELP Quarterly Growth (%, left) CONSTANT CONTACT Quarterly Growth (%, left)

Cumulative Active Listings (thousands, right) Cumultive Active Custmers (thousands, right)

7

7

Software Purchase Plans1

Investment Cycle:

Cloud Computing Adoption:

- 51% of SMBs make at least one new software purchase every 6 months (not including upgrades).

- 66% of SMBs using cloud-based solutions by end of 2013 (up from 14% 2H 2010).

SMB as Consumer

SMB Owners Conditioned:

Demand-side Diversity:

- Tools like Gmail, Drive (Google) and Box began as purely consumer focused before penetrating B2B.

- From a servicing and pricing perspective, the fragmented SMB market resembles B2C approach.

Innovation/Procurement Cycle

Source: 1. Spiceworks State of SMB IT 1H 2013

Rapidly growing and changing market Willingness to try innovative solutions

8

8

Macro Tailwinds

1. SaaS model excellent fit for SMB needs

Huge cost advantages over client-server software (i.e. upfront fee, implementation, maintenance, security); flexibility to scale up/down as needed.

2. Self-serve distribution/sales through Internet

Low cost of customer acquisition, customer service, maintenance through largely self-serve/DIY internet platform.

3. Bottom up approach to market penetration

Earlier to minimum viable product, faster to iterate, improved unit economics through increased ASP, modulated platform by customer size.

9

9

Precedent Cases

SMB Clients/Product Focus Location Exit Value Date Notes

CPA’s, accounting firm/bookkeeping Palo Alto NA$80mm raised

11/13Mix of strategic and VC investment

Web designers, SoHocompanies/domain registration

Scottsdale Acquired $2.25bn 06/11 KKR, Silver Lake, TCV LBO

Wholesaler, biz. services/resource planning*

San MateoIPO:

(NYSE: N)$1.5bn 12/07 Current Market Cap: $6.1bn

Payroll, non-profits/human capital management

Palo Alto Acquired $169mm 06/09Intuit Payroll Services for Small Business

Sales and marketing organizations/CRM*

San FranciscoIPO

(NYSE: CRM)$504mm 06/04 Current Market Cap: $33bn

Bars, restaurants, retail/local listings San FranciscoIPO

(NYSE: YELP)$900mm 03/12 Current Market Cap: $4.9bn

High reward for strong execution across a wide range of horizontal and vertical subsets.

High Bay area concentration

* SMB roots, expanded upmarket

to Enterprise

Source: Capital IQ

10

1 0

Investor Landscape

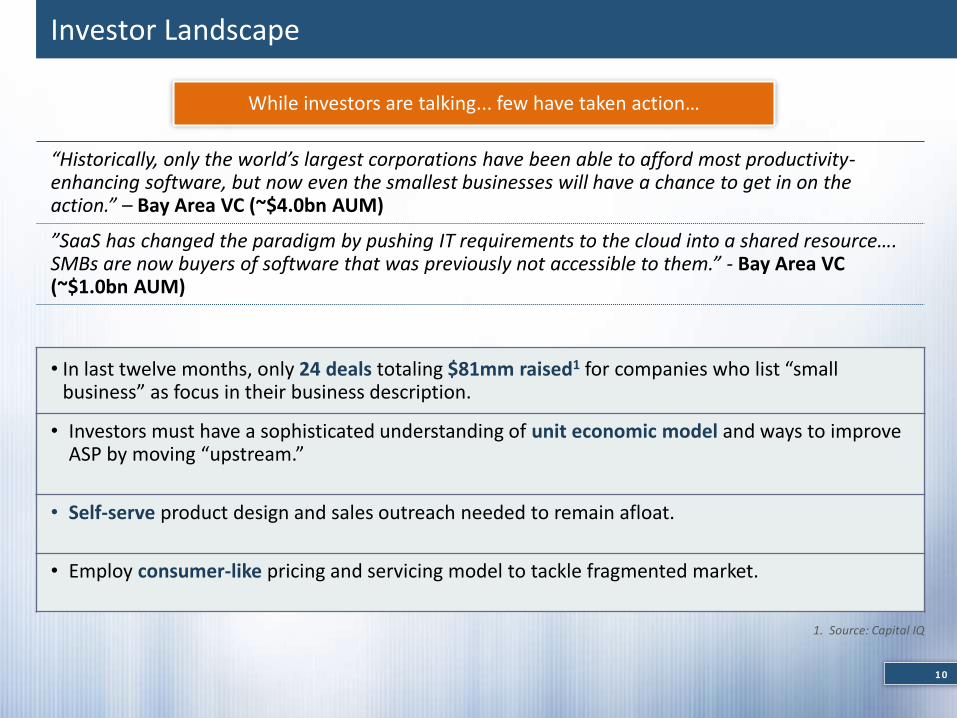

“Historically, only the world’s largest corporations have been able to afford most productivity-enhancing software, but now even the smallest businesses will have a chance to get in on the action.” – Bay Area VC (~$4.0bn AUM)

”SaaS has changed the paradigm by pushing IT requirements to the cloud into a shared resource…. SMBs are now buyers of software that was previously not accessible to them.” - Bay Area VC (~$1.0bn AUM)

• In last twelve months, only 24 deals totaling $81mm raised1 for companies who list “small business” as focus in their business description.

• Investors must have a sophisticated understanding of unit economic model and ways to improve ASP by moving “upstream.”

• Self-serve product design and sales outreach needed to remain afloat.

• Employ consumer-like pricing and servicing model to tackle fragmented market.

While investors are talking... few have taken action…

1. Source: Capital IQ

11

1 1

Table of Contents

Summary – Reasons for Interest

3-5 Market Size, Fragmentation, Refresh Rate

6, 7 Innovation/Procurement Cycle

8 Macro Tailwinds: SaaS flexibility, internet distribution, bottom up scaling

9 Precedent Cases

10 Investor Landscape

Industry Map

12 Lifecycle of an SMB

13-16 Business Formation Tools

ERP, Legal, Website/Hosting, Productivity/Communication

17-19 Growth and Customer Acquisition Tools

Sales/CRM, Marketing, Commerce/POS

20-23 Business Management Tools

HCM, Finance, Supply Chain/Product Development, BI/IT

Exit Activity & Incumbent Landscape

25 Current Incumbents

26 Acquisition Activity

12

1 2

Lifecycle of an SMB

Year

0 1 3

5

Business Formation

Growth/User Acquisition

Business Management

Average lifespan: 5 years

• Enterprise Resource Planning

• Legal Solutions• Website and Hosting

Services• Productivity and

Communication Tools

• Human Capital Management

• Finance and Accounting• Supply Chain and

Product Management• Business Intelligence

and Information Technology

• Sales and CRM Tools• Marketing Automation

Services• Commerce and Point of

Sale

13

1 3

(Enterprise) Resource Planning Solutions

Business Formation Tools

Leader: Palo Alto Software

• HQ: Eugene, OR

• Founded: 1988

• Funds raised: NA – bootstrapped since inception

• FTE: 56 (LinkedIn)

• Key Exec: Tim Berry, Founder/President

Category Landscape

• 2015 estimated SaaS Penetration: 10%1

• Enterprise Leaders: Netsuite, Oracle, SAP

• 88 solutions listed on Capterra (web-based, 50-99 users)

• Contenders: Aptean, Kenandy, Lettuce, Syspro

• Summary: Product complexity and strength of enterprise players creates significant headwind.

1. Source: Bain & Co., www.bain.com/Images/BAIN_BRIEF_The_cloud_reshapes_the_business_of_software.pdf

14

1 4

Legal Solutions

Business Formation Tools

Leader: Rocket Lawyer

• HQ: San Francisco, CA

• Founded: 2002

• Funds raised: ~$72mm (IGC, Google Ventures, Morgan Stanley, August Capital)

• FTE: 183 (LinkedIn)

• Key Exec: Charley Moore, Founder/Exec. Chairman

Category Landscape

• 2015 estimated SaaS Penetration: NA

• Enterprise Leaders: Advisory Board Co., Docusign

• 19 solutions listed on Capterra (web-based, 50-99 users)

• Contenders: Clio, LegalZoom, Shake

• Summary: Particularly fragmented nature of clientele led to early movers and adoption in this space, validation of model, winners largely determined.

15

1 5

Website/Hosting/CMS

Business Formation Tools

Leader: Go Daddy

• HQ: Scottsdale, AR

• Founded: 1997

• Funds raised: $2,250mm (KKR, Silver Lake, Technology Crossover Ventures)

• FTE: 2,435 (LinkedIn)

• Key Execs: Blake Irving, CEO; Bob Parsons, Founder

Category Landscape

• 2015 estimated SaaS Penetration: 11%1

• Enterprise Leaders: Sharepoint (MSFT), SpringCM

• 103 solutions listed on Capterra (web-based, 50-99 users)

• Contenders: Endurance, Network Solutions (Web.com), Rackspace, Squarespace

• Summary: SoHo solutions predominate, trouble is increasing ASP/scaling to more profitable market segments.

1. Source: Bain & Co., www.bain.com/Images/BAIN_BRIEF_The_cloud_reshapes_the_business_of_software.pdf

16

1 6

Productivity/Communication Solutions

Business Formation Tools

Leader: Ring Central

• HQ: San Mateo, CA

• Founded: 2003

• Funds raised: $44mm+ (DAG, Hermes Growth, Khosla, Scale, Sequoia)

• Exit: 9/13, $97.5mm IPO (NYSE: RNG)

• FTE: 976 (LinkedIn)

Category Landscape

• 2015 estimated SaaS Penetration: 75%1

• Enterprise Leaders: Blue Jeans Network, Cisco, LogMeIn, Skype

• 118 solutions listed on Capterra (web-based, 50-99 users)

• Contenders: Grasshopper, PivotDesk, Speek, Twilio

• Summary: Office Suite tools far less developed (only 6%1 est. 2015 SaaS penetration) than web communication/collaboration.

1. Source: Bain & Co., www.bain.com/Images/BAIN_BRIEF_The_cloud_reshapes_the_business_of_software.pdf

17

1 7

Sales/CRM Solutions

Growth and User Acquisition Tools

Category Landscape

• 2015 estimated SaaS Penetration: 38%1

• Enterprise Leaders: RightNow, Salesforce, ServiceNow

• 138 solutions listed on Capterra (web-based, 50-99 users)

• Contenders: 37Signals (High Rise), Workbooks, Zestia (Capsule), Zoho

• Summary: Fragmented landscape with a number of startups in last 5-7 years, particularly int’l (UK, IN)

1. Source: Bain & Co., www.bain.com/Images/BAIN_BRIEF_The_cloud_reshapes_the_business_of_software.pdf

Leader: Insightly

• HQ: San Francisco, CA

• Founded: 2009

• Funds raised: $13mm (Emergence Capital, SozoVentures, TrueBridge Capital)

• FTE: 50 (Crunchbase)

• Key Execs: Anthony Smith, Founder/CEO

18

1 8

Marketing Automation Solutions

Growth and User Acquisition Tools

Category Landscape

• 2015 estimated SaaS Penetration: 15%1

• Enterprise Leaders: Hubspot, Marketo, Oracle, Salesforce

• 68 solutions listed on Capterra (web-based, 50-99 users)

• Contenders: Act-On, Constant Contact, MailChimp, Nurture

• Summary: Enterprise vendors strong but, with vast SaaS penetration ahead, room persists for SMB tools.

1. Source: Bain & Co., www.bain.com/Images/BAIN_BRIEF_The_cloud_reshapes_the_business_of_software.pdf

Leader: InfusionSoft

• HQ: Chandler Heights, AZ

• Founded: 2001

• Funds raised: $73mm (Arthur Ventures, Goldman Sachs, Mohr Davidow)

• FTE: 546 (LinkedIn)

• Key Execs: Clate Mask , Founder/CEO

19

1 9

Commerce/Point of Sale Solutions

Growth and User Acquisition Tools

Category Landscape

• 2015 estimated SaaS Penetration: NA

• Enterprise Leaders: Amazon Webstore, Deem, Demandware, Digital River, IBM Websphere

• 116 solutions listed on Capterra (web-based, 50-99 users)

• Contenders: BigCommerce, DropShip, Magento

• Summary: Consumer and retail solutions prevail, leaving underserved verticals (manufacturing) and services (shipping/logistics).

Leader: Shopify

• HQ: Ottawa, ON

• Founded: 2005

• Funds raised: $122mm (Bessemer, Felicis, FirstMarkGeorgian, Insight)

• FTE: 395 (Crunchbase)

• Key Execs: Tobias Lutke, Co-founder/CEO

20

2 0

Human Capital Management

Business Management Tools

Category Landscape

• 2015 estimated SaaS Penetration: 22%1

• Enterprise Leaders: HireVue, Successfactors (SAP), Taleo (Oracle), Workday

• 122 solutions listed on Capterra (web-based, 50-99 users)

• Contenders: Namely, Octopus

• Summary: As with Marketing, many strong enterprise-level tools ignore smaller end and/or niche services (i.e. video interviewing).

1. Source: Bain & Co., www.bain.com/Images/BAIN_BRIEF_The_cloud_reshapes_the_business_of_software.pdf

Leader: Halogen Software

• HQ: Ottawa, ON

• Founded: 1996

• Funds raised: $8mm+ (JMI, Covington Capital, TD Capital, Triax Capital)

• Exit: 4/13, $55mm IPO (TSX: HGN)

• FTE: 297 (CapIQ)

21

2 1

Finance/Accounting Solutions

Business Management Tools

Category Landscape

• 2015 estimated SaaS Penetration: 27%1

• Enterprise Leaders: Intuit, Ultimate Software, MSFT

• 73 solutions listed on Capterra (web-based, 50-99 users, Accounting + Loan Servicing)

• Contenders: Bill.com, Freshbooks, Intacct(accounting tools); Bond St, Fundera, Kabbage(lenders/loan brokers)

• Summary: Like Legal (i.e. licensed trade) early movers and adoption, now likely consolidation.

1. Source: Bain & Co., www.bain.com/Images/BAIN_BRIEF_The_cloud_reshapes_the_business_of_software.pdf

Leader: Xero

• HQ: Wellington, NZ

• Founded: 2006

• Funds raised: $355mm+ (Accel, Matrix Capital, ValarVentures, Peter Thiel)

• Exit: 4/13, $55mm IPO (TSX: HGN)

• FTE: 297 (CapIQ)

22

2 2

Supply Chain/Product Development

Business Management Tools

Category Landscape

• 2015 estimated SaaS Penetration: 25%1

• Enterprise Leaders: Arena Solutions, Atlassian, DropShip, Ketera, Rally Software

• 106 solutions listed on Capterra (web-based, 50-99 users, PLM + Supply Chain Mgmt.)

• Contenders: Trello, Mozilla Firebug, uShip

• Summary: Serving hard asset businesses perhaps more overlooked than software/tech./media.

1. Source: Bain & Co., www.bain.com/Images/BAIN_BRIEF_The_cloud_reshapes_the_business_of_software.pdf

Leader: GitHub

• HQ: San Francisco, CA

• Founded: 2008

• Funds raised: $100mm (Andreeson Horowitz, SV Angel)

• FTE: 202 (Crunchbase)

• Key Execs: Chris Wanstrath, Co-founder/CEO

23

2 3

Business Intelligence/IT Solutions

Business Management Tools

Category Landscape

• 2015 estimated SaaS Penetration: 6%1

• Enterprise Leaders: Cloudera, Informatica, Iron Mountain, Pentaho

• 120 solutions listed on Capterra (web-based, 50-99 users, Business Intel + IT Mgmt)

• Contenders: Box, EVault, Evernote, KISSmetrics, Mixpanel, Womply

• Summary: Low SaaS penetration of wide & deep market, leads to high competition but significant greenfield opportunity.

1. Source: Bain & Co., www.bain.com/Images/BAIN_BRIEF_The_cloud_reshapes_the_business_of_software.pdf

Leader: Dropbox

• HQ: San Francisco, CA

• Founded: 2007

• Funds raised: $1.1bn (T. Rowe, Blackrock, Accel, Sequoia, Glynn Capital, Valiant, Goldman, Benchmark, IVP, Greylock, SVA, Index, et al.)

• FTE: 642 (Crunchbase)

• Key Execs: Drew Houston, Founder/CEO

24

2 4

Table of Contents

Summary – Reasons for Interest

3-5 Market Size, Fragmentation, Refresh Rate

6, 7 Innovation/Procurement Cycle

8 Macro Tailwinds: SaaS flexibility, internet distribution, bottom up scaling

9 Precedent Cases

10 Investor Landscape

Industry Map

12 Lifecycle of an SMB

13-16 Business Formation Tools

ERP, Legal, Website/Hosting, Productivity/Communication

17-19 Growth and Customer Acquisition Tools

Sales/CRM, Marketing, Commerce/POS

20-23 Business Management Tools

HCM, Finance, Supply Chain/Product Development, BI/IT

Exit Activity & Incumbent Landscape

25 Current Incumbents

26 Acquisition Activity

25

2 5

Current Incumbents

Category LocationYear

Formed Size Type

MarketingBoston Area(NDAQ: CTCT)

19951,235 FTE

$1.0bn MVDirect

Commerce/POSBay Area(NDAQ: EBAY)

199531,800 FTE

$67.6bn MVDirect

Website/Hosting, MarketingBoston Area(NDAQ: EIGI)

19972,200 FTE

$1.75bn MVDirect

Finance/AccountingBay Area(NDAQ: INTU)

19838,000 FTE

$23.4bn MVDirect

Finance, ERP, CRM, BusinessIntel, Payments

UK(LSE: SGE)

198112,760 FTE$4.3bn MV

Direct

CRM, MarketingBay Area (NYSE: YELP)

20042,345 FTE

$5.9bn MV Direct

Credit CardsCA, NY, NY

As old as 1850 (AmEx)

Up to 63k FTE (AmEx)

Indirect

Wireless NetworksKS, TX, NY, WA

As old as 1899 (Sprint)

Up to 248k FTE (AT&T)

Indirect

Cable CompaniesPA, NY 1963, 1985 136k,51k FTE Indirect

Payroll, HR ServicesNJ, NY 1949, 1971 61k, 13k FTE Indirect

Concentration in Boston and Bay

Areas

Gaps: Legal, Productivity, Supply Chain/Product Dev.

Source: Capital IQ

26

2 6

Exit Activity

Sources: Capital IQ, Crunchbase

Notable Transactions

Buyer Date Target Size(USD,mm) xRevenue PriorRaised* Prior(LTM)Revs SelectedInvestors

Priceline Jul-14 OpenTable 2,613.0 13.2x 2,426.1 198.3 JATCapital,T.RowePrice,BlackRock(NASDAQ:OPEN)

NetSuite Jul-14 Venda 50.5 2.6x 30.0 19.8 GFPrivateEquity,InvestorGrowthCapital

Netsuite Oct-13 TribeHR 24.8 -- 2.5 ND MatrixPartners,RelayVentures

eBay Sep-13 Braintree 800.0 -- 70.0 ND Accel,Greycroft,NEA,RRE

(+Venmo)

Constant Jun-13 SinglePlatform 92.9 168.8x 4.7 0.6 FirstRound,DFJGotham,PritzkerGroup,RRE

Contact

InfusionSoft Jan-13 GroSocial 30.0 -- 2.2 ND KickstartSeedFund,Monarch,Rock&HammerVentures

Yelp Oct-12 Qype 48.8 4.6x 20.1 10.6 AdventVP,Partech,VodafoneVentures,Wellington

Intuit Apr-12 DemandForce 423.0 33.6x 10.0 12.6 Benchmark,FLOODGATE,PaloAltoVP

BestBuy Nov-11 MindSHIFT 175.0 8.0x 63.4 21.9 ColumbiaCapital,FidelityVentures,TDF,Volition

Intuit Jun-09 PayCycle 169.0 15.8x 29.0 10.7 AugustCapital,CCPEquity,DCM,DraperRichards

Sage Mar-08 Hallco1390 41.9 7.0x 23.5 6.0 InflexionPrivateEquity,YFMPrivateEquity

Average 406.3 31.7x 25.5 35.1Median 92.9 10.6x 21.8 11.7 *FundraisingaveragesexcludeOpenTable