sip report_surabhi narad_hdfc bank

DESCRIPTION

ready to printTRANSCRIPT

A REPORT

ON

CORPORATE FINANCIAL ANALYSIS

COMPANY GUIDE FACULTY GUIDEMR.SANJIV BHUYAN DR.BHARATHI KAMATHDEPUTY VICE PRESIDENT ICFAI B-SCHOOLCORPORATE BANKING MUMBAI

SUBMITTED BY SURABHI NARAD

06BS2966

ACKNOWLEDGMENTS

No significant achievement can be solo performance especially when starting a project from ground up; this is true with the project called “CORPORATE FINANCIAL ANALYSIS” also.

Mr. Sanjiv Bhuyan, has been very supportive and involved in this project. It was his support that helped the project to start in its earliest and most vulnerable stages. I would like to extend my gratitude towards him as he took out time from his extremely busy schedule, for guiding and helping me during this project.

I would like to thank Mr. Rajeev Bhide, who helped me with his valuable suggestions irrespective of his health problem.

This project could not have taken its present shape without the proper direction shown by Dr.Bharathi Kamath.

My sincere thanks to all at HDFC BANK, who directly and indirectly helped me to carry forward this project.

TABLE OF CONTENTS

Executive Summary.............................................................................1

Introduction..........................................................................................2

About the company..............................................................................3 Objective and flow of the project........................................................4 Analysis of Chemical industry............................................................5 Analysis of Power equipment industry..............................................37

Analysis of Auto ancillary industry...................................................62

Analysis of Textile industry..............................................................86

Analysis of Food processing industry.............................................114

Conclusion.......................................................................................140

Value additions from the project.....................................................141

References.......................................................................................142

EXECUTIVE SUMMARY

This is a project which is being done for HDFC CORPORATE BANK. The aim of this project is to identify those companies which can be potential clients for HDFC's business.These companies belong to five industries (industries have been decided by Mr.Sanjiv Bhuyan, the company guide) in India.

HDFC Bank's aim behind bringing this project on floor is that it wanted to have more volume of business with less number of clients. It is more useful to do business with few big clients rather than dealing with various small clients. Because the ultimate aim of any business is increasing profit and reducing cost. With the above aim in mind HDFC Bank will achieve both.

This project deals with following five industries:

Chemical Industry Power Equipment Industry Auto Ancillary Industry Textile industry Food Processing Industry

The first step is to do analysis of the industry. By analysis of the industry one gets a good and in depth understanding of that particular industry. For e.g. It helps in analyzing whether the industry requires large investment or has large working capital requirement. Industry analysis clearly shows investment opportunities present in the industry and the risks associated with it.

This is useful in analyzing global scenario of the industry and its impact on the Indian industry. This also helps in identifying the major competitors present in the market and to study their strategies and moves. All this is similar to equip yourself properly before you enter the battle field so that the chances of victory increases.

Then, the second step is to find databases containing all companies present in Indian in that particular industry .

Third step is to sort out companies in western India with a turnover of more than Rs. 300 crores. And then financial analysis of each firm is done.

In fourth and the last step is to understand all the products provided by HDFC Corporate Bank. Then decide which product will be best suited to which firm in above mentioned industries.

1

INTRODUCTION

BANK: STRUCTURE AND FUNCTIONS

A bank is a business which provides financial services for profit. Traditional banking services include receiving deposits of money, lending money and processing transactions. Traditionally, a bank generates profits from transaction fees on financial services and from the interest it charges for lending. Much of a bank's income is provided by overdraft fees and riskier investments.

Banks' activities can be divided into retail banking, dealing directly with individuals and small businesses, and investment banking, relating to activities on the financial markets.

Banks have a long history, and have influenced economies and politics for centuries.

A bank raises funds by attracting deposits, borrowing money in the inter-bank market, or issuing financial instruments in the money market or a capital market. The bank then lends out most of these funds to borrowers. However, it would not be prudent for a bank to lend out all of its balance sheet. It must keep a certain proportion of its funds in reserve so that it can repay depositors who withdraw their deposits. Bank reserves are typically kept in the form of a deposit with a central bank. This behavior is called fractional-reserve banking and it is a central issue of monetary policy.

Banks are susceptible to risks which include liquidity risk (the risk that many depositors will request withdrawals beyond available funds), credit risk (the risk that those that owe money to the bank will not repay), and interest rate risk (the risk that the bank will become unprofitable.

Banks, especially commercial banks play a crucial role in accelerating the tempo of growth in a developing economy. Therefore, there must be a central governing body which may run the system smoothly and economy of the country keeps on rolling. Such a body is known as CENTRAL BANK of the country.

A central bank or reserve bank is an entity responsible for the monetary policy of its country. It has supervisory powers to ensure that banks and other financial institutions do not behave recklessly or fraudulently. A central bank is usually state-owned and headed by a Governor.

“THE RESERVE BANK OF INDIA” is the central bank of the country entrusted with monetary stability, the management of currency and the supervision of the financial as well as the payments system.

The Bank was constituted to

Regulate the issue of banknotes. Maintain reserves with a view to securing monetary stability To operate the credit and currency system of the country to its advantage.

2

ABOUT THE COMPANY

HDFC Bank was incorporated in August 1994 in the name of 'HDFC Bank Limited', with its registered office in Mumbai, India. The Bank commenced operations as a Scheduled Commercial Bank in January 1995.

Headquartered in Mumbai, HDFC Bank, has a network of around 650 branches spread over 270 cities across India. All branches are linked on an on line real-time basis. Customers in over 120 locations are serviced through Telephone Banking. The Bank also has a network of about over 1050 networked ATMs across these cities.

HDFC offers various services, some of them are Branch Banking, Retail Assets, Product Development, Operations, Marketing, Treasury, Equities, Corporate Banking, Cash Management Services, Custody and Depositories etc.

HDFC IN CORPORATE BANKING

Corporate Banking is a part of wholesale banking. Corporate Banking reflects HDFC Bank's services to their corporate clients in India, a wide array of commercial, transactional and electronic banking products. They achieve this through innovative product development and a well-integrated approach to relationship management. HDFC offers top companies in the India, a full range of client-focused corporate banking services, including working capital finance, trade and transactional services, foreign exchange and cash management, to name a few. The product offerings are suitably structured taking into account a client's risk profile and specific needs. Based on their superior product delivery, industry benchmark service levels and strong customer orientation, they have made significant inroads into the formal banking consortia of a number of Indian companies including multinationals, domestic business houses and prime public sector companies.

3

OBJECTIVE AND FLOW OF THE PROJECT

Basically the project is all about to identify those companies, in five industries, which can be potential clients for HDFC's business.

In this project, I have to deal with following five industries, namely:

Chemical Industry Power Equipment Industry Auto Ancillary Industry Textile industry Food Processing Industry

The flow of the project will be the same as explained in following few paragraphs.The first and the foremost step is to do analysis of the industry. Through this analysis following things become clear about the particular industry:

Characteristics of the industry. Growth drivers of the industry. Risk factors involved in the industry. Major players in the industry. Whether the industry requires large investment or has large working capital

requirement. Investment opportunities present in the industry.

Through industry analysis one can understand Requirements of the industry. Dynamics of the industry. Major competitors present in the market and their strategies.

After this search of databases begins, here aim is to find as many companies present in the industry as possible. Then financial analysis of each firm is done. Firstly, from the balance sheet of the company, its turnover is checked. If turnover is less than Rs. 300 Crs, that company is removed from the list. Secondly, profitability and Net worth of the company is calculated.

After this, study of all the products provided by HDFC Corporate Bank will be done thoroughly so that those products can be sorted out which fit into that particular industry and accordingly marketed to the potential clients.

The study of all the five industries will follow the same flow as explained above.

4

ANALYSIS

OF THE

CHEMICAL INDUSTRY

5

INDIAN CHEMICAL INDUSTRY

India is one of the fastest growing economies in the world, making rapid progress since 1991. The country has undertaken far-reaching economic reforms of deregulation and liberalization as well as financial and corporate restructuring, which have enhanced economic growth rates considerably.

Chemical industry is one of the oldest industries in India. It not only plays a crucial role in meeting the daily needs of the common man, but also contributes significantly towards industrial and economic growth of the nation. The industry, including petro-chemicals, and alcohol-based chemicals, has grown at a pace outperforming the overall growth of the industry.

The global chemical market is estimated at approximately USD 1.7 trillion. Western Europe is the largest chemical-producing region followed by North America and Asia.

The Indian chemicals and materials industry is the second largest industrial sector in the country,behind information technology (IT). The chemicals, materials, and foods (CMF) industry is one of the oldest in India, contributing significantly to its industrial and economic growth. India ranks 12th in the world and third in Asia in the production of chemicals and materials and is poised to become a major venue for out souring chemical manufacturing.

The current economy and the general economic policies have stimulated various segments of the Indian CMF industry and its industry-specific policies have facilitated its development. The Indian CMF industry is mainly demand-driven and increasing foreign and industrial investments drive the industry further. Trends in investment, exports, and imports have also greatly influenced the CMF industry.

Chemicals, Materials, and Foods Country Industry Forecast service provides vital inputs for evaluating the attractiveness of a country and its CMF industry. Besides enabling decision makers to assess the impact of non-market forces, it also helps in identifying new market opportunities. This service provides a strong base for preparing contingency plans. In addition, investors can assess industry-specific risk factors as well as conduct a more in-depth micro research.

The Indian Chemicals Industry comprises both small and large scale units. The fiscal concessions granted to small sector in mid-eighties led to establishment of large number of units in the Small Scale Industry (SSI) sector. Currently, the Indian Chemical Industry is in the midst of major restructuring and consolidation phase. With the shift in emphasis on product innovation, brand building and environmental friendliness, this industry is increasingly moving towards greater customer-orientation. Even though India enjoys an abundant supply of basic raw materials, it will have to build upon technical services and marketing capabilities to face global competition and increase its share of exports.

The Indian Chemical Industry ranks 12th by volume in the world production of chemicals. The industry’s current turnover is about USD 30.8 billion which is 14% of the

total manufacturing output of the country. The export of chemicals in the year 2002 was USD 5.875 billion, which forms almost 0.9 % of the world export of chemical products and about 13% of the country’s total export. Substantial proportion of these exports goes to the USA, Europe and other developed nations. Its contribution to the national revenue by way of custom and excise duties is about 20%. India is strong in basic chemicals that go into production of consumer items like paints, dyes, soaps, medicines, toiletries, cosmetics, etc.

The chemical, petrochemical and pharmaceutical industry in India is one of the fastest growing segments of the industrial sector with an annual growth rate of 12.5% per year for the last 10 years. It accounts for 12.5% of India's industrial production and 16.2% of the country's exports of manufactured goods. This rate of growth has been consistently high as the country has one of the largest resources of scientific and technical manpower in the world with the capacity to absorb, upgrade and develop high technology. India also has excellent engineering and project management skills.

CHEMICAL INDUSTRY STRUCTURE IN INDIA

Source: KPMG Survey of the Indian chemical industry, 2002

Highly fragmented and widely dispersed. Wide product range – basic, speciality and knowledge segments. Basic comprising of petrochemicals, inorganic chemicals and fertilizers is the largest segment.

Output 2% of the world total output --- USD 30 billion. Petrochemicals --- usd 7 billion (22% of India's total chemical output). Industry growth rate is approx. 5% during the last 5 years. Profit margin- 14%. Western India accounts for 45-50% of total Indian chemical Industry. Gujarat, Maharastra , West Bengal and Andhra Pradesh has the largest

concentration of chemical and petro chemical industries. Large players in bulk chemicals. Both large and small players in Fine and

Speciality chemicals. Presence of many multinational companies also.

Factors Responsible for Limiting the Growth of Chemical Industry

Indian manufacturers compare favourably in terms of key manufacturing conversion costs with the best in the world.

High Power Cost (Utility costs are higher) Inefficient Process Technology

Basic Feed Stock Prices are High Cascading Effects of various Taxes and Duties Stringent labour Laws Uneconomic Size of plants (due to erstwhile licensing system) High Cost of Finance (Interest rates are high) Inadequate infrastructure Facility (Road, Rail and Ports) International Competition (Dumping) Drastic Reduction in Import Duties (unable to compete in global scenario)

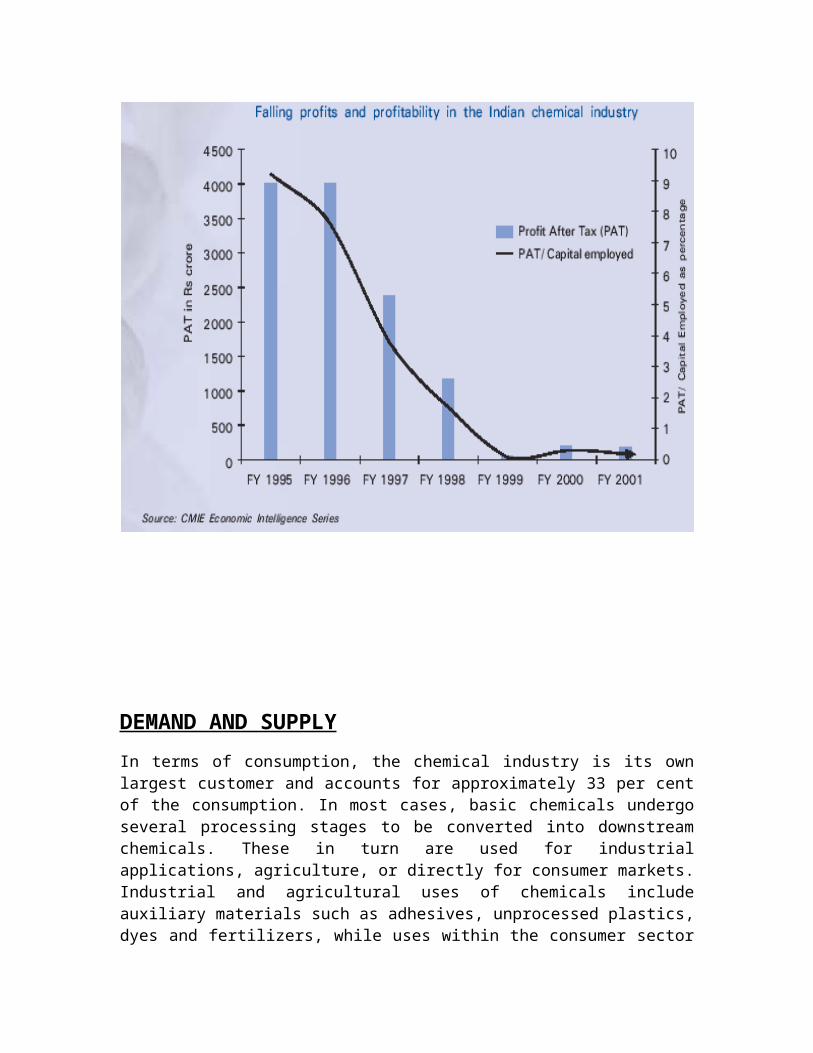

Source – CMIE

Above weaknesses are the reason of the declining profitability of the Indian chemical industry. Following statistic substantiates the above made statement.

DEMAND AND SUPPLY

In terms of consumption, the chemical industry is its own largest customer and accounts for approximately 33 per cent of the consumption. In most cases, basic chemicals undergo several processing stages to be converted into downstream chemicals. These in turn are used for industrial applications, agriculture, or directly for consumer markets. Industrial and agricultural uses of chemicals include auxiliary materials such as adhesives, unprocessed plastics, dyes and fertilizers, while uses within the consumer sector include pharmaceuticals, cosmetics, household products, paints, etc.

INDIAN DEMAND AND SUPPLY SCENARIO

The Indian chemical industry manufacturers a wide spectrum of products spanning the Basic, Speciality and Knowledge segments.

At 57 percent , Basic chemicals comprise the largest segment of the Indian chemical industry. The composition of the industry, however , is shifting in favour of Speciality and Knowledge chemicals.

GLOBAL CHEMICAL MARKET AND THE CURRENT TREND

Source: KPMG survey of the Indian chemical industry, 2002

GLOBAL CHEMICAL INDUSTRY

Globally, the Basic segment accounts for about 52 percent of the industry, Speciality 20 percent and Knowledge 28 percent.

Source: Department of chemicals & petrochemicals, GOI

Knowledge is the fastest growing segment – growing at more than six times the growth rate of Basic. Speciality has a growth rate faster than Basic, but lags behind the Knowledge segment as shown in the following figure.

Cost structure of the three segments highlight distinct characteristics. Basic has high feedstock and other raw material costs, whereas speciality has very high selling and product development costs. Knowledge segment, on the other hand is characterised by large spends on advertising and R&D. Basic is the most mature segment with the lowest profitability , while knowledge chemicals have the highest profitability and growth projections.

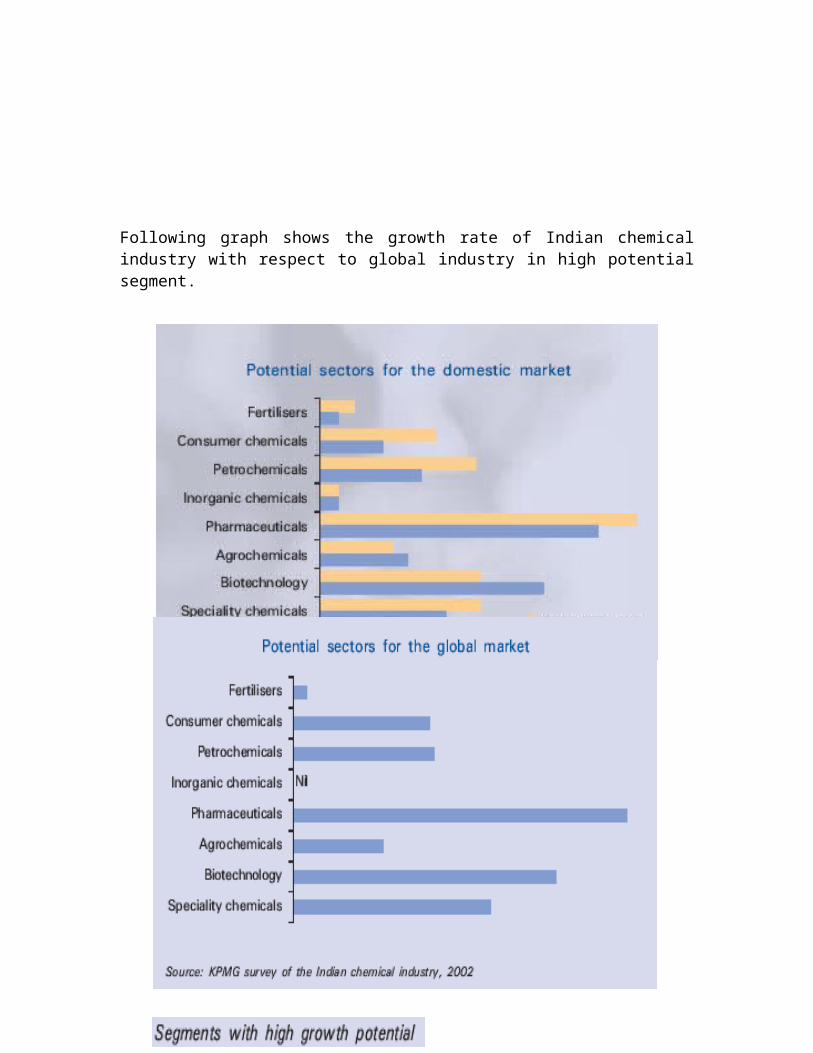

Following graph shows the growth rate of Indian chemical industry with respect to global industry in high potential segment.

SEGMENTAL ANALYSIS

Highly heterogeneous, the chemical industry in India encompasses many sectors like organic, inorganic chemicals, dyestuffs, paints, pesticides, specialty chemicals, etc. Some of its more prominent individual chemical industries are caustic soda, soda ash, carbon black, phenol, acetic acid, methanol and azo dyes. Broadly, the chemical industry in India is classified into polymerization products, basic chemicals, fine chemicals and pharmaceuticals. It accounts for more than 10% of the country's total export earnings.

India also produces a large number of fine and speciality chemicals, which have very specific uses and are essential for increasing industrial production. These find wide usage as food additives, pigments, polymer additives, anti-oxidants in the rubber industry, etc. Some of the important manufacturers of speciality chemicals include NOCIL, Bayer (India), ICI (India), Hico Products and Colourchem.

The Dyestuff sector is one of the important segments of the chemicals industry in India, having forward and backward linkages with a variety of sectors like textiles, leather, paper, plastics, printing ink and foodstuffs.India has emerged as a global supplier of dyestuff and dyes intermediates, particularly for reactive, acid, vat and direct dyes. As for a global production of dyes is concerned, India accounts for 6% of the world production.

Chemical fertilizers and pesticides played an important role in the "Green Revolution" during the 1960s and 1970s. The consumption of pesticides in India is low in comparison to other countries. Indian exports of agrochemicals have shown an impressive growth over the last five years.

The key export destination markets are USA, UK, France, Netherlands, Belgium, Spain, South Africa, Bangladesh, Malaysia and Singapore.

Chemical industry is broadly segmented into :

u Petrochemicals u Inorganic Chemicals u Organic Chemicals u Fine and specialties u Bulk Drugs u Agrochemicals u Paints and Dyes

Source:Department of chemicals & petrochemicals, GOI

INDIAN PETROCHEMICALS

✔ Domestic market size – US$700 million✔ Fastest growing sector at 15%✔ Reliance – key player in this market

INORGANIC CHEMICALS✔ Market size – US$260 million✔ Growth rate – 9%✔ 4.5% of global market✔ Mainly used in detergent, glass, soap, fertilizer and alkalis

PHARMACEUTICALS✔ India ranks 4th In terms of volume & 13th in terms of value.✔ Domestic market size – US$450 million✔ Indian market is 1.6% of the global market✔ Domestic market growth rate – 8 to 9%✔ Strong player in generic market--several of the world’s leading drug

companies are based in India.✔ Significant export led growth

AGRO CHEMICALS AND FERTILISERS✔ Domestic market size – US$88 million

✔ Domestic market growth rate – 10% annually✔ 2.5% of the global market.✔ In India, insecticide commands major share 76%.✔ Globally, herbicides commands major share 48% & insecticide only 29%.✔ India is largest manufacture of basic pesticide chemicals among South Asia

& Africa, next only to Japan.

SPECIALITY & FINE CHEMICALS✔ Market size – US$860 million✔ Major used in textile, leather, paper, detergent, rubber,✔ Paints, polyester, oil & gas.✔ Growth rate – 10-12%.

DYES & PAINTS✔ Market size – US$110 million.✔ Growth rate – 12%✔ Indian market is 6% of the global market✔ Major used in✔ Paints, inks, textiles, polymers.✔ Highly fragmented market✔ 25 large & medium players holding 50% of the market.✔ Remaining 50% is with another small 2000 un-organized players

Success Stories in Fine & Specialty Chemicals

In the pharmaceutical industry, India has demonstrated repeatedly its ability to produce the latest drugs available in the world cost effectively. Within six months after Pfizer launched ‘Viagra’ globally, 3 -4 Indian pharmaceutical companies had introduced it to India market. Demonstrated ability to develop and absorb the latest technologies. Examples are given below :

Rallis manufactures Hexaconazole, a complex Agro-Chemical with purity of 95% withindigenous technology. The innovator produces this product with 90% purity.Gharda manufactures Dicamba, another complex Agro Chemical with purity of 95% withindigenous technology. The innovator of this product produces this product with a purity of 87%.

Other examples include the anti-AIDS drugs including ‘Lamivudine’ ‘Zidovudine’ and‘Indinavir’ each of which are being produced in India at a cost which is a fraction of the price at which these products are being sold internationally.

The following diagram, very well expresses the industry opinion regarding future of various segments in chemical industries:-

(MCIE stands for Mega Chemical Complexes)

Source: Department of chemicals & petrochemicals, GOI

INDUSTRY DYNAMICS

The Government is promoting research on the use of alternative and unharmful pesticides using neem seeds. A country programme entitled "Development and Production of Neem Products as Environment Friendly Pesticides" is being undertaken by the Department of Chemicals & Petrochemicals with the financial assistance of United Nations Development Programme (UNDP)/ United Nations Industrial Development Organization (UNIDO). The project is being implemented at two locations viz., Nimpith in West Bengal and Nagpur in Maharashtra to promote production, processing and use of neem-based products, thereby aiding wasteland development, generating rural employment and providing farmers with eco-friendly/ bio-degradable pesticides.

MAJOR COSTS INVOLVED IN CHEMICAL MANUFACTURING

Raw materials R & D Processing Preservation Special containers for storage

INDIAN GENERIC INDUSTRYIndia has a significant share in the global generics market and is ranked third. In recent years, this segment has been facing stiff competition which makes the scale of production important to improve profitability. India has pre-dominantly been a generic player and has the potential to gain a global presence for the following key developments:

Multiple branded drug patent expirations in the short term. According to IMS Health, in 2006 and 2007 a total of US$ 28 bn and US$ 20 bn, respectively, of branded sales were likely to become susceptible to the entry of generic equivalents.

Increasing confidence of consumers in generics in the developed markets. A pro-generic sentiment from healthcare authorities driven by the pressure of

containing rising healthcare costs. An aging population across the world, leading to increasing demand for low cost

therapies. Global healthcare crisis like AIDS in the developing world, necessitating

affordable medication for the masses.

Generic companies in India are recognizing the importance of patent expiries and are making significant incremental investments in research and drug development

INDIAN BIOTECH INDUSTRY

India, today, holds a small share of the global biotech market, but has all the capabilities to become a dominant player. The consumption of biotech products in India is expected to quadruple in the next decade. The human and animal segment of the industry alone is growing by at least 20%.

While India has been practicing conventional biotechnology for decades modern biotechnology is rather new to India. In 1997, the total biotech market in India was

valued at $ 500 million. This grew to $ 1 billion in 1999 and is expected to grow to $ 4.5 billion by 2010. Human health biotech accounts for 60 % of the total sales, while agro biotech and veterinary-biotech together account for 15 % of the total revenue and medical devices, contract R&D and reagents and supplies constitute the remainder. There exist 800 companies, operating in all sectors of biotechnology, but there are only 25 companies that are working in the modern biotech sectors.

India has very interesting natural features like bio-diversity, varied species of flora and fauna, varied climatic zones, large population with varied demography, largest agriculture sectors, world-class information-technology industry, vibrant pharmaceutical sector and a large pool of scientific talent that creates almost a perfect environment for biotech companies to shift base here. With its large population of over a billion people India also provides a huge market for products and services.

India has a rich human capital, which is the strongest asset for this knowledge-based industry. India has a large English speaking base and produces roughly 2.5 million graduates in IT, engineering and life sciences, about 650,000 postgraduates and nearly 1500 PhDs qualified in biosciences and engineering each year. India has proved its competency in selected areas of biotechnology such as capacity in bioprocess engineering, skills in gene manipulation of microbes and animal cells, capacity in downstream processing and isolation methods, and its competence in recombinant DNA technology of plants and animals.

India has also allowed assisted stem cell research that permits researchers to use embryos from fertility clinics upon informed consent of the donors, thus giving it a clear head start in this new and promising field in Biotech. Clearly, India has the strength and capabilities in this industry, and a definite advantage to forge ahead and become the chosen location for many biotech companies looking for large markets and low cost qualified manpower to work in their R&D division.

The inherent strengths of the Nation combined with rising public interest in this sector, growing investment by traditional business houses, tax incentives and the significant foreign investment available, poises Indian biotechnology sector to emerge as a significant force on the global biotech map.

GROWTH DRIVERS FOR INDIAN CHEMICAL

INDUSTRY

Consolidation Growing orientation towards Research and Development (R&D) Outsourcing Growing Demand Pharma sector going strong Environmental consciousness

Consolidation

Industry Segment Key Drivers

Basic Segment Falling duties; scale in manufacturing, logistics, marketing and finance.

Speciality Segment Proprietary knowledge, research initiatives, accessibility of funds for R&D.

Knowledge Segment Product registrations, research initiatives, joint funds for combined R&D.

Growing orientation towards Research and Development (R&D)

The Indian chemical market is shifting from commodity selling industry to skilled industry producing speciality products. Following figures reveal the fact: In India, presently there are approximately,

200 National laboratories. 1300 R&D units. 244 universities. 200,000 scientific personnel

Following are the factors which act as driver in R&D:

Efficiencies in manufacturing to reduce costs, scale in processes at each stage. Investment in bio-technology by pharma and agro-chemical sectors to derive

“first advantage”. New products or applications.

The introduction of product patent has led the domestic industry towards exploring new avenues of drug development, which would require higher capital investment in R&D, and greater thrust towards innovation. Current trends indicate that R&D expenditure of top domestic companies has increased from a mere 2% of total turnover in CY00 to nearly 4% in CY05.

Outsourcing

India's workforce ranks first in the availability of qualified, skilled engineers. This leads to many advantages like lower capital outlay , focus on core activities , reduce risk , generate faster cycle times.

Growing Demand

In Indian industry , following are the growth rates for different segment:

Speciality chemical industry = 8% Paints = 8 – 10 % Pharmaceuticals = 9% Knowledge chemicals = 12%

Pharma sector going strong

Globally , the output of Indian pharmaceutical industry ranks fourth in terms of volume and 13th in terms of value.

In FY02, the domestic Indian pharma market was valued at $4.5bn , representing 1.6% of the global market, and is growing at an annual rate of 9%.

The industry produces about 60,000 finished medicines and roughly 400 bulk drugs, which are used in formulations.

In FY03, the Indian pharma market is estimated to have exported drug worth Rs. 110bn.

In the past eight years, the pharma exports grew by 30% per annum.

Following are the growth drivers for the pharma industry;

High number of manufacturing units approved by USFDA. Manufacturing costs less than 1/10th of developed nations. Well established API manufacturing industry. High level of IT awareness of R&D staff. Expertise in process development.

Environmental consciousness

Government initiative in consultation with the industry Formalization of charter on Corporate Responsibility for Environmental

Protection (CREP) for 17 categories of industry.

Leveraging CRAMs opportunities

India is emerging as the global hub for contract research and manufacturing services (CRAMs) due to its low cost advantage and world class quality standards. The Indian chemical industry possesses world standard manufacturing facilities as per the GMP norms which are approved by various regulatory agencies across the globe.

Majority of the contract manufacturing deals relate to production of active pharmaceutical ingredients (APIs) and intermediates, in which India possesses

competence. Nicholas Piramal, Shasun Chemicals, Divi’s Lab, Dishman Pharma, Cadila Healthcare, Lupin, Matrix Lab and Aurobindo Pharma are some of the companies which have witnessed impressive growth in revenues from their CRAMs business under various tie-ups with global pharmaceutical majors.

Growing exports

The proportion of exports in domestic turnover has been increasing over the years, despite the growing domestic demand. Exports have been the major growth enabler of the Indian chemical industry in recent years. India exports chemical products, APIs and intermediates to more than 200 countries across the world.

Expanding presence in regulated market

Over the years, India has shown better regulatory awareness and superior technical skills, which has enabled Indian companies to penetrate the high-value markets like the US and EU. For instance, exports of pharmaceutical products (finished products as classified under heading 30 of ITC-HS code) to the US grew by an impressive 33% to Rs 23 bn and by a whopping 62% to Rs 35 bn to the EU during FY04-FY06. Regulated markets, though difficult to penetrate due to stringent regulations, are known to give better value and margin to exporters. The increasing presence in high-value markets like the USA and Europe has strongly boosted the overall growth of the Indian chemical industry. However, with competition getting stiffer in the regulated markets and the consequent pressure on margins, Indian players are also expanding their geographical reach to high-growth regions

Rise in new product launches

In the pharmaceutical industry, new product launches create new demand. After the introduction of product patent in India, the domestic industry has witnessed a fresh spell of new product launches. New products launched since 2005 accounted for around 12% of the overall market growth. These launches have been done by both domestic and international players and some of them are first time launch of new chemical entity (NCE).

ENTRY BARRIERS

This well-diversified sector covers more than 70,000 commercial products and is intensive in knowledge, capital and power. This sector has made good progress during the last five years, and turned from a net importer in the 1990s to a net exporter. During 2005-06, however, there was a deceleration in the growth rate of the sectorto 8.2 per cent from 14.5 per cent in 2004-05. Major part of Indian exports of chemicals goes to highly developed western countries, where the quality standards are very strict. And therefore following are the industry specific barriers for a new entrant:

Heavy investment in Research and development. Expensive infrastructure Quality assurance norms have to be strictly adhered to.

RISK AND CONSTRAINTS

Cost of power: Very high cost and poor quality of power. Cost of Finance: Chemical industry is highly capital-intensive, cost of finance in

India is very high. Infrastructure: Infrastructure facilities are not of world class.

Weakness: Legacy of Past policies of Industrialization Technology: Low Investment in R&D to be able to sell value added products and

compete in developed countries is absent. Cost Disadvantages : Locational disadvantages, such as extra transport cost for

raw materials as well as finished products. Scale of Production : Plant sizes are not comparable to world scale operations. Multiplicity of Taxes: Multiple levies (various taxes and duties likes sales tax,

turnover tax, Octroi, service tax, electricity duty and cross subsidies etc)..

Threats:

Quantitative Restrictions for imports have been removed already. Most of the chemicals are now in the Open General List(OGL) of import.

Tariff levels in India for most chemicals are significantly higher than in other countries manufacturing the chemicals.

Pressure on the government to reduce these tariff levels. Unless industry acquires competitiveness, it may face extinction.

Price erosion in generics

Indian generics market is witnessing a margin pressure in most of the product categories due to two main reasons: the proposed price control likely to be imposed by the Government and the stiff competition among domestic players. In fact, India has witnessed a fast rise in the number of players over a period of time. Moreover, the expansion of capacities by certain leading players has also fuelled competition in certain product categories, which restricts margins of the smaller players.

The fall in prices of generic drugs are not limited to India only. The US, which is the world’s largest pharmaceutical market, is also experiencing a sharp reduction in prices of generic drugs due to stiff competition. Some other developed countries like the UK and Germany have also witnessed the same scenario. The erosion in prices is to the extent of 90% in some cases. Indian players, which have been operating in these markets, have also witnessed erosion in margins in certain therapeutic segments.

Low R&D productivity

Despite the increasing expenditure on R&D, the introduction of new molecules by Indian players has been limited. It is, in fact, a hit-and-miss situation in the field of discovery and developments of new chemical entity (NCEs), where misses are more than hits. Very few discoveries reach the final stages of approvals, and in most of the cases, the claim for patent gets stuck in legal battles.

In spite of the rising expenditure in R&D, the level of investment in R&D is still low, at average 4% as compared to the global practice of spending 12-16% of sales on R&D.

The European generics market has emerged as a major attraction for acquisitions by Indian companies. According to reports, margin erosion in Europe is much less compared to the US when a drug or formulation becomes generic.

INVESTMENT REQUIREMENTS

Chemical and Petrochemical Industry occupies an important place in the country’s economy, as the Chemical industry has grown at a pace outperforming the overall growth of the industry. The Chemical Industry produces a wide spectrum of products, which include Pharmaceuticals, Dyes, Man-made Fibers, Plastics, Pesticides, Fertilizers, Cosmetics and Toiletries, Paint, Auxiliary Chemicals and wide range of Organic and Inorganic compounds for applications ranging from automobiles, textile industry, engineering industry, construction chemicals and food additives to veterinary and health care products.

The lower per capita consumption of many important items at present and growing middle class with increasing purchase power constitutes an attractive market for various products The development of Chemical and Petrochemical Industry requires creation of basic and allied infrastructure facilities and in view of the availability of the same, the Indian/Gujarat Chemical Industry has opportunity to grow within as well as outside the country. Further the motivated entrepreneurs, pool of technical manpower and flexibility to changes in production set up which forms the competitive strength of the Chemical Industry in the State and therefore, will rise to all opportunities for development and growth in the investment.

The Chemical Industry needs to engage in strategic partnerships with foreign partners with a view to realize and capitalize the latent potential. The existing technology needs to be upgraded with the help of foreign partners. The Chemical Industry in India/Gujarat provides a large scope for collaboration in Technology tie-up, Process Development, Joint Research and Development, Solid and Liquid Waste Management and Market Access for various sub-sectors of the industry.

GOVERNMENT POLICIES

Government policies play an important role in shaping the future of any business. Decision makers at both macros as well micro level will have to take into account existing policies, the way Govt. and other bodies are thinking about them and what will be the shape of these policies in future to come.

Industrial Policy: The items, which require compulsory license are Hydrocyanic acid and its derivatives; Phosgene and its derivatives; Naptha/Gas cracker complexes producing and its ethylene, propylene, aromatic complexes manufacturing benzene, toluene & xylenses- o-xylene, ethylene oxide and polyethylene having a specific gravity of less than 0.94

Policy for foreign direct investments facilities approval through automatic route. The following categories of FDI proposal are only approved through foreign investment promotion board. All proposal that require industrial licence includes, the items requiring an industrial licence under the IDR Act, 1951; all items which require industrial licence in terms of locational policy notified by government under the new industrial policy. All proposals relating to acquisition of shares in existing Indian company in favour of a foreign/NRI/OCB investor. All proposals failing outside sectoral policy/caps or under sectors in which FDI is not permitted and/or whenever any investor chooses to make an application to the FIPB an not to avail of the automatic route

KEY PLAYERS IN INDIAN INDUSTRY

Indian Chemical Council, ICC is the apex national body representing all the sectors of the chemical industry in India viz. Organic and Inorganic, Plastics and Petrochemicals, Dyes and Dye-intermediates, Drugs and Pharmaceuticals, Agrochemicals and Pesticides, Fine Chemicals, Specialty Chemicals etc. ICC has its members spread all over India. Since the concentration of the chemical industry is mainly in Maharashtra and Gujarat, the western region consists about 60 % of the total membership of ICC.

Few well known and major Indian players of this industry are Ranbaxy in pharmaceuticals, Asian paints, Pidilite in paints and dye segment.

FUTURE OUTLOOK

The Indian chemical industry is passing through a transformation and industry players are organizing themselves to avail of the immense opportunities that have opened up globally. The sector is set to report impressive growth in the years to come and outlook for the industry remains strong.

Following are the factors which substantiate the strong outlook for the industry:

Demographic factorsPopulation growth coupled with rise in per capita income and increasing usage are factors which will continue to drive domestic demand for the chemical industry. According to projections given in the Economic Survey 2005-06, India’s population is likely to touch 14.11 bn by 2026.

New product launchesAfter the introduction of product patent laws in India, multinational companies have shown renewed interest in launching some blockbuster products in India. This trend is likely to continue in future as well. Launches of new molecules by MNCs will accrue contract manufacturing and in-licensing opportunities for Indian players including the small and medium enterprises. SMEs have acquired expertise in formulations & chemical synthesis. Manufacturing under contracts gives them a safe position against margin fluctuations.

Increasing investments in R&D in pharmaceutical industryGiven the long gestation period right from the discovery of molecules to the final approval for marketing, the current investments made towards R&D will lead to sustainable growth. Some important molecules developed by Indian players have already reached different stages of clinical trials, some of which have reached the critical phase-II.

Growing generics market - an opportunity for IndiaIncreasing number of products getting off-patent and recognition of generic drugs by some developed countries is set to expand opportunities for India in the generics market. The generic industry is estimated to grow by more than 20% annually till 2008 and the total size is estimated to be around US$ 80 bn by 2008. In the US, generic drugs make up for 55% of the prescription written.

Leveraging the cost-effective production capabilities of Indian manufacturers, better scientific skills and favourable regulatory environment, the Indian pharmaceutical industry is well-placed to tap these opportunities.

Growing exports marketExports will continue to remain strong and an enabler of growth for the chemical industry. Impressive performance of Indian exports, achieved during last few years, is likely to continue in the near future. Despite the growing competition in the global generics market and increased participation among developing countries in the global chemical market, Indian companies have already proven their ability to compete.

CRAMs opportunities will continue to pick upContract manufacturing and contract research will gain prominence among the Indian pharmaceutical companies. There has been a spate of tie-ups and acquisitions by companies in the CRAMS segment in India. The driving factors include the rising manufacturing costs in developed countries and falling prices in the generics segment world over. India aptly suits the changing global scenario, having the largest number of US FDA approved facilities outside the US and low cost manpower with technical expertise. Contract manufacturing business is estimated to touch US $30 bn by 2010 and is likely to grow at 10-12%.

In the field of R&D, Indian companies are capable of conducting various clinical trials at relatively lower costs. Although India has also started experiencing rising bills on skilled manpower, it is still in a relatively advantageous position on the cost front. Contract research business is estimated at US$ 6-10 bn, and is growing in the range of 16-18%.

Competitive Advantage of India Large resource of scientific and technical manpower Large domestic market for various sectors of chemicals. Long coast line and abundant availability of salt. Tropical region: facilitating open storage for bulk chemicals. A developed financial market. A large English-speaking population Rapid growth in Information Technology provides competitive access to the rich

European and American market.

Vision for the Future

Developing a global outlook World scale capacities Mutually beneficial strategic alliances Responsible care

Following diagram shows Indian chemical industry and how can it increase its hold in global market

RECOMMENDATIONS

For most of the leading companies in speciality segment and pharmaceutical sement, the future is indeed promising. Biotech, is also an upcoming sector and its market will shoot high with coming period.

The establishment of business relations with these companies will definately prove fruitful to HDFC Bank and will open new avenues for its growth and success.

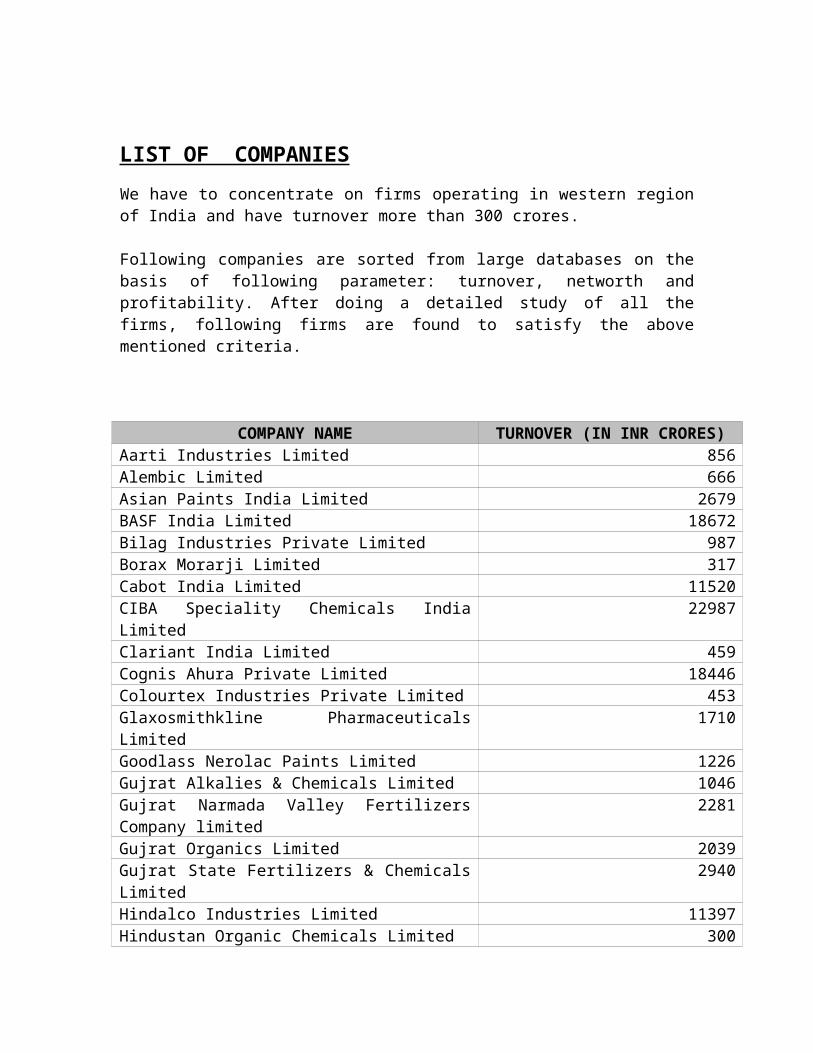

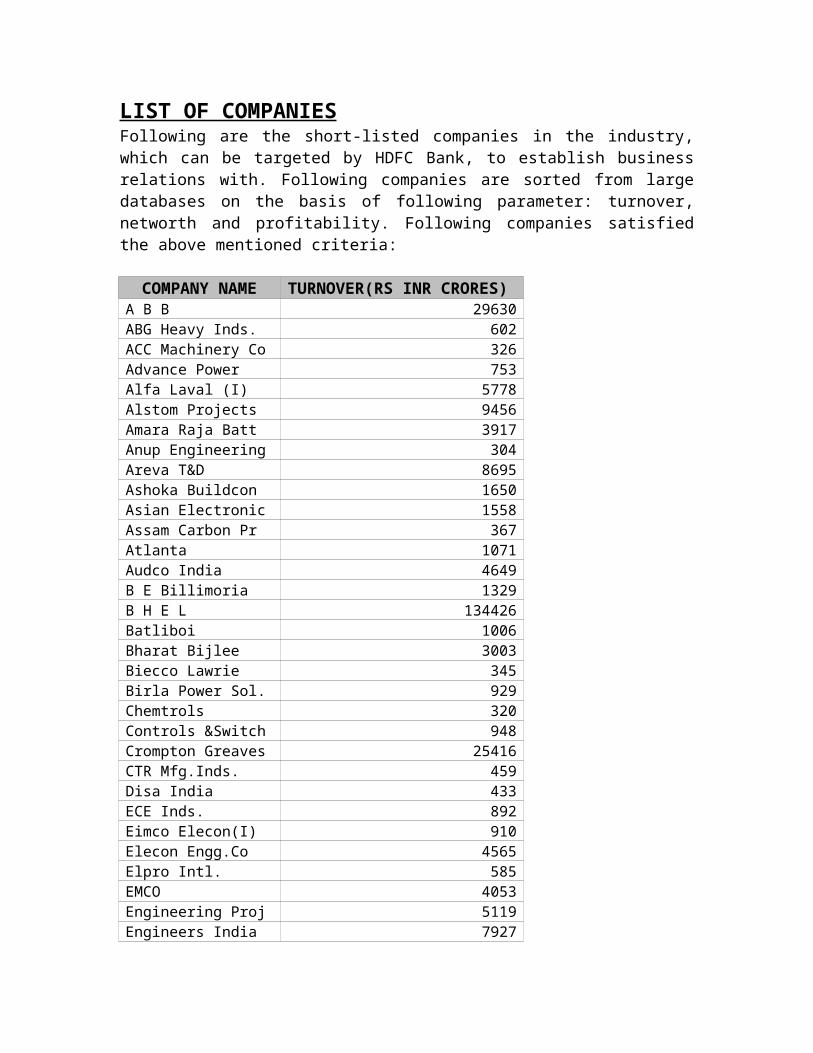

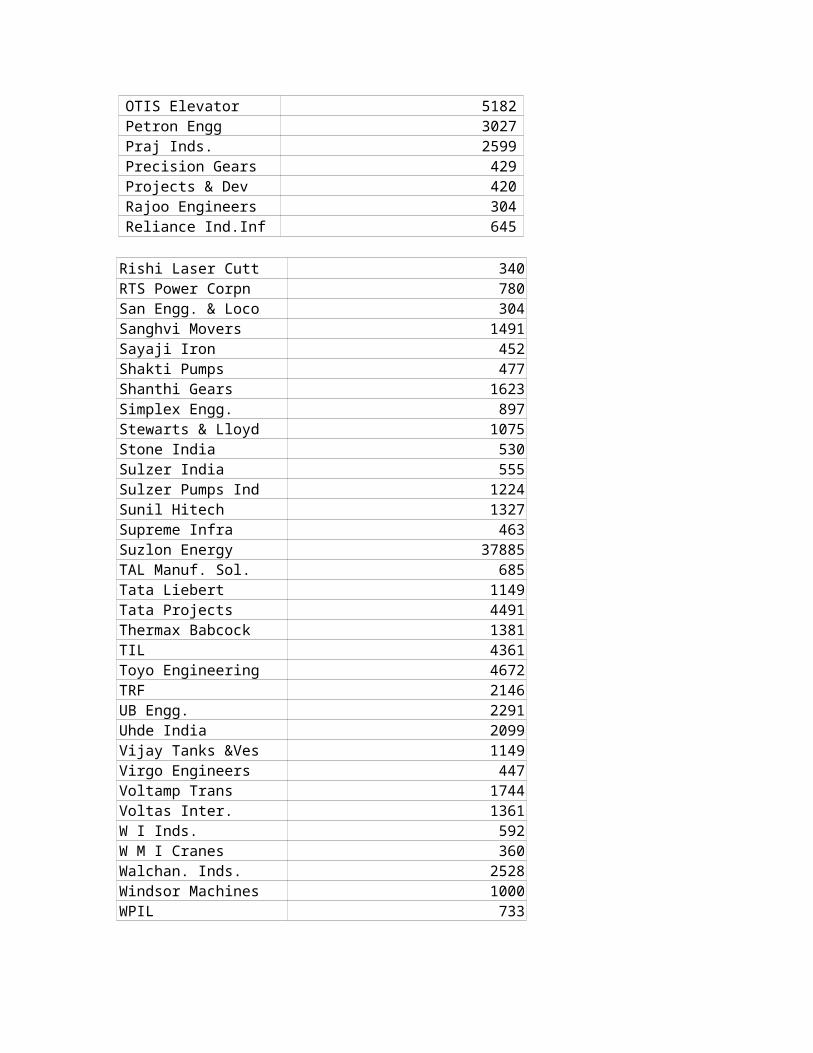

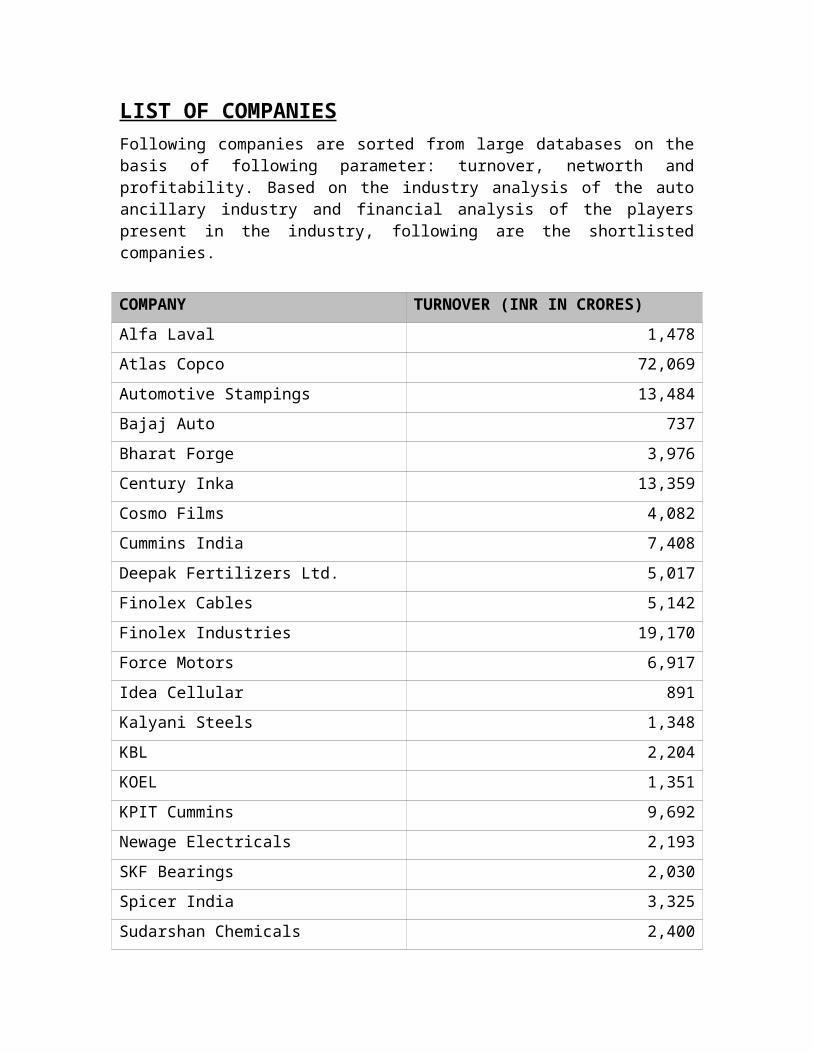

LIST OF COMPANIES

We have to concentrate on firms operating in western region of India and have turnover more than 300 crores.

Following companies are sorted from large databases on the basis of following parameter: turnover, networth and profitability. After doing a detailed study of all the firms, following firms are found to satisfy the above mentioned criteria.

COMPANY NAME TURNOVER (IN INR CRORES)Aarti Industries Limited 856Alembic Limited 666Asian Paints India Limited 2679BASF India Limited 18672Bilag Industries Private Limited 987Borax Morarji Limited 317Cabot India Limited 11520CIBA Speciality Chemicals India Limited 22987Clariant India Limited 459Cognis Ahura Private Limited 18446Colourtex Industries Private Limited 453Glaxosmithkline Pharmaceuticals Limited 1710Goodlass Nerolac Paints Limited 1226Gujrat Alkalies & Chemicals Limited 1046Gujrat Narmada Valley Fertilizers Company limited 2281Gujrat Organics Limited 2039Gujrat State Fertilizers & Chemicals Limited 2940Hindalco Industries Limited 11397Hindustan Organic Chemicals Limited 300Hindustan Engg. & Industries Limited 386Indian Petrochemicals Corporation Limited 12362Indofil Chemicals Company 328Lanxess ABS Limited 473Lubrizol India Private Limited 365Lupin Laboratories Limited 1661Merck Limited 99714Nirma Limited 2244Pidilite Industries Limited 1044Rashtriya Chemicals & Fertilizers Limited 952TATA Chemicals Limited 3517United phosphorous Limited 363

ANALYSIS

OF THE

POWER EQUIPMENT

INDUSTRY

37

POWER INDUSTRY OVERVIEW

India's power market is the fifth largest in the world. The power sector is high on India's priority as it offers tremendous potential for investing companies based on the sheer size of the market and the returns available on investment capital.

India is witnessing more than 8% growth in GDP for third year in succession. With huge and rising investment in infrastructure, capacity additions across the industry, the demand for power is set to escalate on a sustainable basis for years to come. Already, the country is witnessing widening of demand supply gap, and to fuel the growth, there is urgent need to scale up power generation and distribution capacities and to reduce transmission and distribution losses. While significant progress have been made in facilitating private participation, the weak link remains to be the poor financials of State Electricity Boards and populist and lack of political will to charge market related rates for residential and agriculture sector. The ultra mega power projects can partly satisfy the growing demand, and Central PSUs keep bringing in fresh capacities.

Power sector in India aims to provide power to all by FY 2011-12, to achieve it, a multi-pronged strategy has been chalked out, which includes:

Distribution reforms Renovation and modernization of old power plants Demand-side management and capacity addition.

INDUSTRY STRUCTURE

The power equipment industry can be broadly classified into three segments.

Power generation equipment such as turbines, generators and boilers. Transmission and distribution equipment such as transformers, distributors and

instrumentation and control systems. Services for renovation and modernisation.

Though part of the same industry, these segments are different when it comes to business characteristics.

Analysts reckon power equipment makers/solutions provider to the power sector stand to benefit from the expected huge expansion in the power generation sector and transmission & distribution segment over the next few years. Easing copper and steel prices also bodes well for these firms.

MARKET

INDIAN MARKETThe current installed capacity of power plants is 124, 287 MW (as of March 2006). Almost 55 percent of this capacity is based on coal, about 10 percent on gas, 26 percent on hydro, just under 5 percent on renewable sources, about 2.6 percent on nuclear and 1 percent on diesel.

In the past few years, there has been considerable growth in power plants based on renewable sources of energy. The current installed capacity based on these sources is about 6,200 MW of total utility capacity. In addition, as the merits of hydro have become apparent, in an era of high fuel prices, there has been a big push for hydro. An initiative to add 50,000 MW of hydro capacity by 2017 was announced in 2003. The current installed capacity, at about 32,000 MW, utilizes just over one -fifth of 150,000 MW hydro potential.

The Plant Load Factor (PLF) of generating plants has improved consistently over the last 10 years. In 2005-06, the PLF of generating plants was almost 74 percent, compared to 60 percent in 1994-95.

In the past five years, there has been a much greater emphasis on transmission and distribution reforms. The interregional transmission capacity has been increased to 9,500 MW. The National Grid Development Programme calls for 37,150 MW of interregional capacity by 2012.

The reform process in the power sector continues. Thirteen states have unbundled SEBs into separate entities for transmission, distribution and generation. Two states have privatized distribution. Regulatory authorities have been set up in 24 states. These authorities are applying commercial principles to tariff setting, monitoring the performance of state utilities and paying attention to areas such as demand side management and grid discipline.

The government aims to provide "power to all" by 2012. To achieve that promise, it will have to add as much as 1,00,000 MW of generation capacity, cut AT&C losses substantially to below 20 percent, rationalize tariffs and ensure that average revenue realization is greater than the cost of production. It will have to continue to push the process of reform and restructuring and ensure greater private participation, in every segment.

DEMAND AND SUPPLYAs India is a rapidly growing economy, the demand for power is ever rising and thus cannot be quantified. However, it is very clear from this analysis of this industry that there exist an acute gap between the supply and ever growing demand.

INDUSTRY DYNAMICS

ELECTRICITY ACT 2003Electricity Act 2003 has been enacted. The objective is to introduce competition, protect consumer's interests and provide power for all. The Act provides for National Electricity Policy, Rural Electrification, Open access in transmission phased open access in distribution, mandatory SERCs, license free generation and distribution, power trading, mandatory metering and stringent penalties for theft of electricity.

It is a comprehensive legislation replacing Electricity Act 1910, Electricity Supply Act 1948 and Electricity Regulatory Commission Act 1998. The aim is to push the sector onto a trajectory of sound commercial growth and to enable the States and the Centre to move in harmony and coordination.

The Electricity Act 2003 has had a positive effect on the entire sector, including generation. Overall, this legislation has liberalized generation and freed it from licensing. The requirement of techno - economic clearance has also been removed. In addition, the recently announced National Tariff Policy makes it mandatory that all future requirements of power should be produced through a competitive bidding mechanism instead of cost-plus route.

The positive environment created by the electricity act and the proactive role-played by the ministry of power in helping private projects achieve financial closure have led to a revival of the IPP model.

Seven ultra mega coal based power projects with a capacity of 4000 MW each in the first phase are on the anvil. These projects will be set up at Sasan in Madhya Pradesh, Mundra in Gujarat, Akaltara in Chhattisgarh, Karvar in Karnataka, Ratnagiri in Maharashtra, Krishnapatnam in Karnataka, and in Orissa. For the Orissa project, three sites- Hirma, Derabahai and Bhashma have been short-listed.

The initial development work (land acquisition, water linkage, EIA studies, preparation of project report, etc.) is being done through SPV companies, with initial funding provided by the Power Finance Corporation (PWC). Each company will be a fully owned subsidiary of PFC. These projects will be awarded on the basis of competitive bidding. The bidding will be based on the first year of tariff quoted. The projects will be transferred to the investors by the end of 2006. These projects will entail a total cost of Rs. 750 billion. They are likely to be financed at debt-equity ratios of 70:30. The cost of power from these projects is estimated to be about Rs. 2.50- 2.75 per unit.

The recent Indo-US nuclear deal makes nuclear power a much more realistic option for the future. The centre has given approval for the construction of eight new nuclear reactors with a combined capacity about 6,800 MW.

The Government plans to add 32,000MW in the tenth plan and an additional 67,500 MW in the eleventh plan. The capacity addition target for the twelfth plan stands at 66,500 MW.

GENERATIONIndia's power generation capacity (excluding captive plants) stood at 124,287 MW in March 2006. Actual generation has grown at a CAGR of about 5.82 per cent in the last decade from 350,490 MUs in 1995-96 to 617,382 MUs in 2005-06.

The overall generation in the country has increased (Thermal + Nuclear + Hydro) in public utilities in the country over the years is as under:

YEARGENERATION (BILLION

UNITS)

1990-91 264.3

1995-96 380.1

2000-01 499.5

2001-02 515.3

2002-03 531.4

2003-04 558.3

2004-05 587.4

2005-06 (Upto Feb. 2006) 562.7

Source: Annual Report 2005-06, Ministry of Power

The bulk of the capacity is thermal (coal, gas, liquid fuel and diesel). Thermal plants contribute 66.3 percent to overall capacity. Of this coal contributes 55 percent of the capacity, gas another 10 percent, while the rest (1 percent) is based on diesel.

Over the years, the fuel mix has changed. The share of power from thermal sources decreased from 71 percent in 1994-95 to 66.3 percent in 2005-06. The share of hydro has increased from 25.7 percent to 26 percent. Growing environmental concerns have led to an interest in renewable sources of energy (comprising wind energy, solar photovoltaic energy, biomass power and mini hydro plants). But despite great potential, renewable sources contribute only a little over 6,000 MW at present.

The contribution of the private sector to installed generation capacity was 14, 139 MW or 11.3 percent in 2005-06. Amongst the private players, Tata Power has the highest installed capacity at 2,300 MW. In terms of actual generation, private contribution is 8.7 percent. There is renewed interest in IPPs in the power sector. Private IPPs contributed 5,961 MW to installed generation capacity in March 2006.

The PLF of generating plants has improved consistently over the last few years. The all India average PLF on March 2006 stood at 73.6 percent compared to 60 percent in 1994-95. The PLF of central plants in 2005-06 was 82.1 percent while the average PLF of the

state sector units was close to 67 percent. The average PLF of the private sector was 85.4 percent in 2005-06.Drivers of power generation are:

Orders from new power projects and is thus heavily dependent on their commissioning.

Replacement demand is limited and restricted to renovation and modernisation.

Being heavy capital equipment they have a long manufacturing time cycle. Typically, the manufacture of a turbine/generator for a 500 MW plant would take about 36-42 months from the order's date. The approximate value of such equipment would be about Rs 2,000 crore.

Technology in this segment is mature and there have been few developments in turbine or generator technology in the last two decades. The last major development in turbine technology was the development of gas turbines by General Electric in the 1980s. Since then there have been rapid improvements in gas turbine technology but there has been nothing radical or path-breaking. There are just a handful of companies in the whole world in this business such as,

GE Siemens Alstom Mitsubishi

They are either present on their own in different countries across the world or they license their technology to others.

TRANSMISSION Transmission lines have grown from 3,708 ct. Km in 1950 to more than 2,64,240 ct. km in 2005. In the last four years, the network has grown by about 12.5 percent. It is projected to grow to 3,50,000 ct. km.

Transmission projects continue to be accorded a high priority in the context of the need to evacuate power from generating stations to load centres, system strengthening and creation of National Grid. The construction targets of transmission projects for the year 2005-06 and the achievements up to December 2005 are summarized below:

Parameter MOU Target (Excellent)

Achievement upto December 2005

Percentage of Achievement

No. of Ckt Kms. Ready for commissioning 3800 4040 106.00%

Transformation Capacity Addition 4885 4670 95.50%

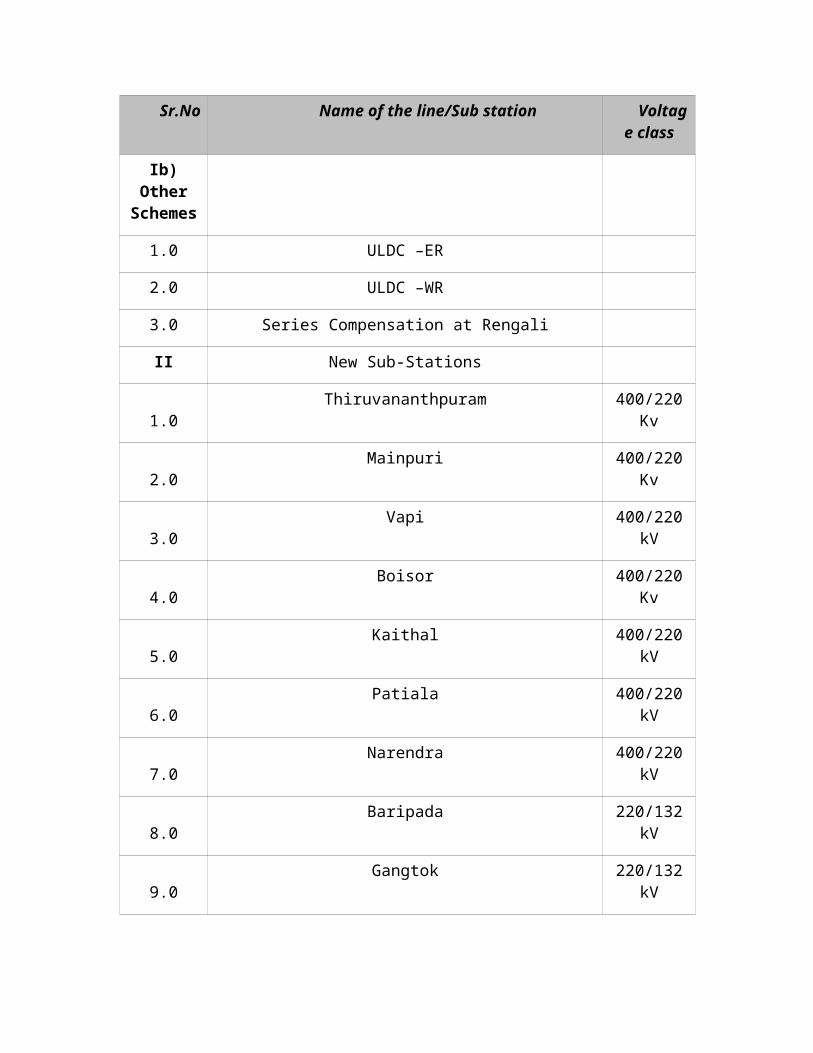

Transmission lines and sub-stations completed during the year 2005-06 (upto December 2005) are shown in the following table:

Sr.No Name of the line/Sub station Voltage class

Ia Transmission Lines

1.0 Rihand- Allahabad-Mainpuri D/c line 400 Kv

2.0 Mainpuri-Ballabgarh D/c line 400 Kv

3.0 Patiala- Malerkotla S/C line 400 kV

4.0 LILO of Nalagarh-Hissar at Patiala & Kaithal D/C 400 Kv

5.0 Raipur- Chandrapur D/C 400 kV

6.0 LILO of Bongaigaon –Malda at Siliguri D/C 400 kV

7.0 Madurai- Thiruvananthapuram D/C 400 kV

8.0Dhauliganga (NHPC) –Bareily (UPPCL) D/C

(to be initially charged at 220 KV level)400 kV

9.0 Tarapur 3&4- Boisor D/C transmission Line 400 kV

10.0 Tarapur 3&4 –Padghe D/C transmission line (Ckt –II) 400 kV

11.0 LILO of S/C Gandhar – Padghe line at Boisor 400 kV

12.0 Kaiga – Narendra D/C Line 400 kV

13.0 LILO of S/C Gandhar – Padghe at Vapi 400 kV

14.0 LILO of S/C Nagarjunsagar –Raichur at Mahaboobnagar 400 kV

15.0 Meerut (POWERGRID)- Shatabdi Nagar S/C line 220kV

16.0 Tarapur 3&4 – Boisor S/C Tr. Line 220kV

17.0 LILO of D/C Siliguri- Gangtok at Melli 132kV

18.0 LILO of 1st Ckt. Of D/C Siliguri- Rangit at Gangtok (New) 132kV

Ib) Other Schemes

Sr.No Name of the line/Sub station Voltage class

1.0 ULDC –ER

2.0 ULDC –WR

3.0 Series Compensation at Rengali

II New Sub-Stations

1.0 Thiruvananthpuram 400/220 Kv

2.0 Mainpuri 400/220 Kv

3.0 Vapi 400/220 kV

4.0 Boisor 400/220 Kv

5.0 Kaithal 400/220 kV

6.0 Patiala 400/220 kV

7.0 Narendra 400/220 kV

8.0 Baripada 220/132 kV

9.0 Gangtok 220/132 kV

GROWTH DRIVERS

Unlike the generation equipment segment the T&D equipment business relies equally on new orders and replacement demand. It has been able to survive even in the complicated business environment of the last decade thanks to business from the replacement market. Of course, the replacement market is not as large as it should be for the installed capacity of 1 lakh MW in the country because of the absence of a good renovation and maintenance programme in most power plants.

The companies engaged in laying of power transmission lines in India historically had been getting business of laying power transmission lines at Middle East / North Africa on account of being cost competitive. Lately companies engaged in laying of power transmission lines in India have been getting business of laying power transmission lines at Middle East / North Africa due to increase in income level of this region on account of increase in oil prices / due to reconstruction activity undertaken in countries like Iraq.

Restrictions on GrowthThe orders for laying of power transmission lines historically were mainly received from SEBs (are incurring losses and have track record of delayed payments of retention

money). This resulted in restricted business opportunities for the companies in India engaged in power transmission line business.

This segment is highly competitive, especially as one goes down the value chain. For small products such as distribution transformers and energy meters there is tremendous competition that thins out in the high value/high technology products. Competition is more even here between BHEL and MNCs such as ABB, Siemens and Alstom. After the worldwide divorce between ABB and Siemens in 2000, ABB now concentrates on the transmission and distribution business leaving the generation equipment area to Alstom.

DISTRIBUTIONThe demand for electrical energy is ever increasing. Today over 21% of the total electrical energy generated in India is lost in transmission (4-6%) and distribution (15-18%). The electrical power deficit in the country is currently about 18%. Clearly, reduction in distribution losses can reduce this deficit significantly. It is possible to bring down the distribution losses to a 6-8 % level in India with the help of newer technological options (including information technology) in the electrical power distribution sector that will enable better monitoring and control.

Electric power is normally generated at 11-25kV in a power station. To transmit over long distances, it is then stepped-up to 400kV, 220kV or 132kV as necessary. Power is carried through a transmission network of high voltage lines. Usually, these lines run into hundreds of kilometres and deliver the power into a common power pool called the grid. The grid is connected to load centres (cities) through a sub-transmission network of normally 33kV (or sometimes 66kV) lines. These lines terminate into a 33kV (or 66kV) substation, where the voltage is stepped-down to 11kV for power distribution to load points through a distribution network of lines at 11kV and lower.

Distribution Companies

With State Electricity Boards (SEBs) having to restructure themselves following the passage of the Electricity Act, 2003, the power sector has undergone a significant structural change. A key constituent of the evolving industry structure in each State will be the Distribution Companies (DISCOMs), which will be providing the “last mile” connectivity to the final consumers, both retail and wholesale. Several large players in the power sector plan to acquire majority stakes in the state owned DISCOMs once they are up for privatisation. While traditionally, DISCOMs have been purchasing power from the State Transmission Utilities (Transcos) —usually the successors of the SEBs—through long-term power purchase agreements (PPAs), the procurement pattern could also undergo a change with the Electricity Act, 2003 allowing freedom to licensees to source power from any source. Also since Transcos are not allowed to trade in power as per the Electricity Act, 2003, the PPAs would also need to be reassigned.

The demographic profile of the service area that a DISCOM serves determines the quality of cash flows, as well as the extent of likely threat from competition. Given the level of cross-subsidy currently prevalent in the tariff structure, a high proportion of agricultural consumption inevitably implies greater burden of subsidy payment on the State

Government, as well as relatively higher levels of cross-subsidy. At the same time, a higher proportion of Commercial and High Tension(HT) segment in the consumer mix implies greater vulnerability to competition in a liberal regime for captive power plants (CPPs) and in an open access scenario that allows freedom to consumers to source power from alternative sources. The key determinants of demographic profile are:

Proportion of various consuming segments Growth rates in different segments Extent of agricultural consumption Geographical dispersion of HT consumers

The extent of geographical dispersion within the HT segment is an indicator of concentration risk and hence competitive threats. ICRA also assesses the steps being taken by the utilities /State Government to minimise the impact of high paying consumers switching from the incumbent licensee. ICRA notes, for instance, that utilities in some states have initiated supply of power to HT industrial consumers through a special incentive scheme at tariffs that are substantially lower than the normal tariff levels applicable for such consumers. Further, some State Governments have been levying taxes on captive power generation, which also mitigates the threat from CPPs to an extent, although questions remain about the sustainability of such measures.

The major power equipment makers in the distribution segment are,

Company Name SalesEMCO 405.37

Bharat Bijlee 300.29 Voltamp Trans 248.79 Accurate Trans. 150.74

Indo Tech 97.34 Trans. & Elec. 82.90

RTS Power Corpn 78.01 IMP Powers 67.40

Services

Services is a lucrative activity given the large installed base and it is not surprising that MNCs such as Alstom and ABB are rather active in this business. Here again, the market has not really taken off as it should have and the reasons are familiar. State electricity boards that own the majority of the stations in need of renovation and modernisation are in no position to use the limited funds they generate in R&M activity. That this market is lucrative is evident from the two joint ventures floated by BHEL with GE (BHEL-GE Gas Turbine Services Ltd) and Siemens (Powerplant Performance Improvement Ltd). These two companies service the existing installations based on their respective technologies. A measure of their success is that both these companies are doing very well financially, with one of them declaring a 95 per cent dividend for 2000-01. Others such

as Alstom are equally active in this business. In fact, it is these areas that provide them with business in this difficult environment.

Towards Formation of National Grid

Ministry of Power has envisaged establishment of an integrated National Grid in the country by the year 2012 with an inter regional power transfer capacity of about 37,150 MW (enhanced from earlier planned target of 30,000 MW). A perspective transmission plan has been evolved for strengthening the regional grids with the ultimate objective of establishment of strong and vibrant National Power Grid to support the generation capacity addition program of about 1,00,000 MW during the tenth and eleventh plans.

Private Sector Participation in Transmission

The first major step towards encouraging private investment in the power sector was taken in 1991 by providing a legal framework through an amendment of the then existing Electricity (Supply) Act, 1948 enabling private sector participation in generation. Subsequently, a definite tariff framework was also put in place through notification issued by the government of India.

POWERGRID has established First Public -Private joint venture in Indian Power sector with M/s Tata Power (POWERGRID's stake is 49 percent and M/s Tata Power's stake is 51 percent in the joint venture company viz. "Powerlinks Transmission Limited") for implementation of major transmission lines of Transmission System associated with Tala HEP in Bhutan, East-North inter connector and northern region transmission costing about Rs. 1612Crore. This letter received excellent response from International Funding Institutions like IFC, Washington including multilateral financing from private sector arm of ADB, Manila, and Indian Financial Institutions like IDFC and SBI.

The JV Company has received its transmission license from CERC, the first such license in Indian Power Sector. Financial closure of the project was achieved in May 2004. A debt of Rs. 980mCrore has been tied up with the consortium of multilateral and domestic financial institutions.

Action has been initiated to bring in more private investment in transmission projects and two more projects. For example: transmission systems associated with Koldam and Parbati- II (Estimated Cost: Rs.660 Crore) have been floated under joint venture route. In addition, some transmission lines under Western Region Strengthening Scheme are envisaged to be implemented through 100 percent private sector participation (IPTC).Ministry of Power is in the process of finalizing policy guidelines for private investment in transmission.

ENTRY BARRIERS

As the number of companies in power transmission line sector in India is low (as there are high entry barriers on account of power transmission line projects being awarded on the basis of project execution track record), leading companies like KPTL will reap the benefits of growth in power transmission line sector in India. Also the trend in the power transmission line sector in India is increasingly to go for laying of HVDC power transmission lines, where transmission and distribution losses are lower, thereby KPTL would be again benefited as very few companies including KPTL along with global majors like ABB have expertise in HVDC power transmission lines.

RISK & CONSTRAINT

CHINESE Threats to POWER EQUIPMENT Industry

Chinese electrical equipment manufacturers are set to enter India due to the ultra mega power projects (UMPPs) and the renewed interest in India’s power sector. Companies such as Dongfang, Chint Electrics, Wenzhou Hezhong and China National may claim a sizeable stake in India’s electrical power spectrum, if talks with domestic players succeed.

Dongfang is planning to tie up with Lanco Infratech, which outbid players to win the country’s first UMPP at Sasan, for supplying super critical boilers. But Dongfang has to get licence to sell its products outside China and talks are currently on. Chint and Wenzhou Hezhong are evaluating the opportunities and may start equipment supply to medium-scale projects in the country. China National had held talks with two power generation companies, though they are yet to materialise.

At present, out of 95 private power projects, 58 projects for around 36,000-mega watt (MW) capacity have foreign developers. As per the information available, around Rs 10,500 crore foreign investments has already been made in the private power sector. Global majors such as Siemens, Samsung, LG, ABB and Areva have units in India. As of now, the presence of Chinese companies in the power sector is marginal, but this scenario may change when the other UMPP bids are finalised,.

Encouraged by the response to the first two UMPPs, the government plans to award three more UMPPs in 2007. The first project, Krishnapatnam in Andhra Pradesh, is targeted for award in April 2007, second one in May-June 2007 and third by the year-end.

Chinese companies are now looking at opportunities outside their country. Once the growth within China is saturated, these companies will have to find new markets. Comparing the economy growth and market potential, both India and China have many similarities.

The south Asia region, consisting of Bangladesh, Bhutan, India, the Maldives, Nepal, Pakistan and Sri Lanka, is witnessing rapid growth in energy demand. With a 1.4 billion population, this region constitutes almost one-fifth of the world population. But half of this population still lives in darkness. “Traditionally, Chinese companies were considered to be weak in after-sales-service. But the situation is changing This may lead to Indian companies importing equipment from China at competitive prices.

With the government’s commitment to scale-up capacity, Chinese players are now taking a serious look at the Indian market. With a project of 4,000 MW on hand, Dongfang may consider setting up a stronger base in India. If the Sasan project proves successful, more Chinese investments can be expected, and Bhel’s market share in new projects may come under pressure.

INVESTMENT REQUIREMENTS

Investment needs in the power sector:

New Power Plants – Rs. 150,000 Crs Transmission Line – Rs. 71,000 Crs Renovation of Old power plants – Rs. 100,000 Crs

Investment Opportunities and Potential

According to Central Electricity Authority's sixteenth electric power survey, peak demand is expected to increase by a staggering 77 percent to 157,107 MW by 2012. Similarly, the energy requirement is also expected to increase by 274 percent to 975,222 MU by 2012. It is estimated that a capacity addition of over 100,000 MW units by 2012 to bridge the supply deficit and keep up with the increasing demand. The total investment required in capacity creation, along with necessary investments in transmission and distribution segments is estimated at US$ 200 billion. This quantum of investment calls forth public -private partnerships in the sector.

Hydro Projects Sixty eight percent, i.e., 101,454 MW of potential capacity is still not

developed. Seventy-seven schemes with a cumulative total of 33,000 MW have been

identified. Captive Power

At present, CPP accounts only for fifteen percent, i.e., 22,100 MW of total combined capacity. Government plans to bring further 5000 MW into mainstream.

"Open Access" and "Group Captive" allowed under recent policy initiatives.

Ultra Mega Power Projects Seven projects with an individual capacity of 4000 MW, requiring an

investment of approximately US$ 3.26 billion (INR 15,000 crore) each have been identified.

Nuclear Power In the post indo-US agreement period, there is scope for private -public

partnership in this sector National Grid Program

The program envisages addition of over 60,000 ckm of transmission network in a phased manner by 2012 with an estimated investment of about US$ 15.18 billion. Of this about US$ 4.33 billion is ought to be mobilized through private participation.

Distribution: with respect to distribution, the following opportunities exist a) Rural Electrificationb) Privatization of Discomsc) Participation under Franchise Model

Trading "Power Pools" system has been established to facilitate trading

opportunities for licenses. Renewables

Existing untapped wind energy potential of 45,000 MW. Untapped Bio-power potential of 52,000 MW. Untapped Cogeneration- bagasse based potential of 5000 MW.

Investment PolicyThe 1991 Power Policy seeks to attract significant private sector investment in the Indian power sector. The key initiatives include:

Private sector permitted to set up cool, gas or liquid based thermal project, hydel projects and wind or solar projects of any size.

Foreign equity participation brought under automatic approval of generation, transmission and distribution of power generated in hydro-electric, oil based and coal/lignite based power projects.

Role of the Central Government curtailed and the State Governments and State Electricity Boards (SEBs) empowered to negotiate directly with developers, facilitating speedy clearances for the investor.

Ancillary sector such as cool significantly deregulated. 100% foreign equity permitted.

Opportunities

Demand is expected to grow to 570 billion Kwh by 2001-02 and to 782 billion Kwh by 2006-07. Over the 10 year period from 1997-2007, a total capacity addition of 98,000 MW is envisaged, entailing an investment of Rs. 5,750 billion in power generation, transmission and distribution.

The specific project opportunities expected in the near future include:Liquid Fuel Based Projects using low sulphur heavy stock (LSHS), furnace oil (FO), heavy petroleum stock (HPS), Naphtha, Vacuum Residue, Condensate and Orimulsion are permitted by the Government. Import of liquified natural gas (LNG) is also being considered for setting up large capacity combined cycle power plants, Transmission projects for power transfer are available for competitive bidding by the Central Transmission Utility (Power Grid) and State Transmission Utilities (SEBs)/Grid Corporations). The transmission system project are being identified for competitive bidding by the Central and State Transmission Utilities.

Attractive investment opportunities are likely to develop in distribution of power as several State governments have agreed to allow the gradual entry of the private sector in distribution.

Non-Conventional Energy Sources

Investment Policy