simulating exchangeable multivariate archimedean copulas and its applications authors: florence wu...

Post on 19-Dec-2015

249 views

TRANSCRIPT

Simulating Exchangeable Simulating Exchangeable Multivariate Archimedean Copulas Multivariate Archimedean Copulas

and its Applicationsand its Applications

Authors:

Florence Wu

Emiliano A. Valdez

Michael Sherris

LiteraturesLiteratures

Frees and Valdez (1999)– “Understanding Relationships Using Copulas”

Whelan, N. (2004)– “Sampling from Archimedean Copulas”

Embrechts, P., Lindskog, and A. McNeil (2001)– “Modelling Dependence with Copulas and

Applications to Risk Management”

This paper:This paper:

Extending Theorem 4.3.7 in Nelson (1999) to multi-dimensional copulas

Presenting an algorithm for generating Exchangeable Multivariate Archimedean Copulas based on the multi-dimensional version of theorem 4.3.7

Demonstrating the application of the algorithm

Exchangeable Archimedean Exchangeable Archimedean CopulasCopulas

One parameter Archimedean copulasArchimedean copulas a well known and

often used class characterised by a generator, φ(t)

Copula C is exchangeable if it is associative– C(u,v,w) = C(C(u,v),w) = C(u, C(v,w)) for all

u,v,w in I.

Archimedean CopulasArchimedean Copulas

Charateristics of the generator φ(t): (1) = 0– is monotonically decreasing; and

– is convex (’ exists and ’ 0). If ’’ exists, then ’’ 0

C(u1,…,un) = -1((u1) + … + (un))

Archimedean Copulas - Archimedean Copulas - ExamplesExamples

Gumbel Copula (t) = (-log(u))1/

-1(t) = exp(-u)

Frank Copula (t) = - log((e-t – 1)/(e- – 1)

-1(t) = - log(1 – (1 - e- )e-t) /log()

Theorem 4.3.7Theorem 4.3.7

Let (U1,U2) be a bivariate random vector with uniform marginals and joint distribution function defined by Archimedean copula C(u1,u2) = -

1((u1) + (u2)) for some generator . Define the random variables S = (u1)/((u1) + (u2)) and T = C(u1,u2). The joint distribution function of (S,T) is characterized by

H(s,t) = P(S s, T t) = s KC(t)

where KC(t) = t – (t)/ ’(t).

Simulating Bivariate CopulasSimulating Bivariate Copulas

Algorithm for generating bivariate Archimedean copulas (refer Embrecht et al (2001):

Simulate two independent U(0,1) random variables, s and w.

Set t = KC-1

(w) where KC(t) = t – (t)/ ’(t).

Set u1 = -1(s (t)) and u2 = -1((1-s) (t)).

x1 = F1-1(u1) and x2 = F2

-1(u2) if inverses exist. (F1 and F2 are the marginals).

Theorem for Multi-dimensional Theorem for Multi-dimensional Archimedean Copulas (1)Archimedean Copulas (1)

Let (U1,…,Un)’ be an n-dimensional random vector with uniform marginals and joint distribution function defined by the Archimedean copula

C(u1,…,un) = -1((u1) + … + (un)) or some generator .

Define the n tranformed random variables S1,…,Sn-1 and T, where

Sk = ((u1) + … + (uk)) / ((u1) + … + (uk+1))

T = C(u1,…un) = -1((u1) + … + (un))

Theorem for Multi-dimensional Theorem for Multi-dimensional Archimedean Copulas (2)Archimedean Copulas (2)

The joint density distribution for S1,…,Sn-1 and T can be defined as follows.

h(s1,s2,…,sn,t) = |J| c(u1,…un)

or

h(s1,s2,…,sn-1,t) = s10s2

1s32…. sn-1

n-2 -1(n)(t)[(t)] /’(t)

Hence S1,…,Sn-1 and T are independent, and

1. S1and T are uniform; and

2. S2,…,Sn-1 each have support in (0,1).

Theorem for Multi-dimensional Theorem for Multi-dimensional Archimedean Copulas (3)Archimedean Copulas (3)

Distribution functions for Sk:

Corollary: The density for Sk for k = 1,2,…n-1 is given by

fSk(s) = ksk-1, for s (0,1)

The distribution functions for Sk can be written as:

FSk(s) = sk , for s (0,1)

Corollary: The marginal density for T is given by:

fT(t) = -1(n)(t)[(t)]n-1 ’(t) for t (0,1)

Algorithm for simulating multi-Algorithm for simulating multi-dimensional Archimedean Copulasdimensional Archimedean Copulas

1. Simulate n independent U(0,1) random variables, w1,…wn.

2. For k = 1,2,…, n-1, set sk=wk1/k

3. Set t = FT-1

(wn)

4. Set u1 = -1(s1…sn-1(t)), un = -1((1-sn-1) (t)) and for k = 2,…,n , uk = -1((1-sk-1)sj(t).

5. xk = Fk-1(uk) for k = 1,…,n.

Example: Multivariate Gumbel Example: Multivariate Gumbel CopulaCopula

Gumbel Copulas (u) = (-log(u))1/

-1(u) = exp(-u)

-1(k) = (-1)k exp(-u)u-(k+1)/ k-1(u)

k (x) = [(x-1) + k] k-1 (x) - ’k-1 (x) Recursive with 0 (x) = 1.

Example: Gumbel Copula (Kendall Example: Gumbel Copula (Kendall Tau 0.5, Theta =2)Tau 0.5, Theta =2)

Example: Gumbel Copula (3)Example: Gumbel Copula (3)

Normal vs Lognormal vs Gamma

Application:Application:VaR and TailVaR (1)VaR and TailVaR (1)

Insurance portfolio– Contains multiple lines of business, with tail dependence

Copulas – Gumbel copula – distributions have heavy right tails– Frank copula – lower tail dependence than Gumbel at the same

level of dependence Economic Capital: VaR/TailVaR

– VaR: the k-th percentile of the total loss– TailVaR: the conditional expectation of the total loss at a given

level of VaR (or E(X| X VaR))

Application: VaR and TailVaR (2)Application: VaR and TailVaR (2)

Density of Gumbel Copulas

Density of Frank Copulas

Application: VaR and TailVaR (3)Application: VaR and TailVaR (3)

Assumptions:– Lines of business: 4– Kendall’s tau = 0.5 (linear correlation = 0.7)– theta = 2 for Gumbel copula– theta = 5.75 for Frank copula

Mean and variance of marginals are the same

Application: VaR and TailVaR (4)Application: VaR and TailVaR (4)

Frank Gumbel

Application: VaR and TailVaR (5)Application: VaR and TailVaR (5)

Gumbel copula has higher TailVaR’s than Frank copula for Lognormal and Gamma marginals

Lognormal has the highest TailVaR and VaR at both 95% and 99% confidence level.

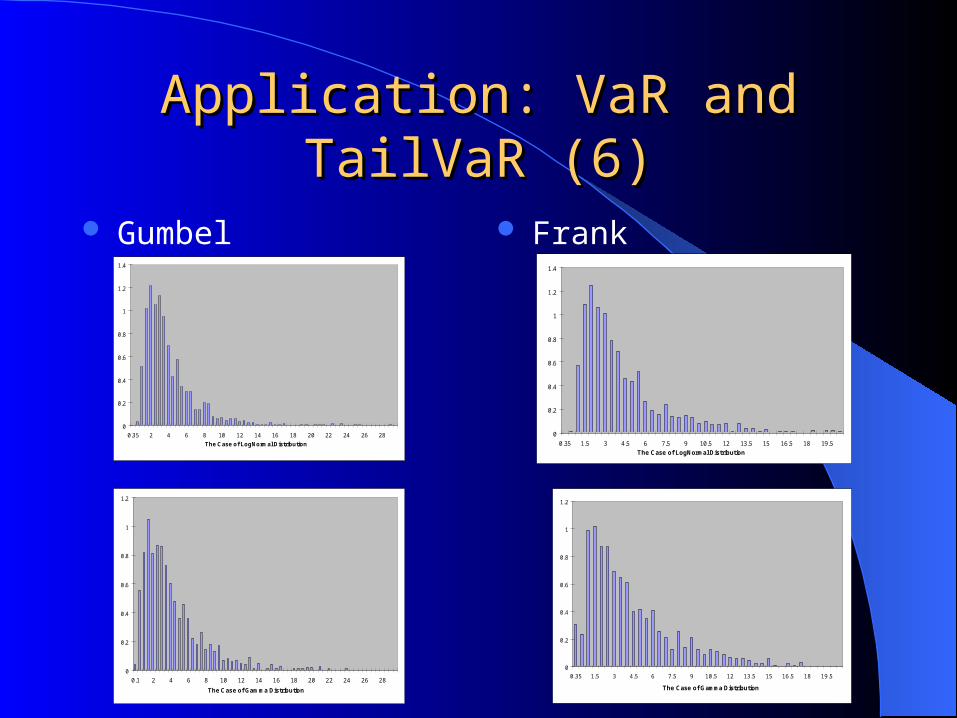

Application: VaR and TailVaR (6)Application: VaR and TailVaR (6)

Gumbel Frank

The Case of LogNormal Distribution

0

0.2

0.4

0.6

0.8

1

1.2

1.4

0.35 2 4 6 8 10 12 14 16 18 20 22 24 26 28

The Case of Gamma Distribution

0

0.2

0.4

0.6

0.8

1

1.2

0.1 2 4 6 8 10 12 14 16 18 20 22 24 26 28

The Case of LogNormal Distribution

0

0.2

0.4

0.6

0.8

1

1.2

1.4

0.35 1.5 3 4.5 6 7.5 9 10.5 12 13.5 15 16.5 18 19.5

The Case of Gamma Distribution

0

0.2

0.4

0.6

0.8

1

1.2

0.35 1.5 3 4.5 6 7.5 9 10.5 12 13.5 15 16.5 18 19.5

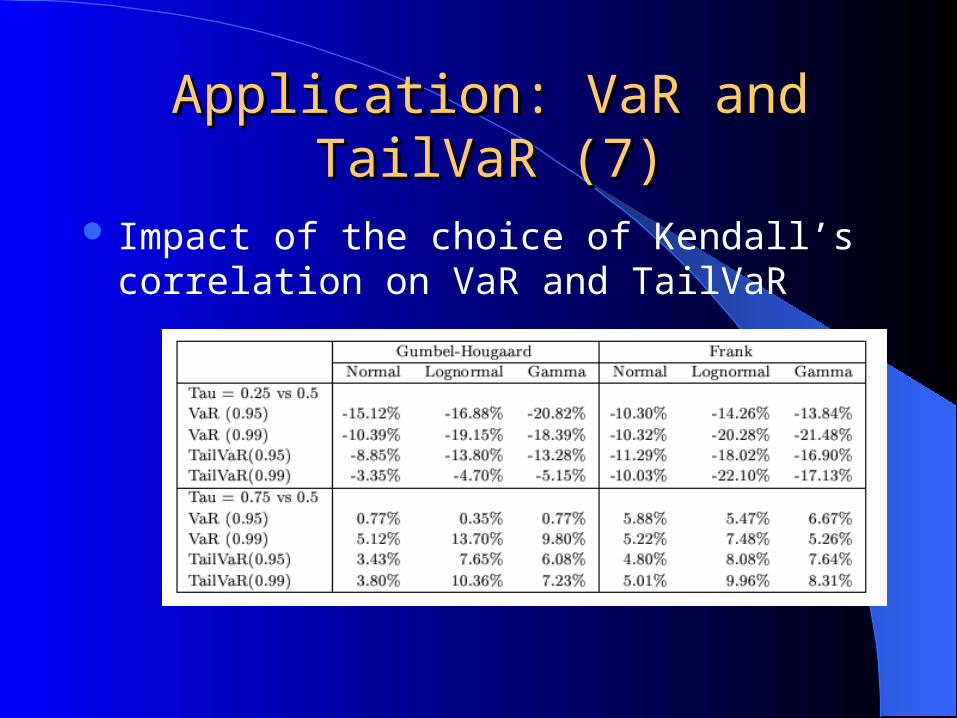

Application: VaR and TailVaR (7)Application: VaR and TailVaR (7)

Impact of the choice of Kendall’s correlation on VaR and TailVaR

ConclusionConclusion

Derived an algorithm for simulating multidimensional Archimedean copula.

Applied the algorithm to assess risk measures for marginals and copulas often used in insurance risk models.

Copula and marginals have a significant effect on economic capital