shelter afrique financing affordable housing for africa ... · shelter afrique financing affordable...

TRANSCRIPT

Shelter Afrique Financing Affordable Housing For Africa AUHF Durban 2015

Kevin Kihara Head of Strategy October 26th 2015

2 |

Focus on Affordability

Contents

“The Purpose”

“What We Do”

Supporting Housing

The State of Housing in Africa

Our Products

Our Projects and Investment Thesis

Our Performance

3 |

There is a tremendous need for affordable housing across the continent that resonates with SHAF’s founding mandate, its purpose and capability

… and serves as the raison d'être for the creation of SHAF ▪ Article 4 of SHAF’s charter states that its

purpose is to “promote financing in housing and urban development”, via: – Mobilization of capital – Equity participation – Joint ventures – Raising funds variable equity – Research – Any other relevant activities

The dire need for affordable housing across the continent is colossal…

The number of persons moving into African cities every 24 hours

The Housing deficit in Nigeria per annum

Africa’s population expected to double between now and 2050

Percentage of the urban population living in informal settlements across Sub Saharan Africa

Source: World Bank; IFC; UN Habitat Picture: Kibera: the largest informal settlement in Nairobi, Kenya

4 |

Housing Deficits are Skyrocketing: Projections to 2030 in Nairobi

SOURCE: Team analysis

5 |

SHAF’s Vision Is Grounded In A Few Core Principles-Relevance and Impact

Maximise the impact of your funds

▪ Funds disbursed by SHAF significantly increase supply and/or generate IMPACT in the affordable housing market (e.g., through new technologies, job creation): – SHAF targets segments of the value chain that will

have a meaningful impact on housing provision – SHAF provides sufficient oversight to ensure

investments are executed as planned and translate into quality affordable housing

Focus on affordable housing

▪ SHAF invests when there is a RELEVANCE between the investment and the development of affordable housing at scale

Attract additional funding

▪ SHAF seeks to “CROWD-IN” other funds: from governments, other DFIs and the private sector- to maximize the impact of its investments

SOURCE: Team analysis

6 |

SHAF’s vision is to become a relevant leader with impact in affordable housing across Africa

SOURCE: Team analysis

Expert on best practice government policies and processes to support affordable housing

“Go-to Lender” for affordable housing projects and investor in projects with significant social impact

Expert in innovative private-public partnerships (PPPs) to unlock and develop land

Knowledge repository for new and innovative technologies to reduce costs of housing

7 |

Realizing this vision requires addressing a number of Africa’s affordable housing challenges

Problem 1: ▪ Low cost projects often

do not attract buyers due to the lack of a mortgage market

Solution: ▪ SHAF provides

banks with LoCs and a pipeline of quality projects

OUR ROLE

Problem 2: ▪ Local governments

lack supportive housing policy and have bureaucratic processes

Solution: ▪ SHAF acts as

policy advocate to provide research on successful policies and standardized processes

Problem 3: ▪ New, potentially cost-reducing technologies

are not used because they are unproven Solution: ▪ SHAF actively pilots new technologies

in its projects

Problem 5: ▪ Idle government land is not being

used for housing Solution: ▪ SHAF orchestrates PPPs to unlock

land and bring in quality developers

Government Policy

Demand Supply

Finance

Problem 4: ▪ Developers lack

knowledge of criteria for successful affordable housing

Solution: ▪ SHAF educates

developers on guidelines for affordable housing best practices (e.g., locations, materials)

SOURCE: Team analysis

8 |

By playing this multifaceted role, SHAF intends to have a significant impact across the continent over the next 5 years

SOURCE: Team analysis

~$1bn in 2020

Grow Portfolio to

~45K Affordable

homes

Build

~30K Mortgages

Provide

~30K jobs

Create

100 Direct Loans to developers

Disburse

50 Lines of Credit

to banks

Disburse

For 100+ Housing projects

across Africa

Act as a catalyst

9 |

Focus on Affordability

Contents

“The Purpose”

“What We Do”

Supporting Housing

The State of Housing in Africa

Our Products

Our Projects and Investment Thesis

Our Performance

10 |

%, 100%=USD 285M

SHAF assets by product type SHAF Net Loans and Advances

USD M

SHAF has grown its portfolio 25% annually, with a current book of $285M, split ~50/50 between project finance and lines of credit

SOURCE: SHAF Finance; Annual Report

285

217195

145

10189

+25% p.a.

2015 YTD

14 13 12 11 2010

2

51 47

Project Finance Debt

JVs & Equity nvestments

LoCs

11 |

SHAF currently has ~80 loans across 21 countries with need for additional capital across the Board

SOURCE: Annual report; SHAF finance

No. of loans

Share capital in SHAF, % of total

Share of outstanding loans, %, 100% = $247m

111112222345567

1013

1518

Cameroon

~0 Benin Burundi Gambia

~0

Malawi

Mauritania

DRC Nigeria

Mozambique Zambia

Togo

Uganda

Senegal Cote d’Ivoire

Madagascar

Mali

Kenya

Ghana Tanzania

Rwanda Zimbabwe

101

4011223

1

41

1211

101

01124

7 6 6 2 4 4 6 4 1 2 2 2 2 3 2 1 2 1 1 1

12 |

Value of Investment, USD M

SHAF currently has 7 equity investments worth a total of ~USD 12M with intentions to grow this 10 fold in the next 5 years

SOURCE: SHAF Annual Report

3.0

3.02

0.9

1.0

1.3

1.4

1.5

Joint Venture Equity Investment Committed, not yet disbursed

XX%

Equity Share

1 SHAF committed USD 5M to PAHF but as of yet has only disbursed USD 1.3M 2 Expected to increase to USD 5M

Banque de L’Habitat du Burkina Faso (BHBF)

Pan African Housing Fund (PAHF)1

Everest Park Project Joint Venture

Caisse Régionale de Refinancement Hypothécaire(CRRH)

Tanzania Mortgage Refinance Company (TMRC)

Rugarama, City of Kigali

▪ BHBF is a USD 9M bank created to support the development of the housing and mortgage sectors

▪ A 50/50 5-year JV with Everest Limited to develop, construct and sell property on a site in Nairobi, Kenya

▪ The Pan African Housing Fund (PAHF) is a ~USD 42M private equity fund to promote housing in Africa

Description

▪ CRRH is a USD 8.3M regional mortgage-refinancing fund in Togo to support long-term loans by mortgage lenders

▪ TMRC is a USD 6.5M Mortgage Liquidity Facility to make loans more affordable in Tanzania

▪ A PPP JV with Development Bank of Rwanda to develop 2,700 affordable housing units

50%

15%

12%

11%

15%

50%

Nigeria Mortgage Refinance Company (NMRC)

▪ NMRC is a ~USD 300M wholesale financial institution to refinance mortgages in Nigeria <15%

Total 12.1

SHAF is also in negotiations in a number of additional projects e.g., Bukerere (Uganda), Lafarge (Nigeria), Shauri Moyo (Kenya)

13 | SOURCE: Team analysis

To achieve this Competitive Advantage, SHAF is seeking to establish local presence through offices with a regional mandate across Africa

Phase 1: 2016-2017

Cement presence in Nigeria, deploy 2 regional country representatives (RCRs) for Francophone (Cote d’Ivoire) and Southern Africa (Zambia)

North Africa

East Africa

Southern Africa

West Africa

2016

2 RCRs

How it would work

▪ In initial phase a “skeleton team” of 1-2 individuals would be based in-country with a regional mandate to understand the market and develop a SHAF presence

▪ They would be responsible to develop an “affordable housing toolkit” with key information on the housing sector to understand the needs of the industry and inform the country-specific product offering

▪ SHAF could continue to expand its local presence through additional RCRs once it has solidified its presence in these initial countries

Phase 2: 2018-2020

Once sufficient pipeline and deal flow is established, build the Francophone and Southern Africa offices

North Africa

East Africa

Southern Africa

West Africa

Central Africa Central Africa

14 |

Cote d'Ivoire

Nigeria

Kenya Democratic Republic of the Congo

Zambia

SHAF has looked across a number of deep dive countries to better understand the challenges to affordable housing

Key Affordable Housing issues: ▪ Expensive land near economic

activity ▪ Underdeveloped financial market

Zambia

Nigeria

Key Affordable Housing issues: ▪ Onerous long lease

processes ▪ Cost of land in city can

be ~3x above average ▪ Underdeveloped

mortgage market

Kenya Key Affordable Housing issues: ▪ Expensive financing ▪ Expensive land near

economic activity and social infrastructure

Democratic Republic of Congo

Cote d'Ivoire Key Affordable Housing issues: ▪ Short tenors in financing ▪ Limited government

capacity to execute affordable housing goals

Key Affordable Housing issues: ▪ Limited legal framework ▪ Underdeveloped

financial market

SOURCE: CAHF; World Bank; Interviews

15 |

Focus on Affordability

Contents

“The Purpose”

“What We Do”

Supporting Housing

The State of Housing in Africa

Our Products

Our Projects

Our Performance

16 |

Today SHAF offers a spectrum of potential products to address the challenges present across its member states

“Enabler” “Implementer”

6 Market Development: Products focused on convening and influencing stakeholders ▪ Urban Planning/Development Research ▪ Policy advocacy ▪ Developer education/ Open houses ▪ Hosting conferences

Description ▪ Provides full service turnkey operations in affordable housing – from developing the strategy through to execution

▪ Provides equity, either directly or through a partner, to fund innovative projects

▪ Provider of lines of credit to local banks to support affordable housing mortgage and developer financing

▪ Provides loans and advisory services to developers to grow developer financing of quality projects

▪ Orchestrate innovative transactions involving governments and developers to unlock land

▪ Project Developers ▪ Private Equity Funds ▪ O&M Companies

Target Clients

▪ Government agencies ▪ Local Banks ▪ Mortgage institutions

▪ Project Developers ▪ National Governments

▪ Cities ▪ Project Developers

Sample Customers

▪ City of Antananarivo (Madagascar)

▪ Pan-African Housing Fund

▪ Heritage Bank (Nigeria)

▪ Oakpark Developers (Kenya)

▪ City of Lusaka (Zambia)

Affordable Housing Partnership

Equity Investment

Focused Financial Intermediation

Value-Added Direct Loans

Orchestration of Innovative PPPs

1 2 4 3 5

17 |

Two Key Products: Lines of Credit and Project Finance Loans FOCUSED FINANCIAL INTERMEDIATION

Product Description

▪ Lines of credit (LoC) to banks targeting affordable housing mortgage and project finance, with the objective of: – Reducing the cost of finance to end users

and developers – Increase the tenor of loans available in the

market ▪ Value added services to further enhance

market development – Technical assistance to banks to set up or

improve mortgage lending products (e.g.., providing uniform underwriting standards)

– Providing banks with a pipeline of quality projects for mortgage lending and developer finance

Lines of Credit

▪ Project finance loans to developers for affordable housing projects which will – Reduce finance to developers

– Increase payback period ▪ Value added services to optimize

marketability of projects for affordable segment

– Market specific guidance on how to improve the affordability (e.g.., location of affordable land, quality contractors)

– Introduction of new technologies to reduce costs (e.g.., construction materials processes)

Product Description

Project Finance

18 |

Going Forward Shelter Afrique is Focusing 3 Key Enablers to Reach Its Full Potential and To Be The Driver of the Housing Agenda in Africa

▪ SHAF is presently making a number of organizational changes, including: – Increasing staffing levels for the larger portfolio – Developing new capabilities – Developing new roles and groups

Alignment of the organization to the “new SHAF”

C

▪ SHAF will improve its business development and financial analysis capabilities to better assess potential projects and improve asset quality

▪ SHAF will actively engage in project monitoring to ensure projects are proceeding as planned

Improving its core business development and project monitoring capabilities

B

Increasing its capital base

▪ SHAF will seek to attract significantly more capital, both debt and equity, to fund future growth

▪ The Engagement with our member states, the AUHF and its members is important to this effort

A

SOURCE: Team analysis; Interviews

19 |

Focus on Affordability

Contents

“The Purpose”

“What We Do”

Supporting Housing

The State of Housing in Africa

Our Products

Our Projects and Our Investment Thesis

Our Performance

Sebel Invest, Dakar, Senegal

Everest Park, Mombasa Road, Nairobi Kenya

Komarock 5A, Eastlands, Nairobi

Komarock 5A- Solar Street Light and Solar Powered Boundary Electric Fencing

Devinco Apartments Kinshasa, Democratic Republic of Congo

Rehoboth Properties, Accra Ghana

Karibu Homes-Athi River Nairobi

Karibu Homes-Athi River Nairobi

Karibu Homes-Athi River Nairobi

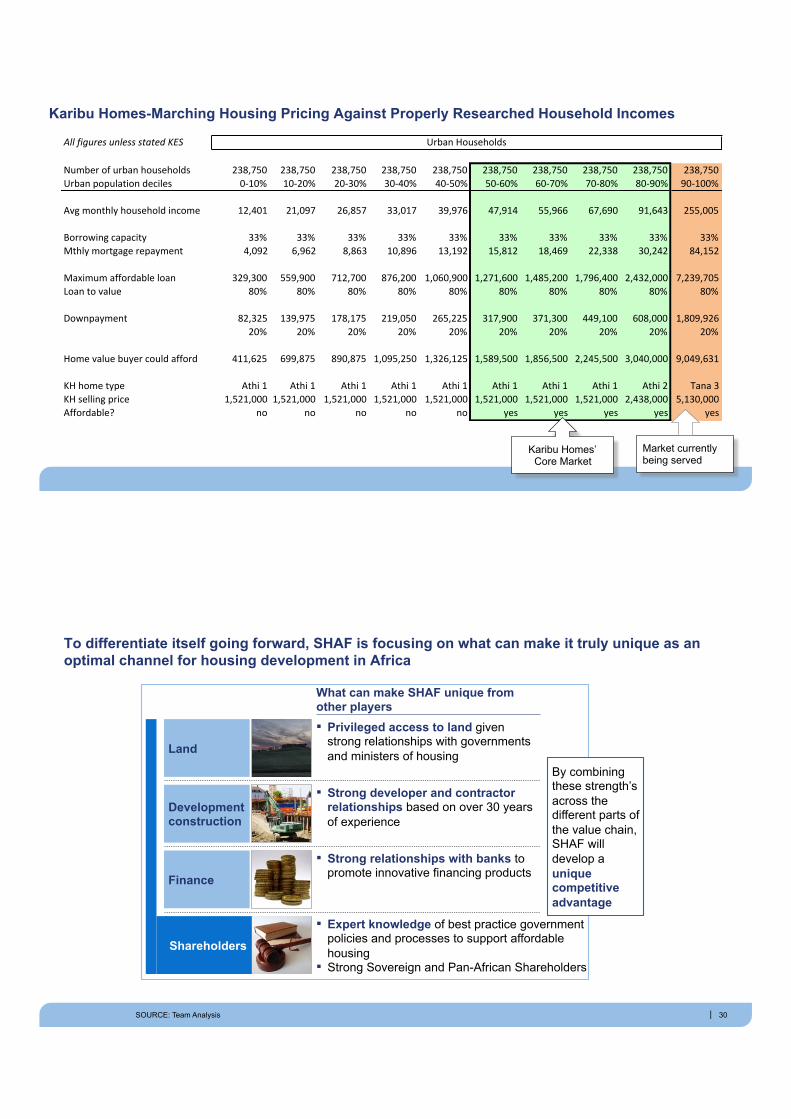

Karibu Homes-Marching Housing Pricing Against Properly Researched Household Incomes

All#figures#unless#stated#KES

Number'of'urban'households 238,750 238,750 238,750 238,750 238,750 238,750 238,750 238,750 238,750 238,750Urban'population'deciles 0<10% 10<20% 20<30% 30<40% 40<50% 50<60% 60<70% 70<80% 80<90% 90<100%

Avg'monthly'household'income 12,401 21,097 26,857 33,017 39,976 47,914 55,966 67,690 91,643 255,005

Borrowing'capacity 33% 33% 33% 33% 33% 33% 33% 33% 33% 33%Mthly'mortgage'repayment 4,092 6,962 8,863 10,896 13,192 15,812 18,469 22,338 30,242 84,152

Urban'Households

Maximum'affordable'loan 329,300 559,900 712,700 876,200 1,060,900 1,271,600 1,485,200 1,796,400 2,432,000 7,239,705Loan'to'value 80% 80% 80% 80% 80% 80% 80% 80% 80% 80%

Downpayment 82,325 139,975 178,175 219,050 265,225 317,900 371,300 449,100 608,000 1,809,92620% 20% 20% 20% 20% 20% 20% 20% 20% 20%

Home'value'buyer'could'afford 411,625 699,875 890,875 1,095,250 1,326,125 1,589,500 1,856,500 2,245,500 3,040,000 9,049,631

KH'home'type Athi'1 Athi'1 Athi'1 Athi'1 Athi'1 Athi'1 Athi'1 Athi'1 Athi'2 Tana'3KH'selling'price 1,521,000 1,521,000 1,521,000 1,521,000 1,521,000 1,521,000 1,521,000 1,521,000 2,438,000 5,130,000Affordable? no no no no no yes yes yes yes yes

Karibu Homes’ Core Market

Market currently being served

30 |

To differentiate itself going forward, SHAF is focusing on what can make it truly unique as an optimal channel for housing development in Africa

SOURCE: Team Analysis

By combining these strength’s across the different parts of the value chain, SHAF will develop a unique competitive advantage

What can make SHAF unique from other players

▪ Privileged access to land given strong relationships with governments and ministers of housing Land

▪ Strong developer and contractor relationships based on over 30 years of experience

Development construction

▪ Strong relationships with banks to promote innovative financing products Finance

▪ Expert knowledge of best practice government policies and processes to support affordable housing ▪ Strong Sovereign and Pan-African Shareholders

Shareholders

31 |

In the next 5 years Shelter Afrique will establish a Market Development group that assist the AUHF and its members

AU

OUR ROLE

Technical advisory

Examples Description

Research specialist

▪ Maintain database of information from internal and external research institutions e.g., CAHF and AUHF

▪ Coordinate research on affordable housing sector

External relations

▪ Host a roundtable on innovative construction materials in DRC

▪ Plan and convene events (e.g., conferences, round tables)

▪ Develop rental housing as a theme that can be interworked across SHAF publications, conferences etc.

▪ Develop SHAF communications strategy & share with regional business teams

Partnerships ▪ Partner with Lafarge to introduce

new low cost cement into its projects

▪ Manage partnerships with governments, civil society organizations and the private sector

▪ Advising the Uganda ministry of housing on how to standardize building codes

▪ Provide technical advisory to private and public sector organizations on scalable affordable housing strategies

PRODUCT DEEP DIVE: ADDITIONAL SERVICES

▪ Provide grants for technical and vocational training

▪ Manage SHAF Trust fund

AUHF and Shelter Afrique: Anchoring Affordable Housing in Africa