shareholder agreement - ستاکsetak.sharif.ir/main/wp-content/uploads/2017/07/w1-v2.4.pdf ·...

TRANSCRIPT

Shareholder Agreement

MohammadReza Farahi | 1396/2/21

About me

Seyed MohammadReza FarahiFinance Director Rahnema Ventures

Besides academic education in finance in France and Spain, he has a great

experience of valuation and investment affairs with tens of startups in

Rahnema ventures.

NoticeAll rights reserved. This document is an exclusive property of the author. No part of it may be reproduced or quoted, in any form or by any means, electronic or mechanical, without the prior written permission of the owner. Copyright © 2017. For a list of references, you can contact the author via [email protected]

/113

Index – Today’s Roadmap

Investment Concept– how VC is different from traditional investment 8:30

Shareholder agreement– basic rules and financial tools

Launch Break – let’s meet each other and talk

Design shareholder agreement– based on preferred stock

Preferred stock characteristics

10:30

12:30

13:45

16:30

3

Investment

How people manage their wealth?

/113

Investment history• Code of Hammurabi(1700 BC) provided a legal framework for investment by

codifying debtor and creditor rights.

• First venture investors: maritime expeditions were first case; navigators were the most adventurous entrepreneurs, and ship owners were first VCs.

• Why investment emerged? Because of specialization; some people have expertise without capital. Some other people have capital, but not enough time or expertise in lucrative fields

• Don’t mix speculators with value investors: value investors are seeking value in investments, and make money by rising or falling values. But speculators make money through arbitrage.

5

/113

Traditional Investment vs. VC• The main difference is between Risk & Reward

• Risk factors in ventures are:• Innovation risk

• Business model risk

• Operation and scale up risk

• +90% of Ventures have no earning for investor

• VC is a Knowledge-base investor, you need to be expert in some fields.

• So, you can help out and control management.

• Also, you are doing something unique, so it has Social impacts and personal identity

6

/113

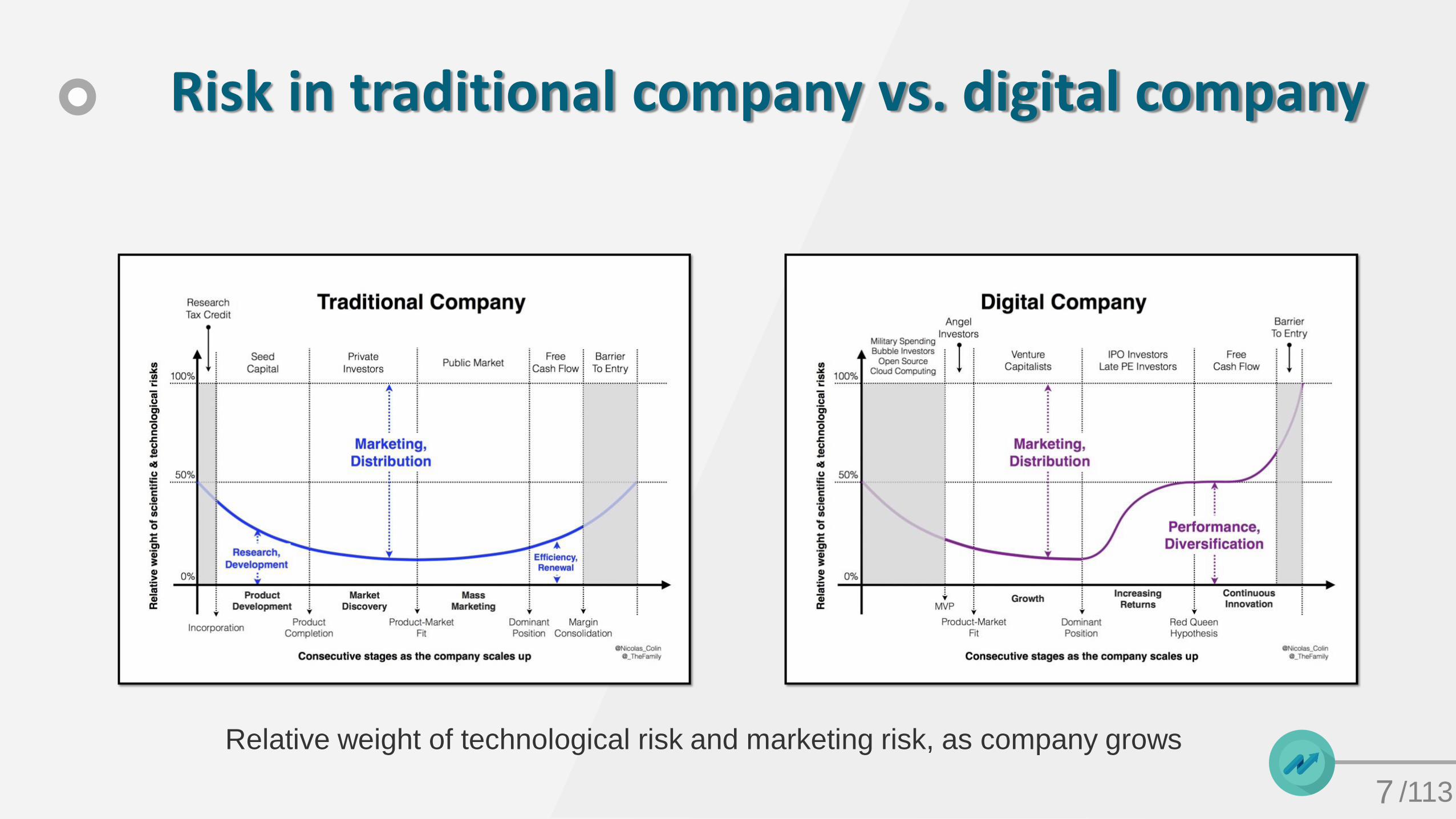

Risk in traditional company vs. digital company

7

Relative weight of technological risk and marketing risk, as company grows

/113

Why VC emerged in 20 century• In the past, Information from inside company could not effectively

communicate to outside; so investors didn’t know what they are investing in.

• It was very risky to take an equity stake in a company; Limited liability made it possible. So, investors are not liable for company default.

• Before these two, lending money was much safer than buying shares for investment.

8

/113

VC timeline

Georges Doriot (the father of venture capitalism) started First VC: ARDC(American research and development corporation) after world war II

1946

The first star: 70K$ investment in digital equipment corporation in 1957 valuedmore than 355M$ in 1968 (101% annual rate) after IPO

Small business act; licenses private companies to finance other businesses inUS and gave tax breaks to them

US labor department removed some restrictions, allowing corporate pension

funds to invest 10% of their funds in venture funds, providing a major source of

capital available to VC (the industry became ~40X)

Dot-com bubble have shriveled industry to about its half

1968

1958

1978

2003

9

/11310

/113

Upside & downside in investment• Risk means you have the possibility of losing some, or even all of your

investment.

• In investment, usually risk and return are tradeoffs. (two sides of a coin)

• Some people are risk averse, and some others are risk seeker.

• The person who refuses a fair bet is risk-averse

Example: Lets Flip a coin; which option do you choose?• You will receive 1MT without flipping coin

• Or you will receive 2MT if heads

• Which one does VC choose?

11

/113

Salesman case studyAn ordinary man with fixed 15K$ salary in a job with no certainty

• A proposal comes: a salesman commission-based job with 30K$ (upside) if works well, and 10K$ (downside) if result are not good

• probability of good and bad result in salesman mind are same, 50%

• So, will you take the proposal? Like any other answer in management, It depends.

12

/113

Salesman solutionThe utility function is: E (U) = 0.5 U (10,000) + 0.5 U (30,000)

• So, the answer depends on each person utility and attitude to risk.

• The utility for risk seeker is 60, (more than 43 in 20K$), so he takes job

• and for risk averter is 37.5 (less than 65 in 20K$), so he refuses.

13

Liquidation

When you can liquidate your investment?Simply “cash out”

/113

Liquidation and exit• Liquidation: a process by which a company is brought to an end, good or bad

• Exit: when an investor gets a return on their investment in a venture-backed startup

• Different types of exit:• Acquisition

• Acquihire

• Merger and acquisition

• IPO

• Not selling the startup

• Investors are looking for a return of 10-100 times on their original investment

15

/113

Liquidation and exit• Acquisition:

• Buyer takes over startup using cash or stock as a compensation

• Team usually stays at company for a period of time to cash out and vest their stock

• Acquihire: acquisition + hire• Buyer usually is more interested in team, than product

• Often leads to closure of products, or change the direction of product

• One example is: Waze, acquired by Google in 2013. The technology is used in Google maps for estimating traffic .

16

/113

Linkedin timeline; IPO and acquisition case

Raised 4.7 M$ in first year2003

Raised 53M$ with valuation 1b$, joining unicorn club.

Raised 22.7m$, more than 100M$ in total funding

Went public, the record market cap was +20b$ in 2015

Acquired by Microsoft with 28B$ valuation

2008

2008

2011

2016

17

/113

Number and value of M&A worldwide

18

/113

Liquidation and exit• IPO: (initial public offering): When rising more capital from VC or private

equity firm is no longer an option, let’s go for IPO

19

Num

ber

of IP

O in U

.S.

/113

Facebook timeline

Raised 500 k$ in first year2004

Refused Yahoo acquisition proposal with 1b$ valuation

Raised 200M$ with valuation 10b$, total funding exceeded 700M$

Raised 1.5b$ from Goldman sachs & DST Global

Went public, the record market cap

2006

2009

2011

2012

20

/113

Liquidation and exit• M&A

• Merging with similar or a larger company

• Often chosen by big companies looking for complimentary products.

• Not selling the company, milking the cow:• When you can establish a solid business model and revenue

• You invest your profit in your company

• part of those profits can also be distributed amongst investors as a dividend

21

Further reading: The hard thing about hard things; a real story of ups and downs

in IPO and acquisition

/113

Liquidation in Iran• Some challenges:

• There are not many large IT companies in Iran. So no one acquires your startup

• The IPO process is not well-known among startups, because success stories are few

• Interest rates are higher, so investors cant wait until you make your own profit

• Some cases of liquidation in Iran• App (*733#): went public on 1395, now market cap is around 1500BT

• Zoodfood: acquired by rocket in 2014, merged with bodofood, to accelerate partnership with restaurants

• Fidibo: acquired by digikala, to offer customers both physical book and ebook

22

Investment rounds

/113

Investment rounds• Seed investment: a preliminary investment for an idea

• Series A: when you have a strong defined idea

• Series B: when you truly established your business

• Series C and beyond: no technical limit

24

/113

Investment rounds• Seed investment

• To achieve:• Product identification

• Marketplace orientation

• Customer targeting

• Team creation

• Series A

• To achieve:• Build Distribution channels

• Pay for marketing

• Develop new markets

25

/113

Investment rounds• Series B:

• To achieve: • Team expansion

• Globalization

• Acquisitions (if needed)

• Series C and beyond:• There is no technical limit, mainly it is related to market expansion and growth rate

• Be aware of anti-dilution agreements, which prevents founders stake to water down

26

Further reading:

- infographics in funders and founders

- Company profiles in crunchbase

/11327

/11328

/113

Uber fund raising rounds• Founded in 2009

• Raised 200k$ in seed round in 2009

• Raised 1.25M$ from angels in 2010

• Raised 11M$ in series A in 2011

• Raised 37M$ in series B in 2011

• Raised 363M$ in series C in 2013

• Raised 2.6B$ in series D & E in 2015

• Raised 1.6B$ debt financing in 2015

• Raised 2B$ in series E & F in 2015

• …

• Raised 3.5B$ in series G in 2016

• …

8.8B$ in 14 rounds from 78 investors29

/113

IP rights• intellectual property protection, such as patents, can minimize competition

• Intellectual property also can attract or solidify funding and partnerships

You should:

• File early, and keep quiet

• File again as the invention evolves

• Do not wait for your patent to issue

• Consider design patents

• But, Do not rely solely on patents

30

/113

bibliography• A brief history of venture capital; https://www.financialpoise.com/a-brief-history-of-venture-

capital/

• Why venture capital thrives in digital world; https://salon.thefamily.co/low-risk-high-reward-why-venture-capital-thrives-in-the-digital-world-ed56d0b14dc

• Utility theory and attitude toward risk; http://www.economicsdiscussion.net/articles/utility-theory-and-attitude-toward-risk-explained-with-diagram/1384

• How can startups exit and investors make money; https://startupxplore.com/en/blog/exit-strategies-for-startups-and-investors/

• Startup Investment 101: Investment Rounds Explained; http://blog.onevest.com/blog/2015/4/23/startup-investment-101-investment-rounds-explained

• Intellectual property strategies for startups; https://techcrunch.com/2016/10/31/intellectual-property-strategies-for-startups/

• Silicon valley venture survey; https://www.fenwick.com/publications/Pages/Silicon-Valley-Venture-Survey---Second-Quarter-2014.aspx

31

Shareholder agreement

How to make a deal

/113

definitions• Term sheet: a non-binding agreement that sets forth the basic terms and

conditions under which an investment will be made

• Shareholder agreement:• A shareholding agreement is the final document.

• It is definitive and legally binding.

• It outlines the shareholders' rights and obligations.

• It depicts how company operates.

• SHA should be fair, and should be perceived fair, unless, the company will get locked, because founders or investors will not be interested enough to continue this hard journey.

• Shareholder agreement has different characteristics,

but before that, lets see when should we use it:

33

/113

Basic types of investor funding

investor will receive a stake in exchange for money

2Loan

3Convertible debt

a mash-up of debt & equity

1 Equity

34

you borrow money now, and pay it back later

/113

Basic types of investor funding• Equity: investor will receive a stake in exchange for money

• When to do it:• When you need a long runaway

• When you have zero collateral

• When you can’t possibly bootstrap

• When you are positioned for astronomical growth

• Things to keep in mind• Equity narrows your options: because equity investors are interested in one thing: liquidity

• Equity investors are taking big risk for big results

• Competition for getting investment is very high

• It takes time: about 3-6 month

• It is a one-way street: the investor is part of your world, whether like it or not.

35

/113

Basic types of investor funding• Loan: you borrow money now, and pay it back later, with an established rate

of interest

• Important features:• Interest rate

• Repayment schedule

• Collateral

• When to do it:• When you don’t need too much

• When you need capital quickly

• When you need money for a very concrete, tangible reason

• Finally, When equity isn’t available

36

/113

Basic types of investor funding• Convertible note: you borrow money from investors with the understanding that the loan will either

be repaid or turned into a share

• How it works:

• Discount: investor receive a discount on

• Warrant

• Interest rate: for a straight rate

• Valuation cap: maximum company valuation at which investors can convert their debt into equity

• When to do it:

• When you are not ready for valuation

• When you believe your company valuation is to skyrocket

• Keep in mind:

• Investors really like it, because they have exit strategy of debt structure, and they can see how you perform and jump on equity train.

• Case study

37

/113

Convertible note case• Seed round:

• Valuation cap: 4M$

• Discount rate: 20%

• Investment: 100K$

• Series A:• 12M$ pre-money valuation

• 1M number of shares

• How many shares for convertible note holders?

• shares= 100,000/(4,000,000*0.8) * 1,000,000 = 31,250

38

/113

What do investors need in SHA?• Downside protection:

• Liquidation preference: an investor receives its investment back, prior to common investors.

• IPO conversion provision: if IPO valuation is below the certain value, the investor gets additional share.

• Anti-dilution adjustments: reduce current deal price, if valuation declines in future.

• Upside benefits:• Liquidation participation: after an investor receives its money back, the investor

then gets to participate with common shareholders in remaining.

• Super voting stock

39

/113

Google acquired Slide; case study• After sale of company, lets see how much different people made:

• Max Levchin (founder) – $39mm

• Scott Banister who also took part in the series A made $5m from the sale.

• BlueRun Ventures, who invested $8m in the series B round made $28m.

• The Founders Fund and Mayfield Fund, both investors in the series C, each made their money back.

• Fidelity Investments, part of the series D: also made their money back.

• The reason Fidelity, Founders Fund, and Mayfield got their money back is they had a liquidation preference. Otherwise they would have lost money in a transaction where the founder made $39mm

• what do you think about this deal? Was it fair?

40

/113

bibilography• Convertible notes; examples and how it works;

https://www.seedinvest.com/blog/startup-investing/how-convertible-notes-work

• The types of investor funding's; https://www.fundable.com/learn/resources/guides/investor-guide/types-of-investor-funding

• Journey from term sheet to shareholding agreement – Startup Funding; https://yourstory.com/2015/08/termsheet-to-shareholding-agreement/

41

Preferred stock

/113

Preferred stock; terminology• Preferred stock is a class of stock that provides certain rights, privileges, and

preferences to investors

• Compared to common stock, which is normally held by the founders, it is a superior security

• Preferred stock takes its name from a critical feature of preferred stock called liquidation preference• Liquidation preference means that in a sale (or liquidation) of the company, the

preferred stock holders will have the option of taking their cost out or sharing in the proceeds with the founders as common stock holders

43

/113

Preferred stock; terminology• Almost all venture capital firms and many angel and seed investors will

require the company they are investing in to issue them preferred stock• Common stocks are usually to be issued to founders & Employees through the

employee stock option program

• Preferred stocks are usually the exclusive offer for investors; but why?

• Common stock should be thought of as a vehicle for issuance in exchange for effort, or “sweat equity”

• Preferred stock has preferential rights in matters such as liquidation and board representation

• These are rights generally reserved for those who have invested cash in the business. (After all, this is a Chicago-wise economic system!)

44

/113

Preferred stock; terminology• Depending on how hard the investors have pushed for more rights and

provisions, we have different standardized and non-standardized classes of preferred stocks

• It’s not uncommon for the value of preferred-stock shares to be 10 times that of common-stock shares

• Ultimately, both types of stock are converted into common shares at the time of the Initial Public Offering

• How Frequent? Kaplan & Stromberg of Chicago Booth:

45

Further reading:

An Empirical Analysis of Venture Capital Contracts; Kaplan & Stromberg

/113

Rationale motives behind the scene• As usual, it’s all about “conflict of interests”…

• Founders want to build a company, keep control and earn a fair share of any windfall

• Investors want to profit from your company as much as possible, minimizetheir financial risk and, often, gain the operating control needed to do so

• Balancing these interests is a delicate process that requires a clear-eyed understanding of the terms involved during negotiations…

46

/113

ingredients• Let’s be clear: We, investors, are nothing more than a chef!

• In this case, our ingredients are different rights, legal concepts, contingencies, etc.

• Our cooked meal is the particular type of the preferred stock that we manage to achieve, among many classes: Ashe-Sholeh-Ghalamkaar!

47

/113

Many ingredients

• Conditions Precedent to Financing

• Information Rights

• Board Control

• Dividend Rights

• Blocking Rights

• Pro-rata Rights

• Registration Rights

• Restriction on Sales

• Right of First Refusal

48

• Participating vs. Non-participating Preferred Stock

• Vesting

• Drag Along

• No-Shop-Agreement (Unilateral or Serial Monogamy)

• Indemnification

• IPO Shares Purchase

• Pay-to-Play

• Option Pool

• Liquidation Preferences

• Anti-Dilution Provisions

/113

bibilography• “Differences Between Common and Preferred Stock”, AllBusiness Networks

http://goo.gl/QUuQr8

• “Everything You Ever Wanted To Know About Convertible Note Seed Financings”, Scott Edward Walker, TechCrunch

http://goo.gl/GYKlsh

• “I Just Heard Some Startling Things About Uber”, Henry Blodget, BusinessInsider

http://goo.gl/kKl7QD

• “Convertible note agreement templatenths”, PandaDoc

https://goo.gl/eFILSx

49

Liquidation preference

/113

Liquidation Preference• Certain multiple of the original investment per share is returned to the

investor before the common stock receives any consideration.

• For many years, a “1x” liquidation preference was the standard. Starting in2001, investors often increased this multiple, sometimes as high as 10x!(Note: that it is mostly back to near 1x nowadays)

• What is the typical legal language of communicating this?

51

In the event of any liquidation or winding up of the Company, the holders of the Series A

Preferred shall be entitled to receive in preference to the holders of the Common Stock a per

share amount equal to [x] the Original Purchase Price plus any declared but unpaid dividends.

/113

Liquidation Preference• In my opinion, after price, liquidation preferences are the second most

important “financially legalized term”

• The liquidation preference determines how the pie is shared on a liquidityevent

• There are two components that make up what most people call theliquidation preference: the actual preference and participation

• Multiple of the Original Purchase Price (the [X]): If the participation multipleis 3 (three times the Original Purchase Price), it would mean that thepreferred would stop participation (on a per share basis) once 300% of itsoriginal purchase price was returned including any amounts paid out on theliquidation preference.

52

/113

Participating vs. Non-participating• Remember: Preferred stock owners often get a 1x liquidation preference; in

the event of a sale or bankruptcy, they get their money back before common stock holders get a chance to recoup anything

• Now Consider this Scenario:• The company realizes a more successful exit

• Therefore, common stock holders are left with equity worth 4x what preferredstock owners paid per share at the time of their investment

• Preferred stock owners can still exercise their liquidation preference to get theirmoney back, but…

• If everyone else is making four times that money, it makes more sense toconvert those preferred shares into common stock to enjoy the 4x gains

53

During successful outcomes, preferred stock owners are essentially forced to

convert to common stock.

/113

Participating vs. Non-participating• For non-participating stockholders, this is where it ends; they convert their

shares to common stock and enjoy the same 4x returns as everyone else: Simple enough!

• Participating preferred stock, however, allows venture investors to double dip in the company’s gains• They get to exercise both their liquidation preference and enjoy a pro-rata

share of common stock gains simultaneously

• So, if a participating stockholder owns 25% of the company at the time of a liquidation event, they get their money back plus 25% of the remaining proceeds.

54

/113

exampleAt T=1, my company worth 2.5 million dollars

• So, what is your ownership share from my company? Simply 50%

• You agree to invest $2.5M in my company, making my valuation jump to $5M

• At T=2, I sell my almost-successful company at $10M

• Now What happens if I’d given you at first place:• Participating Preferred Stock

• Non-Participating Preferred Stock

55

/113

solution• Non-Participating shares: You are legally obligated to convert those 50%

shares to common stock, leaving you with $5 million. Simple and fair, right?

• Participating Shares: A significant change of result!• First you can exercise their 1x liquidation preference, leaving you with $2.5M.

(Conceptually, getting your money back)

• But it doesn’t end there. In addition to that $2,5M, you are entitled to a 50% share of the remaining $7.5 million: You get another $3.75 million.

• This leaves you with $6.25 million. So, you capture most of the exit’s value even though we, both, own half of the company equally.

• So, this $6.25M is as if I owned X% of the company under participating

• So, adding a “non”, costed me 12.5% of my company; such a looser I am!

56

/113

Tree types, not two• Let’s make it a bit more complicated: There are three varieties of

participation:• Full participation (Investor-Friendly): sharing the liquidation proceeds on a pro

rata basis after payment of liquidation preference. (Same as our example)

57

After the payment of the Liquidation Preference to the holders of the Series A Preferred,

the remaining assets shall be distributed ratably to the holders of the Common Stock and the

Series A Preferred on a common equivalent basis.

/113

• Capped participation (Moderate): Capped participation indicates that the stock will share in the liquidation proceeds on a pro rata basis until a certain multiple return is reached

58

After the payment of the Liquidation Preference to the holders of the Series A Preferred,

remaining assets shall be distributed ratably to the holders of the Common Stock and the

Series A Preferred on a common equivalent basis; provided that the holders of Series A

Preferred will stop participating once they have received a total liquidation amount per share

equal to [X] times the Original Purchase Price, plus any declared but unpaid dividends.

Thereafter, the remaining assets shall be distributed ratably to the holders of Common Stock.

Drag along

/113

Intro• Why? As transactions starts occurring that are at or below the preferred

liquidation preferences, entrepreneurs and founders – not surprisingly –start to resist doing these transactions since they often aren’t gettinganything in the deal

• This is a very key provision for consideration by both founders andinvestors, hence it should be carefully reviewed

• There are several mechanisms to address sharing consideration below theliquidation preferences; e.g. the “carve out” – which we’ll talk moreextensively about later on

60

/113

Intro• The fundamental issue is that if a transaction occurs below the liquidation

preferences, it’s likely that some or all of the VCs are losing money on thetransaction

• VCs would much rather control their ability to compel other shareholders tosupport the transaction being considered

• As more of these situations appear, the major holders of common stock(even if they are in the minority of ownership) begin refusing to vote for theproposed transaction unless the holders of preferred, waive part of theirliquidation preferences in favor of the common

• Needless to say, this “hold out technique” did not go over well in theventure community and, as a result, the drag-along became more prevalent

61

/113

Intro• The VC point of view on this varies widely and is often dependent on the

situation• Some VCs can deal with this and are happy to provide some consideration to

management to get a deal done

• Others are stubborn in their view that since they lost money, managementshouldn’t receive anything

• A “drag-along” provision requires the founders and certain otherstockholders to enter into an agreement with the venture capital investorthat will allow the investor (perhaps acting with certain other stockholders)to force a sale of the company if certain conditions are satisfied

62

/113

Is it fair

• Most founders and early shareholders say that “it’s not fair – I want to be

able to vote my stock however I want to.”

• Remember that this term is one of a basket of terms that are part of an

overall negotiation associated with injecting money into your company

• There are tradeoffs in any negotiation and nothing is standard; so “fair” is an

irrelevant concept

• If you don’t like the terms, don’t do the deal!

• However, using this concept is getting more and more standard and it’s

difficult to avoid one form of drag along or another

63

/113

Main elementsThere are several important concepts we should understand with regard tothe “drag-along” provision, most important of which are the following:

• Which stockholders can elect to trigger the drag-along provision

• Whether it needs the board of directors' approval

• Types of transactions that triggers drag-along right

• Limitations on the applicability of the provision

• Potential liability of stockholders in a drag-along sale

• How the sale proceeds will be distributed

64

/113

Electing holders• When a company is faced with a drag along in a VC financing proposal, the

most common compromise position is to try to get the drag along to pertainto following the majority of the common stock, not the preferred

• This way – if you own common – you are only dragged along when a majorityof the common consents to the transaction

• This is a graceful position for a very small investor to take (e.g. I’ll play ball ifa majority of the common plays ball) and one that we should always beenwilling to take when I’ve owned common in a company; e.g. I’m not going tostand in the way of something a majority of folks that have rights equal tome want to do

65

/113

Electing holders• Of course, preferred investors can always convert some of their holding to

common to generate a majority, but this also results in a benefit to the common asit lowers the overall liquidation preference

• Typically, stockholders who can trigger the drag-along right are defined as holdersof a certain percentage of the outstanding shares of preferred stock on an as-converted basis

• Venture capital investors may commonly try to include 51% as the applicablepercentage

• For founders, this means that stockholders owning 51% or more of the preferredshares on an as-converted basis can force them to sell, even on terms that could bevery unfavorable for the founders

• This exactly happened in the In Re Trados Incorporated Shareholder Litigationcase, to be discussed later on

66

/113

Electing holders• Founders should carefully consider the definition of Electing Holders…

• They should bargain for a higher percentage for approval (e.g., 66 2/3% ofthe preferred)

• They should also attempt to require some percentage of the common stockto approve the transaction as well; e.g., 66.7% of the preferred and morethan 50% of the common

• Reminder: Preferred stockholders may be able to convert some of their stockto common in order to make sure the required common vote is achieved,although they will usually lose some or all of their liquidation preference indoing so, which benefits the common

67

/113

Board approval• Drag-along provisions could include the requirement of board approval of a

sale and founders should push for this

• Venture capital investors may resist the board approval requirement due topotential liability concerns, but they can incorporate mechanisms to protecttheir directors from claims of breach of duty

• In the 2013 Delaware Chancery Court decision, In Re Trados IncorporatedShareholder Litigation, board approval of a sale can expose the ventureinvestor-appointed directors to liability

• In that case, a merger was approved for a price that was, in effect, below thepreferred liquidation preference; i.e., the common stockholders received $0

68

/113

Board approval• The common stockholder plaintiffs claimed that the board breached its

fiduciary duties to the company and the common stockholders by approvingthe merger

• Eight years after the merger, the court ruled that the directors did not breachtheir duties because they were able to prove that the merger transactionwas “entirely fair”

• Although this case exonerated the directors, it highlights the issue that israised when the board has to approve a transaction such as a “drag along”sale

69

/113

Transactions Subject to the Drag-AlongIn the NVCA (National Venture capital Association) model term sheet, the drag-along provisioncomes into play when the Electing Holders (and the board, if applicable) haveapproved one of the following types of transactions:

• Merger or consolidation (other than one in which the company’s stockholders owna majority of the survivor or acquirer);

• Sale, lease, transfer, exclusive license, or other disposition of all or substantially allof the company’s assets

• Transaction in which 50% or more of the company’s voting power is transferred.

• this list of transactions is fairly standard and would not typically be heavilynegotiated.

• The company should also include a similar provision (and a waiver of dissenter’srights) in its stock option agreements.

70

/113

Price limitation• One of the most important aspects for founders to consider while designing

drag along provision

• A price below the preferred liquidation preference results in the commonstockholders walking away with nothing

• To avoid that result, founders might try to push for a minimum purchaseprice before the drag-along provision is triggered

• For example, the minimum purchase price could be twice the total preferredliquidation preference

• Solve the Quiz!

71

/113

Price limitation• Venture capital investors might be reluctant to agree to this! Why? Since a

transaction in which they exit the company at a price that doesn’t leavemuch or anything for the common is exactly the type of situation in whichthey would need drag-along rights

• Nevertheless, founders should carefully consider a minimum pricerequirement and seek to protect themselves from being “dragged” into asale transaction that is very unfavorable

• What do you think? What is a fair deal value here?

72

/113

Potential Stockholder Liability• When stock is sold, the sellers usually must give certain representations and

warranties to the purchaser and the seller has liability for breaches of those representations and warranties

• That liability can either be joint or several• Under joint liability, each of the stockholders would be liable for the entire amount of

any liability to the purchaser

• Under several liability, each stockholder is only liable for its pro rata share of any liability

• Drag-along provisions are often structured so that the shareholders being “dragged-along” are only required to subject themselves to several, rather than joint, liability

• Obviously, founders should insist on including it. In addition, founders should push for capping their liability at the amount of consideration they received

73

/113

How proceeds are distributed• The NVCA model term sheet conditions the drag-along rights on the

allocation of sale consideration as if it were liquidation proceeds to bedistributed under the company’s certificate of incorporation

• The certificate of incorporation, which is amended in a venture capitaltransaction to reflect the rights and preferences of the new preferred stock,will describe how the proceeds from a liquidation of the company must beallocated to the common and preferred stockholders

• This provision is also fairly standard and not generally heavily negotiated

74

/113

Case study: FilmLoopThe FilmLoop used to provide a free software enabling people andbusinesses to broadcast, find, and share digital images

• A rough timeline of what happened:

75

FilmLoop raises $5.5 million from Garage Technology Ventures (Guy Kawasaki) and Globespan Capital Partners

January 2005

FilmLoop raises $7 million from troubled venture firm ComVentures. Roland Van de Meer joins the board of directors.

FilmLoop 2.0 launches. Company and investors are optimistic about FilmLoop

May 2006

October 2006

/113

Case study: FilmLoopOn November 2006, ComVentures, under pressure from its own limitedpartners to clean up its portfolio and discard any unprofitable startups, metwith FilmLoop founders to tell them they must find a buyer by end of year

• The FilmLoop founders made it clear that they thought they had a goodchance at success and did not want to sell

• However, thanks to its ownership percentage as well as drag along rights,ComVentures could force the other investors and the company founders tosell.

• Founders, did not manage to find any fair buyer in such a short time

76

/113

Case study: FilmLoopIn December 2006, ComVentures proposed Fabrik, another one of theirportfolio companies, as the acquirer

• FilmLoop founders were not happy at all with that deal. So, they tried hardlyto find any other acquirer in the last two weeks of the year. But no success…

• Finally, Fabrik acquired FilmLoop for little more than the cash ($3 million)that FilmLoop had in its bank account

• Due to liquidation preference rights, the founders and all employees walkaway with exactly nothing’

• FilmLoop’s desktop and other software will play a part in a future Fabrikconsumer storage product. SimpleTech, also acquired by Fabrik andannounced today, will provide another piece of the product.

77

/113

Case study: FilmLoopComVentures had a significant interest in forcing a sale to Fabrik on such ashort timetable, during the holidays, when competitive bids would beimpossible to find

• The acquisition was not in the best interests of anyone except ComVentures• One day, the founders and employees of FilmLoop had a viable company with

$3 million in the bank

• The next day they had no stock, no job, and no company…

• At the very least, ComVentures should have abstained from voting on theacquisition

78

/113

Case study: FilmLoopFounders are under incredible pressure not to rock the boat when venture capitalists pullstunts like this

• Engaging in litigation means other VCs will be very hesitant to invest in them in the future

• So, for reputation purposes, founders tend to simply take their beating and walk away,hoping to start all over again with another venture and, hopefully, non-ethically challengedinvestors

• If you are a founder:• Take heed of the FilmLoop story: only do business with VCs that have a track record of holding

up their end of the implicit bargain; to stay with you during tough times as well as good

• VCs don’t have any obligation to put good money after bad, but to liquidate a viable startupsimply to help out another portfolio company is evil stuff

• Make sure you read and smartly negotiate those drag along and liquidation preference clausescarefully before signing

79

/113

conclusion• Founders, as well investors, should be aware that drag-along rights are

increasingly common and very important to consider

• They should pay very close attention to the drag along provision and shouldbe prepared to negotiate the some of the key terms discussed above,particularly those concerning who can trigger the “drag along” provision andany minimum price requirement.

80

/113

Legal text

81

“Drag-Along Agreement: The [holders of the Common Stock] or [Founders] and Series A

Preferred shall enter into a drag-along agreement whereby if a majority of the holders of

Series A Preferred agree to a sale or liquidation of the Company, the holders of the remaining

Series A Preferred and Common Stock shall consent to and raise no objections to such sale.”

Anti dilution

/113

Anti dilution• Investors may also ask for anti-dilution protection.

• This provision protects early investors from having their share of ownership reduced or diluted if subsequent investors invest in the company at a lower price.

• There are also tax advantages to having two kinds of stock. • You want the lowest price per share attributed to the common stock in order to

issue it with the least tax consequences to those who work to earn the stock.

• This distinction is important, because investors want the highest possible tax basis without paying more for the investment than its fair value. The common investors want the lowest value attributed so they don’t get stuck with a tax liability for the shares they receive.

• This is one of the key issues for employee stock-ownership programs.

83

/113

What does it mean?• Boring Definition: To place or give into the possession or discretion of some

person or authority; especially, to give to a person a legally fixed immediate right of present or future enjoyment of an authority, right, security or property

• Cool definition: Well you want me to invest in your company? What if you get bored in the middle of the road, or get to find a better job, and then leave me alone with your stupid idea and my innocent “wasted” money? What if I don’t manage to find a monster like you to rock it?

• Caution: A simple concept; a profound and unexpected implications

• Typically, stock and options vest over four years: you have to be around for four years to own all of your stock or options

84

/113

What is the logic behind• If you leave the company earlier than the four year period, the vesting

formula applies: you only get a percentage of your stock...

• So, many entrepreneurs view vesting as a way for VCs to “control them, their involvement, and their ownership in a company”

• While it can be true, is only a part of the story… Why? Is there a benefit on this for the founders themselves?

85

/113

What is the logic behind• Vesting works for the founders as well as the VCs

• These situations is quite typical under which, one or more founders don’t work out and the other founders wanted them to leave the company• If there had been no vesting provisions, the person who didn’t make it would

have walked away with all their stock

• The remaining founders would have had no differential ownership going forward

• By vesting each founder, there is a clear incentive to work your hardest and participate constructively in the team, beyond the elusive founders “moral imperative.”

• The same rule applies to employees; equity is compensation and should be earned over time, vesting is the mechanism to insure the equity is earned over time

86

/113

definition• Dilution refers to the phenomenon of a shareholder’s ownership percentage

in a company decreasing because of an increase in the number of outstanding shares

• This leaves the current shareholders with a smaller piece of the corporate pie

• Total number of outstanding shares can increase for any number of reasons, such as the issuance of new shares to raise equity capital or the exercise of stock options or warrants• Diff between Option and Warrant: Unlike a stock option, a stock warrant is

issued directly by the company. So, when a stock option is exercised, the shares usually are given by one investor to another; but when a stock warrant is exercised, the shares are not received from another investor, but directly from the company. Local dilution vs global dilution.

87

/113

Anti dilution• Dilution becomes a concern for preferred stockholders when confronted

with a “down round”: a later issuance of stock at a price that is lower than the preferred issue price

• Anti-dilution provisions protect against a down round by adjusting the price at which the preferred stock converts into common stock; keeping the investor's original ownership percentage intact

• The two common types of anti-dilution clauses are known as "full ratchet" and "weighted average"

88

/113

No Anti dilutionAs a simple example of full dilution, consider the following case:

• An investor owns 200,000 shares of company which has 1,000,000 shares outstanding. Therefore, the investor owns 20% of the company

• The price per share is $5, meaning that the investor has a $1,000,000 stake in a company valued at $5,000,000

• Now, the company enters a new round of financing and issues 1,000,000 more shares, bringing the total shares outstanding to 2,000,000

• At that same $5 per share price, the investor owns a $1,000,000 stake in a $10,000,000 company. Instantly, the investors ownership has been diluted to 10%

89

/113

Full ratchet• Simplest type of anti-dilution provision; but also most burdensome on the

common stockholders

• Can have significant negative effects on later stock issuances

• With a full ratchet provision, the conversion price of the existing preferred shares is adjusted downwards to the price at which new shares are issued in later rounds

In the last case, if the original conversion price was $5 and in a later round the conversion price is $2.50, the investor's original conversion price would adjust to $2.50

90

/113

Weighted average• Following is the calculation for a typical weighted average anti-dilution

provision presented by the NVCA’s term sheet

• CP2 = CP1 * (A+B) / (A+C)• CP2= Conversion price immediately after new issue

• CP1= Conversion price immediately before new issue

• A =Number of shares of common stock deemed outstanding immediately before new issue

• B = Total consideration received by company with respect to new issue divided by CP1

• C = Number of new shares of stock issued

91

/113

exampleLet’s suppose a company has 1,000,000 common shares outstanding and then issues 1,000,000 shares of preferred stock in a Series A offering at a purchase price of $1.00 per share

• So, the Series A stock is initially convertible into common stock at a 1:1 ratio for a conversion price of $1.00

• Next, the company conducts a Series B offering for an additional 1,000,000 new shares of stock at $0.50 per share. The new conversion price for the Series A shares will be calculated as follows:

92

/113

solutionThe weighted average provision uses the following formula to determine new conversion prices, CP2 = CP1 * (A+B) / (A+C), where the variables equal the following

• CP2 = $1.00 x (2,000,000 + $500,000) / (2,000,000 + 1,000,000) = $0.8333

• This means that each of the Series A investor’s Series A shares now converts into 1.2 shares of common (Series A original issue price/conversion ratio = $1.0 /$0.8333 = 1.2)

93

Pay to play

/113

Pay to play• What is Pay-to-Play? In such a provision, an investor must keep “paying”, i.e.

participating pro ratably in future financings, in order to keep “playing”(not have his preferred stock converted to common stock) in the company

• A company-friendly term: causes the investors “stand up” and agree to support the company during its lifecycle; if they do not, the stock they have is converted from preferred to common and they lose the associated rights

• A Pay-to-play term insures that all the investors agree in advance to the “rules of engagement” concerning participating in future financings

• Twenty years ago, a pay-to-play provision was rarely seen; but after the bubble burst in 2001, it became somehow common

95

/113

Pay to Play• Motives behind the scene: Pay-to-play provision tied to dilutive financings,

provides that only investors that participate in the dilutive financing are entitled to the benefit of the anti-dilution formula in effect

• This technique is beneficial for both for the company and for the investor group because it encourages all investors to continue to fund the company during those times when such incentive is most needed, i.e., when the company is undertaking a difficult financing

96

/113

Several versions• Full Pay-to-Play:

• Somehow unfair for investor since a particular investor may be unable to participate due to circumstances outside of its control

• This is especially applicable to funds out of money, or strategic investors or angels that do not expect to participate in subsequent rounds

• Most investors do not want to give up the liquidation preference and preferred rights other than anti-dilution protection merely because they decided not to participate in a particular dilutive financing

97

In the event of a Qualified Financing (as defined below), shares of Series A Preferred held by any

Investor which is offered the right to participate but does not participate fully in such financing by

purchasing at least its pro rata portion as calculated above under “Right of First Refusal” below will be

converted into Common Stock

/113

Several versions• Partial Pay-to-Play:

• A key issue in these versions, is the appropriate level of participation. Both full and partial Pay-to-Play clauses are written to require each investor to participate in the dilutive financing to the extent of its percentage ownership of the company

• Although this is typically the amount of the financing that current investors can purchase based on their contractual rights of first refusal, this approach may not work properly… Why?

98

If such holder participates in the next Qualified Financing but not to the full extent of its pro rata

share, then only a percentage of its Series A Preferred Stock will be converted into Common Stock

(under the same terms as in the preceding sentence), with such percentage being equal to the percent

of its pro rata contribution that it failed to contribute.]

/113

Several versions• Because the sum of the ownership percentages of the various investors will

be less than 100%, and the primary purpose of the pay to play clause is to assist the company in raising the total amount of financing which it requires

• Requiring each investor to purchase a percentage of the dilutive financing equal to its pro rata ownership among the investor group won’t quite work either… because the sum of these percentages will always be 100%, leaving no room for a potential new investor

• Board Decision: the optimal approach for the company, is to require each investor to purchase a percentage equal to its pro rata ownership among the investor group of that portion of the financing allocated to the existing investors by the board of directors of the company, with the balance of the financing (if any) being purchased by the new investors

99

/113

Several versions• Under this formula, if all of the preceding investors participate, together with

any new investors, the company will receive 100% of the funds it is seeking to raise.

• If the required percentage is higher than the percentage which such investor has a contractual right to purchase, the company must offer the investor the opportunity to purchase this greater amount in order to implement the pay to play clause

100

/113

Several versions• Shadow Preferred: Instead of merely losing anti-dilution protection with

regard to the initial dilutive financing in which the investor does not participate, the investor loses anti-dilution protection in all subsequent dilutive financings which may occur

• Mechanically, this can be accomplished by creating a “shadow” series of preferred stock identical in all respects to the original series but without any anti-dilution protection. If an investor fails to participate in a dilutive financing, all shares of preferred stock held by such investor are automatically converted into the shadow preferred

101

/113

Several versions• Pull-Up or Pull-Through: Instead of merely losing anti-dilution protection

with regard to the initial dilutive financing in which the investor does not participate, the investor loses anti-dilution protection in all subsequent dilutive financings which may occur

• Mechanically, this can be accomplished by creating a “shadow” series of preferred stock identical in all respects to the original series but without any anti-dilution protection. If an investor fails to participate in a dilutive financing, all shares of preferred stock held by such investor are automatically converted into the shadow preferred

102

/113

Pros & cons• Founders need to consider that pay-to-play provisions, although is not a rare

provision, is not typically be included in a term sheet and that they generally need to raise and appropriately discuss with the investors

• The conversation might begin like this: “We are looking for investors who are in for the long haul and will agree to support the company throughout its lifecycle.”

• If founders get push-back from the investors, they can offer to limit the pay-to-play provisions to down rounds

• In this case, reasoning is easier; investors who are not willing to support the company in the event of a hiccup should not benefit from the anti-dilution protection, particularly if it’s a full ratchet, and should lose some or all of their preferential rights

103

/113

Pros & cons• It may be unrealistic to expect angel and certain non-lead investors

(including strategic investors) to participate in future financing rounds and appropriate carve-outs should be negotiated and inserted into the term sheet

• Accordingly, pay-to-play provisions will need to contractual (i.e., outside of the Certificate of Incorporation) because each share of the same series must have the same rights, preferences and privileges as other shares of that series in the company’s charter

• From a capitalization perspective, it’s simpler to have the preferred stock automatically convert into common stock rather than a new class of shadow preferred. Also, automatic conversion into common stock obviously provides a stronger incentive to the investors to participate in a future financing round and has the added benefit of reducing the company’s “preference overhang.”

104

/113

Pros & cons• A disadvantage of the automatic conversion approach, whether into common stock or

preferred stock, is that once an investor has been converted, the pay to play provision provides no further incentive for that investor to participate in the next dilutive financing

• If the goal for the company and the lead investors is to maximize the incentive for all investors to participate in all dilutive financings, the better approach would be to provide that if an investor fails to participate in the initial dilutive financing, she receives no anti-dilution protection with regard to such financing, but in the event that she elects to participate in a subsequent dilutive financing, then she would be entitled to anti-dilution protection with regard to such subsequent financing

• Although this formula can be implemented with regard to multiple dilutive financings by creating several series of shadow preferred, each having a different conversion rate, this approach results in a very complicated capital structure for the company which can become overly cumbersome.

105

/113

Pros & cons• The pay-to-play provision impacts the economics of the deal by reducing

liquidation preferences for the non-participating investors

• It also impacts the control of the deal, as it reshuffles the future preferred shareholder base by insuring only the committed investors continue to have preferred stock and the corresponding rights

• When companies are doing well, the pay-to-play provision is often waived, as a new investor wants to take a large part of the new round

• This is a good problem for a company to have, as it typically means there is an up-round financing, existing investors can help drive company-friendly terms in the new round, and the investor syndicate increases in strength by virtue of new capital (and – presumably – another helpful co-investor) in the deal

106

/113

bibilography• What is a pay to play provision?;

http://www.startupcompanylawyer.com/2007/08/04/what-is-a-pay-to-play-provision/

• Demystifying the VC term sheet: Pay-to-play provisions, Venturebeat; https://goo.gl/VOI6zq

• VC Term Sheets – Pay To Play Provisions, Walker Corporate Law Group; https://goo.gl/f3v5Ag

• How Investors Get Burned Fast In A Downturn, Techrunch; https://goo.gl/0ajx3p

• Term Sheet: Pay-to-Play; http://feld.com/archives/2005/03/term-sheet-pay-to-play.html

107

No shop agreement

/113

No-shop agreement• no shop agreement reinforces the handshake that says “ok – let’s get a deal

done – no more fooling around looking for a better / different one.

• the entrepreneur should bound the no shop by a time period – usually 45 to 60 days

• The aim is to accelerate the deal

• Also, investors don’t like to put much time for a runaway founder.

109

/113

No shop agreement- legal text

110

“No Shop Agreement: The Company agrees to work in good faith expeditiously towards a closing. The Company and the Founders agree that they will not, directly or indirectly, (i) take any action to solicit, initiate, encourage or assist the submission of any proposal, negotiation or offer from any person or entity other than the Investors relating to the sale or issuance, of any of the capital stock of the Company or the acquisition, sale, lease, license or other disposition of the Company or any material part of the stock or assets of the Company, or (ii) enter into any discussions, negotiations or execute any agreement related to any of the foregoing, and shall notify the Investors promptly of any inquiries by any third parties in regards to the foregoing. Should both parties agree that definitive documents shall not be executed pursuant to this term sheet, then the Company shall have no further obligations under this section.”

/113

bibilography• Anti-Dilution Provision; http://www.investopedia.com/terms/a/anti-

dilutionprovision.asp

• Venture Capital Term Sheet Negotiation — Part 7: Anti-dilution Provisions; http://www.strictlybusinesslawblog.com/2014/03/08/venture-capital-term-sheet-negotiation-part-7-anti-dilution-provisions/

• Anti-Dilution Provision; http://www.investinganswers.com/financial-dictionary/businesses-corporations/anti-dilution-provision-2522

• The terms behind the unicorn valuation; https://www.fenwick.com/FenwickDocuments/The-Terms-Behind-The-Unicorn-Valuations.pdf

111

Questions?Feel free to ask!