sg cowen & co. health care conference - iis windows...

TRANSCRIPT

SG Cowen & Co. SG Cowen & Co. Health Care Health Care ConferenceConference

David C. Colby,Executive Vice President &Chief Financial OfficerMarch 6, 2006

2

Safe Harbor StatementSafe Harbor Statement

Safe Harbor Statement Under the Private Securities Litigation Reform Act of 1995:

The statements made during this presentation that are not historical facts are forward-looking statements within the meaning for the Federal securities laws, and may involve a number of risks and uncertainties.

Factors that could cause actual results to differ materially from expectations include, but are not limited to, the risks discussed in the Company’s most recent filings with the SEC, including its Annual Report on Form 10-K for the year ended December 31, 2005.

3

Basis of PresentationBasis of Presentation

• Unless otherwise indicated, results of the former WellPoint Health Networks Inc. are included for periods following November 30, 2004. Periods prior to November 30, 2004, only include results of the former Anthem, Inc.

• Unless otherwise indicated, results of the former WellChoice, Inc. (WC) are included in 2006 income statement and operating cash flow estimates, however WC results are not included in income statement and operating cash flow results for 2005 and prior. WC is included in balance sheet and membership information as of December 31, 2005, and beyond. However, WC is not included in balance sheet and membership information prior to December 31, 2005.

• Estimates for 2006 include the estimated impact of FAS123(R). However, amounts reported for 2005 and prior do not include such an impact.

• All per share amounts presented reflect the Company’s 2-for-1 stock split on May 31, 2005.

4

AgendaAgenda

• WellPoint Profile

• Superior Value Proposition

• Revenue Growth Opportunities

• 15%+ EPS Growth Target

• Investment Considerations

5

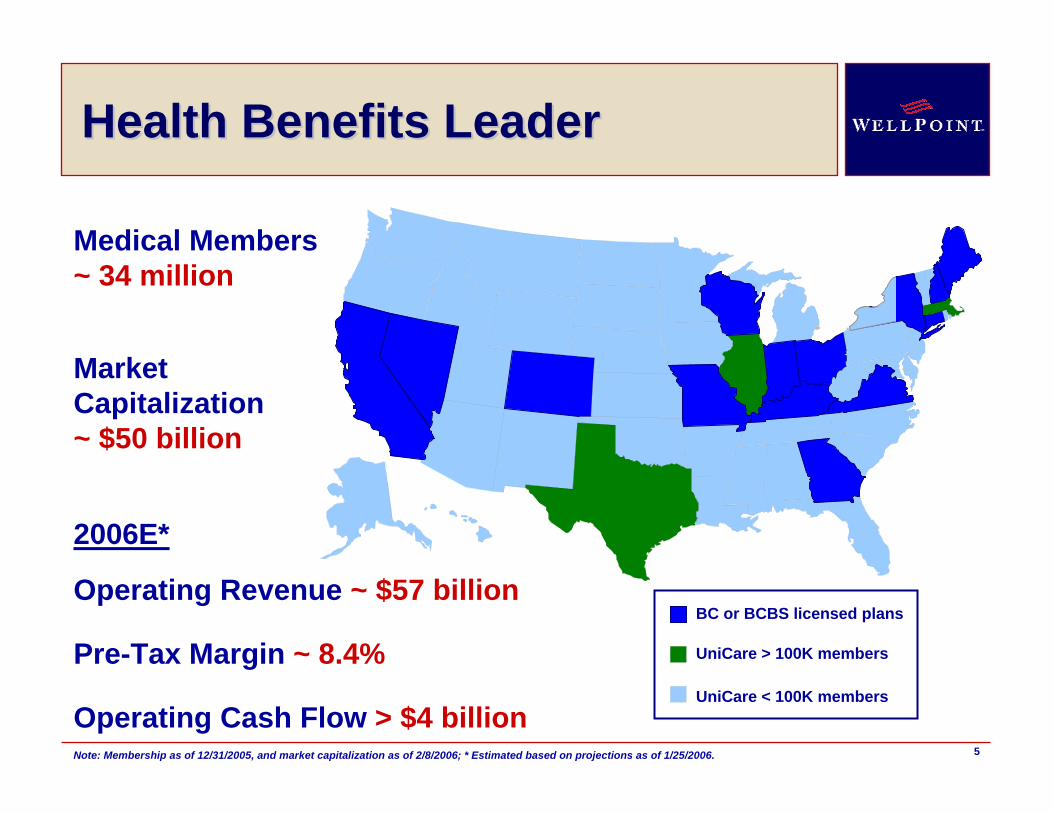

Health Benefits LeaderHealth Benefits Leader

Medical Members~ 34 million

2006E*

Operating Cash Flow > $4 billion

BC or BCBS licensed plans

UniCare > 100K members

UniCare < 100K members

Market Capitalization~ $50 billion

Pre-Tax Margin ~ 8.4%

Operating Revenue ~ $57 billion

Note: Membership as of 12/31/2005, and market capitalization as of 2/8/2006; * Estimated based on projections as of 1/25/2006.

6

Diverse Membership BaseDiverse Membership Base

Individual & Small Group

Senior1.2M

5.7M

State Sponsored1.9M

National Accounts4.8M

BlueCard3.9M

Large Group16.4M

Self-Funded~ 48%

Fully Insured~ 52%

Note: Membership data as of 12/31/2005.

No commercial customer represents more than 2% of earnings

7

Cos

t

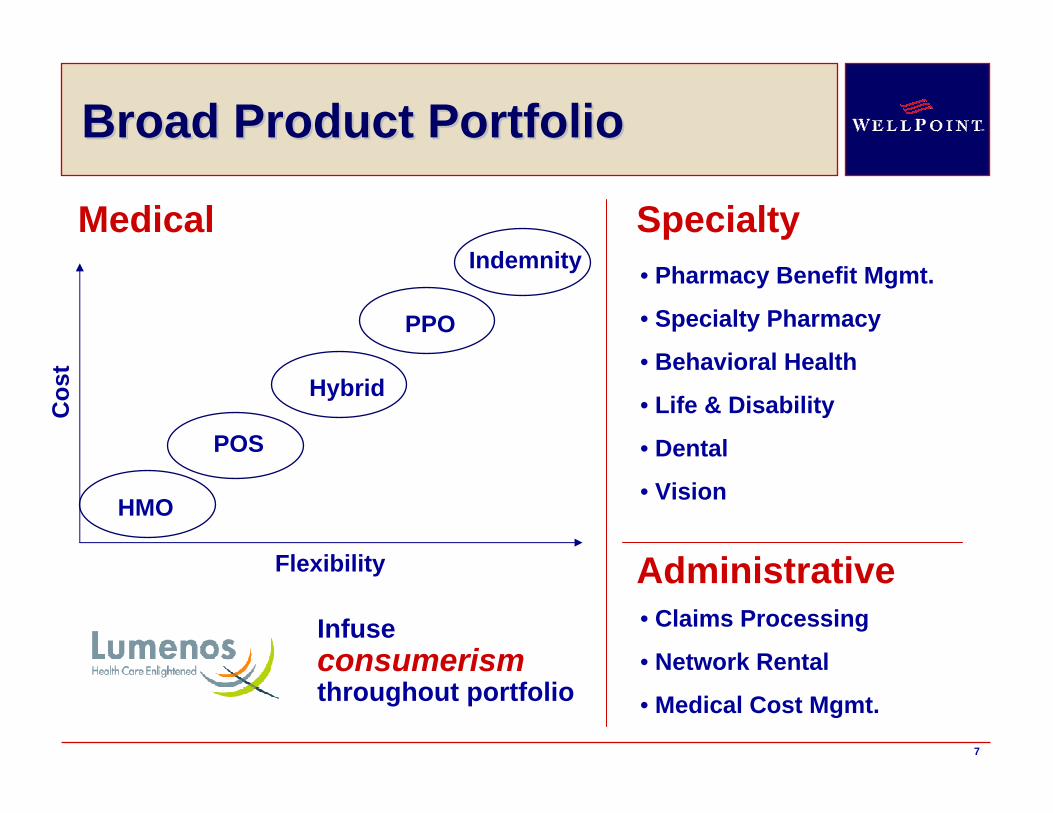

Broad Product PortfolioBroad Product Portfolio

Medical

Flexibility

SpecialtyIndemnity

PPO

Hybrid

POS

HMO

Infuse consumerismthroughout portfolio

• Pharmacy Benefit Mgmt.

• Specialty Pharmacy

• Behavioral Health

• Life & Disability

• Dental

• Vision

Administrative• Claims Processing

• Network Rental

• Medical Cost Mgmt.

8

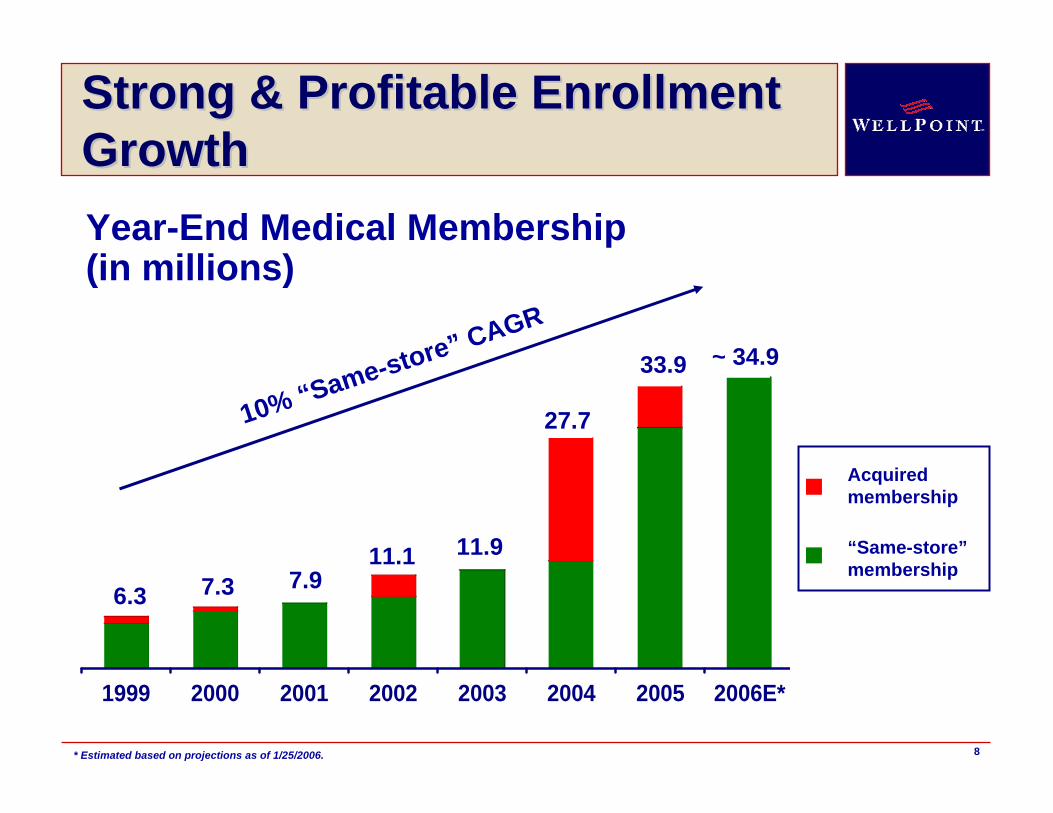

Acquiredmembership

1999 2000 2001 2002 2003 2004 2005 2006E*

Strong & Profitable Enrollment Strong & Profitable Enrollment GrowthGrowthYear-End Medical Membership (in millions)

6.311.1

7.97.3

27.7

11.9

33.9

10% “Same-store” CAGR

“Same-store”membership

~ 34.9

* Estimated based on projections as of 1/25/2006.

9

AgendaAgenda

• WellPoint Profile

• Superior Value Proposition

• Revenue Growth Opportunities

• 15%+ EPS Growth Target

• Investment Considerations

10

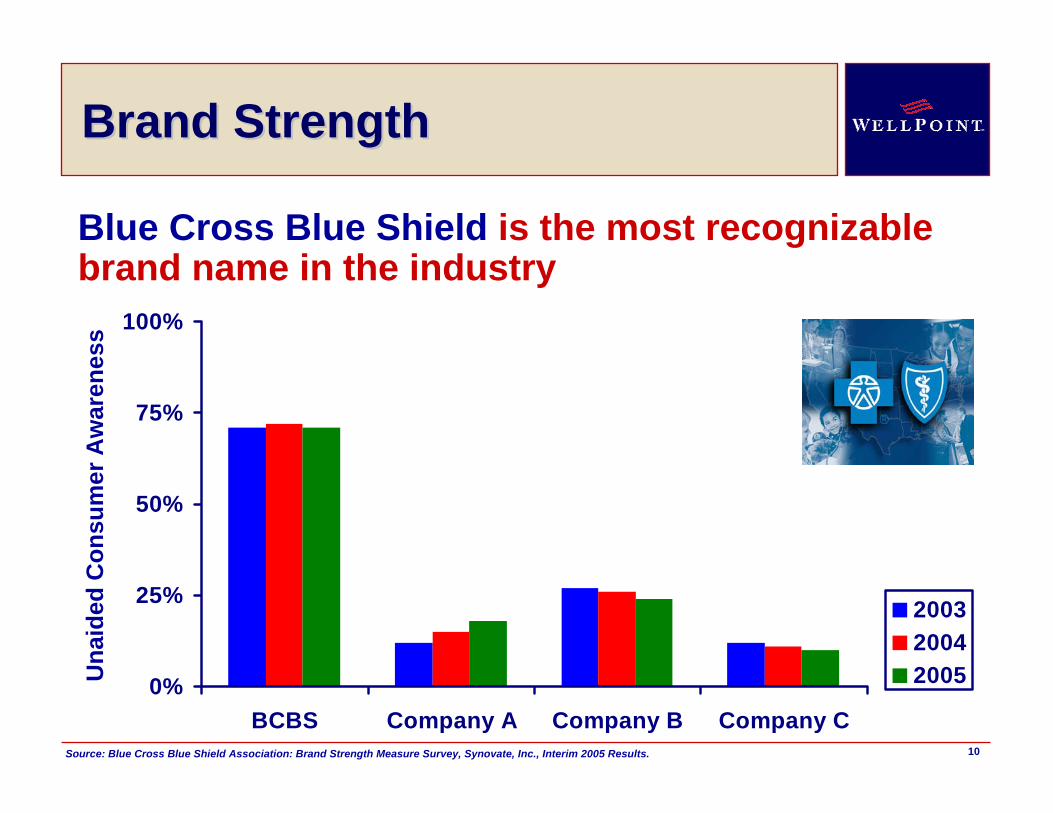

0%

25%

50%

75%

100%

BCBS Company A Company B Company C

200320042005

Brand StrengthBrand Strength

Source: Blue Cross Blue Shield Association: Brand Strength Measure Survey, Synovate, Inc., Interim 2005 Results.

Una

ided

Con

sum

er A

war

enes

s

Blue Cross Blue Shield is the most recognizable brand name in the industry

11

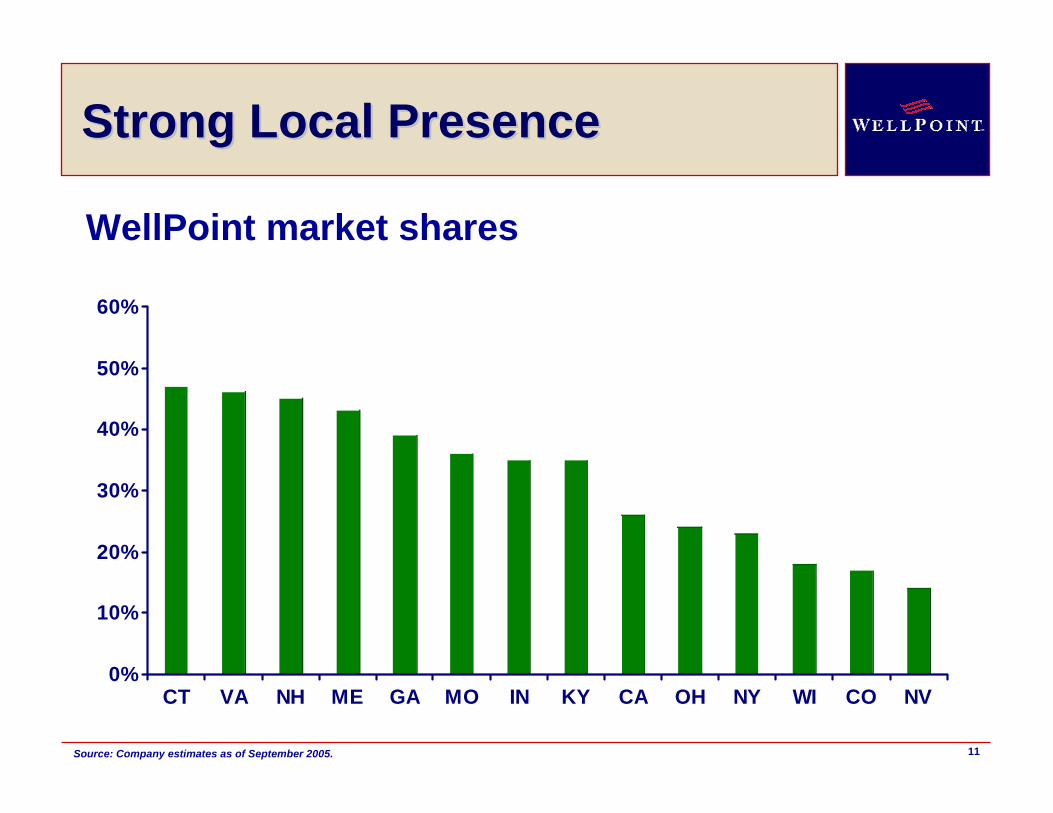

Strong Local PresenceStrong Local Presence

0%

10%

20%

30%

40%

50%

60%

CT VA NH ME GA MO IN KY CA OH NY WI CO NV

Source: Company estimates as of September 2005.

WellPoint market shares

12

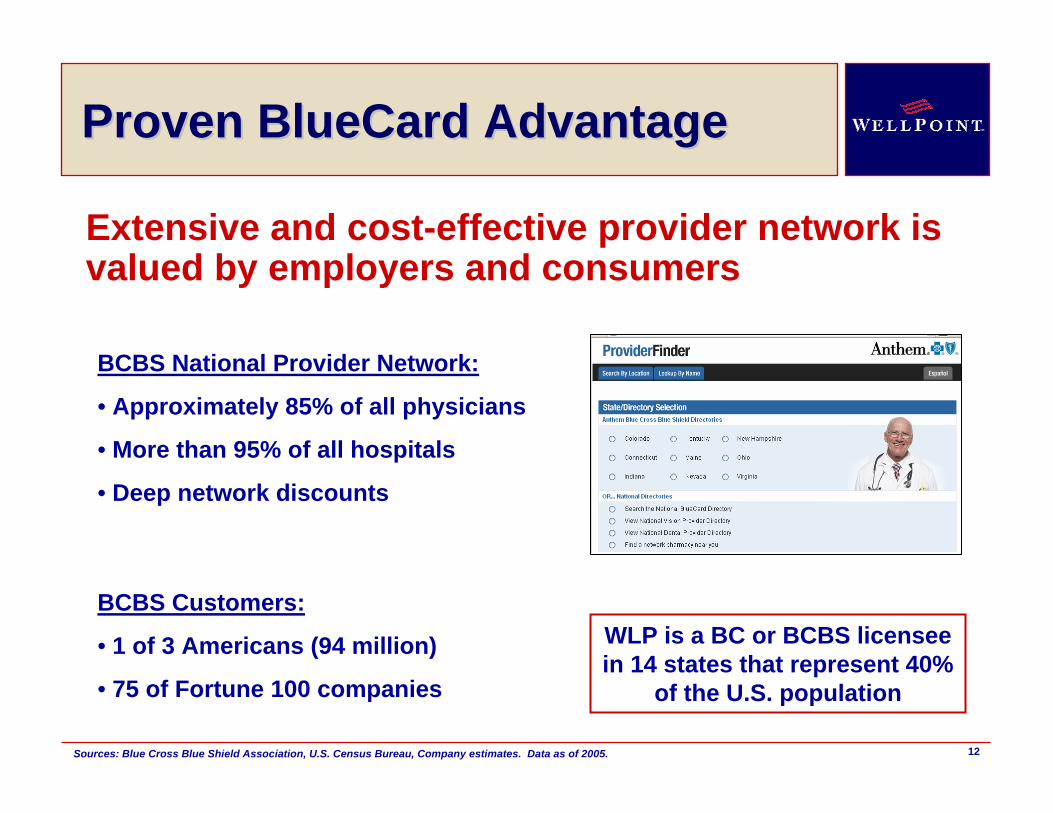

Proven BlueCard Advantage Proven BlueCard Advantage

Extensive and cost-effective provider network is valued by employers and consumers

BCBS National Provider Network:

• Approximately 85% of all physicians

• More than 95% of all hospitals

• Deep network discounts

BCBS Customers:

• 1 of 3 Americans (94 million)

• 75 of Fortune 100 companies

Sources: Blue Cross Blue Shield Association, U.S. Census Bureau, Company estimates. Data as of 2005.

WLP is a BC or BCBS licensee in 14 states that represent 40%

of the U.S. population

13

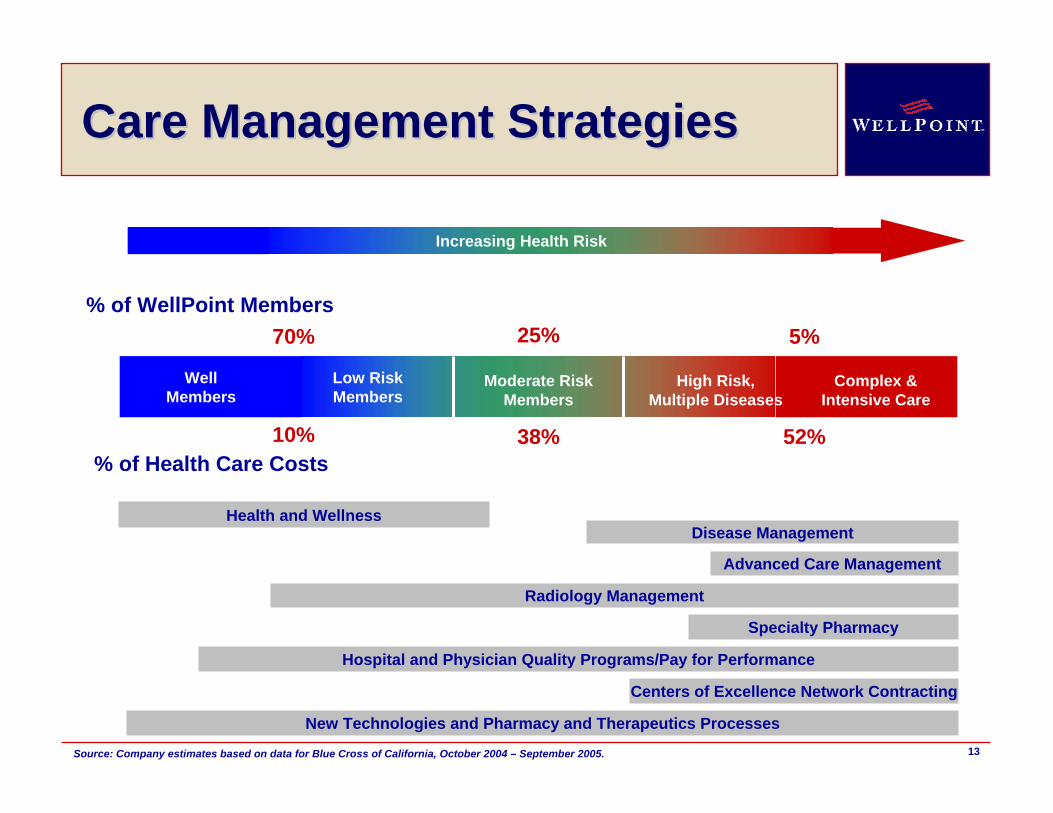

Increasing Health Risk

% of WellPoint Members

% of Health Care Costs

WellMembers

Low RiskMembers

Moderate Risk Members

High Risk,Multiple Diseases

Complex & Intensive Care

Health and WellnessDisease Management

Specialty Pharmacy

Advanced Care Management

Radiology Management

Centers of Excellence Network Contracting

Hospital and Physician Quality Programs/Pay for Performance

New Technologies and Pharmacy and Therapeutics Processes

25%

38% 52%

Care Management StrategiesCare Management Strategies

70%

10%

5%

Increasing Health Risk

Source: Company estimates based on data for Blue Cross of California, October 2004 – September 2005.

14

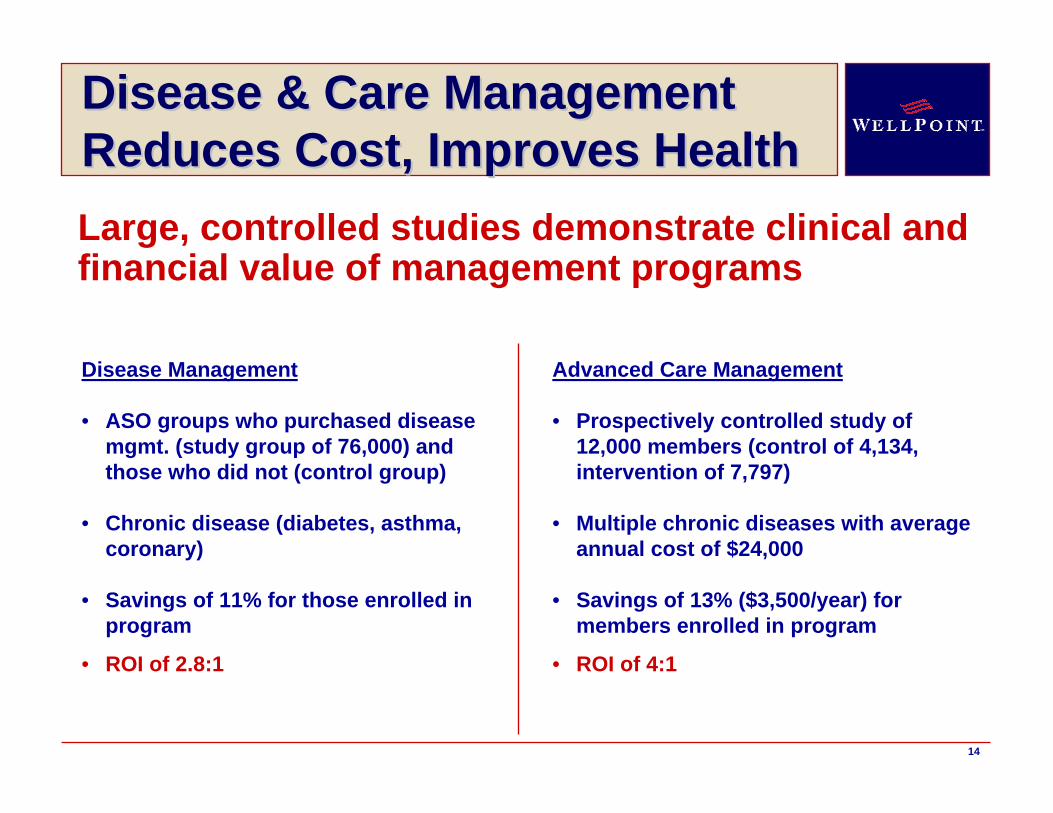

Disease & Care Management Disease & Care Management Reduces Cost, Improves HealthReduces Cost, Improves Health

Disease Management

• ASO groups who purchased disease mgmt. (study group of 76,000) and those who did not (control group)

• Chronic disease (diabetes, asthma, coronary)

• Savings of 11% for those enrolled in program

• ROI of 2.8:1

Large, controlled studies demonstrate clinical and financial value of management programs

Advanced Care Management

• Prospectively controlled study of 12,000 members (control of 4,134, intervention of 7,797)

• Multiple chronic diseases with average annual cost of $24,000

• Savings of 13% ($3,500/year) for members enrolled in program

• ROI of 4:1

15

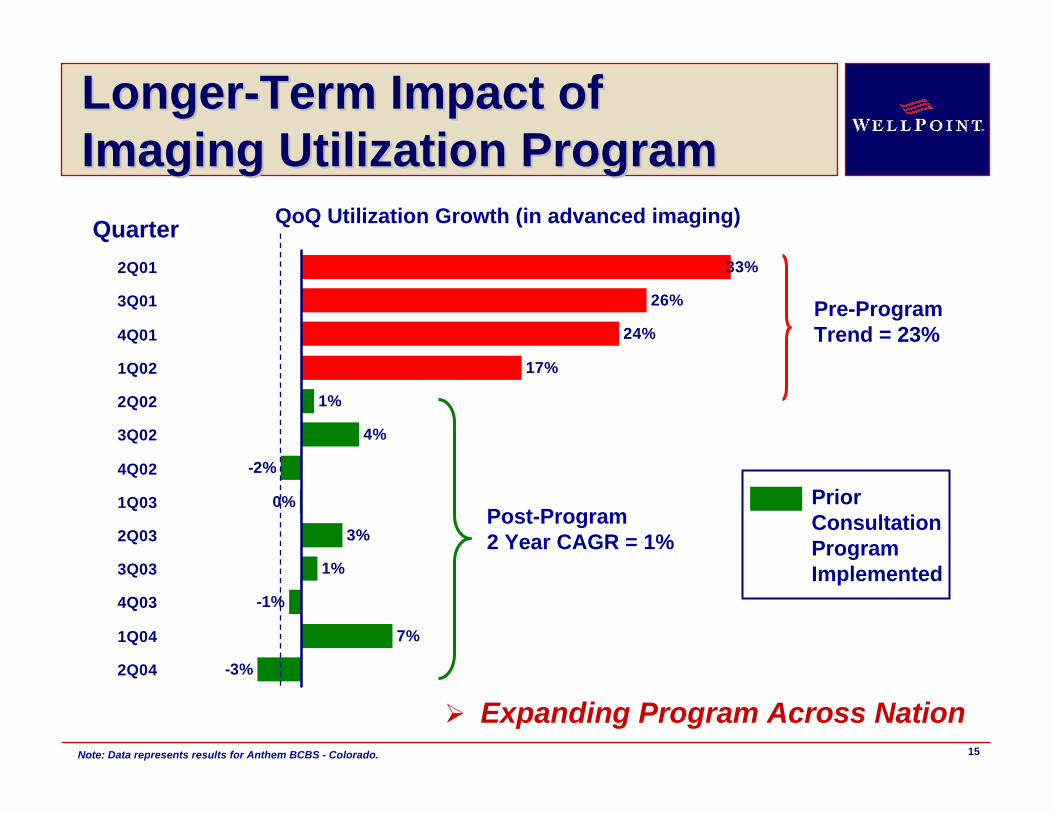

LongerLonger--Term Impact ofTerm Impact ofImaging Utilization ProgramImaging Utilization Program

QoQ Utilization Growth (in advanced imaging)Quarter

-3%

7%

-1%

1%

3%

0%

-2%

4%

1%

17%

24%

26%

33%2Q01

3Q01

4Q01

1Q02

2Q02

3Q02

4Q02

1Q03

2Q03

3Q03

4Q03

1Q04

2Q04

Note: Data represents results for Anthem BCBS - Colorado.

Prior Consultation Program Implemented

Post-Program2 Year CAGR = 1%

Pre-ProgramTrend = 23%

Expanding Program Across Nation

16

AgendaAgenda

• WellPoint Profile

• Superior Value Proposition

• Revenue Growth Opportunities

• 15%+ EPS Growth Target

• Investment Considerations

17* Data includes both the former Anthem, Inc. and the former WellPoint Health Networks Inc.

5,599

6,675

8,691

National Accounts Year-End Membership

Increase of almost2 million members, or 35%,

over last 2 years(excluding WellChoice)

(In T

hous

ands

)

BlueCard membership

Control Accounts

The Choice for National AccountsThe Choice for National Accounts

7,549

2003 * 2004 2005(w/o WC)

2005(w/ WC)

18

ABC, Inc.WellPoint Value Summary

January 01, 2005 Through December 31, 2005

17.83$ 2,503,332$

9.00$ 1,263,600$ 21,060,000$

26.83$ 3,766,932$ 21,060,000$

IRIS Patient Safety 2.54$ 356,616$ 820,217$

1.95$ 273,780$ 903,474$

Primary Nurse 0.25$ 35,100$ 63,180$

0.90$ 126,360$ 265,356$

0.75$ 105,300$ 136,890$

6.39$ 897,156$ 2,189,117$

15.39$ 2,160,756$ 23,249,117$ Total Savings

Total ROI per $1 in Provider Management fees 16.7 Total ROI per $1 in Medical Management fees 2.4

Total ROI per $1 in Provider and Med Management fees 10.8

* Any network access fees are subtracted from provider savings.

Basic Administrative Fees

TPA services

Claims cost and Provider management services

Provider Management Savings

Other Programs -- Interventions by Anthem ( Baby Benefits, Health Advocate)

Basic Administrative Fee Total

Medical Mangement Fees Medical Management Savings

Disease State Management Programs

Other Programs -- Employee Initiative Programs ( 24 hour Nurseline, HRA, Web Site, Worksite wellness, Intune)

Total Medical Mangement Administrative fees Total Med Mgmt Savings

Grand Total - All Administrative Fees, except TPA services

WellPoint Value Administrative

fees PEPM

WellPoint Value Administrative fees

Total PaidWellPoint Savings on

Services Provided

Provider Discounts, Claims Quest, Provider Review, Precert

Report 1.3Report 1.3

WellPoint saves $10.80 for every $1.00 of Provider and Medical Management fees invested by ABC, Inc.

Demonstrating Value to Demonstrating Value to CustomersCustomers

10.8Total ROI per $1 in Provider and Med. Mgmt. Fees2.4Total ROI per $1 in Medical Management Fees

16.7Total ROI per $1 in Provider Management Fees

Sample report for illustrative

purposes

19

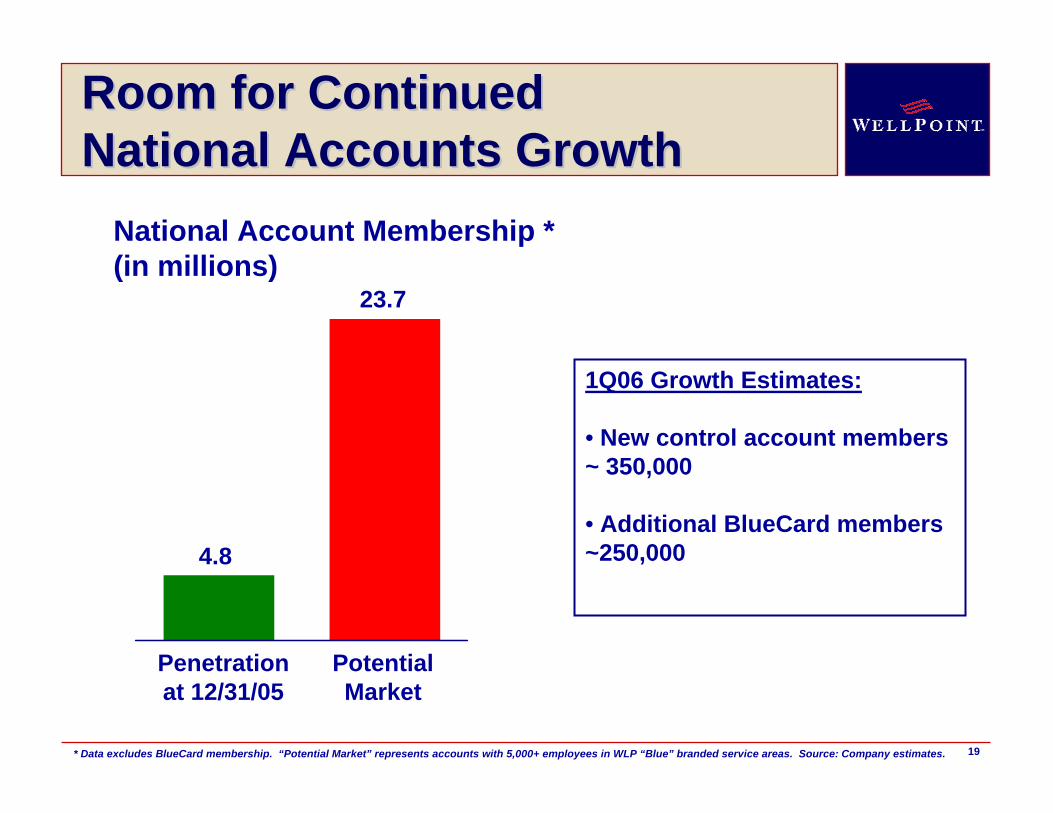

Room for ContinuedRoom for ContinuedNational Accounts GrowthNational Accounts Growth

* Data excludes BlueCard membership. “Potential Market” represents accounts with 5,000+ employees in WLP “Blue” branded service areas. Source: Company estimates.

National Account Membership * (in millions)

23.7

4.8

Penetrationat 12/31/05

PotentialMarket

1Q06 Growth Estimates:

• New control account members ~ 350,000

• Additional BlueCard members ~250,000

20

A Leader in ConsumerA Leader in Consumer--Directed Directed Health CareHealth Care

• 75% of 1/1/06 National Account RFP’s requested CDHP options

• 12 new 1/1/06 account wins were joint sales with Lumenos

• 507,000 CDHP members at 12/31/05, including an increase of 28% since 6/30/05

21

Empowering ConsumersEmpowering Consumers

22

Selected Lumenos CustomersSelected Lumenos Customers

Fortune 100:Global

Technology Company

StaplesStaplesNational Office Supply

Company

Nokia

Now expanding CDHP offerings to smaller-sized groups

23

DirigoChoice

Uninsured Americans:Uninsured Americans:A Growth OpportunityA Growth OpportunityIn 2005, approximately 378,000 new WLP enrollees were previously uninsured

Tonik

Blue Access Economy

BeneFits

Community resource centers

Enrollment vans

Low-to-moderate

income~ 16M

Eligible for public programs~14M

Household income > $50,000

~ 16M

SelectHMO & PPO

Sources: Blue Cross Blue Shield Association, U.S. Census Bureau, August 2005.

BasicChoice

24

Product InnovationProduct Innovation

www.tonik.com

69% of applicants previously uninsured

25

Addressing Multiple PopulationsAddressing Multiple Populations

26

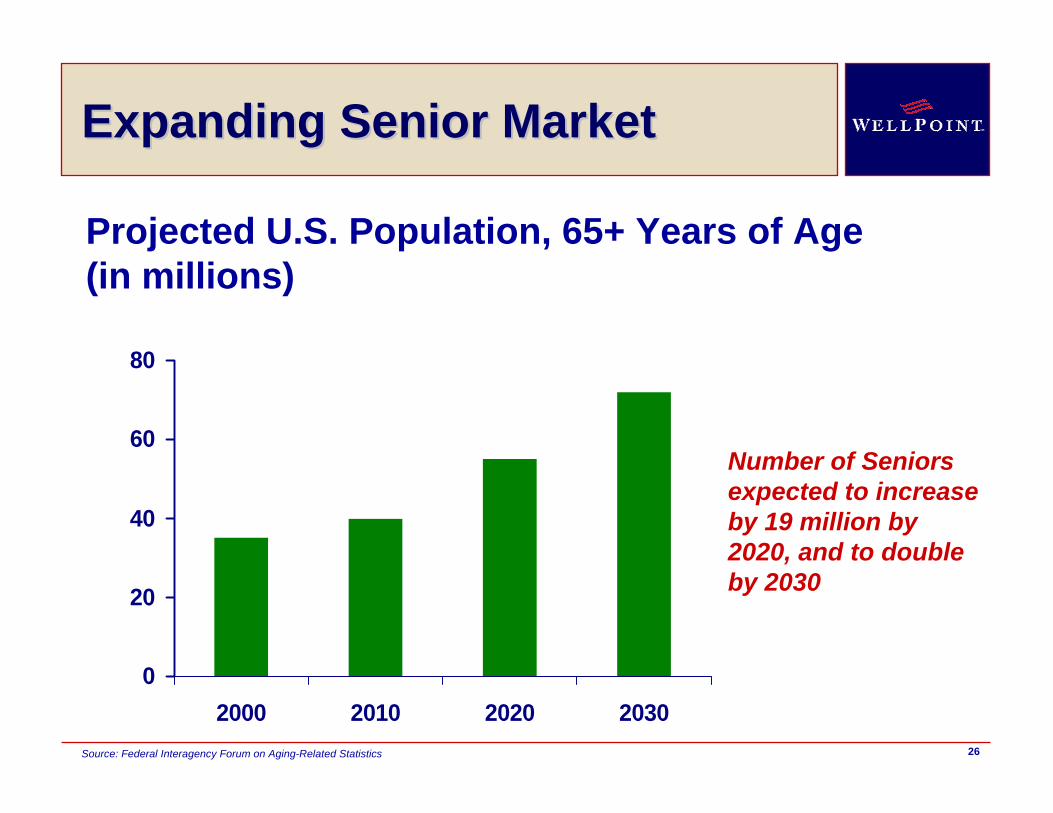

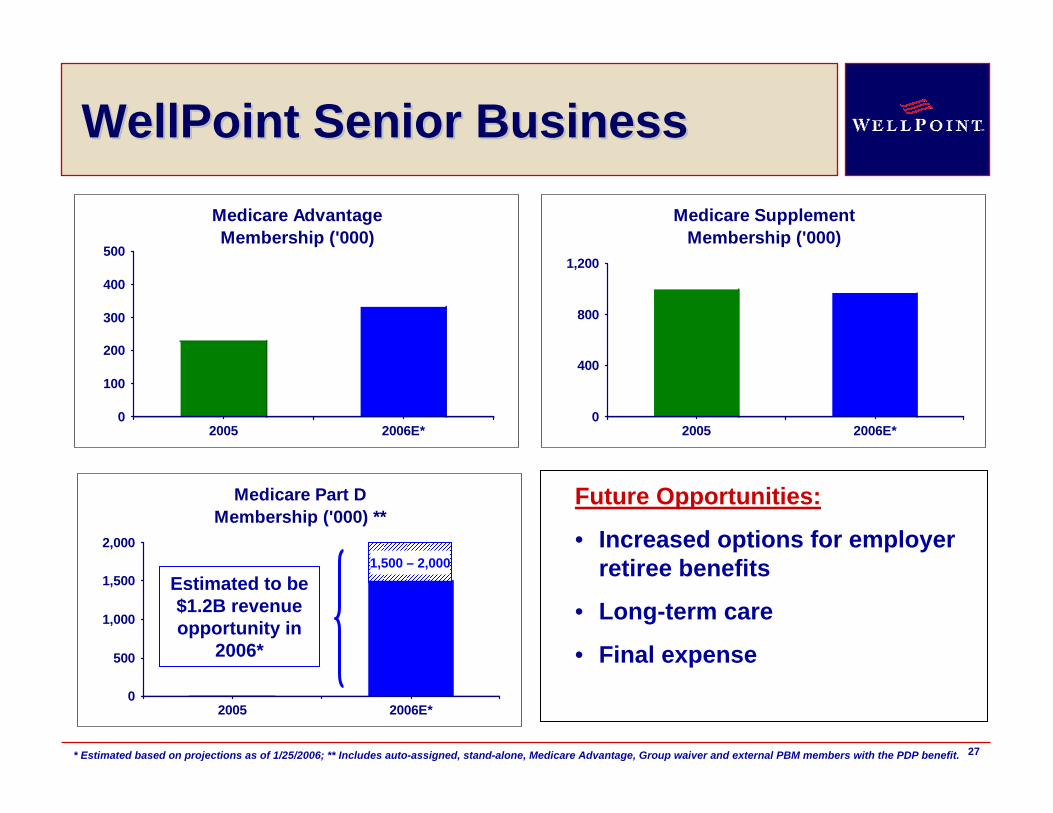

Expanding Senior MarketExpanding Senior Market

0

20

40

60

80

2000 2010 2020 2030

Projected U.S. Population, 65+ Years of Age (in millions)

Source: Federal Interagency Forum on Aging-Related Statistics

Number of Seniors expected to increase by 19 million by 2020, and to double by 2030

27

0

500

1,000

1,500

2,000

2005 2006E*

Medicare Part DMembership ('000) **

WellPoint Senior BusinessWellPoint Senior Business

0

100

200

300

400

500

2005 2006E*

Medicare AdvantageMembership ('000)

0

400

800

1,200

2005 2006E*

Medicare SupplementMembership ('000)

* Estimated based on projections as of 1/25/2006; ** Includes auto-assigned, stand-alone, Medicare Advantage, Group waiver and external PBM members with the PDP benefit.

Estimated to be $1.2B revenue opportunity in

2006*

Future Opportunities:

• Increased options for employer retiree benefits

• Long-term care

• Final expense

1,500 – 2,000

28

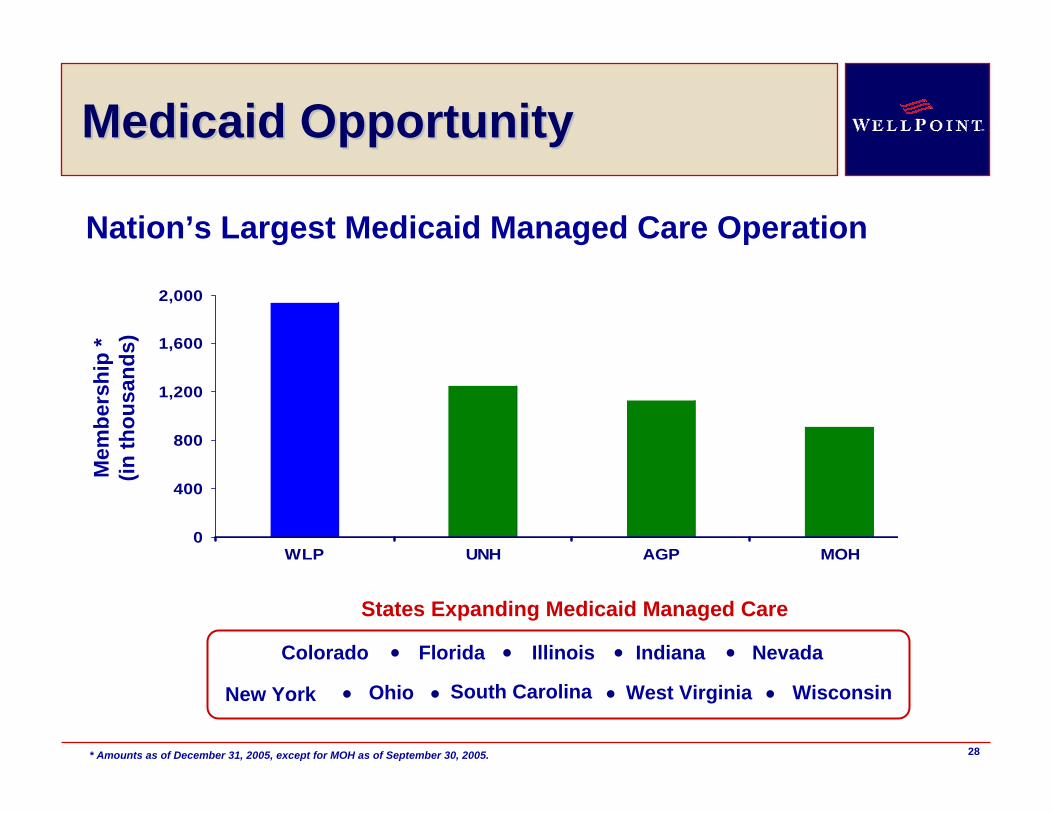

0

400

800

1,200

1,600

2,000

WLP UNH AGP MOH

States Expanding Medicaid Managed Care

Medicaid Opportunity Medicaid Opportunity

Nation’s Largest Medicaid Managed Care Operation

Mem

bers

hip

* (in

thou

sand

s)

* Amounts as of December 31, 2005, except for MOH as of September 30, 2005.

Ohio

Indiana

South Carolina Wisconsin

FloridaColorado Illinois Nevada

New York West Virginia

29

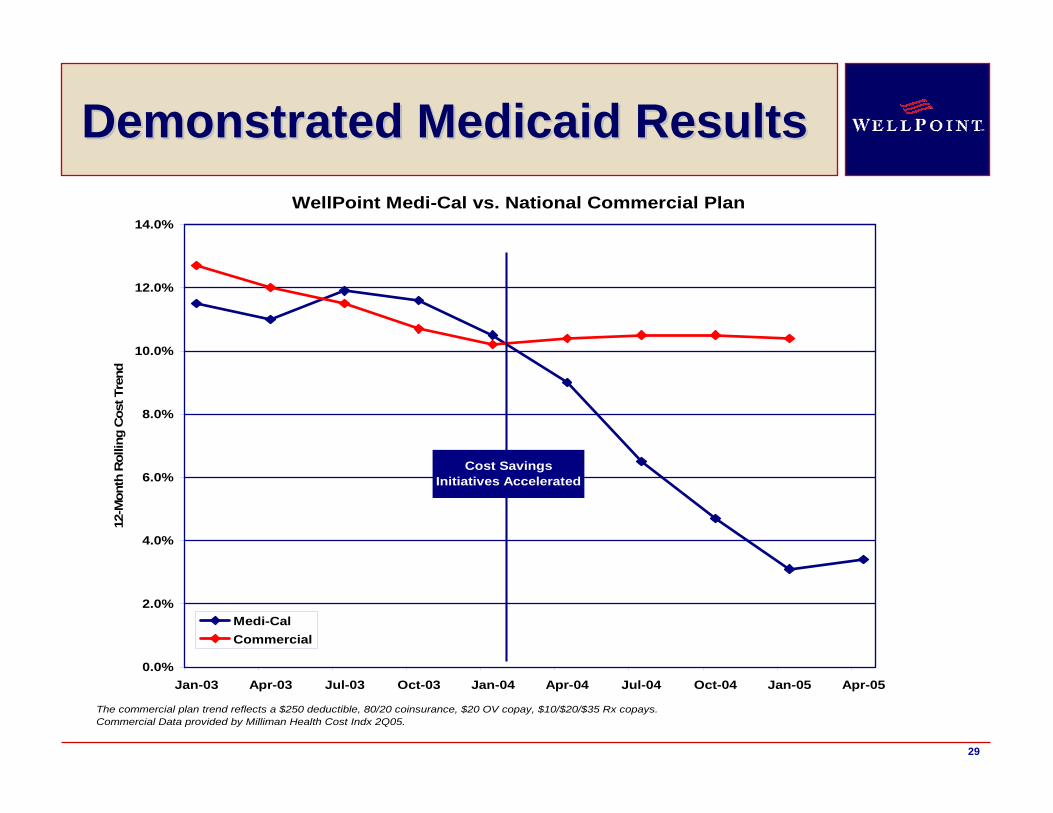

Demonstrated Medicaid ResultsDemonstrated Medicaid ResultsWellPoint Medi-Cal vs. National Commercial Plan

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Jan-03 Apr-03 Jul-03 Oct-03 Jan-04 Apr-04 Jul-04 Oct-04 Jan-05 Apr-05

12-M

onth

Rol

ling

Cos

t Tre

nd

Medi-CalCommercial

The commercial plan trend reflects a $250 deductible, 80/20 coinsurance, $20 OV copay, $10/$20/$35 Rx copays.Commercial Data provided by Milliman Health Cost Indx 2Q05.

Cost Savings Initiatives Accelerated

30

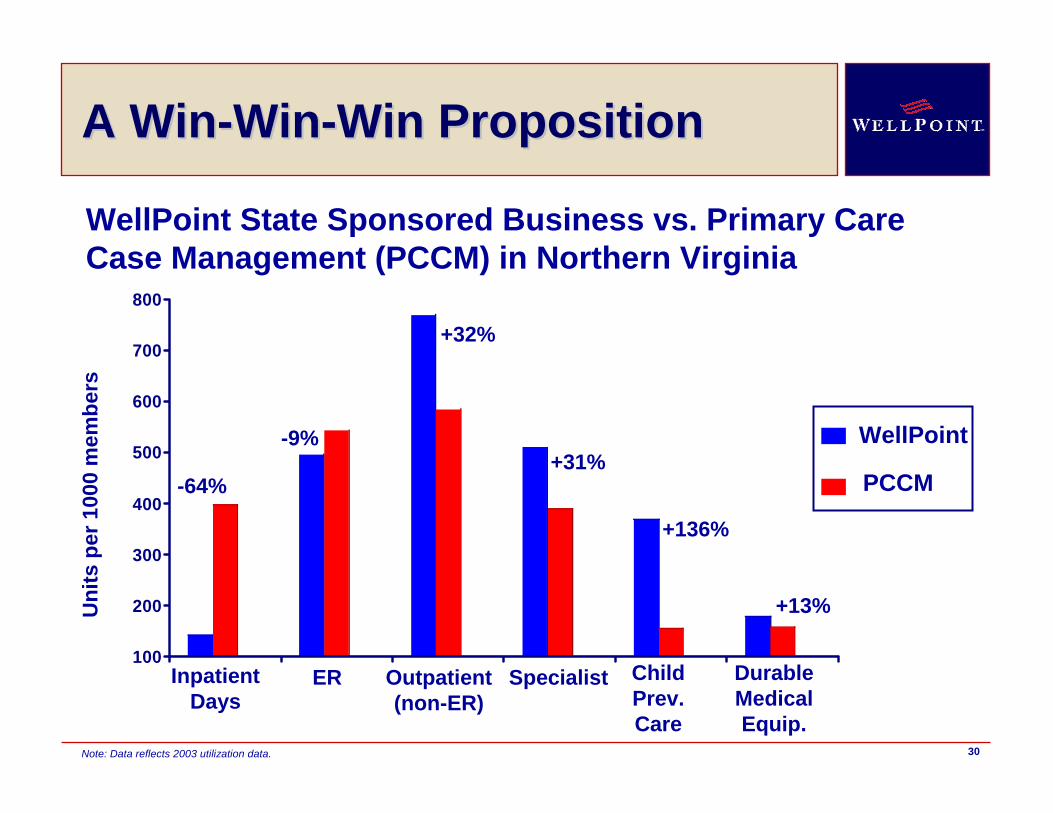

100

200

300

400

500

600

700

800

WellPoint

PCCM-64%

-9%

+32%

+31%

+136%

+13%Uni

ts p

er 1

000

mem

bers

Inpatient Days

ER Outpatient(non-ER)

Specialist Child Prev. Care

Durable Medical Equip.

WellPoint State Sponsored Business vs. Primary Care Case Management (PCCM) in Northern Virginia

A WinA Win--WinWin--Win PropositionWin Proposition

Note: Data reflects 2003 utilization data.

31

AgendaAgenda

• WellPoint Profile

• Superior Value Proposition

• Revenue Growth Opportunities

• 15%+ EPS Growth Target

• Investment Considerations

32

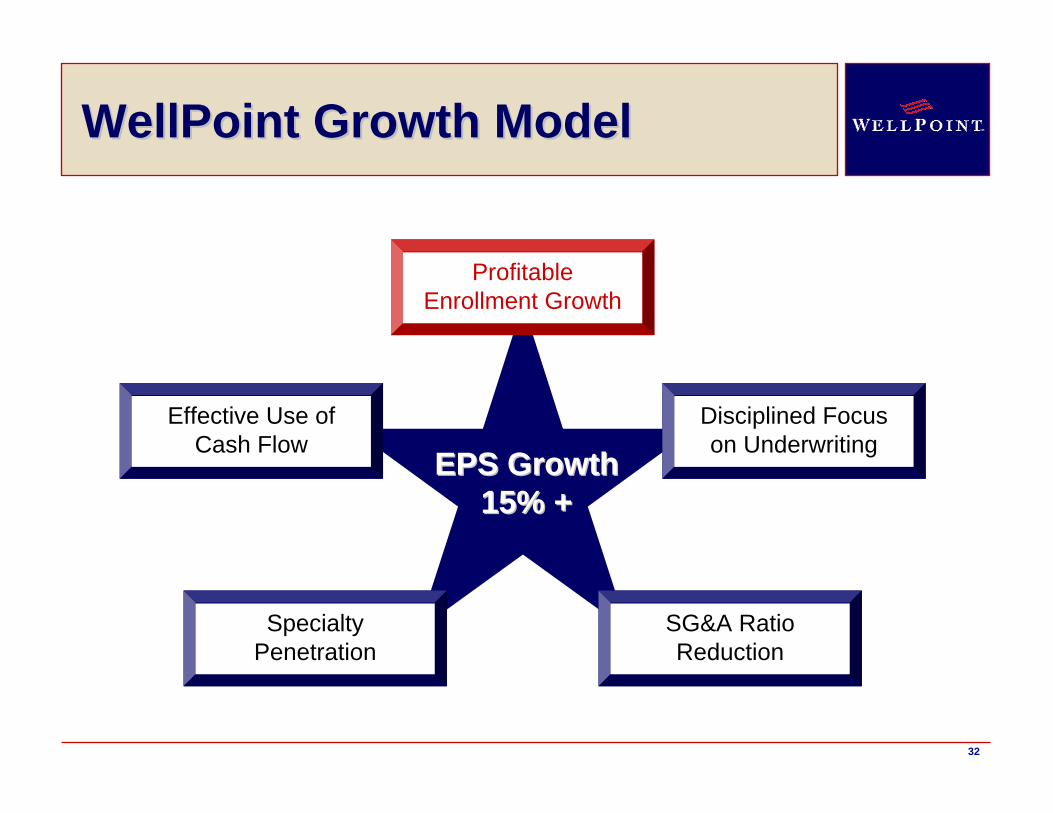

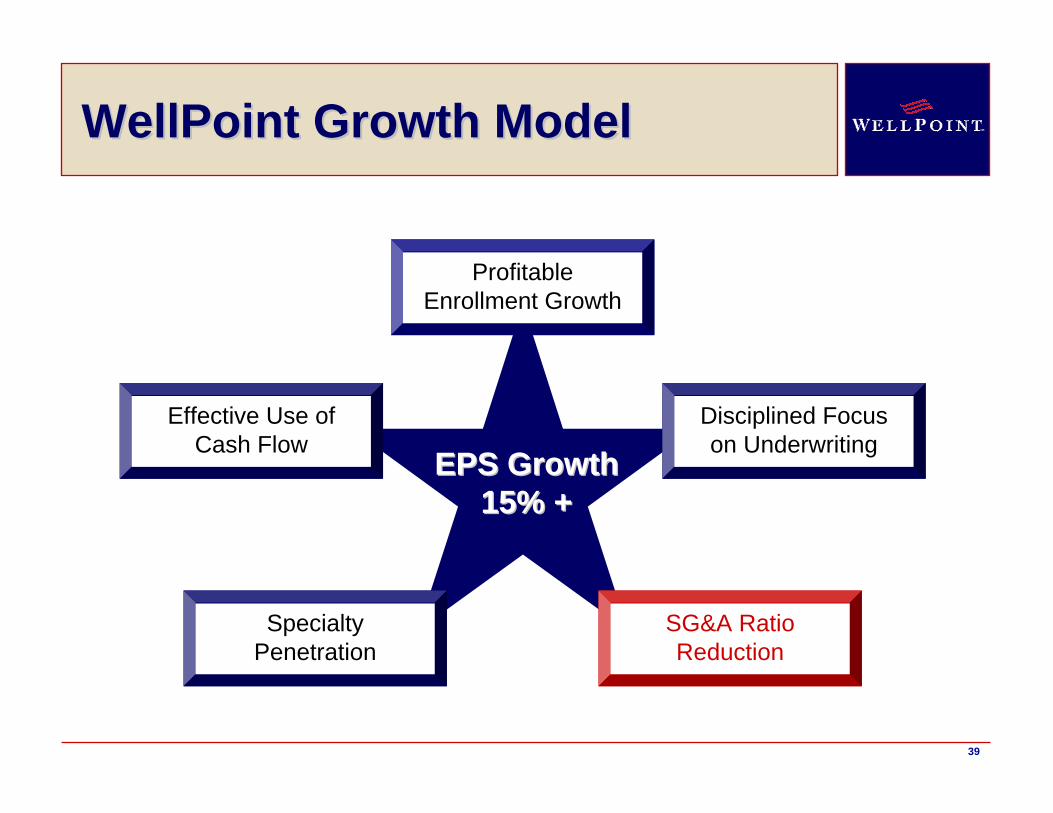

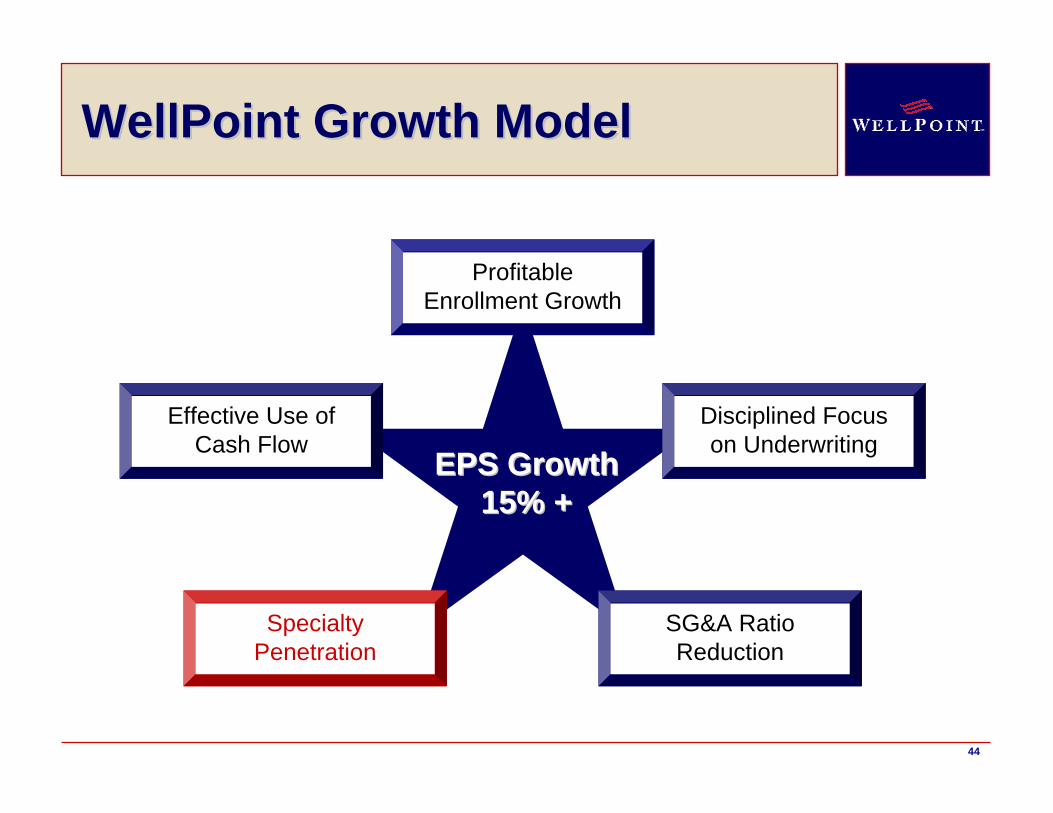

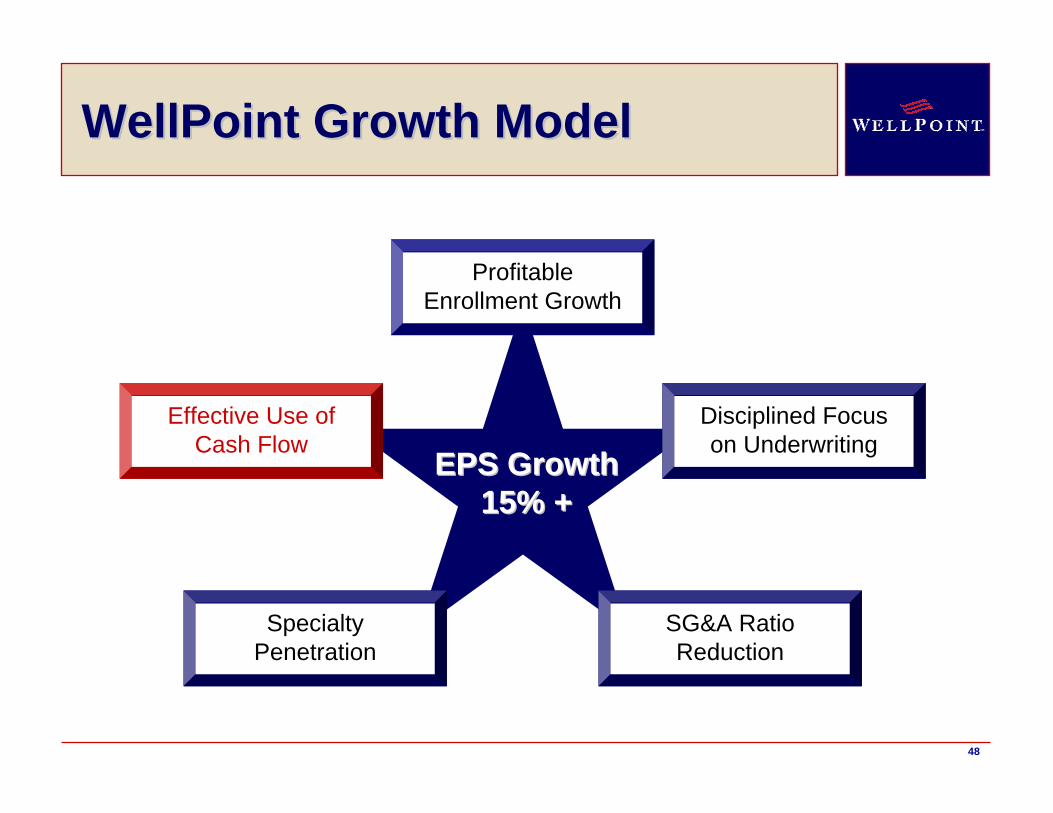

WellPoint Growth ModelWellPoint Growth Model

EPS GrowthEPS Growth15% +15% +

Profitable Enrollment Growth

Disciplined Focus on Underwriting

Effective Use of Cash Flow

SG&A Ratio Reduction

Specialty Penetration

33

Significant Growth OpportunitiesSignificant Growth Opportunities

34

WellPoint Growth ModelWellPoint Growth Model

EPS GrowthEPS Growth15% +15% +

Profitable Enrollment Growth

Disciplined Focus on Underwriting

Effective Use of Cash Flow

SG&A Ratio Reduction

Specialty Penetration

35

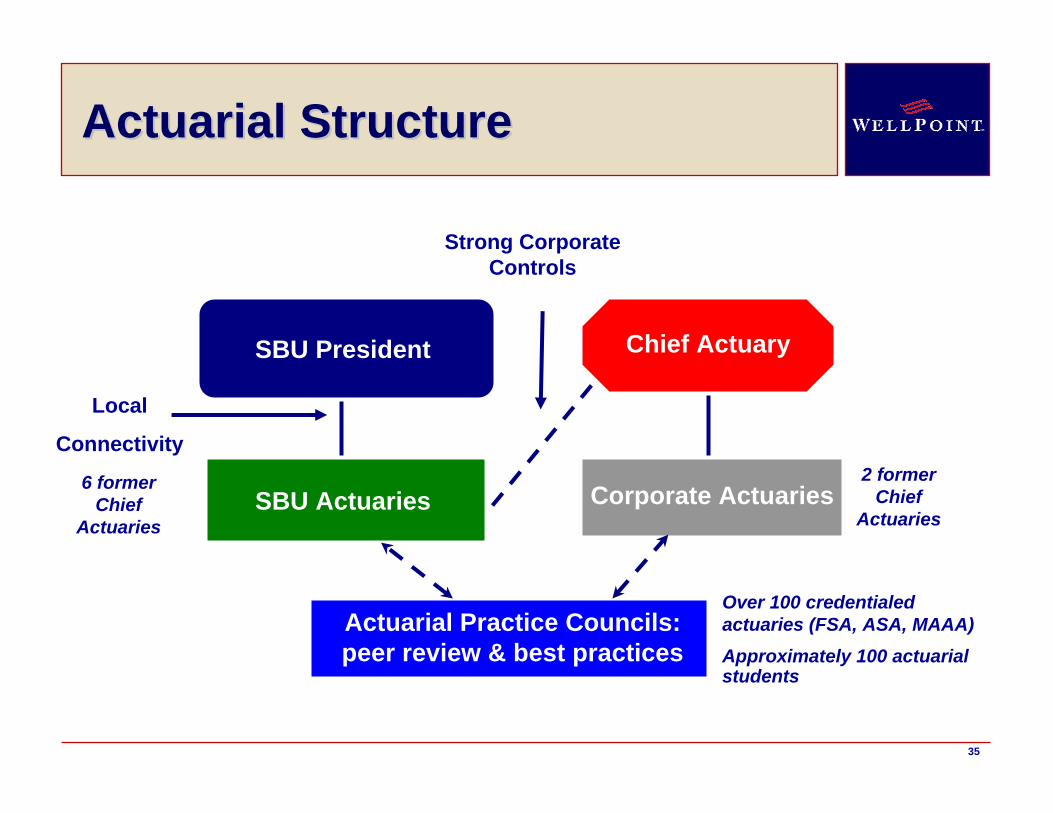

Actuarial StructureActuarial Structure

Actuarial Practice Councils:peer review & best practices

SBU President

SBU Actuaries

Chief Actuary

Local

Connectivity

Over 100 credentialed actuaries (FSA, ASA, MAAA)Approximately 100 actuarial students

Corporate Actuaries2 former

Chief Actuaries

6 formerChief

Actuaries

Strong Corporate Controls

36

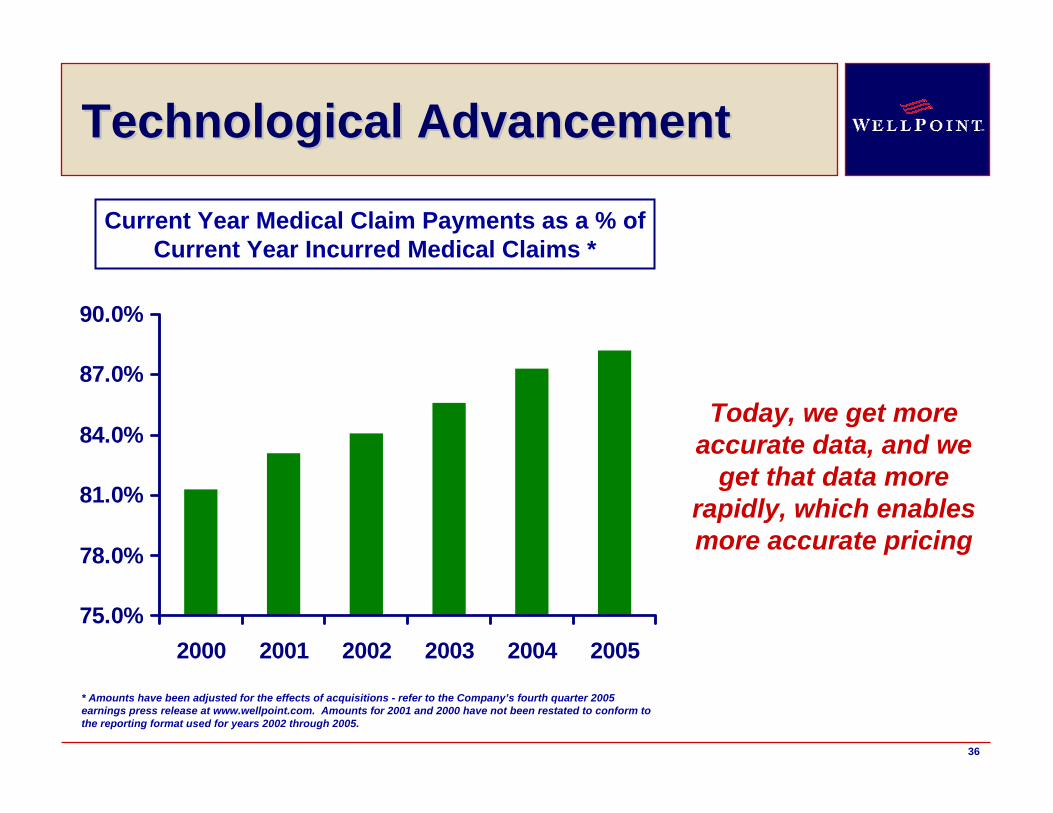

Technological AdvancementTechnological Advancement

Today, we get more accurate data, and we

get that data more rapidly, which enables more accurate pricing

75.0%

78.0%

81.0%

84.0%

87.0%

90.0%

2000 2001 2002 2003 2004 2005

Current Year Medical Claim Payments as a % of Current Year Incurred Medical Claims *

* Amounts have been adjusted for the effects of acquisitions - refer to the Company’s fourth quarter 2005 earnings press release at www.wellpoint.com. Amounts for 2001 and 2000 have not been restated to conform to the reporting format used for years 2002 through 2005.

37

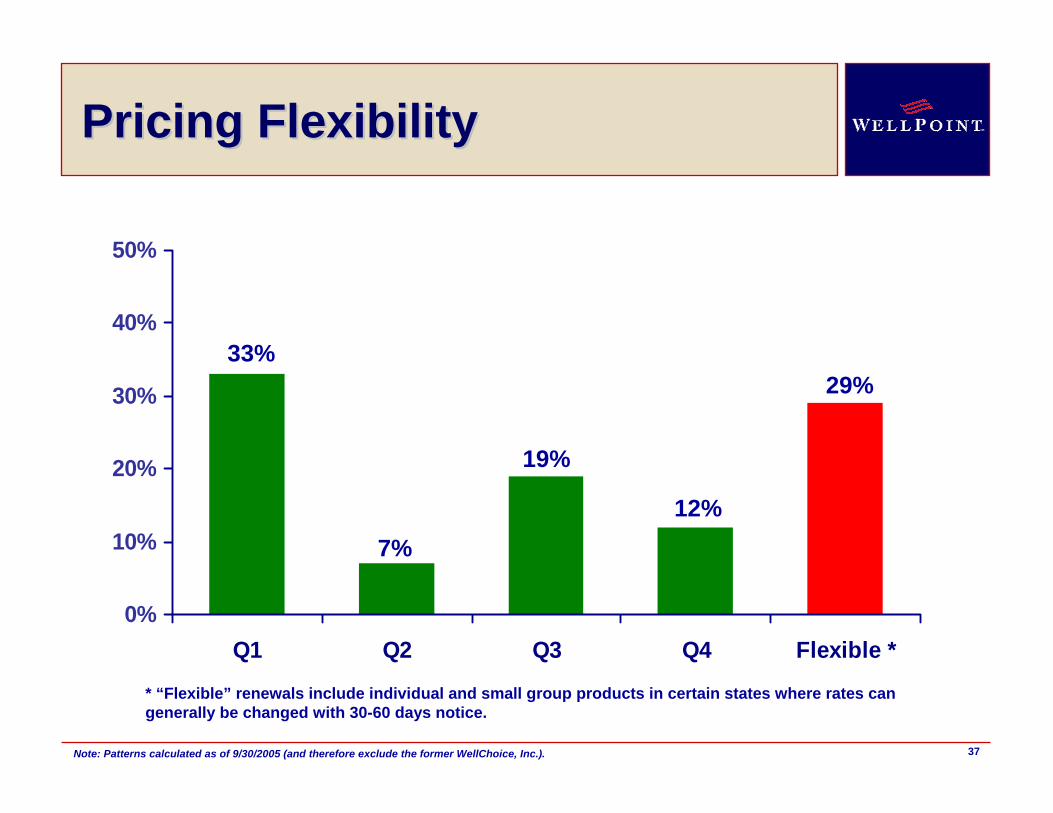

Pricing FlexibilityPricing Flexibility

0%

10%

20%

30%

40%

50%

Q1 Q2 Q3 Q4 Flexible *

* “Flexible” renewals include individual and small group products in certain states where rates can generally be changed with 30-60 days notice.

33%

7%

19%

12%

29%

Note: Patterns calculated as of 9/30/2005 (and therefore exclude the former WellChoice, Inc.).

38

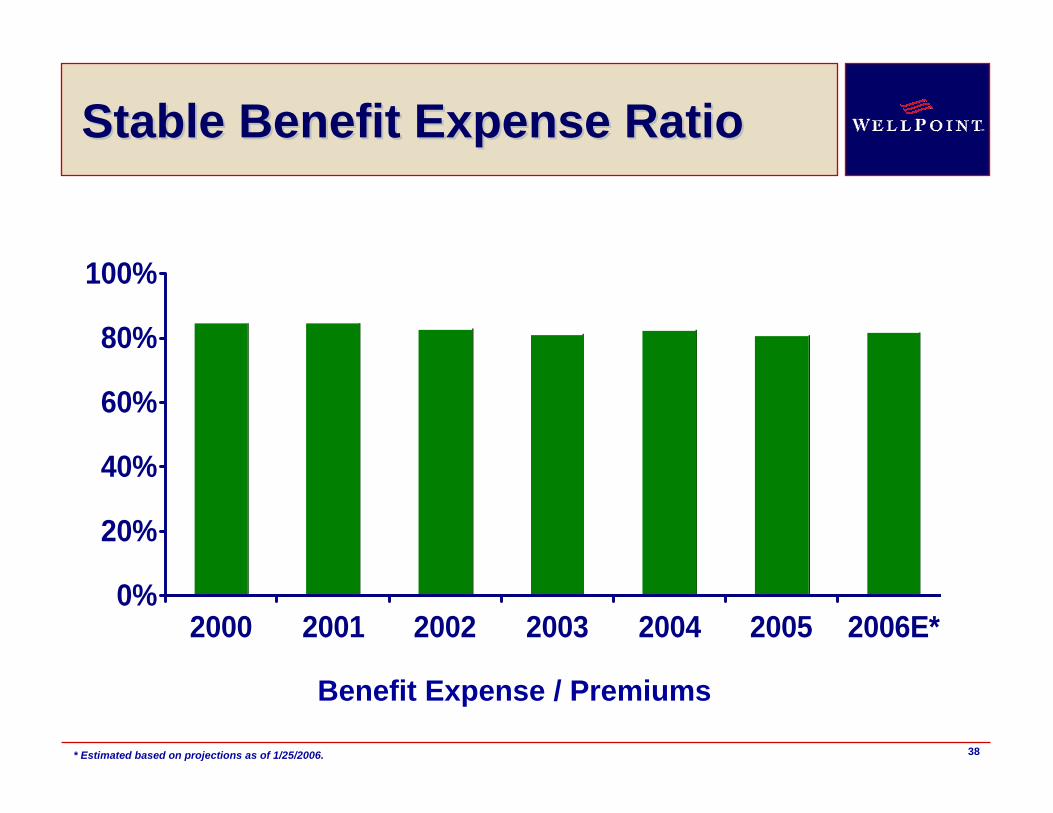

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003 2004 2005 2006E*

Benefit Expense / Premiums

Stable Benefit Expense RatioStable Benefit Expense Ratio

* Estimated based on projections as of 1/25/2006.

39

WellPoint Growth ModelWellPoint Growth Model

EPS GrowthEPS Growth15% +15% +

Profitable Enrollment Growth

Disciplined Focus on Underwriting

Effective Use of Cash Flow

SG&A Ratio Reduction

Specialty Penetration

40

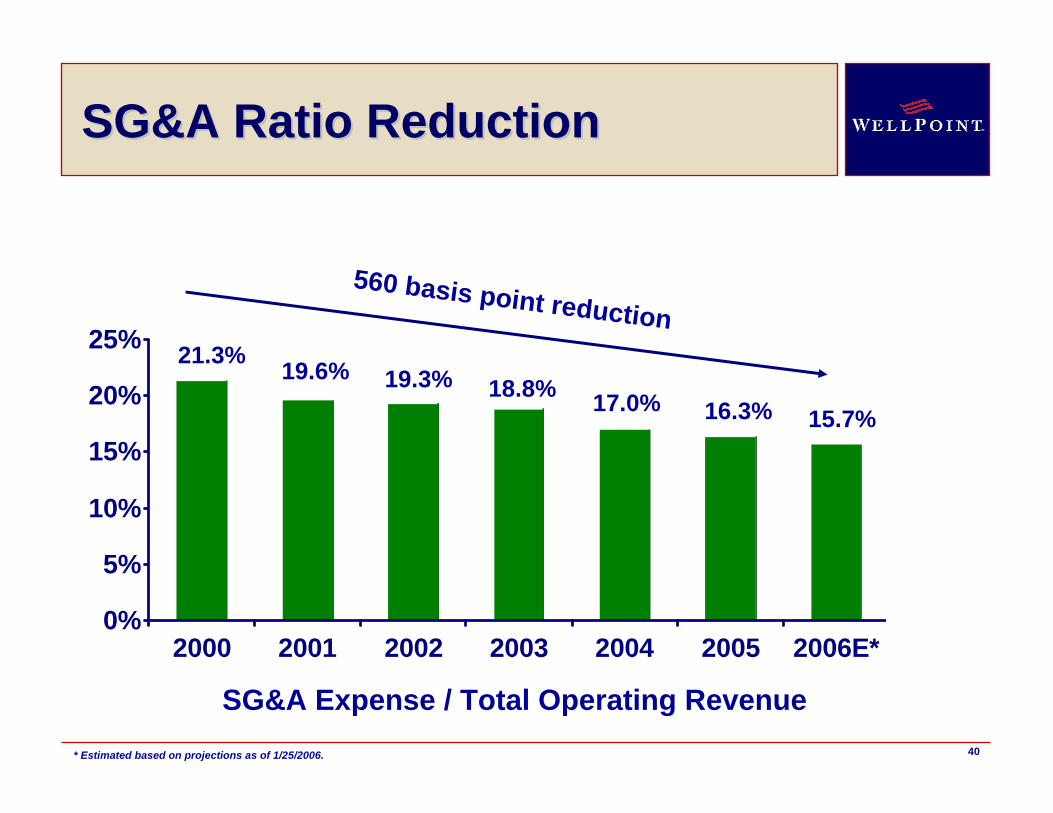

0%

5%

10%

15%

20%

25%

2000 2001 2002 2003 2004 2005 2006E*

SG&A Expense / Total Operating Revenue

SG&A Ratio ReductionSG&A Ratio Reduction

560 basis point reduction21.3% 19.6% 19.3% 18.8% 17.0% 16.3%

* Estimated based on projections as of 1/25/2006.

15.7%

41

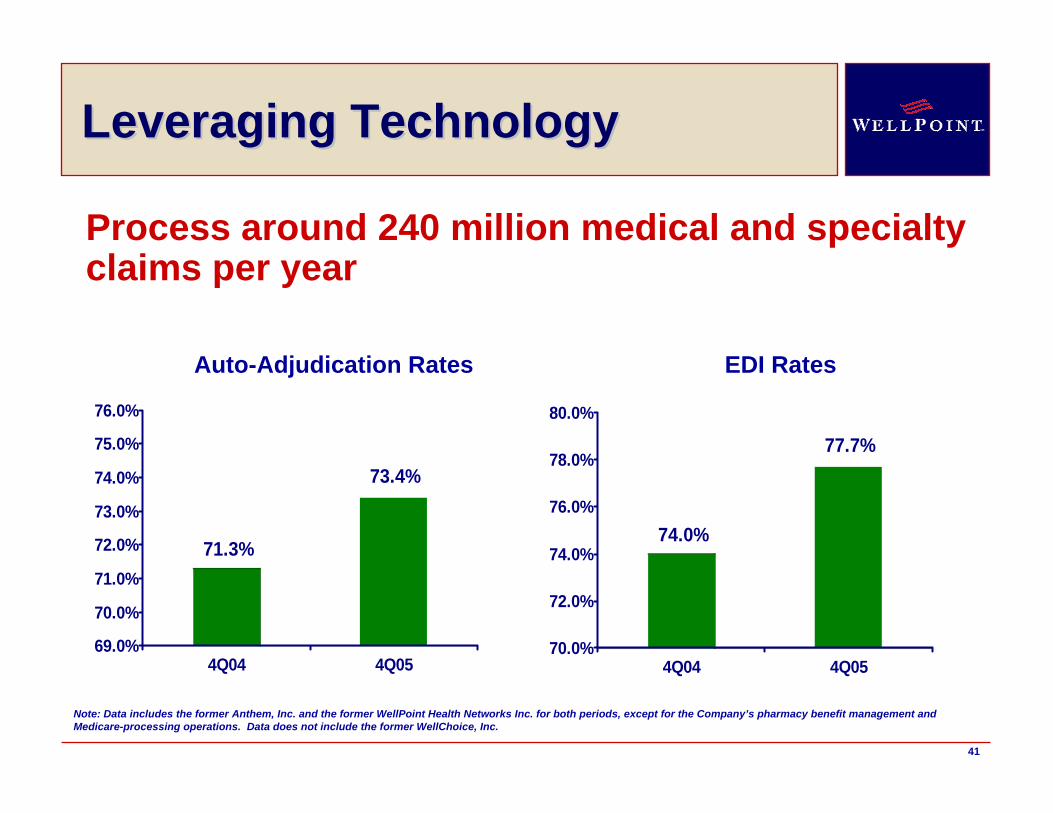

Leveraging TechnologyLeveraging Technology

71.3%

73.4%

69.0%

70.0%

71.0%

72.0%

73.0%

74.0%

75.0%

76.0%

4Q04 4Q05

Auto-Adjudication Rates

Process around 240 million medical and specialty claims per year

74.0%

77.7%

70.0%

72.0%

74.0%

76.0%

78.0%

80.0%

4Q04 4Q05

EDI Rates

Note: Data includes the former Anthem, Inc. and the former WellPoint Health Networks Inc. for both periods, except for the Company’s pharmacy benefit management and Medicare-processing operations. Data does not include the former WellChoice, Inc.

42

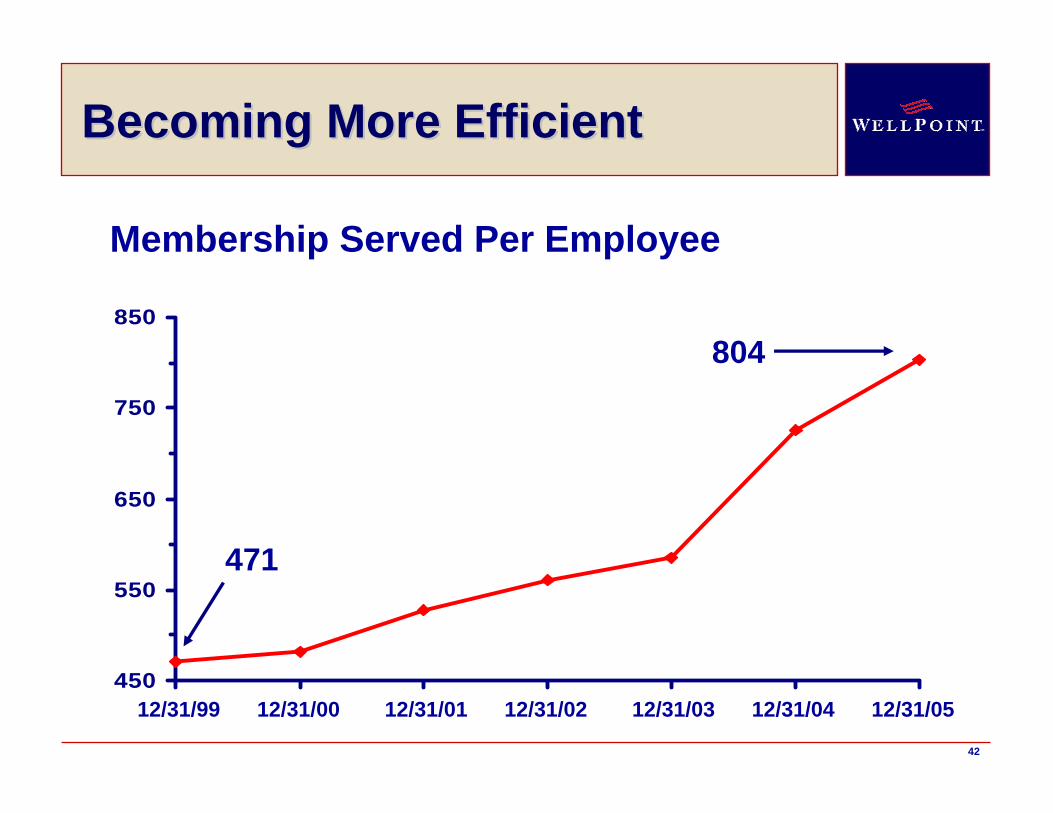

Becoming More EfficientBecoming More Efficient

450

550

650

750

850

Membership Served Per Employee

12/31/99 12/31/01 12/31/03 12/31/0512/31/00 12/31/02 12/31/04

804

471

43

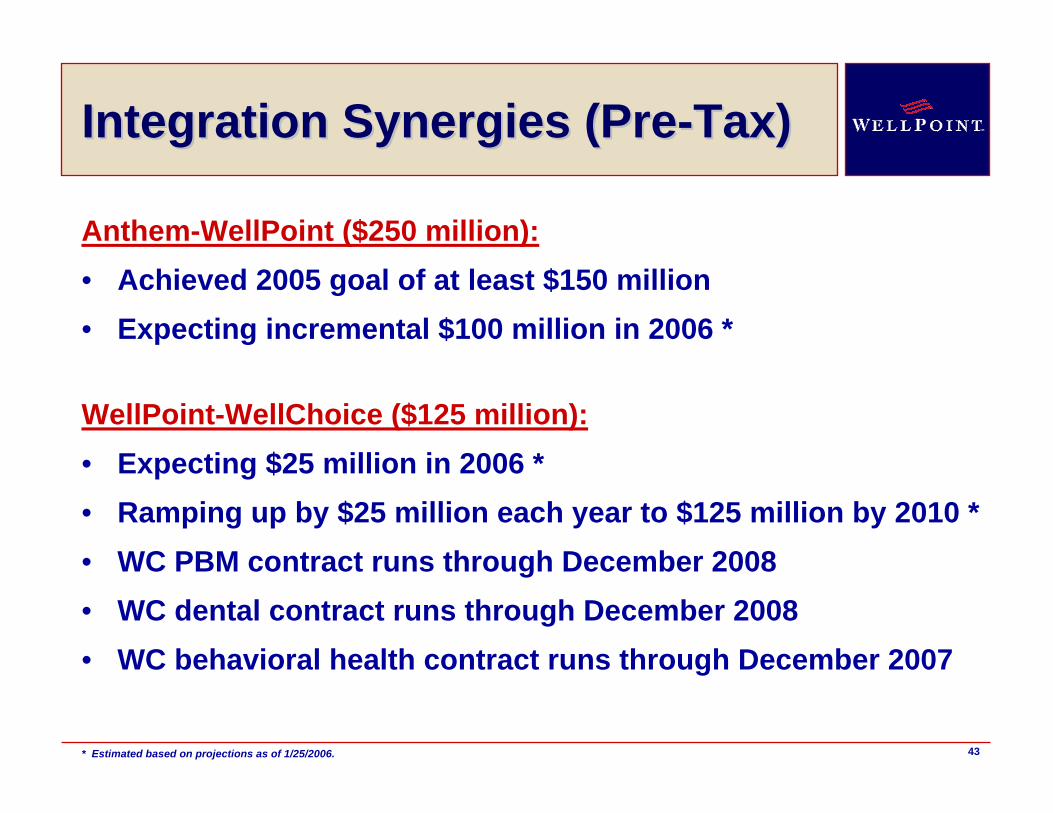

Integration Synergies (PreIntegration Synergies (Pre--Tax)Tax)

Anthem-WellPoint ($250 million):• Achieved 2005 goal of at least $150 million• Expecting incremental $100 million in 2006 *

* Estimated based on projections as of 1/25/2006.

WellPoint-WellChoice ($125 million):• Expecting $25 million in 2006 *• Ramping up by $25 million each year to $125 million by 2010 *• WC PBM contract runs through December 2008• WC dental contract runs through December 2008• WC behavioral health contract runs through December 2007

44

WellPoint Growth ModelWellPoint Growth Model

EPS GrowthEPS Growth15% +15% +

Profitable Enrollment Growth

Disciplined Focus on Underwriting

Effective Use of Cash Flow

SG&A Ratio Reduction

Specialty Penetration

45

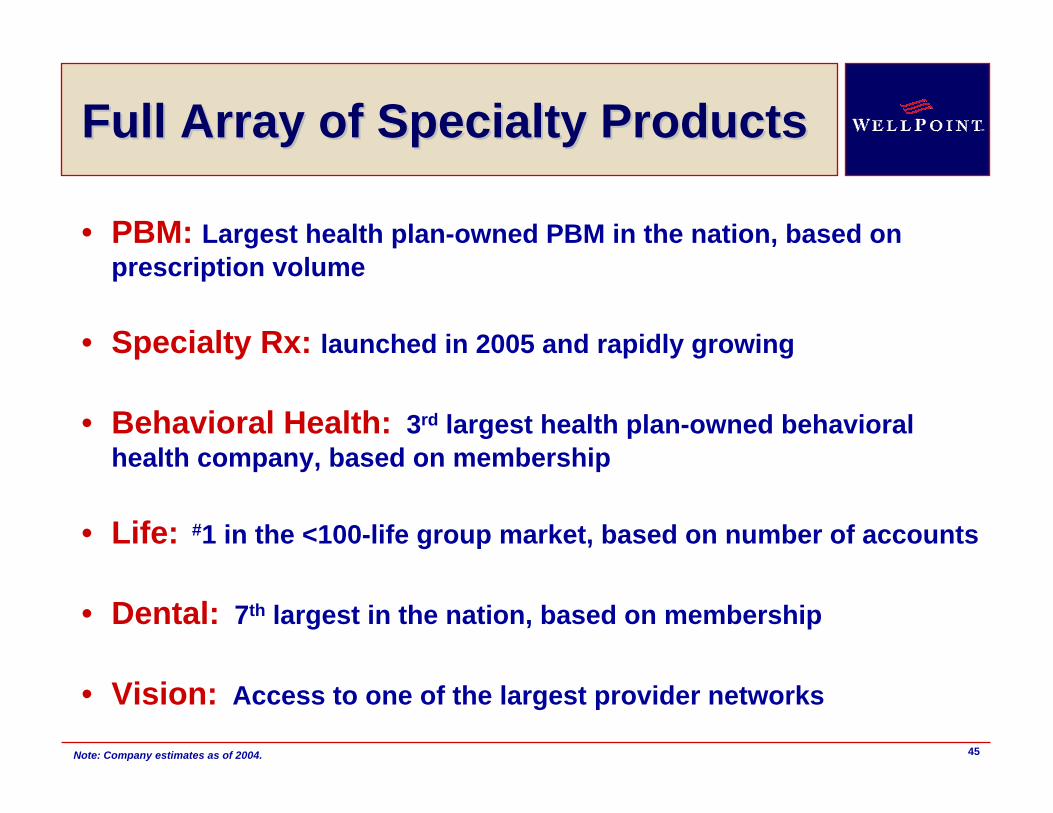

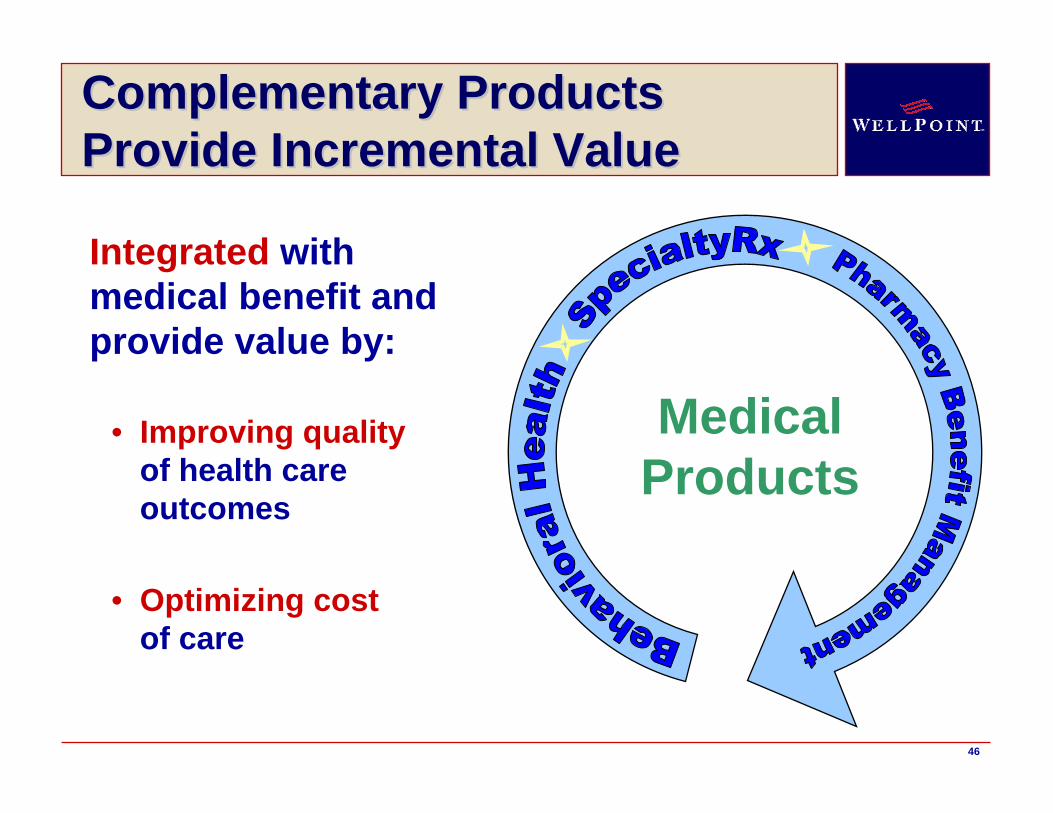

• PBM: Largest health plan-owned PBM in the nation, based on prescription volume

• Specialty Rx: launched in 2005 and rapidly growing

• Behavioral Health: 3rd largest health plan-owned behavioral health company, based on membership

• Life: #1 in the <100-life group market, based on number of accounts

• Dental: 7th largest in the nation, based on membership

• Vision: Access to one of the largest provider networks

Full Array of Specialty Products Full Array of Specialty Products

Note: Company estimates as of 2004.

46

Integrated with medical benefit and provide value by:

• Improving qualityof health care outcomes

• Optimizing cost of care

Medical Products

Complementary Products Complementary Products Provide Incremental ValueProvide Incremental Value

47

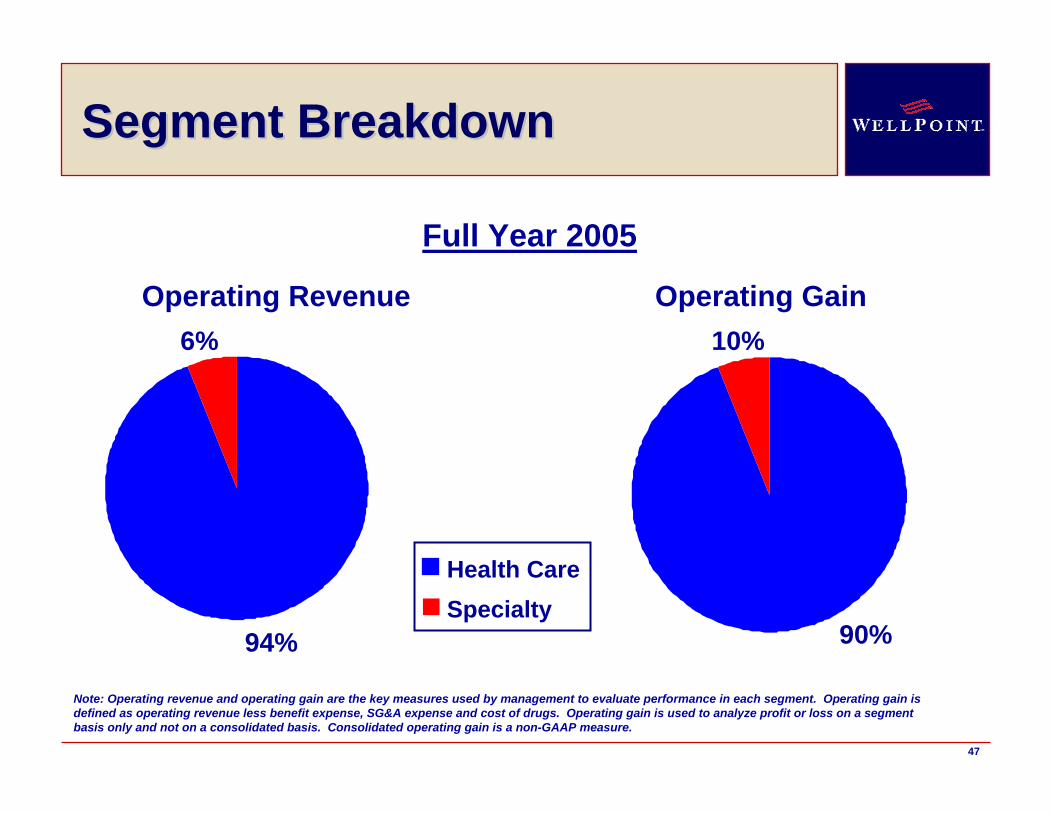

Segment Breakdown Segment Breakdown

94%

6% 10%

90%

Health CareSpecialty

Operating Revenue Operating Gain

Note: Operating revenue and operating gain are the key measures used by management to evaluate performance in each segment. Operating gain is defined as operating revenue less benefit expense, SG&A expense and cost of drugs. Operating gain is used to analyze profit or loss on a segment basis only and not on a consolidated basis. Consolidated operating gain is a non-GAAP measure.

Full Year 2005

48

WellPoint Growth ModelWellPoint Growth Model

EPS GrowthEPS Growth15% +15% +

Profitable Enrollment Growth

Disciplined Focus on Underwriting

Effective Use of Cash Flow

SG&A Ratio Reduction

Specialty Penetration

49

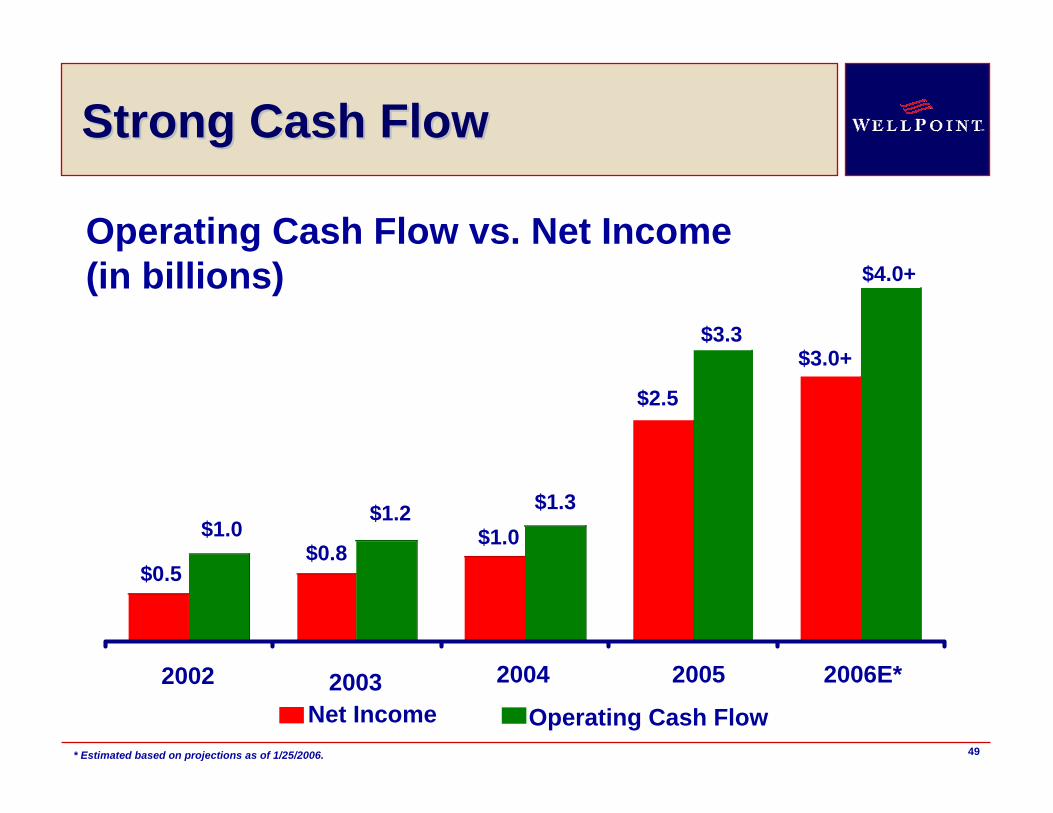

Strong Cash FlowStrong Cash Flow

2002 2003 2004Net Income Operating Cash Flow

$0.5

$1.0$0.8

$1.2$1.0

$1.3

$3.3

$2.5

2005

Operating Cash Flow vs. Net Income(in billions)

* Estimated based on projections as of 1/25/2006.

2006E*

$3.0+

$4.0+

50

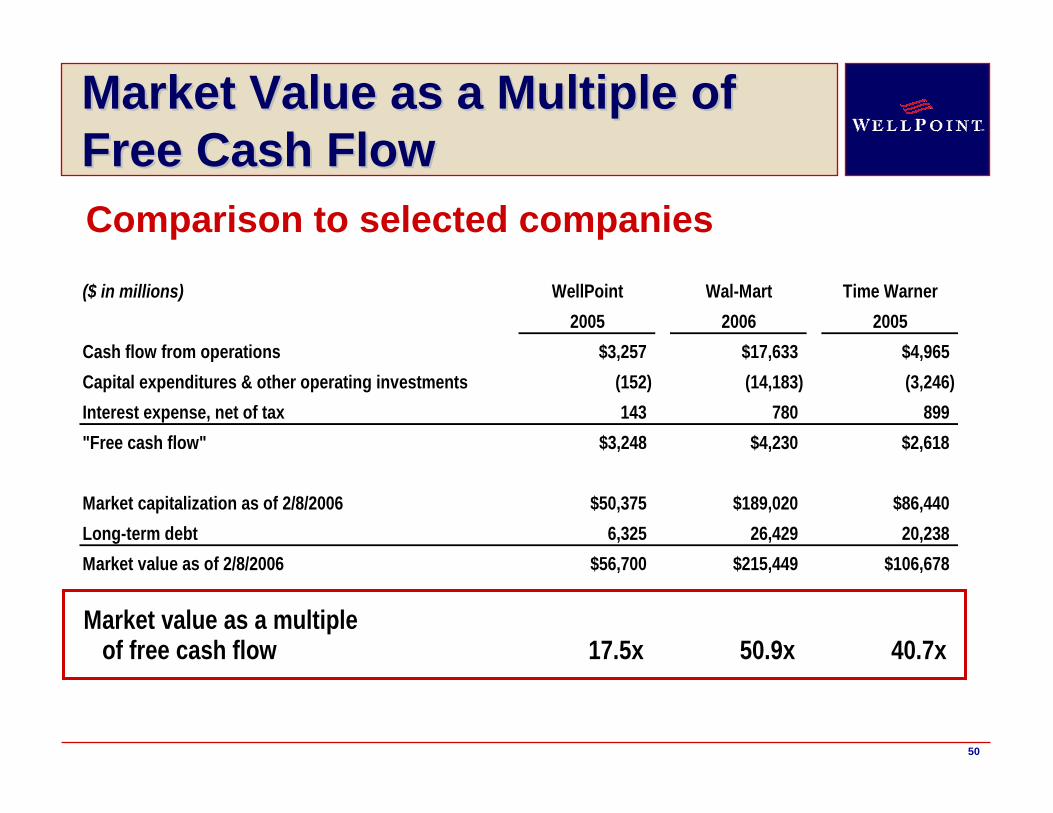

Market Value as a Multiple of Market Value as a Multiple of Free Cash Flow Free Cash Flow Comparison to selected companies

($ in millions) WellPoint Wal-Mart Time Warner2005 2006 2005

Cash flow from operations $3,257 $17,633 $4,965Capital expenditures & other operating investments (152) (14,183) (3,246) Interest expense, net of tax 143 780 899 "Free cash flow" $3,248 $4,230 $2,618

Market capitalization as of 2/8/2006 $50,375 $189,020 $86,440Long-term debt 6,325 26,429 20,238 Market value as of 2/8/2006 $56,700 $215,449 $106,678

Market value as a multiple of free cash flow 17.5x 50.9x 40.7x

51

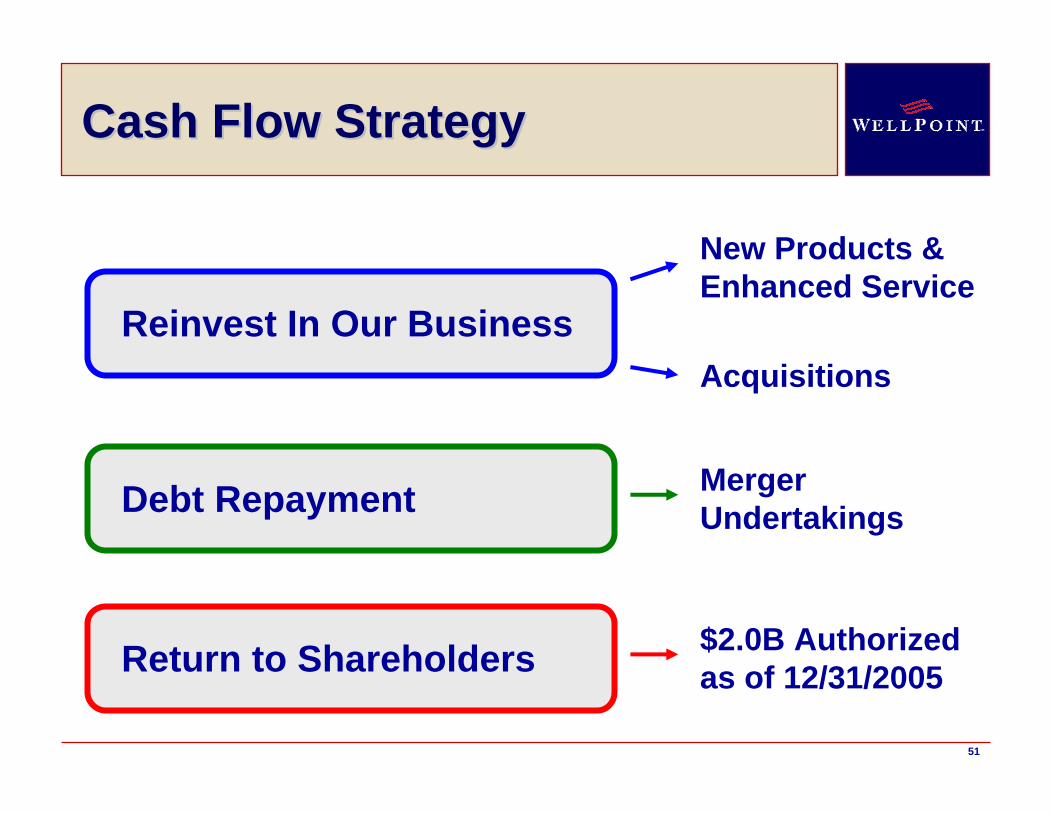

Cash Flow StrategyCash Flow Strategy

Reinvest In Our Business

New Products & Enhanced Service

Debt Repayment

Acquisitions

Return to Shareholders

Merger Undertakings

$2.0B Authorized as of 12/31/2005

52

AgendaAgenda

• WellPoint Profile & Success

• Superior Value Proposition

• Revenue Growth Opportunities

• 15% EPS Growth Target

• Investment Considerations

53

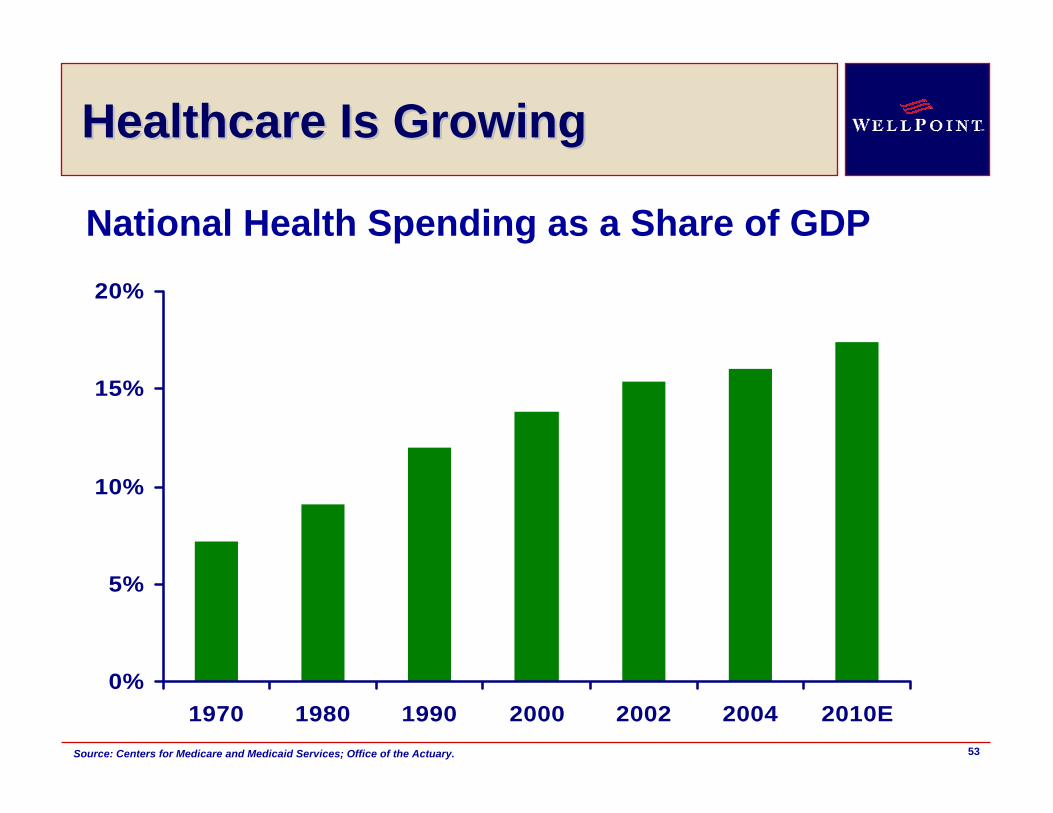

Healthcare Is GrowingHealthcare Is Growing

0%

5%

10%

15%

20%

1970 1980 1990 2000 2002 2004 2010E

National Health Spending as a Share of GDP

Source: Centers for Medicare and Medicaid Services; Office of the Actuary.

54

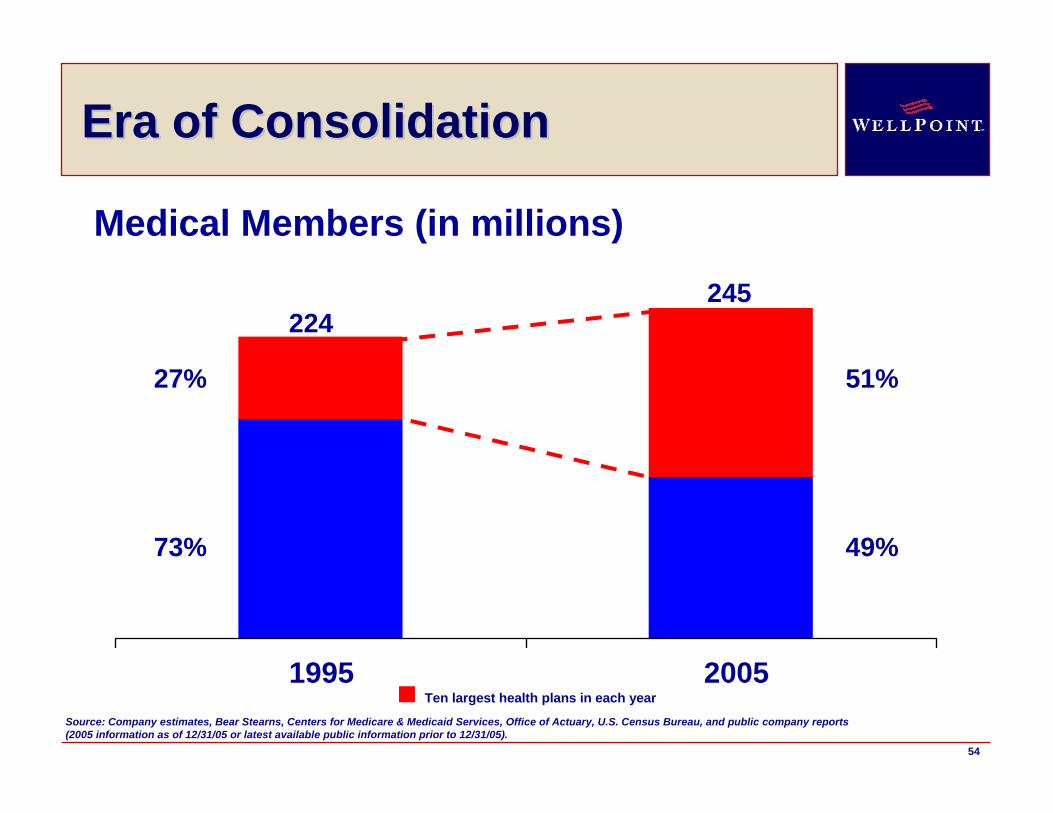

Era of ConsolidationEra of Consolidation

Ten largest health plans in each year1995 2005

27%

73%

51%

49%

224 245

Medical Members (in millions)

Source: Company estimates, Bear Stearns, Centers for Medicare & Medicaid Services, Office of Actuary, U.S. Census Bureau, and public company reports (2005 information as of 12/31/05 or latest available public information prior to 12/31/05).

55

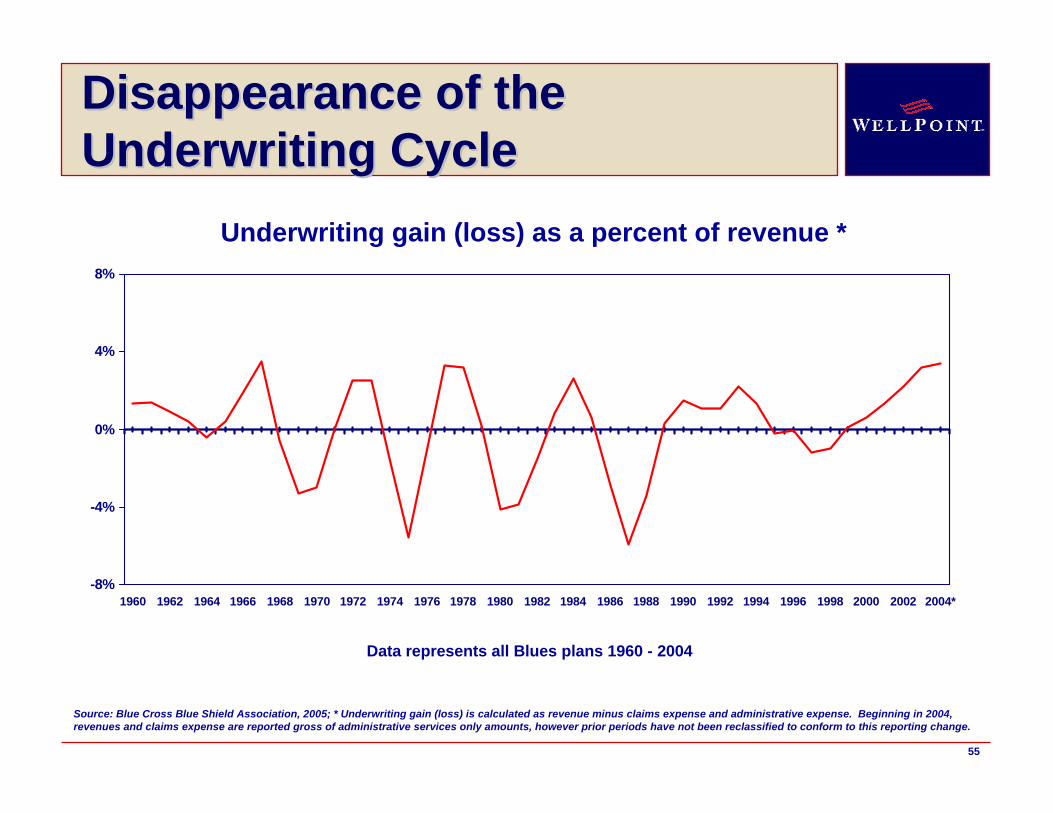

-8%

-4%

0%

4%

8%

1960 1962 1964 1966 1968 1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004*

Underwriting gain (loss) as a percent of revenue *

Source: Blue Cross Blue Shield Association, 2005; * Underwriting gain (loss) is calculated as revenue minus claims expense and administrative expense. Beginning in 2004, revenues and claims expense are reported gross of administrative services only amounts, however prior periods have not been reclassified to conform to this reporting change.

Data represents all Blues plans 1960 - 2004

Disappearance of the Disappearance of the Underwriting CycleUnderwriting Cycle

56

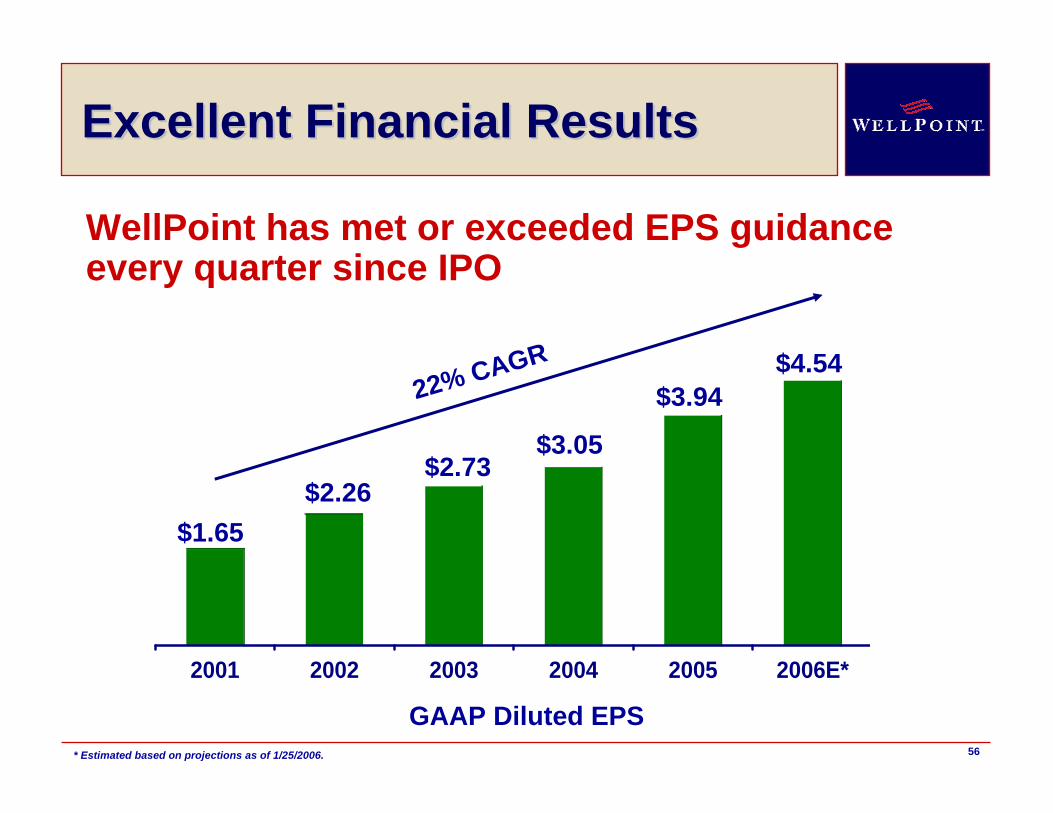

Excellent Financial ResultsExcellent Financial Results

2001 2002 2003 2004 2005 2006E*

$1.65$2.26

$2.73$3.05

$4.5422% CAGR

$3.94

WellPoint has met or exceeded EPS guidance every quarter since IPO

* Estimated based on projections as of 1/25/2006.

GAAP Diluted EPS

57

Compelling Value PropositionCompelling Value Proposition

WWide-reaching, cost-effective provider networksEExcellent financial performance LLarge local market shares with revenue diversityLLeading brand in the sector PPositive cash flow in excess of net incomeOOutstanding management teamIIntegration discipline and success for M&ANNation’s largest health plan membershipTTremendous industry with growth opportunities

58