sg cowen technology conference wednesday, … · safe harbor statement under the private securities...

TRANSCRIPT

SG Cowen Technology ConferenceWednesday, September 3, 2003

Safe Harbor Statement

Under the Private Securities Litigation Reform Act of 1995:

Except for historical information, the matters discussed in this presentationthat may be considered forward-looking statements may be subject to

certain risks and uncertainties that could cause the actual results to differmaterially from those projected, including uncertainties in the market,

pricing, competition, procurement and manufacturing efficiencies,and other risks detailed from time to time in the Company’s SEC reports.

The Company assumes no obligation to update the information in this presentation.

Corporate Overview

Technology Leaders Face a Rapidly Changing Landscape

Faster rates of end market changeAlliances & relationships increase strategic advantageCustomer loyalty & diversification key to sustainable growthCustomization increases value of products & servicesOutsourcing trends continue

Shorter Product Life

Cycles

Relationships Broadening

Consolidation

Global IndustryMaturing

Lower Cost

Structure

ChangingBusiness

Landscape

Photronics’ Core Values Define Success

Flexibilit

y

Technology

Speed

Cost

Technical Diversity and Investment

PLAB FY03 YTD vs. WW IC Rankings 02

4 of Top 5Asia-Pac

2 of Top 3Europe

3 of Top 5NA

3 of Top 5WW

PLABCustomers

Region

Thin FilmHead

Semiconductor

Photonics

Other Electronic

MarketsFlat Panel

DisplayGlobal Markets

Research and Development

$0$5

$10$15$20$25$30$35

1998 1999 2000 2001 20020.0%1.0%2.0%3.0%4.0%5.0%6.0%7.0%8.0%9.0%

R&D Expense % of Sales

Company Sites

Under Construction

Source: IC Insights, 2002 Final IC Ranking vs. PLAB YTD through Q3FY03

Speed and Flexibility Pacing Industry and Regional Dynamics

Source: Dataquest & IC Insight, LSI & INTEL, ITRS Roadmap, SIA June03

DRAM47%/Year

INTEL MPU42%/Year

Flash57%/Year

LSI ASIC47%/Year

SIA Total Semiconductor Forecast

20000

30000

40000

50000

60000

70000

80000

90000

2003 2004 2005 2006

$ in

Mill

ions

NA Europe Japan AsiaPac

Projected Fab Capacity <.20 Micron

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2002-2006

8" W

afer

Equ

ivalen

ts

AP EUR JPN NAITRS Line Width Trend Chart

5060708090

100110120130140

2001 2002 2003 2004 2005 2006 2007

Nod

e (n

m)

Year of Production

Shifting Sands

Efficiency…The Value EquationInnovative & Cost Effective Solutions

Extending Optical LithographyPhase Shift & OPC Masks

Simulation Modeling

Extending Technology

Multi-Market FlexibilityLeading Edge and Mature Technologies

Nano-Technology Lines

StreamlinedManufacturing

Customer InterfaceMask PilotTM

CyberMaskTMAutomation

Localized ManufacturingAdvanced Global R/DStrategic Expansion

Globalization

Global OverviewRegional Highlights

Global Shift in Demand

10%

70%

2000 Q1:0320022001Region

40%47%69% Domestic

43%34%19%Asia

Global Sales Mix

18%

72%

2000 Q3:0320022001Region

41%50%64% NA

16%16%17%Europe

Global Sales Mix

Asian Business Environment

Foundries dominate Asian landscape130nm production release• Focus is on improving 130nm yields• There is a pipeline of designs processed on MPW sets

that have not yet become production orders90nm test chips beginning to rampIDM’s continue pursuing fablite and fabless

strategiesFlat Panel Display market showing healthy

growth

European Business Environment

Regional economic pressures abatingFlat market in 2003, share gains drive growth

Partnerships at Leading Edge• Crolles II - a $5.7bn investment shared between ST, Philips and

Motorola

3 of World’s Top 10 IDMs committed to Europe

North America Business EnvironmentBusiness model is shifting as an increasing number of IDM’s pursue a fablite and/or fabless strategy Pricing environment is stable• Today, Photronics is pursuing opportunities to increase

prices, even among certain mature technology customers

Leverage technology position with process driven customers

Technology Update

A Focused Approach to Tech Leadership

Technology

Partners

hips

Global

Development

Model

Focused core

technology

Market Driven

Tech Leadership

Positioned to take advantage...

Photronics brings efficiency to design & fabrication ofhigh performance IC’s by leading theIntegration of the Lithography Plane

Proven track record of increasing the pace of developmentbeing applied to 90nm and 65nm nodes

Have the most extensive global leading-edge capability

Have industry leading automation backplane

Financial Highlights

Photronics Financial HighlightsBenefit from technology driven demandMultiple sources of margin leverage• Improving mix shift & stable pricing• Global presence

Increased global market shareImproved liquidityStrategically scaled infrastructure

5 Year Revenue Growth

$269.3 $277.4$331.2

$378.0 $387.0

$0

$100

$200

$300

$400

$500

Net

Sal

es ($

M)

1998 1999 2000 2001 2002

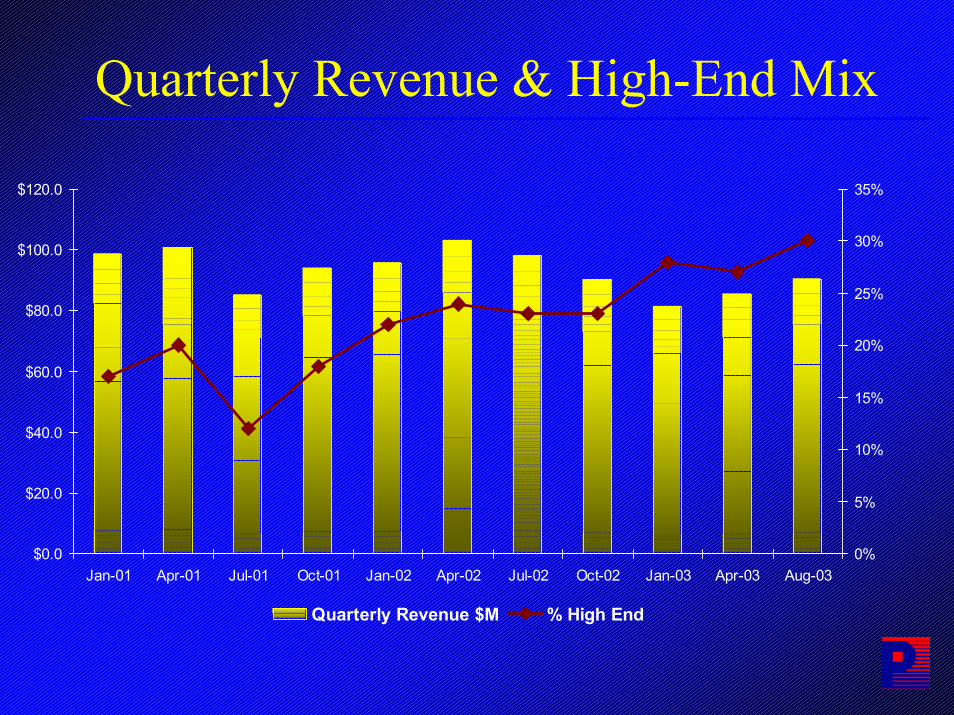

Quarterly Revenue & High-End Mix

$0.0

$20.0

$40.0

$60.0

$80.0

$100.0

$120.0

Jan-01 Apr-01 Jul-01 Oct-01 Jan-02 Apr-02 Jul-02 Oct-02 Jan-03 Apr-03 Aug-030%

5%

10%

15%

20%

25%

30%

35%

Quarterly Revenue $M % High End

Operating Income (Recent Quarters)(excludes consolidation and restructuring charges)

$16.0 $17.1

$5.2 $6.8 $7.0

$9.6

$5.3

$0.4 -$4.4$0.6

$7.5

$0

$5

$10

$15

$20

Jan-01

Apr-01

Jul-01

Jan-02

Jan-

03

Oct-01

Jul-0

2

Apr-02

Oct-02

Ope

ratin

g In

com

e

Apr-03

Aug-03

Improving Liquidity Solid Financial Position

$ millions

November 3, August 3,2002 2003

Cash and Short Term Investments $129 $211

Working Capital $142 $246

Current Ratio 2.3:1 4.2:1

Total Assets $852$832

Long Term Debt $380$297

Equity $297$339

Cash Flow Highlights$ millions

Fiscal YearEnded 2002

Capital Expenditures

Free Cash Flow

(35)

$7

Operations $ 42$ 136

(126)Acquisitions of Photomask Operations ––

$10

Net Issuance of Convertible Debt

Net Repayment of Debt

Other, Net

Increase (Decrease) in Cash and Investments

(73)

2

($81)

193

(115)

(6)

$94

145

First Nine Months 2003

Short-Term Financial Goals

Increase shareholder value

Maximize liquidity

Generate free cash flow

De-lever balance sheet

Improve gross and operating margins

Increase high-end mix

Sustainable profitability

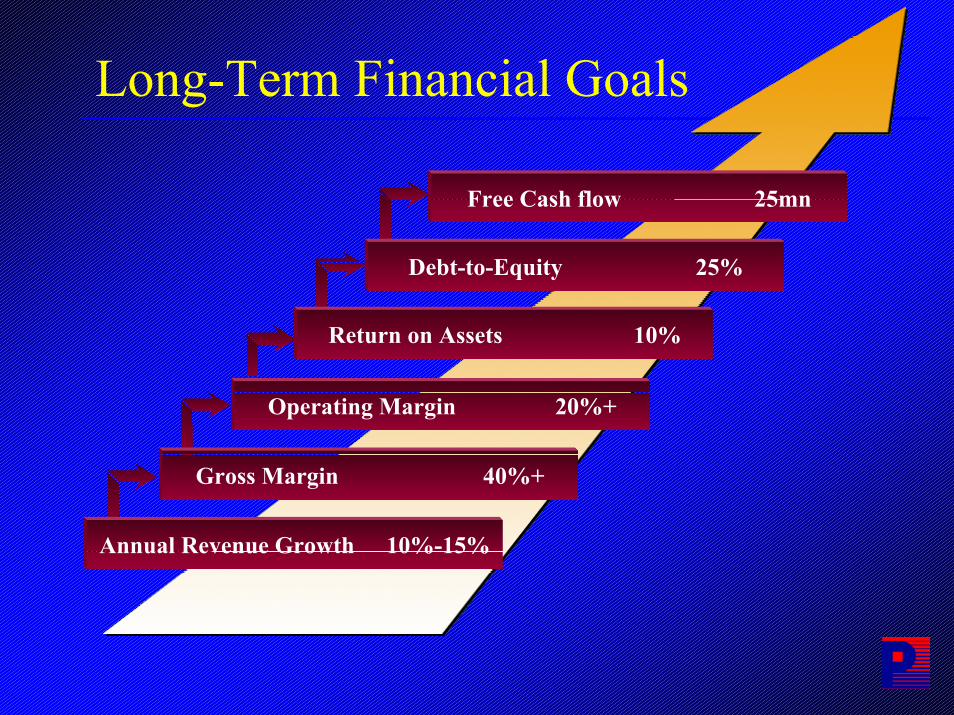

Long-Term Financial Goals

Gross Margin 40%+

Operating Margin 20%+

Annual Revenue Growth 10%-15%

Return on Assets 10%

Debt-to-Equity 25%

Free Cash flow 25mn

Summary

Meeting Today’s Market Demands

ShareholderValue

Global

CustomerLoyalty

Responsive

Connected(Automated)

Flexible

Integrating the

Lithography Plane

SG Cowen Technology ConferenceWednesday, September 3, 2003