session 7: capital structure c15.0008 corporate finance topics

Post on 22-Dec-2015

219 views

TRANSCRIPT

Session 7: Capital Structure

C15.0008 Corporate Finance Topics

Outline

• Distress costs

• Agency conflicts

• Finding the optimal capital structure

Financial Distress Costs

• Direct costs– Lawyers, accountants, consultants fees– Forced asset sales

• Indirect costs– Wasted time and energy– Deterioration of reputation and customer,

supplier, and employee relationships

• Total ~10-20% of firm value

Agency Conflicts

• Bondholders vs. stockholders (managers)– Occur when debt is risky– Stockholders control the firm

• Management vs. stockholders– Occur when corporate governance system

does not work perfectly– Managers can misuse the firms assets

Stockholder Incentives

• Take risk, i.e., undertake high risk (possibly negative NPV) projects

• Under-invest, i.e., reject positive NPV projects that require equity investment

• Pay dividends, i.e., distribute wealth to shareholders

Agency Costs

Since the market is smart, bondholders anticipate future actions and demand protection up front• Bond covenants (restrict the actions of managers and may reduce value)• Higher promised payments• These are all costs to the firm

Valuation Implications

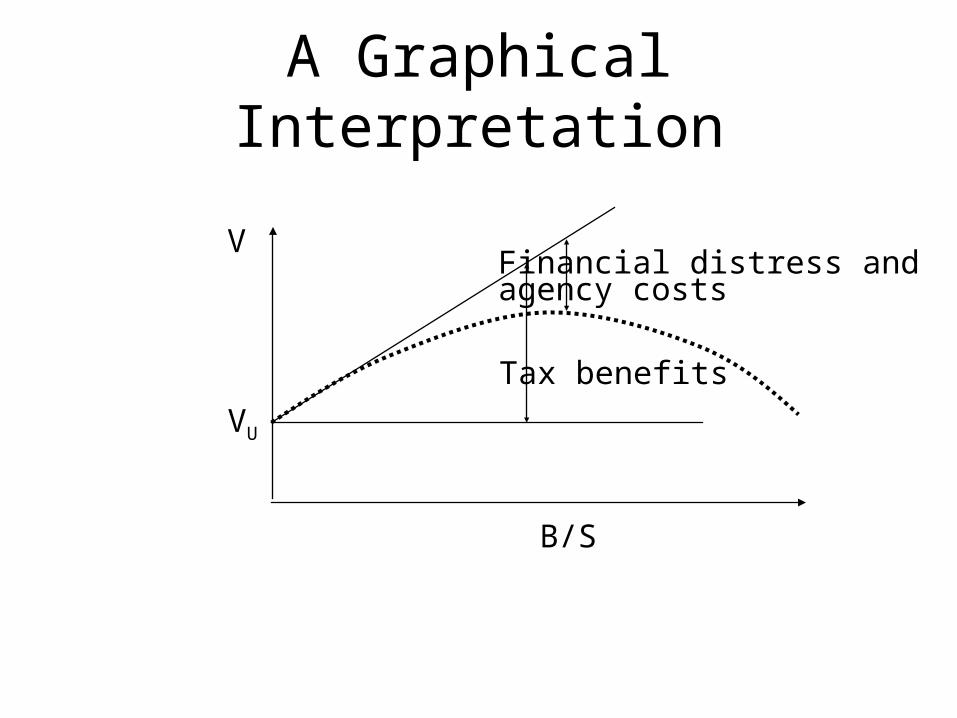

VL = VU + PV(tax shield) - PV(financial distress costs) - PV(agency costs)Financial distress and agency costs (bondholder vs. stockholder) increase as the amount of debt increases.Optimal capital structure trades off the tax benefits of debt with financial distress and agency costs.

A Graphical Interpretation

V

B/S

VU

Tax benefits

Financial distress and agency costs

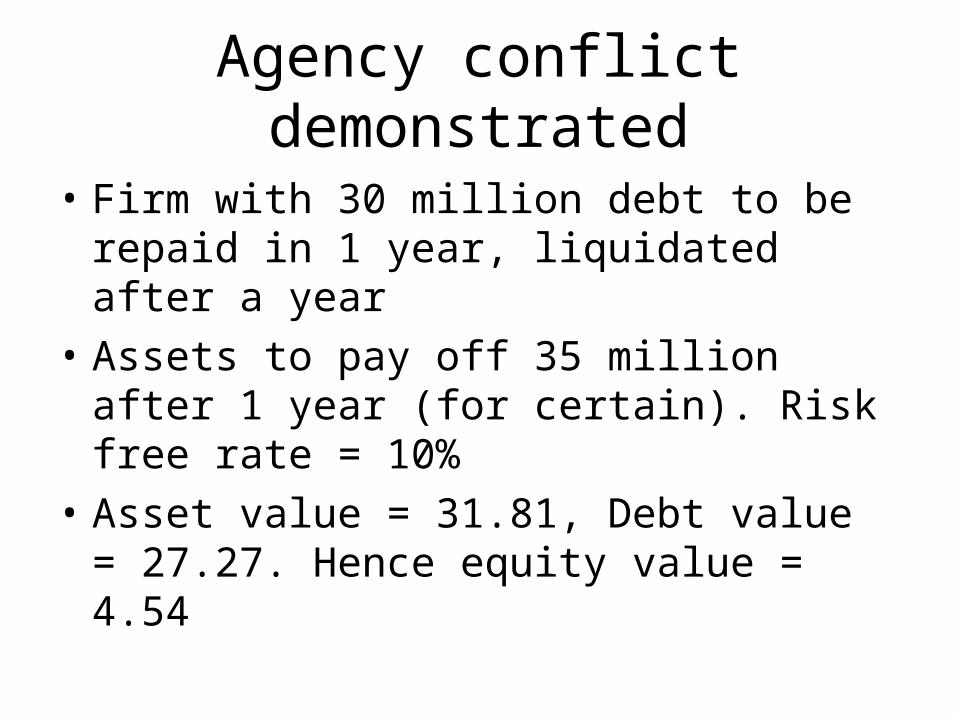

Agency conflict demonstrated

• Firm with 30 million debt to be repaid in 1 year, liquidated after a year

• Assets to pay off 35 million after 1 year (for certain). Risk free rate = 10%

• Asset value = 31.81, Debt value = 27.27. Hence equity value = 4.54

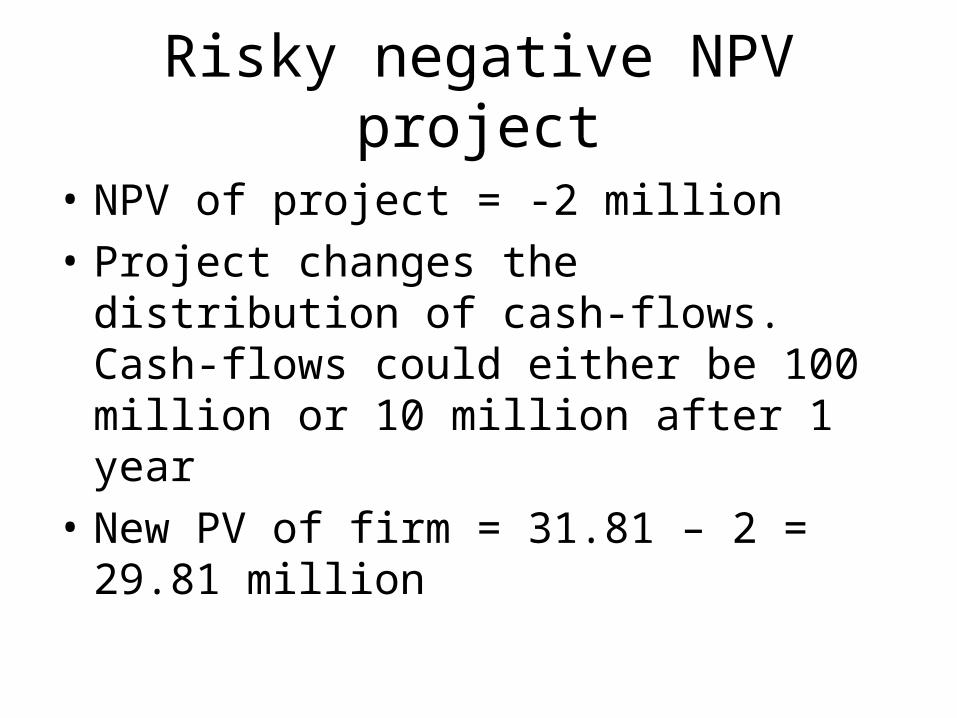

Risky negative NPV project

• NPV of project = -2 million

• Project changes the distribution of cash-flows. Cash-flows could either be 100 million or 10 million after 1 year

• New PV of firm = 31.81 – 2 = 29.81 million

Equity Pay-off

• H = 0.72

• B = 6.56

• Equity value = 14.96 : It increased, even though firm value decreased!

S

65

0

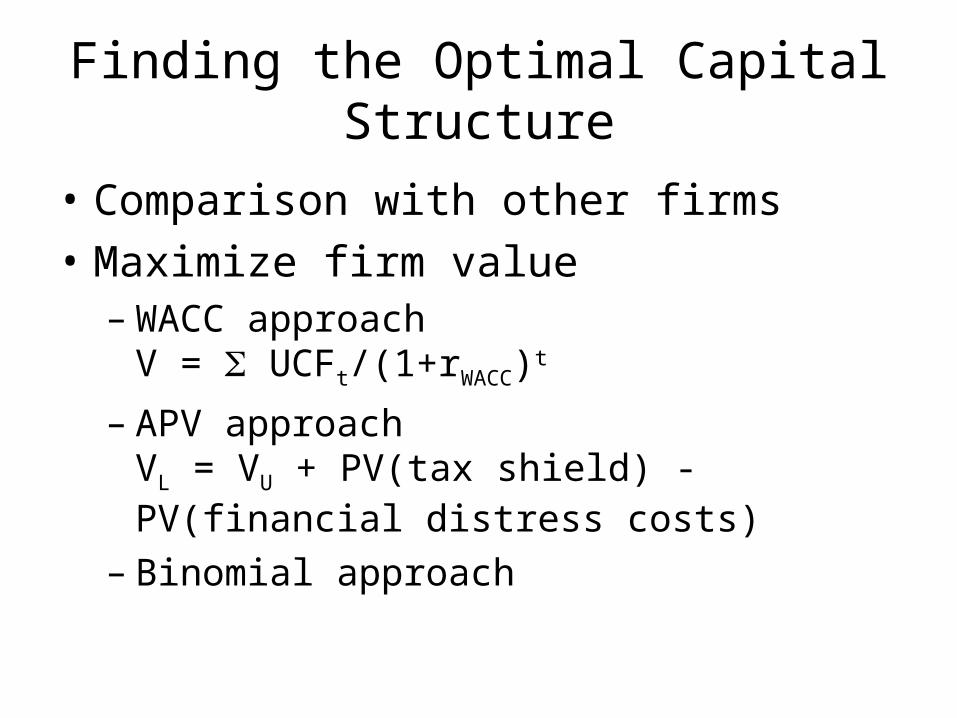

Finding the Optimal Capital Structure

• Comparison with other firms

• Maximize firm value– WACC approach

V = UCFt/(1+rWACC)t

– APV approachVL = VU + PV(tax shield) - PV(financial distress costs)

– Binomial approach

The WACC Approach

V = UCFt/(1+rWACC)t

UCF = EBIT(1-T) + depreciation – capex – nwc• Calculate WACC at various debt levels

– rB from debt rating via interest coverage and leverage ratios

– rS from Prop. IIrS = r0 + (1- TC)(B/S)(r0 - rB)

– WACC = (B/(S+B)) rB(1-T)+(S/(S+B)) rS

• Adjust expected cash flows for financial distress costs

Example

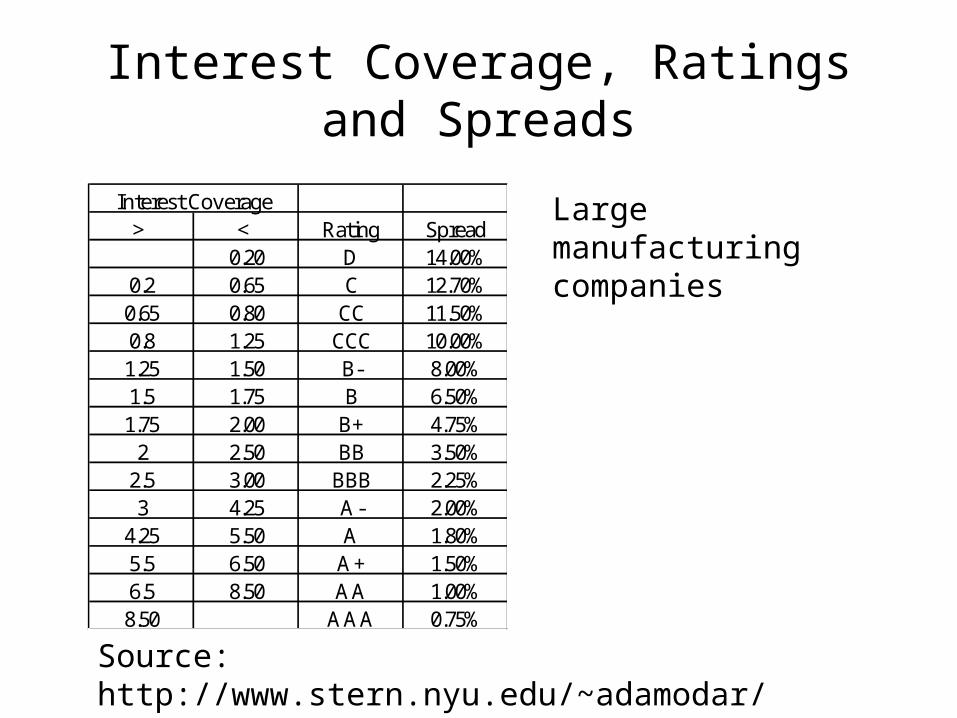

Interest Coverage, Ratings and Spreads

Interest Coverage> < Rating Spread

0.20 D 14.00%0.2 0.65 C 12.70%0.65 0.80 CC 11.50%0.8 1.25 CCC 10.00%1.25 1.50 B- 8.00%1.5 1.75 B 6.50%1.75 2.00 B+ 4.75%

2 2.50 BB 3.50%2.5 3.00 BBB 2.25%3 4.25 A- 2.00%

4.25 5.50 A 1.80%5.5 6.50 A+ 1.50%6.5 8.50 AA 1.00%8.50 AAA 0.75%

Large manufacturing companies

Source: http://www.stern.nyu.edu/~adamodar/

Issues with the WACC Approach

• How big is the cash flow adjustment?

• You get a tax shield on interest expenses only

as long as you are making a profit and are

paying taxes.

• Financial distress costs and tax shields have

option like pay-offs.

The APV Approach

VL = VU + PV(tax shield) - PV(financial distress costs)

• PV(tax shield) = t [TC(interest expense)t] / (1+ rB)t

– The expected tax rate decreases as debt increases

• PV(financial distress costs) =

Prob * PV(financial distress costs | financial distress)

– The probability increases as the debt rating declines

– Cost are usually estimated as a percentage of pre-distress firm

value (~10-20%)

• Financial distress costs and tax shields have option like payoffs

Ratings and Default Risk

Rating Default RiskAAA 0.01%AA 0.28%A+ 0.40%A 0.53%A- 1.41%BBB 2.30%BB 12.20%B+ 19.28%B 26.36%B- 32.50%CCC 46.61%CC 52.50%C 60%D 75%

Source: http://www.stern.nyu.edu/~adamodar/

Rating ProbAAA 0.03%AA 0.55%A 0.78%BBB 9.33%BB 20.03%B 38.19%CCC 54.88%

Source: Altman, 1971-2002

Time Series of Default Rates

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

Year

Def

ault

Rat

e

% of high yield bonds defaulting in a given year

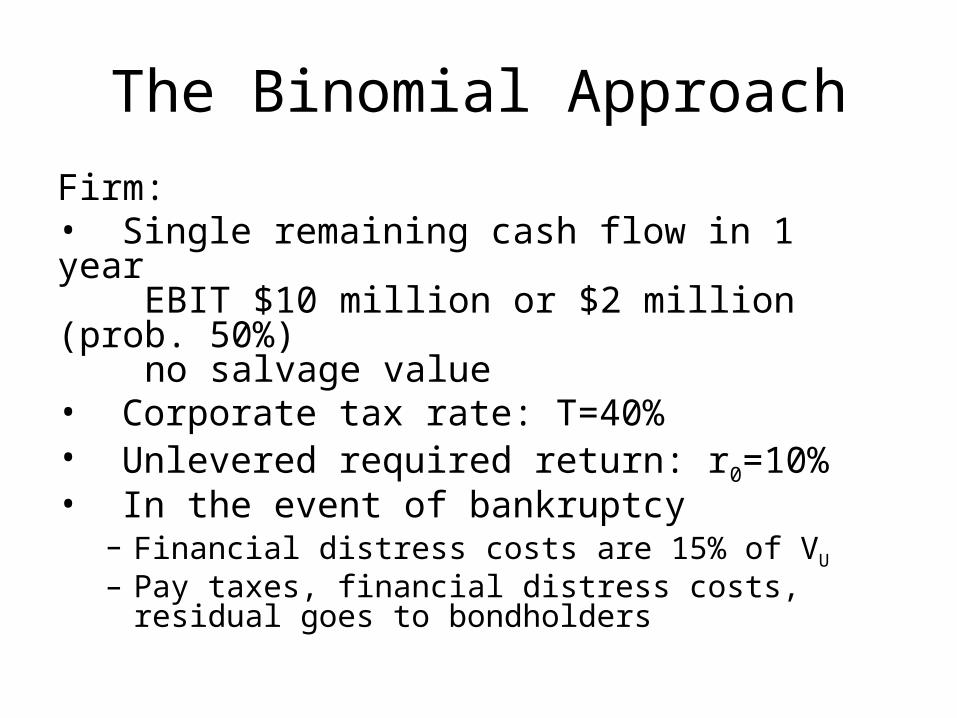

The Binomial Approach

Firm:• Single remaining cash flow in 1 year EBIT $10 million or $2 million (prob. 50%) no salvage value• Corporate tax rate: T=40%• Unlevered required return: r0=10%• In the event of bankruptcy

– Financial distress costs are 15% of VU

– Pay taxes, financial distress costs, residual goes to bondholders

The Unlevered Firm

VU = S

Liquidating dividend is only cash flow

Value via DCF

[0.5(6)+0.5(1.2)]/1.1=3.27

EBIT(1-T)=10(1-0.4)=6

EBIT(1-T)=2(1-0.4)=1.2

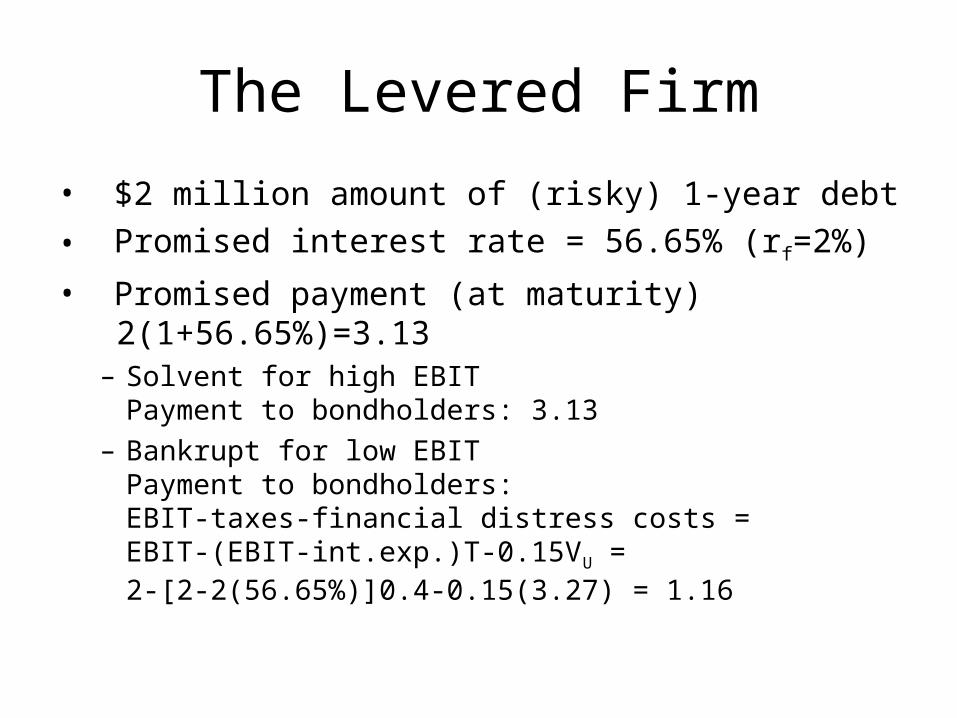

The Levered Firm

• $2 million amount of (risky) 1-year debt

• Promised interest rate = 56.65% (rf=2%)

• Promised payment (at maturity) 2(1+56.65%)=3.13

– Solvent for high EBITPayment to bondholders: 3.13

– Bankrupt for low EBITPayment to bondholders:EBIT-taxes-financial distress costs = EBIT-(EBIT-int.exp.)T-0.15VU = 2-[2-2(56.65%)]0.4-0.15(3.27) = 1.16

Debt Value

H=0.41, B*=-0.656, B=2 (trading at par!!)

B

3.13

1.16

Replicate using the unlevered firm (rf=2%)

3.27

6

1.2

Equity Value

H=0.69, B*=0.814, S=1.45 rS=14.49%

S

(EBIT-56.65%(B))(1-T)-B=3.32

0

Replicate using the unlevered firm (rf=2%)

3.27

6

1.2

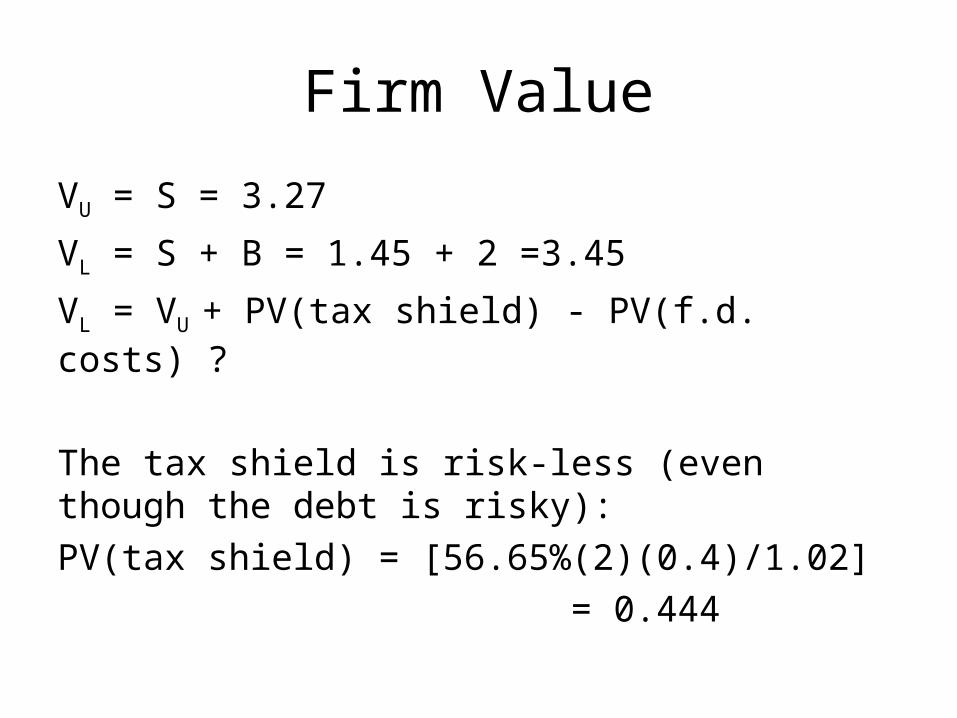

Firm Value

VU = S = 3.27

VL = S + B = 1.45 + 2 =3.45

VL = VU + PV(tax shield) - PV(f.d. costs) ?

The tax shield is risk-less (even though the debt is risky):

PV(tax shield) = [56.65%(2)(0.4)/1.02]

= 0.444

Financial Distress Costs

H = -0.102, B* = -0.602, FD = 0.267

VL = VU + PV(tax shield) - PV(f.d. costs) = 3.27 + 0.444 - 0.267 = 3.45

FD

0

0.491

Replicate using the unlevered firm (rf=2%)

3.27

6

1.2

Assignments

• Chapter 18

• Problems 18.6,18.14, 18.16

• Problem set 3 due in 1 week