special topics in banking & finance ch 7

DESCRIPTION

Dr. Karim KobeissiTRANSCRIPT

Special Topics In Banking & Finance

Dr. Karim KobeissiArts, Sciences and Technology University in Lebanon

Chapter 7: Risk Management in Financial Institutions

Keyword: Risk Management

The process of identification, analysis and either

accept or reduce the level of uncertainty in

investment decision-making.

Introduction

Managing financial institutions has never been an easy

task. But, uncertainty in the economic environment has

increased, making the job of the financial institution

manager much harder specifically when it comes to

managing credit risk and interest-rate risk. In this

chapter, we explore the tools available to managers to

measure these risks and strategies to reduce them.

Managing Credit Risk

• A major part of the business of financial institutions is making loans, and the major risk with loans is that the borrow will not repay.

• Credit risk is the risk that a borrower will not repay a loan according to the terms of the loan, either defaulting (failure to pay) entirely or making late payments of interest or principal.

Managing Credit Risk (con)

The concepts of moral hazard and adverse

selection will provide our framework to

understand the principles financial managers

must follow to minimize credit risk, yet make

successful loans.

Asymmetric Information

In financial markets, one party often does not know enough about the other party to make accurate decisions. This inequality is called asymmetric information. For example, a borrower who takes out a loan has better information about the potential returns and risks associated with investment projects than the lender does. Lack of information creates problems in the financial system on two fronts: before the transaction is entered into and after.

Managing Credit Risk (con)

• Moral hazard is the problem created by asymmetric

information after the transaction occurs. It is the risk

(hazard) that the borrower might engage in activities that

are bad (immoral) from the lender’s point of view because

the borrower might not pay back the loan.

• Adverse selection is a problem in the market for loans

because those with the highest credit risk have the biggest

incentives to borrow from others.

Managing Credit Risk (con)

• Solving The Moral Hazard Problem: Financial managers have a number of tools available to assist

in reducing or eliminating the asymmetric information problem:

1. Screening and Monitoring:

Collecting reliable information about prospective

borrowers. Screening and monitoring also involves

requiring certain actions, or prohibiting others.

Managing Credit Risk (con)

• Specialization in Lending helps in screening.

This has lead some institutions to specialize

in regions or industries, gaining expertise in

evaluating particular firms or individuals. It

allows financial institutions to better predict

problems by having in depth knowledge.

Managing Credit Risk (con)

• Monitoring and Enforcement also helps.

Financial institutions write protective clauses

into loans contracts and actively monitor

them to ensure that borrowers are

complying with these articles.

Managing Credit Risk (con)

2. Long-term Customer Relationships:

Past information contained in checking accounts, savings

accounts, and previous loans provides valuable

information to more easily determine credit

worthiness.

3. Collateral:

A guarantee of property or other assets that must be

surrendered if the terms of the loan are not met ( the

loans are called secured loans).

M a n a g i n g C r e d i t R i s k ( c o n )

4. Compensating Balances:

Reserves that a borrower must maintain in an account that act as collateral should the

borrower default.

5. Questioning the substance of the borrowers’ transaction not just the form:

Substance over form is an accounting principle used "to ensure that financial

statements give a complete, relevant, and accurate picture of transactions and

events". If an entity practices the 'substance over form' concept, then the

financial statements will show the overall financial reality of the entity

(economic substance), rather than the legal form of transactions (form).

Substance over form is critical for reliable financial reporting. It is particularly

relevant in cases of revenue recognition, sale and purchase agreements, etc. The

key point of the concept is that a transaction should not be recorded in such a

manner as to hide the true intent of the transaction, which would mislead the

readers of a company's financial statements.

M a n a g i n g C r e d i t R i s k ( c o n )

• Solving The Adverse Selection Problem:This problem can be solved by avoiding high risk customers

(Credit Rationing). More risk sometimes means more interest revenue but most of the time it will lead to default on payments. Consequently, lenders will:

(1) Refuse to lend to some borrowers, regardless of how much interest they are willing to pay, or

(2) Only finance part of a project, requiring that the remaining part come from equity financing.

Managing Interest-Rate Risk

Interest-rate risk refers to the risk that a security’s

value will change due to a change in interest rates.

For example, Let's assume the bank purchased a bond from

Company XYZ. Because bond prices typically fall when

interest rates rise, an unexpected increase in interest rates

means that the investment (bond) could suddenly lose

value. If the bank expect to sell the bond before it matures,

this could mean that the bank will end up selling the bond

for less than paid for it (a capital loss).

Managing Interest-Rate Risk

• Financial institutions, banks in particular, specialize

in earning a higher rate of return on their assets

relative to the interest paid on their liabilities.

• As interest rate volatility increased in the last 20

years, interest-rate risk exposure has become a

concern for financial institutions.

Managing Interest-Rate Risk

• To see how financial institutions can measure and manage interest-rate risk exposure, we will examine the balance sheet for The First National Bank (next slide).

• We will develop two tools, (1) Income Gap Analysis (for short term analysis) and (2) Duration Gap Analysis (for long term analysis), to assist the financial manager in this effort.

Managing Interest-Rate Risk

Income Gap Analysis• Income Gap Analysis: measures the sensitivity of a bank’s current

year net income to changes in interest rate.

• For the financial institution manager, the first step in assessing

interest-rate risk is to decide which assets and liabilities are rate-

sensitive, that is, which have interest rates that will be reset

(reprised) within the year. Let us note that rate-sensitive assets or

liabilities can have interest rates reprised within the year either

because the debt instrument matures within the year or because the

reprising is done automatically, as with variable-rate mortgages. For

many assets and liabilities, deciding whether they are rate-sensitive is

straight forward.

I n c o m e G a p A n a l y s i s ( c o n )In our example, the obviously rate sensitive assets are securities with

maturities of less than one year ($5 million), variable-rate mortgages ($10 million), and commercial loans with maturities less than one year ($15 million), for a total of $30 million.

However, some assets that look like fixed-rate assets whose interest rates are not reprised within the year actually have a component that is rate-sensitive. Thus these assets are partially, but not fully rate-sensitive. For example, although fixed-rate residential mortgages may have a maturity of 30 years, homeowners can repay their mortgages early by selling their homes or repaying the mortgage in some other way. This means that within the year, a certain percentage of these fixed-rate mortgages will be paid off, and interest rates on this amount will be reprised. From past experience the bank manager knows that 20% of the fixed-rate residential mortgages are repaid within a year, which means that $2 million of these mortgages (20% of $10 million) must be considered rate-sensitive. The bank manager adds this $2 million to the $30 million of rate-sensitive assets already calculated, for a total of $32 million in rate-sensitive assets.

I n c o m e G a p A n a l y s i s ( c o n )

Using a similar procedure, the bank manager could determine the total

amount of rate-sensitive liabilities. The obviously rate-sensitive liabilities

are money market deposit accounts ($5 million), variable-rate CD and CDs

with less than one year to maturity ($25 million), federal funds ($5 million),

and borrowings with maturities of less than one year ($10 million), for a

total of $45 million. Checkable deposits and savings deposits often have

interest rates that can be changed at any time by the bank, although banks

often like to keep their rates fixed for substantial periods. Thus these

liabilities are partially, but not fully rate-sensitive. Suppose that the bank

manager estimates that 10% of checkable deposits ($1.5 million) and 20%

of saving deposits ($3 million) should be considered rate-sensitive. Adding

the $1.5 million and $3 million to the $45 million figure yields a total for

rate-sensitive liabilities of $49.5 million.

I n c o m e G a p A n a l y s i s ( c o n )

• In this moment the bank manager can analyze what will happen if interest rates rise

by 5 percentage points, say, on average from 10% to 15%. The income on the assets

rises by $1.6 million ( = 5% x $32 million of rate-sensitive assets), while the payments

on the liabilities rise by $2.475 million (= 5% x $49.5 million of rate sensitive

liabilities). The First National Bank’s current year net income will now decrease by

$0.875 million (= $1.6 million - $2.475 million).

• Conversely, if interest rates fall by 5%, similar reasoning tells

us that The First National Bank’s current year net income will

now increase by $0.875 million (= -$1.6 million +2.475

million).

• Income Gap Analysis is essentially a short term focus. A

longer-term focus uses duration gap analysis.

I n c o m e G a p A n a l y s i s ( c o n )

This example illustrates the following point:

If a financial institution has more rate-sensitive

liabilities than assets, a rise in interest rates will

reduce the net income and a decline in interest rates

will raise the net income.

Duration Gap Analysis

Bank’s owners and managers not only care

about the impact of interest rate exposure on

current year net income, but they are also

interested in the impact of interest rate

changes on the market value of balance sheet

items and the impact on the bank net worth.

Duration Gap Analysis (con)

• Duration Gap Analysis: measures the sensitivity

of the market value of the bank’s net worth to

changes in interest rates.

• Requires determining the duration for assets and

liabilities, items whose market value will change

as interest rates change. Let’s see how this looks

for The First National Bank.

Durati on GAP Analysis (con)It is important to understand the concept of duration prior

to learning about duration gap analysis. Duration is the average time it takes to receive an

Investment 's Net present value. A zero-Bond with a maturity of 7-years would have a duration of 7-years because it only makes one payment consisting of interest and the principle at the maturity date. However, a coupon-Bond with a maturity of 7-years makes coupon payments throughout the maturity-term, therefore it actually returns portions of the investments net present value sooner than 7 years which shortens its duration.

Duration is a complicated concept but is very useful for companies, especially banks when attempting to immunize their portfolios against interest rate risk.

Durati on GAP Analysis (con)

Duration is additive; that is, the duration of a portfolio of securities is the weighted average of the durations of the individual securities, with the weights reflecting the proportion of the portfolio invested in each.

What this means is that the bank manager can figure out the effect that interest-rate changes will have on the market value of net worth by calculating the average duration for assets and for liabilities and then using those figures to estimate the effects of interest-rate changes.

Duration Gap Analysis

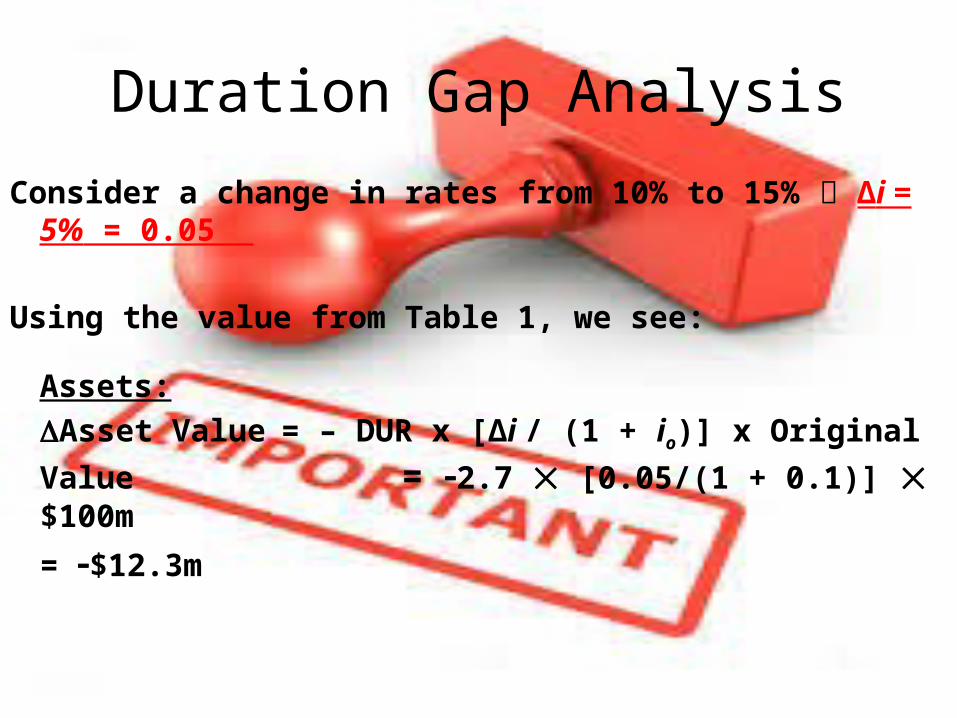

The basic equation for determining the change in market value for assets or liabilities is:

% Change in Value = – DUR x [Δi / (1 + io)]

or

Change in Value = – DUR x [Δi / (1 + io)] x Original Value

Duration Gap Analysis

Consider a change in rates from 10% to 15% Δi = 5% = 0.05

Using the value from Table 1, we see:

Assets:Asset Value = – DUR x [Δi / (1 + io)] x Original Value = 2.7 [0.05/(1 + 0.1)] $100m

= $12.3m

Duration Gap Analysis

Liabilities:Liability Value = – DUR x [Δi / (1 + io)] x Original Value

= 1.03 [0.05/(1 + 0.1)] $95m

= $4.5m

Net Worth:

NW = Assets – Liabilities

NW = $12.3m ($4.5m) = $7.8m

Duration Gap Analysis (con)

• For a rate change from 10% to 15%, the net worth of The First National Bank will fall, changing by $7.8m.

• Recall from the balance sheet that The First National Bank has “Bank capital” totaling $5m. Following such a dramatic change in rate, the capital would fall to $2.8m.

Managing Interest-Rate Risk

• Problems with GAP Analysis– Assumes slope of yield curve unchanged

and flat

– Manager estimates % of fixed rate assets and liabilities that are rate sensitive

Managing Interest-Rate Risk

• Strategies for Managing Interest-Rate Risk

– In general, the interest rate risk can be reduced by

diversifying the durations of the fixed-

income investments that are held at a given time.

– In the example above, shorten duration of bank assets or

lengthen duration of bank liabilities