session 7

TRANSCRIPT

LMT SCHOOL OF MANAGEMENT, THAPAR UNIVERSITYMasters of Business Administration

Course: Financial Reporting and AnalysisFaculty: Dr. Sonia Garg (Email: [email protected])

Session 7: Process of Preparation of Financial Statements for Corporate Entities

Duration: 60 minsSlides: 17

21/04/2023 Process of Preparation of Financial Statements for Corporate Entities

2

Basic Features of CompanyRegistration: Register with the Registrar of Companies under the Companies Act 1956

Registration process involves registration of two important documents• Memorandum of Association: name of company, name of state of registered

office, objects of company, statement of liability, authorized share capital, no. of shares taken by each subscriber

• Articles of Association: Rules for internal management (issue of shares and debentures, rights of members, shareholders’ meetings, appointment of directors, board meetings, buy back, etc)

Preliminary Expenses: expenses incurred in company formation

Board of Directors: Promoters/eminent person who look after the business of the company

21/04/2023 Process of Preparation of Financial Statements for Corporate Entities

3

Types of Companies

Public Limited

• Limited/Ltd.• Minimum 7 members or

shareholders• Can raise capital from public• Minimum 90% subscription

required before allotment

Private Limited

• Private Limited/Pvt. Ltd.• Minimum 2 and maximum

50 shareholders• Kept away from public

domain

21/04/2023 Process of Preparation of Financial Statements for Corporate Entities

4

Example of Shares to be taken by shareholders/members in MoA

21/04/2023 Process of Preparation of Financial Statements for Corporate Entities

5

Share Capital• Authorized Capital: Maximum capital that a company may raise authorized by its

MoA

• Issued Capital: is that part of the authorized capital which the company has actually issued at a given point in time

• Subscribed capital: is that part of the issued capital that has been actually subscribed to by the investors (Co. can go ahead with allotment only if 90% of the issued is subscribed to)

• Called-up capital: is that part of the subscribed capital that the company has actually called on the investors; this may be done in trenches: partly on application, partly on allotment and the balance in one or more calls

• Paid-up capital: is that part of the called-up capital that is fully paid by the investor

21/04/2023 Process of Preparation of Financial Statements for Corporate Entities

6

Types of Capital

• Preference Share Capital: have preferential rights in respect of fixed dividends and repayment of capital in case of liquidation

• Equity Share Capital: residual right- the real owners of the company

Public Issue Expenses: fees to managers to the issue and legal advisers, fees paid to SEBI, fees to ROC, underwriting commission, brokerage to members of stock exchange, printing and publication of application forms, advertising, etc.

21/04/2023 Process of Preparation of Financial Statements for Corporate Entities

7

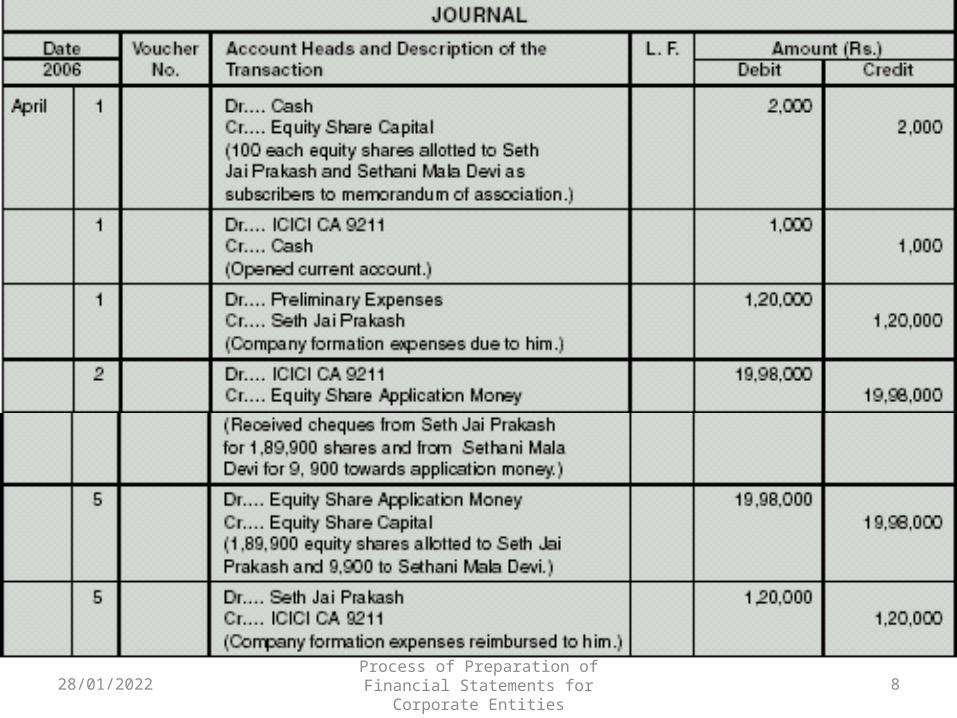

Accounting treatment of Share Capital(1) Example of Private Limited

21/04/2023 Process of Preparation of Financial Statements for Corporate Entities

8

21/04/2023 Process of Preparation of Financial Statements for Corporate Entities

9

(2) Example of Public Limited

21/04/2023 Process of Preparation of Financial Statements for Corporate Entities

10

21/04/2023 Process of Preparation of Financial Statements for Corporate Entities

11

21/04/2023 Process of Preparation of Financial Statements for Corporate Entities

12

21/04/2023 Process of Preparation of Financial Statements for Corporate Entities

13

Share Capital in Balance Sheet

21/04/2023 Process of Preparation of Financial Statements for Corporate Entities

14

Forfeiture of Shares

• If in the above example, the company decides to forfeit the 4 lac shares on which the first call money of Rs. 2 has not been paid by the 100 share holders. This means– The 4 lac shares will be treated as unsubscribed– Rs. 24 lac already paid by the shareholders stands

forfeited– Call-in-Arrears of Rs. 8 lacs is automatically no more due

21/04/2023 Process of Preparation of Financial Statements for Corporate Entities

15

Note:1. Now 1.36 crore shares are subscribed instead of 1.4 crores2. Some companies show the amount paid-up on shares forfeited as a

reserve

21/04/2023 Process of Preparation of Financial Statements for Corporate Entities

16

Issue of shares for consideration other than cash: when a company purchases another business it may issue capital in lieu of paying cash

The effect of purchasing land woth 1.5 crores for 15 lac shares is shown below

21/04/2023 Process of Preparation of Financial Statements for Corporate Entities

17