september 2009 staffordshire county council 2008/09...

TRANSCRIPT

Government and Public Sector

September 2009

Staffordshire County Council

2008/09 Report to those charged with governance

PricewaterhouseCoopers LLP is a limited liability partnership registered in England with registered number OC303525. The registered office of PricewaterhouseCoopers LLP is 1 Embankment Place, London WC2N 6RH.PricewaterhouseCoopers LLP is authorised and regulated by the Financial Services Authority for designated investment business.

PricewaterhouseCoopers LLP

Cornwall Court

19 Cornwall Street

Birmingham

B3 2DT

Telephone +44 (0) 121 265 5000

Facsimile +44 (0) 121 232 2414

pwc.com/uk

The Members

Members of the Audit Committee

Staffordshire County Council

St Chad's Place

Stafford

ST16 2LR

Ladies and Gentlemen

2008/09 Report to those charged with governance

We are pleased to present our report on the results of our audit work for 2008/09. We hope that the information contained in this report provides a useful sourceof reference for members.

Yours faithfully

PricewaterhouseCoopers LLP

PricewaterhouseCoopers LLP3

Contents

Section Page

Executive summary ................................................................................................................................................................................................................................ 4

Financial statements............................................................................................................................................................................................................................... 7

Value for Money in the Use of Resources............................................................................................................................................................................................ 10

Audit plans and fee update................................................................................................................................................................................................................... 12

Appendix A: Audit reports issued in relation to the 2008/09 audit year ............................................................................................................................................... 13

Appendix B: Summary of adjusted misstatements............................................................................................................................................................................... 14

Code of Audit Practice and Statement of Responsibilities of Auditors and of Audited Bodies

In April 2008 the Audit Commission issued a revised version of the ‘Statement of responsibilities of auditors and of audited bodies’ which applies to the 2008/09audit. It is available from the Chief Executive of each audited body. The purpose of the statement is to assist auditors and audited bodies by explaining where theresponsibilities of auditors begin and end and what is to be expected of the audited body in certain areas. Our reports and management letters are prepared inthe context of this Statement. Reports and letters prepared by appointed auditors and addressed to members or officers are prepared for the sole use of theaudited body and no responsibility is taken by auditors to any Member or officer in their individual capacity or to any third party.

PricewaterhouseCoopers LLP4

The purpose of this report

This report summarises the results of our audit work from our 2008/09 auditof accounts.

It includes the issues arising from our audit of the financial statements andthose issues which we are formally required to report to you under the AuditCommission’s Code of Audit Practice and International Standard of Auditing(UK & Ireland) (ISA(UK&I)) 260 - “Communication of audit matters withthose charged with governance”.

It also includes the results of the work we have undertaken on ‘Value forMoney in the Use of Resources’ under the Code of Audit Practice, to supportour formal conclusion in this area.

Our work during the year was performed in line with the plan that wepresented to you on 2

ndJune 2009 and the Pension Fund plan presented on

26th

March 2009. We have issued a number of reports during the audit year,detailing the findings from our work and making recommendations forimprovement, where appropriate. A list of these reports is included atAppendix A to this letter.

We have set out below the most important issues and recommendations thatwe have discussed with you in the course of our work.

Financial Statements

We anticipate issuing an unqualified audit opinion on the financialstatements. This includes the summary financial statements for theStaffordshire Pension Fund.

There are no unadjusted misstatements for us to bring to the attention ofmembers.

We have identified no material weaknesses in the Council’s accounting andinternal control systems during our audit.

The financial statements presented for audit were of a good standard.

There were two adjustments made to the financial statements for which wehave provided further information on below in the body of this report, theserelate to:

The accounting treatment of government grants.

The accounting treatment of a prior period adjustment made inrelation to Church Schools.

There are no material matters of irregular expenditure, fraud or misconduct,or poor standards of financial integrity which we need to bring to yourattention.

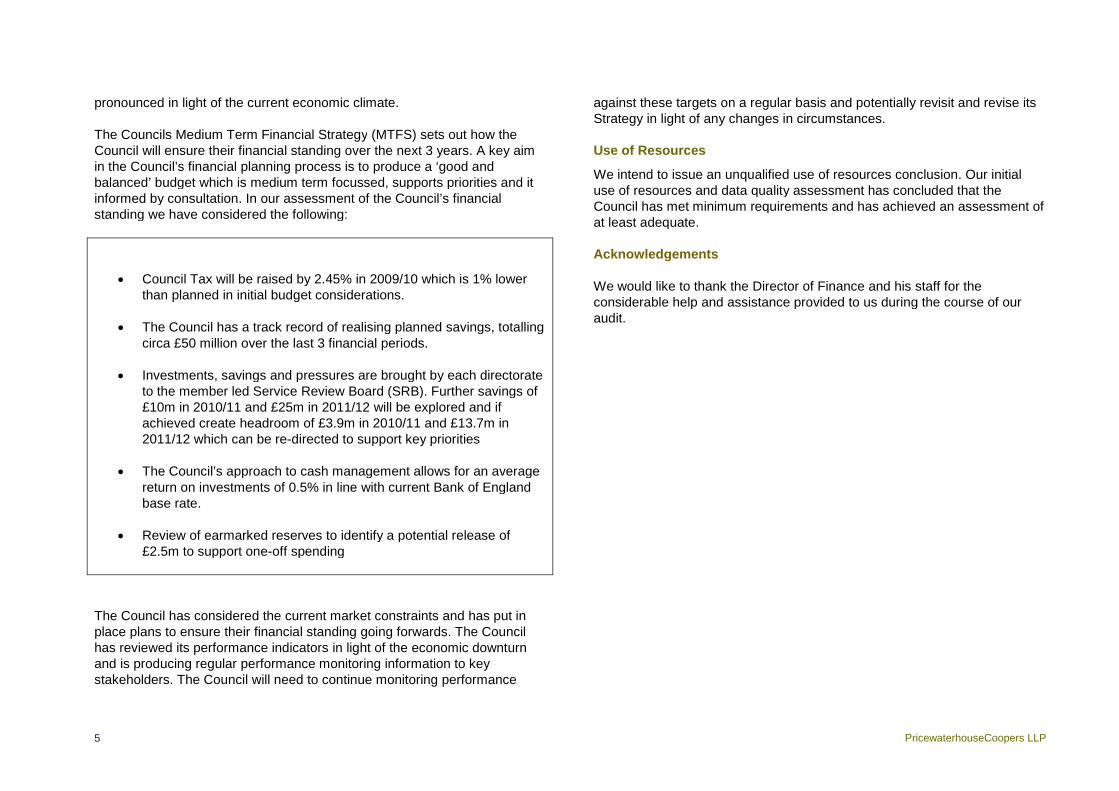

Financial Standing

The Council is responsible for ensuring that it has arrangements in place tosecure an adequate financial standing. This requirement has become more

Executive summary

PricewaterhouseCoopers LLP5

pronounced in light of the current economic climate.

The Councils Medium Term Financial Strategy (MTFS) sets out how theCouncil will ensure their financial standing over the next 3 years. A key aimin the Council’s financial planning process is to produce a ‘good andbalanced’ budget which is medium term focussed, supports priorities and itinformed by consultation. In our assessment of the Council’s financialstanding we have considered the following:

Council Tax will be raised by 2.45% in 2009/10 which is 1% lowerthan planned in initial budget considerations.

The Council has a track record of realising planned savings, totallingcirca £50 million over the last 3 financial periods.

Investments, savings and pressures are brought by each directorateto the member led Service Review Board (SRB). Further savings of£10m in 2010/11 and £25m in 2011/12 will be explored and ifachieved create headroom of £3.9m in 2010/11 and £13.7m in2011/12 which can be re-directed to support key priorities

The Council’s approach to cash management allows for an averagereturn on investments of 0.5% in line with current Bank of Englandbase rate.

Review of earmarked reserves to identify a potential release of£2.5m to support one-off spending

The Council has considered the current market constraints and has put inplace plans to ensure their financial standing going forwards. The Councilhas reviewed its performance indicators in light of the economic downturnand is producing regular performance monitoring information to keystakeholders. The Council will need to continue monitoring performance

against these targets on a regular basis and potentially revisit and revise itsStrategy in light of any changes in circumstances.

Use of Resources

We intend to issue an unqualified use of resources conclusion. Our initialuse of resources and data quality assessment has concluded that theCouncil has met minimum requirements and has achieved an assessment ofat least adequate.

Acknowledgements

We would like to thank the Director of Finance and his staff for theconsiderable help and assistance provided to us during the course of ouraudit.

PricewaterhouseCoopers LLP6

The dashboard below summarises our view of your performance in relation to the completion of the accounts and the audit. For further detail see later sectionsof the report.

RED AMBER GREEN COMMENTS

Quality of accounts Good quality accounts were submitted to the Audit Committeeand PwC on a timely basis.

Readiness for start of audit and workingpapers

Comprehensive working papers were ready at the start of theaudit in the vast majority of cases. However we did encountersome delays with documentation from the Social Care and Healthdirectorate.

Availability and responsiveness of staff Key staff were available during the audit and finance staffresponded to audit requests on a timely basis.

Significant audit and accounting issues No significant audit or accounting issues were found during theaudit.

Weaknesses in internal control systems We have not identified any material weaknesses in InternalControl.

Follow up of prior yearrecommendations

The Council addressed our prior year recommendations.

Key

Red – significant improvements required

Amber – some improvements required

Green – no or some minor improvements required

PricewaterhouseCoopers LLP7

Accounts

We have completed the audit of the Council’s accounts in line with the Codeof Audit Practice and Auditing Standards. We anticipate issuing anunqualified audit opinion on the financial statements.

Accounting Issues

Unadjusted Differences

We are required to report to you all unadjusted misstatements which wehave identified during the course of our audit, other than those of a trivialnature.

There are no unadjusted misstatements for us to bring to the attention ofmembers of the Audit Committee.

Adjusted Differences

We are also required to bring to your attention misstatements which havebeen corrected by management, but which we consider you should beaware of in fulfilling your governance responsibilities.

We discussed all these matters with the Director of Finance and his teamboth prior to and at the clearance meeting on Thursday 13th August 2009.The net effect of these adjustments on both the County and Pension Funddraft accounts can be summarised as follows:

County Fund:

£0.1m increase in net assets’

£3.3m increase in net assets in relation to the restated 2007/08Balance Sheet

No impact on the Councils surplus/deficit in year

Pension Fund

£0.4m increase in net assets

£0.4m increase in the fund account

The following items were the most significant adjustments made to thefinancial statements:

£4.6m increase in government grants deferred

This was a classification amendment which has no impact on the generalfund balance.

Financial statements

PricewaterhouseCoopers LLP8

This adjustment relates to the treatment of 2 grants (NHS Campus Closureand Waste Infrastructure) which were treated as revenue creditors in thedraft accounts. Further inspection of the grant terms identified that thesegrants were awarded for capital schemes and therefore should be classifiedas government grants deferred on the Balance Sheet.

£3.3m increase in net assets in the restated 2007/08 Balance Sheet

The Council restated their 2007/08 accounts in order to remove the value ofthose assets owned by Church Schools. The £3.3m adjustment relates torevaluation reserves that were being held for these schools. These wereincorrectly deducted from the Fixed Asset balance in the draft accounts. Theadjustment has reversed this entry and taken the balance to the CapitalAdjustment Account in line with SORP guidance.

This was a technical accounting amendment which has no impact on theGeneral Fund balance.

Systems of internal control

We are required to report to you any material weaknesses in the accountingand internal control systems identified during the audit. We have notidentified any significant matters during the course of our work.

Accounting practices

We are also required to report to you our view on qualitative aspects of theCouncil’s accounting practices and financial reporting to Council.

The Council was required to approve their draft accounts by 30th

June 2009.This was achieved, and the draft accounts were supported by both a verbalpresentation to members and formal reports explaining the key issuesaffecting the financial statements.

We agreed a schedule of working papers and other information required withthe Council in advance of the audit. We are pleased to report that thequality of working papers was of a good standard and has improvedmarkedly in comparison to prior year. The Council increased the level of

review and scrutiny of working papers and this has clearly paid dividends.

The Council’s finance staff were co-operative in helping us to resolve anyqueries that we had during the audit process. We would like thank thefinance team for their support and assistance during the course of the audit

We will be working with the Council’s finance team to further improve theprocess going forward and will work with you to achieve this.

Other matters

Audit Matters

As with any audit process, there have been a number of matters which wehave considered and satisfactorily concluded on. Below, we have recordedthe most significant of these matters for the information of members.

Impairments

The Councils accounting policy for Fixed Assets states that all major classesof assets will be reviewed at year end to identify any indication ofimpairment. Given the current market climate, the Council has recorded adownward movement in the value of their Land and Buildings ofapproximately 20%. The charge to the Income and Expenditure account forthis movement is £91.2m, and has no impact upon Council Tax.

Prior Period Adjustment – Church Schools

The 2008 Statement of Recommended Practice (SORP) providedclarification on the treatment of Church Schools. The Council undertook anexercise ahead of the year end to analyse the level of control they held overChurch schools on their Balance Sheet. It was concluded that the risks andrewards of owning these assets laid with the respective Churches andtherefore a prior period adjustment was made to remove these assets fromthe Council’s 2007/08 Balance Sheet. The total value of these assets was£143.3m. This adjustment had no impact on the income and expenditureaccount or the General Fund Balance.

PricewaterhouseCoopers LLP9

Job Evaluation

In prior year, the Council provided for the costs of all payments that wouldbe made to Council employees under the Job Evaluation scheme. Duringthe 2008/09 the vast majority of payments were paid out of this provision.The provision held at the year end (£2.8m) represents the potential futurecosts of the Job Evaluation scheme, including any potential equal pay claimsfrom employees. We are satisfied that the Council has been prudent in theirprovision and has adequate reserves in place should additional costs beincurred.

Increase in PFI Energy Commitment

As part of their Private Finance Initiative (PFI) for Street Lighting, the Councilpays a Unitary Payment to cover the provision of this service. The paymentsmade in year and the future commitments at year end are disclosed in note28 to the main financial statements. The commitment disclosed in the2008/09 (£241m) has increased by £31m from prior year. This changereflects an adjustment in the commitment calculation by the Council toreflect the general increase in energy costs. We are satisfied that theCouncil has been prudent in acknowledging the current market trend andhas reflected this in their future liabilities.

Fraud and Corruption

Examples of matters to be reported under this heading are instances ofirregular expenditure or evidence of fraud or misconduct, or poor standardsof financial integrity. There are no such matters that we need to bring to yourattention.

Electors Questions/Objections

At the date of this report we had not been made aware of any elector’squestions and objections under the Local Government and PublicInvolvement in Health Act 2007.

PricewaterhouseCoopers LLP10

Work performed

We have performed work to conclude on the Council’s arrangements forachieving economy, efficiency and effectiveness in its use of resources. Ourwork to support our conclusion comprised the following elements:

Use of Resources assessment, supported by our conclusions on the keylines of enquiry (KLoEs) as specified by the Audit Commission

Review of the Annual Governance Statement.

Use of resources

From April 2009, the Audit Commission has been implementingcomprehensive area assessment (CAA), jointly with the other public serviceinspectorates. The audit year 2008/09 is a year of transition to CAA. Ouruse of resources judgements in 2008/09 will therefore input into the firstresults of CAA which the Audit Commission will report on in autumn 2009 aswell as acting as the basis for our value for money conclusion. The AuditCommission have therefore issued new Key Lines of Enquiry (KLoEs) forauditors to assess Local Authorities’ arrangements against.

We have assessed the Council’s arrangements against a series of KeyLines of Enquiry (KLoEs) grouped into three themes which form the Use ofResources framework. The assessment has changed to focus on theCouncil’s achievements, outputs and outcomes rather than the Council’sprocesses. Auditors are therefore considering the Council’s strategiesrather than the detailed processes that the Council has put in place.

KLoEs are scored as follows:

1 – Failure to meet minimum requirements – inadequate performance;

2 – Meets only minimum requirements – performs adequately;

3 – Exceeds minimum requirements – performs well; or

4 – Significantly exceeds minimum requirements – performs excellently.

Value for Money in the Use of Resources

PricewaterhouseCoopers LLP11

Value for Money Conclusion

Under the Code of Audit Practice we are required to provide a conclusion onthe Council’s arrangements for securing economy, efficiency andeffectiveness in its use of resources. This conclusion is reached byassessing the Council’s arrangements against a set of criteria issued by theAudit Commission. From 2008/09 the Key Lines of Enquiry for the scoreduse of resources assessment also form the criteria for the Use of Resourcesconclusion. A score of Level 2 or higher under the KLoEs will usually resultin an assessment of ‘adequate’ arrangements for the purposes of the Codecriteria. In reaching our conclusions, we also consider whether the KLoEscores should be adjusted for other factors such as whether thearrangements have been in place for the whole financial year.

We intend to issue an unqualified value for money conclusion.

The final results of the use of resources assessment will be published by theAudit Commission in the autumn of 2009.

Annual Governance Statement

Local Authorities are required to produce an Annual Governance Statement(AGS) which is consistent with guidance issued by CIPFA / SOLACE. TheAGS was included in the financial statements.

We reviewed the AGS to consider whether it complied with the CIPFA /SOLACE guidance and whether it is misleading or inconsistent with otherinformation known to us from our audit work. We found no areas of concernto report in this context.

PricewaterhouseCoopers LLP12

Audit Plan 2008/09

We issued our Audit Plan for 2008/09 and presented it to Members on 2nd

June 2008 and our Pension Fund Audit Plan on 26th

March 2009.

We have performed appropriate reporting procedures for each of the risksidentified in our Audit Plans of 2008/09. In this report we comment only onthose areas where we believe we need to communicate with those chargedwith governance.

Audit fees update for 2008/09

We reported our fee proposals as part of the Audit Plans for 2008/09.

Our actual fees were in line with our proposals.

Our fees charged were:

2008/09 Outturn

£000

2008/09 Fee proposal

£000

Accounts

Council

Pension Fund

157

45

157

45

Use of Resources 90 90

Total 292 292

Audit plans and fee update

PricewaterhouseCoopers LLP13

The following audit reports have already been issued in relation to the 2008/09 audit year:

The following reports have been issues in relation to the 2008/09 financial year:

Audit Committee Reports relating to the 2008/09 financial year

June 2008 County Council 2008/09 Audit Plan

March 2009 Pension Fund 2008/09 Audit Plan

April 2009 Audit Protocol between Internal & External Audit

September 2009 ISA (UK&I) 260 “Report to those charged with governance”.

Appendix A: Audit reports issued in relation to the2008/09 audit year

PricewaterhouseCoopers LLP14

We have not identified any material errors during our audit of the financial statements that have not been adjusted by management.

However, we did identify the following significant misstatements during our audit which management have corrected. For the Council’s main Statement ofAccounts the adjustments were as follows:

County Council Accounts

Income & Expenditure Account Balance SheetAdjusted Misstatement

Dr £m Cr £m Dr £m Cr £m

2008/09 accounts

NHS Campus Closure Revenue

(£3.3m) & Waste Infrastructure Grant(£1.3m)

The above grants were treated asrevenue creditors in the draft accounts.Further inspection of the grant termsidentified that these grants were awardedfor capital schemes and therefore shouldbe classified as government grantsdeferred on the Balance Sheet.

Creditors

4.6

Government GrantsDeferred

4.6

Appendix B: Summary of adjusted misstatements

PricewaterhouseCoopers LLP15

Income & Expenditure Account Balance SheetAdjusted Misstatement

Dr £m Cr £m Dr £m Cr £m

COT3 Payments

Invoices relating to Quarter 4 JobEvaluation (COT3) were not beenaccrued for in 2008/09.

These payment were provided for inprevious years and therefore have noeffect on the I&E.

Job Evaluation Provision

2.4

Creditors

2.4

Other AdjustmentsCreditors

0.8

Debtors

0.8

Net effect 7.8 7.8

2007/08 restated accounts

Church Schools Prior PeriodAdjustment

Revaluation reserves held for ChurchSchools were incorrectly credited to theFixed Asset Balance in the prior periodadjustment. All balances should be takento the Capital Adjustment Account.

Fixed Assets

3.3

Capital AdjustmentAccount

3.3

Net effect 3.3 3.3

Total Adjustments 11.1 11.1

PricewaterhouseCoopers LLP16

Pension Fund Accounts

Net Assets Statement Fund AccountUnadjusted Misstatement

Dr £000 Cr £000 Dr £000 Cr £000

The Funds Alliance's emerging marketinvestment have been wrongly classifiedas segregated equities

Investments - segregatedoverseas quoted equities

4,127

Investments - overseaspooled investmentvehicles

4,127

Other Adjustments 411 1,401 990

Net effect 411 5,528 6,117

©2009 PricewaterhouseCoopers LLP. All rights reserved. PricewaterhouseCoopers refers to the network of member firms of PricewaterhouseCoopers International Limited, eachof which is a separate and independent legal entity.