semifinal case solution by benchmark company at changellenge cup moscow 2012

TRANSCRIPT

PwC Proposal to Polesye Agro Providing audit and advisory services to help

the client move business on a higher level

Made by Benchmark Company exclusively for CL Cup Moscow’12 >>

5 December 2012

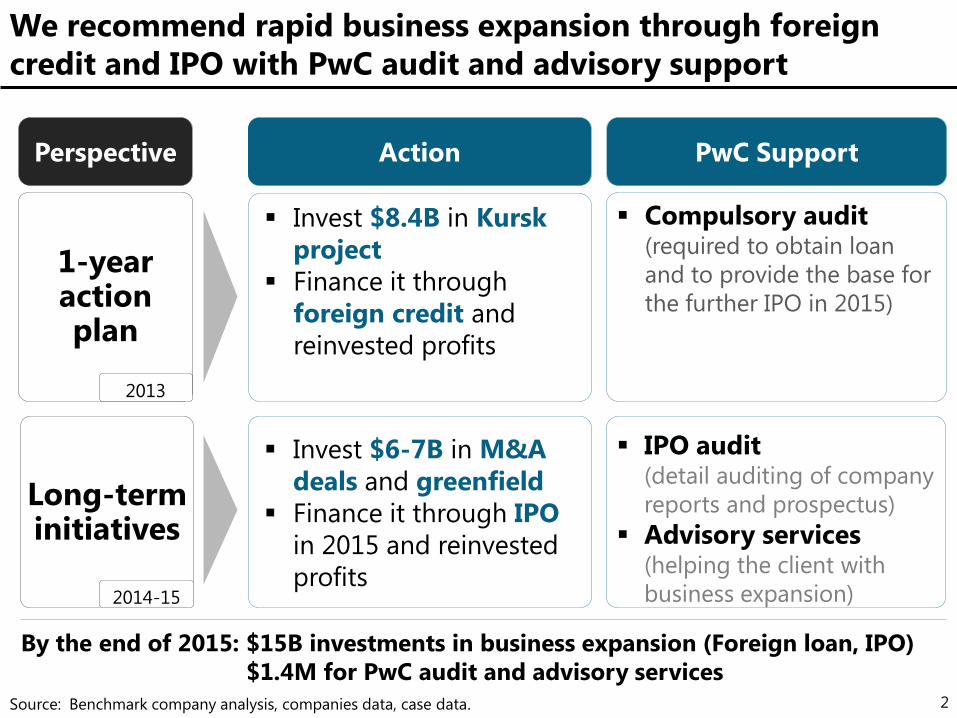

1-year action plan

2 Source: Benchmark company analysis, companies data, case data.

We recommend rapid business expansion through foreign

credit and IPO with PwC audit and advisory support

Invest $8.4B in Kursk

project

Finance it through

foreign credit and

reinvested profits

Perspective Action

PwC Support

Long-term initiatives

Invest $6-7B in M&A

deals and greenfield

Finance it through IPO

in 2015 and reinvested

profits

IPO audit (detail auditing of company

reports and prospectus)

Advisory services (helping the client with

business expansion)

Compulsory audit (required to obtain loan

and to provide the base for

the further IPO in 2015)

By the end of 2015: $15B investments in business expansion (Foreign loan, IPO)

$1.4M for PwC audit and advisory services

2013

2014-15

1. Industry analysis and competitors comparison

2. Choosing the right option for business

3. PwC Offer: services description and its rationale

4. Final recommendations

3

Agenda

Pork consumption 2011-2015

Millions of tons

The growing pork market will be driven by domestic top-

players with government support and shifts in consumption

4 Source: Benchmark company analysis, companies data, case data, Euromonitor, Russian Meat Union.

42% 40% 37% 34% 30%

22% 20% 18% 16% 15%

36% 40% 45% 50% 55%

2015F 2014F 2013F 2012F 2011

Other domestic

Import

Domestic Top-10

2,9 3,0 3,1 3,3 3,4

2015F

+17%

2011 2014F 2013F 2012F

The pork market will grow by 17% by the end of 2015

Agroholdings will capture 10-15% of market from import and small players

35 35 35 36 36

Pork share of meet consumption

Percent

Pork market breakdown 2011-2015

Percent

Meet consumption will continue to switch from beef to

pork and poultry

According to Russian Meat Union, the market leaders will

build additional 0.8M capacities by the end 2015

Import will continue to decrease through strong govern-

ment support of the industry due to WTO transition period

Market leaders have super-ambitious plans to expand its

business in all segments of value chain

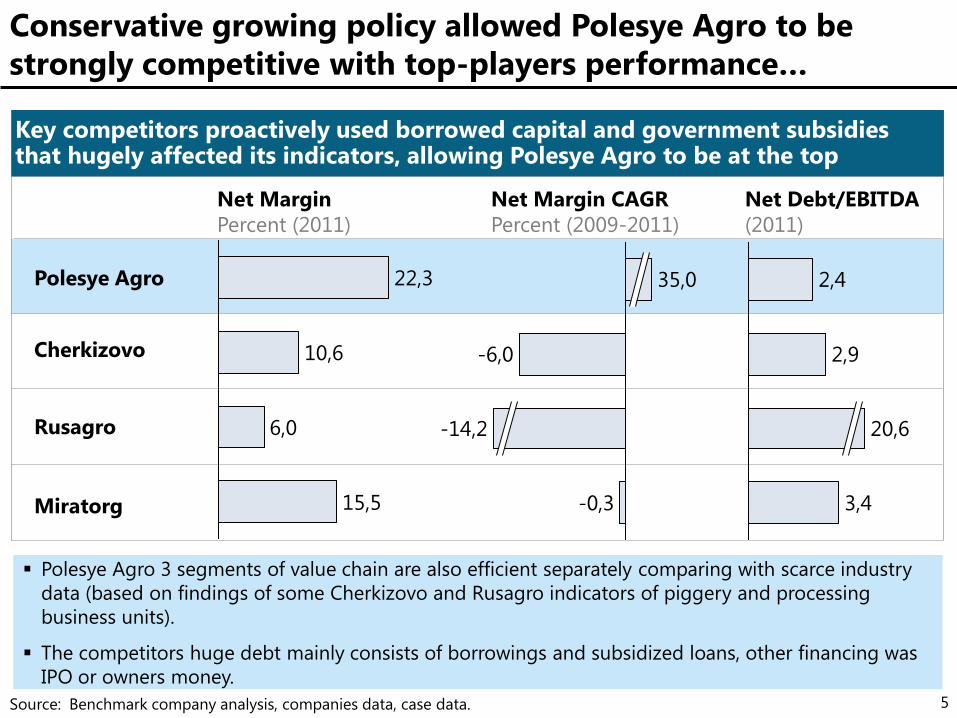

Net Margin

Percent (2011)

Conservative growing policy allowed Polesye Agro to be

strongly competitive with top-players performance…

5 Source: Benchmark company analysis, companies data, case data.

Net Margin CAGR

Percent (2009-2011)

Net Debt/EBITDA

(2011)

15,5

6,0

10,6

22,3

-0,3

-14,2

-6,0

35,0

3,4

20,6

2,9

2,4

Cherkizovo

Rusagro

Miratorg

Polesye Agro

Key competitors proactively used borrowed capital and government subsidies that hugely affected its indicators, allowing Polesye Agro to be at the top

Polesye Agro 3 segments of value chain are also efficient separately comparing with scarce industry

data (based on findings of some Cherkizovo and Rusagro indicators of piggery and processing

business units).

The competitors huge debt mainly consists of borrowings and subsidized loans, other financing was

IPO or owners money.

6 Source: Benchmark company analysis, companies annual reports, case data.

…However, the company has to respond to the aggressive

rivals’ moves by expanding its business

Polesye Agro

Cherkizovo

Rusagro

Miratorg

KoPITANIYA

Agro Belgorye

Vertical Integration

Polesye Agro is the only company that is represented in half of the value chain with modest investment plans.

Grain Feed-

stuff Piggery

Proces-

sing

Distri-

bution Retail Investment plans in all segments

Investment position

3 projects in piggery and feedstuff are taken

into consideration (1-8B rub by 2015)

Aggressive M&A strategy (Mosselprom in 2011)

Active capacity increasing (20B rub by 2015)

Distribution development

Aggressive growth in piggery, grain &

feedstuff (3x increase by 2015)

Launching of new capacities (4,3B rub by 2013)

Distribution & Retail Excellence

Aggressive growth in piggery & processing

(100B rub in 3 years)

Value chain further development

Piggery & processing investments (20B rub

in the mid-term perspective)

15B rub investments in mid-term range

Included

Not included

1. Industry analysis and competitors comparison

2. Choosing the right option for business

3. PwC Offer: services description and its rationale

4. Final recommendations

7

Agenda

8 Source: Benchmark company analysis.

The proposed aggressive expansion can be done only by

non-organic growth of Polesye Agro

Non-organic growth

Organic growth

Sell business

Selection factors (key findings from first part)

Steady industry

growth

Company strong

competitiveness

Huge competitors

expansion Business Options

1

2

3

Client weak

vertical integration

Non-organic growth seems like the only available option in the client situation that needs

huge investments to response to the competitors

Organic growth is an open issue in the long-term perspective after the proposed expansion

Client can sell its business, but it makes more sense to retain control and develop the business

Fits the option

Doesn’t fit the option

9 Source: Benchmark company analysis, case data.

Among company investment projects the 3rd one will provide

maximum synergy, but additional expansion is needed

Current investment

projects

Project 1

Expansion of piggery current

capacities

Project 2

New feed mill plant and piggery

in Chelyabinsk district

Project 3

New feed mill plant and piggery in Kursk district

Non-organic growth

+

Non-organic growth

Non-organic growth

The cheapest option -

+ -

+ -

Full grain supply of piggery

Capacities will grow by 2.5x

No vertical synergy due to

remoteness of main capacities

No working experience and

own processing in the region

Overpayment (4B higher than

3rd option)

Doesn’t provide rapid growth

No vertical synergy since

processing is fully loaded

New capacities won’t work on

the own processing

The projects provide expansion of capacities only in current segments of value chain

To be more efficient and completely vertically integrated the company should enter grain,

distribution and retail businesses

Capacities will grow by 2.5x

Great vertical synergy due to

closeness to current facilities

No overpayment, average

investments

Only 50% feedstuff supply of

piggery

Short-term perspective

10 Source: Benchmark company analysis, case data, Warsaw Stock Exchange, LSE.

Chosen project should be financed by foreign loan, while

further expansion will be based on IPO in long-term range

Eurobonds

Required

Time Key benefits

Price or %

Rate

Control

Maintenance

Maximum Sum,

$ mln Options

Foreign credit

Domestic credit

IPO

Strategic Investor

Finance Investor

No

1

year

Long-term perspective

12-13%

10-11%

150

130

Fast deal speed

No reports transform

12-13%+

currency risk

IFRS

Need

1

year

1

year

1

year

3

years

>150

100

100

50

5 mln

2 mln

1 mln

Long-term range

Cheaper than domestic

Large financial support

Long-term range

Raising company`s brand

Future financing through

add.emission

Large sums of money

Independent company

strategy

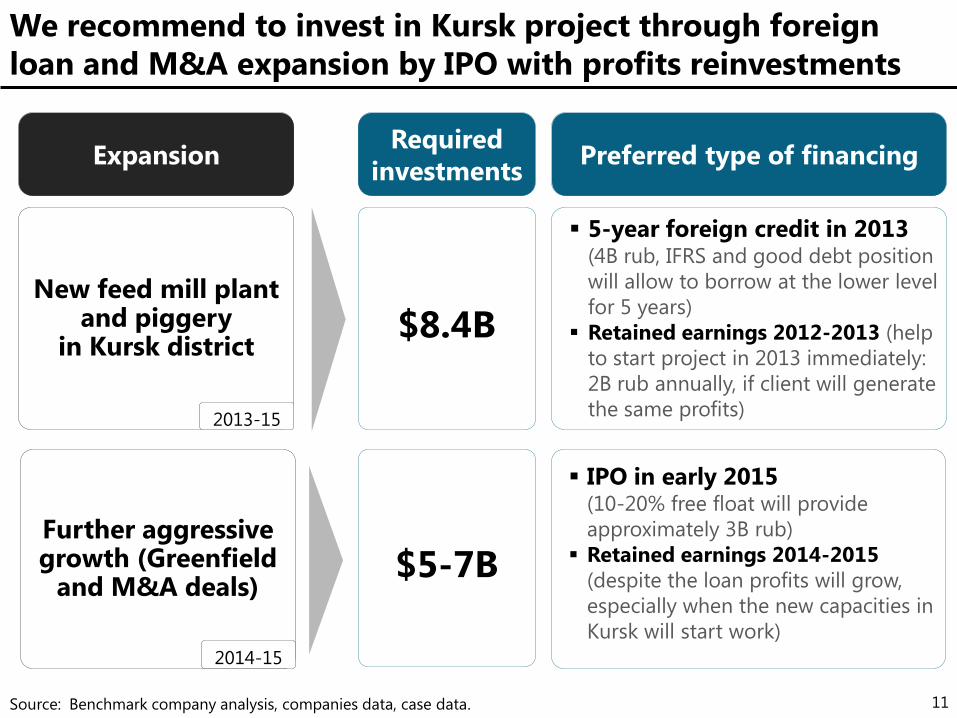

New feed mill plant and piggery

in Kursk district

2013-15

11 Source: Benchmark company analysis, companies data, case data.

We recommend to invest in Kursk project through foreign

loan and M&A expansion by IPO with profits reinvestments

$8.4B

Expansion Required

investments

Preferred type of financing

5-year foreign credit in 2013 (4B rub, IFRS and good debt position

will allow to borrow at the lower level

for 5 years)

Retained earnings 2012-2013 (help

to start project in 2013 immediately:

2B rub annually, if client will generate

the same profits)

Further aggressive growth (Greenfield

and M&A deals)

2014-15

$5-7B

IPO in early 2015 (10-20% free float will provide

approximately 3B rub)

Retained earnings 2014-2015

(despite the loan profits will grow,

especially when the new capacities in

Kursk will start work)

1. Industry analysis and competitors comparison

2. Choosing the right option for business

3. PwC Offer: services description and its rationale

4. Final recommendations

12

Agenda

PwC offers annual audit services including the pre-IPO audit

in 2015 and strategy consulting service

2012 2013 2014 2015

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

5.12.12

Investment project

IPO

1st year audit

Foreign loan

Advisory services

Activities

M&A

IPO audit

Annual audit

Compulsory audit in long-term starting from

2013 (in 2013 to gain a foreign credit)

Acting as the IPO auditor in 2014

Transaction support, Strategy Development,

Assistance in getting state benefits,

Market Sounding

Audit

services

Advisory

services

2m 2013

3 m 2014-15

3 m 2014

2 m 2015

Description Length Service Price

$770K

$600K

13

1-y

ear

Lo

ng

-term

Source: Benchmark company analysis, companies data, case data. 13

Company’ activities PwC Support

Thousand $

Source: Benchmark company analysis, companies data, case data.

The fee for audit services is almost the same as the one for

advisory and in total the fee equals $1.4M

200

40

4

20

264

Technical questions

Additional manager

Basic rate

Total fee

Jan-March period

2 $146K

Audit with pre-IPO audit service will be held in 2013-2015 and cost $770k

Length of audit

period, months

Audit

period Total fee

1st year

2nd year

3rd year

3 Mar-May 2013 $264K

2 $160K Jan-Feb 2014

Jan-Feb 2015

IPO audit ? Sep-Dec 2014 $200K

Thousand $

200

300

0

600

Market Sounding

Assistance in getting

state benefits 100

Transaction Support

Strategy Development

Total fee

14

The total advisory fee consists of 3 components

Following services will optimize the future performance of the company

Strategy

Development

Transaction

Support

Assistance in get-

ting state benefits

Marketing

Sounding

Develop strategy and plans

for future, identify priorities

Pre-deal preparations & ne-

gotiations, analyzing options

Support to get tax benefits,

direct government financing

Analyzing players, potential

collaborators

The total audit fee for the 1st year consists of 4 components

Closeness to the clients

Transportation and labor cost savings

No main competitors in the region

Wide opportunities identification for

the growth of the company

The best possible advice on long-term

strategy

Effective and efficient audit services

High commitment to the company

Providing services in correspondence

with the company’s goals

Additional services

and support

New PwC office

in Voronezh

Top service value

for competitive fee

Clear understanding of the

company’s business framework

Top-clients in agribusiness

Extensive experience

in agribusiness audit

15 Source: Benchmark company analysis, case data, PwC site.

PwC has a range of competitive advantages to beat the

competitors and exceed the client’s expectations

16 Source: Benchmark company analysis, companies data, case data.

PwC beats its main competitors in terms of geographical

benefits and significant experience in agribusiness

Geography closeness*

Agribusiness experience **

IFRS experience

Report reliability

Additional Services

* Based on the analysis of companies’ offices in Russia.

** Valuation is based on the analysis of Ukrainian and Russian agricompanies’ auditors.

BIG-4

Competitors

BDO, Grant

Thornton Small Russian

audit firms PwC

worse better

PwC is far better to Polesye Agro than its direct competitors by geography closeness and

agribusiness experience that allow to be with client in touch and provide best experienced teams

17 Source: Benchmark Company analysis, case data.

Customer sees no

potential return

PwC audit service is essential for successful

achieving of the long-term goals.

Advisory services will help to consider deeply the

business expansion options needed for success

Risk of price

issue importance Risk elimination

Customer will pay attention primarily to the value of service

as the risk of the competition based solely on price is not high

Customer is not

able to pay

Dumping by

competitors

The customer has an ability to pay the amount

needed due to the good company’s performance

BIG-4 competitors have the comparable price and

are not likely to dump

Second-tier competitors provide limited range of

services at lower price with poor quality

1. Industry analysis and competitors comparison

2. Choosing the right option for business

3. PwC Offer: services description and its rationale

4. Final recommendations

18

Agenda

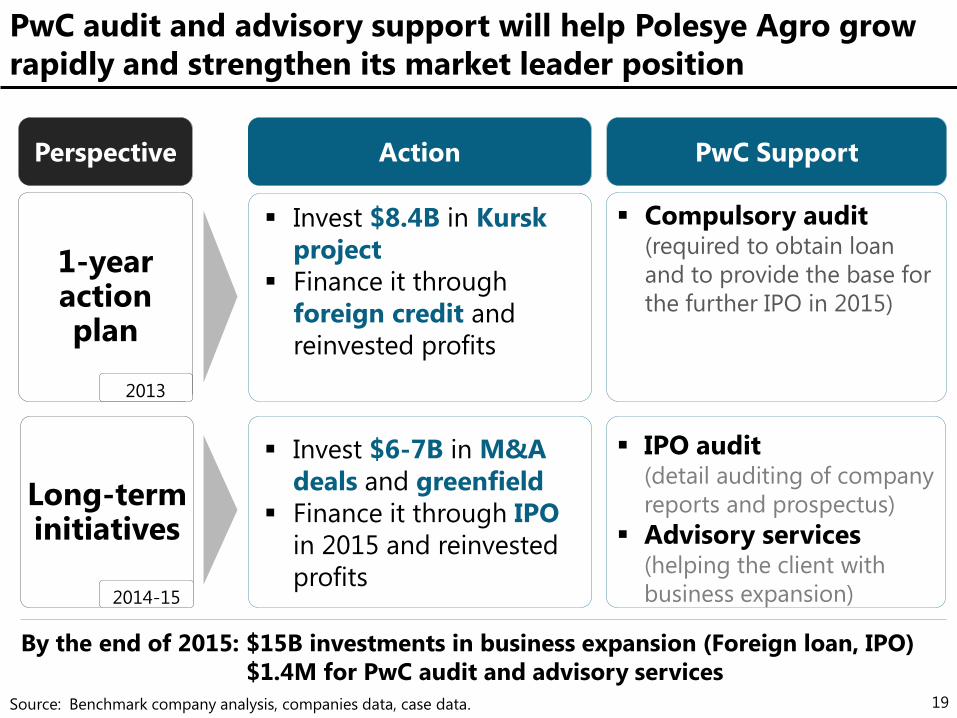

1-year action plan

19 Source: Benchmark company analysis, companies data, case data.

PwC audit and advisory support will help Polesye Agro grow

rapidly and strengthen its market leader position

Invest $8.4B in Kursk

project

Finance it through

foreign credit and

reinvested profits

Perspective Action

PwC Support

Long-term initiatives

Invest $6-7B in M&A

deals and greenfield

Finance it through IPO

in 2015 and reinvested

profits

IPO audit (detail auditing of company

reports and prospectus)

Advisory services (helping the client with

business expansion)

Compulsory audit (required to obtain loan

and to provide the base for

the further IPO in 2015)

By the end of 2015: $15B investments in business expansion (Foreign loan, IPO)

$1.4M for PwC audit and advisory services

2013

2014-15

Great case cracking track

Semifinal of McKinsey&Co BD

Championship’12

3rd place at Microsoft Case

Competition’11

Semifinal of CL Cup Russia’11

Excellent academic study

High achievers of Finance

University, top-5% of course rating

Grants from Russian Economy

Fund, Potanin Foundation, Lukoil,

Gazprombank, Vozrozhdenie

Unique working experience

Worked in PwC, JTI, MCG

Organized Fincontest’12, Russian

Innovation Convention’11

Participated in student consulting

project with BCG ad-hoc support

Sergey

Slutskiy

Mark

Khlynov

Maria

Kochmola

Elizaveta

Ivahnenko

Benchmark Company high-experienced team of fellows with strong

spirit that study and work together for 4 years

Thanks for your attention! Any questions?