sector report, january 9, 2015 capital goods in japan and ...€¦ · sandvik (nsk, kito, doosan,...

TRANSCRIPT

Equity Research

Sector report, January 9, 2015

Capital Goods in Japan and Korea

We met 19 companies in five days

Conclusions for twelve Nordic Capital Goods companies

Regional winners are Autoliv and Atlas Copco

Regional losers are shipbuilding companies (Alfa Laval/Wartsila/Cargotec) and SKF

Contents Executive summary: Rising suns and falling stars 3

Who, what and where: company overviews, trip agenda 6

BoJ saves Japan but puts pressure on South Korea 10

Shipbuilding: Slow steaming until 2016 demand pick-up 12

Japanese truck market: From a vacuum to growth 32

ABB (Hyosung) 36

Alfa Laval (Alfa Laval, Wartsila, Cargotec, DSME, etc.) 38

Atlas Copco (Atlas Copco, Komatsu, etc.) 40

Autoliv (Hyundai, Suzuki and Denso) 42

Cargotec (Cargotec, shipbuilding) 47

Konecranes (Kito) 49

Metso (Metso Flow Control in South Korea) 51

Nokian Tyres (Bridgestone) 53

Sandvik (NSK, Kito, Doosan, Komatsu, Mitsubishi) 54

SKF (NSK, Kito, Denso, Bridgestone, etc.) 56

Volvo in Japan 60

Wartsila (Wartsila, shipbuilding) 63

Disclaimers 64

Peder Frölén +46 8 701 12 51 [email protected] Hampus Engellau +46 8 701 35 76 [email protected]

Tom Skogman +358 10 444 27 52 [email protected] Carl Bertilsson +46 8 701 82 84 [email protected]

Sector report, January 9, 2015

3

Executive summary: Rising suns and falling stars This report contains details and outlooks about some of the Nordic companies in our universe with operations

in South Korea and Japan, reflecting our recent visit to those countries and discussions with local and Nordic

companies there. In this report, we also reach conclusions about how the shipping industry will affect our

Nordic universe, and we take a deep dive into the Japanese heavy truck market, as well as reviewing operations

and prospects in Japan and South Korea for companies in our Nordic Capital Goods universe. We rank our

universe based on size, position and demand outlook in the region. Autoliv and Atlas Copco score the best,

while the companies exposed to shipbuilding (Alfa Laval, Cargotec and Wartsila) and SKF score the worst.

Overall outlook for Japan and South Korea Much of the success in turning deflation into inflation and boosting company profits, the labour market and wages can be pinned on the dramatic expansion of the Bank of Japan’s balance sheet. Last month the BoJ revealed that it will do more of the same. We now estimate that USD/JPY will reach 130 next year, further boosting profits and stocks. South Korean exporters will face increasing competition from Japan and this will make the central bank dovish, putting downward pressure on interest rates and ultimately stimulating domestic demand conditions.

Companies in Japan foresee a healthier domestic economic climate, with the Construction segment highlighted during most discussions. Although companies expect some growth of industrial demand in 2015 after a flat 2014, one should bear in mind that the absolute level is rather constant (NSK has had flat sales in Japan since 2005). Strength from improved local demand will be used to seek expansion overseas and not only in the rest of Asia, which could play out interestingly in some industries. Although this viewpoint does not take FX developments into account, currency movement advantages are quite obvious and will likely be even stronger ahead. It is quite clear that Japanese companies are skeptical about Chinese demand. Both NSK and Kito claim that the low-end market for industrial distribution products is shrinking in China.

Shipbuilding industry Ship orders collapsed in 2014 and at our meetings in South Korea and Japan we did not meet anybody who expected a swift 2015 recovery. Instead, the common message was that a generally better global economy hopefully should lead to better ship orders in 2016 and that the Korean yards will enter a restructuring phase. On the other hand, a performance ‘Ice Age’ looms for offshore, with the risk of spillover effects from surprisingly weak demand for gas carriers.

We argue that high energy prices together with cheap financing have prevented the shipbuilding industry from starting heavy restructuring earlier. Notably, yards also still presented great profitability in 2011-12, stemming from late deliveries of orders booked at a high gross margin in 2008. Now restructuring seems unavoidable and we see it likely that the entire industry will shrink, offering fewer opportunities for the Nordic suppliers.

Based on historical ship orders and our new knowledge gained in Asia, we estimate ship orders ahead and how that transfers into business for Nordic suppliers in our coverage. Thanks to favourable currency movements, sizeable acquisitions and large Service businesses, the outlook is luckily far less acute for these suppliers than could be judged from poor vessel orders.

BoJ balance sheet

expansion fuels

turnaround

Lift in demand

expected in Japan,

not in China

Dim picture for a fast

recovery…

…but Nordic

suppliers to benefit

from FX, buyouts

and Service

Sector report, January 9, 2015

4

Table 1: HCMe vessel order growth (number of vessels), y-o-y

Source: Handelsbanken Capital Markets

Table 2: Total Marine order growth y-o-y in reporting currencies, Nordic suppliers*

Source: Handelsbanken Capital Markets

* Including Service and presented acquisitions

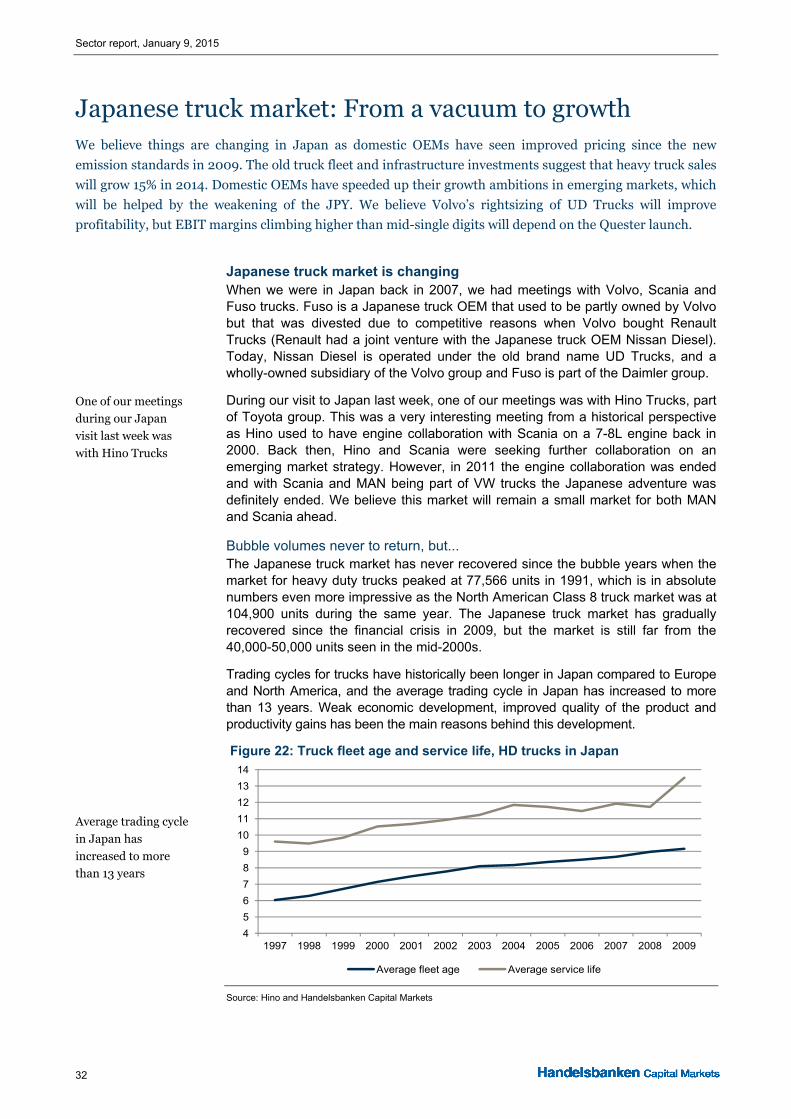

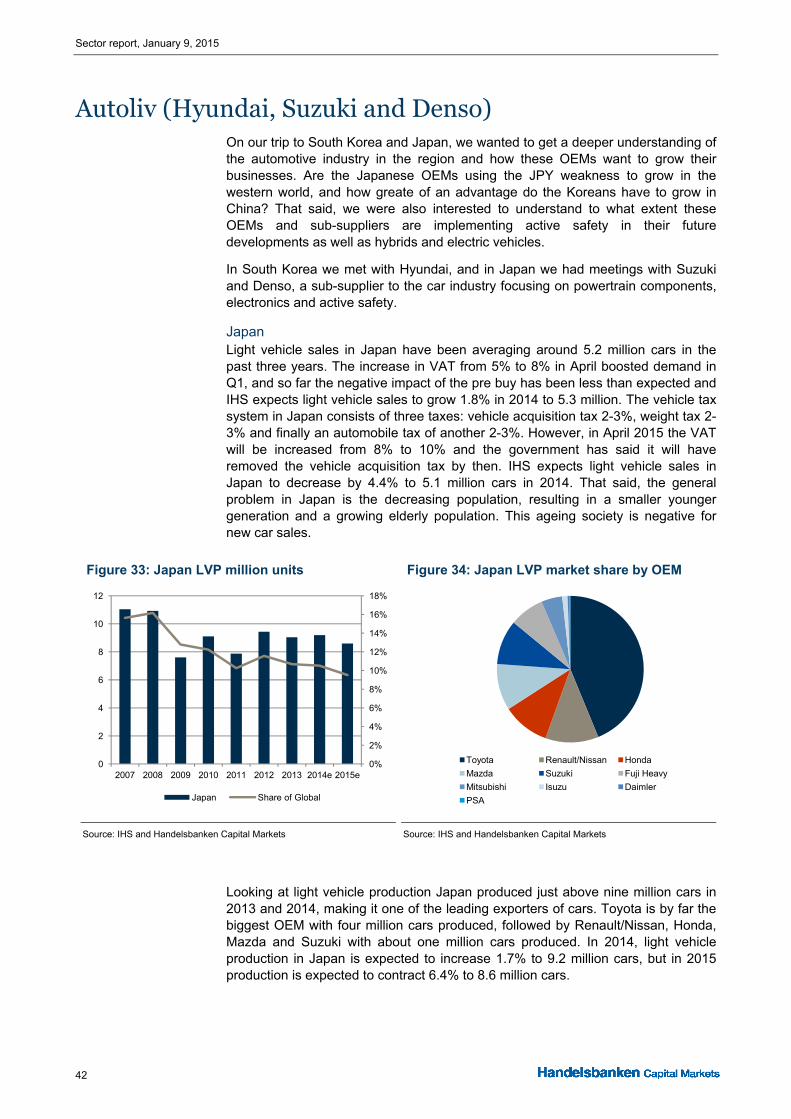

Japanese heavy truck industry The Japanese heavy truck market has been extremely competitive since the bubble years, due to structurally lower volumes and four established local players. The tough pricing situation has made Japan a low-margin market with an EBIT margin for OEMs that is about 3 p.p. lower on average compared to average profitability for European and North American truck OEMs. However, growing demand in Japan and Southeast Asia as well as a gradual return of pricing power suggest that margins might be on the rise in Japan, while the opposite has been the case in Europe and North America since the financial crisis. We expect the 2014 market to have reached close to 39,000 units from a combination of an ageing truck population, improving business confidence and infrastructure investments from build-ups following the Fukushima disaster, but also investments ahead of the 2020 Olympics. We expect 2015 to continue on the growth lane as new JPN 16 emission standards in 2016 will spur investments in mid-2015.

How Nordic companies measure up We look at the size, position and demand outlook in the region and rank our covered Nordic Capital Goods companies from +++ to ---, presented in order of rank.

Figure 1: Nordic Capital Goods, share of sales in Japan and South Korea

Source: Company data and Handelsbanken Capital Markets

Bulk & Container Tankers Offshore Gas Others2014 -58% -23% -47% -5% -31%2015e -10% 5% -70% -30% 15%2016e 10% 10% 15% 5% 10%2017e 0% 5% 100% 20% 5%2018e 10% 5% 50% 20% -10%

Alfa Laval MacGregor Wartsila

2015e -24% -16% -4%

2016e 15% -22% -3%

2017e 16% -6% 8%

0%1%2%3%4%5%6%7%8%9%

10%

Japan & South Korea, share of group sales

Fierce competition

due to low volumes,

local players

From basically none

to 9% of sales for the

Nordic Cap Goods

universe in Japan

and South Korea

Sector report, January 9, 2015

5

Autoliv (+++): Autoliv has a strong position in Asia, especially in Japan and China. We believe Autoliv will gain further market share in this region on the back of Takata’s problems.

Atlas Copco (++): A strong local position, favourable segment exposure and ongoing efforts make Atlas look good in the region. Atlas is also one of the few Nordic suppliers that has managed to land local acquisitions.

ABB (+): Transformer demand remains challenging but Korean profitability speaks of clearly better pricing.

Volvo (+): With the finalised acquisition of Donfeng we believe Volvo is in a better position to leverage its Quester mid-segment product. That said, Japan will remain a mid-single digit EBIT margin market.

Metso (+): Metso has a still small but very interesting position in South Korea, supplying valves to the country’s vibrant EPC companies building global infrastructure projects.

Nokian Tyres (+): We met with Nokian’s main owner Bridgestone (15% of the shares), which states it also has a great EBIT margin in its Winter Tyres division at ~26%.

Sandvik (+/- to -): Sandvik Machining Solutions (SMS) will enjoy a better general economic climate and Sandvik Materials Technology (SMT) will gain some help from nuclear power partly being put back online. However, both SMS and SMT have strong local competitors, which could potentially hurt pricing.

Konecranes (-): Konecranes is not present in South Korea or Japan but it owns 22% of Japan’s leading crane manufacturer Kito. Kito is struggling to see growth in Japan and its market comments about China were negative while the company is optimistic about the US.

SKF (-): Japan is the Mecca of ball bearings, and we are fearful of more exposure for SKF to the weak JPY, especially as main peer NSK is sceptical about volume and has excess capacity.

Cargotec (---): Cargotec’s MacGregor division has an excellent market position in Korean shipbuilding, but orders unfortunately collapsed in 2014 with no clear sign for any improvement in 2015.

Alfa Laval (---): With its relatively large exposure to the region and to the Marine industry, Alfa scores poorly in the group.

Wartsila (---): Wartsila has a great market position in South Korea in particular. However, 2014 ship orders and especially critical offshore orders were very low and we got the impression that yards are preparing for restructuring, as the order outlook remains weak for 2015.

Leaders benefitting

from niches, local

initiatives

Laggards hurting

from weak macro

economies,

shipbuilding

Sector report, January 9, 2015

6

Who, what and where: company overviews We present here our impressions of the operations, performances and prospects of Nordic Capital Goods

companies that have sales or operations in Japan and South Korea. We also provide more detailed rankings

of our perception of these companies in the region, according to size, position and demand outlook. An

itinerary of our recent trip is included at the end of this section. For fuller details on a company’s operations

in Japan and South Korea, refer to that company’s separate chapter further on in this report.

Overviews and ranking of Nordic companies in the region We look at the size, position and demand outlook for companies in the region and rank them from +++ (highest) to --- (lowest), presented in alphabetical order.

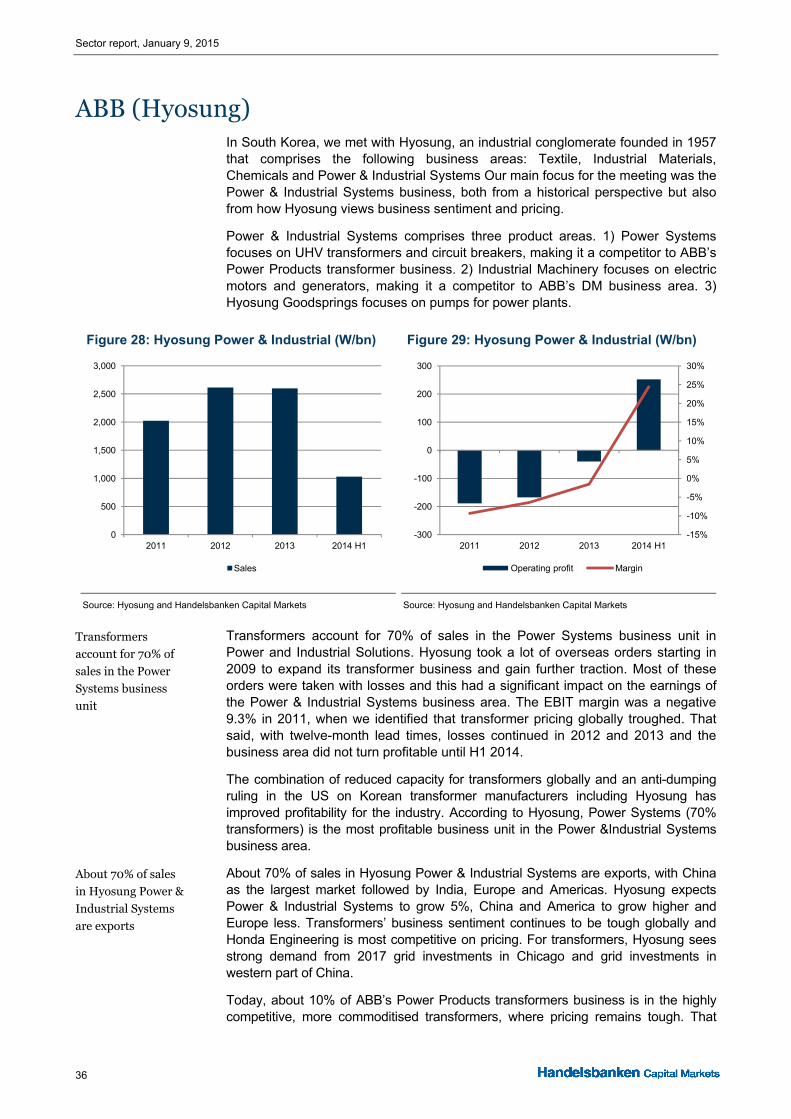

ABB (+): In South Korea, we met with Hyosung, an industrial conglomerate that comprises four business areas. Our main focus in this meeting was the Power & Industrial Systems business area and its two product areas: 1) Power Systems focusing on UHV transformers and circuit breakers, making it a competitor to ABB’s Power Products transformer business. 2) Industrial Machinery focusing on electric motors and generators, making it a competitor to ABB’s DM business area. The combination of reduced capacity for transformers globally and an anti-dumping ruling in the US on Korean transformer manufacturers including Hyosung has improved profitability for the industry. According to Hyosung, Power Systems (70% transformers) is the most profitable business unit in the Power &Industrial Systems business area. Hyosung expects Power & Industrial Systems to grow 5%, China and America to grow higher and Europe less. Transformers’ business sentiment continues to be tough globally and Honda Engineering is most competitive on pricing. Today, about 10% of ABB’s Power Products transformers business is in the highly competitive, more commoditised transformers, where pricing remains tough. That said, we believe this transformers business in ABB Power Products is a low double-digit-margin business.

Alfa Laval (---): Energy imports and more efficient energy usage will boost demand for Alfa Laval in Japan and will increase construction activity. The Marine segment is the most important for Japan and South Korea and faces a tough future (see the section on shipbuilding and our separate research report on Alfa Laval for more details). Alfa Laval has a relatively good balance with locally produced products in Marine, but in total we consider the company to be a net importer in Japan, hurting earnings a bit from FX reasons apart from translation effects. If we combine a relatively large exposure (4% of orders in Japan and 5% in South Korea) with the tough Marine outlook, Alfa scores poorly in our ranking.

Atlas Copco (++): Atlas has around 2% of its sales in Japan and 2.5% in Korea and has benefitted from acquiring companies in Japan (Fuji) or companies with a presence in the region (Drilling Solutions, SCA, Edwards). We find the positive positioning journey in CT, IT and Construction to be of great interest, as it creates good growth prospects in addition to the improving construction activity. Thus, we see relatively good growth prospects for Atlas Copco in the region, helped by expansion plans from Samsung in South Korea. On global mining, Komatsu expects rebuilding activity improvement soon, while parts inventory destocking could continue for a while longer. For construction globally, Komatsu paints a very bleak picture in China and raises a warning about the standard view that US construction activity will continue to rise.

Autoliv (+++): Autoliv is one of the companies in this group with the highest exposure to Asia, which accounts for 33% of group of sales, with China at 15.8%, Japan 7.5% and the rest of Asia at 9.6%. Hyundai is by far Autoliv’s biggest customer among the Asian OEMs and accounts for 9% of Autoliv’s sales. This is followed by Toyota and Honda with 6% of sales each. We believe Korean OEMs are well positioned to grab further

Transformers

providing a firm

foundation

Marine prospects

look really poor

A strong local

position, favorable

segment exposure

and ongoing efforts

make Atlas look good

in the region

Takata airbag

inflator recall could

inflate Autoliv

market share

Sector report, January 9, 2015

7

market share in Asia, while the Triad is less prioritised. That said, we believe Japanese OEMs will grow more aggressively in the Triad, benefitting from the more favourable FX situation, even though much production is localised. Given the recall problems for Takata in relation to airbag inflators (Takata is a Japanese competitor to Autoliv that we did not get to meet), we believe Autoliv will gain more market share in Asia. Takata has become less reluctant to call for a nationwide recall in the US, which we believe will be the first step toward a global recall that could involve as many as 30 to 60 million cars at a total cost of USD 3-6bn for Takata. This will create massive problems for Takata financially, and likely either trigger a rights issue or a restructuring. We believe OEMs will help Takata stay in business, but this is likely going to make Takata a smaller company than today, resulting in long-term global market share gains for Autoliv and TRW of potentially a couple of percentage points each.

Cargotec (--): The company had 7% of group sales in South Korea in 2013 and 1% in Japan. All of Cargotec’s three divisions operate in Korea. Kalmar exports some container port equipment to the country and Hiab has a small factory producing truck-mounted cranes there. However, the majority of Cargotec’s business in these countries comes from MacGregor supplying load-handling equipment and offshore cranes to the building industry for large vessels. The company has an excellent market position in Korea with a 50-60% market share, while it is comparatively weak in Japan. MacGregor expects Korean yards to struggle with order booking in 2015, with the greatest hopes on large container vessels; the offshore outlook is weak, forcing Korean yards to restructure their businesses. Just as with the other yard and shipping equipment suppliers we met, MacGregor shared the view that demand will likely recover in 2016.

Konecranes (+/- to -) has no direct sales in South Korea or Japan but owns 22% of Japan’s biggest crane manufacturer, Kito, with which it also shares some procurement activities, and a cross-selling agreement also exists between the companies. Kito is the global leader in chain hoists while Konecranes is the global leader in wire-rope hoists. Kito has managed to lift its EBIT margin from 4.0% in 2010 to just below 10% in 2014e, indicating it is not impossible to improve profitability in the crane industry. Looking ahead, Kito’s CEO said he remains optimistic about the demand outlook in the US, while he is pessimistic about China for the coming 12-18 months, with only the Automotive and Power Plant segments showing health.

Metso (+) booked 1.3% of group orders from South Korea but all of this came from Flow Control (i.e. nothing from Mining & Construction). However, orders there are expected to rise significantly in the coming years, as after our visit Metso opened a new valves factory, raising the company’s global valves production by 5%. This factory represents one out of Metso’s seven valve factories globally. More than half of Metso’s South Korean sales go to the country’s large and vibrant EPC industry construction’s oil refineries, gas systems, petrochemical factories and power plants across the world. Metso’s idea is that local engineering and production can significantly improve its market position at these EPC companies from the current market share of just above 5%. Of the global valves companies only two have local manufacturing in South Korea, implying Metso has a first-mover advantage.

Nokian Tyres (+/-) has no sales in Japan or South Korea, but China is a potential growth market to which Nokian will deliver some 300,000 tyres in 2014e. In Tokyo, we met with Nokian’s main owner Bridgestone, holding 15% of the shares. Bridgestone expressed no intention to increase or reduce its holding. Currently, the key cooperation between the companies involves Bridgestone offering its Southern European distribution chain to Nokian while Nokian offers its distribution chain in Northern Europe. A key lesson from the meeting is that Bridgestone has a ~26% EBIT margin in winter tyres, i.e. almost in line with Nokian. The key winter tyre markets for Bridgestone are Europe, Japan and Canada. China is still a very small winter tyre market and Bridgestone did not see any great opportunity in China over the next few years. Bridgestone is due to open a factory in Russia in 2016. Approximately 30% of the

Near-term threat in

Korea from yard

orders, restructuring

Can Konecranes

succeed with a

similar turnaround

as Kito’s?

Metso has just

opened a valves

factory in Korea

Bridgestone is

Nokian’s main owner

Sector report, January 9, 2015

8

output from the new Russian factory is planned to go car manufacturers in Russia. While Nokian currently manufactures 45,000 tyres in Russia per day, the Bridgestone factory will at full capacity produce 12,000 tyres by 2018. It is interesting to note that Bridgestone’s biggest factory globally produces 50,000 tyres per day – i.e. Nokian’s factory is one of the biggest tyre factories in the world.

Sandvik (+/- to -): Sandvik has a relatively small exposure to the region (2% of sales to Japan and 1% to South Korea). The company will enjoy a potentially warmer economic climate in SMS and from parts of nuclear power being turned back on driving some modernisation need although we do not expect any investments in new reactors. We do not look for expect Sandvik to win over local suppliers of pipes for gas transportation. Regarding pricing, there is a small downside risk in Sandvik Machining Solutions (SMS) due to competition and in Sandvik Materials Technology (SMT) from both competition and weak energy capex sentiment. Overall, we rank Sandvik as neutral to slightly negative when it comes to potential growth in and from the region.

SKF (-) has limited sales in Japan and South Korea (4%) but the market is very important, as three out of the six largest global players in bearings are Japanese. A possible consolidation (which we actually find unlikely in the short term) could mean less fierce competition for SKF. We fear that insufficient volume growth (demand and distributor destocking) in combination with excess capacity for bearings players, tempting FX advantages for Japanese competitors, increased Chinese competition and an overall weak pricing climate, will force SKF to work even harder to sustain profitability. From a Japanese perspective, a large European exposure, potential positive indirect effects from weaker oil prices, and limited exposure to oil and marine has driven the SKF share recently, and we expect that this could continue in the short term.

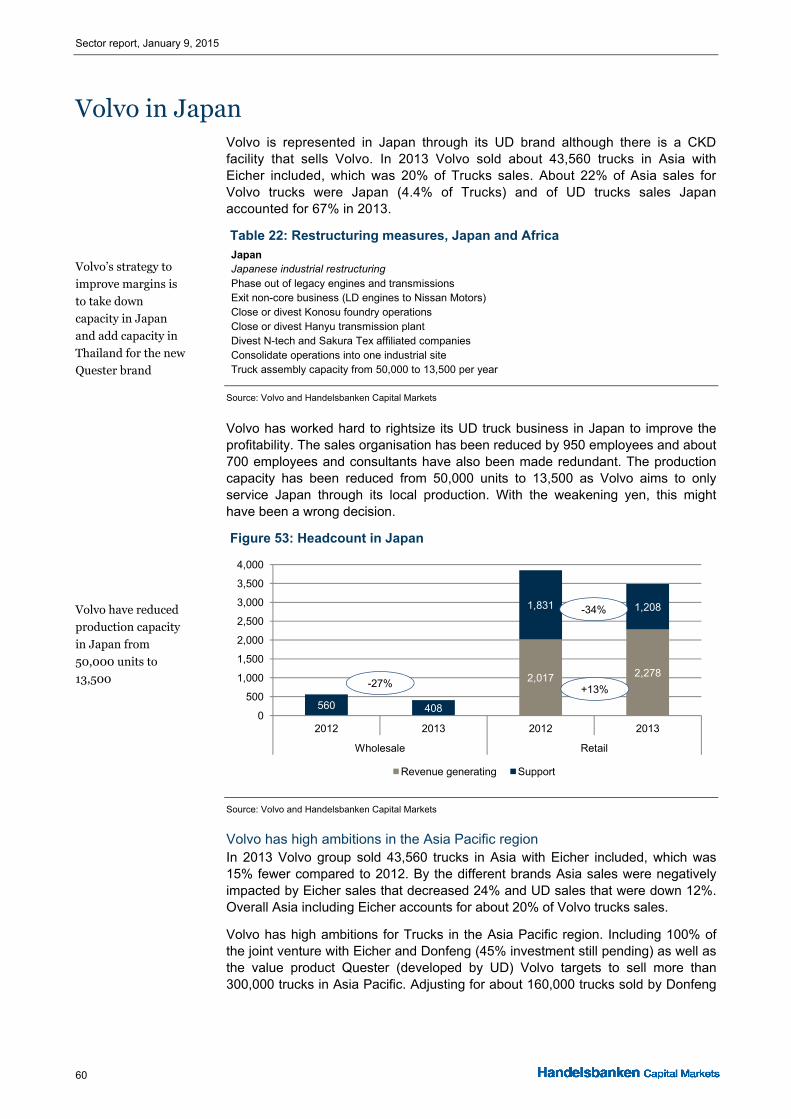

Volvo (+): Volvo is represented in Japan through its UD brand, although there is a CKD facility that sells Volvo. In 2013, Volvo sold about 43,560 trucks in Asia including Eicher, representing 20% of Trucks sales. About 22% of Asia sales for Volvo trucks were to Japan (4.4% of Trucks) and Japan accounted for 67% of UD truck sales in 2013. Even though Volvo is adjusting capacity and streamlining its UD business in Japan, we believe it will continue to be a mid-single-digit margin business with a potential repeat of the historical peak EBIT margin of 7.5%. However, if the introduction of Quester turns out to be a successful volume story reaching 30,000 units, incremental earnings on the UD technology could yield over-the-cycle higher margins. From listening to Volvo and also annualising the previous action programme to increase margins over the cycle, we believe the Quester product is part of the programme to increase the Asia profitability over the cycle. Higher volumes in Asia for Volvo, but also the possibility to extend the life of old technologies from ended products in the Volvo group, speak for better margins, if successful.

Wartsila (--) generated 7% of its 2013 sales in South Korea, with Japan <1% but China another 6%. Almost all of Wartsila’s sales in these countries come from Ship Power with some from Service, implying that Korea and China are the two most important end-markets for Wartsila’s Ship Power. The company has a very strong market position in advanced offshore solutions and gas system solutions. For instance, within LNG (liquefied natural gas) systems Wartsila said it has a market share of >70% in South Korea. The outlook for offshore solutions is weak, and within gas carriers, LPG (liquefied petroleum gas) ship orders will likely weaken while LNG vessels should be strong in 2015. We got the general impression that Korean shipyards expect low orders in 2015 with a recovery expected in 2016.

Local metal-cutting

exposure and little

presence offset a

warmer economic

climate

Japanese bearing

industry getting

stronger

Great market

position in gas

systems

Quester, volumes

and extended life for

old technologies

could boost margins

Sector report, January 9, 2015

9

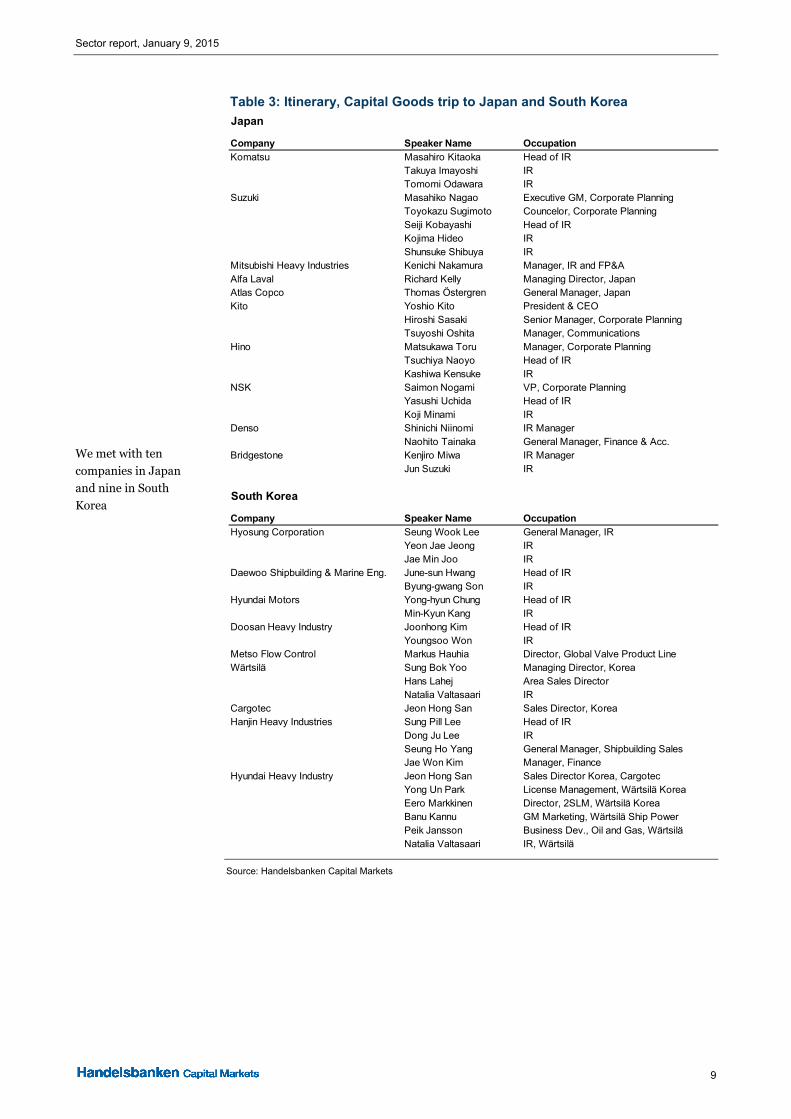

Table 3: Itinerary, Capital Goods trip to Japan and South Korea

Source: Handelsbanken Capital Markets

Japan

Company Speaker Name OccupationKomatsu Masahiro Kitaoka Head of IR

Takuya Imayoshi IRTomomi Odawara IR

Suzuki Masahiko Nagao Executive GM, Corporate PlanningToyokazu Sugimoto Councelor, Corporate PlanningSeiji Kobayashi Head of IRKojima Hideo IRShunsuke Shibuya IR

Mitsubishi Heavy Industries Kenichi Nakamura Manager, IR and FP&AAlfa Laval Richard Kelly Managing Director, JapanAtlas Copco Thomas Östergren General Manager, JapanKito Yoshio Kito President & CEO

Hiroshi Sasaki Senior Manager, Corporate PlanningTsuyoshi Oshita Manager, Communications

Hino Matsukawa Toru Manager, Corporate PlanningTsuchiya Naoyo Head of IRKashiwa Kensuke IR

NSK Saimon Nogami VP, Corporate PlanningYasushi Uchida Head of IRKoji Minami IR

Denso Shinichi Niinomi IR ManagerNaohito Tainaka General Manager, Finance & Acc.

Bridgestone Kenjiro Miwa IR ManagerJun Suzuki IR

South Korea

Company Speaker Name OccupationHyosung Corporation Seung Wook Lee General Manager, IR

Yeon Jae Jeong IRJae Min Joo IR

Daewoo Shipbuilding & Marine Eng. June-sun Hwang Head of IRByung-gwang Son IR

Hyundai Motors Yong-hyun Chung Head of IRMin-Kyun Kang IR

Doosan Heavy Industry Joonhong Kim Head of IRYoungsoo Won IR

Metso Flow Control Markus Hauhia Director, Global Valve Product LineWärtsilä Sung Bok Yoo Managing Director, Korea

Hans Lahej Area Sales DirectorNatalia Valtasaari IR

Cargotec Jeon Hong San Sales Director, KoreaHanjin Heavy Industries Sung Pill Lee Head of IR

Dong Ju Lee IRSeung Ho Yang General Manager, Shipbuilding SalesJae Won Kim Manager, Finance

Hyundai Heavy Industry Jeon Hong San Sales Director Korea, CargotecYong Un Park License Management, Wärtsilä KoreaEero Markkinen Director, 2SLM, Wärtsilä KoreaBanu Kannu GM Marketing, Wärtsilä Ship PowerPeik Jansson Business Dev., Oil and Gas, WärtsiläNatalia Valtasaari IR, Wärtsilä

We met with ten

companies in Japan

and nine in South

Korea

Sector report, January 9, 2015

10

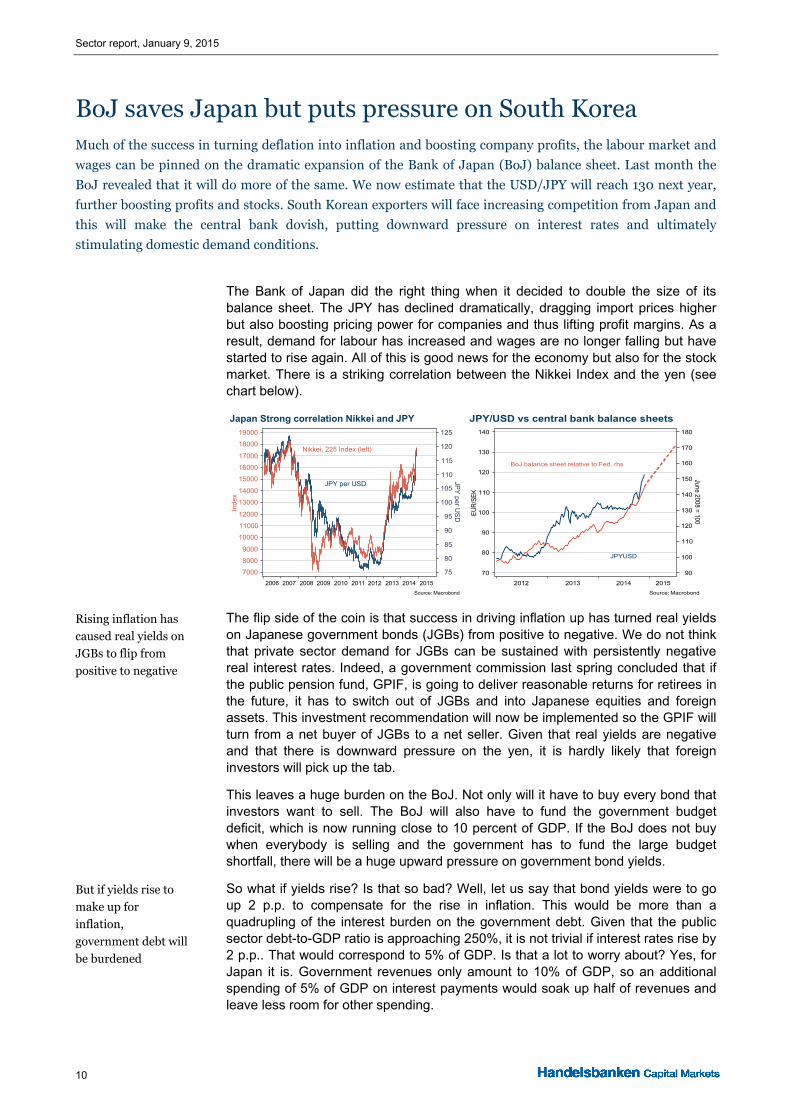

BoJ saves Japan but puts pressure on South Korea Much of the success in turning deflation into inflation and boosting company profits, the labour market and

wages can be pinned on the dramatic expansion of the Bank of Japan (BoJ) balance sheet. Last month the

BoJ revealed that it will do more of the same. We now estimate that the USD/JPY will reach 130 next year,

further boosting profits and stocks. South Korean exporters will face increasing competition from Japan and

this will make the central bank dovish, putting downward pressure on interest rates and ultimately

stimulating domestic demand conditions.

The Bank of Japan did the right thing when it decided to double the size of its balance sheet. The JPY has declined dramatically, dragging import prices higher but also boosting pricing power for companies and thus lifting profit margins. As a result, demand for labour has increased and wages are no longer falling but have started to rise again. All of this is good news for the economy but also for the stock market. There is a striking correlation between the Nikkei Index and the yen (see chart below).

Japan Strong correlation Nikkei and JPY

JPY per USD

Nikkei, 225 Index (left)

Inde

x

7000

8000

9000

10000

11000

12000

13000

14000

15000

16000

17000

18000

19000

JPY

per US

D

75

80

85

90

95

100

105

110

115

120

125

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Source: Macrobond

JPY/USD vs central bank balance sheets

JPYUSD

BoJ balance sheet relative to Fed, rhs

EU

R/S

EK

70

80

90

100

110

120

130

140

June 2008 = 100

90

100

110

120

130

140

150

160

170

180

2012 2013 2014 2015

Source: Macrobond

The flip side of the coin is that success in driving inflation up has turned real yields on Japanese government bonds (JGBs) from positive to negative. We do not think that private sector demand for JGBs can be sustained with persistently negative real interest rates. Indeed, a government commission last spring concluded that if the public pension fund, GPIF, is going to deliver reasonable returns for retirees in the future, it has to switch out of JGBs and into Japanese equities and foreign assets. This investment recommendation will now be implemented so the GPIF will turn from a net buyer of JGBs to a net seller. Given that real yields are negative and that there is downward pressure on the yen, it is hardly likely that foreign investors will pick up the tab.

This leaves a huge burden on the BoJ. Not only will it have to buy every bond that investors want to sell. The BoJ will also have to fund the government budget deficit, which is now running close to 10 percent of GDP. If the BoJ does not buy when everybody is selling and the government has to fund the large budget shortfall, there will be a huge upward pressure on government bond yields.

So what if yields rise? Is that so bad? Well, let us say that bond yields were to go up 2 p.p. to compensate for the rise in inflation. This would be more than a quadrupling of the interest burden on the government debt. Given that the public sector debt-to-GDP ratio is approaching 250%, it is not trivial if interest rates rise by 2 p.p.. That would correspond to 5% of GDP. Is that a lot to worry about? Yes, for Japan it is. Government revenues only amount to 10% of GDP, so an additional spending of 5% of GDP on interest payments would soak up half of revenues and leave less room for other spending.

Rising inflation has

caused real yields on

JGBs to flip from

positive to negative

But if yields rise to

make up for

inflation,

government debt will

be burdened

Sector report, January 9, 2015

11

Consequently, we think that the BoJ has ended up on a one-way street. Unlike the Fed, which has stopped buying US treasuries without creating any turmoil, the BoJ likely will have to keep on buying Japanese treasuries in order to prevent government debt funding costs from skyrocketing. Unless there is a spectacular turnaround in Japanese government finances, the BoJ might find itself pushing the JPY. We estimate that the USD/JPY will reach 130 next year if the BoJ continues to buy bonds in 2015 to the tune of JPY 80tr per year.

This will clearly have an impact on South Korean exporters, who compete with Japanese producers in many markets. The relative performance of the Korea Composite Stock Price Index (KOSPI) to the Nikkei illustrates how Japanese companies have gained compared to South Korean competitors.

Real Effective Exchange Rates (BIS)

South Korea

Japan

Inde

x

70

80

90

100

110

120

130

140

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Source: Macrobond

Nikkei vs Kospi

South Korea, KOSPI 50

Japan, Nikkei 225

Inde

x 20

10-0

1-02

70

80

90

100

110

120

130

140

150

160

170

2010 2011 2012 2013 2014

Source: Macrobond

The relative strength of the South Korean won (KRW) has led to a relative soft stance for Korean monetary policy. Money supply growth is approaching 10% and the policy rate has been cut by 125bp in 18 months down to 2%, a level not seen since the depth of the financial crisis in 2009. This is despite the fact that core inflation at the same time has doubled to close to 3%. No doubt, the aggressive Bank of Japan policy is having a spillover effect on South Korea. The situation is actually a little similar to the relationship between the ECB and the Swedish Riksbank.

Bond yields have also nosedived to a record-low 2.50 for the government 10-year bond. But although monetary conditions are expansionary, there has not yet been a dramatic impact on domestic demand conditions. Consumer confidence is rather bleak, resulting in relatively downbeat retail sales, and house prices are only rising moderately. Further depreciation of the Japanese yen might well put additional pressure for monetary easing in South Korea, in which case domestic demand is likely to pick up and compensate for adverse competitive conditions in export markets.

Jan Häggström, +46 8 701 197, jaha05

BoJ on a one-way

street

KRW’s strength has

softened monetary

policy; policy rate

now at its lowest

since 2009

Sector report, January 9, 2015

12

Shipbuilding: Slow steaming until 2016 demand pick-up The shipbuilding industry was a key reason for our trip to South Korea and Japan; these countries are of

global importance for the sector, with more than 50% of all ships being built (compensated gross tones, CGT)

in these countries. During our trip we met with the world’s two biggest shipbuilders, Hyundai Heavy and

Daewoo in South Korea, and with number five Mitsubishi Heavy Industries in Tokyo. We also met with a

smaller Korean shipbuilder, Hanjin, and the key Nordic suppliers to the shipbuilding industry of Alfa Laval,

Cargotec and Wartsila. The key common denominator from the meetings seemed to be that all of these

companies expect weak ship orders in 2015 following a very weak 2014 but that a general economic pick-up

will improve ship demand from 2016. For offshore, companies now seem to expect several hard years ahead.

Gas carrier demand signals are mixed. Based on our new knowledge and ship order data, we have built a

model to estimate 2015e-17e Marine orders and sales for the Nordic suppliers.

Executive summary Within Nordic engineering we maintain that shipbuilding-related orders are harder to estimate than most other segments despite access to ship order data on a monthly basis. Equipment order value by ship category and lead times makes estimates unusually difficult. In our search for a better understanding, we met with Hyundai Heavy Industry (global no. 1) and Daewoo Shipbuilding and Marine Engineering (DSME, global no. 2) in South Korea and Mitsubishi Heavy Industries (global no. 5) in Tokyo. We also met with the small Korean shipbuilder Hanjin and with all three big Nordic suppliers to the shipbuilding industry: Alfa Laval, Cargotec (MacGregor division) and Wartsila.

They all seemed to agree that ship orders will be weak in 2015 with a recovery expected in 2016. In 2015e, shipbuilders basically hope to book large container and LNG ship orders. The outlook for bulk ships, LPG carriers and offshore was said to be weak. On the back of this and the 2014 ship order collapse, we conclude that ship building-related orders are set to decline for Nordic suppliers in 2015.

The sole argument presented to us as to why 2016 ship orders might recover is a general global economic pick-up and yards offering heavy discounts, as they are getting increasingly desperate with overcapacity and too-low orders. We did not get the sense there would be new innovations or that any certain ship segment would see orders booming ahead. Notably, the merchant ship mini-boom in orders in H2 2013-Q1 2014 was driven primarily by heavy discounting and financing being available. As soon as order books at the yards were filled to a good level, yards hiked their prices, resulting in another collapse of orders. Due to lower oil prices the Koreans might be right about a general economic pick-up; but on the other hand, we note the record amount of vessels at anchor which could be run at healthy profitability with lower fuel costs, given that fuel typically amounts to ~50% of the total sailing cost in shipping.

South Korean yards are already starting to restructure, as 2014 orders have been far below budgeted levels, implying the order books are dropping below the critical two-year level at all major yards apart from DSME. The aim with restructuring for the Korean yards seems to be to regain competitiveness with cheaper Chinese yards (whose salaries are one third lower) for capacity in lower-tech merchant ships. They are forced to restructure, as it is obvious that offshore orders that filled the order books in 2010-13 will not come back soon. However, this strikes us as an act of desperation and not a long-term solution. Taking a 5-10 year perspective, we would bet that almost all production of merchant ships will move from South Korea

Companies we met

all expect weaker

orders in 2015, but

rising in 2016

Korean restructuring

a desperate act

against longer-term

perspective of China

taking over merchant

ship production

Sector report, January 9, 2015

13

to China. This would not be an issue for the Nordic suppliers that have equally good market positions in China as in South Korea.

We argue there are three reasons for the abnormally large ship orders in 2010-14:

High energy prices boosted orders for offshore vessels and gas carriers but also for new energy-efficient merchant vessels.

Too much shipbuilding capacity was built up in 2006-08, based on China’s seemingly endless need for raw materials and the world facing an energy challenge. Yards with too much capacity at hand enjoyed strong earnings in 2011-12 from old orders but almost all profits are now eroded, implying heavy discounting cannot continue. Instead, we expect shipbuilders to accelerate dock closures.

Cheap financing with private equity became an important source of financing during times of unusual central bank policies, with some regular banks exiting ship financing due to the high risks.

Looking ahead, we fear that all three of these factors will turn more negative, with the result of a reduced normal state for the shipbuilding industry. The oil price has been cut in half, implying there is less incentive to order new, more fuel-efficient vessels, and it looks as though a new ‘Ice Age’ awaits offshore investments. We also fear that lower oil prices will spill over into disappointingly low orders for gas carriers.

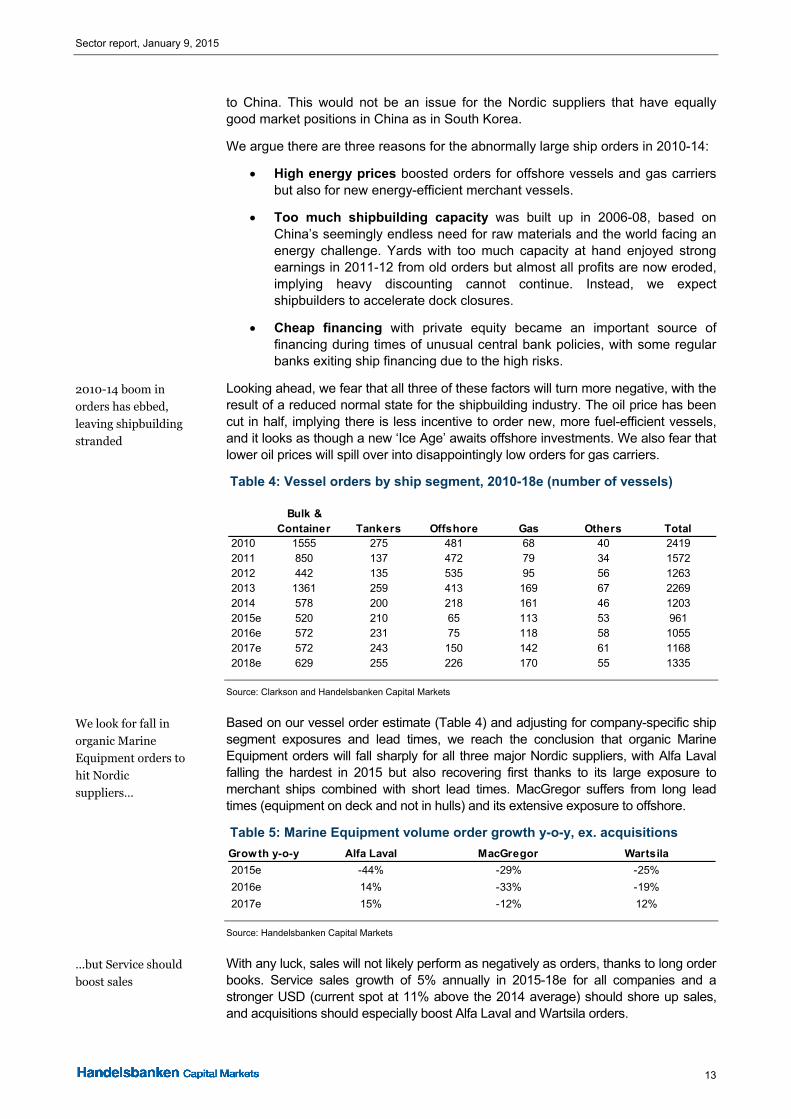

Table 4: Vessel orders by ship segment, 2010-18e (number of vessels)

Source: Clarkson and Handelsbanken Capital Markets

Based on our vessel order estimate (Table 4) and adjusting for company-specific ship segment exposures and lead times, we reach the conclusion that organic Marine Equipment orders will fall sharply for all three major Nordic suppliers, with Alfa Laval falling the hardest in 2015 but also recovering first thanks to its large exposure to merchant ships combined with short lead times. MacGregor suffers from long lead times (equipment on deck and not in hulls) and its extensive exposure to offshore.

Table 5: Marine Equipment volume order growth y-o-y, ex. acquisitions

Source: Handelsbanken Capital Markets

With any luck, sales will not likely perform as negatively as orders, thanks to long order books. Service sales growth of 5% annually in 2015-18e for all companies and a stronger USD (current spot at 11% above the 2014 average) should shore up sales, and acquisitions should especially boost Alfa Laval and Wartsila orders.

Bulk & Container Tankers Offshore Gas Others Total

2010 1555 275 481 68 40 24192011 850 137 472 79 34 15722012 442 135 535 95 56 12632013 1361 259 413 169 67 22692014 578 200 218 161 46 12032015e 520 210 65 113 53 9612016e 572 231 75 118 58 10552017e 572 243 150 142 61 11682018e 629 255 226 170 55 1335

Growth y-o-y Alfa Laval MacGregor Wartsila

2015e -44% -29% -25%

2016e 14% -33% -19%

2017e 15% -12% 12%

2010-14 boom in

orders has ebbed,

leaving shipbuilding

stranded

We look for fall in

organic Marine

Equipment orders to

hit Nordic

suppliers…

…but Service should

boost sales

Sector report, January 9, 2015

14

Table 6: Marine sales growth y-o-y in reported currencies*

Source: Handelsbanken Capital Markets

* Including acquisitions and Service

Exposure of Nordic suppliers to the shipbuilding industry Alfa Laval, Cargotec and Wartsila have remained key suppliers to the shipbuilding industry even though production of ships has moved almost completely to Asia. All Nordic suppliers have a very strong market position in South Korea, which for these suppliers is at least as important as the other leading shipbuilding nation of China.

To put Nordic supplier shipbuilding exposures into perspective, we begin by looking at the amount of sales in EURm that Nordic suppliers have to the Marine industry.

Figure 2: Nordic suppliers, Marine sales (EURm) in 2014e

Source: Handelsbanken Capital Markets

This means that Wartsila is the company having the largest relative exposure to the Marine industry for both sales and profits.

Figure 3: 2014e Marine exposure in Alfa Laval, Cargotec and Wartsila

Source: Handelsbanken Capital Markets

Alfa Laval MacGregor Wartsila

2015e 21% 12% 13%

2016e 2% -17% -4%

2017e 3% -11% -4%

0

500

1000

1500

2000

2500

3000

Alfa Laval Cargotec-MacGregor Wartsila

Equipment Service

0%

10%

20%

30%

40%

50%

60%

Alfa Laval Cargotec-MacGregor Wartsila

% of 2014e Sales % of 2014e EBIT

Wartsila has largest

relative exposure to

Marine

Wartsila is the big

play on shipbuilding

in the Nordics but it

is geared towards

specialised ships

rather than

merchant ships

Sector report, January 9, 2015

15

Next we notice that Wartsila, thanks to its huge installed base and relatively service-intensive products, has the greatest share of its Marine sales in Service. 97% of Wartsila’s Service sales are made to the company’s own installed base, and roughly half of Service sales are generated from spare parts and a quarter from field service, with the rest coming from projects and long-term contracts.

Figure 4: Share of Marine sales in Service

Source: Handelsbanken Capital Markets

Finally, we study the extent of exposure for each supplier by different ship segment. Here we note MacGregor has no sales to oil or gas tankers or any other special vessels apart from offshore. We also note Alfa Laval is very exposed to merchant vessels.

Figure 5: Q1-Q3 2014 orders split by four key ship segments

Source: Handelsbanken Capital Markets

Finally, we look at how large a share of the Nordic suppliers’ orders in the first nine months of 2014 came from up-, mid- and downstream activities in oil and gas.

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Alfa Laval Cargotec-MacGregor Wartsila

2014e share of Marine sales in Service

0%

10%

20%

30%

40%

50%

60%

Bulk & Container Tankers Offshore Gas Others

Alfa Laval Cargotec-MacGregor Wartsila

Wartsila has the

most developed

Service business out

of the three Nordic

Marine Equipment

suppliers

Very big differences

when it comes to

ship type exposures

Sector report, January 9, 2015

16

Figure 6: Oil & gas share of orders, Q1-Q3 2014, up-, mid- and downstream

Source: Handelsbanken Capital Markets

South Korean shipbuilding from past to present From a 30-year perspective the South Korean shipbuilding industry has been a major success story, as it has grown from nothing to the biggest shipbuilding nation in the world. However, in the aftermath of the financial crisis the Korean yards have struggled from increasingly fierce competition in merchant ships from Chinese yards. It appears as if the strong push to offshore will only be a temporary solution due to the foggy order outlook. Thus, Korean yards are now about to start restructuring to regain competitive ability against low-cost Chinese yards in the production of merchant ships.

Figure 7: Shipbuilding constantly moving between countries

Source: Wartsila and Clarksons

0%

5%

10%

15%

20%

25%

30%

Alfa Laval Cargotec Wärtsilä

Upstream Midstream Downstream

Tough future for

Korean yards despite

excellent history

Sector report, January 9, 2015

17

Table 7: Major yards in South Korea

Source: Wartsila

Profitability collapsing at major South Korean yards, triggering restructuring South Korean shipbuilding peaked in 2011 when 500 vessels were delivered, while approximately 400 will be delivered in 2014 with Hyundai Heavy Industry (HHI) representing half of the value. As the Chinese yards have improved significantly, the Korean yards have until recently managed to keep their leading position by switching production to more advanced ships, with offshore making up 60% (value in USD) of Korean yard orders in 2012. However, due to the lower oil price, this has now turned into a problem as the share of offshore has fallen to only 15% in the first nine months of 2014 while total orders have also collapsed.

Despite offshore deliveries still being high on the back of strong orders in 2011-13, the South Korean shipyards are currently fighting financial difficulties, with many struggling to deliver profits. 2014 is proving to be an even more difficult year than the tough 2013.

With 2014 orders disappointing, we think the outlook is far from promising for the South Korean yards. In H1 2014, South Korean shipbuilders won orders valued at USD 3.9bn, which is only 26% of the communicated FY 2014 target of USD 15bn. With yards not expressing any confidence in an order recovery in 2015 during our meetings and basically only pointing out hopes of a 2016 order recovery being based on improving global economic growth, we fear that the South Korean shipyards face difficult times ahead.

Offshore made up

only 15% of orders at

Korean yards in Q1-

Q3 2014 vs. 60% in

2012

Profitability already

low at Korean yards

despite still very high

delivery volumes

Sector report, January 9, 2015

18

Figure 8: Adj. net income (EURm) for top four South Korean shipbuilders

Source: FactSet

Figure 9: Share prices* for top South Korean shipbuilders

Source: FactSet

*EUR indexed to 100 five years ago

South Korean yards look set to lose market shares to Chinese yards During the boom years of 2005-08, Chinese yards built up massive but mostly unproductive capacity (a huge number of small yards). The South Korean yards still enjoy a size and productivity advantage over Chinese yards, but as the remaining Chinese yards improve and as Chinese salaries are about one third of Korean pay, it is not a wild guess to bet on Chinese yards increasing their market shares in the coming ten years.

The question, in our view, is whether any merchant ship production will be left in South Korea by 2025, or if Korean yards will fully concentrate on special ships. (During our trip, we heard Koreans even talking about starting to build cruise ships that are still made predominantly in Europe.) After the 2009 crisis many Korean yards have focused strongly on offshore applications. However, even if Korean yards shift entirely to special ships such as offshore and gas carriers, they will remain top customers for Alfa Laval, Cargotec and Wartsila, which all are important suppliers to special ship types.

-500

0

500

1,000

1,500

2,000

2,500

2009 2010 2011 2012 2013

Hyundai Heavy Industries Co., Ltd.

Daewoo Shipbuilding & Marine Engineering Co., Ltd

Samsung Heavy Industries Co., Ltd.

Hanjin Heavy Industries & Construction Co., Ltd

050

100150200250300350400

14/12/09 14/12/10 14/12/11 14/12/12 14/12/13

Hyundai Heavy Industries Co., Ltd. (Rebased)

Daewoo Shipbuilding & Marine Engineering Co., Ltd (Rebased)

Samsung Heavy Industries Co., Ltd. (Rebased)

Hanjin Heavy Industries & Construction Co., Ltd (Rebased)

Chinese salaries

appear to be about

one third of South

Korean

Korean merchant

shipbuilding clearly

at risk but Korean

yards will remain key

customers to Nordic

suppliers due to

strong position in

special vessels

Sector report, January 9, 2015

19

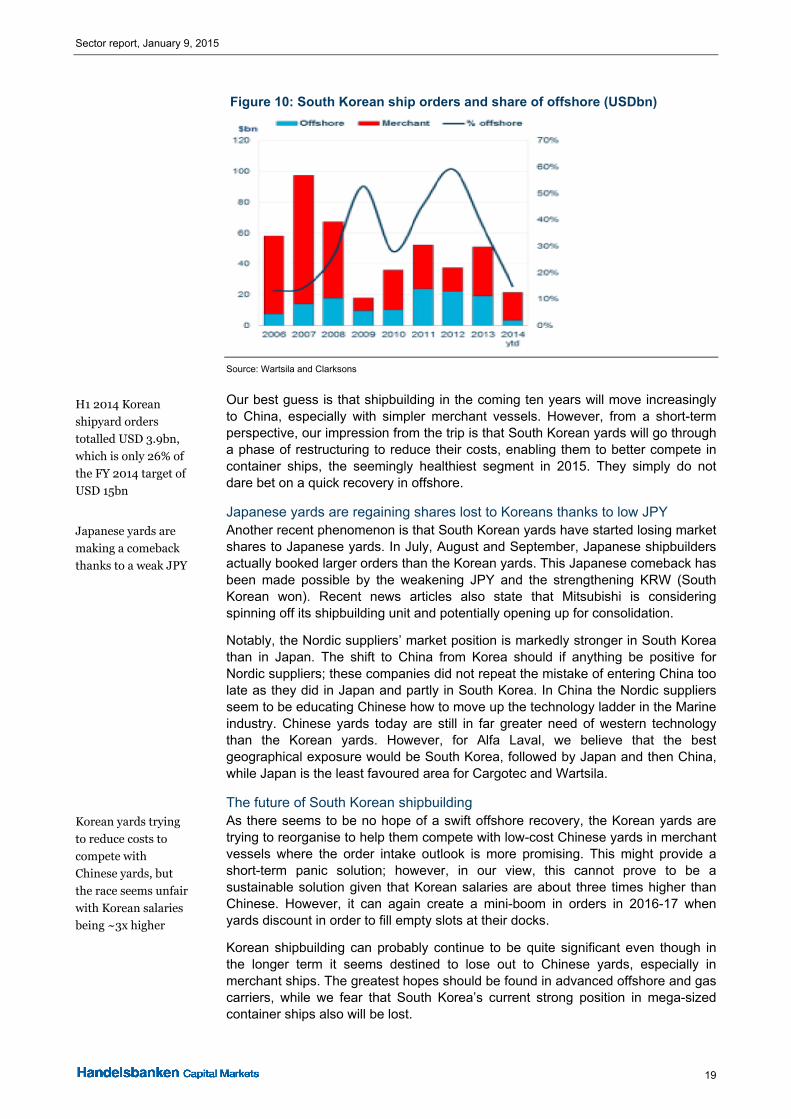

Figure 10: South Korean ship orders and share of offshore (USDbn)

Source: Wartsila and Clarksons

Our best guess is that shipbuilding in the coming ten years will move increasingly to China, especially with simpler merchant vessels. However, from a short-term perspective, our impression from the trip is that South Korean yards will go through a phase of restructuring to reduce their costs, enabling them to better compete in container ships, the seemingly healthiest segment in 2015. They simply do not dare bet on a quick recovery in offshore.

Japanese yards are regaining shares lost to Koreans thanks to low JPY Another recent phenomenon is that South Korean yards have started losing market shares to Japanese yards. In July, August and September, Japanese shipbuilders actually booked larger orders than the Korean yards. This Japanese comeback has been made possible by the weakening JPY and the strengthening KRW (South Korean won). Recent news articles also state that Mitsubishi is considering spinning off its shipbuilding unit and potentially opening up for consolidation.

Notably, the Nordic suppliers’ market position is markedly stronger in South Korea than in Japan. The shift to China from Korea should if anything be positive for Nordic suppliers; these companies did not repeat the mistake of entering China too late as they did in Japan and partly in South Korea. In China the Nordic suppliers seem to be educating Chinese how to move up the technology ladder in the Marine industry. Chinese yards today are still in far greater need of western technology than the Korean yards. However, for Alfa Laval, we believe that the best geographical exposure would be South Korea, followed by Japan and then China, while Japan is the least favoured area for Cargotec and Wartsila.

The future of South Korean shipbuilding As there seems to be no hope of a swift offshore recovery, the Korean yards are trying to reorganise to help them compete with low-cost Chinese yards in merchant vessels where the order intake outlook is more promising. This might provide a short-term panic solution; however, in our view, this cannot prove to be a sustainable solution given that Korean salaries are about three times higher than Chinese. However, it can again create a mini-boom in orders in 2016-17 when yards discount in order to fill empty slots at their docks.

Korean shipbuilding can probably continue to be quite significant even though in the longer term it seems destined to lose out to Chinese yards, especially in merchant ships. The greatest hopes should be found in advanced offshore and gas carriers, while we fear that South Korea’s current strong position in mega-sized container ships also will be lost.

H1 2014 Korean

shipyard orders

totalled USD 3.9bn,

which is only 26% of

the FY 2014 target of

USD 15bn

Japanese yards are

making a comeback

thanks to a weak JPY

Korean yards trying

to reduce costs to

compete with

Chinese yards, but

the race seems unfair

with Korean salaries

being ~3x higher

Sector report, January 9, 2015

20

South Korea enjoys a very strong market position in gas carriers Wartsila is today the only complete supplier of gas solutions in ships and its market share is above 70% in LNG carriers produced in South Korea. Thus, Korea’s strong push in LNG carriers should benefit Wartsila. This is also important for Alfa Laval given the value of equipment in those ships. We got the impression that South Korean yards are strongly pushing LNG-fuelled merchant vessels. However, we also sensed that it is too early to bet on merchant ships turning to gas in the next couple of years also in newbuilds. Most definitely the strong slide in the oil price will further postpone this transfer to LNG fuelled Merchant ships. However, this trend presents an interesting long-term opportunity for South Korean yards and Wartsila. For Alfa Laval, though, a transformation to gas engines might slightly drive up value for equipment aside from the engines, but scrubbers would not be needed, which would negative some of the benefits to Alfa from a switch to LNG.

The likely outcome of this is that South Korean yards must restructure and cut prices heavily. However, we do not believe Wartsila and Alfa Laval will be forced, to any major extent, to cut their prices despite ship prices falling. Another key conclusion from our meeting was that it still feels too early to bet on merchant ships turning to LNG as a main fuel in the next couple of years.

‘Koreanisation’ and its impact for Nordic suppliers South Korea is ambitiously climbing the technology ladder in shipbuilding, as shown by the manufacturing of advanced offshore vessels taking place now mainly by Korean shipbuilders. In Korea there is a strong push for Koreanisation, i.e. the use of more technologies developed and produced in South Korea. This might naturally be a long-term threat to companies such as Alfa Laval, Wartsila, Cargotec and Rolls-Royce. However, we still got the impression that the Korean companies have not really managed to position themselves to, for instance, take the lead in 4-stroke mid-speed engines due to lack of a service network and references, despite HHI having produced Himsen engines for more than a decade.

In our view, it actually appeared as if the Korean engineering skills are in material technology (strength of materials, etc.) rather than in developing new shipping concepts and fuel-saving designs. It appears that the epicentre of this innovation is still in Norway. According to Wartsila, Koreans are slowly building Service capabilities, but it will take many years before they become a threat to companies such as Wartsila and Alfa Laval.

Things to consider when studying the outlook for ship orders Long-term ship orders are naturally a function of demand/supply in sea transportation. However, the world is not quite that simple. Thus, we continue by describing other key drivers for ship orders that must be taken into account when building our forecast models.

Number of ships ordered and value are two completely different things A mega-sized 19,000 TEU container ship is priced at only USD 120m (according to HHI) vs. the largest bulk ship (Capesize) carrying a price of USD 550m (according to DSME), while the price of a FPSO stretches up to USD 2-3bn or more per unit. There is also a great variation between the different ship segments when it comes to the delivery value per vessel for the Nordic suppliers.

Korean yards

strongly pushing

LNG-fuelled

merchant vessels but

customers do not

seem eager to order

in coming years

Still too early to bet

on merchant ships

turning to LNG as a

main fuel

Strong push for more

local content but lack

of Korean innovation

in shipbuilding

despite excellent

quality

Sector report, January 9, 2015

21

Figure 11: Ship orders by type and country

Source: Samsung Heavy Industries

Longer cycles than in other industries Delivery times are generally exceptionally long in the shipbuilding industry but they also vary greatly between different ship segments. Merchant ships typically have two years from order to delivery while offshore vessels have three years and FPSOs four years, and oil platform order-to-deliver times stretch even to five years.

During our meetings in South Korea, we concluded that shipbuilders think an order backlog of two to two and a half years is ideal. If the order backlog goes below two years, the yards typically start heavy discounting. Currently 97% of all shipbuilders today have a backlog below two years, according to DSME, which itself has a backlog of 2.3 years.

The long cycles in the shipbuilding industry mean book-to-bill goes from very low to very high levels. When prices bottom out, some customers typically start speculative buying, and then everybody is in a hurry to order.

China has overtaken

South Korea’s

leading position as

ship builder

Sector report, January 9, 2015

22

Table 8: DSME ship orders and backlog

Source: DSME

Figure 12: Yard contracting and deliveries

Source: Alfa Laval, Clarksons

Pricing New shipbuilding prices recovered as the big yards returned to a healthy order book length during the mini-boom in H2 2013 and Q1 2014. This triggered shipbuilders to raise prices but orders disappeared immediately, signalling there are no strong underlying fundamentals at the moment.

At the end of October 2014 the world’s largest shipbuilder, HHI, had booked vessel orders YTD amounting to USD 4,936m, while the FY 2014 target has been set at USD 9,150m, implying that only 54% of the 2014 target had been reached with

H2 2015 and Q1

2014 saw a rebound

that has played out

Sector report, January 9, 2015

23

only two months left in the year. No doubt, we are again approaching a heavy discounting season.

According to DSME the price of a ship is the most important factor, followed by lead time and quality. This naturally differs depending on ship type and owner. The expected lifetime for a vessel starts at 20 years for a simple carrier and ranges up to 40 years for an oil production structure.

Figure 13: Newbuild price trend

Source: HHI and Clarksons

Scrap prices Another factor to take into account is the scrap prices of vessels due for retirement. The Chinese government has worked with this tool, for instance, when shipyards have had low order books.

Financing European banks were the key sources of financing until 2008, but their share has now fallen from 80% to 60% with some major banks exiting ship financing. When no one else ordered vessels, private equity suddenly began to order ships.

Currency swings between shipbuilding nations Currency movements make up the greatest cost item between shipbuilding nations that yards cannot control or hedge longer term. Currently, Japan is making a comeback in shipbuilding thanks to the low JPY.

‘Invest or die’ phenomenon The shipping industry has through the years experienced a lot of technological breakthroughs that have reduced the cost of shipping. As soon as one shipping company orders a more fuel-efficient vessel, its competitors must do the same to stay competitive. Currently, this can be seen in Maersk’s Triple E 18,000-TEU container ships soon getting competition from even larger container vessels.

In addition to larger ships, key innovations have been revolutionary hull designs and slow steaming. Our impression after visiting South Korea and Japan is that innovations still come mainly from Europe.

Large need for global aftersales activities Many buy ships purely on speculation. These and basically all advanced shipowners want to own a liquid asset that can be sold. This however demands well-known brands and global aftersales on everything that can break down. Based on our meetings, we conclude that the South Korean shipbuilders are slowly trying

Big drop in newbuild

prices in 2009-10,

followed by

stagnancy

Sector report, January 9, 2015

24

to build up service activities, but that western companies still have more than a twenty-year head start in this field.

Green shipping Shipping is subject to limited regulation when compared to land-based traffic. However, things are now changing with the IMO introducing new regulations on SOx and NOx emissions and ballast water treatment.

Different dynamics in different shipping segments Ship buyers also need to take the different business dynamics into account. Within LNG, LPG and FSRU, more than 80% of the vessels run on charter rates, while spot rates are usual in bulk and container shipping. A higher share of charter rates naturally decreases the risk level when ordering a ship.

Order intake comments by ship segment from companies we met in Asia We start by highlighting comments made by the companies we met on the different ship types:

Bulk: The bulk shipping market may improve in line with global economic recovery from 2015 (DSME). The problem is that the economic recession in emerging markets has slowed down the need for iron ore. However, will the low raw material prices turn into a demand improvement? Hanjin foresees that bulk shipping will remain poor.

Container: All of the companies we met see the greatest chance for 2015 order growth in container ships.

Figure 14: Trade fleet growth and container ship orders

Source: Samsung Heavy Industries and Clarksons

Tanker: There are signs of demand picking up, according to general comments by the companies we met. Hanjin sees some demand for crude oil and chemical bunkers. The low oil price should support demand for gasoline and diesel.

Gas: Strong growth for global LNG demand is pushing the LNG industry to embrace the concept of FSRU, which could replace onshore storage terminals. LNG trading volumes will increase with Australia’s exports of offshore gas and US shale gas from 2017. Considering a three-year building period, ship owners need to place LNG orders by 2015 at the latest to meet the exporting schedule in 2017. 410 LNG vessels today are in operation out of a total global vessel fleet of more than 22,000. DSME sees 10-15% CAGR in LNG carriers in the next ten years. However, what would happen to investment with a lower oil price? There was news out on December 3 that Petronas informed the government of Canada that it will defer a decision on a huge USD 36bn LNG export terminal complex proposed for the West Coast of Canada. Also, Santos, which is developing a huge LNG project in Australia, announced that it is delaying a plan to raise capital and that it plans to make significant cuts to both capex and opex in 2015.

Fleet capacity

outgrowing trade

growth for many

years, forcing

shipping companies

to also anchor fairly

new vessels

Sector report, January 9, 2015

25

LPG: Many LPGC orders have already been placed so additional orders could be limited, according to DMSE.

LNG: DSME said that the outlook for LNG carriers is better for LNG than for LPG. The key argument is that significant infrastructure projects are in the pipeline. However, this might change with a lower energy price, when the attractiveness of LNG as a substitute for oil decreases, which also implies a narrower price difference between US gas and Russian gas. In Japan, however, Mitsubishi Heavy Industry said it is not seeing any gas turbine orders, suggesting Japan will soon restart a significant share of its currently closed nuclear power plants. The company also said that the LNG ship orders it has booked recently should be seen as replacement orders, rather than Japan preparing for a nuclear-free future in which gas would be a more important component in energy generation.

Background to our ship order intake forecasts Based on comments from the companies we met in Asia and on the recent oil price collapse, we have every reason to believe 2015 will be difficult for Asian shipyards and thereby, with company-specific lags, the year will also be tough for Nordic equipment suppliers. We highlight that ship order comparisons y-o-y remain very difficult in Q1 2015e.

Ship orders have at least partly been better than they rationally should have been in 2010-14, given the high amount of ships at anchor.

Figure 15: Anchored vessels and fleet development

Source: Wartsila and Bloomberg

We maintain that three reasons pushed ship orders unrealistically high in 2010-14 and increased the risk of a catch-up period in 2015-18:

High energy prices boosted ship orders to irrational levels

Shipbuilding capacity built up during the boom years will now be closed

Cheap financing for shipbuilding might end

High energy prices boosted ship orders to irrational levels High energy prices in 2010-14 pushed up orders for offshore vessels and gas carriers but also for new energy-efficient merchant vessels. Now the oil price has been cut in half, implying vessels put at anchor can again be used profitably. We also fear there will be a coming ‘Ice Age’ for offshore investments and that spillover effects will lead to lower-than-expected demand for gas carriers.

Shipbuilding capacity built up during boom years will now be closed Too much shipbuilding capacity was built up in 2006-08. Before the boom an average of 1,500 ships were ordered annually, but at the peak of the boom as many as 5,000 ships were ordered in one year. China advanced greatly in shipbuilding during this hectic period, and all major Korean yards also invested

2015 likely to be the

Year of the Sheep in

orders, too

Slashed oil price

could float some

anchored vessels

Shipbuilding boom

has gone bust…

Sector report, January 9, 2015

26

heavily. Yards with too much capacity at hand have since then offered heavy discounting in 2010-14 to fill up capacity instead of closing down docks. Now, in contrast to 2011-12 when shipbuilders still delivered orders taken at great prices during the boom, the entire industry is suffering from low profitability. In our view, this suggests that yards will close down capacity and end crazy discounting. With lower capacity available, the number of ships ordered will also decline ahead, leading to a smaller available market for the Nordic equipment suppliers.

Cheap financing for shipbuilding might end Cheap financing with private equity becomes an important source of financing at times of unusual central bank policies, and some regular banks exited ship financing due to the high risks and a prolonged period of very low profitability in shipping in general. Unless private equity companies succeed in making profits on their investments in shipping, there is an increased risk that money available for shipbuilding will decrease ahead, as some banks have made irreversible decisions to exit ship financing.

Our ship order estimates 2014 ship orders were a great disappointment to shipyards, with hardly any reaching budgeted orders. This means almost all shipbuilders are starting 2015 with order books below optimal 2-year levels. DSME said as many as 97% of all shipbuilders currently have an order book below this benchmark.

Figure 16: 2014 growth y-o-y, in numbers of ships

Source: Clarkson

Based on the arguments presented above and on our impressions from meetings in South Korea and Japan, tough times will continue in 2015 at the least, despite yards offering hefty discounts. For 2015 we see scope for order growth only in tankers (lower oil prices should shoot up demand) and in ‘Others’, where strong consumerism coupled with new environmental regulations should lead to renewed interest in cruise ship and passenger ferry orders. Looking into 2016 we see a high likelihood for an order recovery especially in container ships.

Table 9: HCMe 2015-18 ship order growth y-o-y (number of ships)

Source: Handelsbanken Capital Markets

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

Bulk & Container Tankers Offshore Gas Others

Bulk & Container Tankers Offshore Gas Others2015e -10% 5% -70% -30% 15%2016e 10% 10% 15% 5% 10%2017e 0% 5% 100% 20% 5%2018e 10% 5% 50% 20% -10%

…and shipbuilding

money likely to

tighten

Tanker, cruise ship

and ferry orders

could give some

relief to tough 2015e

Sector report, January 9, 2015

27

Table 10: Number of ships ordered annually by key segments

Source: Clarkson and Handelsbanken Capital Markets

We continue by presenting our scenario in detail for the five key different ship types for the 2015e-18e order intake outlook.

Bulk and container ship order intake outlook, 2015e-18e We expect bulk and container ship orders to fall moderately by 10% y-o-y in 2015 given tough comparisons in Q1. In 2016 we expect a 10% order recovery boosted by global consumption growth stemming from lower oil prices. Fundamentals are certainly negative for merchant ship orders at the moment, but simultaneously the world has an almost given shipbuilding capacity that can decrease only slowly, forcing yards to provide heavy discounting to sustain work. There is a record amount of ships at anchor and all of the companies we met in South Korea and Japan cannot see a 2015 recovery for bulk ship orders. Their pessimism is based on the slowdown of the Chinese economy and the great orders in 2013 that were boosted at least partly private equity companies entering the scene as major shipbuilding financers, when banks restricted lending to shipping in the aftermath of the financial crisis.

However, lower oil prices should start to boost private consumption and thereby the demand for container ships. Furthermore, the introduction of Maersk’s Triple E-class vessel is now forcing other container lines to order ultra-large container vessels if they want to stay in business. We understand that oil consumption per container is up to 40% lower in these ships than in five-year-old large container vessels. Finally, we also highlight that the short order books of many shipbuilders are forcing them to offer heavy discounting in 2015. However, on the negative side, we expect several ship yards to close in 2015 and Korean yards to start heavy restructuring for the first time, implying a decline in total shipbuilding capacity.

Figure 17: Bulk and container ship orders in number of ships, 12-month rolling

Source: Clarkson and Handelsbanken Capital Markets

Bulk & Container Tankers Offshore Gas Others Total

2010 1555 275 481 68 40 24192011 850 137 472 79 34 15722012 442 135 535 95 56 12632013 1361 259 413 169 67 22692014 578 200 218 161 46 12032015e 520 210 65 113 53 9612016e 572 231 75 118 58 10552017e 572 243 150 142 61 11682018e 629 255 226 170 55 1335

0

200

400

600

800

1000

1200

1400

1600

1800

2010-Q4

2011-Q1

2011-Q2

2011-Q3

2011-Q4

2012-Q1

2012-Q2

2012-Q3

2012-Q4

2013-Q1

2013-Q2

2013-Q3

2013-Q4

2014-Q1

2014-Q2

2014-Q3

2014-Q4

2015-Q1e

2015-Q2e

2015-Q3e

2015-Q4e

2016-Q1e

2016-Q2e

2016-Q3e

2016-Q4e

2017-Q1e

2017-Q2e

2017-Q3e

2017-Q4e

2018-Q1e

2018-Q2e

2018-Q3e

2018-Q4e

Merchant (Bulk & Container)

10% y-o-y drop

expected in 2015e

Maersk Triple E

could spur ultra-

large orders

Sector report, January 9, 2015

28

Oil and chemical tanker orders in 2015e-18e We expect the lower oil price to increase demand for oil and chemical products in the coming years. Thus, there will be a greater need for oil and chemical transportation capacity.

Figure 18: Oil & chemical tanker orders in number of ships, 12-month rolling

Source: Clarkson and Handelsbanken Capital Markets

Offshore vessel orders in 2015e-18e We expect offshore orders to remain under severe pressure given the low oil price. As the oil price seems lately to have stabilised at a low level, nobody seems willing any more to speculate about a quick price recovery to USD 100/bbl. Thus, we fear offshore orders will be weaker for a longer period, and some observers are starting to speculate about a new ‘Ice Age’ for deepwater oil investments. Notably, yards have some time to adjust capacity and wait for a recovery, as delivery times are exceptionally long, with some deliveries for the current order book taking place in 2018.

Figure 19: Offshore ship orders in number of ships, 12-month rolling

Source: Handelsbanken Capital Markets

Gas carrier order outlook in 2015e-18e Shipbuilders and suppliers put great faith in strong gas carrier orders ahead. We argue that this could be a false hope, with this segment potentially providing the

0

50

100

150

200

250

300

350

2010-Q4

2011-Q1

2011-Q2

2011-Q3

2011-Q4

2012-Q1

2012-Q2

2012-Q3

2012-Q4

2013-Q1

2013-Q2

2013-Q3

2013-Q4

2014-Q1

2014-Q2

2014-Q3

2014-Q4

2015-Q1e

2015-Q2e

2015-Q3e

2015-Q4e

2016-Q1e

2016-Q2e

2016-Q3e

2016-Q4e

2017-Q1e

2017-Q2e

2017-Q3e

2017-Q4e

2018-Q1e

2018-Q2e

2018-Q3e

2018-Q4e

Merchant (Oil & Chemical tankers)

0

100

200

300

400

500

600

2010-Q4

2011-Q1

2011-Q2

2011-Q3

2011-Q4

2012-Q1

2012-Q2

2012-Q3

2012-Q4

2013-Q1

2013-Q2

2013-Q3

2013-Q4

2014-Q1

2014-Q2

2014-Q3

2014-Q4

2015-Q1e

2015-Q2e

2015-Q3e

2015-Q4e

2016-Q1e

2016-Q2e

2016-Q3e

2016-Q4e

2017-Q1e

2017-Q2e

2017-Q3e

2017-Q4e

2018-Q1e

2018-Q2e

2018-Q3e

2018-Q4e

Offshore

Lower oil price

expected to keep

tanker orders

buoyant

Offshore orders

taking a hit from

sagging oil price

Sector report, January 9, 2015

29

biggest disappointment in 2015, when we expect orders to fall by 30% y-o-y when calculating the number of vessels.

The yards we visited in Asia remained optimistic about the gas carrier order outlook, even if they acknowledge LPG orders likely will decline from exceptionally high levels. However, the outlook for LNG vessels was said to be quite robust.

However, after we heard these statements, the oil price has fallen so sharply that we fear some potential buyers of LNG ships will postpone planned orders while they watch what happens to energy prices generally. Perhaps shipping gas from the US to Europe is not such a great idea after all if the oil price stabilises at USD 50/bbl or even lower. Order volumes should not implode, however, as some 80% of gas carriers run on long-term charter rates. However, in the longer term, gas carriers should be a growth segment due to the environmental benefits of gas vs. oil. Thus, we expect a moderate 5% order recovery in 2016 followed by even stronger growth in 2017e-18e.

‘Other’ ship segment order outlook in 2015e-18e We expect orders for ‘Other’ special ship segments (including fishing boats, harbor tugs, cruise ships, ferries, Ro-Ro wheeled cargo carriers, etc.) to show the best growth in the coming years. The outlook seems especially promising for cruise ship orders given US consumer strength and the evolution of cruise holidays in Asia. Ferry and RoRo vessel orders can also be boosted by strengthened SOx emission rules which are now being enforced.

Figure 20: Gas and Other ship orders in number of ships, 12-month rolling

Source: Handelsbanken Capital Markets

Our order intake forecast model for Alfa, MacGregor and Wartsila Ship Power After presenting our vessel order scenario above, we continue by studying the Nordic suppliers’ different exposures by the five ship types: Bulk and container, Tankers, Offshore, Gas and Others. We then look at the demand outlook by different ship segment and thus obtain an estimate for 2015-17 equipment order growth for within the respective marine businesses of Alfa Laval, Cargotec (MacGregor) and Wartsila.

0

50

100

150

200

2502010-Q

42011-Q

12011-Q

22011-Q

32011-Q

42012-Q

12012-Q

22012-Q

32012-Q

42013-Q

12013-Q

22013-Q

32013-Q

42014-Q

12014-Q

22014-Q

32014-Q

42015-Q

1e2015-Q

2e2015-Q

3e2015-Q

4e2016-Q

1e2016-Q

2e2016-Q

3e2016-Q

4e2017-Q

1e2017-Q

2e2017-Q

3e2017-Q

4e2018-Q

1e2018-Q

2e2018-Q

3e2018-Q

4e

Gas Others

Long-term charter

rates should help

2016e order recovery

Consumer strength

steering ‘Other’

outlook

Sector report, January 9, 2015

30

Figure 21: Q1-Q3 2014 orders split by five key ship segments

Source: Handelsbanken Capital Markets

The next step is to note the significant differences in lead times from the vessel order to when the Nordic supplier books its orders. The reason for MacGregor’s comparatively long lead times is that its equipment is installed on the topside of a vessel, while Alfa Laval and Wartsila deliver equipment built into the hull of a vessel.

Table 11: Lead times from vessel order to equipment order, by ship type

Source: Handelsbanken Capital Markets

To smooth out the order volumes, compared to the hefty volatility in vessel orders that might show extreme peaks and valleys, we distribute the 6-18 month lead times between quarters.

Table 12: Lead time distribution

Source: Handelsbanken Capital Markets

Compiling the order and lead time information, and also adjusting for seasonality patterns, we conclude that 2015e will be a very tough year for the Nordic suppliers, with Alfa Laval, MacGregor and Wartsila showing organic equipment order declines of 44%, 29% and 25% respectively. Tough times should first turn into order growth for Alfa Laval, thanks to its large exposure to container vessels and oil tankers combined with the relatively short lead times. In contrast MacGregor will continue to suffer in 2016e and 2017e due to its long lead times and substantial exposure to offshore.

0%

10%

20%

30%

40%

50%

60%

Bulk & Container Tankers Offshore Gas Others

Alfa Laval Cargotec-MacGregor Wartsila

Alfa Laval MacGregor Wartsila

Bulk & Container 6 12 6

Tankers 6 12 6

Offshore 6 18 12

Gas 6 12 9

Others 6 12 6

Months/Quarter -3 -2 -1 0 1 2 3

6 15% 60% 25%

9 5% 15% 55% 20% 5%

12 5% 20% 45% 25% 5%

18 5% 10% 15% 35% 20% 10% 5%

Topside installation

draws out

MacGregor’s lead

time

Tough times await

Marine in 2015e, but

Alfa should rebound

more quickly

Sector report, January 9, 2015

31

Table 13: Marine Equipment order growth y-o-y in constant currencies ex. acquisitions