section 2: an adverse spiral develops. chart 2.1 international gdp growth forecasts source:...

TRANSCRIPT

Section 2: An adverse spiral

develops

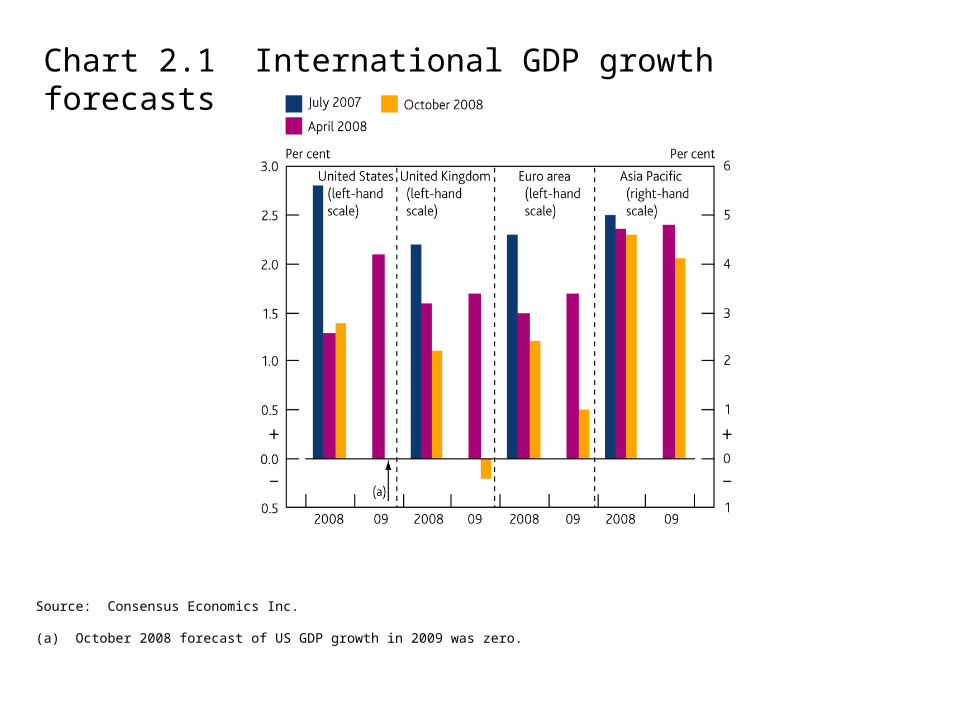

Chart 2.1 International GDP growth forecasts

Source: Consensus Economics Inc.

(a) October 2008 forecast of US GDP growth in 2009 was zero.

Chart 2.2 UK house prices and activity

Sources: Bank of England, Halifax, HM Treasury, Nationwide and Bank calculations.

(a) October 2007.(b) House price projections are based on a range of forecasts from ‘Forecasts for the UK economy: a comparison of independent forecasts’, October 2008 (compiled by HM Treasury), as represented by the orange shaded area.(c) Average of Halifax and Nationwide house price indices.

Chart 2.3 Loan to value ratios in selected UK house price fall scenarios(a)

Sources: 2008 NMG Research survey and Bank calculations.

(a) NMG Research survey conducted between 19 September and 2 October 2008.

Chart 2.4 Spreads on mortgage products by credit quality of borrower(a)

Sources: Bank of England, Bloomberg, Moneyfacts Group and Bank calculations.

(a) Spread of quoted mortgage rates over final observation of maturity-matched swap rate from previous month.(b) Average of three-year fixed-rate mortgages.(c) Five-year fixed-rate mortgage. September 2008 data provisional.(d) The size of the sample on which these data are based has fallen markedly since the start of the financial market turmoil: the most recent data (September 2008) are based on only three products; in July 2007, data were based on a sample of twelve products.

Chart 2.5 Share of corporate debt accounted for by businesses with interest payments greater than profits(a)(b)

Sources: Bureau van Dijk and Bank calculations.

(a) Non-financial firms of at least 100 employees.(b) Profits are defined as earnings before interest and tax.

Chart 2.6 Decomposition of sterling-denominated investment-grade corporate bond spreads(a)(b)

Sources: Bloomberg, Merrill Lynch, Thomson Datastream and Bank calculations.

(a) Webber, L and Churm, R (2007), ‘Decomposing corporate bond spreads’, Bank of England Quarterly Bulletin, Vol. 47, No. 4, pages 533–41.(b) Option-adjusted spreads over government bond yields.(c) April 2008 Report.

Chart 2.7 European and US speculative-grade corporate default rates and forecasts(a)(b)

Source: Moody’s Investors Service.

(a) Trailing twelve-month issuer-weighted speculative-grade corporate default rates.(b) Solid lines show historical data. Dashed lines show Moody’s forecasts for October 2008 to September 2009.

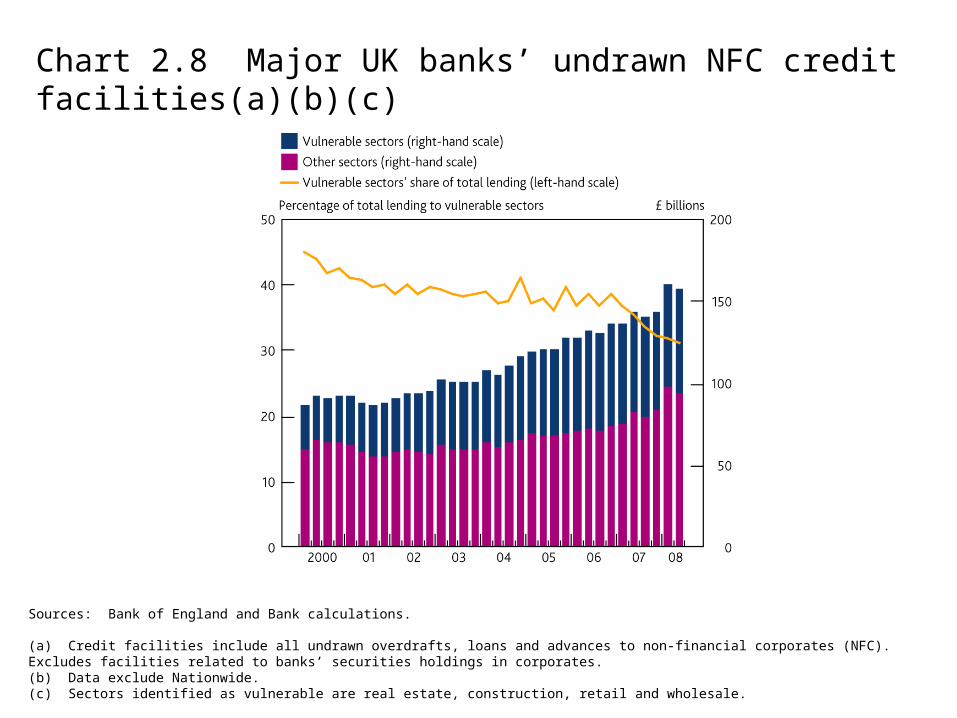

Chart 2.8 Major UK banks’ undrawn NFC credit facilities(a)(b)(c)

Sources: Bank of England and Bank calculations.

(a) Credit facilities include all undrawn overdrafts, loans and advances to non-financial corporates (NFC). Excludes facilities related to banks’ securities holdings in corporates.(b) Data exclude Nationwide.(c) Sectors identified as vulnerable are real estate, construction, retail and wholesale.

Chart 2.9 Global residential mortgage-backed securities issuance(a)

Sources: Dealogic and Bank calculations.

(a) Non-retained issuance proxied by issuance eligible for inclusion in underwriting league tables. Retained issuance proxied by issuance not eligible for inclusion.(b) This includes RMBS used as collateral in central bank operations.(c) Shaded area is total up to 20 October 2008.

Chart 2.10 Bid-ask spreads on UK residential mortgage-backed securities(a)(b)

Sources: Markit Group Limited and Bank calculations.

(a) Spread between the average bid and ask prices quoted by dealers for UK RMBS.(b) Five-day centred rolling average.(c) April 2008 Report.

Chart 2.11 Anomalies in prices of the ABX sub-prime index (2007 H1 vintage)(a)(b)

Sources: JPMorgan Chase & Co. and Bank calculations.

(a) The pricing model is an adaptation of that used in ‘A simple CDO valuation model’, Bank of England Financial Stability Review, Box 1, December 2005, pages 105–06.(b) For the purposes of this chart, the loss given default rate is assumed to be 50%.(c) 19 January 2007.(d) 13 July 2007.

Chart 2.12 Major UK banks’ and LCFIs’ write-downs and capital issuance since 2007 Q3 (a)

Sources: Bloomberg, company releases, published accounts and Bank calculations.

(a) Issuance qualifying for total capital must have been completed or announced between 2007 Q3 and 20 October 2008. Total capital raised was US$460 billion, of which 37% was common equity.

(b) Includes write-downs due to mark-to-market adjustments on trading book positions where details have been disclosed by firms.(c) Issuance announced on or after 13 October 2008.

Table 1 Mark-to-market losses on selected financial assets(a)(b)

Outstanding Losses: Apr. Losses: Oct.amounts 2008 Report 2008 Report

United Kingdom (£ billions)Prime residential mortgage-backed securities 193 8.2 17.4Non-conforming residential mortgage-backed securities 39 2.2 7.7Commercial mortgage-backed securities 33 3.1 4.4Investment-grade corporate bonds 450 46.2 86.5High-yield corporate bonds 15 3.0 6.6Total 62.7 122.6

United States (US$ billions)Home equity loan asset-backed securities (ABS)(c) 757 255.0 309.9Home equity loan ABS collateralised debt obligations (CDOs)(c)(d) 421 236.0 277.0Commercial mortgage-backed securities 700 79.8 97.2Collateralised loan obligations 340 12.2 46.2Investment-grade corporate bonds 3,308 79.7 600.1High-yield corporate bonds 692 76.0 246.8Total 738.8 1,577.3

Euro area (€ billions)Residential mortgage-backed securities(e) 387 21.5 38.9Commercial mortgage-backed securities(e) 34 2.8 4.1Collateralised loan obligations 103 6.8 22.8Investment-grade corporate bonds 5,324 283.8 642.9High-yield corporate bonds 175 29.1 75.9Total 344.1 784.6

Source: Bank calculations.

(a) Estimated loss of market value since January 2007, except for US collateralised loan obligations which are losses since May 2007.(b) Data to close of business on 20 October 2008.(c) 2005 H1 to 2007 H2 vintages. The home equity loan asset class is comprised mainly of US sub-prime mortgages, but it also includes, for example, other mortgages with high loan to value ratios. Home equity loans are of lower credit quality than US Alt-A and prime residential mortgages.(d) High-grade and mezzanine ABS CDOs, excluding CDO-squareds.(e) Germany, Ireland, Italy, Netherlands, Portugal and Spain.

Chart A AAA-rated UK prime RMBS and US sub-prime RMBS spreads(a)(b)

Sources: JPMorgan Chase & Co. and Nomura.

(a) ABX.HE 2006-1 credit default swap premia and five-year UK prime RMBS spread over Libor.(b) Data to close of business on 20 October 2008.(c) April 2008 Report.

Chart B Credit losses on UK prime RMBS(a)(b)

Source: Bank calculations.

(a) Loss of principal assuming a loss given default of 45%, and adjusting the composition of the collateral pool every six months to account for partial principal amortisation using mortgage pre-payments.(b) AA-rated and AAA-rated tranches start to be eroded when loss rates on the mortgage collateral pool reach 5.8% and 9.2% respectively.

Chart C Comparison of mark-to-market losses on UK prime RMBS and US sub-prime RMBS(a)

Source: Bank calculations.

(a) Data to close of business on 20 October 2008.(b) Percentage of mark-to-market losses explained by expected credit losses. Actual credit losses are likely to be significantly lower for UK prime RMBS than US sub-prime RMBS.

Chart D Estimated pre-crisis investor base in UK prime RMBS by institution type and rating(a)

Sources: Citi, European Securitisation Forum, JPMorgan Chase & Co. and Bank calculations.

(a) Estimated from a number of investment bank surveys relating to the period 2004–06.(b) Includes money market funds.(c) Includes supranational, sovereign wealth funds and agencies.