sec doj enforcement trends 2017 - ey · 2yhu ploolrq sdlg wr dssur[lpdwho\ zklvwoheorzhuv vlqfh...

TRANSCRIPT

What doyou want toachieve?

Regulatory Enforcement& Litigation Update

A Joint Presentation by

Dean C. Bunch | EY Partner | Fraud Investigation & Dispute Services

Steven J. Olson | O’Melveny & Myers Partner | Litigation

Page 1

Disclaimer

► Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited located in the US.

► The Ernst & Young organization is divided into five geographic areas and firms may be members of the following entities: Ernst & Young Americas LLC, Ernst & Young EMEIA Limited, Ernst & Young Far East Limited and Ernst & Young Oceania Limited. These entities do not provide services to clients.

► This presentation is ©2017 Ernst & Young LLP. All rights reserved. No part of this document may be reproduced, transmitted or otherwise distributed in any form or by any means, electronic or mechanical, including by photocopying, facsimile transmission, recording, rekeying or using any information storage and retrieval system, without written permission from Ernst & Young LLP. Any reproduction, transmission or distribution of this form or any of the material herein is prohibited and is in violation of US and international law. Ernst & Young LLP expressly disclaims any liability in connection with use of this presentation or its contents by any third party.

► Any US tax advice contained herein was not intended or written to be used, and cannot be used for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code or applicable state or local tax law provisions.

► These slides are for educational purposes only and are not intended, and should not be relied upon, as accounting advice.

► The views expressed by speakers at this event are not necessarily those of Ernst & Young LLP.

Page 2

Regulatory Enforcement and Litigation Update

Page 3

Polling question

What % of CFO’s could rationalize unethicalconduct to improve financial performance?

A. 2%B. 5%C. 11%D. 23%E. 36%

Page 4

Polling question answer

Based on EY’s 14th Global Fraud Survey of 2,825 executives in 62 countries, we found that 36% of CFOs surveyed felt they could rationalize unethical conduct to improve financial performance.

Other results of CFOs surveyed:► 18% would be prepared to change assumptions determining

valuations and reserves

► 3% would be prepared to misstate financial performance

► 13% would offer cash payments to win or retain business

► 9% would be prepared to backdate contracts

► 7% would book revenues earlier than they should

Other results of survey participants:► Further, 46% of other finance team members surveyed felt that

they could rationalize unethical conduct to improve financial performance.

► 42% of respondents could justify unethical behaviors to ensure they met financial targets.

Recent enforcement developments

Page 6

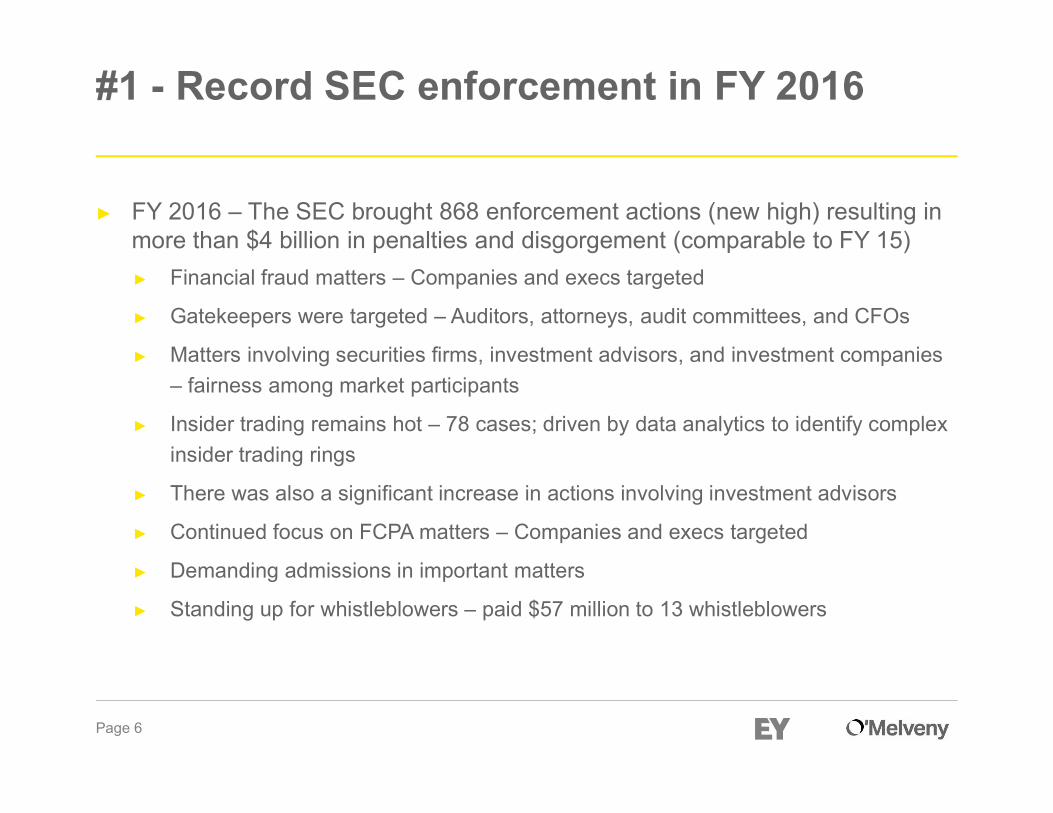

#1 - Record SEC enforcement in FY 2016

► FY 2016 – The SEC brought 868 enforcement actions (new high) resulting in more than $4 billion in penalties and disgorgement (comparable to FY 15)

► Financial fraud matters – Companies and execs targeted

► Gatekeepers were targeted – Auditors, attorneys, audit committees, and CFOs

► Matters involving securities firms, investment advisors, and investment companies

– fairness among market participants

► Insider trading remains hot – 78 cases; driven by data analytics to identify complex

insider trading rings

► There was also a significant increase in actions involving investment advisors

► Continued focus on FCPA matters – Companies and execs targeted

► Demanding admissions in important matters

► Standing up for whistleblowers – paid $57 million to 13 whistleblowers

Page 7

SEC enforcement in FY 2017 expected to decline

► The new administration has indicated a strong desire to deregulate

► Within days of taking office, President Trump signed the “Two-fer”

Executive Order, which requires an agency to repeal two existing

regulations for every new regulation it promulgates

► The new administration also brought significant changes to the composition of

the SEC’s leadership

► Mary Jo White was replaced by Jay Clayton, who has spent the majority

of his career doing M&A work at Sullivan & Cromwell

► Clayton is expected to implement the current administration’s stated goal

to deregulate

► Resultantly, enforcement actions are down as compared to FY 2016

Page 8

Notable SEC enforcement cases

► Insider trading and beneficial ownership reporting-related charges against the CEO of a major investment advisory firm.

► Insider trading charges against a professional gambler and his source of material inside information, who was the former chairman of a major food company.

► A $415 million enforcement action against the wealth management division of a major bank for violating customer protection rules by misusing customer cash and putting customer securities at risk. The firm also admitted wrongdoing.

► A $267 million enforcement action against a bank’s management subsidiaries, for failing to disclose conflicts of interest to clients. The firms also admitted wrongdoing.

► FCPA cases against a hedge fund and its CEO and CFO and against a major telecommunications company, in which the companies over $795 million to settle the charges.

Page 9

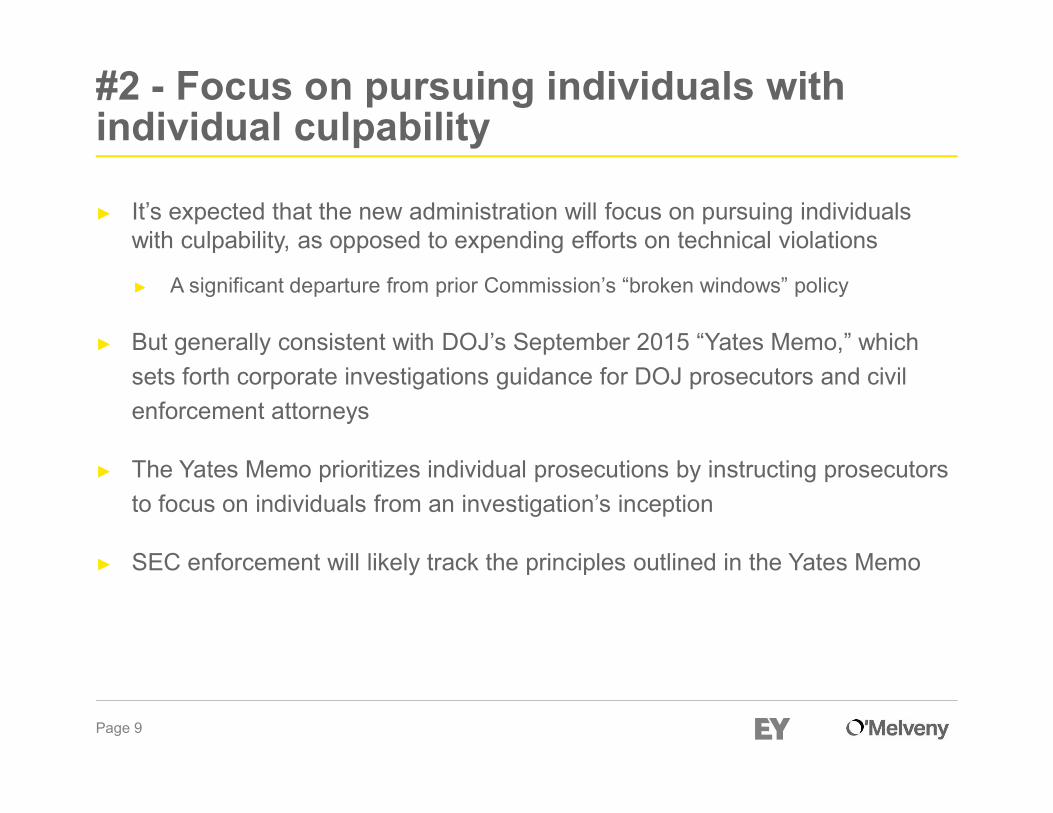

#2 - Focus on pursuing individuals with individual culpability

► It’s expected that the new administration will focus on pursuing individuals with culpability, as opposed to expending efforts on technical violations

► A significant departure from prior Commission’s “broken windows” policy

► But generally consistent with DOJ’s September 2015 “Yates Memo,” which

sets forth corporate investigations guidance for DOJ prosecutors and civil

enforcement attorneys

► The Yates Memo prioritizes individual prosecutions by instructing prosecutors

to focus on individuals from an investigation’s inception

► SEC enforcement will likely track the principles outlined in the Yates Memo

Page 10

Focus on pursuing individuals and individual culpability – changes ahead?

► In a recent speech, DOJ Deputy Attorney General Rod Rosenstein said the policies under the Yates Memo are “under review” and that he anticipates the DOJ will make an announcement in the “near future about what changes we’re going to make.”

► Rosenstein suggested he supported a continued focus on prosecuting individuals. “The issue is can you effectively deter corporate crime by prosecuting corporations or do you in some circumstances need to prosecute individuals? ….I think you do.”

► Attorney General Jeff Sessions added to the topic in a speech earlier this year. He said that in a compliance setting, a company cannot “be a guarantor that any of its thousands, perhaps, employees never do something wrong.”

► Mr. Sessions also asked, “Is it just to punish a corporation for wrongdoing that only one member of the corporation did?”

Page 11

#3 - Whistleblowing

► There has been a significant increase in Whistleblower protection / enforcement

► SEC has approximately 18 dedicated staff attorneys, paralegals and support staff

► Dodd Frank Act Requirements

► Qualified individual;

► Voluntarily provides original information; and

► that information leads to a successful enforcement action in which the

SEC is awarded monetary sanctions of over $1 million.

► A whistleblower that satisfies the above requirements may receive an award 10-30% of the monetary sanctions

► All payments are made out of an investor protection fund established by Congress that is financed entirely through monetary sanctions paid to the SEC by securities law violators.

Page 12

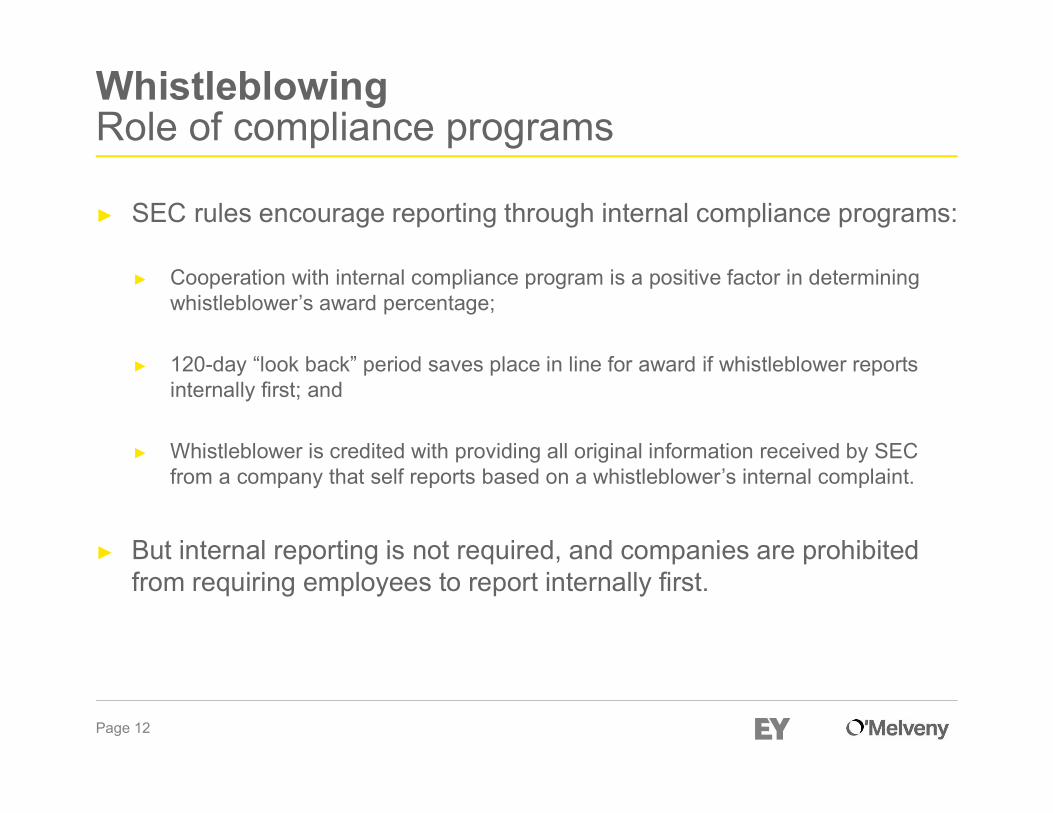

WhistleblowingRole of compliance programs

► SEC rules encourage reporting through internal compliance programs:

► Cooperation with internal compliance program is a positive factor in determining whistleblower’s award percentage;

► 120-day “look back” period saves place in line for award if whistleblower reports internally first; and

► Whistleblower is credited with providing all original information received by SEC from a company that self reports based on a whistleblower’s internal complaint.

► But internal reporting is not required, and companies are prohibited from requiring employees to report internally first.

Page 13

WhistleblowingAwards on the rise

► Law prohibits retaliating against whistleblowers, even when whistleblowers are contractors, not employees ► Late 2016 case against a casino gaming company

► Recent SEC actions implicate confidentiality agreements and severance agreements► No person may impede an individual from communication with the SEC about a possible

securities law violation.

► Annual number of tips increasing ► Over 15,000 tips from over 95 foreign countries

► Few, but significant, awards to date and on the rise► Over $158 million paid to approximately 37 whistleblowers since inception

► SEC paid $57 million to 13 whistleblowers in 2016, $20.2 million 2017 YTD (50% of awards in 2016 – 2017)

► Largest whistleblower award to date: $30 million to a single whistleblower

► Largely from current or former employees

Page 14

#4 - All things FCPA

► Prohibits the payment of bribes to foreign officials assist in obtaining or retaining business

► Applies to conduct anywhere in the world, by any employee or agent

► Issuers must maintain accurate books and records and have internal controls sufficient to provide reasonable assurances that transactions are executed in accordance with management’s authorization

► SEC and DOJ are jointly responsible for enforcement

► FCPA sanctions can be significant, and may include civil penalties:

► In early 2017, UK-based engineering company resolved an FCPA matter with multiple authorities agreeing to pay a combined $800 million, in connection with alleged bribes of state-owned oil companies.

Page 15

all things FCPA continued…

► Criminal Fines up to $2 million

per bribery violation and

$25 million per accounting

violation

► Civil penalties up to

$10 thousand per bribery

violation and $500 thousand per

accounting violation

► Disgorgement of profits,

corporate compliance monitor

► Up to 5 years imprisonment

plus criminal fines up to

$100 thousand per bribery

violation and up to 20 years

imprisonment plus a $5 million

fine per accounting violation

► Civil penalties up to

$10 thousand per bribery

violation and $100 thousand

per accounting violation

Companies Individuals

Page 16

Polling question answer

► Globally, bribery and corruption are still perceived to occur widely, and our respondents do not believe that the situation has improved since our last survey in 2014. ► 39% of those surveyed considered bribery and

corrupt practices to happen widely in their countries, consistent with 38% in our last survey. The situation appears to have deteriorated in developed markets where 21% of respondents reported that such behaviors were widespread, increasing from 17% in our last survey.

► Worryingly, 32% of respondents reported that they have had concerns when asked about bribery and corruption in their workplace.

► This contrasts with the trend seen in emerging markets, where our results indicate a small improvement, with the perceived prevalence of bribery and corruption down from 53% to 51%.

Page 17

all things FCPA continued…

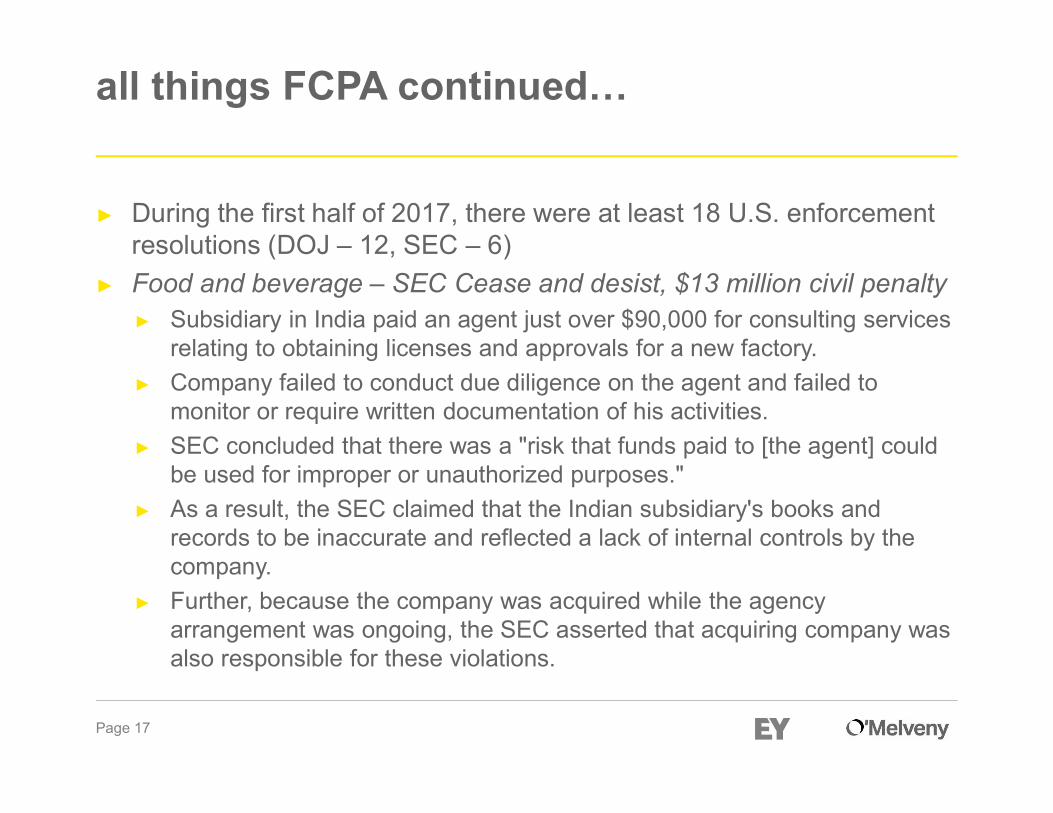

► During the first half of 2017, there were at least 18 U.S. enforcement resolutions (DOJ – 12, SEC – 6)

► Food and beverage – SEC Cease and desist, $13 million civil penalty► Subsidiary in India paid an agent just over $90,000 for consulting services

relating to obtaining licenses and approvals for a new factory.

► Company failed to conduct due diligence on the agent and failed to monitor or require written documentation of his activities.

► SEC concluded that there was a "risk that funds paid to [the agent] could be used for improper or unauthorized purposes."

► As a result, the SEC claimed that the Indian subsidiary's books and records to be inaccurate and reflected a lack of internal controls by the company.

► Further, because the company was acquired while the agency arrangement was ongoing, the SEC asserted that acquiring company was also responsible for these violations.

Page 18

all things FCPA continued…

► Oilfield Services Company – SEC cease and desist, $29.2 million civil penalty► Charged with violating the books and records and internal accounting

controls provisions of the FCPA.

► Connected to selecting and making payments to a local company in Angola in the course of winning lucrative oilfield services contracts.

► Angola’s state oil company told the company that it was required to partner with more local Angolan-owned businesses to satisfy local content regulations.

► A business owned by a former company employee who was also neighbors of the official who would ultimately approve the award of the contracts was selected.

► In total $13 million in contracts were awarded to the local business and then subsequently the scope of services to be provided by the business were determined.

Page 19

Impact of FCPA Pilot Program and 2017 Announced Declinations (1/2)

FCPA Pilot Program► One-year trial to encourage self-reporting, accountability

and cooperation with FCPA investigations and expire in April 2017

► Increase from 13 to 22 companies that made voluntary disclosures in the first year of the Pilot Program

Announced declinations 2017

► At least 8 companies disclosed declination letters received from the SEC and/or DOJ

► First declination in 2017 under the Pilot Program

► Demonstrate DOJ and SEC willingness to exercise greater prosecutorial discretion

Developments

► March 10, 2017: Acting Assistant Attorney General Ken Blanco announced that the DOJ plans to continue the program “in full force until we reach a final decision about its efficacy.” This relates to the utility of the Program, whether to extend it, and what revisions, if any, should be made to it

► Continuous promotion of cooperation, reporting and remediation

Page 20

Impact of FCPA Pilot Program and 2017 Announced Declinations (2/2)► To qualify for a credit, the company must:

► Voluntary self-disclosure in FCPA matters

► Full cooperation in FCPA matters

► Timely and appropriate remediation in FCPA matters

► Corporations that self-disclose can:► Receive a declination of prosecution (if also pay disgorgement of ill-gotten gains)

► Earn a fine reduction of up to 25% off the bottom of the sentencing guideline range (no voluntary self-disclosure)

► Earn a fine reduction of up to 50% off the bottom end of the sentencing guideline range (voluntary self-disclosure)

► Should not require the imposition of an independent monitor if the company has implemented an effective compliance program at the time of resolution

► Caveats:► Disclosures that are required by law or agreement do not constitute voluntary self-disclosure under the Program

► Disclosure must take place “prior to an imminent threat of disclosure or government investigation”

► And must take place “within a reasonably prompt time” after the company became aware of the offense

► Remediation includes firing or disciplining responsible employees and setting up a quality compliance program

► “Cooperation” includes fully investigating the company’s employees and turning the evidence over to the government; making employees available for interview; “de-conflicting” internal investigations to allow the government to decide who talks to whom first; preserving and producing all relevant evidence; and regularly updating the government on the company’s internal investigation

► The program only applies to companies that self-disclose during the time the pilot program is in effect

Page 21

all things FCPA continued…

U.S. Supreme Court Limits the Scope of SEC Disgorgement

► Resolutions with the SEC often involve disgorgement of ill gotten gains (i.e., profits).

► Questions about the potential limitations on disgorgement relative to the five-year statute of limitations have persisted. SEC has taken the position that disgorgement is an “equitable remedy” (versus a penalty), and therefore, not subject to the 5 year limitation.

► On June 5, 2017 the U.S. Supreme court unanimously held that disgorgement in an SEC enforcement proceeding is a “penalty,”and therefore is subject to the five-year statute of limitations.

► The significance of this finding is that it now limits the SEC’s ability to seek disgorgement in connection with conduct that occurred more than 5 years earlier. The SEC has historically believed that disgorgement was a claim for equitable relief and was not subject to any limitation.

► We now may see the SEC trying to bring cases and resolve cases more quickly in response to this ruling.

Page 22

all things FCPA continued…

DOJ’s Scrutiny over Compliance Programs

► DOJ hired its first Compliance Counsel in November 2015 to assist prosecutors and DOJ officials in evaluating compliance programs.

► Produced detailed topical questions that provide great insights into how the DOJ evaluates corporate compliance programs, including the following topics:► Analysis and Remediation of Underlying Misconduct

► Senior and Middle Management

► Autonomy and Resources

► Policies and Procedures

► Risk Assessments

► Training and Communications

► Confidential Reporting and Investigation

► Incentives and Disciplinary Measures

► Continuous Improvement, Periodic Testing and Review

► Third Party Management

► M&A

Page 23

FCPA enforcement – words from the regulators under the new administration

Statements under the Trump Administration

Nov. 2016 Dec. Jan. 2017 Feb. Mar. Apr. May June

April 24, 2017“[DOJ] will continue to strongly enforce the FCPA. Companies should succeed because they provide superior products and services, not because they pay off the right people.” – Jeff Sessions, Attorney General at Ethics and Compliance Initiative Annual Conference

April 18, 2017“[DOJ] remains committed to enforcing the FCPA and to prosecuting fraud and corruption more generally.” – 10th Anti-Corruption, Export Controls & Sanctions Compliance Summit in Washington, D.C. May 24, 2017“[DOJ] takes a robust attitude towards the jurisdictional reach of the FCPA primarily to help ensure there is an even playing field for honest businesses everywhere.” – American Conference Institute’s 7th Brazil Summit on Anti-Corruption

February 16, 2017 “The Criminal Division will continue to prioritize

prosecutions of individuals who have willfully andcorruptly violated the FCPA.”

“Attorney General Sessions explicitly noted his commitment to enforcing the FCPA, and to prosecuting fraud and corruption more generally. The fight against official corruption is a solemn duty of the Justice Department, each generation of

Department leaders and line prosecutors takes up his mantle from their predecessors, regardless of party affiliation.”

– Global Investigations Review Remarks

November 7, 2016Donald Trumpelected president

January 17, 2017“Yes, if confirmed as attorney general, I will enforce all federal laws, including the Foreign Corrupt Practices Act and the International Anti-Bribery Act of 1988, as appropriately based on the facts and circumstances of each case.” – Jeff Sessions, Written Responses to AG Confirmation Questions from Senator Whitehouse

March 23, 2017When asked his specific plan for enforcement of the FCPA, Clayton responded: “Bribery and corruption have no place in society. . . . I believe the FCPA can be a powerful and effective means to [combat government corruption]. . . . If confirmed, Ilook forward to working with my fellow Commissioners, Enforcement Division staff, and other authorities in the U.S. and abroad to coordinate enforcement of the FCPA and other anti-corruption laws.” – Jay Clayton, Chair of the SEC, written testimony to the Committee on Banking, Housing and Urban Affairs

Trevor McFadden, U.S. Deputy

Assistant Attorney General

• DOJ invests significantly more resources on prosecuting FCPA violations

Increased use of monitorships

DOJ employing “Blue-Collar” investigative techniques

Importance of individual prosecution – changes ahead?

Page 24

#5 - Cybersecurity enforcement

► SEC enforcement reportedly views cybersecurity as one of its top focus areas. In several speeches, Co-Director of Enforcement, Stephanie Avakian, has noted that the enforcement staff is focusing on cyber failures.

► The SEC Chairman, Jay Clayton, has also weighed in on the issue:

"I am not comfortable that the American investing public understands the substantial risks

that we face systemically from cyber issues….I’d like to see better disclosure around that.”

► In these cases, the SEC is pursuing matters based on three types of issues:1. When registrants fail to take appropriate steps to safeguard information.

2. When material nonpublic information is stolen to gain market advantage.

3. When cyber disclosure is false or misleading.

► The SEC is pursuing companies based on perceived shortcomings of their internal control over financial reporting to the extent that unauthorized persons are able to access, steal, or destroy material assets on their information technology systems.

Page 25

Cybersecurity enforcement – SEC Chairman commentary

► In a July 2017 speech given by SEC Chairman, Jay Clayton, (his first as SEC Chairman) he acknowledge the responsibilities of public companies around cybersecurity and their requirements to disclose material information about cyber risks and cyber events.

► However, he also noted that although being a victim of a cyber penetration is not, in itself, an excuse, the SEC needs to be cautious about punishing responsible companies who are victims of sophisticated cyber penetrations.

► Jay Clayton noted that the SEC needs to have a broad perspective and bring proportionality to this area that affects not only investors, companies, and our markets, but our national security and our future.

► And just days ago, Clayton disclosed that the SEC itself had been the victim of cyber attack when its Edgar system was hacked in 2016. In disclosing the breach, Clayton reiterated that “Cybersecurity is critical to the operations of our markets, and the risks are significant and, in many cases, systemic.”

Page 26

Example case – financial services company

► The SEC announced that large financial services company agreed to pay a $1 million penalty to settle charges related to its failures to protect customer information, some of which was hacked and offered for sale online.

► The SEC’s order found that the company failed to adopt written policies and procedures reasonably designed to protect customer data. As a result of these failures, over a three-year period, a former employee impermissibly accessed and transferred the data regarding approximately 730,000 accounts to his personal server, which was ultimately hacked by third parties.

► According to the SEC’s order, “the federal securities laws require registered broker-dealers and investment advisers to adopt written policies and procedures reasonably designed to protect customer records and information.”

Page 27

#6 - Financial Reporting and Audit Group (FRAud Group)

► The formation of this SEC enforcement task force was announced 4 years ago and its operations have taken shape.

► The SEC Enforcement Division’s Financial Reporting and Audit (FRAud) Group is strengthening the agency’s efforts to identify and prosecute securities law violations related to financial reporting and audit failures.

► In addition to identifying securities law violations in the preparation of financial statements and the disclosure of financial information to investors, the FRAudGroup is identifying and exploring areas susceptible to fraudulent financial reporting. These efforts include an ongoing review of financial statement restatements and revisions, an analysis of performance trends by industry, and the use of technology-based tools.

Page 28

Example 2017 cases – alleging revenue recognition issues

► Medical device company and former executives resolve accounting fraud charges. Recording revenue on shipments with outstanding contingencies and recording revenue with extended payment terms.

► Government contractor settled charges that it failed to maintain accurate books and records and had inadequate internal accounting controls. SEC investigation found that the company improperly recorded revenue on long-term contracts by creating invoices associated with unresolved claims against the customer that were not delivered when the revenue was recorded.

► SEC charged former CFO and director of accounting of a computer network testing company in regards to a scheme to prematurely recognize revenues and concealed the improper revenue recognition practice from the company’s auditors. The SEC simultaneously announced a settlement with the company and the former CEO in regards to the same alleged conduct.

Page 29

Example 2017 cases – alleging revenue recognition issues

► SEC charged the former CFO of a Colorado-based environmental solutions company with accounting and books and records violations. Numerous errors in the financial statements resulted in a 2016 restatement by the company.

► Mexico-based homebuilding company settled charges that it recorded fake sales of more than 100,000 homes resulting in $3.3 billion in overstated revenue over a three-year period. Satellite images were used to show that an entire development of homes that had been reported to have been completed had not even broken ground.

► South Korean-based Semiconductor manufacture and its former CFO agreed to settle charges related to an accounting scheme to artificially inflate revenue and manipulate the financial results reported to investors.

Page 30

Example 2017 cases – alleging earnings management

► Fraud and other charges were brought against the former EVP and SVP of a publicly traded manufacturer of wire and cable products. The CEO and CFO of a subsidiary in Brazil were alleged to have fraudulently concealing inventory accounting errors. The SEC claims that in January 2012 the two individuals became aware of an overstatement of inventory by tens of millions of dollars and allegations of an inventory theft scheme by certain employees.

► SEC charged a shipping conglomerate and its former CFO with failing to recognize hundreds of millions in tax liabilities in its financial statements that had accumulated over 12 years from a controlled foreign subsidiary. Following the discovery, the company filed for bankruptcy.

► SEC charged a Canadian-based oil and gas company and three of its former top finance executives for their roles in what is alleged to be an extensive, multi-year accounting fraud. The SEC alleges that the company moved hundreds of millions of dollars in expenses from operating expense accounts to capital expenditure accounts.

Page 31

#7 - Enforcement matters involving alleged non-GAAP financial measures

► In early 2016, the SEC issued updated guidance on non-GAAP financial

measures

► Most viewed this as the SEC placing greater emphasis on non-GAAP

disclosure requirements

► This was followed by an uptick in non-GAAP related enforcement and

litigation

► For example, the SEC permanently suspended a firm’s chief accounting officer for violating non-GAAP regs. The SEC complaint alleged, among other things, that the CAO and a former CFO manipulated and falsely reported their firm’s "Adjusted Funds from Operations," which is a key non-GAAP financial metric. The complaint alleged that the inflated figures made it appear that the firm had met analysts' consensus AFFO estimates for the quarter and concealed the fact that the firm had overstated that number for the previous quarter.

Page 32

Enforcement matters involving alleged non-GAAP financial measures

► Several speeches by SEC officials have noted this area of interest. Takeaways from these speeches:► Concerns over issuers who take non-GAAP financial measures “too far and beyond

what is intended and allowed.”

► Non-GAAP disclosures that do not comply with SEC rules could result in enforcement actions.

► Warnings that the SEC may adopt “further rulemaking if necessary to achieve the optimal disclosures for investors and the markets.”

► The SEC’s updated guidance on non-GAAP financial measures can be found here:

https://www.sec.gov/divisions/corpfin/guidance/nongaapinterp.htm

Page 33

#8 - Insider Trading

► High priority enforcement area in last several years

► 240+ individuals and entities in a 3-year span

► Financial professionals, hedge fund managers, corporate insiders, and

attorneys

► Aggressive new tactics

► Use of sophisticated data analysis

► Close cooperation with DOJ

Page 34

Recent Notable Insider Trading Cases

► Case 1: SEC v. Issuer

► Issuer was held responsible for employees’ trades because it knew or

recklessly disregarded that a controlled person was likely to engage in

prohibited trading

► The SEC also alleged it failed to take appropriate steps to prevent the

trades before they occurred

► Demonstrates that companies need to employ industry accepted best

practices to prevent fraudulent trades and rebut a claim of recklessness

► Well-publicized Insider Trading Policy with training

► Code names on deals

► Network security

► Limited group of insiders

Page 35

Recent Notable Insider Trading Cases

► SEC v. Corporate Controller

► Part of M&A due diligence team

► Bought company stock during blackout period in accounts held by

relatives

► 5 year bar

► $34,000 penalty and $34,000 disgorgement

► SEC v. Retail Vice President

► Regional VP received regular sales reports

► Purchased company stock repeatedly just prior to earnings releases

► $26,000 penalty and $26,000 disgorgement

Page 36

Q&A

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2017 Ernst & Young LLP.All Rights Reserved.

BSC no. 1508-1636584ED none.

ey.com