school district of township of lower township school district introductory section letter of...

TRANSCRIPT

SCHOOL DISTRICTOF

TOWNSHIPOF

LOWER

Township of Lower Board of EducationLower Township, New Jersey

Comprehensive Annual Financial ReportFor the Fiscal Year Ended June 30,2012

Comprehensive AnnualFinancial Report

of the

Township of Lower Board of EducationLower Township, New Jersey

For the Fiscal Year Ended June 30, 2012

Prepared by

Township of Lower Board of EducationFinance Department

LOWER TOWNSHIP SCHOOL DISTRICT

INTRODUCTORY SECTION

Letter of TransmittalOrganizational ChartRoster of OfficialsConsultants and Advisors

FINANCIAL SECTION

Independent Auditor's Report

K-l Report on Compliance and on Internal Control Over Financial Reporting Basedon an Audit of Financial Statements Performed in Accordance withGovernment Auditing Standards

Required Supplementary Information - Part IManagement's Discussion and Analysis

Basic Financial Statements

A. District-wide Financial Statements:

A-IA-2

Statement of Net AssetsStatement of Activities

B. Fund Financial Statements:

Governmental Funds:B-1 Balance SheetB-2 Statement of Revenues, Expenditures, and Changes in Fund BalancesB-3 Reconciliation of the Statement of Revenues, Expenditures, and Changes in

Fund Balances of Governmental Funds to the Statement of Activities

Proprietary Funds:B-4 Statement of Net AssetsB-5B-6

Statement of Revenues, Expenses, and Changes in Fund Net AssetsStatement of Cash Flows

Fiduciary Funds:B-7 Statement of Fiduciary Net AssetsB-S Statement of Changes in Fiduciary Net Assets

Notes to the Financial Statements

Page2S910

12

14

17

2728

3031

32

333435

3637

38

Required Supplementary Information - Part II

C. Budgetary Comparison Schedules

C-I Budgetary Comparison Schedule - General FundC-la Combining Schedule of Revenues, Expenditures and Changes

in Fund Balance - Budget and Actual (if applicable)C-l b Budgetary Comparison Schedule - Education Jobs FundC-2 Budgetary Comparison Schedule - Special Revenue Fund

58

N/A6465

Notes to the Required Supplementary InformationC-3 Budget-to-GAAP Reconciliation 66

Other Supplementary Information

D. School Level Schedules: N/A

E. Special Revenue Fund:

E-l Combining Schedule of Revenues and ExpendituresSpecial Revenue Fund - Budgetary Basis

Preschool Education Program Aid Schedule of Expenditures -Budgetary Basis

69E-2

71

F. Capital Projects FundF-l Summary Schedule of Revenues, Expenditures, and Changes in Fund

Balance - Budgetary BasisF-2 Summary Schedule of Project Expenditures

7374

G. Proprietary Fund:

Enterprise Fund:G-l Combining Statement of Net Assets 76G-2 Combining Statement of Revenues, Expenses and Changes in

Fund Net AssetsCombining Statement of Cash Flows

7778G-3

Internal Service Fund: N/A

H. Fiduciary Funds:H-I Combining Statement of Fiduciary Net AssetsH-2 Combining Statement of Changes in Fiduciary Net AssetsH-3 Student Activity Agency Fund Schedule of Receipts and DisbursementsH-4 Payroll Agency Fund Schedule of Receipts and Disbursements

80818283

I. Long-Term Debt:

I-I1-21-3

Schedule of Serial BondsSchedule of Obligations Under Capital LeasesBudgetary Comparison Schedule

N/AN/AN/A

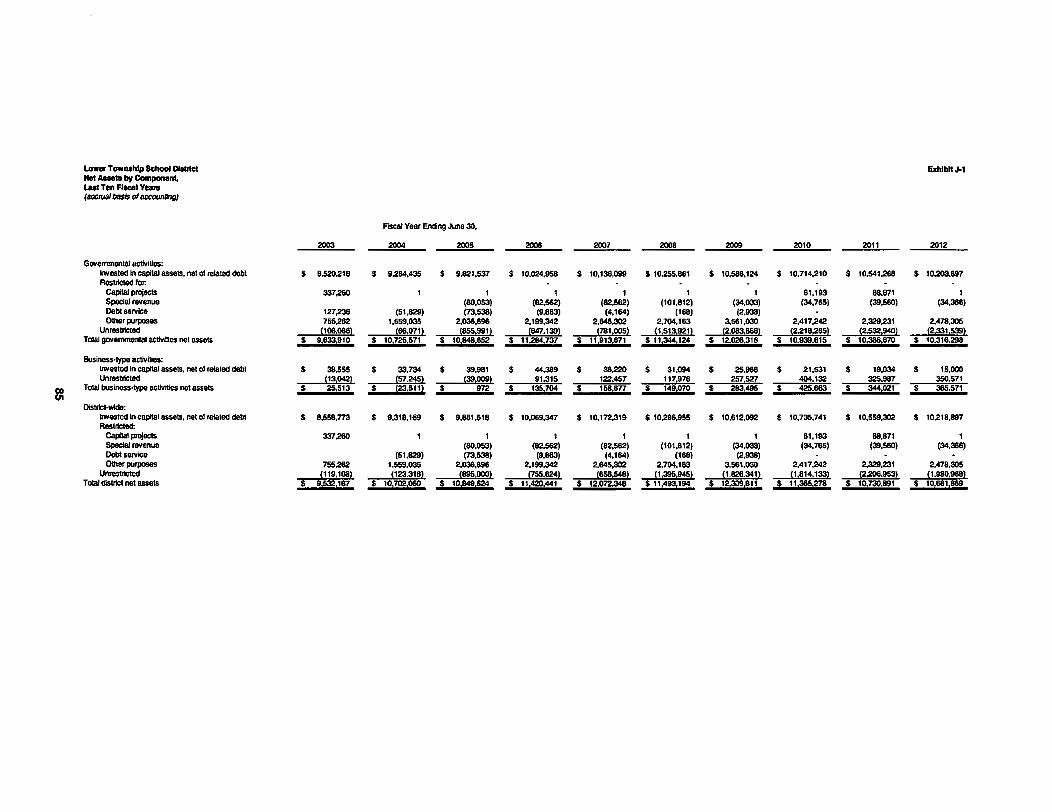

STATISTICAL SECTION (Unaudited)Financial TrendsJ-l Net Assets by Component, Last Ten Fiscal YearsJ-2 Changes in Net Assets, Last Ten Fiscal YearsJ-3 Fund Balances, Governmental Funds, Last Ten Fiscal Years

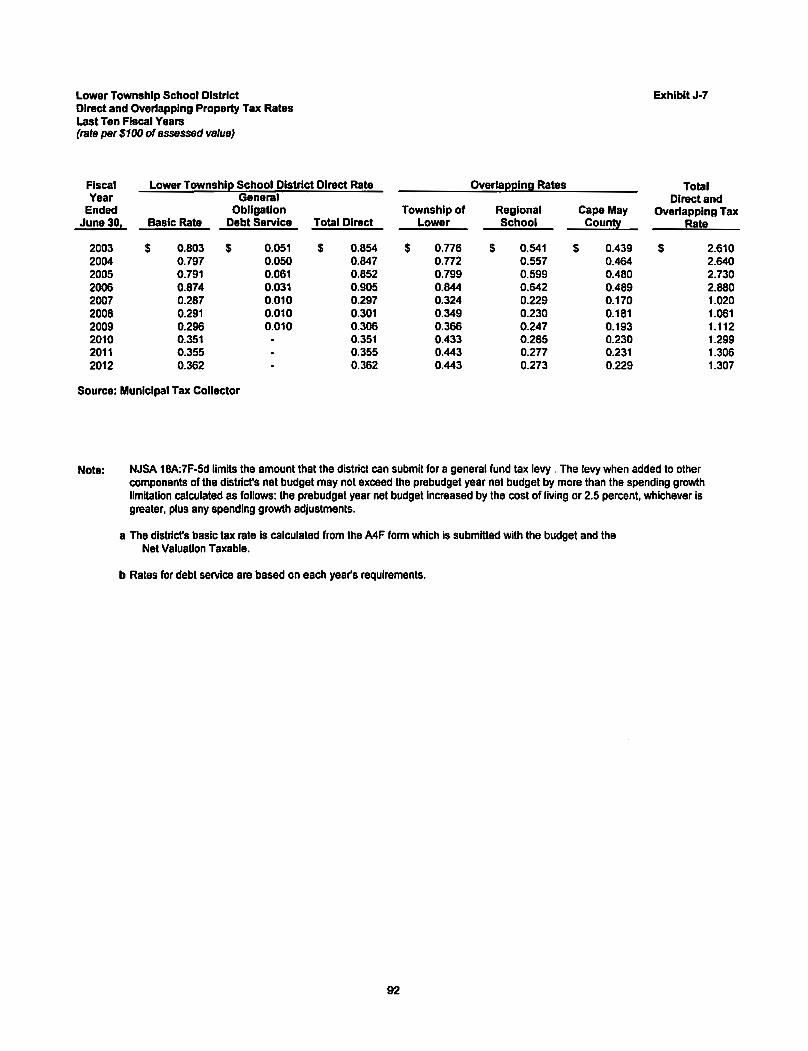

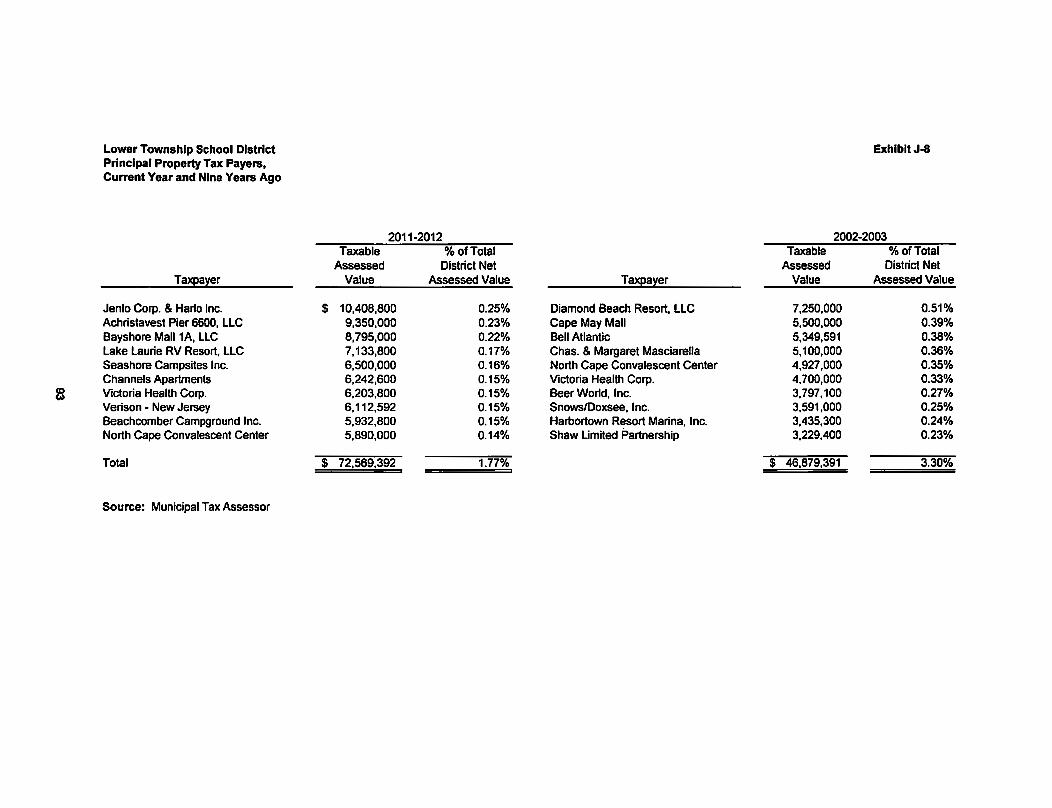

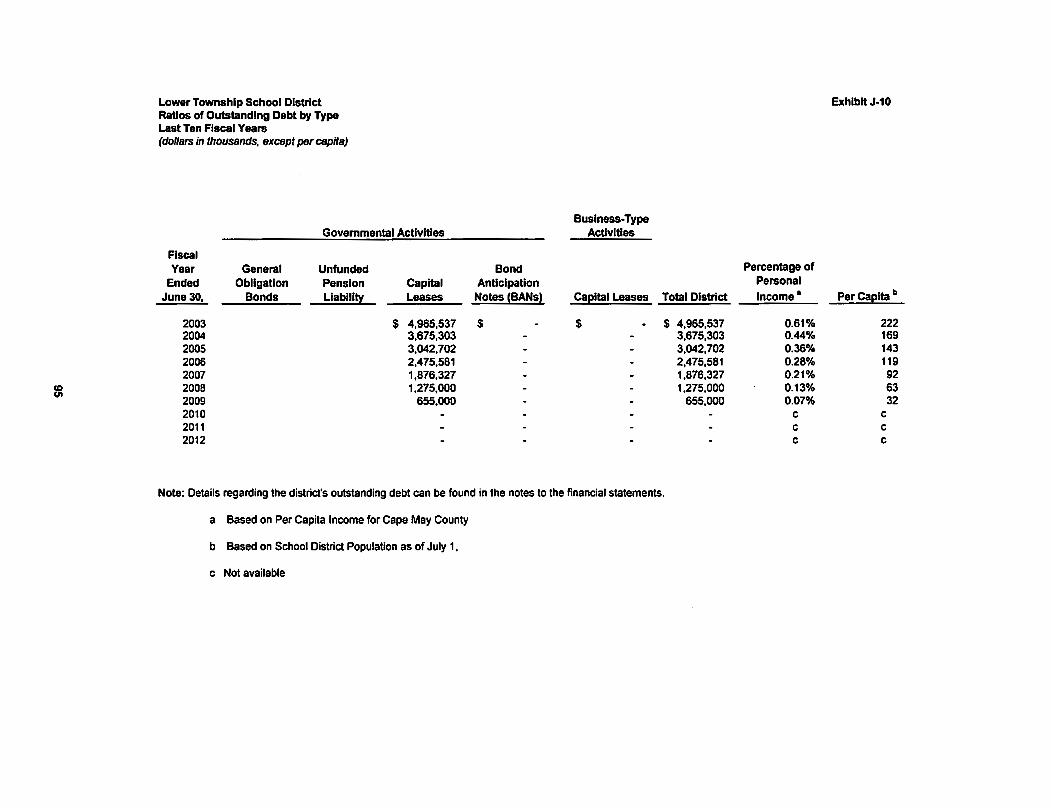

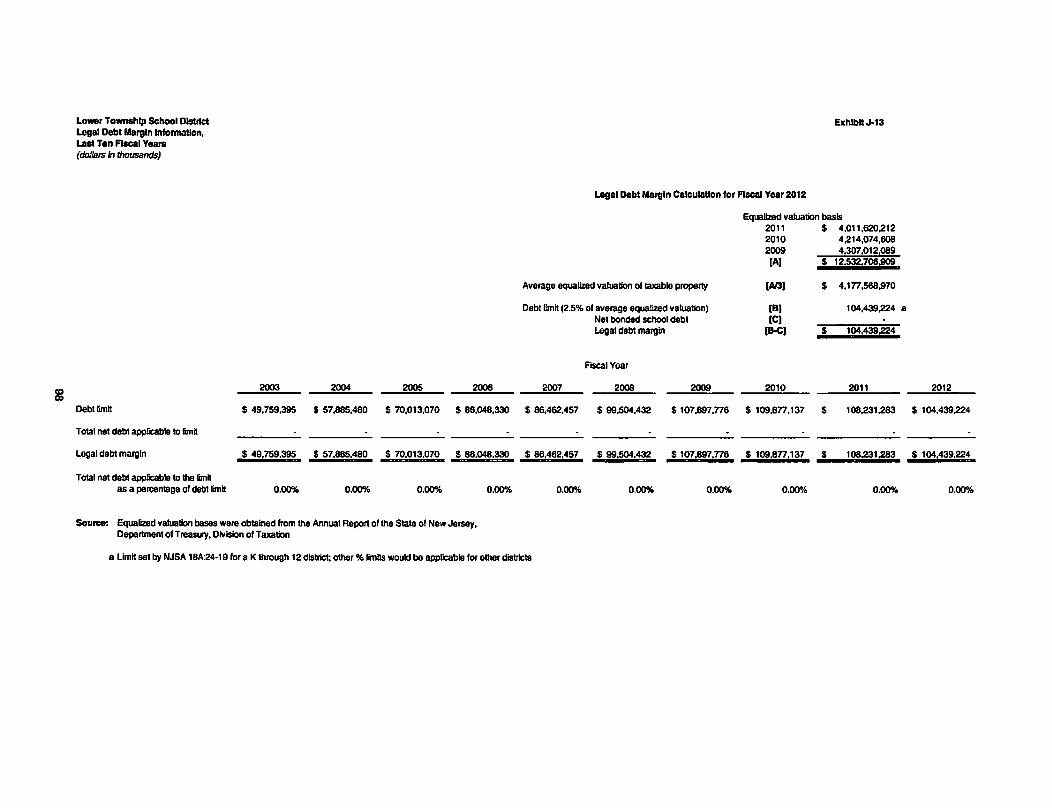

Revenue CapacityJ-6 Assessed Value and Actual Value of Taxable Property, Last Ten Fiscal YearsJ-7 Direct and Overlapping Property Tax Rates, Last Ten Fiscal YearsJ-8 Principal Property Tax Payers, Current Year and Nine Years AgoJ-9 Property Tax Levies and Collections, Last Ten Fiscal YearsDebt CapacityJ-10 Ratios of Outstanding Debt by Type, Last Ten Fiscal YearsJ-11 Ratios of Net General Bonded Debt Outstanding, Last Ten Fiscal YearsJ-12 Ratios of Overlapping Governmental Activities Debt, As of December 31, 2011J-13 Legal Debt Margin Information, Last Ten Fiscal YearsDemographic and Economic InformationJ-14 Demographic and Economic Statistics

J-4J-5

J-15

Changes in Fund Balances, Governmental Funds, Last Ten Fiscal YearsGeneral Fund - Other Local Revenue by Source, Last Ten Fiscal Years

8586888990

91929394

95969798

Principal Employers, Current Year & Nine Years Ago (information not available)99

N/AOperating InformationJ-16 Full-time Equivalent District Employees by Function/Program, Last Ten Fiscal Years 100

K-2 Report on Compliance with Requirements Applicable to Each MajorProgram and on Internal Control Over Compliance in Accordance withOMB Circular A-133 and New Jersey OMB Circular Letter 04-04

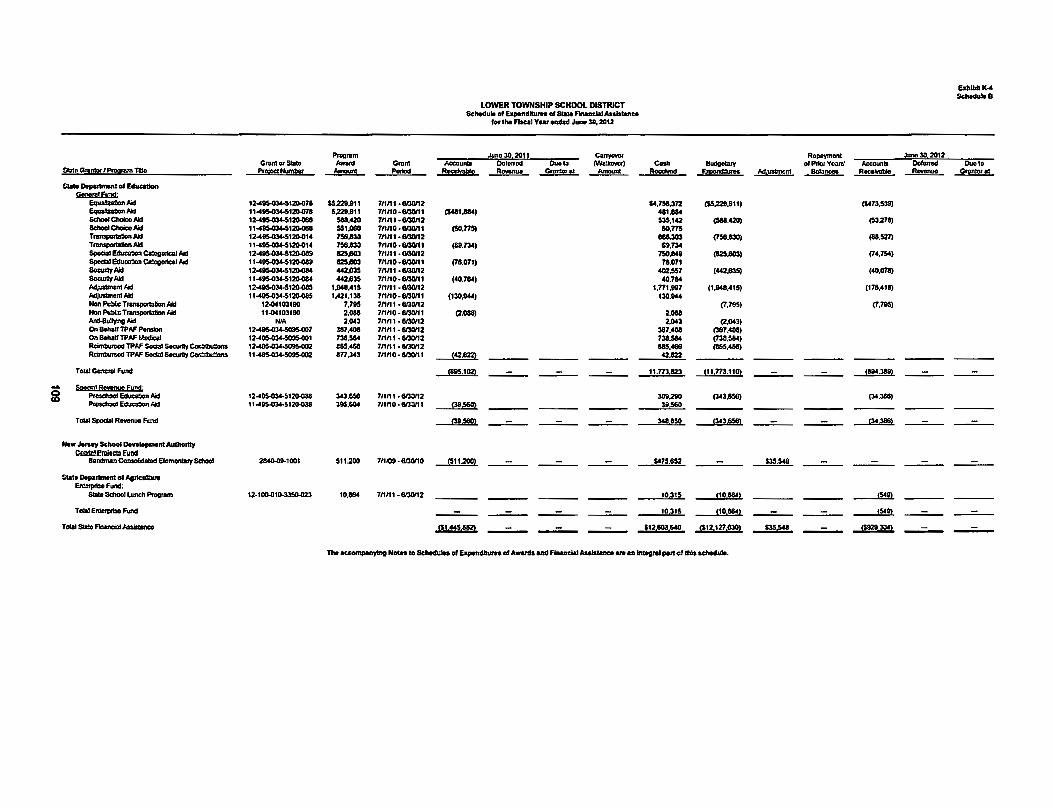

Schedule of Expenditures of Federal Awards, Schedule ASchedule of Expenditures of State Financial Assistance, Schedule BNotes to the Schedules of Awards and Financial AssistanceSchedule of Findings and Questioned CostsSummary Schedule of Prior Audit Findings

J-17J-18J-19J-20

K-3K-4K-5K-6K-7

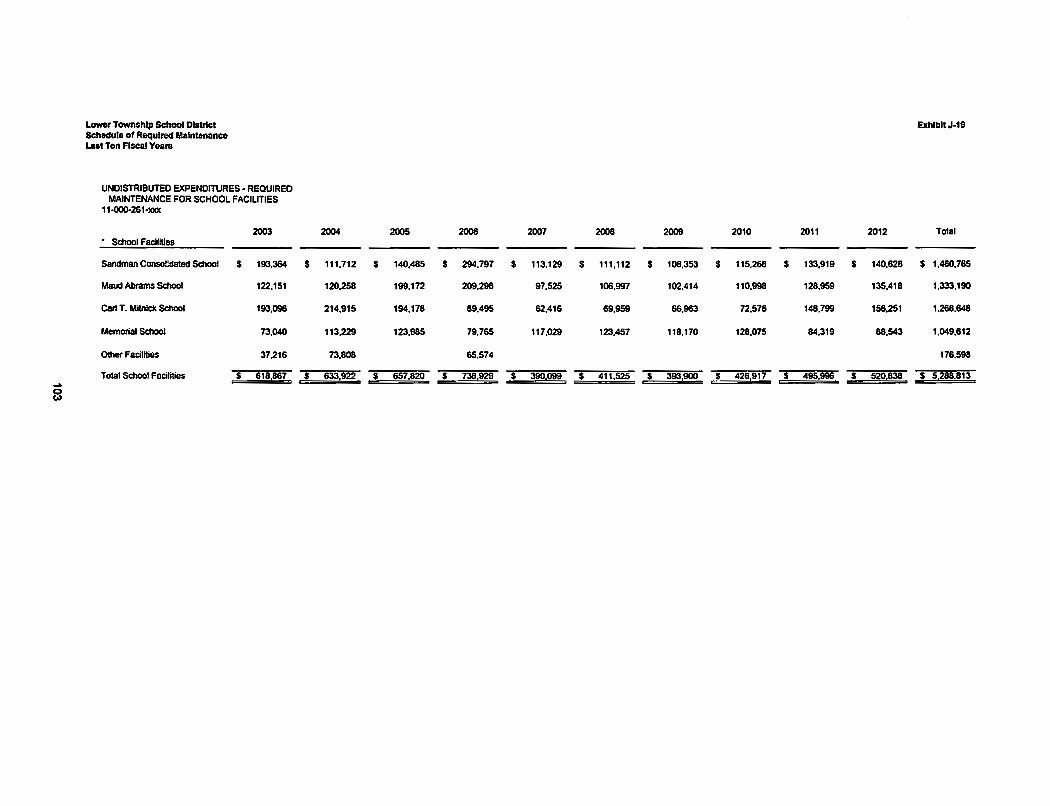

Operating Statistics, Last Ten Fiscal YearsSchool Building Information, Last Ten Fiscal YearsSchedule of Required Maintenance, Last Ten Fiscal YearsInsurance Schedule

101102103104

SINGLE AUDIT SECTION

106108109110112116

Introductory Section

Maud Abrams School714 Town Bank RoadCape May. NJ 08204Telephone: (609) 884-9-120Fax: (609) 884-9421

LOWER TOWNSHIP ELEMENTARY SCHOOL DISTRICT834 SEASHORE ROAD

CAPE MAY, NEW JERSEY 08204

TELEPHONE: (609) 884-9400FAX: (609) 884-1821www.lowcrtwpschools.com

Memorial School2600 Bayshore RoadVillas. NJ OR251Telephone: (609) 884-9430Fax: (609) 886-0515

Sandman Consolidated School838 Seashore RoadCape May. NJ 08204Telephone: (609) 884-9410Fax: (609) 884-9-112

Carl T_ Mitnick School905 Seashore RoadCape May, NJ 08204Telephone: (609) 884-9470Fax: (609) 898-9481

October 16, 2012

Iionorable President andMembers of the Board of EducationLower Township School DistrictCounty of Cape MayCape May, New Jersey

Dear Board Members:

The comprehensive annual financial report of the Township of Lower School District forthe fiscal year ended June 30, 2012 is hereby submitted. Responsibility for the accuracy of thedata and completeness and fairness of the presentation, including all disclosures, rests with themanagement of the Board of Education. To the best of our knowledge and belief, the datapresented in this report is accurate in all material respects and is presented in a manner designedto present fairly the financial position and results of operations of the various funds and accountgroups of the District. All disclosures necessary to enable the reader to gain an understanding ofthe District's financial activities have been included.

The comprehensive annual financial report is presented in four sections: introductory.financial, statistical and single audit. The organizational chart and a list of principal officials.The financial schedules, as well as the auditor's report thereon. The statistical section includesselected financial and demographic information, generally presented on a multi-year basis. TheDistrict is required to undergo an annual single audit in conformity with the provisions of theSingle Audit Act of 1984 and the U.S. Office of Management and Budget Circular A-I33,"Audits oj State. Local Governments and Non-Profit Organizations ", and the State TreasuryCircular letter 04-04 OMB, "Single Audit Policy jar Recipients oj Federal Grants. State Grantsand State Aid". Information related to this single audit, including the auditor's report oncompliance and internal control with applicable laws and regulations and findings andrecommendations are included in the single audit section of this report.

2

1. REPORTING ENTITY AND ITS SERVICES:

The Township of Lower School District is an independent reporting entity within the criteriaadopted by the GASB as established by GASB Statement No. 14. All funds and accountgroups of the District are included in this report. The Township of Lower Board of Educationand all its schools constitute the District's reporting entity.

The District provides a full range of educational services appropriate to grade levelsPreschool through 6. These include regular education, academic enrichment programs andSpecial Education instruction and Child Study Team services. The District completed the2011-2012 fiscal year with an enrollment of 1,828 students (June 2012). The followingdetails the changes in the student enrollment of the District over the last ten years.

AVERAGE STUDENT ENROLLMENTAS REPORTED TO THE STATE

Fiscal Year2011-122010-112009-102008-092007-082006-072005-062004-052003-042002-03

Average Daily Enrollment1,8281,8481,8851,8571,8271,8921,9191,9001,9081,977

Percent Change-1.08%-1.96%1.51%1.65%

-3.44%-1.40%1.00%

-0.42%-3.49%-3.94%

2. ECONOMIC CONDITION AND OUTLOOK:

The Township of Lower encompasses 30.5 square miles in the southern part of Cape MayCounty. Its boundaries include the Delaware Bay, the Atlantic Ocean, Cape May City, CapeMay Point, Wildwood Crest, and the Township of Middle. The area was purchase from theoriginal settlers, the Kechemeche Indians, in the early 1600's. It was a natural site andbecame a center for whaling, fishing and fur trading.

The township was formed as a precinct in 1723 and was incorporated on February 21, 1798.From its incorporation until July I, 1984, three members formed a township committee thatgoverned the Township. Since July 1984, the governing body consists of a mayor, elected bythe people, and four council members (three elected from wards and one at-large.) Inaddition, a township manager, since 1984 supervises all departments and is responsible forthe preparation and administration of the annual budget.

3

3. MAJOR INITIATIVES:

During the 2011-2012 school year, numerous programs were strengthened to further promotestudent achievement in the New Jersey Department of Education's newly adopted CommonCore State Standards for English Language Arts. Common Core State Standards are the firststep in providing our young people a high-quality 2151 Century Education and have beenadopted by 46 states. Although the English Language Standards are divided into Reading,Writing, Speaking and Listening, the Language strands for conceptual clarity and theprocesses of communication are closely connected. Through continued emphasis on the 6+ ITraits of Writing in curriculum structure, the individual grade proficiencies & assessments inreading, writing and speaking will ensure that our next generation will be college and/orcareer ready in literacy by high school graduation. BookFlix© subscriptions continue to beweb-posted for preschool thru grade 4 students and families benefit from this readingintervention program for English and Bilingual students. BookFlix© is a program of popularchildren's reading titles, web-posted in Spanish and English, possessing visual text, optionalauditory support and possessing individual student progress monitoring capabilities. Otherdistrict provided online student resources for elementary grade levels include: World BookKids (K-3), World Book Students (4-6), World Book Discover (Focus: science),Encyclopedia Estudiantil Hallazgos (Spanish encyclopedia) and the Early World of Learning(Focus: visual learning modality).

Continuing with the Common Core Standards Initiative, considerable emphasis was placedon aligning the third grade through sixth grade mathematics curriculum to incorporate thenew content standards into our existing ENVISION© MATH program. Kindergarten throughsecond grade implemented the Common Core Curriculum during the 20 I0-11 SY. Wholegroup math lessons continue to incorporate Mimio technology, enhancing studentcomprehension of math concepts via the visually-rich manipulatives. Continuous teacher-training with the comprehensive digital capabilities and visual animations reinforce studentcomprehension of the mathematics standards.

Preschool and kindergarten instructional staff having completed training in High/Scope'sCOR (Child Observation Record) method of assessment This meaningful assessment forpreschool students has replaced the previously-used DIBELS assessment (DynamicIndicators of Basic Early Learning Skills).

Kindergarten literacy achievement is assessed via Fountas & Pinnell Benchmark AssessmentSystems and the Journeys© Unit & Benchmark Assessments. In addition, the KindergartenLiteracy Survey is administered three (3) times per year.

HANDWRITINGWITHOUT TEARS© (HWT) curriculum was adopted by preschool andkindergarten during 2008-09 SY and expanded to district-wide implementation in 20 I0-11.

According to the district's five-year evaluation cycle, other programs that were revisitedincluded Basic Skills, Child Study Team and Speech. Regarding the district's SCIENCEprogram, all curriculum guides were realigned to the recently released 2009 NJCCCS toincorporate technology integration, student modifications and differentiated methods ofinstruction in order to greater meet the needs of all learners.

Staff development activities are implemented on an ongoing basis in accordance with thedistrict's Professional Development Plan, which is closely aligned with the district's five-yearplan for the evaluation and development of curriculum. Staff development priorities are

4

identified as a result of the comprehensive review and analysis of numerous data sources.including: state assessments, standardized tests, district benchmark/annual assessments,anecdotal records, literacy portfolios, attendance records, discipline records, staff/parentsurveys, teacher/administrative input, parent-teacher conferences, school-based planningteam meetings, guidance office referrals, intervention and referral services committees,student mobility data and program evaluation reports.

The district is committed to addressing the identified priority needs and, as a result, enablingstudents to meet both the New Jersey Core Curriculum Content Standards as well as the newCommon Core State Standards. To accommodate staff schedules and learning styles, manydifferent approaches for providing professional development have been created. Theyinclude professional development days, half-day/full-day release time, before/after schoolmeetings/workshops, faculty meetings, demonstration lessons during class periods, structuredindependent study groups, inter-classroom visitations, out-of-district classroom/programvisitations, focus groups, on-line training, coaching, mentoring, training of trainers,teleconferences, distance learning, out-of-district workshops/conferences, college courses(tuition reimbursement) and the NJEA Convention.

Major staff development during the 2011-12 school year focused on integrating additionalteaching strategies and modalities into all instructional areas to increase student progressthrough varying teaching methods to reach all learners.

• Staff members participated in numerous workshops/seminars/courses. Professionaldevelopment is provided by consultants and district staff members. These inserviceopportunities were related to staff members' individual needs as identified on theirProfessional Development Plans (PDPs). All professional development activities areevaluated in writing and discussed informally at faculty/curriculum meetings. Theresults are compiled and utilized for future inservice opportunities. Teachers turnkeyappropriate information acquired at out-of-district workshops.

The district implemented training on all levels in compliance with the New JerseyHarassment, Intimidation and Bullying Law. All board of education members, administrators,staff, volunteers and students participated in mandatory training in the new law guidelinesincluding behavior expectations, staff and pupil responsibilities, rights and reporting. Thedistrict appointed a district anti-bullying coordinator, four (4) school anti-bullying specialistsand four (4) school safety teams all of which participated in intensive training promoting pro-social behaviors. Each school focused on strengthening practices and creating programs todevelop, foster and maintain a positive school climate. In accordance with the regulatorycomponents of the New Jersey Department of Education, the district was one of the fewdistricts in Cape May County that did not have a single HIB incident occur during the 2011-12 SY.

Entitlement funds from Title I, Title IIA, Title III and the Individuals with DisabilitiesEducation Act, Part B Aid assisted in providing additional specialized educationalopportunities for at-risk students. The American Recovery & Reinvestment Act (ARRA) of20 I0 funds for equipment and training continues to incorporate SMART© Technology as thepreferred method to introduce new material in the whole classroom instructional setting. 1-Respond carts provide opportunities for students to respond individually to a visual prompt,or interact with whiteboard or SMART© screen activities.

The entire district has wireless internet which maximizes each teachable moment. Whileclassroom teachers provide small group instruction, remaining students engage in individual

5

independent practice via the technology resources including Leapster, Book Flix©(preschool-a"), web-developed classroom websites via Site@School, Study Island (readinginterventionlNJASK skills: grades 3-6), and SkillsTutor© (NJPASS skills: grades 1-2).WEB-DRVs (web-digital video recordings) of grade-appropriate educational videos, accessto online graphic novels and utilization of additional educational software, such as Journeys,EnVision and World Book resources complimented the 2151 Century and Technology Toolsavailable to all students. All instructional staff participated in technology sessions focusing onthe ever-growing menu of technology enhancements available.

Lower Township School District's Technology Initiative requires every teacher to developand complete at least one integrated technology project per academic year. With the plethoraof technology initiatives, teachers can now create and present interactive lessons geared forthe multiple intelligences of the visual, auditory and special intelligence modalities. Theseadvancements in instructional techniques and processes provide students greater opportunitiesto reach their potential.

4. INTERNAL ACCOUNTING CONTROLS:

Management of the District is responsible for establishing and maintaining an internal controlstructure designed to ensure that the assets of the District are protected from loss, theft ormisuse and to ensure that adequate accounting data are complied to allow for the preparationof financial statements in conformity with generally accepted accounting principles (GAAP).The internal control structure is designed to provide reasonable, but not absolute, assurancethat these objectives are met. The concept of reasonable assurance recognized that: ( I) thecost of a control should not exceed the benefits likely to be derived; and (2) the valuation ofcosts and benefits requires estimates and judgments by management.

As a recipient of federal and state financial assistance, the District also is responsible forensuring that an adequate internal control structure is in place to ensure compliance withapplicable laws and regulations related to those programs. This internal control structure isalso subject to periodic evaluation by the District management.

As part of the District's single audit described earlier, tests are made to determine theadequacy of the internal control structure, including that portion related to federal and statefinancial assistance programs, as well as to determine that the District has complied withapplicable laws and regulations.

5. BUDGETARY CONTROLS:

In addition to internal accounting controls, the district maintains budgetary controls. Theobjective of these budgetary controls is to ensure compliance with legal provisions embodiedin the annual appropriated budget approved by the voters of the municipality. Annualappropriated budgets are adopted for the general fund, the special revenue fund, and the debtservice fund. Project-length budgets are approved for the capital improvements accounted forin the capital project fund. The final budget amount as amended for the fiscal year isreflected in the financial section.

An encumbrance accounting system is used to record outstanding purchase commitments ona line item basis. Open encumbrances at year-end are canceled or are included asreappropriations of fund balance in the subsequent year. Amounts to be reappropriated arereported as reservations of fund balance at June 30, 2012.

6

6. ACCOUNTING SYSTEM AND REPORTS:

The District's accounting records reflect generally accepted accounting principles, aspromulgated by the Governmental Accounting Standards Board (GASB). The accountingsystem of the District is organized on the basis of funds and account groups. These funds andaccount groups are explained in "Notes to the Financial Statements", Note I.

7. CASH MANAGEMENT:

The investment policy of the District is guided in large part by state statute as detailed in"Notes to the Financial Statements," Note 2. The District has adopted a cash managementplan which requires it to deposit public funds ill the New Jersey Cash Management Fund or inpublic depositories protected from loss under the provisions of the Government Unit DepositProtection Act ("GUDPA"). GUDPA was enacted in 1970 to protect Governmental Unitsfrom a loss of funds on deposit with a failed banking institution in New Jersey. The lawrequires governmental units to deposit public funds only in public depositories located inNew Jersey, where the funds are secured in accordance with the Act.

8. RISK MANAGEMENT:

The Board carries various forms of insurance, including but not limited to general liability,automobile liability and comprehensive/collision, hazard and theft insurance 011 property andcontents, and fidelity bonds.

9. OTHER INFORMATION:

<I. Independent Audit - State statutes require an annual audit by independentcertified public accountants or registered municipal accountants. The accountingfirm of Inverso & Stewart, LLC, was selected by the Board's audit committee.In addition to meeting the requirements set forth in state statues, the audit alsowas designed to meet the requirements of the Single Audit Act of 1984 and therelated OMB Circular A-133 and State Treasury Circular Letter 04-04 OMB.This auditor's report on the general purpose financial statements and combiningand individual fund statements and schedules is included in the financial sectionof this report. The auditor's reports related specifically to the single audit areincluded in the single audit sections of this report.

10. ACKNOWLEDGEMENTS:

We would like to express our appreciation to the members of the Township of Lower SchoolBoard for their concern in providing fiscal accountabil ity to the citizens and taxpayers of theschool district and thereby contributing their full support to the development and maintenanceof our financial operation. The preparation of this report could not have been accomplishedwithout the efficient ancl dedicated services of our financial ancl accounting staff.

Respectfully subm itted,

7

Lower Township School DistrictCape May, New Jersey

ORGANIZATIONAL CHART

LOWER TOWNSHIP BOARD OF EDUCATION(Elected by the Voters of Lower Township)

File Code: 1110ADOPTED: MAY 10, 2011

INTERIM SUPERINTENDENT(All Sta~

SUPERVISOR OFSPECIAL SERVICES

SCHOOL BUSINESS ADMINISTRATOR/BOARD SECRETARY(All Business Office S Iaf/)

ALLSPEClALEDUCATION STAFFFOOD SERVICE

BUlI.DINGS ANDTRANSPORT AnON

GROUNDSSUPERVISOR SUPERVISOR

SUPERVISOR

Au. TRANSPORTATION ALL FOOD SERVICE Al.L MAINTENANCE

STAFF STAFF & CUSTODIAL STAFF

PRINCIPALS

ALL BUILDING-LEVEL STAFF

C:VlsiolOrpnl1~llon.J Chan 2011

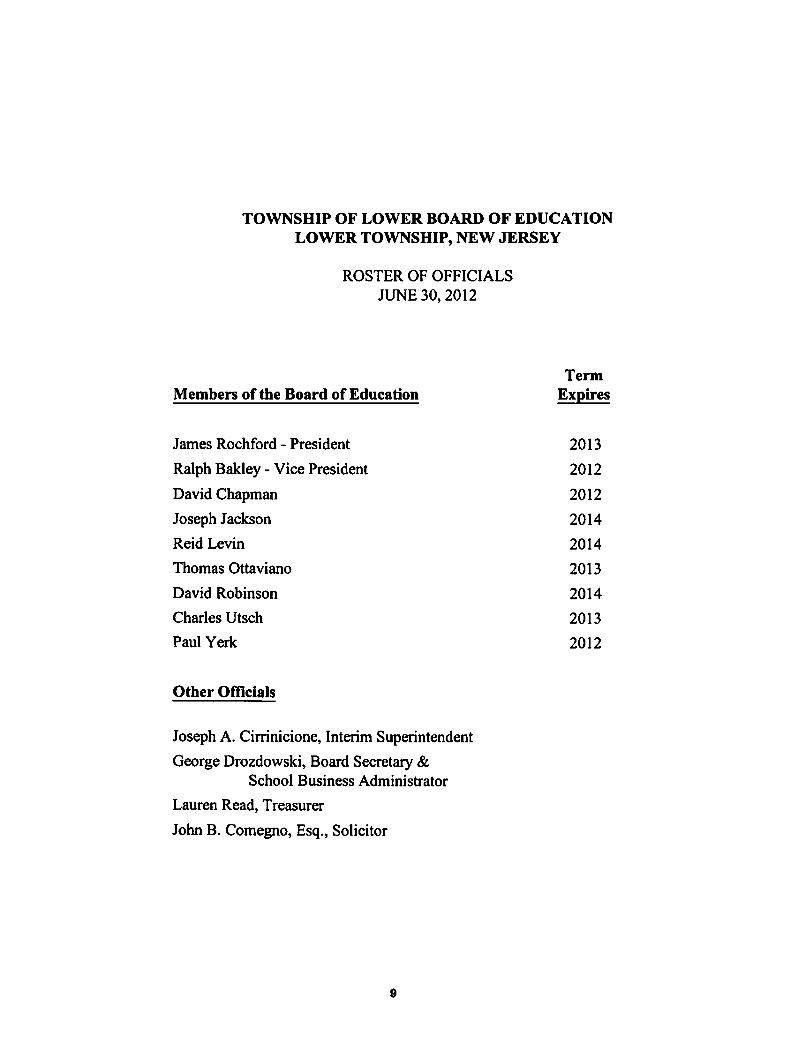

TOWNSHIP OF LOWER BOARD OF EDUCATIONLOWER TOWNSHIP, NEW JERSEY

ROSTER OF OFFICIALSJUNE 30, 2012

Members of the Board of EducationTerm

Expires

James Rochford - President

Ralph Bakley - Vice President

David Chapman

Joseph Jackson

Reid Levin

Thomas Ottaviano

David Robinson

Charles Utsch

Paul Yerk

2013

2012

2012

2014

2014

2013

2014

2013

2012

Other Officials

Joseph A. Cirrinicione, Interim Superintendent

George Drozdowski, Board Secretary &School Business Administrator

Lauren Read, Treasurer

John B. Comegno, Esq., Solicitor

9

Attorney

TOWNSHIP OF LOWER SCHOOL DISTRICTCONSULTANTS AND ADVISORS

Audit Firm

Inverso & Stewart, LLC12000 Lincoln Drive West

Suite 402Marlton, NJ 08053

John B. ComegnoComegno Law Group

521 Pleasant Valley AvenueMoorestown, NJ 08057

Official Depository

Sturdy Savings Bank3851 Bayshore Road

North Cape May, NJ 08204

lU

Financial Section

INVERSO & STEWART, LLC

Certified Public AccountantsRegistered Municipal Accountants

12000 Lincoln Drive West, Suite 402Marlton, New Jeney 08053(856) 983-2244Fax (856) 983-6674E-Mail: Iscnas(cilcllncentrir.net

-Member of-American Institute of CPAsNew Jenty Society orCPAs

INDEPENDENT AUDITOR'S REPORT

The Honorable President and Membersof the Board of Education

Township of Lower School DistrictCounty of Cape MayCape May, New Jersey

We have audited the accompanying financial statements of the governmental activities, the business-type activities, eachmajor fund and the aggregate remaining fund information of the Lower Township School District, in the County of CapeMay, State of New Jersey (School District), as of and for the fiscal year ended June 30, 2012, which collectively comprisethe School District's basic financial statements as listed in the table of contents. These financial statements are theresponsibility of the School District's management. Our responsibility is to express opinions on these financial statementsbased on our audit.

We conducted our audit in accordance with auditing standards generally accepted in the United States of America; thestandards applicable to financial audits contained in Government Auditing Standards. issued by the Comptroller Generalof the United States; and in compliance with audit requirements as prescribed by the Division of Finance, Department ofEducation, State of New Jersey. Those standards require that we plan and perform the audit to obtain reasonableassurance about whether the financial statements are free of material misstatement. An audit includes consideration ofinternal control over financial reporting as a basis for designing audit procedures that are appropriate in thecircumstances, but not for the purpose of expressing an opinion on the effectiveness of the School District's internalcontrol over financial reporting. Accordingly, we express no such opinion. An audit includes examining, on a test basis,evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing theaccounting principles used and significant estimates made by management, as well as evaluating the overall financialstatement presentation. We believe that our audit provides a reasonable basis for our opinions.

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financialposition of the governmental activities, business-type activities, each major fund and the aggregate remaining fundinformation of the Lower Township School District, in the County of Cape May, State of New Jersey, as of June 30,2012, and the respective changes in financial position and. where applicable, cash flows thereof for the fiscal year thenended in conformity with accounting principles generally accepted in the United States of America.

In accordance with Government Auditing Standards, we have also issued our report dated October 16, 2012 on ourconsideration of the Lower Township School District, in the County of Cape May, State of New Jersey's internal controlover financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts and grantagreements and other matters. The purpose of that report is to describe the scope of our testing of internal control overfinancial reporting and compliance and the results of that testing, and not to provide an opinion on the internal controlover financial reporting or on compliance. That report is an integral part of an audit performed in accordance withGovernment Auditing Standards and should be considered in assessing the results of our audit.

12

The accompanying management's discussion and analysis and budgetary comparison information, as listed in the table ofcontents, are not a required part of the basic financial statements but are supplementary information required byaccounting principles generally accepted in the United States of America. We have applied certain limited procedures,which consisted principally of inquiries of management regarding the methods of measurement and presentation of therequired supplementary information. However, we did not audit the information and express no opinion on it.

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise theLower Township School District's basic financial statements. The accompanying Schedule of Expenditures of FederalAwards and State Financial Assistance are presented for purposes of additional analysis as required by U.S. Office ofManagement and Budget Circular A-l33, Audits of States, Local Governments, and Non-Profit Organizations and Stateof New Jersey Circular 04-04-0MB, Single Audit Policy for Recipients of Federal Grants, State Grants and State Aid,and are not a required part of the financial statements. In addition, the introductory section, combining statements andrelated major fund supporting statements and schedules, and statistical section listed in the table of contents are alsopresented for purposes of additional analysis and are not a required part of the basic fmancial statements. The Schedulesof Expenditures of Federal Awards and State Financial Assistance, combining statements and related major fundsupporting statements and schedules have been subjected to the auditing procedures applied in the audit of the basicfinancial statements and, in our opinion, are fairly stated in all material respects in relation to the basic financialstatements taken as a whole. The introductory and statistical sections have not been subjected to the auditing proceduresapplied in the audit of the basic financial statements, and accordingly, we express no opinion on them.

Respectfully submitted,

INVERSO & STEWART, LLCCertified Public Accountants

(}P A--Robert P. InversoCertified Public AccountantRegistered Municipal Accountant

Marlton, New JerseyOctober 16, 2012

13

INVERSO & STEWART, LLC

Certified Public AccountantsRegistered Municipal Accountants

12000 Uncoln Drive West, Suite 402Marlton, New Jersey 08053(856) 983-2244Fas (8S6) 983-6674E-Mail: Ist.plIstlVcOnCenlril..nel

-Member or-Ameril'an Institute or CPAsNew Jersey Sodety orCpAs

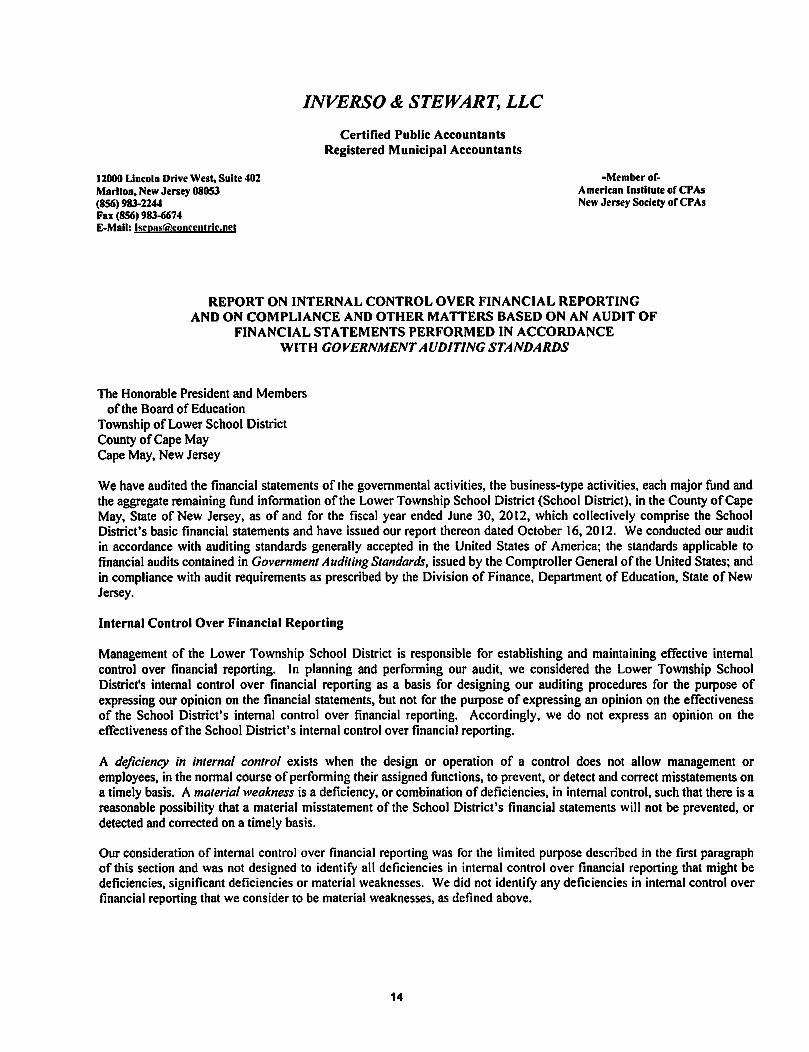

REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTINGAND ON COMPLIANCE AND OTHER MA TIERS BASED ON AN AUDIT OF

FINANCIAL STATEMENTS PERFORMED IN ACCORDANCEWITH GOVERNMENT AUDITING STANDARDS

The Honorable President and Membersof the Board of Education

Township of Lower School DistrictCounty of Cape MayCape May, New Jersey

We have audited the financial statements of the governmental activities, the business-type activities, each major fund andthe aggregate remaining fund information of the Lower Township School District (School District), in the County of CapeMay, State of New Jersey, as of and for the fiscal year ended June 30, 20' 2, which collectively comprise the SchoolDistrict's basic financial statements and have issued our report thereon dated October 16,2012. We conducted our auditin accordance with auditing standards generally accepted in the United States of America; the standards applicable tofinancial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; andin compliance with audit requirements as prescribed by the Division of Finance, Department of Education, State of NewJersey.

Internal Control Over Financial Reporting

Management of the Lower Township School District is responsible for establishing and maintaining effective internalcontrol over financial reporting. In planning and performing our audit, we considered the Lower Township SchoolDistrict's internal control over financial reporting as a basis for designing our auditing procedures for the purpose ofexpressing our opinion on the financial statements, but not for the purpose of expressing an opinion on the effectivenessof the School District's internal control over financial reporting. Accordingly, we do not express an opinion on theeffectiveness of the School District's internal control over financial reporting.

A deficiency in internal control exists when the design or operation of a control does not allow management oremployees, in the normal course of performing their assigned functions, to prevent, or detect and correct misstatements ona timely basis. A material weakness is a deficiency, or combination of deficiencies, in internal control, such that there is areasonable possibility that a material misstatement of the School District's financial statements will not be prevented, ordetected and corrected on a timely basis.

Our consideration of internal control over financial reporting was for the limited purpose described in the first paragraphof this section and was not designed to identify all deficiencies in internal control over financial reporting that might bedeficiencies, significant deficiencies or material weaknesses. We did not identify any deficiencies in internal control overfinancial reporting that we consider to be material weaknesses, as defined above.

14

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Lower Township School District's fmancial statements arefree of material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contractsand grant agreements, noncompliance with which could have a direct and material effect on the determination of financialstatement amounts. However, providing an opinion on compliance with those provisions was not an objective of ouraudit and, accordingly, we do not express such an opinion. The results of our tests disclosed no instances ofnoncompliance or other matters that are required to be reported under Government Auditing Standards and auditrequirements as prescribed by the Division of Finance, Department of Education, State of New Jersey.

We noted certain matters that we reported to management of the Lower Township School District in a separate reportentitled, Auditors Management Report on Administrative Findings - Financial. Compliance and Performance datedOctober 16,2012.

This report is intended solely for the information and use of the management of the School District, the Division ofFinance, Department of Education, State of New Jersey, and federal and state awarding agencies and pass-through entitiesand is not intended to be and should not be used by anyone other than these specified parties.

Respectfully submitted,

INVERSO & STEWART, LLCCertified Public Accountants

Robert P. InversoCertified Public AccountantRegistered Municipal Accountant

Marlton, New JerseyOctober 16,2012

15

Required Supplementary Information - Part I

Management's Discussion and Analysis

Lower Township School DistrictManagement's Discussion and AnalysisFor the Fiscal Year Ended June 30, 2012

As management of the Board of Education of the Township of Lower, New Jersey (School District), weoffer readers of the School District's financial statements this narrative overview and analysis of the SchoolDistrict for the fiscal year ended June 30, 2012. We encourage readers to consider the informationpresented in conjunction with additional information that we have furnished in our letter of transmittal,which can be found in the introductory section of this report.

Financial Highlights

• The assets of the School District exceeded its liabilities at the close of the most recent fiscalyear by $10,681,869 (net assets).

• Governmental activities have an unrestricted net assets deficit of $2,331,539. The accountingtreatments in the governmental funds for compensated absences payable, and the last twostate aid payments, and the state statute that prohibits school districts from maintaining morethan 2% of its adopted budget as unrestricted fund balance are primarily responsible for thisdeficit balance.

• The total net assets of the School District decreased by $49,022, or a 0.5% decrease from theprior fiscal year-end balance.

• Fund balance of the School District's governmental funds increased by $49,656resulting in an ending fund balance of $2,056,958. This increase is largely due to the resultsof operations of the General Fund.

• Business-type activities have unrestricted net assets of$350,571.

• The School District's long-term obligations decreased by $217,518 which is a decrease incompensated absences.

Overview of the Basic Financial Statements

This discussion and analysis is intended to serve as an introduction to the School District's basic financialstatements. Comparison to the prior year's activity is provided in this document. The basic financialstatements are comprised of three components: I) District-wide financial statements, 2} Fund financialstatements, and 3) Notes to the basic financial statements. This report also contains other supplementaryinformation in addition to the basic financial statements themselves.

District-wide Financial Statements

The district-wide financial statements are designed to provide the reader with a broad overview of thefinancial activities in a manner similar to a private-sector business. The district-wide financial statementsinclude the statement of net assets and the statement of activities.

17

The statement of net assets presents information about all of the School District's assets and liabilities. Thedifference between the assets and liabilities is reported as net assets. Over time, changes in net assets mayserve as a useful indicator of whether the financial position of the School District is improving ordeteriorating.

The statement of activities presents information showing how the net assets of the School District changedduring the current fiscal year. Changes in net assets are recorded in the statement of activities when theunderlying event occurs, regardless of the timing of related cash flows. Thus, revenues and expenses arereported in this statement even though the resulting cash flows may be recorded in a future period.

Both of the district-wide financial statements distinguish functions of the School District that are supportedfrom taxes and intergovernmental revenues (governmental activities) and other functions that are intendedto recover all or most of their costs from user fees and charges (business-type activities). Governmentalactivities consolidate governmental funds including the General Fund, Special Revenue Fund, CapitalProjects Fund, and Debt Service Fund. Business-type activities consolidate the Food Service Fund and theAfter-School Program.

Fund Financial Statements

Fund financial statements are designed to demonstrate compliance with finance-related requirements. Afund is a grouping of related accounts that is used to maintain control over resources that have beensegregated for specific objectives. All of the funds of the School District are divided into three categories:governmental funds. proprietary funds and fiduciary funds.

Governmental funds account for essentially the same information reported in the governmental activities ofthe district-wide financial statements. However, unlike the district-wide financial statements, thegovernmental fund financial statements focus on near-term financial resources and fund balances. Suchinformation may be useful in evaluating the financing requirements in the near term.

Since the governmental funds and the governmental activities report information using the same functions,it is useful to compare the information presented. Because the focus of each report differs, a reconciliationis provided on the fund financial statements to assist the reader in comparing the near-term requirementswith the long-term needs.

The School District maintains four individual governmental funds. The major funds are the General Fund,the Special Revenue Fund, the Capital Projects Fund, and the Debt Service Fund. They are presentedseparately in the fund financial statements.

The School District adopts an annual appropriated budget for the General Fund, Special Revenue Fund andthe Debt Service Fund. A budgetary comparison statement has been provided for each of these funds todemonstrate compliance with budgetary requirements.

Proprietary funds are used to present the same functions as the business-type activities presented in thedistrict-wide financial statements. The School District maintains one type of proprietary fund - theEnterprise Fund. The fund financial statements of the enterprise fund provides the same information as thedistrict-wide financial statements, only in more detail.

The School District's two enterprise funds (Food Service Fund and Day Care Program Fund) are listedindividually and are considered to be major funds.

Fiduciary funds are used to account for resources held for the benefit of parties outside the government.Fiduciary funds are not reflected in the district-wide financial statements because the resources of thosefunds are not available to support the School District's programs.

18

Notes to the Basic Financial Statements

The notes to the basic financial statements provide additional information that is essential to a fullunderstanding of the data provided in the basic financial statements.

Other Information

In addition to the basic financial statements and accompanying notes, this report also contains othersupplementary information and schedules required by the New Jersey Audit Program, issued by the NewJersey Department of Education.

District-wide Financial Analysis

The assets of the School District are classified as current assets and capital assets. Cash, investments,receivables, inventories and prepaid expenses are current assets. These assets are available to provideresources for the near-term operations of the School District. The majority of the current assets are theresults of the tax levy and state aid collection process.

Capital assets are used in the operations of the School District. These assets are land, buildings,improvements, equipment and vehicles. Capital assets are discussed in greater detail in the section titled,Capital Assets and Debt Administration, elsewhere in this analysis.

Current and long-term liabilities are classified based on anticipated liquidation either in the near-term or inthe future. Current liabilities include accounts payable, accrued salaries and benefits, unearned revenues,and current debt obligations. The liquidation of current liabilities is anticipated to be either from currentlyavailable resources, current assets or new resources that become available during fiscal year 2012. Long-term liabilities such as long-term debt obligations and compensated absences payable will be liquidatedfrom resources that will become available after fiscal year 2012.

The assets of the primary government activities exceeded liabilities by $10,3 16,298 with an unrestricteddeficit balance of$2,33 1,539. The net assets of the primary government do not include internal balances.

A net investment of $10,203,897 in land, improvements, buildings, equipment and vehicles which providethe services to the School District's public school students. Net assets oUI have been restricted to provideresources for future capital expansion and renovation projects, $1,292,246 has been restricted formaintenance projects, and $1,186,059 has been restricted for budget appropriation.

As mentioned earlier, deficit unrestricted net assets are primarily due to the accounting treatment forcompensated absences payable, the last two state aid payments, and state statutes that prohibit schooldistricts from maintaining more than 2% of its adopted budget as unrestricted fund balance.

19

Lower Township School DistrictComparative Summary of Net Assets

As of June 30, 2012 and 2011

Governmental Activities Business- Type Activities District-Wide

2012 2011 2012 2011 2012 2011

Assets:Current assets s 2,141,201 s 2,025,471 s 441,610 s 417,611 s 2,582,811 s 2.443.082

Capital assets 10,203,897 10,541,268 15.001 18.034 10.218.898 10.559.302

Total assets 12.345.098 12,566,739 456,611 435.645 12.801.709 13.002.384

Liabilities:Current Liabilities 84,243 18.168 954 1.164 85.197 19.332

Noncurrent Liabilities 1.944.557 2.161.701 90.086 90.460 2.034.643 2.252.161

Total liabilities 2,028,800 2.179.869 91.040 91.624 2.119.840 2.271.493

Net assets s 10.316,298 s 10.386.870 s 365.571 s 344,021 s 10.681.869 s 10.730.891

Net assets consist of:Invested in capital

Assets s 10.203,897 s 10,541,268 S 15,000 s 18,034 S 10,218,897 S 10.559.302Restricted net assets 2,443,940 2.378.542 2.443,940 2.378.542

Unrestricted net assets -2.331.539 -2.532.940 350.571 325.987 -1.980.968 -2.206.953

Net assets s 10,316,298 s 10,386.870 s 365.571 s 344.021 s 10.681.869 s 10.730.891

20

Lower Township School DistrictComparative Schedule of Changes in Net Assets

As of and for the Fiscal Year Ended June 30, 2012 and 2011

Governmental Activities Business-Type Activities District-Wide

2012 2011 2012 2011 2012 2011

Revenues:Program Revenues

Charges for services s 677,423 s 666,854 s 677,423 s 666,854

Operating grants and

Contributions s 3,340,003 s 3,025,112 748,186 697,275 4,088,189 3,722,387

General Revenues:

Property Taxes 14,659,327 14,371,889 14,659,327 14,371,889

Unrestricted State Aid 10,199,023 9,435,089 10,199,023 9,435,089

Tuition 19,971 35,869 19,971 35,869

Other Revenues 182,353 82,233 383 993 182,736 83,226

Total Revenues 28,400,677 26,950,192 1.425,992 1,365,122 29,826,669 28,315,314

Expenses:Governmental Activities:

Instruction 12,239,156 12,335,514 12,239,156 12,335,514Tuition 508,575 331,532 508,575 331,532Related Services 2,737,645 2,779,070 2,737,645 2,779,070Administrative

Services 1,195,374 1,123,685 1,195,374 1,123,685Central Services 357,775 351,603 357,775 351,603Operations and

Maintenance 2,464,083 2,181,749 2,464,083 2,181,749Transportation 1,299,670 1,153,759 1,299.670 1,153,759Employee Benefits 7,666,662 7,222,560 7.666.662 7,222,560Interest on long-term

Debt

Other 2,309 23,465 2,309 23,465Business-Type Activities:Food Service Operations 1,119,007 1.154,673 1,119,007 1,132,556

Day Care Program 285,435 336,113 285,435 314,208

Total Expenses 28,471.249 27,502,937 1,404,442 1,446,764 29.875.691 28,949,701

Increase in net assetsBefore transfers -70,572 -552.745 21,550 -81,642 -49,022 -634,387

Transfers

Changes in net assets -70,572 -552,745 21.550 -81,642 -49,022 -634,387Net assets, July I, 101386,870 101939,615 3441021 425,663 10,730,891 11,365.278Net assets. June 30. S 10,316.298 S 10,386,870 s 365,571 S 344,021 s 10,681,869 S 10.730,891

21

Governmental Activities

Governmental activities decreased the net assets of the School District by $70,572 during the current fiscalyear. Key elements of the decrease in net assets for governmental activities are as follows:

• Capital additions less depreciation expense decreased $337,372.

• Compensated absences decreased by $217,144.

Business-type Activities

Business-type activities increased the School District's net assets by $21,550. Key elements of the increasein net assets for business-type activities are as follows:

• The Food Service Fund had a net loss of $14,55 I and the Day Care Program had a netgain of$36,101.

Financial Analysis of the Governmental Funds

As noted earlier, the School District uses fund accounting to ensure and demonstrate compliance withfinance-related legal requirements.

Governmental Funds» The focus of the School District's governmental funds is to provide information onnear-term inflows, outflows, and balances of spendable resources. Such information is useful in assessingthe School District's financing requirements. In particular, unreserved fund balance may serve as a usefulmeasure ofa government's net resources available for spending at the end of the fiscal year.

As of the end of the current fiscal year, the School District's governmental funds reported a combinedending fund balance of $2,056,959, an increase of $49,656 in comparison with the prior year. Most of thisincrease is due to the General Fund results of operations.

The deficit unreserved fund balance for the School District at the end of the fiscal year includes acombination of an unreserved deficit fund balance for the General Fund of ($386,982) and ($34,366)in the Special Revenue Fund. The remainder of the fund balance is reserved to indicate that it is notavailable for new spending because it has already been committed I) as restricted cash reserved for futurecapital outlay expenditures of $1,2) $771,286 appropriated as a revenue source in the subsequent year'sbudget, 3) $407,533 reserved for future budget appropriation in accordance with state statute, 4) $7,239reserved for encumbrances, and 5) $1,292,246 reserved for maintenance.

The general fund is the chief operating fund of the School District. As discussed earlier, the balance in theunreserved fund balance is due, primarily, to the accounting treatment of the last two state aid payments asdiscussed in Note 17 of the notes to the basic financial statements, and state statutes that prohibit NewJersey school districts from maintaining more than 2% of its adopted budget as unrestricted fund balance.

22

General Fund Budgetary Highlights

The difference between the original budget and the final amended budget was $24,929 or a increase of.001%. The increase to the budget was due to reserve for encumbrances, Education Jobs Funds andNonpublic Transportation.

At the end of the current fiscal year, unassigned fund balance (budgetary basis) of the general fund was$499,613 while total fund balance (budgetary basis) was $2,977,919. As a measure of the general fund'sliquidity, it may be useful to compare both unreserved fund balance (budgetary basis) and total fundbalance (budgetary basis) to total general fund expenditures. Actual (budgetary basis) expenditures of theGeneral Fund including other financing uses amounted to $26,952,122. Unreserved fund balance(budgetary basis) represents 1.85% of expenditures while total fund balance (budgetary basis) represents11.05% of that same amount.

Capital Asset and Debt Administration

The School District's investment in capital assets for its governmental and business-type activities as ofJune 30, 2012, totaled $10,218,898 (net of accumulated depreciation). This investment in capital assetsincludes land, improvements, buildings, equipment and vehicles. The total decrease in the District'sinvestment in capital assets for the current fiscal year was $340,404 or a 3.22% decrease. The decrease isdue to depreciation.

Capital Asset (net of accumulated depreciation)June 30, 20ll and 2011

Governmental Activities Business-Type Activities District-Wide

2012 2011 2012 2011 2012 2011

Land S 80,045 S 80,045 S 80,045 S 80,045Consnuctien inProgressBuildings and Building

Improvements 9,524,475 9,887,320 9,524,475 9,887,320Equipment 599,077 573,903 S 15,001 S 18,034 614,078 591,937

Net assets S 10,203,597 S 10,541,268 s 15.001 s 18,034 S 10.218,598 S 10,559,302

Additional information on the School District's capital assets can be found in the notes to the basicfinancial statements (Note 5) of this report.

Long-term debt - During the fiscal year ended June 30, 2012, the School District had $1,944,557 incompensated absences.

State statutes limit the amount of general obligation debt that the District may issue. At the end of thecurrent fiscal year, the legal debt limit was $104,439,224. The available amount as of June 30, 2012 is$104,439,224.

Additional information on the School District's long-term obligations can be found in the notes to the basicfinancial statements (Note 7) of this report.

23

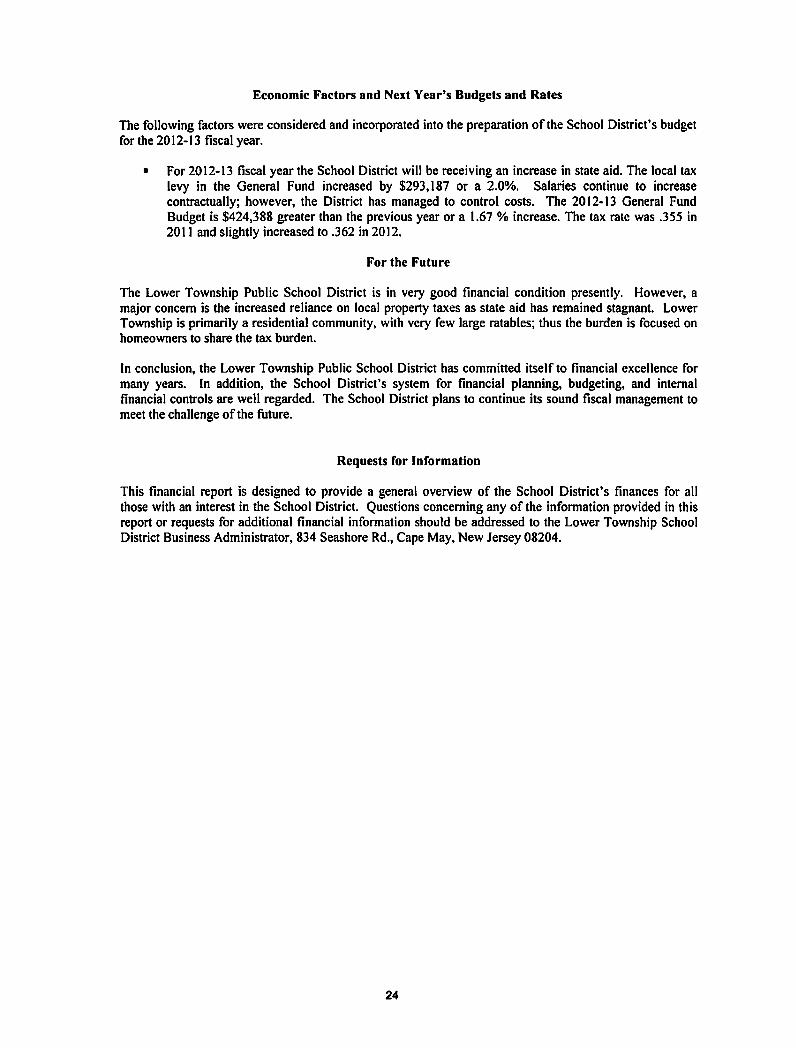

Economic Factors and Next Year's Budgets and Rates

The following factors were considered and incorporated into the preparation of the School District's budgetfor the 2012-13 fiscal year.

• For 2012-13 fiscal year the School District will be receiving an increase in state aid. The local taxlevy in the General Fund increased by $293,187 or a 2.0%. Salaries continue to increasecontractually; however, the District has managed to control costs. The 2012-13 General FundBudget is $424,388 greater than the previous year or a 1.67 % increase. The tax rate was .355 in2011 and slightly increased to .362 in 2012.

For the Future

The Lower Township Public School District is in very good financial condition presently. However, amajor concern is the increased reliance on local property taxes as state aid has remained stagnant. LowerTownship is primarily a residential community, with very few large ratables; thus the burden is focused onhomeowners to share the tax burden.

In conclusion, the Lower Township Public School District has committed itself to financial excellence formany years. In addition, the School District's system for financial planning, budgeting, and internalfinancial controls are well regarded. The School District plans to continue its sound fiscal management tomeet the challenge of the future.

Requests for Information

This financial report is designed to provide a general overview of the School District's finances for allthose with an interest in the School District. Questions concerning any of the information provided in thisreport or requests for additional financial information should be addressed to the Lower Township SchoolDistrict Business Administrator, 834 Seashore Rd., Cape May, New Jersey 08204.

24

Basic Financial Statements

District-Wide Financial Statements

A-1LOWER TOWNSHIP SCHOOL DISTRICT

Statement of Net AssetsJune 30,2012

Governmental Business-typeActivities Activities Total

ASSETS:Cash and cash equivalents $2,037,872 $293,801 $2,331,673Receivables, net 186,863 48,562 235,425Inventory (Note 6) 15,712 15,712Internal balances (83,535) 83,535Restricted assets:

Restricted cash and cash equivalents 1 1Capital assets, net (Note 5) 10,203,897 15,001 10,218,898

Total assets 12,345,098 456,611 12,801,709

UABIUTlES:Accounts payable 84,243 84,243Deferred revenue 954 954Noncurrent liabilities (Note 7):

Due within one yearDue beyond one year 1,944,557 90,086 2,034,643

Total liabilities 2,028,800 91,040 2,119,840

NET ASSETS:Invested in capital assets, net of related debt 10,203,897 15,000 10,218,897Restricted for:

Special Revenue (34,366) (34,366)Capital Projects 1 1Other purposes 2,478,305 2,478,305

Unrestricted (2,331,539) 350,571 (1,980,968)

Total net assets $1013161298 $3651571 $1016811869

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

27

A-2

LOWER TOWNSHIP SCHOOL DISTRICTStatement of Activities

For the Fiscal Year Ended June 30, 2012

FunctionsIPrograms

Program RevenuesNet (Expense) Revenue and

Changes In Net Assets

ExpensesCharges for

Services

OperatingGrants and

ContributionsGovernmental Business-type

Activities Activities Total

Govemmental activities:Instruction:

RegularSpecial educationOther instruction

Support Services:TuitionStudent & instruction related servicesGeneral administrative servicesSchool administrative servicesCentral servicesPlanl operations and maintenancePupiltransportalionUnallocated employee benefits

Unallocated depreciation and amortizationTolal govemmental activities

BUSiness-type activities:Day care programFood service programTotal business-type activities

Total primary govemment

$9,592,665 $681.861 ($8.910,804) ($8,910.804)2,552,724 509.436 (2.043.288) (2.043,288)

93,767 (93.767) (93.767)

508.575 (508.575) (508,575)2.737.645 1n.248 (2,560.397) (2,560.397)

272.846 (272.846) (272.846)922,528 (922.528) (922,528)357,775 (357,775) (357,775)

2,464,083 (2,464,083) (2,464,083)1,299,670 (1,299,670) (1,299,670)7,666,662 1,971,458 (5,695,204) (5,695,204)

2,309 {2,309~ {2,309~28,471,249 3,340,003 (25.131,246) (25,131,246)

285,435 $321,536 $36,101 36,1011,119,007 3551887 748,186 {14,934} {141934}114041442 6n,423 748,186 21,167 21,167

$291875,691 $677,423 $4,088,189 {$25,131,246} $21,167 {$25,110,079}

General revenues:Taxes:

Property taxes, levied for general purposes, net 14,659,327 14,659,327Federat and state aid not restricted 10,199,023 10,199,023Tuition charges 19,971 19,971Miscellaneous income 182,353 383 182,736Transfer

Total general revenues, special items, extraordinary items and transfers 25,060,674 383 25,061,057Change in Net Assets (70,572) 21,550 (49,022)

Net Assets - July 1 10,386.870 344,021 10,730,891Net Assets - June 30 $10,316,298 $365,571 $10,681,869

The accompanying Notes to the Basic Financial Stalements are an integral part of this statement.

Fund Financial Statements

ASSETS

Assets:Cash and cash equivalentsReceivables, netInterfund receivableRestricted cash and cash equivalents

Total assets

UABIU"nES AND FUND BALANCESUabilities:

Accounts payableInterfund payables

Total liabilities

Fund Balances:Restricted for:

Excess surplusExcess surplus - designated for

subsequent year's expendituresMaintenance reserveCapital reserve

Assigned to:Year-end encumbrancesSubsequent year's expenditures

Unassigned

Total fund balances

Total liabilities and fund balances

LOWER TOWNSHIP SCHOOL DISTRICTBalance Sheet

Governmental FundsJune 30,2012

GeneralFund

SpecialRevenue

Fund

CapitalProjects

Fund

DebtServiceFund

$2,037,87216,316

136,6021

$138,315

$2,190,791 $138,315

13,81485,653

70,429102,252

99,467 172,681

B-1

TotalGovemmental

Funds

$2,037,872154,631136,602

1

$2,329,106

84,243187,905

272,148

407,534 407,534

507,648 507,6481,292,246 1,292,246

1 1

7,239 7,239263,638 263,638

(386,982) (34,366) (421,348)

2,091,324 (34,366) 2,056,958

$2,190,791 $138,315

Amounts reported for govemmental activities In the statement of net assets(A-1) are different because:

Capital assets used in govemmental activities are not financial resourcesand therefore are not reported in the funds. The cost of the assets Is$19,481,914 and the accumulated depreciation is $9,278,017.

Long-term liabilities, Including bonds payable, are not due and payableIn the current period and therefore are not reported as liabilities in thefunds.

Net assets of govemmental activities

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

30

10,203,897

(1 ,944,557)

$10,316,298

B-2LOWER TOWNSHIP SCHOOL DISTRICT

Statement of Revenues, Expenditures and Changes In Fund BalancesGovernmental Funds

for the Fiscal Year Ended June 30,2012

Special Capital Debt TotalGeneral Revenue Projects Service Governmental

Fund Fund Fund Fund FundsREVENUES:Local sources:

Local tax levy $14,659,327 $14,659,327Tuition charges 19,971 19,971Miscellaneous 1821353 1821353

Total revenues·1oca1sources 14,861,651 14,861,651

Local sources $1,500 I,SOOState sources 11,736,708 348,850 12,085,558Federal sources 4331n2 11°18.195 114511967

Total revenues 27,0321131 11368.545 28,4001676

EXPENDITURES:Current expense:

Regular instruction 8.811.018 676,667 9,487,685Special education instruction 2.043,288 509,436 2,552,724Other instruction 93,767 93,767Support services and undistributed costs:

Tuition 508.575 508,575Student & instruction related services 2,S60,397 In.248 2.737.645General administrative services 272,846 272,846School administrative services 876,S11 876,511Central services 357,nS 357,n5Plant operations and maintenance 2,313,328 2.313,328Pupil transportation 1,299.670 1.299,670Unallocated employee benefits 7.666.662 7,666,662

Capital outlay 1481285 148.285

Total expenditures 2619521122 113631351 281315.473

Excess (deficiency) of revenues over(under) expenditures 8°1009 51194 851203

Other Financing Sources (Uses):cancelled SOA Grant (35.548) (35,548)Transfers in 53.322 53,322Transfers out (531322} (53,322}

Total other financing sources (uses) 531322 (88.870} (3S1548}

Net change in fund balance 133.331 5,194 (88.870) 49,655Fund balances. July 1 1.9571993 (391560} 88,870 2.007,303

Fund balances. June 30 $2,091,324 ~$34I366l $2,OS6.958

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

31

,........;:::4

B-3LOWER TOWNSHIP SCHOOL DISTRICT

Reconciliation of the Statement of Revenues, Expendibnesand Changes in Fund Balances of Governmental Funds

to the Statement of Activitiesfor the Fiscal Year Ended June 30, 2012

Total net change in fund balances - governmental funds (from B-2) $49.656

Amounts reported for governmental activities in the statement of activities (A-2)are different because:

Capital outlays are reported in the governmental funds as expenditures.However. on the statement of activities. the cost of those assets is allocatedover their estimated useful lives as depreciation expense. This is the amountby which capital outlay exceeded depreciation in the current fiscal year.

Depreciation expenseCapital outlay

($410.720)73.348 (337.372)

In the statement of activities. certain operating expenses. e.g .• compensatedabsences (vacations) are measured by the amounts earned during theyear. In the governmental funds. however. expenditures for these itemsare reported in the amount of financial resources used (paid). When theearned amount exceeds the paid amount. the difference is a reduction inthe reconciliation (-); when the paid amount exceeds the earned amountthe difference is an addition to the reconciliation (+). 217.144

Change in net assets of governmental activities ($70.572)

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

32

LOWER TOWNSHIP SCHOOL DISTRICTStatement of Net Assets

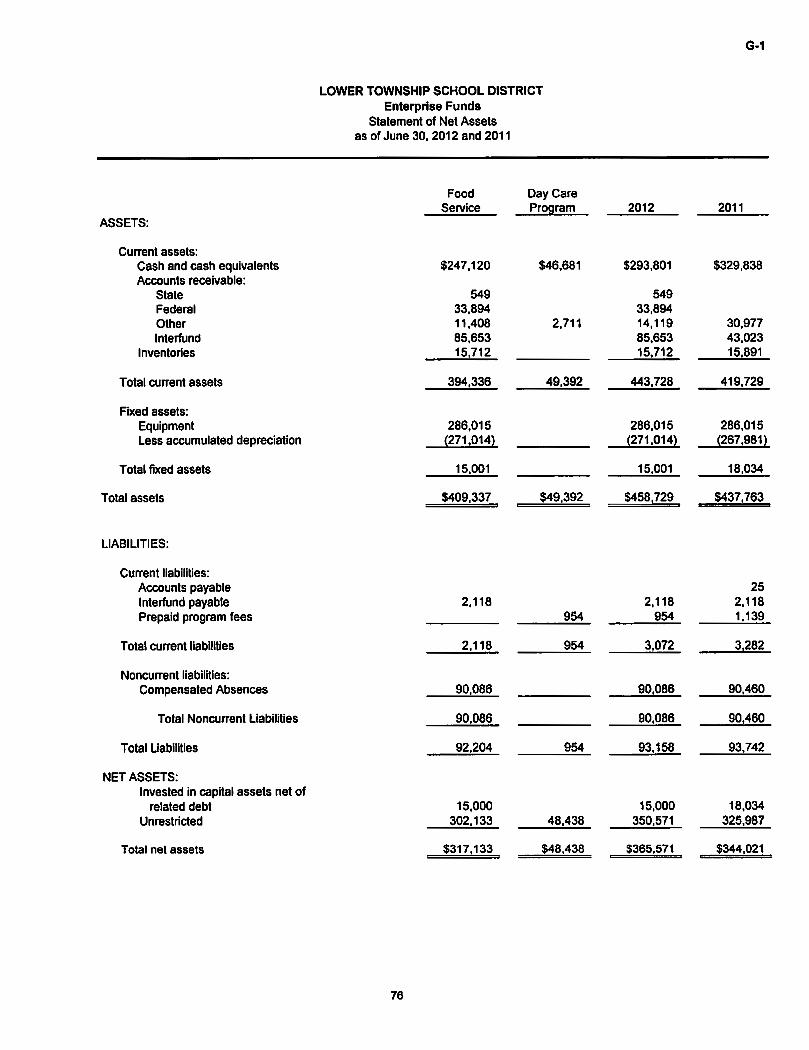

Proprietary FundsJune 30, 2012

B-4

Business-typeActivities

Enterprise Funds

FoodService

FundASSETS:

Current assets:Cash and cash equivalents $247,120

45,85185,65315,712

Accounts receivableInterfund receivableInventories

Total current assets 394,336

Noncurrent assets:EquipmentLess accumulated depreciation

286,015(271,014)

Total noncurrent assets 15,001

Total assets $409,337

LIABILITIES

Current liabilities:Accounts payableDeferred revenueInterfund payable 2,118

Total current liabilities 2,118

Noncurrent liabilities:Compensated absences 90,086

Total noncurrent liabilities 90,086

Total liabilities 92,204

NET ASSETSInvested in capital assets net of

related debtUnrestricted

15,000302,133

Total net assets $317,133

DayCare

Program

$46,681

2,711

49,392

$49,392

954

954

954

48.438

$48.438

33

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

8-5

LOWER TOWNSHIP SCHOOL DISTRICTStatement of Revenues, Expenses and Changes in Fund Net Assets

Proprietary Fundsfor the Fiscal Year Ended June 30, 2012

Business-typeActivities

Enterprise Funds

FoodService

Fund

DayCare

ProgramOperating revenues:

Charges for services:Daily sales-reimbursable programsDaily sales-non-reimbursable programs

$168,748187,139 $321,536

Total operating revenue 355,887 321,536

Operating expenses:SalariesEmployee benefitsSupplies and materialsProfessional servicesDepreciationCost of salesPurchased property servicesOther

395,536233,96831,085

1.2283.033

435,30014,3394.518

239,41918.315

27.701

Total operating expenses 1.119.007 285,435

Operating income (loss) (763,120) 36.101

Nonoperating revenues (expenses):State sources:

State school lunch programFederal sources:ARRA - National school lunch equipmentNational school lunch programSchool breakfast programSnack ProgramU.S.D.A. commodities

Local sources:Operating transfer inInterest revenue

10,864

405,061264.392

3.32264.547

383

748.569

(14,551) 36.101

331.684 12.337

$317.133 $48,438

Total nonoperating revenues (expenses)

Change in net assets

Total net assets - July 1

Total net assets - June 30

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

34

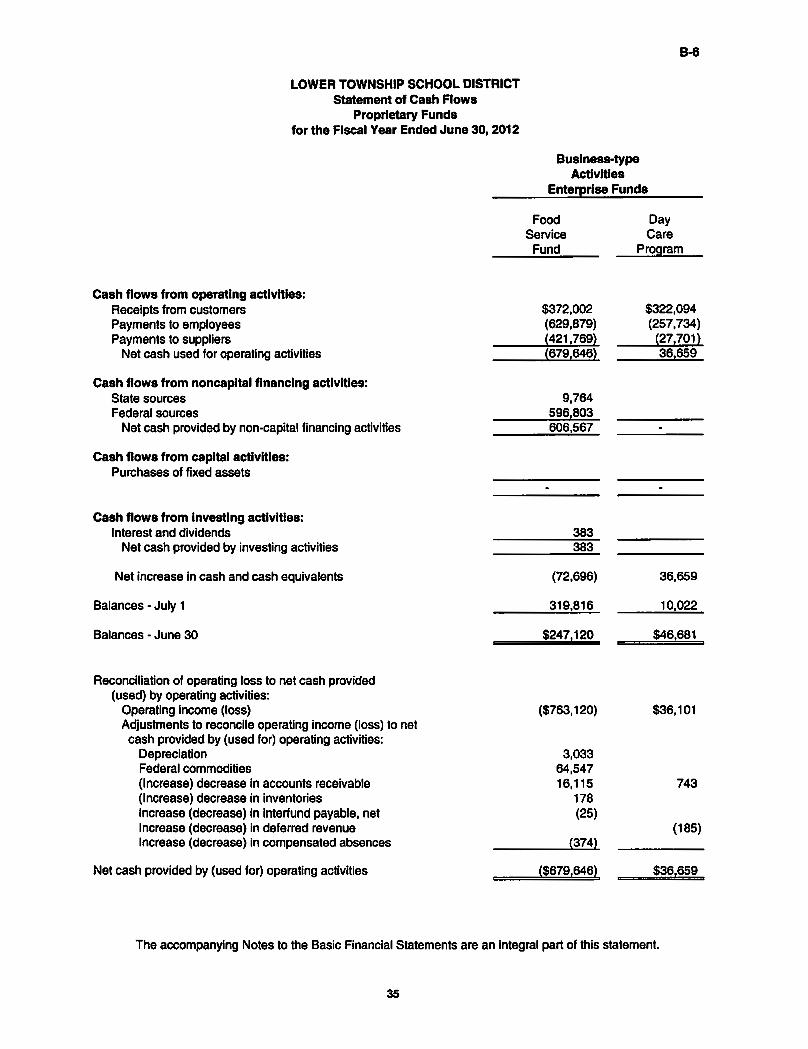

LOWER TOWNSHIP SCHOOL DISTRICTStatement of Cash Flows

Proprietary Fundsfor the Fiscal Year Ended June 30,2012

Business-typeActivities

Enterprise Funds

Cash flows from operating activities:Receipts from customersPayments to employeesPayments to suppliers

Net cash used for operating activities

Cash flows from noncapltal financing activities:State sourcesFederal sources

Net cash provided by non-capital financing activities

Cash flows from capital activities:Purchases of fixed assets

Cash flows from Investing activities:Interest and dividends

Net cash provided by investing activities

Net increase in cash and cash equivalents

Balances - July 1

Balances - June 30

Reconciliation of operating loss to net cash provided(used) by operating activities:

Operating income (loss)Adjustments to reconcile operating income (loss) to net

cash provided by (used for) operating activities:DepreciationFederal commodities(Increase) decrease in accounts receivable(Increase) decrease in inventoriesIncrease (decrease) in interfund payable, netIncrease (decrease) in deferred revenueIncrease (decrease) In compensated absences

Net cash provided by (used for) operating activities

FoodService

Fund

$372,002(629,879)(421,769)(679,646)

9,764596,803606,567

383383

(72,696)

319,816

$247,120

($763,120)

3,03364,54716,115

178(25)

(374)

($679.646)

DayCare

Program

$322,094(257,734)

(27,701)36,659

36,659

10,022

$46.681

$36,101

743

(185)

$36,659

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

35

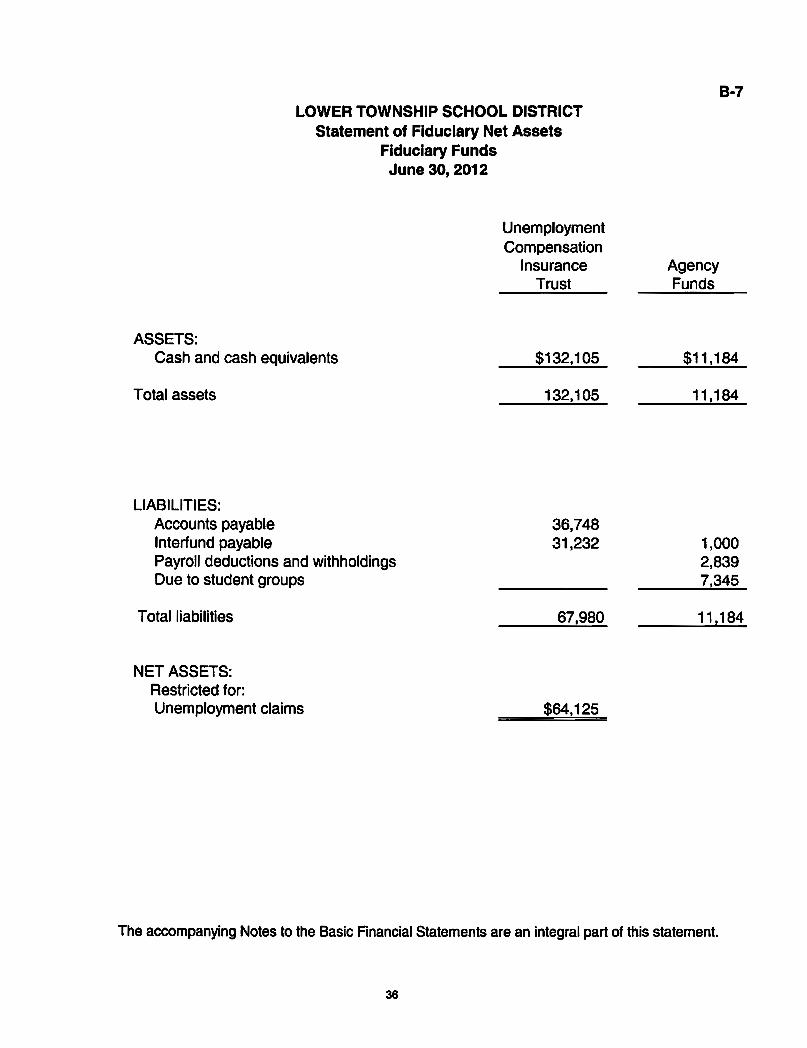

LOWER TOWNSHIP SCHOOL DISTRICTStatement of Fiduciary Net Assets

Fiduciary FundsJune 30, 2012

UnemploymentCompensation

InsuranceTrust

ASSETS:Cash and cash equivalents $132,105

Total assets 132,105

LIABILITIES:Accounts payableInterfund payablePayroll deductions and withholdingsDue to student groups

36,74831,232

Total liabilities 67,980

NET ASSETS:Restricted for:Unemployment claims $64,125

B-7

AgencyFunds

$11,184

11,184

1,0002,8397,345

11,184

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

36

LOWER TOWNSHIP SCHOOL DISTRICTStatement of Changes in Fiduciary Net Assets

Fiduciary FundsFor the Fiscal Year Ended June 30,2012

ADDITIONS:Contributions:

Board contributionsEmployee withholdings

Total Contributions

Investment earnings:InterestNet investment earnings

Total additions

DEDUCTIONS:Unemployment payments

Total deductions

Change in net assets

Net assets - July 1

Net assets - June 30

8-8

UnemploymentCompensation

InsuranceTrust

$48,86048,860

146146

49,006

25,46825,468

23,538

40,587

$64,125

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

37

Lower Township School DistrictNotes to Basic Financial Statements

For the Fiscal Year Ended June 30, 2012

I. DESCRIPTION OF SCHOOL DISTRICT AND REPORTING ENTITY

The Lower Township School District (District) is a Type II school district located in Cape May County, New Jersey andcovers an area of approximately 31 square miles. As a Type II school district, it functions independently through a Boardof Education. The Board is comprised of nine members elected to three-year terms. These terms are staggered so thatthree member's terms expire each year. The purpose of the District is to provide educational services for all of LowerTownship's students in grades preschool through 6. Students in grades 7 through 12 attend Lower Cape May Regional.The Lower Township School District has an approximate enrollment at June 30, 2012 of 1,828students.

The primary criteria for including activities within the School District's reporting entity, as set forth in Section 2100 of theGovernmental Accounting Standards Board (GASB) Codification of Governmental Accounting and Financial ReportingStandards is the degree of oversight responsibility maintained by the School District. Oversight responsibility includesfinancial interdependency, selection of governing authority, designation of management, ability to significantly influenceoperations and accountability for fiscal matters. The combined financial statements include all funds of the School districtover which the Board exercises operating control. There were no additional entities required to be included in the reportingentity under the criteria as described above. Furthermore, the School District is not includable in any other reporting entityon the basis of such criteria.

Basis of Presentation

The basic financial statements of the School District have been prepared in conformity with accounting principles generallyaccepted in the United States of America (GAAP) as applied to governmental units. The Governmental AccountingStandards Board (GASB) is the accepted standard-setting body for establishing governmental accounting and financialreporting principles. The School District also applies Financial Accounting Standards Board (FASB) Statements andInterpretations issued on or before November 30, 1989 to its governmental and business-type activities and to itsproprietary funds, provided they do not conflict with or contradict GASB pronouncements. The more significant of theSchool District's accounting policies are described below.

The School District's basic financial statements consists of government-wide statements, including a statement of net assetsand a statement of activities, and fund financial statements, which provide a more detailed level of financial information.

Government-wide Statements - The statement of net assets and the statement of activities display informationabout the School District as a whole. These statements include the financial activities of the primary government,except for fiduciary funds. The statements distinguish between those activities of the School District that aregovernmental and those that are considered business-type activities. The statement of net assets presents thefinancial condition of the governmental and business-type activities of the School District at fiscal year-end. Thestatement of activities presents a comparison between direct expenses and program revenues for each program orfunction of the School District's governmental activities and for the business-type activities of the School District.Direct expenses are those that are specifically associated with a service, program or department and, therefore,clearly identifiable to a particular function. The policy of the School District is to not allocate indirect expenses tofunctions in the statement of activities. Program revenues include charges paid by the recipient of the goods orservices offered by the program, grants and contributions that are restricted to meeting the operational or capitalrequirements of a particular program and interest earned on grants that is required to be used to support a particularprogram. Revenues, which are not classified as program revenues, are presented as general revenues of the SchoolDistrict. with certain limited exceptions. The comparison of direct expenses with program revenues identifies theextent to which each business segment or governmental function is self-financing or draws from the generalrevenues of the School District.

38

Lower Township School DistrictNotes to Basic Financial Statements

For the Fiscal Year Ended June 30,2012

I. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Fund Financial Statements - During the fiscal year, the School District segregates transactions related to certainSchool District functions or activities in separate funds in order to aid financial management and to demonstratelegal compliance. Fund financial statements are designed to present financial information of the School District atthis more detailed level. The focus of governmental and enterprise fund financial statements is on major funds.Each major fund is presented in a single column. The fiduciary fund is reported by type. The School District usesfunds to maintain its financial records during the fiscal year. A fund is defined as a fiscal and accounting entity witha self-balancing set of accounts. There are three categories of funds: governmental, proprietary, and fiduciary.

Governmental Funds - Governmental funds are those through which most governmental functions typically are financed.Governmental fund reporting focuses on the sources, uses and balances of current financial resources. Expendable assetsare assigned to the various governmental funds according to the purposes for which they mayor must be used. Currentliabilities are assigned to the fund from which they will be paid. The difference between governmental fund assets andliabilities is reported as fund balance. The following are the School District's major governmental funds:

General Fund - The general fund is the general operating fund of the School District and is used to account for allfinancial resources except those required to be accounted for in another fund. Included are certain expenditures forvehicles and movable instructional or non-instructional equipment classified in the capital outlay sub-fund.

As required by the New Jersey State Department of Education, the School District includes budgeted capital outlayin this fund. Accounting principles generally accepted in the United States of America as they pertain togovernmental entities state that general fund resources may be used to directly finance capital outlays for long-livedimprovements as long as the resources in such cases are derived exclusively from unrestricted revenues.

Resources for budgeted capital outlay purposes are normally derived from State of New Jersey aid, district taxes andappropriated fund balance. Expenditures are those which result in the acquisition of or additions to capital assets forland, existing buildings, improvements of grounds, construction of buildings, additions to or remodeling of buildingsand the purchase of built-in equipment.

In addition to the capital outlay sub-fund, the School District is accountable for an additional sub-fund, the EducationJobs Fund ("Ed Jobs"), resulting from federal legislation signed into law on August 10,2011. The Ed Jobs programwas created to provide funding assistance to states in order to save or create education jobs for the period from theSeptember 30, 2011 through September 30, 2012. Jobs funded under this program include those that provideeducational and related services for early childhood, elementary, and secondary education. Ed Jobs revenues andexpenditures are recorded in the general fund (fund 18) on a reimbursement basis. As such, revenue is not includedin the fiscal year surplus, and no portion of general fund balance at June 30, 2012 is considered to be attributable toEd Jobs. Ed Jobs expenditures are included as a component of overall general fund expenditures, and are alsoincluded in general fund expenditures for purposes of the excess surplus calculation.

Special Revenue Fund - The special revenue fund is used to account for and report the proceeds of specificrevenues sources that are restricted or committed to expenditure for specified purposes other than debt service orcapital projects.

Capital Projects Fund - The capital projects fund is used to account and report financial resources that arerestricted, committed, or assigned to expenditure for capital outlays, including the acquisition or construction ofcapital facilities and other capital assets, other than those financed by proprietary funds. The financial resources arederived from New Jersey Economic Development Authority grants, temporary notes or serial bonds which arespecifically authorized by the voters as a separate question on the ballot either during the annual election or at aspecial election.

Debt Service Fund - The debt service fund is used to account for and report financial resources that are restricted,committed, or assigned to expenditure for principal and interest.

39

Lower Township School DistrictNotes to Basic Financial Statements

For the Fiscal Year Ended June 30, 2012

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)