san francisco client forum - … – the 1920’s . b ... innovation-the-good-the-bad-and-the-ugly/...

TRANSCRIPT

SAN FRANCISCO CLIENT FORUM

January 26, 2017

Client Forum – San Francisco

WELCOME

Sheila Frierson, President, U.S. Plan Managers Andrew Moore, President, Computershare Governance Services

Client Forum – San Francisco

3

Agenda

8:50 – 9:00 a.m. Welcome

9:00 – 9:45 a.m. Use Technology to Drive Shareholder Satisfaction Brian Heffernan, Computershare

9:45 – 10:30 a.m. Prepare for Your Yearly Audit Jessica Laddon, Computershare

10:30 – 10:40 a.m. Break

10:40 – 11:25 a.m. Put Entity Management at the Core of Your Business Tom Racicot, Computershare

11:25 – 12:10 p.m. What’s Ahead for the 2017 Proxy Season Chris Dowd, Georgeson

12:10 – 12:30 p.m. Closing Remarks

12:30 – 1:30 p.m. Lunch

1:15 – 2:00 p.m. VIP Tour 1

1:30 – 2:15 p.m. VIP Tour 2

4:30 – 7:00 p.m. Beer Tasting & Brewery Tour @ Thirsty Bear

Client Forum – San Francisco

Use Technology to

Drive Shareholder

Satisfaction

› Brian Heffernan

› Vice President

› Computershare

Client Forum – San Francisco

5

Overview

Technology to Drive Shareholder Satisfaction

› Social Media

› Self Service Options

› Availability of Products or Services – wherever and whenever your customers need it

› Putting data to work

Client Forum – San Francisco

6

Social Media

What is the most active Social Media Site in the World?

A – Twitter B – YouTube C – Facebook D – LinkedIn Facebook – 1.1 BILLION unique visitors worldwide each month

Client Forum – San Francisco

› It’s a whole new world

› It can be discouraging

› It can be eye opening

› We need be part of it

7

Using Social Media to Your Advantage

Client Forum – San Francisco

› Social Media growth continues

› 78% of Americans have a Social Media Profile

8

Using Social Media to Your Advantage

https://www.statista.com/statistics/273476/percentage-of-us-population-with-a-social-network-profile/

Client Forum – San Francisco

› FOMO (fear of mission out) Stay in touch with Friends – 55%

› Stay up to date with news and events – 41%

› Fill spare time – 41%

› Funny or entertaining content – 39%

› “TO SHARE MY OPINION” – 39%

It is often one of the most unfiltered mediums by which you hear the concerns and frustrations of customers

It can be demoralizing at times!

It presents a great opportunity to provide a public forum for accountability and response

9

What are they using it for??

Client Forum – San Francisco

Your most unhappy customers are your greatest source of learning. ~ Bill Gates

10

Facing the music

› Be where your customers are

› Listen & Respond

› High Priority Items - Direct technical or account-related questions

- Complaints from dissatisfied customers

- Service or product requests that are urgent

- Issues (or outages) that affect many users or raise a potential PR crisis

› Secondary Items - Responding to general references to your products or services***

- Thanking customers who provided positive feedback

Client Forum – San Francisco

11

Social Media Responses

Client Forum – San Francisco

12

In action at Computershare

Social Media comments help to drive technology prioritization

Items which were developed in part in response to shareholders direct feedback

› Transfer Wizard

› Refinement of registration process for Investor Center

› Turbotax / HR Block compatibility

› Medallion Waiver options

› Live Chat support

Client Forum – San Francisco

13

Self Service

IVR is probably the most familiar self service tool. When did IVR first appear?

A – the 1920’s B – the 1940’s C – the 1960’s D – the 1980’s The 1960’s. Businesses began to recognize the importance of call center support, but could not find a cost effective solution. Limited due to telephone technology.

Client Forum – San Francisco

14

Helping Shareholders Help Themselves

Servicing customers / shareholders is expensive

Provide quality service at minimal cost

In an ideal world, customers will help themselves – and love doing it!

However - What we managers want… does not always sync with what customers want

Client Forum – San Francisco

15

Self Service – The Good!

ATM Machines

Rental Car Kiosks

Movie Rentals/ music purchases

IVR

Online Brokerages / Trading

“favorable impact of increased customer participation on customer satisfaction and service quality depends on the readiness of the customer to participate”

http://innovationexcellence.com/blog/2016/02/29/self-service-innovation-the-good-the-bad-and-the-ugly/

Client Forum – San Francisco

›

16

Customer Service – Self Service

http://www.creativevirtual.com/us/new-survey-takes-closer-look-top-self-service-channels/

Client Forum – San Francisco

17

The Computershare IVR Platform

› We provided IVR services for 4,302 client companies

› Received over 10 and a half million calls (10,578,477)

› Kept almost 70% within the IVR (69.73%)

› Account balance – 1.5 Million

- Sales – 700k

- Transfers – 670k

- Check Repl – 170k

- Address Changes – 125k

- Statements – 89k

- Tax information – 77k

- Tax Forms – 64k

Client Forum – San Francisco

›

18

Penny – Our Virtual Agent

http://www.creativevirtual.com/us/new-survey-takes-closer-look-top-self-service-channels/

Over 100,000 interactions each month. 92% Completion / over 70% “effective”

Client Forum – San Francisco

19

Websites

Client Forum – San Francisco

20

Availability of Products and Services

What percentage of Americans have a “Smartphone”?

A – 92% B – 77% C – 55% D – Less than 40% According to Pew Research – 77% of Americans own a smartphone. In 2012 it was less than 40%

Client Forum – San Francisco

21

Availability of Products and Services

Shareholders – Customers must have access to products and services

› Mobile availability

› Voice Technology

› Global access

› “Live Meetings”

› Text Communications

› Omni-Channel

Support for product

› Customer Support is no longer a 9 to 5 job. We need to service them where they want, when they want

› Mobile customer service

› Integration with Social Media

› Live chat

Client Forum – San Francisco

With “responsive Design” shareholder enjoy an optimized mobile website experience

No need to search for download or install an app

We detect the size of your device, and present the right experience

6% of all Investor Center Users

22

Investor Center Mobile

Client Forum – San Francisco

› Computershare launched Live Chat Support in 2013.

- Was a critical tool in helping shareholders thru the new registration process

- 16% of shareholder were less than satisfied with their live chat experience

- Shareholders wanted account specific information

› We needed the ability to offer both authenticated and Non-authenticated chat

› Enhanced Live chat was launched in 2016

- Customer service can identify logged in from non logged in & service them accordingly

23

Live Chat Support

Client Forum – San Francisco

› Computershare has offered text confirmations of trades for over 5 years.

› In July 2016, Computershare launched Support for enhanced texting .

- Over 300,000 shareholders have consented

› We can now alert shareholders:

- Cash investments

- Uncashed Checks

- Completed Transfers

- Completed Sales

24

Text Communications

Client Forum – San Francisco

25

Big Data

How much “data” is the world currently using? A – a million gigabytes B – a billion gigabytes C – a trillion gigabytes D – Too many gigabytes In 2016 the world found out what a Zettabyte looks like… that’s 1 Trillion Gigabytes of data Every day we produce 2.5 exabytes of data, or enough data to produce 90 years worth of HD Video

Client Forum – San Francisco

26

Putting Data to Work

BIG DATA Companies are inundated with incredible amounts of data – some

structured – some not so structured

Data is useless unless it is compiled and analyzed

It provides incredible opportunities for strategic decision making

1. Cost Reductions

2. Time Reductions

3. New product Development and Optimizations

4. Smart Decision Making

Client Forum – San Francisco

27

Putting Data to Work

› Who are your shareholders / customers?

› When do they reach out to you?

› Why do they reach out to you?

› In what mediums do they reach out to you?

› What are you successful in delivering?

› Where do you fall short?

This is a never ending process of analysis, and evolution

More often than not - the data is there. We just need to ask the right questions, and analyze the data appropriately

Client Forum – San Francisco

28

Lets walk thru a real life example

5 million telephone calls answered in 2015.

Who is calling?

When?

Why?

Why aren’t they able to use the IVR?

Client Forum – San Francisco

29

Who…

Every call is categorized

We extract the data

Group the data into manageable categories

We are able to see that over 30% of callers fall into a bucket we call “Other”

- More data needed

We go another level deeper. We pull calls and listen

Its individual “one-time” 3rd parties

Client Forum – San Francisco

30

When…

Client Forum – San Francisco

31

Why are they calling us?

We have lots of “one-time” 3rd parties calling us to ask about Transferring stock.

They cannot login to Investor Center because they not the shareholder

But they actually facilitated submitting the transfer request

The only channel they have to check on the status of that transfer is to call us

Client Forum – San Francisco

32

So – what do we do about it?

Lets build a direct access status portal

A person can enter the account information and get a real time status of a transfer

No NPCI is displayed

Just the status of the transfer

Goes live in March

Client Forum – San Francisco

33

Summary and Questions

› Social Media

› Self Service

› Availability

› Data

Every type of customer service (and shareholder service), every industry in every corner of the globe need to focus on these 4 components to be able to effectively and efficiently service customers.

We are doing this every day at Computershare to provide industry leading service to you and your customers.

Client Forum – San Francisco

PREPARE FOR YOUR YEARLY AUDIT

Jessica Laddon, CEP Senior Relationship Manager Computershare

Client Forum – San Francisco

35

What We Will Cover

› Developing and Performing SOX Controls

› How to Prepare Effectively for an Audit

› SOX, Financial Statements, and Tax Audits

Client Forum – San Francisco

36

Why Is this Important?

Developing and Performing SOX Controls

› Several reasons

- Due to ASC 718 requirements, equity compensation is a “high risk area”

- COSO requirements

- CEO/CFO certification of financials

- Demonstrates Avoidance of fraud

- “Blueprint” of administration

- Reducing Errors

- Promotes best practice and governance

›

Client Forum – San Francisco

37

Developing Controls

Developing and Performing SOX Controls

› Review all internal processes

- Manual vs. automation

- Which areas have most risk

› Determine frequency of when to perform control

› Determine with internal auditors which is primary and secondary controls

› Data Security –Who has access to Database or can instruct vendor?

› Secondary review when all possible

› Internal Controls cross-referencing Vendor controls

- SSAE 16 (SOC1)

› Quarterly internal certification

Client Forum – San Francisco

38

Examples of Controls

Developing and Performing SOX Controls

›

Area of Risk Control Control Activity Frequency Plan Review Plans are reviewed by

designated equity personnel to ensure compliance

• Review plan for expiration

• Share reserve reconciliation

• Grant Recipient eligibility

Annually

Grants Grants are processed accurately by proper delegated authority

• Compare Equity system generated report to HR List

• Compare control totals to Comp Committee Meeting Minutes

Quarterly

Exercises Exercises are processed accurately and timely

• Secondary review of all exercises to ensure transactions are processed correctly per broker instructions

• Comparing stock prices to prices fed into in equity system

Quarterly

Client Forum – San Francisco

39

Examples of Controls

Developing and Performing SOX Controls

›

Area of Risk Control Control Activity Frequency Cancellations Forfeiture of grants are

processed accurately and timely

Compare terms from HRIS to Equity System

Quarterly

ESPP ESPP purchases are processed accurately and timely Only delegated authority can approve ESPP purchases

• Compare contributions from Payroll to Equity System.

• Provide copies of purchase detail report and sign off sheets.

Quarterly

Shares Outstanding Roll forward accurate Compare reconciliation to Transfer Agent Reconciliation of Par Value and APIC GL’s

Quarterly

Data Security Only Delegated personnel has read/write access to equity database

Review team members and access level of equity system database.

Annually

Client Forum – San Francisco

40

Examples of Controls

Developing and Performing SOX Controls

›

Area of Risk Control Control Activity Frequency Share Based Compensation

Expense is recorded properly in financial statements

• Review expense calculation

• Review forfeiture assumption

• Review grant eligibility

Quarterly

EPS Share dilution is calculated accurately

• Proper application of treasury method

• Reconcile with outstanding shares

• Review performance

Quarterly

DTA Tax benefit is calculated accurately

• Review DTA calculation • Review grants not

subject to DTA (162M, grants not eligible for a deduction)

Annually

Client Forum – San Francisco

41

Spreadsheet Controls

Developing and Performing SOX Controls

› Version Control

- Use standard naming conventions

- Maintain historical files no longer available for update in a separate drive

› Security and Integrity of Data

- Locking or protecting cells

› Sheet Protection or Validation

› Documentation

- Notes pages within workbook document the procedures for each spreadsheet

- Assists with knowledge transfer

› Overall Review

- Checklist with all procedures

Client Forum – San Francisco

42

Organization is Key

How to Prepare Effectively for an Audit

› Always be prepared

› Create audit packages per category/transaction

- Grants

- Exercises

- ESPP

› Referencing documentation

- Tick marks

- Recalculation of formulas

› Financial statement work papers

› Roll forward

› Forfeiture calculations

› Establish checklists

Client Forum – San Francisco

43

Working with Auditors

How to Prepare Effectively for an Audit

› Establish process

- Single point of contact in department

- Understand deadlines and what is needed

- Work with internal group

› Ask Questions if you don’t understand what is being asked

› Be confident

- Remember you are the SME

Client Forum – San Francisco

44

Review Package Testing-Grants

Financial Statement Audit

› For each grant, have the following ready:

- All approval documentation

› Comp committee, board meeting minutes

› Control list from HR

- Grant award recap report in PDF format tied out to list received from HR

- Establishment of grant date

› Communication to awardees of grant

- Grant agreements

- Shares granted from correct plan

- Reserve reconciliation

Client Forum – San Francisco Example of Referencing From/To

45

Provided by Compensation

Dear Stock Administrator

Please grant the following RSUs from Stock Plan XYZ 2/ to the following individuals as approved Comp Committee. Grant date is 4/1/16. 2/

Participant Name Employee ID Options/Awards Granted

Employee A 1 46,494

Employee B 2 75,107

Employee C 3 7,153

Employee D 4 7,153

Employee E 5 53,648

Employee F 6 42,918

Employee G 7 7,153

Total 239,626 rx 2/

Please let me know if you have any questions

Sincerely

Judy Brown

Director of Compensation

1/

Client Forum – San Francisco Example of Referencing From/To

46

2/

Grant Plan Number - Name (Type)

Participant Name

Employee ID

Grant Type Code

Grant ID Grant DateOptions/Awards

GrantedGrant Price

FMV at Grant Aggregate Grant Price

1/ Stock Plan XYZ Employee A 1 RSU 29 1/ 04/01/2016 46,494 $0.0000 $0.0000 $0.00

1/ Stock Plan XYZ Employee B 2 RSU 27 1/ 04/01/2016 75,107 $0.0000 $0.0000 $0.00

1/ Stock Plan XYZ Employee C 3 RSU 24 1/ 04/01/2016 7,153 $0.0000 $0.0000 $0.00

1/ Stock Plan XYZ Employee D 4 RSU 25 1/ 04/01/2016 7,153 $0.0000 $0.0000 $0.00

1/ Stock Plan XYZ Employee E 5 RSU 28 1/ 04/01/2016 53,648 $0.0000 $0.0000 $0.00

1/ Stock Plan XYZ Employee F 6 RSU 30 1/ 04/01/2016 42,918 $0.0000 $0.0000 $0.00

1/ Stock Plan XYZ Employee G 7 RSU 26 1/ 04/01/2016 7,153 $0.0000 $0.0000 $0.00

Stock Plan XYZ 1/ 239626 rx $0.00

Totals For All Grant Plans: 239,626 $0.00

Report Last Executed: 07/15/2016 9:22:04 PM GMT-04:00Current User: LaddonJ_EOS4Parameters: Company 123

For Grant Date From 4/1/2016 to 4/1/2016

Client Forum – San Francisco

47

Review Package Testing-Exercises

Financial Statement Audit

› For each exercise-have the following ready:

- Instructions from Broker

- Documentation of funds received

- Confirmation from Equity System tying back to broker instructions showing date of exercise

- Tax Withholding confirmation from Payroll

- Before/After Reports from equity system showing options were vested and fully exercised in system

- Test of stock prices

- Report of all exercises for specific period

Client Forum – San Francisco

48

Review Package Testing-Cancellations

Financial Statement Audit

› For each forfeiture-have the following ready: - Cancellation report from Equity System for specific period

- Completeness Test: Compare of report to HRIS list of terms for that same period

- Forfeiture Rate Memo

Client Forum – San Francisco

49

Review Package Testing – Share Based Compensation/EPS/DTA

Financial Statement Audit

› Be ready to

- Sample calculation

- Equity system SOC1 report

- Do it early

Client Forum – San Francisco

50

Being prepared

Tax Audits

› IRS more determined than ever to recover lost revenue

› Must be prepared to provide documentation on tax reporting/withholding practices

› Common areas for audit

- Section 162M

- Mobility

- 100k Federal Tax Deposit rules

- Forms 3921/3922

- Qualifying/Disqualifying Disposition

Client Forum – San Francisco Q&As

51

Client Forum – San Francisco

52

Contact Information

Jessica Laddon, CEP

Senior Relationship Manager

Computershare

(858) 264-8580

Client Forum – San Francisco

PUT ENTITY

MANAGEMENT AT

THE CORE OF

YOUR BUSINESS

Tom Racicot Vice President, Sales & Marketing Computershare Governance Services

Client Forum – San Francisco

54

The GEMS platform automates global entity management processes enabling companies to stay compliant and minimize business risk.

Using an enterprise entity management system is fundamental to having a long-term governance solution that will evolve with your organization.

As you establish new entities, a customizable platform to help chart information and pull real-time updates will enable you to stay ahead of entity filing requirements.

Defining Entity Management

With a formalized subsidiary governance process in place, your company can establish an auditable date and reporting system to comply with key company policies.

GLOBAL COMPLIANCE MANAGEMENT ENTERPRISE MANAGEMENT

ENTITY STRUCTURE MANAGEMENT SUBSIDIARY GOVERNANCE MANAGEMENT

Understanding the four pillars of entity management

Client Forum – San Francisco Entity Management Platform Structure

55

Connect internal departments for better collaboration on compliance and governance

matters

Avoid costly penalties that can lead to greater oversight

Maintain subsidiary structures to ensure all legal entities in multiple

jurisdictions are tax-efficient

Automate corporate governance functions such as monitoring,

certifying and reporting

Stay ahead of ever-changing regulatory requirements

Centralize the input and output of corporate data and documents that inform business transactions and

filings

Create a single, consolidated global structure

Reduce the complexities and risks associated with compliance and

reporting

Entity Management

Client Forum – San Francisco

56

Entity Management Challenges

Tax Codes

Corporate Secretary Corporate

Planning

Annual Business Filings/Legal

Matters

Global Regulators

Client Forum – San Francisco

57

Global Regulators

› Developing list of regulators:

- US: Dodd Frank, Wall Street Reform, Consumer Protection Act

- EU: FSA, OECD

- Africa: King III

- Globally: Regulatory Oversight Committee (LEI)

› Regulators and governance authorities are placing an increased interest of issuer’s legal entities and subsidiaries, asking:

- Where are they?

- Why are they there?

- What do they do?

- What is the ownership structure?

- Who is running them and what changes are being implemented?

Client Forum – San Francisco

› G-20 initiative post the International Financial Stability Board review 2012

› LEIs are issued by "Local Operating Units" of the Global LEI System

› Accreditation of LEI issuers by the Global LEI Foundation (GLEIF) called Local Operating Units (LOUs), of the Global LEI System.

› The Global LEI System is collecting data on direct and ultimate parents of legal entities in the Global LEI System

58

Legal Entity Identifiers (LEI)

Source: www.leiroc.org – Jan 12,2017 report

480,000 # of entities registered

195 # of countries

with LEIs

29 # of operating

issuers

Client Forum – San Francisco Tax Codes

59

› OECD > BEPS

- Base erosion and profit shifting

- G-20 initiative

- Companies leverage their global entity structure to shift profits away from high tax countries to “tax haven” countries to avoid cost

- The aim of the measures is to realign taxation with economic substance and value creation, while preventing double taxation

- The BEPS package represents the first substantial renovation of the international tax rules in almost a century

› Transfer Pricing

- Setting the price for goods and services sold between controlled legal entities within an enterprise based upon it’s group ownership structure

Client Forum – San Francisco

60

Annual Business Filings

Entity Management

Client Forum – San Francisco

› Entity management today touches many stakeholders

› Project goals are now establishing a single source for core entity data

› Issues with duplicate data sources:

- Major sources of in Accuracies

- Creates risk

- Inefficient use of resources

› Corporate actions

› Entity rationalization trend

61

Corporate Planning

Client Forum – San Francisco Entity Rationalization

62

› Why is it important to rationalize?

- Remove legacy and inefficient tax and legal structures

- Reduce inter-company transactions

- Free up human capital

- Reduce your risk (compliance and overall risk)

- Cost savings (hard and soft costs)

› What’s the cost of an entity?

- $20,000 for basic shell entity

- $40,000 for overseas entity

- More for those with any operational history (sources – KPMG, PWC, E&Y, GEMS clients)

Client Forum – San Francisco

› Today entity management goes way beyond just the gate keeper

› Overload of company information - how do you ensure it’s all accurate?

- Data collection workflows

- Verifications & Attestations

› Increased regulatory demands

› Leveraged as proactive tools designed to ensure company secretaries and other entity

› Exposure and transparency at C-suite / Board Level

› Leveraging software combined with service delivery is vital

You Cannot go it alone! Solicit help from trusted partners

63

The New Paradigm of Entity Management

Client Forum – San Francisco How can Computershare help you?

64

Computershare

Global Entity Management

(GEMS)

Registered Agent

Services

Managed Administrative

Services

A centralized, electronic solution for companies to achieve global compliance and increase business transparency

Computershare’s registered agent services offer a full suite of compliance solutions including document retrieval and annual filing services.

Our experts manage your day-to-day entity management administration to meet your

business needs.

Client Forum – San Francisco

WHAT’S AHEAD FOR THE 2017 PROXY SEASON

Christopher Dowd Senior Managing Director Georgeson LLC

Client Forum – San Francisco AGENDA

66

› Director Elections › Shareholder Proposals › Proxy Access › ISS Policy Survey & Updates › Glass Lewis Policy Updates › Say-on-Pay › Engaging with Shareholders › Board Oversight of Strategy › Shareholder Activism › Board Composition and Refreshment › Director Term Limits & Tenure › Board Diversity › Board Self Evaluation › Corporation Governance Principles

Client Forum – San Francisco Director Elections – Push for Diversity and Tenure Reforms

67

› Average support for directors was very high in 2016

- Russell 3000: 96.1% votes cast n favor

- S&P 500: 97.4% votes cast

› Majority voting provisions have become commonplace among larger companies – activism now targeting smaller caps

› Institutional investors are increasingly concerned about board accountability, responsiveness, succession planning, diversity and skill sets and are seeking to engage directly with the board

Source: Georgeson 2016 Annual Corporate Governance Review

Client Forum – San Francisco 2016 Director Votes (U.S. Russell 3000 Companies)

ISS Recommendations “Withhold” Or “Against”

68

ISS issue

# of Directors Receiving Negative

ISS Recommendations

Average Shareholder Vote for Directors (% of votes

cast)

# of Directors Receiving

<50% of Votes Cast

Independence issues (non-independent directors on

key committees or failure to maintain a majority indep board) 374 87% 7

Compensation issues 192 80% 2

Taking unilateral action that reduces shareholder rights

(or failing to put pre-IPO restrictive provisions to a shareholder vote) 127 85% 1

Absence of a formal nominating committee 100 90% 0

Failure of risk oversight due to pledging of shares by executives 73 84% 0

Lack of responsiveness to shareholder concerns (e.g.,

failure to implement a successful shareholder proposal) 66 66% 11

Poor attendance at board and committee meetings (<75%) 65 72% 5

Client Forum – San Francisco Corporate Governance Shareholder Proposals Voted On

69

269 263 249

333

266

0

50

100

150

200

250

300

350

2012 2013 2014 2015 2016

Number of Proposals – S&P 1500

Source: Georgeson 2016 Annual Corporate Governance Review

Client Forum – San Francisco Voting Results on Selected Shareholder Proposals - 2016 Proxy Season

70

As Percent of Votes Cast

Proposal Type Results Available For Against Abstain

Board Related 125 40.46% 58.03% 1.51%

Adopt Proxy Access 63 50.00% 49.11% 0.89%

Independent Board Chairman / Separate Chair-CEO 43 29.29% 69.35% 1.36%

Majority Vote To Elect Directors 8 51.44% 47.26% 1.31%

Have Implemented A Form of Majority Voting 5 42.84% 56.57% 0.59%

Have Not Implemented A Form of Majority Voting 3 65.77% 31.73% 2.50%

Executive Compensation 54 18.29% 80.05% 1.66%

Eliminate Accelerated Vesting In Termination/Change-of-Control 16 29.48% 70.09% 0.43%

Require Equity To Be Retained 11 16.57% 81.04% 2.39%

Adopt Policy on Recouping Executive Compensation of Senior Executives 5 15.42% 84.12% 0.46%

Report on the Company's incentive compensation programs 4 6.45% 90.88% 2.67%

Add Sustainability Performance Metrics to Compensation 4 13.15% 81.78% 5.06%

Shareholder Right To Act By Written Consent 17 40.79% 58.07% 1.14%

Shareholder Right To Call Special Meeting 16 43.14% 56.22% 0.64%

Adopt a Payout Policy Giving Preference to Share Buybacks Over Dividends 15 1.66% 97.71% 0.63%

Eliminate or Reduce Supermajority Provision 13 57.49% 41.77% 0.74%

Eliminate Dual Class Stock 9 26.42% 72.37% 1.21%

Vote counting standard to exclude abstentions 6 7.21% 92.31% 0.48%

Repeal Classified Board 3 80.10% 19.58% 0.33%

Source: Georgeson 2016 Annual Corporate Governance Review

Client Forum – San Francisco Trends in Shareholder Proposals (S&P 500)

71

11 13

72

62 31.76% 39.11%

55.05% 50.32%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

0

10

20

30

40

50

60

70

80

2013 2014 2015 2016

Adopt Proxy Access

# of Companies Avg. % Support of Votes Cast

53 59 58

43

31.45%

30.63%

29.67% 29.29%

28.00%28.50%29.00%29.50%30.00%30.50%31.00%31.50%32.00%

0

10

20

30

40

50

60

70

2013 2014 2015 2016

Independent Board Chair – Separate Chair-CEO

# of Companies Avg. % Support of Votes Cast

23

13

9

3

79.54%

81.24%

76.68%

80.10%

74.00%

75.00%

76.00%

77.00%

78.00%

79.00%

80.00%

81.00%

82.00%

0

5

10

15

20

25

2013 2014 2015 2016

Repeal Classified Board

# of Companies Avg. % Support of Votes Cast

20

24

7 8

58.55% 57.41% 66.16% 51.44%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

0

5

10

15

20

25

30

2013 2014 2015 2016

Majority Vote to Elect Directors

# of Companies Avg. % Support of Votes Cast

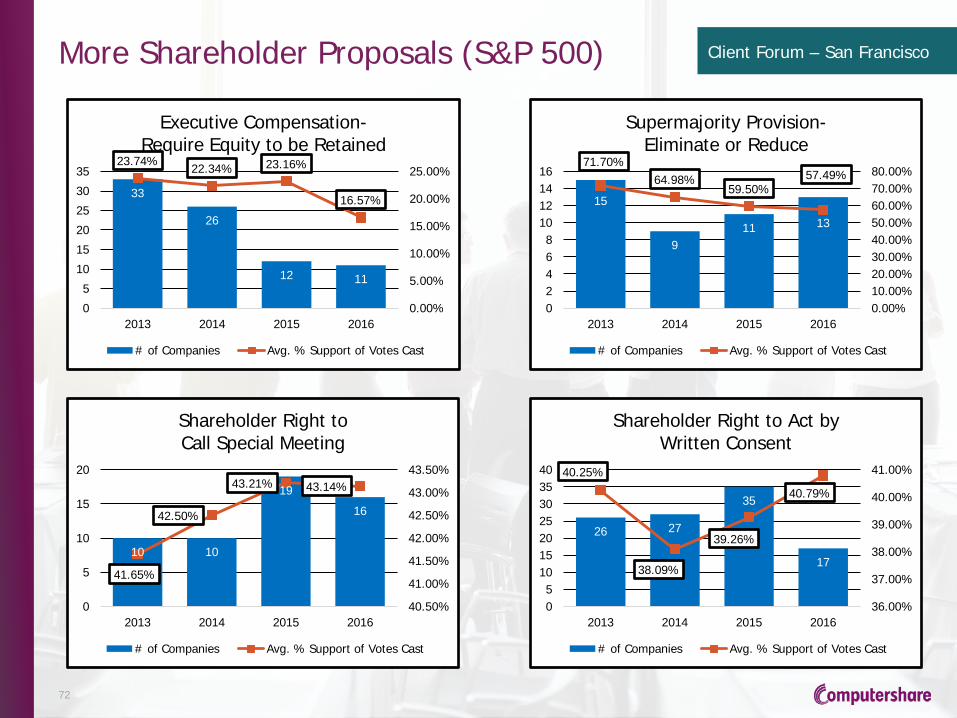

Client Forum – San Francisco More Shareholder Proposals (S&P 500)

72

33

26

12 11

23.74% 22.34% 23.16%

16.57%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

0

5

10

15

20

25

30

35

2013 2014 2015 2016

Executive Compensation- Require Equity to be Retained

# of Companies Avg. % Support of Votes Cast

15

9 11 13

71.70% 64.98%

59.50% 57.49%

0.00%10.00%20.00%30.00%40.00%50.00%60.00%70.00%80.00%

02468

10121416

2013 2014 2015 2016

Supermajority Provision- Eliminate or Reduce

# of Companies Avg. % Support of Votes Cast

10 10

19

16

41.65%

42.50%

43.21% 43.14%

40.50%

41.00%

41.50%

42.00%

42.50%

43.00%

43.50%

0

5

10

15

20

2013 2014 2015 2016

Shareholder Right to Call Special Meeting

# of Companies Avg. % Support of Votes Cast

26 27

35

17

40.25%

38.09%

39.26%

40.79%

36.00%

37.00%

38.00%

39.00%

40.00%

41.00%

05

10152025303540

2013 2014 2015 2016

Shareholder Right to Act by Written Consent

# of Companies Avg. % Support of Votes Cast

Client Forum – San Francisco Proxy Access – 2016 Recap

199 Shareholder Proxy Access Proposals

› 80 went to a vote (+1 pending)

- 38 failed, 42 passed

- 51.4% average support

› 118 did not go to vote

- Withdrawn, omitted, no-action relief granted, etc.

› 5 dueling proposals

- Passed: 3 management proposals; 2 shareholder proposals

› Data compiled for meetings held 1/1/16 through 10/18/16 (Microsoft pending with meeting date 11/30/16)

Higher Support When No Proxy Access in Place

› 79 proposals at companies without a proxy access bylaw already in place

- 53 went to a vote, 38 passed with 59.6% average support

› 120 submitted at companies with a proxy access bylaw

- 27 went to a vote (+1 pending), 4 passed with 38.2% average support

73

Client Forum – San Francisco Proxy Access – 2016 Recap Companies Continue to Adopt Proxy Access

74

› Over 280 companies have adopted proxy access to date

- ~41% of S&P 500, ~8% Russell 3000

› Vast majority of bylaws include “mainstream” terms:

- 3%/3-year ownership/20% of board/20 person nominating group

- Key proponents: NYC Comptroller and individual shareholders

› Significant support from institutional investors; ISS and GL

› Votes cast in favor and number of proposals passing declined in 2016 from 2015 (51% vs. 55% and 39 vs. 53, respectively)

Client Forum – San Francisco Proxy Access – 2016 Recap Focus on SEC No-Action Process: “Substantial Implementation”

75

› In 2016 season, 38 companies excluded proposals under Rule 14a-8(i)(10) where proxy access with mainstream terms was adopted after proposal received

- SEC continues to grant relief for initial adoption even where proposal specifies “essential” terms

› SEC Staff declined to permit exclusion of 7 “fix-it” proposals targeting specific terms of already adopted bylaws

- E.g., cap of greater of 25% or 2 vs. 20%, no holder aggregation vs. 20

› But granted relief in two instances where company partially met shareholder requests, so Staff may be taking nuanced approach

› H&R Block failed ~30% support: ISS recommended “for”; GL “against”

- MSFT also failed; other proposals are subject to future action (Apple, Disney, Whole Foods, Walgreens)

Client Forum – San Francisco Proxy Access – Preparing for the 2017 Season Evaluate Your Company’s Position

76

› Companies that have adopted proxy access may be targeted with “fix it” proposals targeting specific terms, including:

- Aggregation –remove cap/increase

- Number of board nominees – 25%, or at least 2

- Renomination threshold – eliminate

- Treatment of loaned securities – no 3 day recall limit

- Nominees’ potential conflicts of interest

› Companies that have not adopted proxy access, consider:

- Shareholder proposals may evolve to include more specific terms

- Proactive vs. potential exposure to challenge of adopted by-law

- Smaller companies may be targeted

Client Forum – San Francisco Proxy Access – Looking to the 2017 Proxy Season

Developments to Watch

77

› Continued high level of proposals, including 2017 Boardroom Accountability Project target list

› “Fix it” proposals: focus on features beyond 3% for 3 year ownership

› Monitor SEC no-action developments and evolution in investor and proxy advisory voting

- Institutional investors generally support “mainstream” proxy access

- ISS and GL voting recommendations

- Seek investor feedback in off-season shareholder engagement

› First proxy access candidate proposed at National Fuel Gas on November 10 by GAMCO, a Mario Gabelli fund

- GAMCO not typical activist, so not a true challenge to market wisdom that proxy access would not be an attractive tool for activist investors

- GAMCO withdrew nomination after Board rejected candidate on basis of its determination that GAMCO had control intent, contrary to the access bylaw

Client Forum – San Francisco ISS 2016 Policy Survey Takeaways

› Respondents included 115 institutional investors (1/3 of which >$100B under management), 270 corporate issuers and 17 consultants/advisors

› Key Takeaways:

› Both investors and issuers strongly favor using metrics other than TSR to measure pay-for-performance alignment

- In response, ISS will implement changes to the methodology underlying its pay-for-performance models for U.S. companies

› Institutional investors strongly support annual say-on-pay frequency

› Board refreshment matters to institutional investors

› Long-tenured directors, even with refreshment, continue to be a source of investor concern

› Majority of institutional investors favor recommending against directors of IPO companies debuting with multi-class capital structures

› ISS raised in policy survey but did not implement tighter overboarding restrictions on executive chairs (limited to 2 outside boards, same as CEO)

78

Client Forum – San Francisco ISS 2017 Policy Updates: Director Election-Related

On November 21, 2016, ISS published updates to its 2017 proxy voting policies and guidelines:

Overboarding

› ISS will recommend vote against or withhold from individual directors who:

- Sit on more than 5 public company boards (reduced from 6 board limit in 2016)

- Are CEOs of public companies who sit on the boards of more than 2 public companies besides their own—withhold only at their outside boards (same as 2016)

› Certain major institutional investors have more restrictive overboarding policies—e.g., BlackRock may vote against directors who serve on more than 4 public company boards

IPO’s with Unequal Voting Rights/Problematic Governance

› ISS will generally issue adverse director vote recommendations if a company IPO’s with a multi-class capital structure with unequal voting rights or other problematic governance provisions

- ISS will generally require a “reasonable” sunset provision on any shareholder-adverse provisions to avoid a negative recommendation

› Will no longer consider a company’s commitment to put such provisions to a shareholder vote within three years post-IPO

Restrictions on Shareholder Right to Amend Bylaws

› ISS will issue adverse vote recommendations on governance committee members if the company places “undue” restrictions on shareholders’ ability to amend the company’s bylaws. This should generally be limited to certain Maryland REITs

79

Client Forum – San Francisco ISS 2017 Pay-for-Performance Methodology

› On November 8, 2016, ISS updated its pay-for-performance methodology

› Test continues to be based on relative TSR but 2017 reports also will show relative financial performance based on six new financial metrics:

› Return on equity, return on assets, return on invested capital, revenue growth, EBITDA growth and cash flow (from operations) growth—each over a 3-year period

› Will not affect ISS's quantitative analysis of relative pay-for-performance for 2017, which will continue to assess CEO pay against relative three-year TSR

› But may be considered in ISS's qualitative assessment

› Neither measure will apply unless companies have at least two years of CEO pay and trading or financial data

80

Client Forum – San Francisco ISS 2017 Policy Updates: Compensation-Related

Ratification of Director Compensation

› ISS will evaluate 8 qualitative factors in evaluating non-employee director (NED) standalone ratification proposals (which are rare)

- Relative magnitude compared to similar companies, presence of problematic pay practices, stock ownership guidelines and holding requirements, equity award vesting schedules, mix of cash and equity, meaningful limits on NED compensation, availability of retirement benefits or perks, quality of disclosure around the director pay program

› ISS made corresponding changes to evaluation NED-specific stock plans, which do not appear to impact the assessment of omnibus stock plans that include limits on NED compensation

Proposals to Approve or Amend Equity-Based Plans

› Added new factor to Equity Plan Scorecard “plan features” pillar regarding payment of dividends on unvested awards—full points will be awarded only if the plan expressly prohibits the payment of dividends on unvested awards and applies the prohibition to all awards

› Modified the minimum vesting factor, which will now receive full points only if the minimum vesting period of one year applies to all award types (closing a loophole in prior policy) and cannot be eliminated or reduced in individual award agreements, except for up to 5% of shares issued under the plan

Equity Plan Proposals Only for 162(m) Approval

› Clarifies policy to state that it will recommend a vote against proposals solely for approval of performance metrics in cash or equity plans for 162(m) purposes if compensation committee is not composed exclusively of outside directors

81

Client Forum – San Francisco ISS Updated and Rebranded “QuickScore”

82

› On October 31, 2016, ISS announced that it has updated and rebranded its “corporate governance scoring solution”

› The new and rebranded QualityScore adds 15 new governance factors that were not in last year’s QuickScore 3.0

- Board structure: percentage of directors on board fewer than 6 years, percentage of women directors, mechanisms to encourage director refreshment, adequate response to low support for management proposal

- Shareholder rights: inclusion of exclusive forum, fee-shifting or limitation on shareholder litigation in charter documents, proxy access features including nominee cap and aggregation limit on shareholder nominating group

- Compensation: whether company employs at least one compensation metric that compares its performance to a benchmark or peer group

- Audit: tenure of the company’s external auditor

› The ISS data verification portal was open briefly before scores were published and is now again open until the end of the year (except it closes from the date a company files its proxy statement and the annual meeting)

› Companies that have experienced a significant adverse change to their recently published QualityScore from last year’s QuickScore rating should consider using the ISS data verification portal before filing their proxy statement to determine if any requests for corrections should be submitted to ISS

Client Forum – San Francisco Glass Lewis 2017 Policy Updates

On November 18, 2016, GL published its 2017 proxy voting guidelines, noting the following changes: Overboarding › GL will recommend vote against or withhold from individual directors who:

- Sit on more than 5 public company boards (reduced from 6 board limit in 2016) - Are CEOs of public companies who sit on the boards of more than 2 public companies besides

their own—withhold only at their outside boards (same as 2016) - But will give consideration to size and location of company and other mitigating factors

Board Evaluation and Refreshment › Clarified approach to board evaluation, succession planning and refreshment

- A robust board evaluation process focused on the assessment and alignment of director skills with company strategy is more effective than solely relying on age or tenure limits

- Governance Following an IPO or Spin-Off › GL will evaluate governance factors that “significantly restrict” the ability of shareholders to effect

change in recommending votes against members of the governance committee or directors serving when the governance provisions were adopted

- Factors include anti-takeover mechanisms, supermajority vote requirements and general shareholder rights

83

Client Forum – San Francisco Say-on-Pay: ISS Influence

84

› Voting recommendations from the proxy advisory firms, especially ISS, can greatly alter the outcome of a proxy solicitation campaign

› Shareholder support was 28% lower at companies with an ISS ‘Against’

› ISS recommended that shareholders vote ‘Against’ Say on Pay at 12% of companies in 2016 – slightly up from 2015

› While proxy advisory firms and institutional investors use a screen to identify pay for performance misalignment, qualitative review is important

0%

20%

40%

60%

80%

100%

120%

Low Concern Medium Concern High Concern

78% For

49% For

97% For

ISS Recommendations by P4P Concern Level (2012 – 2016)

Client Forum – San Francisco Say-on-Pay; Failures & Red-Zone Results

Pay and performance

relation

Problematic pay practices

Rigor of performance

goals

Shareholder outreach disclosure

Non-Performance Based Equity

Special awards/

Mega-grants

Most common

contributing factors for

failures

85

Client Forum – San Francisco Say-on-Pay: Addressing Concerns

86

Next year’s vote will depend on two criteria:

1. Responsiveness to 2016 poor Say on Pay vote

2. Pay for performance alignment for 2017 Say on Pay vote

Companies should consider the following questions:

› Which is more important: Magnitude of pay or design changes?

› Do pay changes need to be immediate or will forthcoming changes get credit?

› Do we need to address ongoing issues only or do legacy issues also need to be addressed?

› Do we only need to focus on changes to CEO pay or are other NEO pay issues significant as well?

Client Forum – San Francisco Advice on Engaging with Shareholders

› Need to proactively communicate early and often

› People who vote are often not the analysts who cover the stock

› Know your investors’ “hot buttons” and voting guidelines / history

› Be prepared to tackle difficult questions that may arise

› Have an agenda when reaching out to your investors – don’t waste their time

› Consider including board representation on calls with larger investors for certain subjects (i.e. compensation, governance or succession)

› Tie your governance story to the value creation and compensation story

Engagement with shareholders is key in building credibility and convincing shareholders the current path is best

87

Client Forum – San Francisco Engaging with Corporate Governance Contacts is Critically Important

› Many institutional investors have developed teams of governance analysts who are primarily responsible for proxy voting

- Passive / Index funds – governance contacts are outcome determinative

- Active funds – governance contacts can be highly influential

› Do your research about which funds rely more on governance than investment

› Proxy Advisory firm recommendations (ISS and Glass Lewis) are not blindly followed by most institutional investors

- Background research is critical for investors who also prefer the standardization of material in the reports vs proxy statement review

- Used by investors as screens to highlight which companies they should review qualitatively

Governance contacts are critical for securing favorable vote outcomes.

88

Client Forum – San Francisco Board Oversight of Strategy

Investor governance teams are increasingly focused on the board’s oversight of long-term strategy and how governance and executive compensation practices align with that strategy

› Recent public statements by influential investors including BlackRock, State Street Global Advisors and Vanguard support long-term investment and creation of sustainable value.

› Companies should expect more substantive engagement discussions with shareholders regarding the company’s long-term strategy.

› Consider expanding disclosure with respect to strategy and be prepared to engage with investor’s governance teams on specific issues, including:

- Business and segment strategic plan, including key performance metrics and investment/return criteria;

- Implications for management compensation;

- Summary of board oversight; and

- Relationship to board composition/refreshment.

89

Client Forum – San Francisco Board Composition and Refreshment

› Investors are focused on board composition and refreshment practices, including:

› Whether the board has the skills, experience and qualifications necessary to support company strategy;

› The board’s approach to succession planning and refreshment;

› Process for board/director/committee evaluations; and

› Board’s role in risk oversight, including at the committee level (e.g., sustainability risks, cybersecurity).

› Companies should evaluate their board composition, anticipate investor concerns and consider improving disclosure on board composition and refreshment.

› Investors and proxy advisory firms will frequently support board refreshment in light of other perceived corporate governance weaknesses, such as board leadership issues or a failure to respond to investors.

:

90

Client Forum – San Francisco Director Term Limits and Tenure

91

Director Term and Age Limits Not Widely Embraced at S&P 500 Companies

Despite increasing focus on board tenure and refreshment, institutional investors and proxy advisors are still generally against director term and age limits

› Only 3% of companies include term limits in the corporate governance guidelines

› Director Retirement Age

- ~50% of S&P 500 set retirement age at 72 years; relatively consistent

- ~25% of S&P 500 set retirement age at 75+ years, up from 5% in 2005

Board Tenure at S&P 500 Companies

While the average age of independent directors has risen to ~ 63 years of age, most boards have relatively low average tenures (between 6 and 10 years)*

17%

62%

17%

4%

5 years or less 6 - 10 years 11 - 15 years More than 15 years

* Source – Spencer Stuart 2016 Board Index

Client Forum – San Francisco Director Tenure

› Investors are increasingly focused on tenure as a key proxy for director independence and board skills/diversity refreshment.

› Selected policies include:

CalPERS Recently amended its governance principles to target directors with tenures >12 years; ask companies to classify such directors as non-independent or provide a detailed explanation

SSGA Discourages long-tenured directors (13+ years) serving on key committees; greater engagement at companies with average board tenure >13 years and where more than 1/3 of non-management directors have tenures of 16+ years

BlackRock Will engage on director tenure where problematic and may vote against directors based on (1) poor board diversity; (2) evidence of “board entrenchment”; and/or (3) failure to “promote adequate board succession planning over time in line with the company’s stated strategic direction”

ISS Will scrutinize board where average director tenure exceeds 15 years for independence from management and sufficient board turnover/refreshment. ISS 2017 Policy Survey results – 68% of respondents indicated a high proportion of long-tenured directors is cause for concern. Added new QualityScore factors on what proportion of directors on board fewer than 6 years and whether board has any mechanisms to encourage refreshment

92

Client Forum – San Francisco Board Diversity

› Investors and others continue to advocate for greater diversity on corporate boards, especially with respect to gender

› Investor initiatives on diversity includes:

- The Thirty Percent Coalition

- Shareholder proposals requesting better diversity disclosure (e.g., New York Common Retirement Fund)

- Vote “no” campaigns (e.g., CtW Investment Group targeting Chipotle, Discovery Communications and Netflix)

› Companies should consider enhancing proxy disclosure regarding directors’ gender, race and ethnicity. Many companies continue to focus on diversity of viewpoints, experience, education, skill or other qualities or attributes

93

Client Forum – San Francisco Proxy Disclosure of Board Self Evaluation

› Primer: Why disclose in the proxy statement?

- Everyone else is doing it: all but 2% of S&P 500 companies according to the 2015 Spencer Stuart Index. According to the report, investors increasingly want to know more about a company’s board evaluation

- Investors are looking for it: Council of Institutional Investors issued a report entitled Best Disclosure: Board Evaluation, which focused on process of board self-evaluation with recommendations for enhanced disclosure including a detailed description of process and/or a description of takeaways from the most recent evaluation, along with samples of disclosures CII favors

- ISS cares: ISS includes disclosure of board self-evaluation as a factor in evaluating companies’ governance practices in its QualityScore rating system

94

Client Forum – San Francisco Proxy Disclosure of Board Self Evaluation

› A recent review of approximately 25 examples of 2016 proxy statements from Fortune 500 companies shows that, while all addressed self-evaluation, roughly half provided only minimal detail, and the other half provided a range of more detail

› Of particular interest, certain companies utilized the proxy disclosure concerning board self-evaluation to directly address corporate practices that some investors view as problematic, such as having a combined chair/CEO position

› A few reference using a third party to assist with the valuation

› A recommended practice is to vary board self-evaluation practices from year to year in order to keep the process fresh and elicit new insights

› Most of the companies reviewed also listed board and committee self-evaluation in their checklist of corporate governance practices

95

Client Forum – San Francisco Focus on Governance Principles

The publication of corporate governance principles and “best practices” continues to proliferate and is contributing to more public discourse

› Commonsense Corporate Governance Principles (July 2016)

- Developed by a group of 13 public company executives and institutional investors for public companies, their boards of directors and their shareholders

› BRT Principles of Corporate Governance (August 2016)

› NACD – Report of the NACD Blue Ribbon Commission on Building the Strategic-Asset Board (September 2016)

› CII Corporate Governance Policies (updated September 2016)

96

Client Forum – San Francisco Number of Activist Campaigns Remains High

97

353

230 219

242 262

274

347 357

251

0

50

100

150

200

250

300

350

400

2008 2009 2010 2011 2012 2013 2014 2015 2016 (YTD)

US Activism Campaign Announcements

Source: SharkRepellent.net as of October 21, 2016

Client Forum – San Francisco Activism Abounds in Companies of All Sizes

98

98 123 118 139 200 185 124

81 135

108 141

253 236

190

130 130

181

252

355 384

267

61 70 104

144

163 173

189

34 52 51 115 129 166

209

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016

LARGE (>$10b)

MID ($2b - $10b)

SMALL ($250m - $2b)

MICRO ($50m - $250m)

NANO (<$50m)

Source: Activist Insight as of October 17, 2016

Client Forum – San Francisco First Time / Occasional Activists Exceedingly Common

99

› Since January 2014, approximately half of all activist campaigns were led by first time or occasional activists.

Source: SharkRepellent.net as of September 19, 2016

First Time Activist (136 – 31.9%)

Activist with total # of campaigns

between 2 and 5 (78 – 18.3%)

Activist with total # of campaigns >5 (212 – 49.8%)

Client Forum – San Francisco

CLOSING REMARKS

Sheila Frierson, President, U.S. Plan Managers Andrew Moore, President, Computershare Governance Services