safe harbor statement -...

TRANSCRIPT

0

1

Safe Harbor Statement

Except for historical information contained herein, this presentation contains “forward-looking statements.” All statements other than statements of historical fact are “forward-looking statements” for purposes of federal and state securities laws, including any projections of earnings, revenue or other financial items; any statements of the plans, strategies and objectives of management for future operations; any statements concerning proposed new services or developments; any statements regarding future economic conditions or performance; any statements of belief; and any statements of assumptions underlying any of the foregoing. Forward-looking statements may include the words, “may,” “will,” “estimate,” “intend,” “continue,” “believe,” “expect,” or “anticipate” and any other similar words.

Although we believe that the expectations reflected in any of our forward-looking statements are reasonable, actual results could differ materially from those projected or assumed in any of our forward-looking statements. Our future financial condition and results of operations, as well as any forward-looking statements, are subject to change and to inherent risks and uncertainties, such as those disclosed or incorporated by reference in our filings with the Securities and Exchange Commission. Important factors that could cause our actual results, performance and achievements, or industry results to differ materially from estimates or projections contained in our forward-looking statements include, among others, the following:

our relationship with, and our ability to influence the actions of, our distributors;adverse publicity associated with our products or network marketing organization;uncertainties relating to interpretation and enforcement of recently enacted legislation in China governing direct selling;risk of our inability to obtain the necessary licenses to expand our direct selling business in China;adverse changes in the Chinese economy, Chinese legal system or Chinese governmental policies;risk of improper action by our employees or international distributors in violation of applicable law;changing consumer preferences and demands;loss or departure of any member of our senior management team which could negatively impact our distributor relations and operating results;the competitive nature of our business;regulatory matters governing our products, including potential governmental or regulatory actions concerning the safety or efficacy of our products, and

network marketing program, including the direct selling market in which we operate;risks associated with operating internationally, including foreign exchange risks;our dependence on increased penetration of existing markets;contractual limitations on our ability to expand our business;our reliance on our information technology infrastructure and outside manufacturers;the sufficiency of trademarks and other intellectual property rights;product concentration;our reliance on our management team;uncertainties relating to the application of transfer pricing, duties and similar tax regulations;taxation relating to our distributors,product liability claims; andthere can be no assurance that we will purchase any of our shares in the open market or otherwise.

Additional factors that could cause actual results to differ materially from our forward-looking statements are set forth in this presentation. We do not intend, and undertake no obligation, to update any forward-looking statement.

2

Michael O. JohnsonChairman and Chief Executive Officer

3

Investment Highlights

• Successful track record, driven by positive global mega trends

• Unique distribution channel for emerging markets and consultative products

• Geographic diversification throughout 65 markets and across four major product categories

• Financial strength – Strong cash flow– Margin expansion– Strong balance sheet– Economically resilient

• High degree of shareholder focus– Disciplined capital allocation– Free cash flow allocated to high ROI programs

• Share repurchase program - +$200MM completed since April 2007

• Proven management team

Industry Perspectives

5

1886

Industry History(2006 Net Sales of Selected Companies)

2000199019801970196019501940

$8.8B $6.3B

$2.3B

$1.1B

$0.4B

$1.7B

$1.2B

$1.3B

$0.4B

$1.9B

$1.1B*

Source: CapitalIQ, Company Reports; as of 9/20/2007*Only 2005 sales available

6

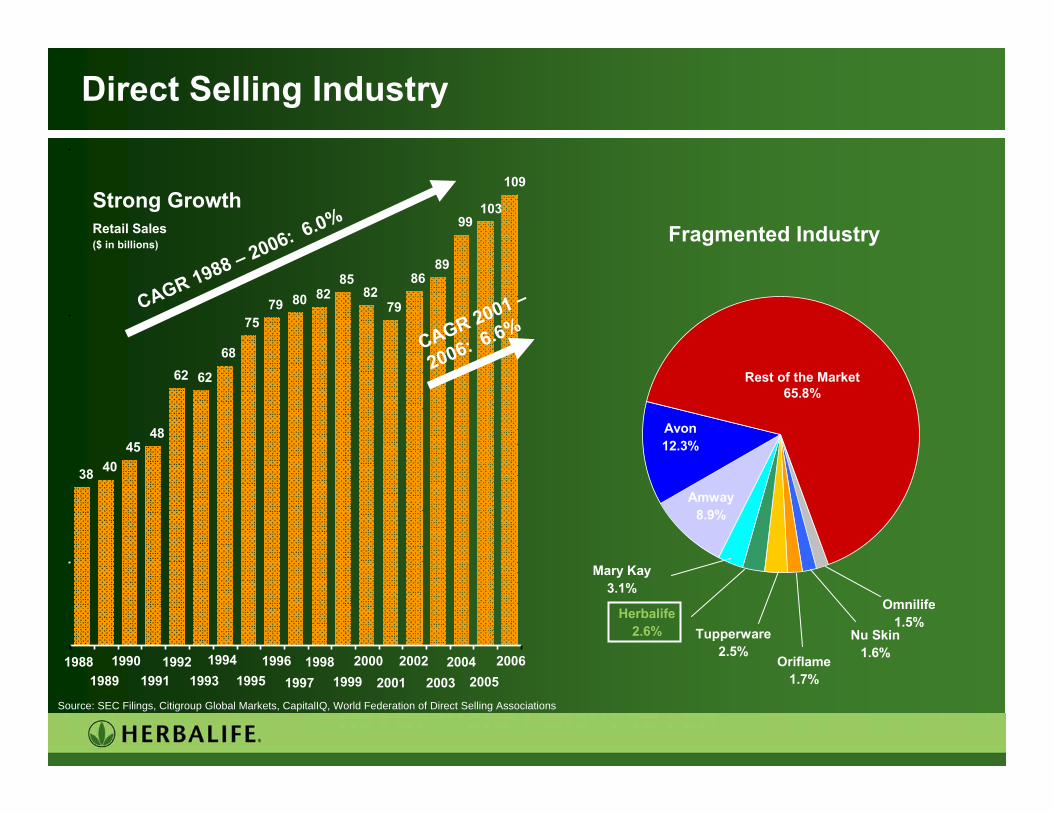

Direct Selling Industry

Fragmented Industry

Source: SEC Filings, Citigroup Global Markets, CapitalIQ, World Federation of Direct Selling Associations

Rest of the Market65.8%

Nu Skin1.6%Oriflame

1.7%

Tupperware2.5%

Mary Kay3.1%

Amway8.9%

Avon12.3%

Herbalife2.6%

Omnilife1.5%

4045

48

62 62

68

7579 80 82

8582

79

8689

99103

109

38

19881989

19901991

19921993

19941995

19961997

19981999

20002001

20022003

20042005

2006

CAGR 2001 –

2006: 6.6%CAGR 1988 – 2006: 6.0%

Strong GrowthRetail Sales($ in billions)

7

“Traditional” companies entering direct selling

BERKSHIRE HATHAWAY INC. Purchased

Source: Company Reports

Start up

Start up

Purchased

Start up

Start up

Start up

Start up

ConsideringIndia

Direct Selling DivisionParent Company

Brazil

Herbalife – Past, Present and Future

9

Herbalife History

2003: A company that had lost confidenceEmployeesDistributors

Restored confidence to HerbalifeManagement teamStrategyTop line revenueDistributor momentumStrategies to strengthen retailing, retention and recruitingExpanded geographic reachSharing of best practices

10

Herbalife Performance ($ in millions)

It took Herbalife - 16 years to reach $1B Retail Sales- 8 years to reach $2B Retail Sales- 2 years to reach $3B Retail Sales

Note: Normalized for non-recurring expenses *2007E based on sell-side analysts consensus for 2007 as published November 2007.

1999 - 2003 2003 - 2007E

CAGR CAGR1999 2003 '99-'03 2003 2007E* '03-'07E

Retail Sales 1,794 1,894 1% 1,894 3,300 15%

Net Sales 1,099 1,159 1% 1,159 2,106 16%

Operating Income 93 107 4% 107 314 31%% Margin 8% 10% 10% 15%

Net Income 57 43 -7% 43 190 45%

Confidence in our company

12

Confidence

Confidence in our Product

Confidence in our Business Opportunity

Confidence in our Brand

Confidence in our Image

13

Confidence in our Product

Herbalife Categories

Global Market Size

Growth Forecast

Source: Euromonitor 2006; Growth CAGR 2005 – 2010 * Includes Energy Drinks only; does not include bars

$33 B

$38 B

+ 7%

+ 7%

$12 B * + 52%

$157 B + 4%

$109 B + 7%

% Herbalife Net Sales

63%

20%

5%

6%

14

Chasing the mega-trends of obesity and anti-aging

15

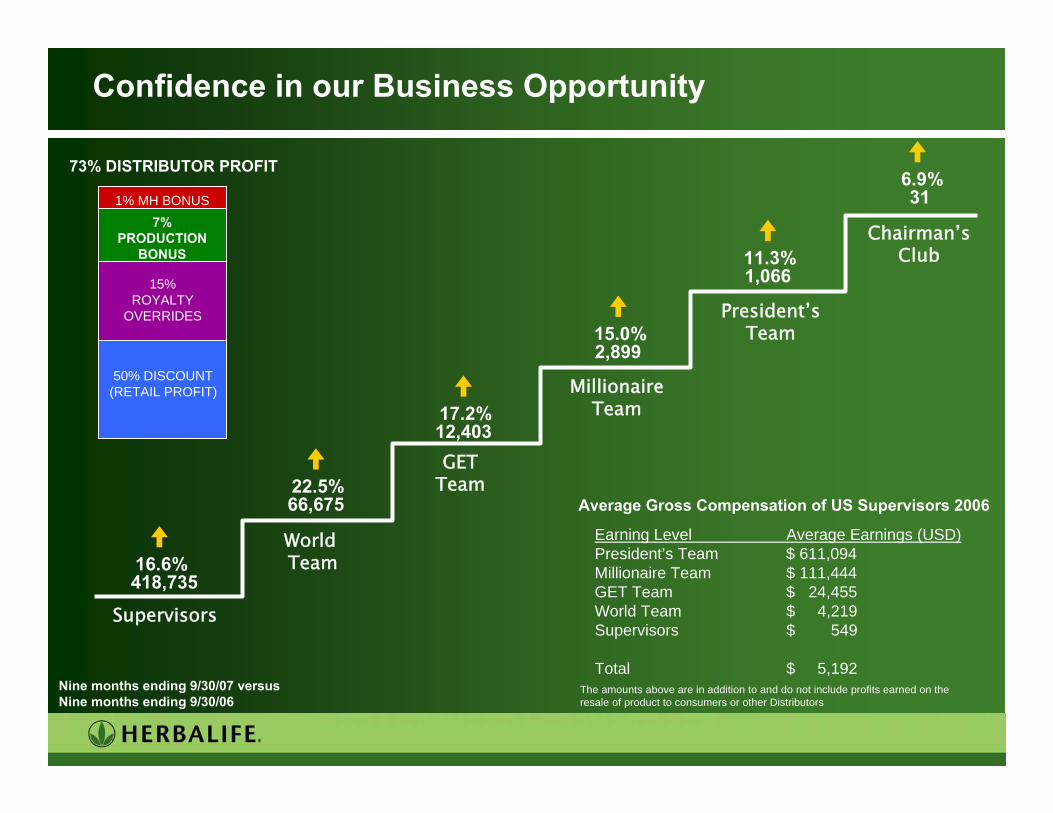

Supervisors

World Team

GETTeam

MillionaireTeam

President’sTeam

Chairman’s Club

Confidence in our Business Opportunity

6.9%31

11.3%1,066

15.0%2,899

17.2%12,403

22.5%66,675

16.6%418,735

Nine months ending 9/30/07 versusNine months ending 9/30/06

73% DISTRIBUTOR PROFIT

1% MH BONUS7%

PRODUCTION BONUS

15% ROYALTY

OVERRIDES

50% DISCOUNT(RETAIL PROFIT)

Earning Level Average Earnings (USD)President’s Team $ 611,094Millionaire Team $ 111,444GET Team $ 24,455World Team $ 4,219Supervisors $ 549

Total $ 5,192

Average Gross Compensation of US Supervisors 2006

The amounts above are in addition to and do not include profits earned on the resale of product to consumers or other Distributors

16

Confidence in our Brand

Distributor Activation

17

Confidence in our Image

Integrity“We do the right, honest and ethical thing. We take the high road.”

Oversight & Enforcement:Invested in staff to strengthen internal controls, policies and procedures

Distributor “whistle blower hotline”Distributor Rules – important safeguardsWorld-wide Ethical Business PracticesWorld-wide internal audit staffHerbalife Audit CommitteeSOX compliantSEC, NYSE, FDA, FTC

18

Dr. Steve HenigChief Scientific Officer

Product

20

Product Aspiration

Vision

• To be the premier nutrition company in the world.

• Lifetime commitment of our distributors and their customers – “Herbalife for Life!”

Mission

• To provide balanced nutrition, personalized for a healthy, active lifestyle.

Resources

• Process

• Science Program

• Equipment

• Talent

21

Obesity Rates Predicted to Double in 30 Years

5%

10%

15%

20%

25%

30%

35%

40%

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

USA

United Kingdom

Germany

Austria

Belgium

Russia

Portugal

Denmark

Netherlands

Sweden

Spain

BMI >30 as a % totalSource: International Obesity Task Force

22

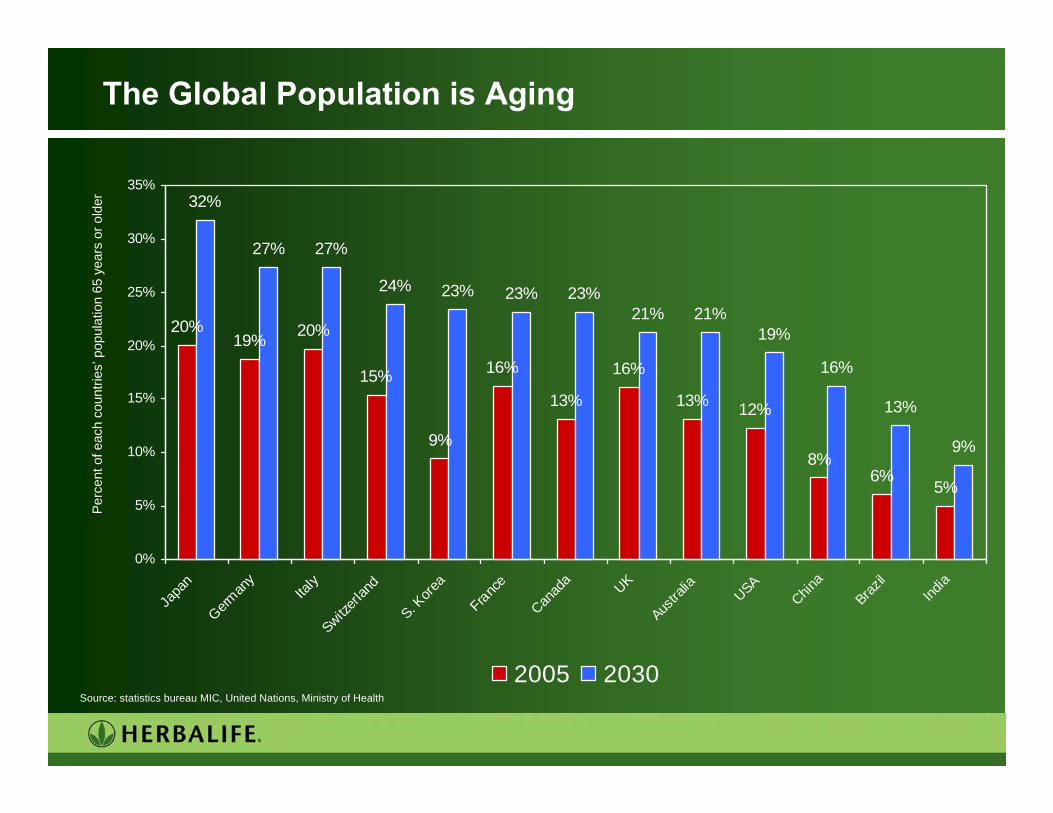

The Global Population is Aging

20%19% 20%

15%

9%

16%

13%

16%

13% 12%

8%6%

5%

32%

27% 27%

24% 23% 23% 23%21% 21%

19%

16%

13%

9%

0%

5%

10%

15%

20%

25%

30%

35%

Japa

n

German

y

Italy

Switzerl

and

S. Kore

a

France

Canad

a UK

Austra

lia

USA

China

Brazil

India

2005 2030

Perc

ent o

f eac

h co

untri

es’p

opul

atio

n 65

yea

rs o

r old

er

Source: statistics bureau MIC, United Nations, Ministry of Health

23

Science behind our products

Targeted Nutrition:

Kid’s Line

Heart Health

Digestive Health

Weight Management:

Core Products:

Formula 1 Shake

Formula 2 Multivitamin

Cell Activator

Energy & Fitness:

Liftoff

H³O

Outer Nutrition:

Skin Activator Line

Nourifusion Line

Science Program

25

Science Program

• Herbalife Product and Science Center

• Botanical Evaluation• Botanical Monograph Program

• Claim Substantiation• Developed scientific reviews in global

format

• Mark Hughes Cellular & Molecular Nutrition Laboratory- UCLA

• University of Mississippi

Herbalife Product and Science Center

University of Mississippi UCLA

The University of California as a matter of policy does not endorse specific products or services

26

Clinical Studies Program

• Niteworks at UCLA – completed

• Meal Replacement at UCLA – completed, submitted for publication

• Meal Replacement, Germany – completed, submitted for publication

• Meal Replacement, Korea – to be completed at the end of 2007

• Other proposed studies in preparation for clinical evaluation• Targeted Nutrition• Weight Management

Quality and Regulatory

28

Corporate Quality

• Upgraded quality systems, policies and procedures

• Improved product testing plan

• Supplier “Quality Success Rating” program

• Global Quality Control lab in Los Angeles

• A new database for specifications

29

Global Licensing

• Global Licensing is structured to build strong relationships with regulatory agencies across 65 countries

• Diverse skill sets

• Leveraging technology (Agile)

Nutrition Advisory Board

31

Nutrition Advisory Board

• Role of the Nutrition Advisory Board

• Strict requirements for membership

• The current NAB representation across many countries

32

Nutrition Advisory Board

33

Nutrition Advisory Board

34

Science behind Herbalife Products

Enhance blood flow to the heart*

Keep blood vessels toned, flexible and youthful for improved circulation*

Support healthy blood pressure levels already within a normal range*

* These statements have not been evaluated by the Food and Drug Administration. This product is not intended to diagnose, treat, cure or prevent any disease.

35

Science behind Herbalife Products

Support circulation and healthy blood vessels*

Maintain healthy homocysteine levels already within normal range*

Antioxidant protection

* These statements have not been evaluated by the Food and Drug Administration. This product is not intended to diagnose, treat, cure or prevent any disease.

36

Training Distributors

Product Training DVDs

37

Greg ProbertPresident and Chief Operating Officer

38

Major Market Strategy– China - expand Direct Selling license approval into additional cities & provinces– Develop Eastern European Strategy– Nurture Brazil DMO Transition– Identify untapped markets

Product Strategy– Product categories: obesity, anti-aging, fitness, children’s, immunity/defense– Accelerate local/regional product development to capitalize on target trends– Enhance science based focus: NAB, patents, clinical studies– Enhance existing product lines to better support distributor DMOs

Distributor Strategy– Targeted market segmentation: Latino, Stay-at-home moms, Fitness enthusiasts– Improve distributor productivity and utilize company infrastructure (BizWorks,

MyHerbalife.com)– Globalize distributor DMOs: Nutrition Clubs, Total Plan, Wellness Coach– Grow top line by increasing Retailing, Retention, and Recruiting (3R’s)

Infrastructure Strategy– Seven strategic business units/Realignment for Growth initiative– Distribution focus: technology and infrastructure to support sales growth (BizWorks,

MyHerbalife.com, Oracle 11i/Internet, Agile)– SOX compliance– Ethics Hotline, Adverse Events Hotline, Worldwide EBP

Focus on the Future –Key Strategic Initiatives

Regional Updates

40

North America – Region Update

Dist ribut or Order St rat if icat ion

20.0%21.0%59.0%

0.0%

20.0%

40.0%

60.0%

80.0%

discountcustomers

small retailers potent ialsupervisor

Supervisor Retention

43.1%41.7%39.2%37.5%

33.0%

36.0%

39.0%

42.0%

45.0%

Feb 04Actual

Feb 05Actual

Feb 06Actual

Feb 07Actual

Volume Points3 Year Growth Trend

13.4% 17.1% 24.6%

-

150,000300,000

450,000

600,000

2005 2006 2007 (YTD Sept)

New Supervisors3 Year Growth Trend

18.3% 21.2% 20.1%

-

10,000

20,000

30,000

40,000

2005 2006 2007 (YTD Sept)

41

North America – 2008 Initiatives

PromotionLatino Market Leadership EventsCollege Market Initiative

ProductLiftoff – new forms and flavorsDigestive HealthFlavored Aloe Powder

BrandGalaxy Jersey Sponsorship

Geographical ExpansionAddition of Quick Service Centers in key markets

42

Mexico & Central America – Region Update

Dist ribut or Order St rat if icat ion

50.0%38.5%11.5%

0 . 0 %

10 . 0 %

2 0 . 0 %

3 0 . 0 %

4 0 . 0 %

5 0 . 0 %

6 0 . 0 %

di scount customer s smal l r etai l er s potent i al super vi sor

Supervisor Retention

55.1%57.5%

51.0%51.0%

44.0%

48.0%

52.0%

56.0%

60.0%

Feb 04 Actual Feb 05 Actual Feb 06 Actual Feb 07 Actual

Volume Points3 Year Growth Trend

-1.8%69.5%

99.9%

-

200,000

400,000

600,000

800,000

2005 Actual 2006 Actual 2007 Actual (YTD Sept)

New Supervisors3 Year Growth Trend

-22.0% 72.9%

116.0%-

15,000

30,000

45,000

60,000

2005 2006 2007 (YTD Sept)

43

Promotion – focused on opening new clubsMexico: Achieve 10 penetration pointsAll qualification to events based on incremental volume plus recruiting

ProductKickoff – Mexico version of LiftoffSingle serve Formula 1

H³O and Kid’s Shake

BrandHoy TVSoccer stadium sampling

Geographical ExpansionOngoing business practice oversightOptimize expanded infrastructureOracle – new country rollout

Mexico and Central America – 2008 Initiatives

44

Brazil – Region Update

Distributor Order Stratification

9.2%

36.4%

54.4%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

discount customers small retailers potential supervisor

Volume Points3 Year Growth Trend

-12.0%7.7%30.3%

-

50,000

100,000

150,000

200,000

2005 2006 2007 (YTD Sept)

Supervisor Retention

28.8%29.0%31.2%30.3%

26.0%

28.0%

30.0%

32.0%

34.0%

Feb 04Actual

Feb 05Actual

Feb 06Actual

Feb 07Actual

New Supervisors3 Year Growth Trend

14.5% 12.8% -24.3%

-

6,000

12,000

18,000

24,000

2005 2006 2007 (YTD Sept)

45

Brazil – 2008 Initiatives

PromotionContinued transition to more balanced mix of 3Rs

ProductActive FiberLocally developed products

Soft Green line extensionsFormula 1 and soup flavor extensions

PricingPrice decreases October 2007

Geographical ExpansionOptimize mix of centers and locations

46

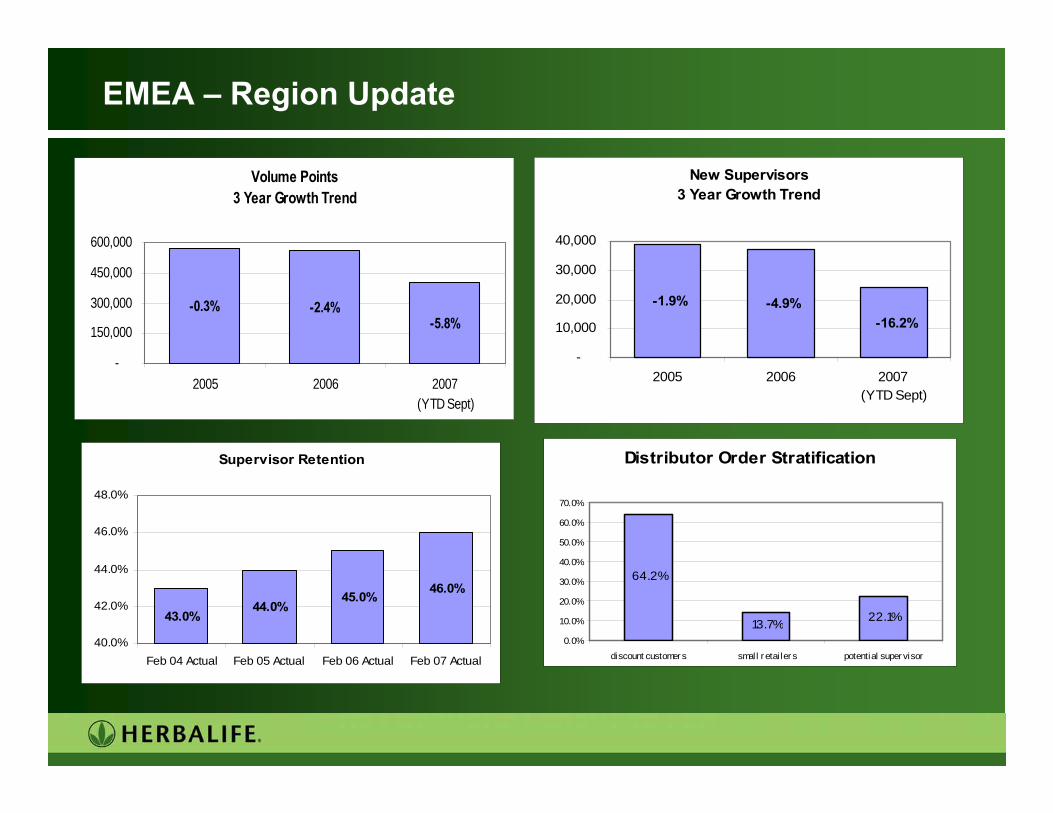

EMEA – Region Update

Distributor Order Stratification

64.2%

13.7% 22.1%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

discount customer s small r etai ler s potential super visor

Supervisor Retention

43.0%44.0%

45.0% 46.0%

40.0%

42.0%

44.0%

46.0%

48.0%

Feb 04 Actual Feb 05 Actual Feb 06 Actual Feb 07 Actual

New Supervisors3 Year Growth Trend

-16.2% -4.9% -1.9%

-

10,000

20,000

30,000

40,000

2005 2006 2007 (YTD Sept)

Volume Points3 Year Growth Trend

-5.8%-2.4%-0.3%

-

150,000

300,000

450,000

600,000

2005 2006 2007 (YTD Sept)

47

EMEA – 2008 Initiatives

PromotionGrowth in Eastern EuropeRevise IBP configuration and price

ProductIsotonic Drink (H³O)Sample Packs

PricingPrice increases across several countries

Geographical ExpansionCountry model changes

48

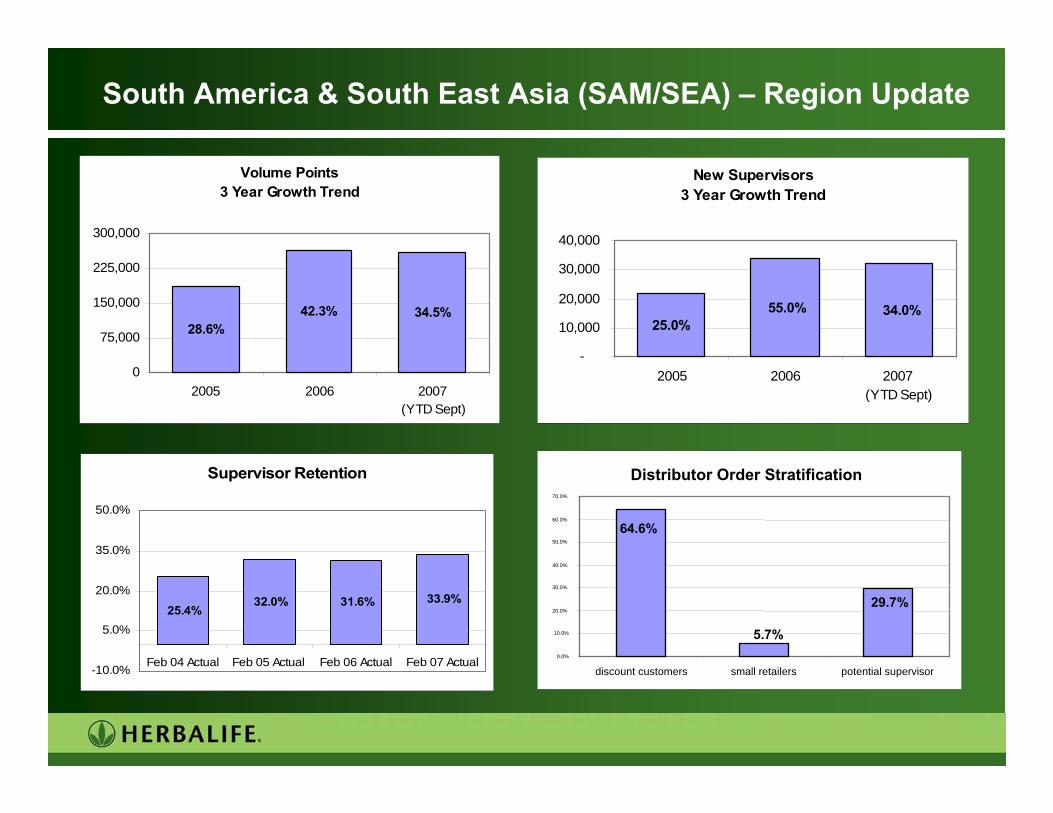

South America & South East Asia (SAM/SEA) – Region Update

Distributor Order Stratification

5.7%

29.7%

64.6%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

discount customers small retailers potential supervisor

Supervisor Retention

33.9%31.6%32.0%25.4%

-10.0%

5.0%

20.0%

35.0%

50.0%

Feb 04 Actual Feb 05 Actual Feb 06 Actual Feb 07 Actual

Volume Points3 Year Growth Trend

28.6%42.3% 34.5%

0

75,000

150,000

225,000

300,000

2005 2006 2007 (YTD Sept)

New Supervisors3 Year Growth Trend

34.0% 55.0%25.0%

-

10,000

20,000

30,000

40,000

2005 2006 2007 (YTD Sept)

49

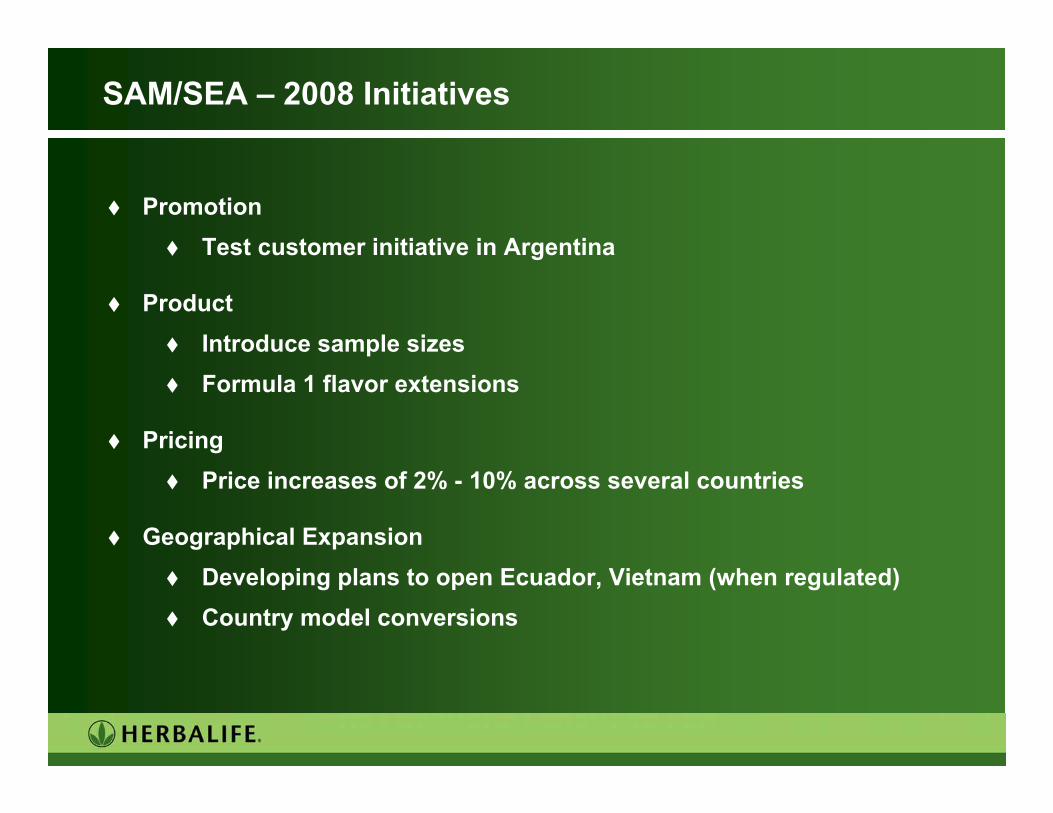

PromotionTest customer initiative in Argentina

ProductIntroduce sample sizesFormula 1 flavor extensions

PricingPrice increases of 2% - 10% across several countries

Geographical ExpansionDeveloping plans to open Ecuador, Vietnam (when regulated)Country model conversions

SAM/SEA – 2008 Initiatives

50

North Asia – Region Update

Dist ribut or Order St rat if icat ion

82.7%

2.3%15.0%0 . 0 %

2 0 . 0 %

4 0 . 0 %

6 0 . 0 %

8 0 . 0 %

10 0 . 0 %

discoun t cust omers small r et ailer s pot en t ial super visor

Supervisor Retention

28.2% 38.9% 48.6% 43.0%

0.0%

15.0%

30.0%

45.0%

60.0%

Feb 04Actual

Feb 05Actual

Feb 06Actual

Feb 07Actual

Volume Points3 Year Growth Trend

6.8% -4.9% 4.4%

-40,00080,000

120,000160,000

2005 2006 2007 (YTD Sept)

New Supervisors3 Year Growth Trend

21.1% 3.1% 2.6%-

4,0008,000

12,00016,000

2005 2006 2007 (YTD Sept)

51

North Asia – 2008 Initiatives

PromotionSupervisor Leadership Development in JapanFacilitate Nutrition Clubs in the region

ProductTri-Shield Fiber ComplexLarge size of Japan drinks

BrandTORAY Pan Pacific Open Tennis Tournament

Geographical ExpansionUpdate Korea offices

52

Greater China – Regional Update

Volume Points3 Year Growth Trend

15.9% 7.4% 46.3%

-

50,000

100,000

150,000

200,000

2005 2006 2007 (YTD Sept)

New Supervisors3 Year Growth Trend

82.2% 20.6% 20.2%

-

6,000

12,000

18,000

24,000

2005 2006 2007 (YTD Sept)

53

Greater China – Regional Update

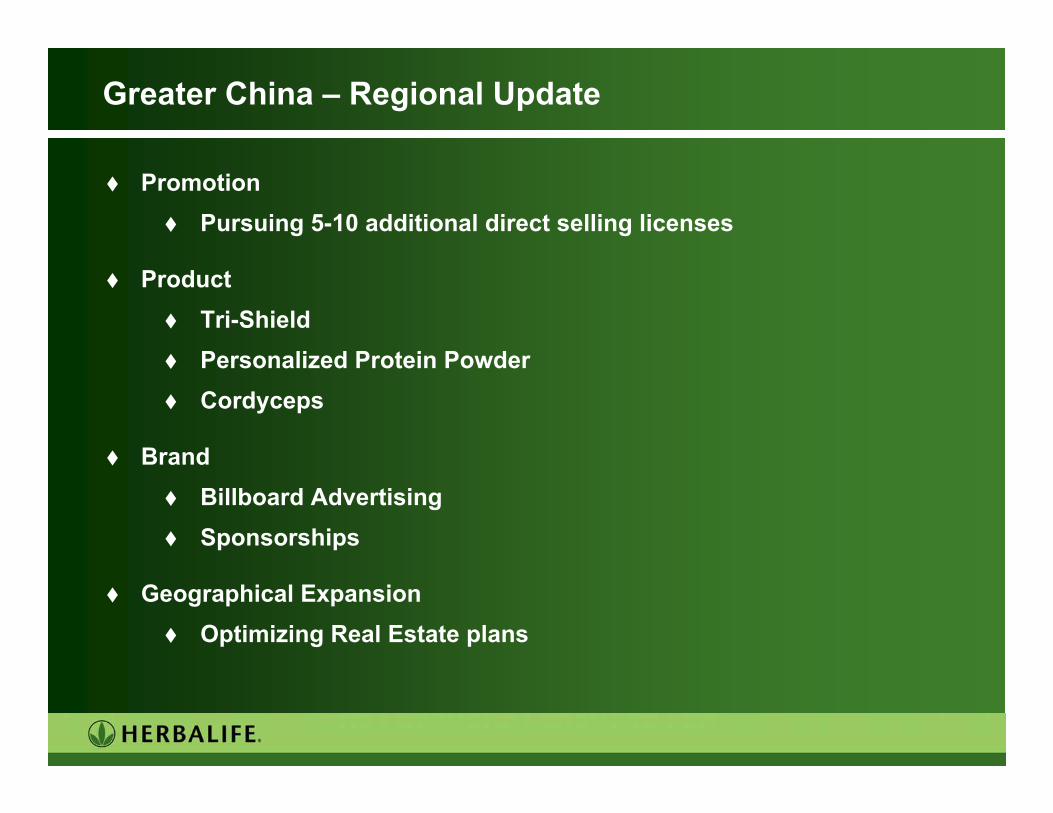

PromotionPursuing 5-10 additional direct selling licenses

ProductTri-ShieldPersonalized Protein PowderCordyceps

BrandBillboard AdvertisingSponsorships

Geographical ExpansionOptimizing Real Estate plans

54

Richard GoudisChief Financial Officer

Financial Statements

56

A Track Record of Growth

$783$867

$956 $944$1,020

$1,094$1,159

$1,309

$1,567

$1,885

$200

$450

$700

$950

$1,200

$1,450

$1,700

$1,950

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007E

$56

$74

$119 $121

$134

$164

$25

$50

$75

$100

$125

$150

$175

2002 2003 2004 2005 2006 2007 YTD

Net Sales $ MM (Y-O-Y growth)

Free Cash Flow ($ MM)

Based on management’s guidance presented in a press release dated 11/6/07. Excludes certain one-time items. Refer to company’s press release dated 11/6/07. Estimates reflect sell-side analysts consensus for 4Q07 as published November 2007.

$2,054 – $2,092

+24%+11% +10% (1%)

+8%+7% +6%

+13%

+19%

+21%9-11%

New Management Team

New Management Team

57

1Q 2006 2Q 2006 3Q 2006 4Q 2006 1Q 2007 2Q 2007 3Q 2007 4Q 2007E

Financial Results

Note: Excludes certain one-time items. Refer to company’s press release dated 11/6/07. Estimates reflect sell-side analysts consensus for 4Q07 as published November 2007.

Operating Income (% of Net Sales)

14.1% 14.0% 13.5%14.5% 14.3%

14.7% 14.8%

15.5% -16.0%

(000s)

$456 $466$487

$508$530 $530

$01Q 2006 2Q 2006 3Q 2006 4Q 2006 1Q 2007 2Q 2007 3Q 2007 4Q

2007E

+22.5% +21.1% +18.8% +19.2%+11.5%

+13.8% +11.1% +9-11%

$531 -$541

$476

Net Sales (% Growth Y-O-Y)

58

Our Financial Model(Based upon September 2007 Y-T-D Results)

Handling & Freight $215m

DISTRIBUTOR ALLOWANCES

$1223m

NET SALES $1556m

21% PRODUCT

COST

36% ROYALTIES

16% DISTRIBUTOR

FACING

12% OVERHEAD

5% TAX1% INTEREST

9% Net Income

73% VARIABLE EXPENSES

18% OVERHEAD EXPENSES

$3.4B RETAIL SALES (Annualized)

Note: Above figures normalized for China distributor royalty payments

59

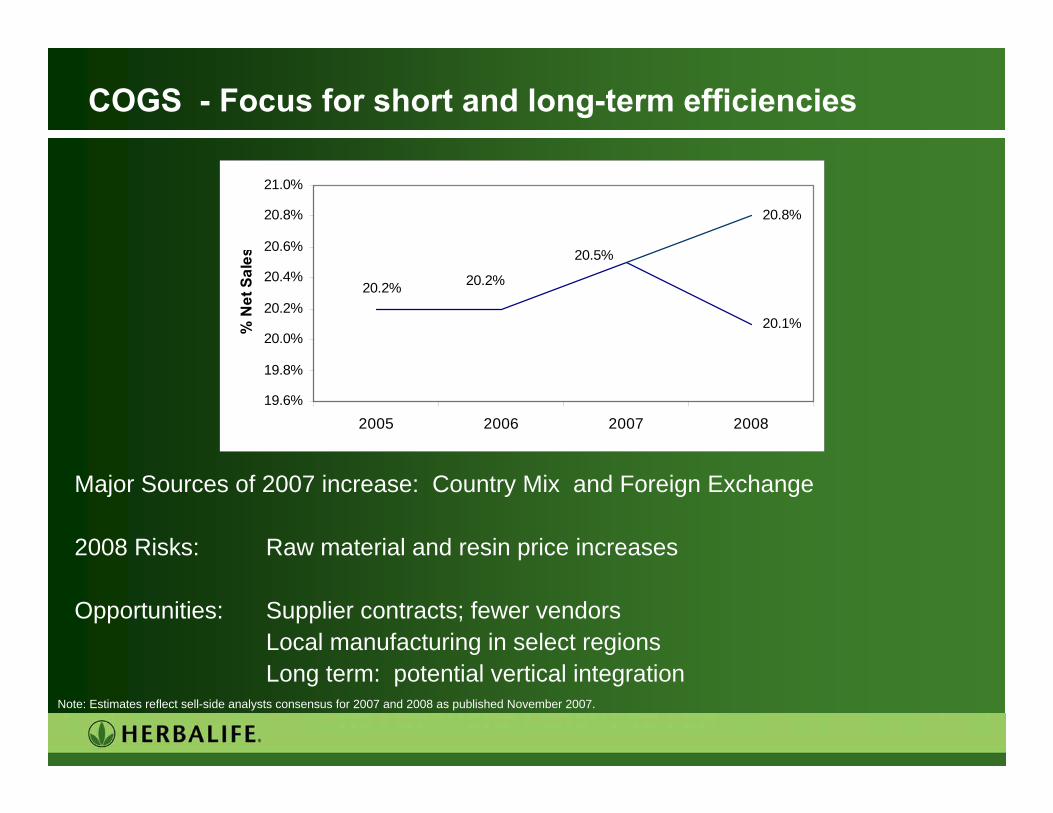

COGS - Focus for short and long-term efficiencies

Major Sources of 2007 increase: Country Mix and Foreign Exchange

2008 Risks: Raw material and resin price increases

Opportunities: Supplier contracts; fewer vendorsLocal manufacturing in select regionsLong term: potential vertical integration

Note: Estimates reflect sell-side analysts consensus for 2007 and 2008 as published November 2007.

20.1%

20.8%

20.2%20.2%

20.5%

19.6%

19.8%

20.0%

20.2%

20.4%

20.6%

20.8%

21.0%

2005 2006 2007 2008

% N

et S

ales

60

SG&A – Improvements

• SG&A as a percentage of net sales continues to decline demonstrating management’s actions to leverage the business

• 2008 Opportunities: Realignment for Growth Phase II

Country Models

28.9%29.5%

28.0%27.3%

30.0%29.2%

29.5%

30.4%

28.0%

25.0%

26.0%

27.0%

28.0%

29.0%

30.0%

31.0%

2005 2006 2007 2008

% N

et S

ales

As reported Normalized for China

Note: Estimates reflect sell-side analysts consensus for 2007 and 2008 as published November 2007.

61

Events by Quarter

20082007

Brazil ExtravaganzaBrazil ExtravaganzaFourth Quarter

North America Extravaganza

Asia Extravaganza

Mexico Extravaganza

Chairman’s Club Retreat (China)

EMEA Extravaganza

North America Extravaganza

Asia Pacific Extravaganza

Mexico Extravaganza

Third Quarter

EMEA ExtravaganzaSecond Quarter

South America Extravaganza

Herbalife Honors (Singapore)

Latin America Extravaganza

Chairman’s Club Retreat (US)

President’s Team Summit (US)

First Quarter

62

Effective Tax Rate

• The effective tax rate has followed an improvement curve reflecting the successful execution of our corporate legal restructuring.

• Operating line exclude significant prior period tax refunds and assessments from our current operating rate.

Note: Estimates reflect sell-side analysts consensus for 2007 and 2008 as published November 2007.

Effective Tax Rate

40.9% 38.1%

lowthirties37.3%

46.8%

34.1%

37.5%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

2005 2006 2007 2008

Operating ETR As Reported

63

Strong Balance Sheet

(1) Excludes certain one-time items.

12/31/2004 12/31/2005 12/31/2006 09/30/07Cash & Cash Equivalents $202 $88 $154 $161Debt:

Borrowings Under Senior Credit Facility

200 90 179 149

9½% Notes 268 161 - -Revolver 79Capitalized Leases & Other Debt 18 12 6 6

Total Debt $486 $263 $185 $234

Shareholders’ Equity 64 169 354 295Total Capitalization $550 $432 $539 $529

Total Debt / LTM EBITDA(1) 2.7x 1.1x 0.6x 0.7xNet Debt / LTM EBITDA(1) 1.6x 0.7x 0.1x 0.2xNet Debt $284 $175 $31 $73

64

2002

2003

2004

2005

2006

YTD 2006

YTD 2007

Net Income $23.2 $36.8 $54.9 $103.6 $159.7 $101.5 $137.6

Depreciation and Amortization 26.8 55.6 43.9 35.4 30.0 21.9 25.9

Write-off of Deferred Financing Costs and Unamortized Discounts ─ 1.4 30.8 6.0 7.1 6.6 0.2

Change in Working Capital 25.0 (1.2) 5.1 20.5 37.0 43.6 40.5

Other (9.1) 1.8 14.6 (11.6) (32.8) (28.6) (9.2)

Cash Flow from Operations $65.9 $94.4 $149.3 $153.9 $201.0 $145.0 $195.0

Capital Expenditures (10.4) (20.4) (30.3) (32.6) (66.9) (45.5) (30.6)

Free Cash Flow $55.5 $74.0 $119.0 $121.3 $134.1 $99.5 $164.4

Strong Cash Flow

(1) Excludes $40.6 million in cash recapitalization expenses.(2) Excludes $10.5 million in cash recapitalization expenses.(3) Excludes $16.6 million in cash recapitalization expenses.(4) Includes $7.5 million in TI allowances that will be amortized over the life of a new facility lease.

(1) (2) (3)

(4)

Guidance

66

Consistently Delivering Results

Street Estimate Reported / Guidance

2004 IPO (2005 EPS) $ 1.14 $1.52

At 2005 Secondary (2006 EPS) $1.85 $2.06

2007 EPS

At November 6, 2006 $ 2.45 $2.40 - 2.47

At February 26, 2007 $ 2.46 $2.43 - 2.50

At May 1, 2007 $2.48 $2.49 – 2.56

At August 6, 2007 $2.54 $2.56 – 2.61

At November 9, 2007 $2.65 $2.62 – 2.64

2008 EPS

At November 9, 2007 $ 3.20 $3.17 - 3.23

(1) Source: Thomson First Call

(1)

2007 Guidance Details: 2007 2008

Net sales growth YOY 9.0% - 11.0% 7.0% - 10.0%Effective tax rate 37.0% - 37.5% -----CapEx (mm’s) $43.0 - $45.0 $85.0 - $95.0

67

Questions

Michael O. JohnsonGreg ProbertRich Goudis

68

Michael O. JohnsonChairman and Chief Executive Officer

Closing Remarks

70

Direct Selling Index Components: AVP, BHIP, MTEX, NATR, NATU3, NUS, ORI.SDB, RELV, TUP, USNA (index is equal weighted to prevent Avon skew at 67% of the index)

266

124

120

HLF IPO to Date: Total Shareholder Value(Relative Performance, 12/16/04 = 100)

Source: CapitalIQNote: HLF share price $38.75 at close 11/26/2007; Total Return = stock price changes + dividends

HLF Direct Selling Index S&P 500

50

100

150

200

250

300

350

Dec-04

Mar-05

Jun-05

Sep-05

Dec-05

Mar-06

Jun-06

Sep-06

Dec-06

Mar-07

Jun-07

Sep-07

71

Investment Highlights

• Successful track record, driven by positive global mega trends

• Unique distribution channel for emerging markets and consultative products

• Geographic diversification throughout 65 markets and across four major product categories

• Financial strength – Strong cash flow– Margin expansion– Strong balance sheet– Economically resilient

• High degree of shareholder focus– Disciplined capital allocation– Free cash flow allocated to high ROI programs

• Share repurchase program - +$200MM completed since April 2007

• Proven management team