rupali - the rupali group

TRANSCRIPT

RUPALI GROUP

Rupali Polyester Limited

THE ROLE OF INCENTIVES IN PERFORMANCE MANAGEMENT

PRESENTED TO RANA NADIR

PRESENTED BY MASOOD AHMAD

ROLL#022(MHRM)

INSITUTE OF ADMINISTRATIVE SCIENCE

UNIVERSITY OF THE PUNJAB, LAHORE

The Rupali Group

The Rupali Group is a leading business group in Pakistan with diverse

commercial interests ranging from manufacturing, exporting and indenting to

banking and trade financing. The Rupali Group is also the largest producer of

polyester filament yarn and a leader in production of staple fiber in Pakistan.

Managed by the Feerasta family, the Group's activities reflect the changing

business environment and emerging needs of the economy.

The philosophy of the Group is to build on its the strength and quality while

maintaining reliability. Products and services offered by the Group are

acknowledged by customers with the highest standards.

People are central to Group’s growth strategy. A large in-house pool of

intellectual capital is the driving force behind Rupali Group’s rapid growth, and is

one of its competitive advantages.

Today, the Group is managed by highly qualified team of professionals with vast

experience in their respective fields. Every department is headed by a

professional, qualified and experienced executive.

Growth opportunities and competitive compensation packages offered by Rupali

Group enables it to attract and retain excellent talent.

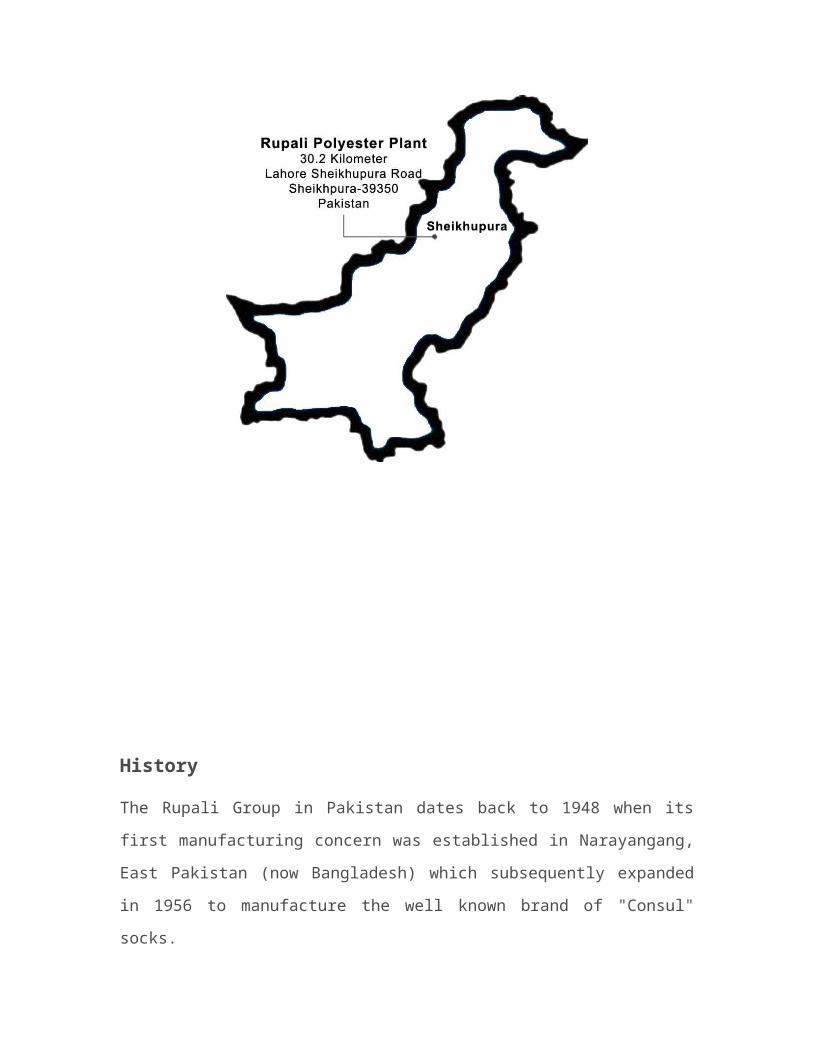

Location

History

The Rupali Group in Pakistan dates back to 1948 when its first manufacturing

concern was established in Narayangang, East Pakistan (now Bangladesh)

which subsequently expanded in 1956 to manufacture the well known brand of

"Consul" socks.

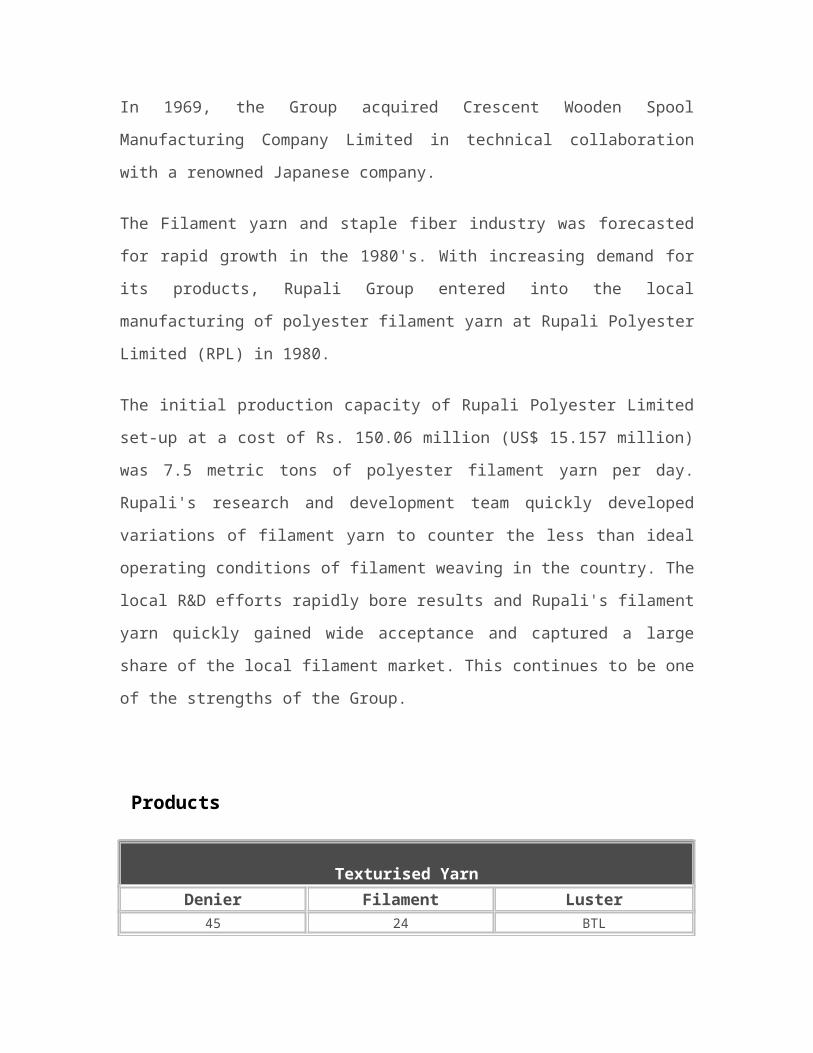

In 1969, the Group acquired Crescent Wooden Spool Manufacturing Company

Limited in technical collaboration with a renowned Japanese company.

The Filament yarn and staple fiber industry was forecasted for rapid growth in the

1980's. With increasing demand for its products, Rupali Group entered into the

local manufacturing of polyester filament yarn at Rupali Polyester Limited (RPL)

in 1980.

The initial production capacity of Rupali Polyester Limited set-up at a cost of Rs.

150.06 million (US$ 15.157 million) was 7.5 metric tons of polyester filament yarn

per day. Rupali's research and development team quickly developed variations of

filament yarn to counter the less than ideal operating conditions of filament

weaving in the country. The local R&D efforts rapidly bore results and Rupali's

filament yarn quickly gained wide acceptance and captured a large share of the

local filament market. This continues to be one of the strengths of the Group.

Products

Texturised Yarn

Denier Filament Luster45 24 BTL

45 24 BTL

75 24 OSD

75 24 OSD

150 48 BTL

160 96 OSD

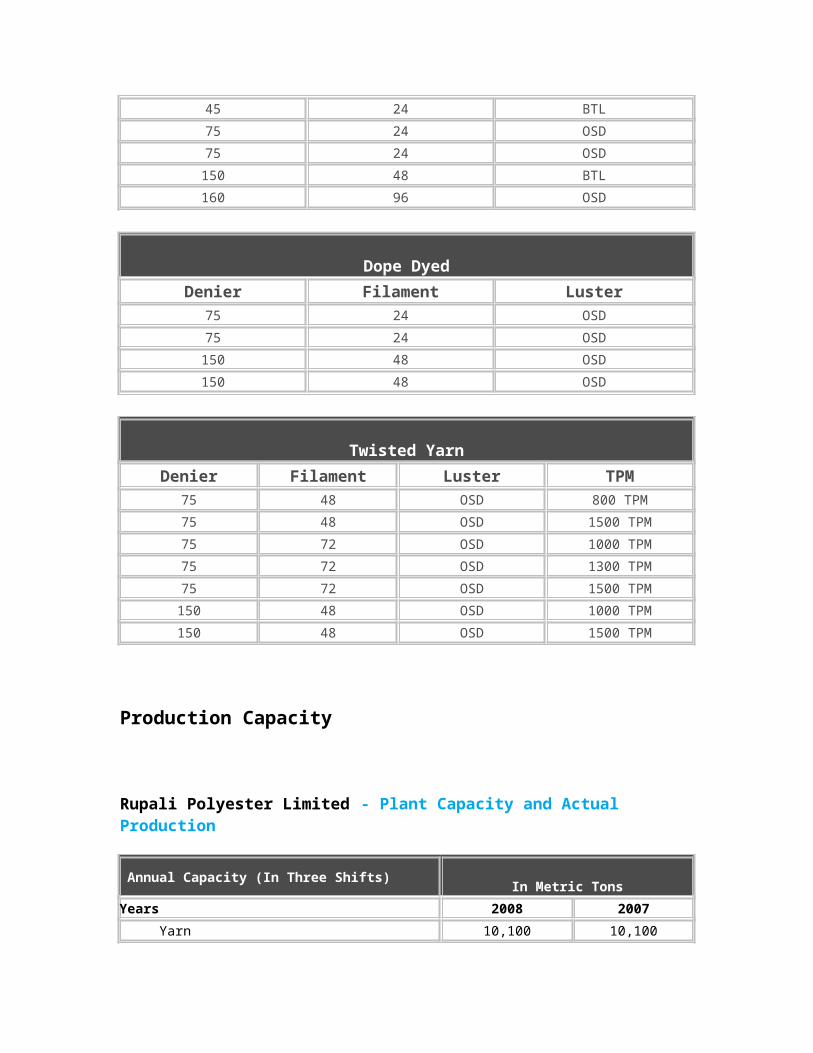

Dope Dyed

Denier Filament Luster75 24 OSD

75 24 OSD

150 48 OSD

150 48 OSD

Twisted Yarn

Denier Filament Luster TPM75 48 OSD 800 TPM

75 48 OSD 1500 TPM

75 72 OSD 1000 TPM

75 72 OSD 1300 TPM

75 72 OSD 1500 TPM

150 48 OSD 1000 TPM

150 48 OSD 1500 TPM

Production Capacity

Rupali Polyester Limited - Plant Capacity and Actual Production

Annual Capacity (In Three Shifts)In Metric Tons

Years 2008 2007

Yarn 10,100 10,100

Fiber 12,000 12,000

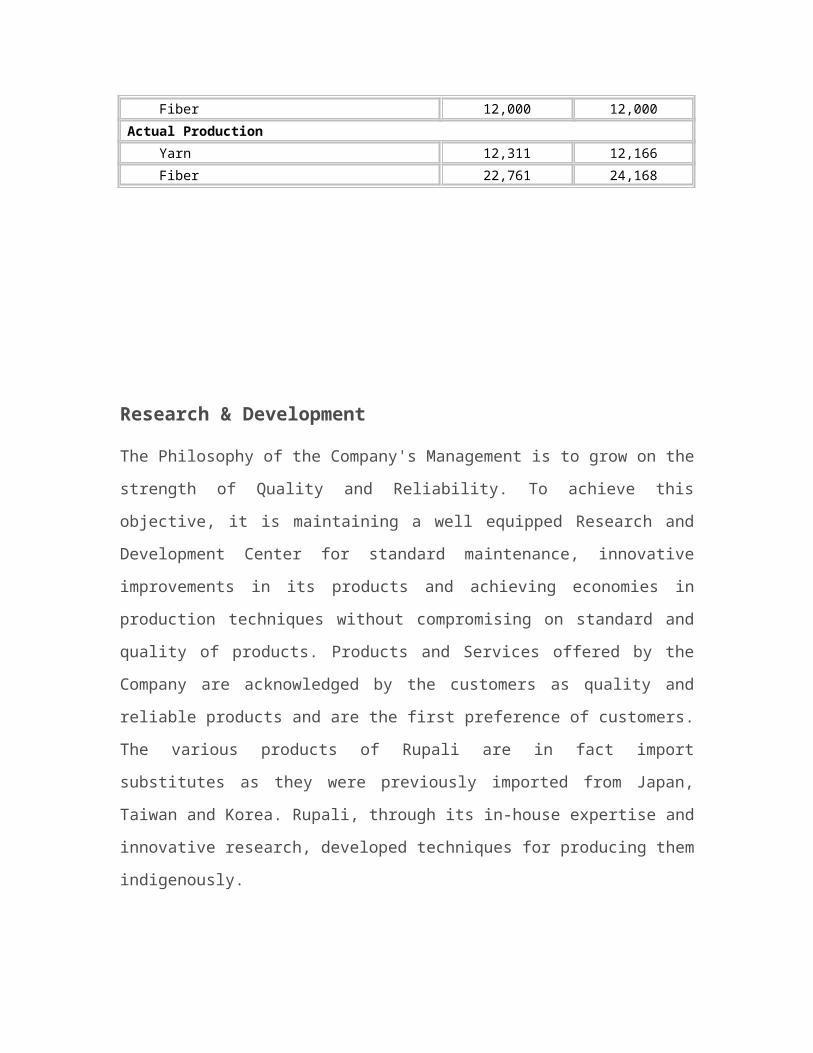

Actual Production

Yarn 12,311 12,166

Fiber 22,761 24,168

Research & Development

The Philosophy of the Company's Management is to grow on the strength of

Quality and Reliability. To achieve this objective, it is maintaining a well equipped

Research and Development Center for standard maintenance, innovative

improvements in its products and achieving economies in production techniques

without compromising on standard and quality of products. Products and

Services offered by the Company are acknowledged by the customers as quality

and reliable products and are the first preference of customers. The various

products of Rupali are in fact import substitutes as they were previously imported

from Japan, Taiwan and Korea. Rupali, through its in-house expertise and

innovative research, developed techniques for producing them indigenously.

Rupali's research and development team has developed variations of filament

yarn to counter the less than ideal operating conditions of weaving in the country,

while its finest quality fiber is excellently processed under local conditions. The

local R&D efforts continue to bear results and the Rupali brand is the preferred

choice of local weavers and processors.

The Company's innovative approach to R&D continues to be one of its strengths.

We also implement extensive quality control at all levels of the organization to

maintain our reputation for excellence. The Company gives high priority to

customer's satisfaction, tries to maintain uninterrupted supply for its products and

provides after sales services, technical support for the trouble shooting.

Quality Control

The philosophy of the company’s management is to grow on the strength of the

quality and reliability. To achieve this objective, it is maintaining a well equipped

Research & Development Center for standard maintenance, innovative

improvements in its products and achieving economies in production techniques

without compromising on standard offered by the Company are acknowledged by

the customers as quality and reliable products and the first preference of

customers.

The company gives high priority to customers, satisfaction, tries to maintain

uninterrupted supply of its products and provides after sales services, technical

support for trouble shooting.

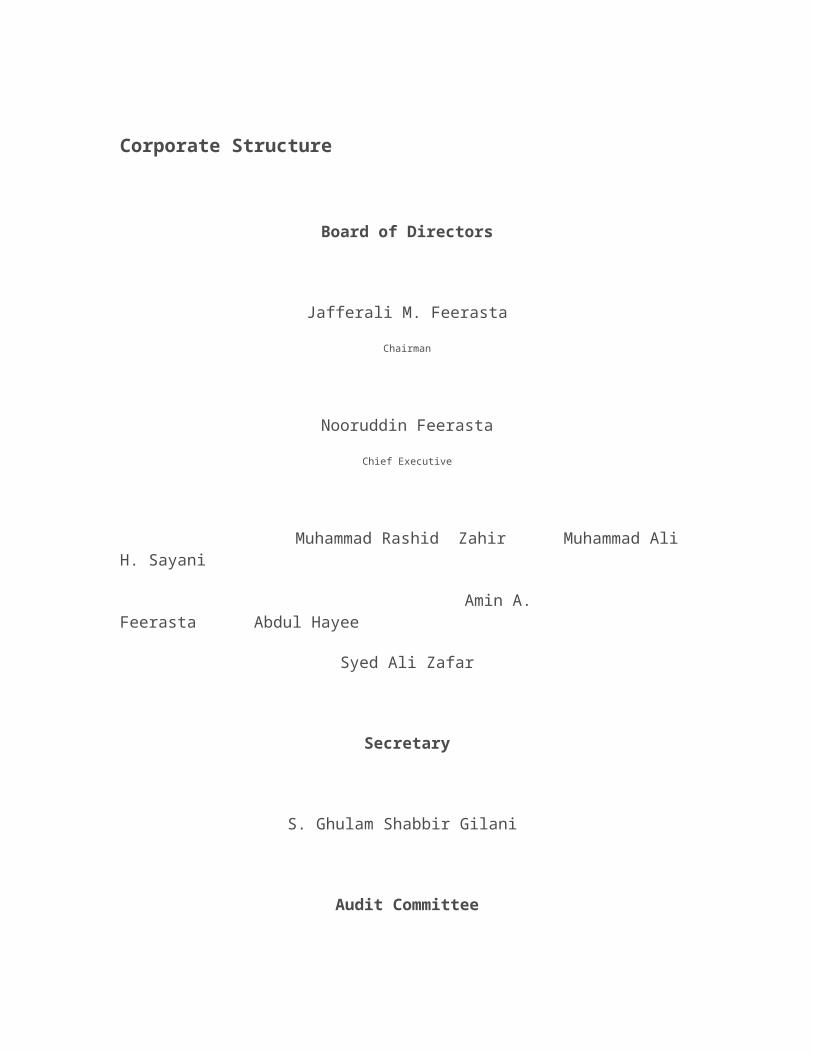

Corporate Structure

Board of Directors

Jafferali M. Feerasta

Chairman

Nooruddin Feerasta

Chief Executive

Muhammad Rashid Zahir Muhammad Ali H. Sayani

Amin A. Feerasta Abdul Hayee

Syed Ali Zafar

Secretary

S. Ghulam Shabbir Gilani

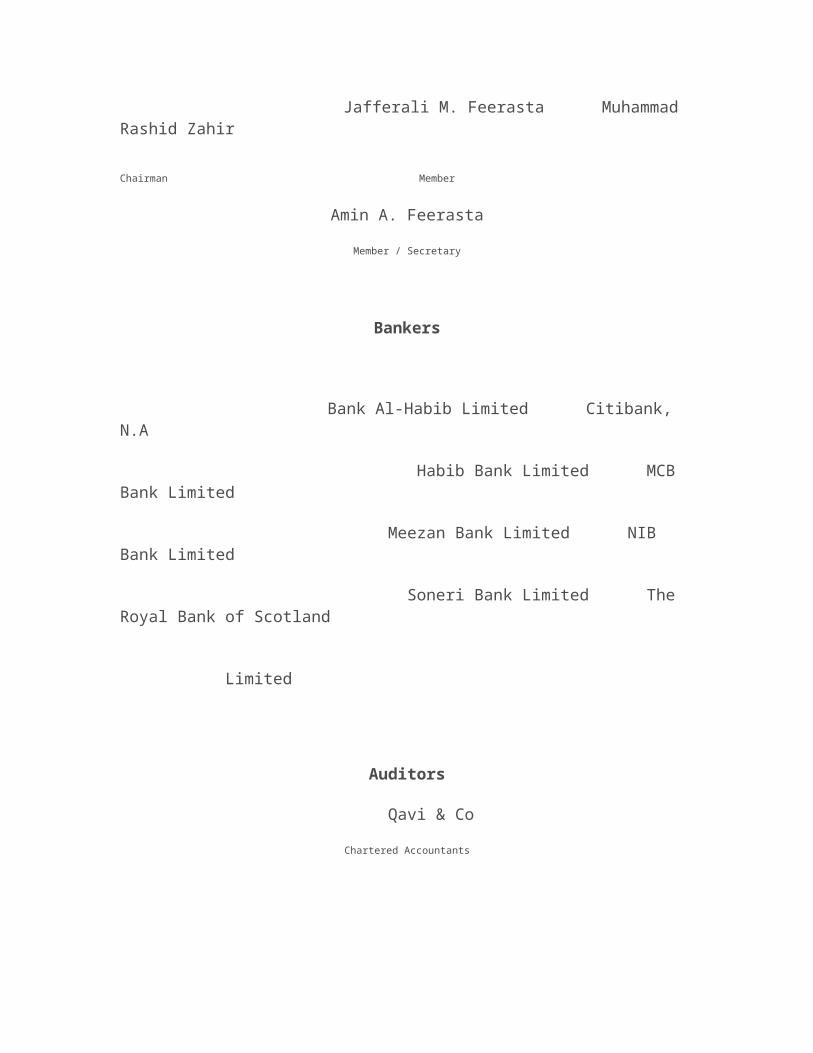

Audit Committee

Jafferali M. Feerasta Muhammad Rashid Zahir

Chairman Member

Amin A. Feerasta

Member / Secretary

Bankers

Bank Al-Habib Limited Citibank, N.A

Habib Bank Limited MCB Bank Limited

Meezan Bank Limited NIB Bank Limited

Soneri Bank Limited The Royal Bank of Scotland

Limited

Auditors

Qavi & Co

Chartered Accountants

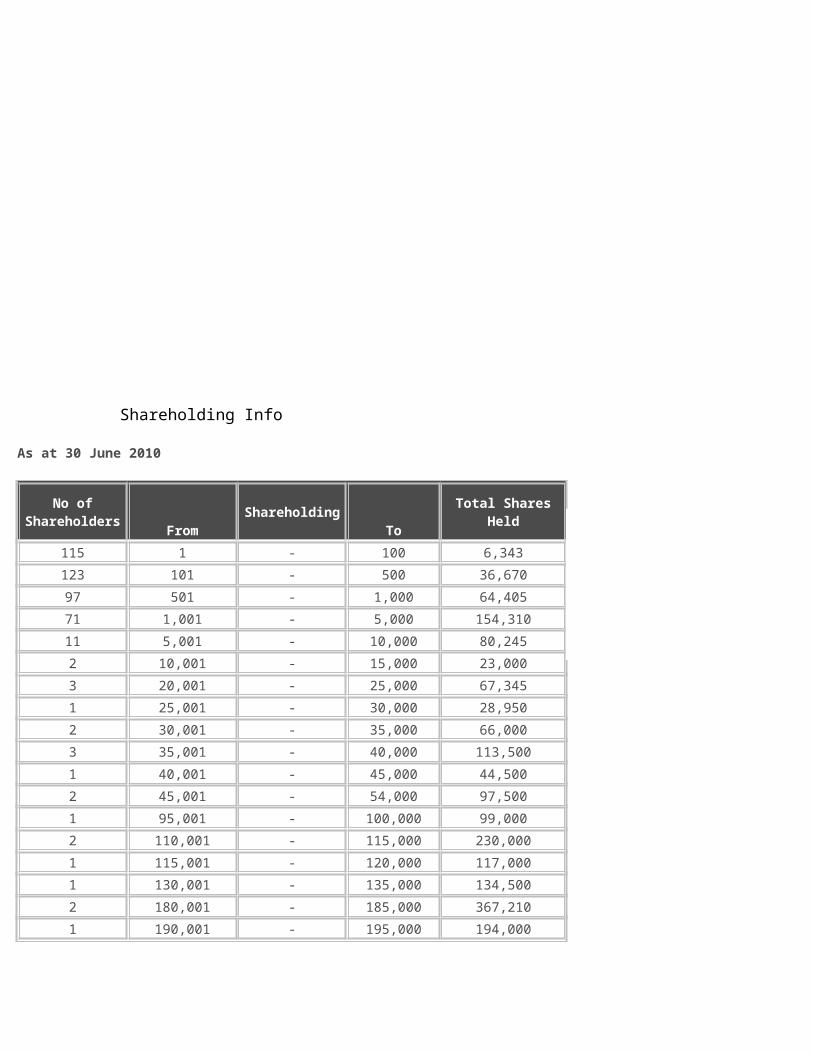

Shareholding Info

As at 30 June 2010

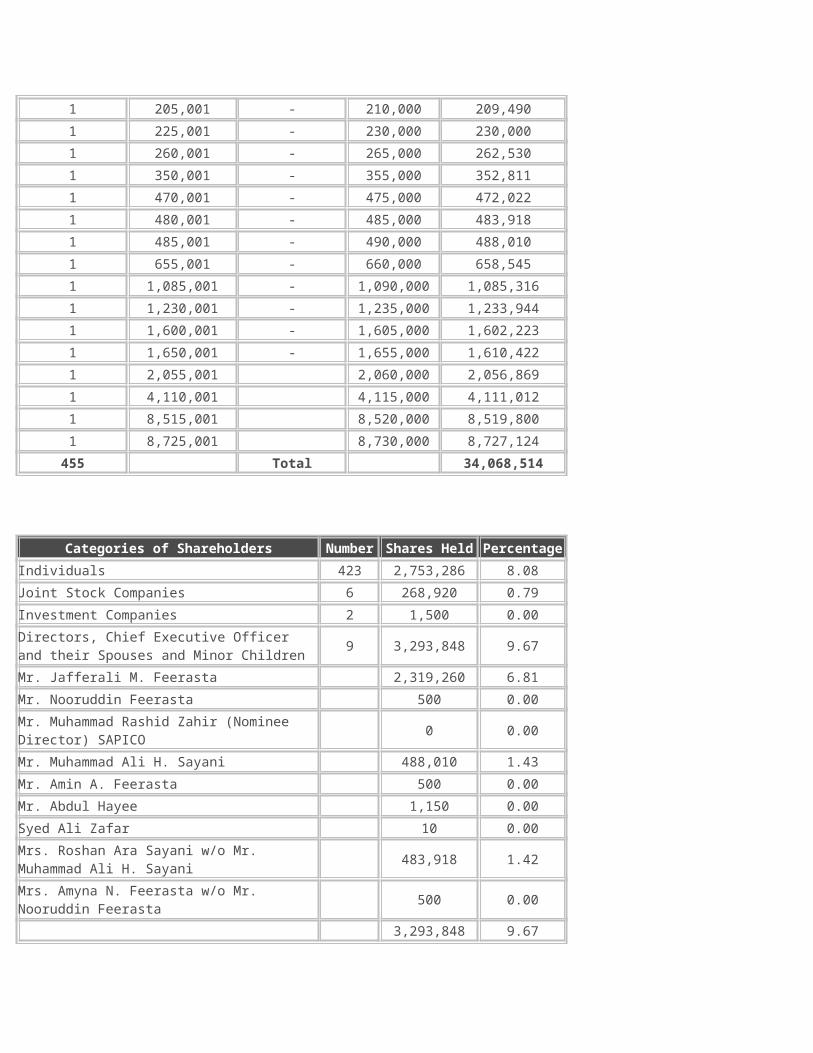

No of Shareholders

FromShareholding

ToTotal Shares Held

115 1 - 100 6,343

123 101 - 500 36,670

97 501 - 1,000 64,405

71 1,001 - 5,000 154,310

11 5,001 - 10,000 80,245

2 10,001 - 15,000 23,000

3 20,001 - 25,000 67,345

1 25,001 - 30,000 28,950

2 30,001 - 35,000 66,000

3 35,001 - 40,000 113,500

1 40,001 - 45,000 44,500

2 45,001 - 54,000 97,500

1 95,001 - 100,000 99,000

2 110,001 - 115,000 230,000

1 115,001 - 120,000 117,000

1 130,001 - 135,000 134,500

2 180,001 - 185,000 367,210

1 190,001 - 195,000 194,000

1 205,001 - 210,000 209,490

1 225,001 - 230,000 230,000

1 260,001 - 265,000 262,530

1 350,001 - 355,000 352,811

1 470,001 - 475,000 472,022

1 480,001 - 485,000 483,918

1 485,001 - 490,000 488,010

1 655,001 - 660,000 658,545

1 1,085,001 - 1,090,000 1,085,316

1 1,230,001 - 1,235,000 1,233,944

1 1,600,001 - 1,605,000 1,602,223

1 1,650,001 - 1,655,000 1,610,422

1 2,055,001 2,060,000 2,056,869

1 4,110,001 4,115,000 4,111,012

1 8,515,001 8,520,000 8,519,800

1 8,725,001 8,730,000 8,727,124

455 Total 34,068,514

Categories of Shareholders Number Shares Held Percentage

Individuals 423 2,753,286 8.08

Joint Stock Companies 6 268,920 0.79

Investment Companies 2 1,500 0.00

Directors, Chief Executive Officer and their Spouses and Minor Children

9 3,293,848 9.67

Mr. Jafferali M. Feerasta 2,319,260 6.81

Mr. Nooruddin Feerasta 500 0.00

Mr. Muhammad Rashid Zahir (Nominee Director) SAPICO

0 0.00

Mr. Muhammad Ali H. Sayani 488,010 1.43

Mr. Amin A. Feerasta 500 0.00

Mr. Abdul Hayee 1,150 0.00

Syed Ali Zafar 10 0.00

Mrs. Roshan Ara Sayani w/o Mr. Muhammad Ali H. Sayani

483,918 1.42

Mrs. Amyna N. Feerasta w/o Mr. Nooruddin Feerasta

500 0.00

3,293,848 9.67

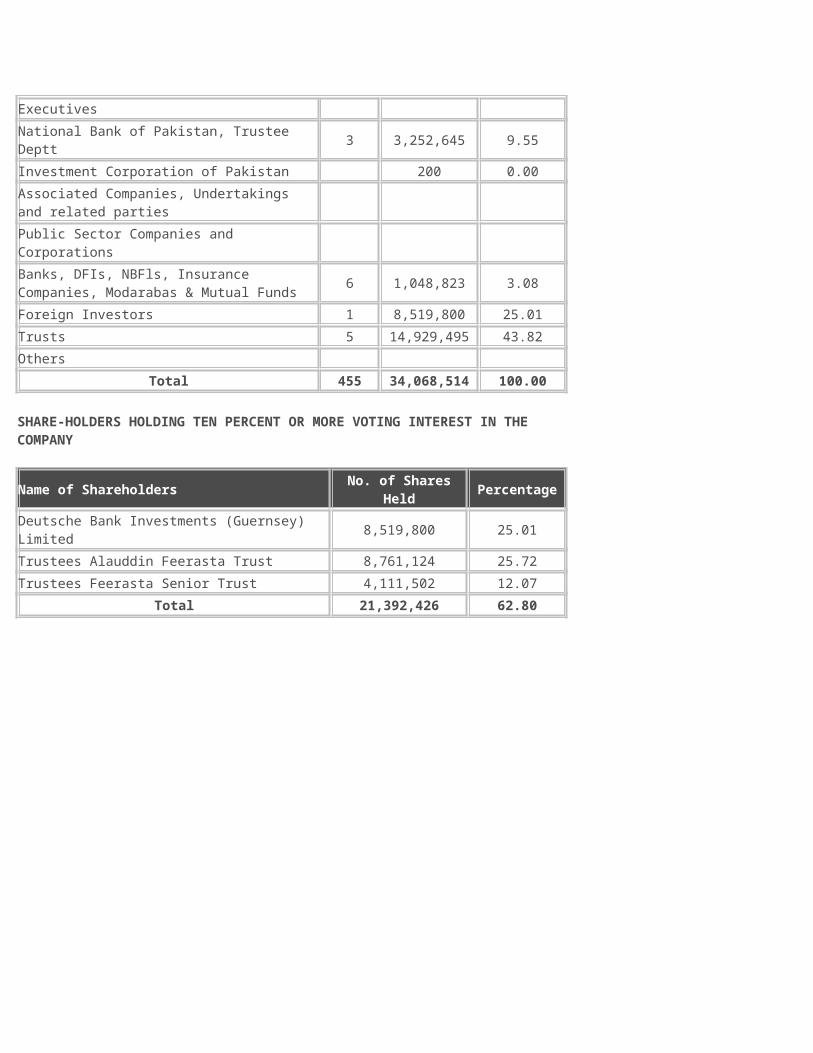

Executives

National Bank of Pakistan, Trustee Deptt 3 3,252,645 9.55

Investment Corporation of Pakistan 200 0.00

Associated Companies, Undertakings and related parties

Public Sector Companies and Corporations

Banks, DFIs, NBFls, Insurance Companies, Modarabas & Mutual Funds

6 1,048,823 3.08

Foreign Investors 1 8,519,800 25.01

Trusts 5 14,929,495 43.82

Others

Total 455 34,068,514 100.00

SHARE-HOLDERS HOLDING TEN PERCENT OR MORE VOTING INTEREST IN THE COMPANY

Name of Shareholders No. of Shares Held Percentage

Deutsche Bank Investments (Guernsey) Limited 8,519,800 25.01

Trustees Alauddin Feerasta Trust 8,761,124 25.72

Trustees Feerasta Senior Trust 4,111,502 12.07

Total 21,392,426 62.80

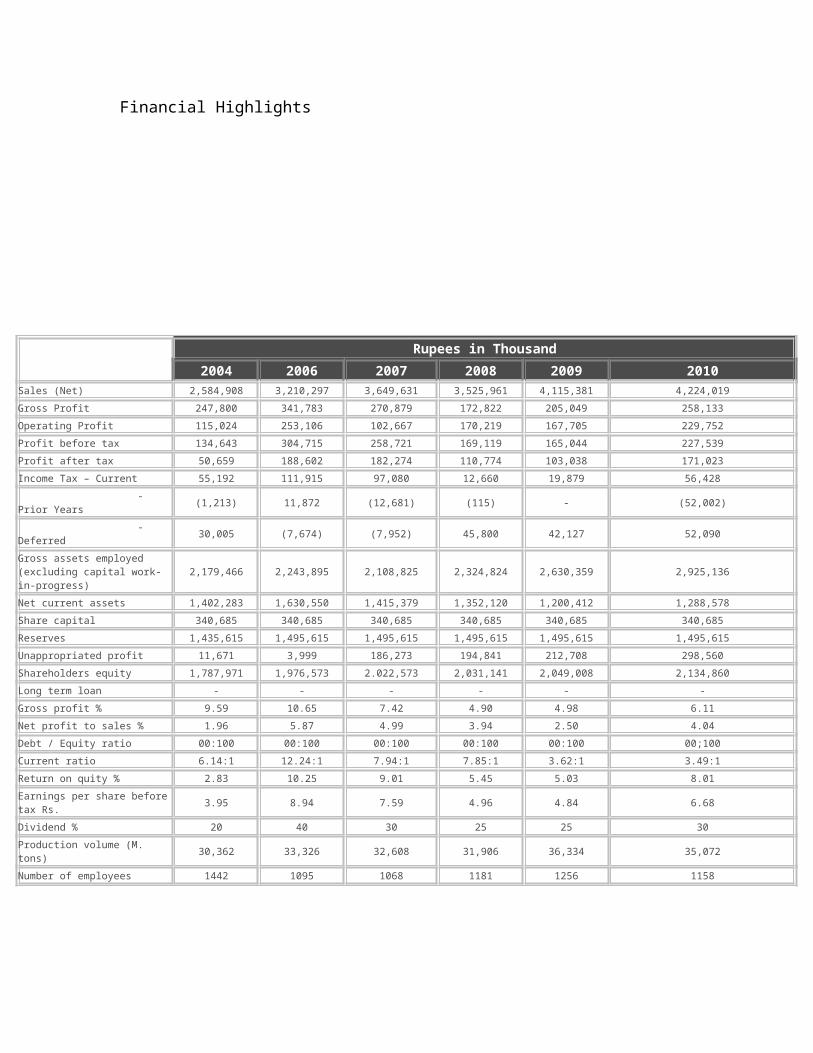

Financial Highlights

Rupees in Thousand

2004 2006 2007 2008 2009 2010Sales (Net) 2,584,908 3,210,297 3,649,631 3,525,961 4,115,381 4,224,019

Gross Profit 247,800 341,783 270,879 172,822 205,049 258,133

Operating Profit 115,024 253,106 102,667 170,219 167,705 229,752

Profit before tax 134,643 304,715 258,721 169,119 165,044 227,539

Profit after tax 50,659 188,602 182,274 110,774 103,038 171,023

Income Tax – Current 55,192 111,915 97,080 12,660 19,879 56,428

- Prior Years (1,213) 11,872 (12,681) (115) - (52,002)

- Deferred 30,005 (7,674) (7,952) 45,800 42,127 52,090

Gross assets employed (excluding capital work-in-progress)

2,179,466 2,243,895 2,108,825 2,324,824 2,630,359 2,925,136

Net current assets 1,402,283 1,630,550 1,415,379 1,352,120 1,200,412 1,288,578

Share capital 340,685 340,685 340,685 340,685 340,685 340,685

Reserves 1,435,615 1,495,615 1,495,615 1,495,615 1,495,615 1,495,615

Unappropriated profit 11,671 3,999 186,273 194,841 212,708 298,560

Shareholders equity 1,787,971 1,976,573 2.022,573 2,031,141 2,049,008 2,134,860

Long term loan - - - - - -

Gross profit % 9.59 10.65 7.42 4.90 4.98 6.11

Net profit to sales % 1.96 5.87 4.99 3.94 2.50 4.04

Debt / Equity ratio 00:100 00:100 00:100 00:100 00:100 00;100

Current ratio 6.14:1 12.24:1 7.94:1 7.85:1 3.62:1 3.49:1

Return on quity % 2.83 10.25 9.01 5.45 5.03 8.01

Earnings per share before tax Rs. 3.95 8.94 7.59 4.96 4.84 6.68

Dividend % 20 40 30 25 25 30

Production volume (M. tons) 30,362 33,326 32,608 31,906 36,334 35,072

Number of employees 1442 1095 1068 1181 1256 1158

RUPALI POLYESTER LIMITED was incorporated at Karachi in May 1980 as a

Public Limited Company and is listed on all stock exchanges of Pakistan. It owns

and operates composite facilities to manufacture Polyester Fiber and Filament

Yarn. It produces quality products by using latest technology and best quality of

raw materials. The Company has the privilege of being one of the pioneers in

Pakistan for manufacture of Staple Fiber of highest quality. Since its inception,

the Company has been growing steadily through expansion and diversified

operations. The assets of the Company have increased to over Rs. 2,931 million

from the initial capital outlay of Rs. 150 million.

The Company has a polymerization unit with a capacity of 105 metric tons per

day, polyester filament yarn capacity of 30 metric tons per day and a polyester

staple fiber capacity of 65 metric tons per day. The various products of Rupali are

in fact import substitution as these were previously imported from Japan,

Indonesia, Taiwan and Korea. Now the Company is importing the basic raw

materials only and through value addition is producing the highest quality

products locally.

Since inception, the philosophy of the Company’s management is to grow on the

strength of quality and reliability. To achieve this objective, it is maintaining a well

equipped Research & Development Centre for standard maintenance, innovative

improvements in its products and achieving economies in production techniques

without compromising on standard and quality of products. Products and services

offered by the Company are acknowledged by the customers as quality and

reliable products and are the first preference of customers.

The Company gives high priority to customers’ satisfaction, tries to maintain

uninterrupted supply of its products and provides after sales services, technical

support for trouble shooting. AL HAMDO LILLAH, the Company enjoys high

prestige and reputation in the business community, banks, financial institutions

and customers. It is also amongst major contributors to the national exchequer.

Career

Rupali Group holds a prime position in the business sector and is a preferred

employer amongst prestigious nationals and multinationals. We recruit highly

qualified and experienced individuals - both at entry level and for vacancies

arising at various levels - who would prove to be assets for the organization. We

provide opportunities for improving personal capability to enable staff to take on

greater responsibility. Having a rich and diverse history, we encourage our

employees to venture forth in new and dynamic areas leading to organizational

progress along with individual growth.

Incentives for Employees in Rupali Group

• Pay, Salaries, “efficiency wages” etc.

• Direct financial benefits, such as , illness/health/life insurance; allowances

(Clothing, housing, etc.), subsidies, gain sharing, pensions (through EOBI)

• Indirect financial benefits such as subsidized meals/clothing/ accommodation/

Transport, scholarships, (through Labour department),

• Study leave, holidays, vacation, etc.

• Work environment/conditions, occupational health, safety, recreational facilities

• Amenities, school access(through Labour department), infrastructure,

transport,

etc.,

• Job security; Career/ professional development/ training opportunities

• Feedback, coaching, valued by organization

• Solidarity, socializing, camaraderie, affection, passion

• Status, prestige, recognition(Long service awards)

• Sense of duty, purpose, mission

• Security, opportunities, stability, risk

Incentives and Performance Management In Rupali Group

When designing a performance management system, does it make

sense to link goal accomplishment to monetary incentives? How does

incorporating incentives into such a system affect workers?

Performance, motivation, and attitudes? What shape should such

incentives take? The purpose of this document is to summarize the

highlights of empirical research that addresses these questions.

What do incentives add to a performance management

system? Are monetary incentives necessary, or are goals and

feedback enough?

From the substantial body of research on goal-setting we know that

workers who are given goals that are specific and difficult outperform

workers who are given a "do your best" goal or no goal at all (Latham

& Lee). Goals do four things: direct attention; mobilize task effort;

encourage task persistence; and facilitate development of task

strategies (Locke; Locke & Latham). In other words, goals provide us

with a clear direction; inform us that we need to try hard; remind us

that an end is in sight; and encourage us to think about the process of

reaching that end.

From the body of research on feedback we know that workers given

information about how they perform generally outperform workers who

are not given such feedback (Enzle & Ross; Harackiewicz).

Furthermore, we know that comparative feedback is especially useful.

In studies that compare task feedback that allows a worker to compare

his/her competence relative to others versus task feedback that allows

a worker to assess his/her competence in isolation only, the

comparative feedback has a stronger impact on workers? feelings of

effectiveness (Sansone). The research does not give a clear answer

regarding the impact on actual effectiveness; the dependent variables

in most feedback studies are related to motivation (self-perceived

effectiveness) rather than performance (actual effectiveness).

We also know that a combination of goals and feedback has a more

powerful effect on task interest and persistence than either goals or

feedback alone (Bandura & Cervone). When goals and feedback are

combined, we know whether we are on the right path, and we know

how much farther we need to go to reach our goal.

What happens when monetary incentives are added to the mix? While

goals and feedback clearly boost performance, adding incentives can

enhance task interest and persistence further still (Locke, et al.). The

key word is "can" ? whether incentives will have a positive effect on

motivation depends upon the nature of the incentives.

What impact do monetary incentives have on motivation?

Early research suggested that when extrinsic rewards such as

monetary incentives were linked to performance on interesting and

appealing tasks, intrinsic motivation decreased. The reason for this

effect was that when workers were rewarded for doing work they

already enjoyed, they observed themselves accepting a reward and

inferred that they must be working for the reward rather than for

intrinsic enjoyment of the task. Extrinsic rewards thus dampened

intrinsic interest (Deci; Lepper, et al.). This finding received a great

deal of attention, but subsequent research, however, provided limited

support. One review of 24 relevant studies found that while 14

reported a negative impact of extrinsic rewards on intrinsic motivation,

10 reported no such impact (Boon & Cummings). It is now clear that

extrinsic rewards can impair or enhance intrinsic motivation,

depending upon how the rewards are constructed and construed.

Harackiewicz, Manderlink, and Sansone explain that rewards have

three aspects: evaluation, performance feedback, and reward value.

Each aspect can have a different impact on intrinsic motivation. The

evaluation aspect promotes feelings of external control and thus

reduces intrinsic motivation. The feedback aspect promotes feelings

internal control and thus enhances intrinsic motivation. The reward

value aspect? The incentive as a symbolic cue of achievement? makes

competence salient and thus enhances intrinsic motivation. In a series

of experiments, Harackiewicz and colleagues showed that introducing

contingent rewards can enhance, inhibit, or have no effect on intrinsic

motivation, depending upon which of the three aspects is made most

salient. Other researchers have obtained similar results (Enzle & Ross).

Researchers are just starting to address the most interesting question:

under what conditions will a given aspect be most salient?

When are rewards likely to have a strong effect on a worker?s

motivation and effort?

The dominant model for understanding and predicting whether a

reward is likely to affect worker motivation and effort is Victor Vroom?s

expectancy model. Several decades of research have largely

substantiated the accuracy and robustness of this model. Vroom

asserts that the strength of a reward?s impact on worker motivation

and effort are a function of three factors: expectancy, instrumentality,

and valence. Expectancy is the worker?s perception of the strength of

the link between effort and performance. If I work hard and put myself

out, will that translate into enhanced task performance?

Instrumentality is the worker?s perception of the strength of the link

between performance and the reward. If my performance is strong, will

I receive commensurate rewards? Valence is the value a worker places

on the reward. Will the rewards I receive be things I really care about?

Vroom?s model highlights the fact that, in order for an incentive

program to have a strong impact on worker motivation and effort, the

worker must believe that effort will lead to performance, that

performance will lead to rewards, and that the rewards will be

desirable. A manager who wants to design an effective incentive

system must take into account the worker?s perceptions along each of

these three dimensions. Empirical research has shown that the

strength of these three factors can in fact predict a worker?s effort and

performance level (Mitchell; Katzell & Thompson). If any one of these

factors is weak, the incentive system is not likely to have a meaningful

positive impact.

The research I have cited until this point is primarily on the individual

level. That is, it focuses on the impact of incentives on individual

workers. (Actually, the research participants are usually college

students rather than workers.) What about the organizational level? Do

organizations that introduce incentives perform better? The evidence is

mixed. Some researchers firmly conclude that linking pay to results

leads to enhanced organizational performance (e.g. Lawler; Ehrenberg

& Bognanno; Kahn & Sherer; Mitra et al.; Zenger & Marshall). Other

researchers conclude that contingent pay has no appreciable impact

on organizational performance (e.g. Milkovich & Wigdor; Pearce,

Stevenson, and Parry; Pearce & Porter; Shay). Part of the reason for

the lack of consensus is that these studies encompass a broad array of

incentive systems, such merit salary increases, one-time bonuses,

gain-sharing programs, and profit-sharing programs. Furthermore,

these studies operationalize performance in very different ways, such

as quality of output, quantity of output, financial status, worker

perceptions, etc. Indeed, recent literature reviews (Heneman; Milkovich

& Wigdor) note that it is too early to draw firm conclusions about the

impact of incentives on firm performance.

Predicting dysfunctional effects of incentives

In an ideal world, incentives lead to enhanced motivation, effort, and

performance. In the real world, however, incentives can have

dysfunctional effects. The dysfunctional effect that has received the

most study is the worker?s lament, "It?s not fair!" When rewards are

contingent on performance, workers are finely attuned to issues of

fairness, and a distribution of rewards that is perceived as even slightly

unfair can lead to significant problems (Greenberg).

Researchers have tried to understand when workers are likely to

perceive their rewards as unfair, and how they are likely to react. A

useful model for understanding these issues is Stacy Adams? equity

theory, which has been supported and refined through decades of

research. Adams? theory, simply put, is this: To assess whether I am

being rewarded fairly, I compare myself to others. I compare not only

the rewards I receive (known as "outcomes" in equity theory) but also

my inputs, and the ratio of my rewards to my inputs. Inputs include

such things as effort, talent, and tenure. If my ratio is smaller than

yours, I perceive the distribution of rewards as unfair. I will try to

redress this injustice by changing the elements of our two ratios to

make them equal. Research has indicated that the most common

approach to equalizing the ratios is decreasing my inputs ? that is,

reducing my effort (Campbell & Pritchard, 1976). When I try to affix

blame for my unjust situation, I am likely to blame external factors,

such as my supervisor, the organization, or the incentive system,

rather than myself (Taylor & Pierce). Not surprisingly then, when

workers feel relatively undercompensated they are more likely to

engage in theft, sabotage, politicking, and turnover (Summers &

Hendrix; Martin; Greenberg).

On the other hand, when assessing the fairness of the distribution of

rewards, it is possible that I will discover that my ratio of rewards to

inputs is bigger than yours. Adams? theoretical framework predicts

that in this situation of relative overpayment, I will react by increasing

my inputs ? effort ? in order to bring our ratios in line. The evidence for

this prediction is mixed. In the short term, workers may indeed react to

feeling overpaid by expending more effort to justify their rewards. Over

the long term, however, workers are likely to simply change their

perception of their deservedness, rather than sustaining an increased

effort level (Campbell & Pritchard).

When I compare my reward-input ratio to yours, it is much more likely

that I will perceive my ratio as too small rather than too big. This is

because people generally have exaggerated perceptions of their

performance (Meyer); this is a fundamental cognitive bias. On top of

that, people generally are prone to compare their pay to others who

are perceived as comparable in performance, but who earn more

(Martin). Given these tendencies, the odds are good that I will be

dissatisfied with my rewards and perceive myself as unjustly

undercompensated.

Coping with dysfunctional effects of incentives

How can a manager cope with the seemingly inevitable dissatisfaction

that performance-contingent rewards will thus produce? One approach

is to reduce the intensity of the pay plan ? that is, to reduce the

proportion of a worker?s pay that is contingent on performance. But

this approach also reduces the positive impact of incentives on

motivation and performance (Zenger & Marshall). Research suggests

the most effective way to cope with a worker?s sense of "distributive

injustice" is by establishing "procedural justice." Distributive justice

concerns the relative size of my rewards; procedural justice concerns

the process by which the size of my rewards was determined.

Greenberg studied the simultaneous impact of distributive and

procedural justice, and discovered a fascinating interaction. Workers

perceived a high pay level as fair regardless of the process by which

the pay level was determined. Workers perceived a low pay level as

fair only when the process by which the pay level was determined was

fair. In other words, workers tolerated a distribution of rewards that

they felt was unfair so long as the process of determining the

distribution seemed fair.

What contributes to workers? sense that a process for determining

rewards is fair? A process is more likely to be perceived as fair when it

is open and transparent, and when workers can contribute to the

process by providing relevant information (Lind & Taylor; Kanfer et al).

How should incentives be structured? What key contingencies

have been identified?

Given the level of interest in contingent pay in both the public and

private sectors, there is surprisingly little research into how best to

structure an incentive system. There are very few studies that

compare the effectiveness of different incentive plans (Milkovich &

Wigdor). This may be due to the difficulty of conducting comparative

research. Comparing the impact of different incentive structures

requires recruiting many organizations into a study. This is costly in

both time and effort. It is much easier for a researcher to focus on the

incentive scheme at one particular organization, although such

analysis does not yield direct information about how one type of

incentive scheme compares to another, or the conditions under which

a particular type of incentive scheme makes sense. As noted earlier,

Zenger & Marshall have found that schemes with greater incentive

intensity (percentage of pay that is contingent on performance and

thus at risk) have a larger positive impact on motivation and

performance than schemes with lesser incentive intensity. We also

know that, when designing group-based incentives, the smaller the

group, the greater the impact of the incentives on motivation (Zenger

& Marshall). But only one feature of incentive system design has

received sustained attention :whether and when incentives should be

individual or team-based.

a. Structuring incentives: Individual versus group

Should incentives be based on individual or on group performance?

Research shows that both approaches have benefits and both have

costs. Basing rewards on individual performance is generally

associated with increased pressure on individuals to perform and to

accept responsibility for their own actions, and increased risk-taking

behavior (Milkovich and Newman). When individualistic schemes

successfully distinguish between high and low performers, such

systems provide a valuable source of performance feedback, and

foster the sense of a meritocracy. Individual rewards can be especially

useful in large organizations where workers might otherwise feel lost in

the system, according to Lawler.

When incentives are based on group performance (which typically

means every group member receives an equal reward) group members

report greater liking and respect for one another, enhanced self-

esteem and perceptions of control, lower anxiety, and more task

enjoyment (Johnson & Johnson). Slavin found greater communication

among team members when rewards were group- rather than

individual-based, even when the task did not require any interaction.

Mesch et al. found higher levels of learning and information sharing

among group members when rewards were based on group

performance. Several investigators have found that group-based

rewards foster cooperation and helping (Milkovich & Newman; Miller &

Hamblin).

Both the individualistic and the egalitarian, group-based approaches

have serious shortcomings. Under the individualistic approach,

resources and information are more likely to be hoarded than shared.

Individualistic systems can exacerbate the sense of a two-tiered

society of organizational winners and losers. Outstanding performance

appraisals are, at least in theory, reserved for a select minority. This

can alienate the very people who most need to improve (Drennan).

Instead of trying harder, low performers may rationalize their poor

performance evaluations as merely a sign of incompetence or bias on

the part of those conducting the performance appraisals. The

organization can produce a residue of disgruntled people who feel they

owe it nothing; indeed, they may

wish it ill (Gabris & Mitchell). High performers also can suffer under

individualistic pay schemes. Several classic case studies of incentive

plans, from that of Roethlisberger & Dickson to William H. Whyte, have

documented the ostracism and other negative social sanctions high

performers must sometimes endure.

Group-based rewards can have dysfunctional effects as well. Group-

based incentives can promote regression to the mean rather than

outstanding contribution (Milkovich and Newman). Low performers

may have little incentive to obtain training and raise their contribution.

So as not to be taken advantage of, high performers may hold back

from exerting themselves (Harkins) or leave the organization

altogether. Alternatively, high performers may become vigilant police

officers who pressure the low performers to try harder (Drabman,

Spitalnik, & Spitalnik). As a result, low performers may feel tremendous

pressure and scrutiny from other group members (Ames), which may

further inhibit improvements in low performers? output. Furthermore,

the group product could suffer if low performers feel their low status

gives them little right to exert influence or express their individual

perspective.

Given the compelling data both pro and con, what can be inferred from

this body of research? Incentives should be team-based when

cooperation and knowledge-sharing are critical to task success, such

as in cross-functional product development (Balkin & Gomez-Mejia;

Milkovich & Wigdor). Task complexity is likely to shape the need for

cooperation and the extent of interdependence among workers. When

task success hinges on individual excellence, individual incentives are

appropriate. This is likely for tasks that are simpler and less

interdependent. The nature of the work should drive the design of the

incentive system.

b. Structuring incentives: Types of worker

How should the design of an incentive system vary based on the type

of worker? Several decades ago, sharp distinctions were drawn

between the types of pay plans appropriate for senior managers,

middle managers, and line workers. Those distinctions have now

largely fallen by the wayside. Only a small amount of research speaks

to this question (and the research addresses the question only

indirectly). Gomez-Mejia & Balkin found that performance-contingent

pay is less appropriate for workers who have a low willingness to take

risks. Placed under a variable compensation regime, such workers are

likely to withdraw, either cognitively or behaviorally. Igalens & Roussel

report that exempt employees are more likely to experience

contingent pay as motivating than are non-exempt employees.

Bushman, Indejejikian, & Smith found that incentive intensity (the

percentage of pay at risk) is greater at higher levels in an

organizational hierarchy than at lower levels. Bushman et al. argue

that this is appropriate, since people at higher levels have greater

influence over the organization?s success.

A study on” The Role of Incentives In Performance Management” in MIAN TYRE & RUBBER COMPANY LIMITED

Research Questionnaire

Dear Mr./Ms./Mrs. Masood Ahmed (Manager Industrial Relations & HR)

Assalam-o-Alaikum!

I am a student of MHRM at Institute of Administrative Sciences (IAS), University of the Punjab. As part of my project of RMT subject, I have been asked to carry out “A Study on the Role of incentives in Performance Management “Mian Tyre & rubber Co. LTD” For that purpose I have been allowed to choose your Organization. I would like to have an understanding of your perceptions/views as to have incentives can play a role in perform Management, which will serve as a fundamental basis for my research. You are therefore, requested to give your valuable input by going through and answering the items tabulated in several sections of this questionnaire.

I would assure you that your response to this questionnaire will be kept confidential and will be not be disclosed or used in any manner other than the research purpose as stated above.

Thanking you for your valuable time and help for this research study.

SHAHAB ALI

Masters of

Human

Resource

Manageme

ntInstitute of Administrative

Sciences

University

of The Punja

bRoll No. 24

(2009-2011)

Section One: Demographic and Attributes, Please Tick the appropriate box0. Name of Employee / Department Masood 1. Position /Designation Ahmed (Manager Industrial Relations & HR)2. Qualification Masters in IR & HR

Ph.D M. Phil/MS Masters √ Bachelor 3. Experience in Job (years) 8 Years with current Organization 055. Age (years) 366. Gender:

Male √ Female

Section Two: Role of Incentives in Performance Management

Strongly agree

Agree Partially agree/ partially disagree

7. I have a clear understanding of organizational vision and mission

√

8. In my organization departmental performance goals are developed in line with organizational vision and mission statement

√

9. In my opinion, performance management system is in existence in my organization

√

10. I am aware of the objective of current performance related reward offerings

√

11. Following type of performance based incentives (PBI) are currently offered by the organization to boost my performance:

Financial Non financial 12. Following financial performance based incentives (PBI) are currently offered to me: (tick the applicable box)

___________ Accelerated √ Salary increment √ Special prize √

Promotion In case of other please specify

Sponsored Travel √

Sponsored Training and Education √

Sponsored recreation / entertainment

13. Following non-financial performance based incentives (PBI) are currently offered to me: (Tick the applicable box)

Assignment of additional charge / authority

Issuance of Certificate of Merit / honor / Appreciation √

Employee of the year award

Acknowledgement of performance in official publication

Ceremony arranged in recognition of performance √

Enclave / place ascription in the name of an excellent employee

Other please specify

Section Two: Role of Incentives in Performance Management Strongly agree

Agree Partially agree/ partially disagree

14. I think that existing performance based incentive system is compatible with other similar organizations in Pakistan known to me

√

15. I feel satisfied with the current availability of performance based incentives system

√

16. Implementation / reinforcement of performance based incentive system based on performance suggested by higher management is suitable.

√

17. In my view there should be a noticeable difference in reward increases among employees based on performance

√

18 Audit should be given higher weightage in my performance evaluation

√

19. When an employee receives a performance incentive the other employees are motivate to exert extra effort.

√

20. Performance based incentives are distributed less frequently

√

21. My suggestions and reservations relating to PBI are duly considered by the concerned authorities.

√

22. I fully understand the results / outcomes expected from me to do my job.

√

23. My supervisor who evaluates my performance is competent enough to discharge such function with due care

√

24. My supervisor who evaluates my performance is generally biased and unfair

√

25. In my view serious attempts are made to mitigate the risks and challenges faced by performance based incentives system

√

26. I am given proper briefing / feedback regarding performance targets, reward entitlements, performance evaluation and reward distribution mechanism

√

27. In my organization a fair budgetary allocation is available for award of performance based incentives system to the employees

√

28. Funds allocated for performance based incentives system can be used as a tool to payroll cost

√

29. I feel that performance based incentives system can improve institutional competitiveness

√

30. Higher I am satisfied with performance based incentives system, higher will be its impact on my performance

√

31. Please tick against the type of other risks and challenges faced by PBI system, which need to be addressed:

√

Lack of vision and strategic direction

Lack of employees involvement in the process

Imposed implementation

Lack of funding and resources√

Lack of Transparency and Fairness

Highly optimistic and difficult to achieve standards

Ineffective PBI system monitoring

Others please specify

Lack of Supervisory competence

Lack of HR management √

Un-controllable elements hindering performance organizational, departmental and individual goal alignment

Lack of awareness in employees √

Vague or ambiguous policies and procedures

32. Followings are my suggestions for PBI improvement, which may be helpful in creating higher and positive impact on an employee performance :

- KPI Should be developed- Awareness Program must be developed- The negative gap should be filled in through performance management.