ron surz president ppca inc [email protected] (949)488-8339 amazingly helpful alternative

TRANSCRIPT

Apathy can be overcome by enthusiasm, and enthusiasm can be aroused by two things: • first, an idea which takes the imagination by storm;• and second, a definite, intelligible plan for carrying that idea into action.

-- Arnold Toynbee (1889-1975)

The Idea: Replace market indexes with a true core non-dilutive complement to active managed money programs. It’s a “A-Ha” moment.

The Plan: Build partnerships to create and distribute this revolutionary idea.

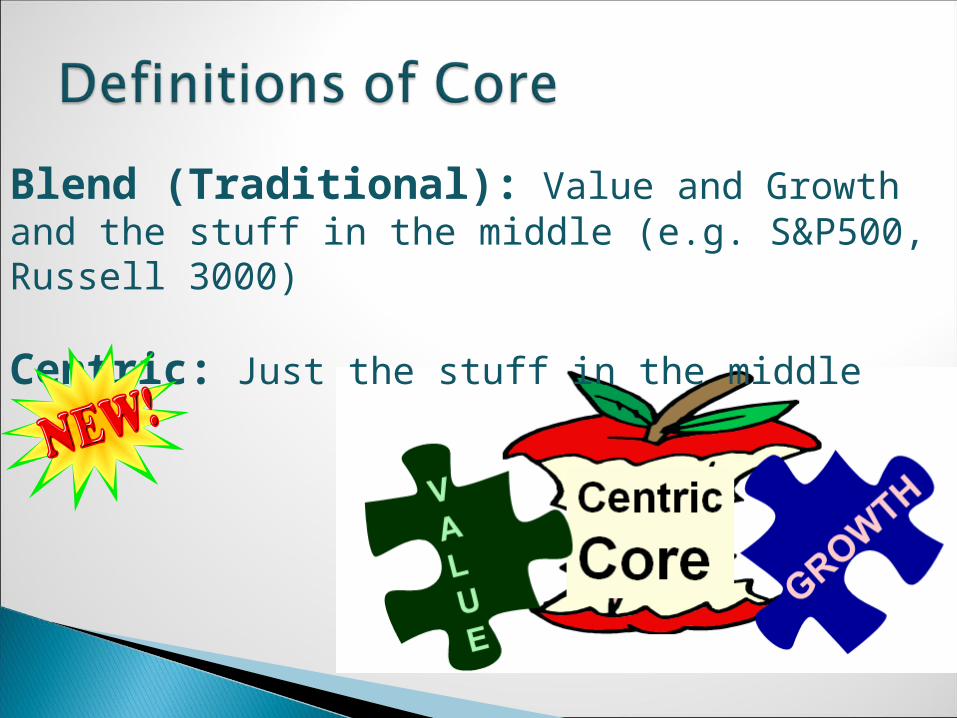

Blend (Traditional): Value and Growth and the stuff in the middle (e.g. S&P500, Russell 3000)

Centric: Just the stuff in the middle

Just as mid-cap serves an important role, so too does mid-style, namely centric core.

Traditional “core” indexes are not mid-style. They are all-style. (S&P500, Russell 3000)

All-style dilutes active managers – it diminishes their merits. Mid-style completes active managers – it rounds out their merits.

Large Mid Sm 65% 25% 10% 225 Stocks 800 4000

Value40%

CentricCentricCore Core 20%20%

Growth40%

45 Names

$14 B $2B

Proprietary process assigns every publicly traded security into a style and capitalization category.◦ Capitalization: Top 65% of market capitalization

identified as large cap (approximately 225 stocks).◦ Style: Top 40% assigned to Growth, Bottom 40%

assigned to Value and remaining 20% assigned to Centric Core

Analyzed quarterly

Rebalanced quarterly

Neutral weight to Total Market index sectors

Equal weight within sectors

Moderate drift to value or growth permitted in order to reduce turnover.

Low cost trading

Tax enhanced availability

True core style and core capitalization

Complements, rather than dilutes, active managers

Market-like style locationMatch sector allocationsExclusively large companies

S&PTotal Market

Centric Core

S&PTotal Mkt

Centric Core

Mid Cap

Large Growth

Large Core

Large Value

Large Growth

Large Core

Large Value

Centric S&P Market

Sector AllocationsSector Allocationsas of June 30, 2011as of June 30, 2011

Energy Mkt Cap Consumer Discretionary Mkt Cap Consumer Staples Mkt CapApache 47.8 Disney Co 77.2 Avon Products 12.8Devon Energy 35.7 Home Depot 58.0 Coca-Cola Co 152.8Occidental Petroleum 87.7 Johnson Controls 26.9 Colgate Palmolive 42.8

News Corp 48.2Target Corp 34.1 Financials Mkt CapTime Warner 26.2 American Express 62.0

Industrials Mkt Cap TJX Cos. 20.5 BB&T 19.23M 67.1 BlackRock 39.5Canadian Natural 35.6 Information Technology Mkt Cap CME Group I 19.1CSX Corp 29.2 Ebay, Inc. 40.5 Marsh & Mcclen 16.8Eaton Corp 17.6 Hewlett Packard 79.5 Price Group 16.4Emerson Electric 41.1 Tyco Electric 16.2 Progressive Corp 14.2Honeywell 46.9Norfolk Southern 25.9 Health Care Mkt Cap Materials Mkt CapUnion Pacific 51.5 Amgen 56.5 Air Products 20.2United Parcel Services 72.6 Baxter Intl 34.0 Dow Chemical 42.5

Becton Dickinson 19.2 Southern Co. 29.4Telecommunication Services Mkt Cap Covidien 27.2 Teck Resources 31.1Public Service 17.0 McKEsson 21.6Rogers - B 20.9 Stryker 24.2

Representative HoldingsRepresentative Holdingsasof June 30, 2011asof June 30, 2011

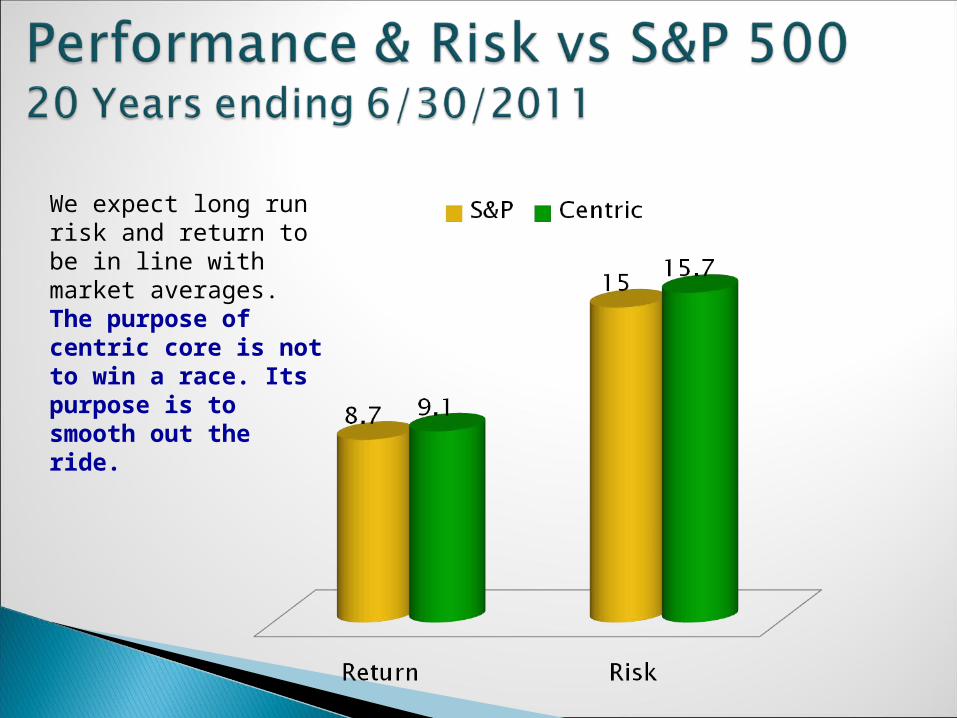

Centric Core is an index designed to capture an important part of the stock market. It is not designed to outperform anything.

We expect long run risk and return to be in line with market averages.The purpose of centric core is not to win a race. Its purpose is to smooth out the ride.

4.34

2.72

Staples Disc Health Matls Tech

Energy

Indus Utility Finance Total

Relative to S&P 500 Index Fund (IVV)

Active Return 16.19Excess Return 1.62Relative Return 1.60Standard Deviation 1.15Tracking Error 4.65

Consistency of Performance Periods Outperforming 58Periods Underperforming 50Consistency Ratio 0.54Up Market Capture 1.09Down Market Capture 1.01Downside Risk 2.78

Annualized Returns Centric Core 4.34%S&P 500 Index Fund (IVV) 2.72%

Regression Results Alpha 1.30Beta 1.12R-Squared 0.94Standard Deviation 19.13T-Value 1.10

Ratio's Information Ratio 0.35Sharpe Ratio 0.23Treynor Ratio 1.45

Higher ReturnsImproved Diversification

1. Basic: 4-Corner

2. Advanced, Level 1: Institutional Optimized Diversification

3. Advanced, Level 2: Sortino Optimized Desired Target Return

Value Growth

Large

Small

Cart before the Horse

Bad bet against the non-corners

Centric

Blend Core Dilutes active managers:S&P500 Russell 3000 Wilshire 5000 500 – 5000 Stocks

Centric Core Complements active managers:Surz Style Pure® Centric Core 45 Stocks

Blend CoreValue + Growth+

Everything Else

1. Develop talent pool: team of managers

2. Optimizer solves for most diversified allocation across team. Can be coupled with risk budgeting.

3. Add core diversifier: compare blend to centric

C o m p le tio n F u n d : S u r z C o r e -c e n tr ic

0

1 0

2 0

3 0

4 0

5 0

6 0

7 0

8 0

9 0

1 0 0

We

igh

t, %

J u n -0 1 D e c -0 2 D e c -0 3 D e c -0 4 D e c -0 5 D e c -0 6 D e c -0 7 D e c -0 8 D e c -0 9 M a r-1 1

Brown Advisory Growth Equity Instl P rudential Jennison Value A LWRoyce Total Return Instl Surz Large Core

C om ple tion Fund: S& P 500

0

1 0

2 0

3 0

4 0

5 0

6 0

7 0

8 0

9 0

1 0 0

We

igh

t, %

J u n -0 1 D e c -0 2 D e c -0 3 D e c -0 4 D e c -0 5 D e c -0 6 D e c -0 7 D e c -0 8 D e c -0 9 M a r-1 1

Brown Advisory Growth Equity Ins tl Prudential Jennison Value A LWRoyce Total Return Instl S&P 500 Index

Optimizer wants 80% in S&P500 but only 20% in Centric Core

S&P500

Centric Core

Optimizer wantsCentric Core buthas to take the entire S&P to getthe 20% it wants.

Centric Core islike the sweet fillingin a sandwich cookie and the S&P is like the entire cookie.

1. Develop talent pool: team of managers

2. Optimizer allocates to maximize achievement of DTR while simultaneously maintaining style neutrality.

3. Final step is filling in style voids, which usually calls for Centric Core.

1. Find Skill by Looking Everywhere, not Just Style Corners.

Use 21st Century tools. (Maximize)

CORE

2.Allocate to Skill to Maintain Diversification (Optimize).

Low correlation to stylesLittle overlap with active managersReturn history on most platformsModels on several UMA platforms

Enhanced Diversification Relative to: All-active construction Blend core – satellite, like S&P

Increased Returns Relative to: Blend core-satellite, like S&P Periods when centric core outperforms, like 2008, when unintended bet against centric penalized performance.

ProofStatement

Placemark

TD Ameritrade

Folio Dynamix

Smartleaf

Adhesion

MPI Zephyr PSN/Informa Morningstar Frontier/Sunguard Investment

Technologies Evestment Alliance First Rate PPCA

Blanchett, David. “Core Vs Blend.” Journal of Indexes, Jan-Feb 2011

Steyer, Robert. “Large-cap funds dominate DC index landscape.” Pensions & Investments, June 13, 2011

Surz, Ronald. “Refining Core-Satellite.” Journal of Performance Measurement, Fall 2010, and Advisor Perspectives, August 17, 2010

Rescue Your Investment Managers

From the SPDRs Web

The Little Index That Could.

45 stocks that improve both performance and diversification.