rockonomics: economics & public policy in the rock & roll industry economics of ticket...

TRANSCRIPT

Rockonomics: Economics & Public Policy in the Rock & Roll Industry

• Economics of Ticket Pricing

• Industry Trends

• Long-Run Explanations Superstar Model

Baumol & Bowen’s Disease Wealth Effects• Short-Run Explanations

Concentration Complimentary Goods Under Priced Asset

Alan B. Krueger

“Somebody said to me, ‘But the Beatles were antimaterialistic.’ That’s a huge myth. John and I literally used to sit down and say, ‘Now, let’s write a swimming pool.”

-- Paul McCartney

“[I]n some fashion, I help people hold on to their own humanity, if I'm doing my job right.”

-- Bruce Springsteen

“I don’t see how carving out the best seats and charging a lot more for them has anything to do with rock & roll.”

-- Tom Petty

• To maximize short run profit “Price Discriminate”

• Charge more to those who are less “price sensitive”

• Extreme example is variation in prices for airline seats

• Don’t go overboard because of tie-in sales & fan loyalty

Seven Lessons from Super Bowl SundayNew York Times

• List price was $325 in 2000; market price was around $2,500

• Secondary market develops if price too low, but its size can be exaggerated (20%)

• Endowment effect

• NFL could raise short-run profit by raising prices

• But NFL wants to reward loyal fans to build enterprise

• Besides, 60% of $4 billion of football revenue from TV

• “Gift Exchange”

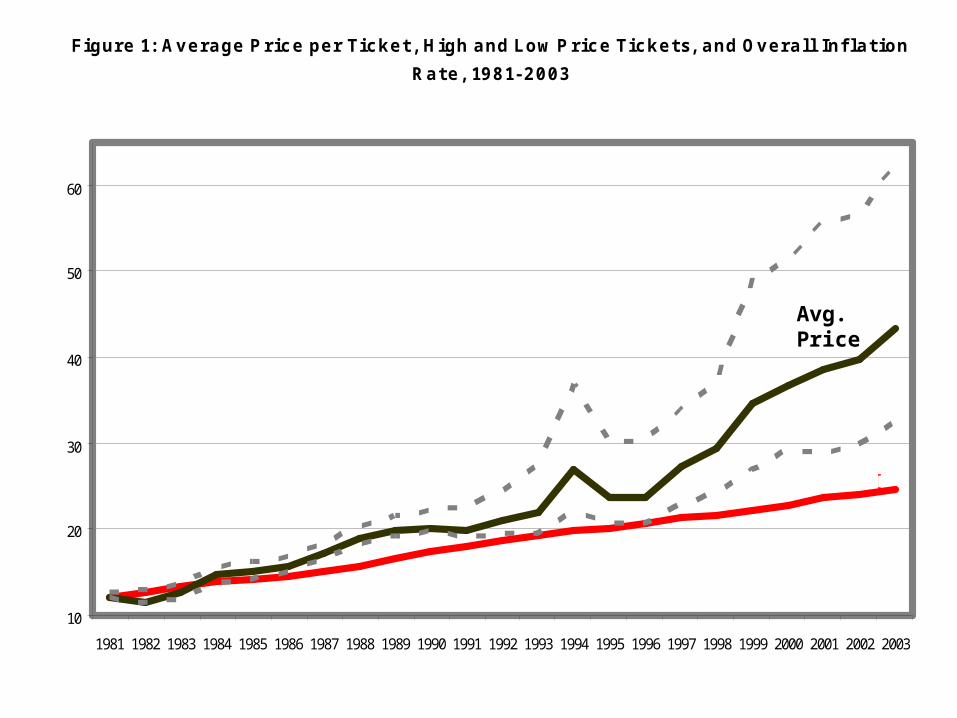

Figure 1: Average Price per Ticket and Overall Infl ation Rate, 1981-2003

10

20

30

40

50

60

1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

CPI

Avg.Price

Figure 1: Average Price per Ticket, High and Low Price Tickets, and Overall Infl ation

Rate, 1981-2003

10

20

30

40

50

60

1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

CPI

Avg.Price

0.301

0.255

0.207

0.620

0.206

0.243

0.1520.128

0.000

0.100

0.200

0.300

0.400

0.500

0.600

0.700

1981-86 1986-91 1991-96 1996-01Per iod

Avg. Ticket

CPI

Ticket Prices Soared Relative to Overall Price Inflation the Last 5 Years Proportionate Price Growth

Pro

port

iona

te G

row

th

© Alan B. Krueger, 2002.

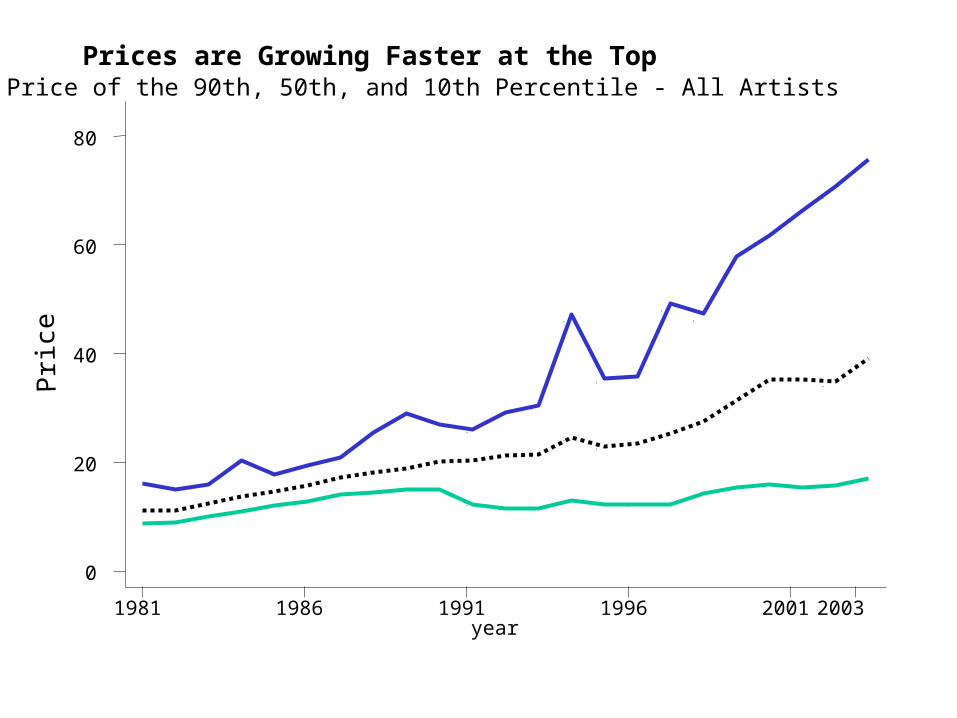

Price of the 90th, 50th, and 10th Percentile - All Artists

year1981 1986 1991 1996 2001 2003

0

20

40

60

80

Pri

cePrices are Growing Faster at the Top

Further Analysis

• October 2001 edition of Rolling Stone’s Encyclopedia of Rock and Roll

• Consistent universe of artists

• 1,786 artists, from Abba to ZZ Top; 1,274 in Pollstar database

• Responsible for 75% of ticket sales, 1981-2003.

• Merged on additional data: year formed; gender; genre; prominence (mm)

10

15

20

25

30

35

40

45

50

55

1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

EncyclopediaBands

Average

Grow atCPI

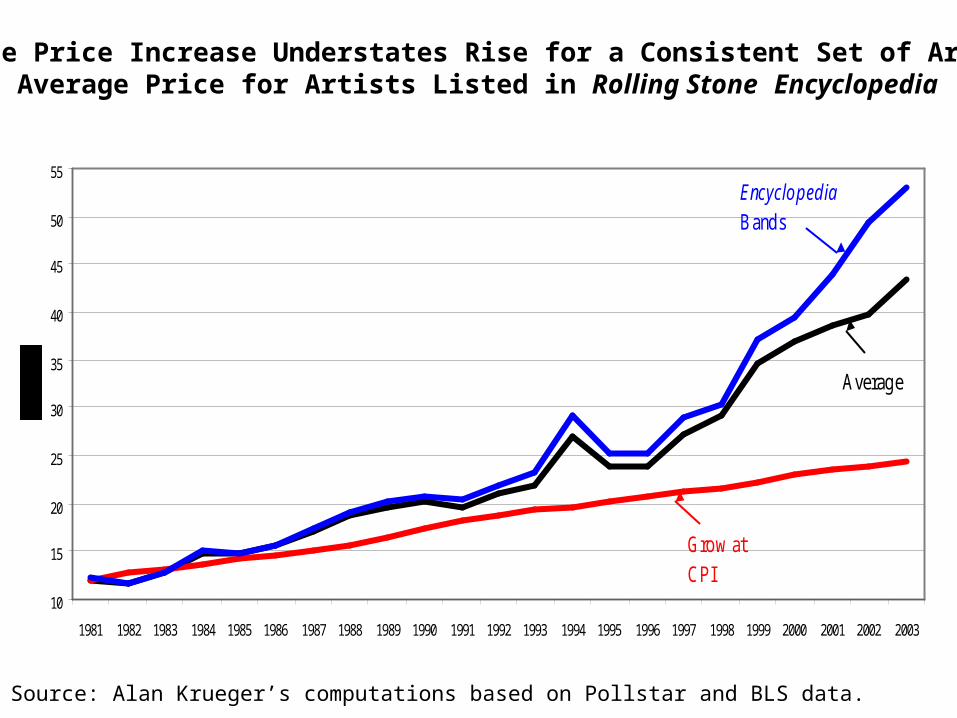

Average Price Increase Understates Rise for a Consistent Set of Artists Average Price for Artists Listed in Rolling Stone Encyclopedia

Source: Alan Krueger’s computations based on Pollstar and BLS data.

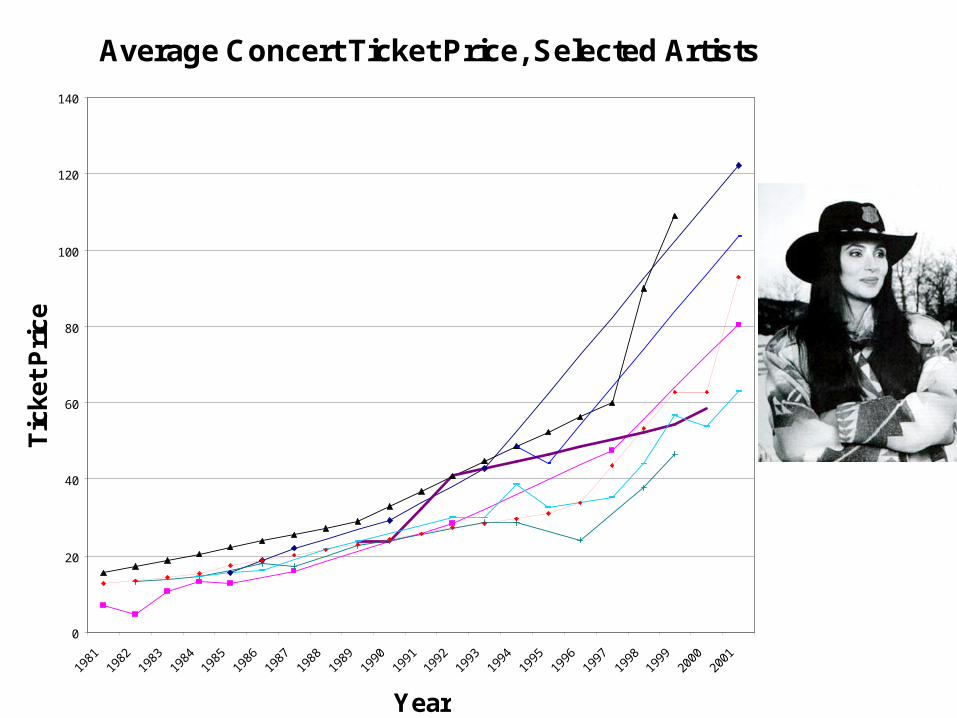

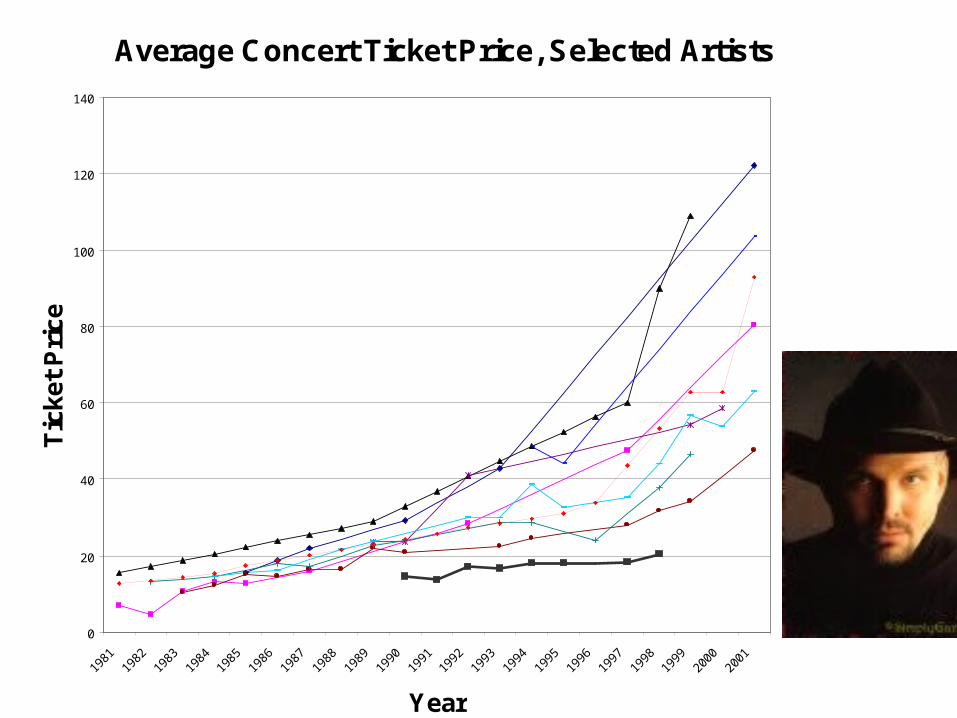

Average Concert Ticket Price, Selected Artists

0

20

40

60

80

100

120

140

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

Year

Tic

ket

Pri

ce

Average Concert Ticket Price, Selected Artists

0

20

40

60

80

100

120

140

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

Year

Tic

ket

Pri

ce

Average Concert Ticket Price, Selected Artists

0

20

40

60

80

100

120

140

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

Year

Tic

ket

Pri

ce

Average Concert Ticket Price, Selected Artists

0

20

40

60

80

100

120

140

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

Year

Tic

ket

Pri

ce

Average Concert Ticket Price, Selected Artists

0

20

40

60

80

100

120

140

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

Year

Tic

ket

Pri

ce

Average Concert Ticket Price, Selected Artists

0

20

40

60

80

100

120

140

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

Year

Tic

ket

Pri

ce

Average Concert Ticket Price, Selected Artists

0

20

40

60

80

100

120

140

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

Year

Tic

ket

Pri

ce

Average Concert Ticket Price, Selected Artists

0

20

40

60

80

100

120

140

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

Year

Tic

ket

Pri

ce

Average Concert Ticket Price, Selected Artists

0

20

40

60

80

100

120

140

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

Year

Tic

ket

Pri

ce

Average Concert Ticket Price, Selected Artists

0

20

40

60

80

100

120

140

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

Year

Tic

ket

Pri

ce

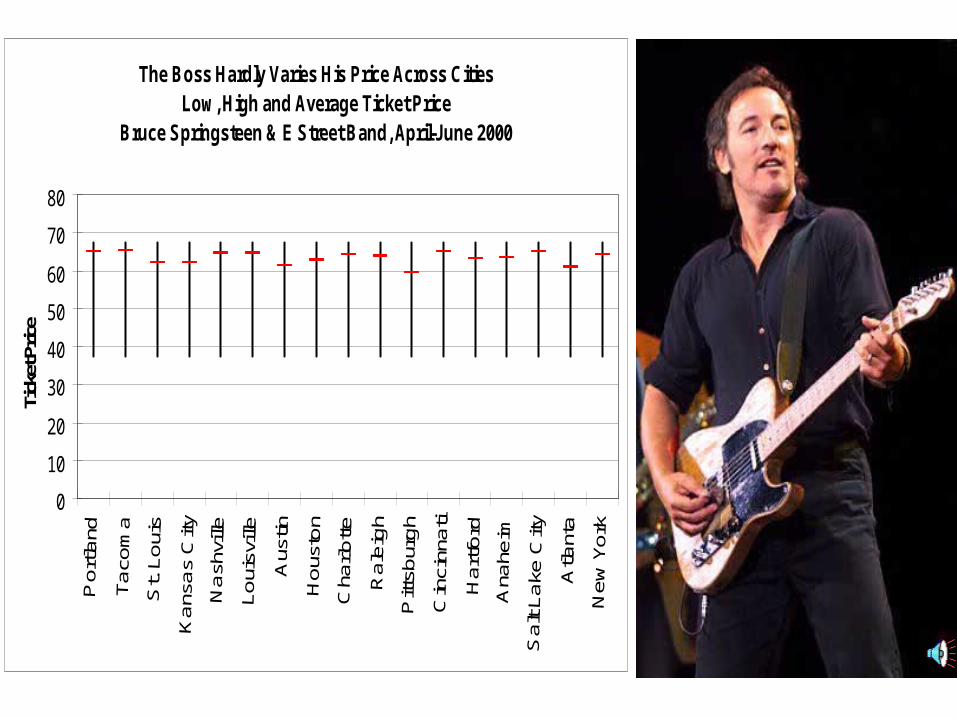

The Boss Hardly Varies His Price Across CitiesLow, High and Average Ticket Price

Bruce Springsteen & E Street Band, April-J une 2000

0

10

20

30

40

50

60

70

80

Tick

et P

rice

Figure 4a: Number of Shows Each YearRolling Stone Encyclopedia Artists

0

1000

2000

3000

4000

5000

6000

7000

8000

1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Num

ber

of S

how

s

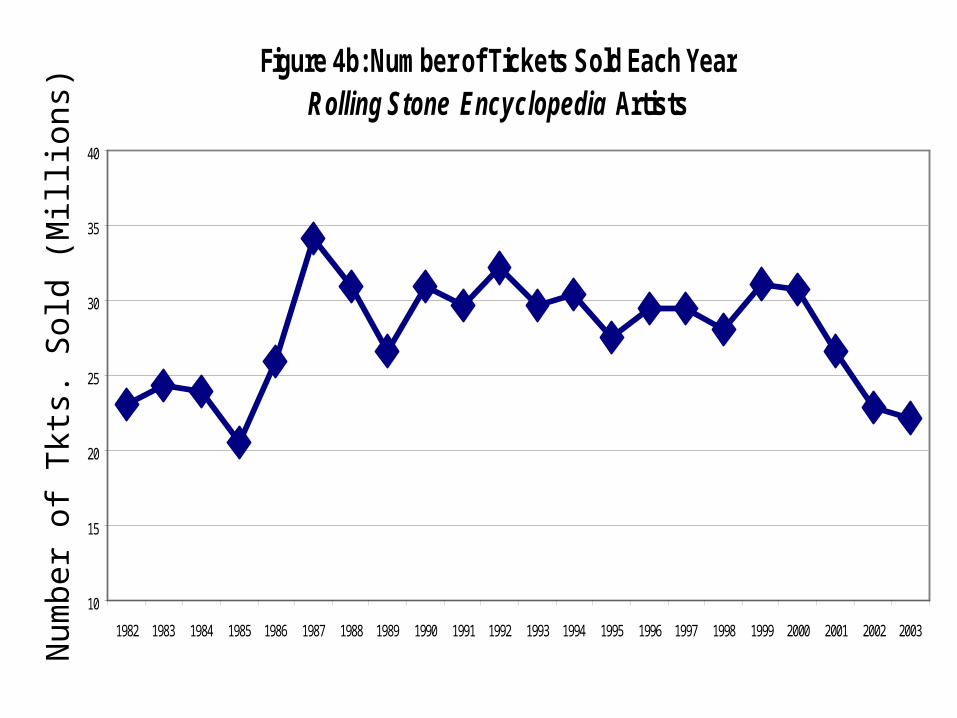

Figure 4b: Number of Tickets Sold Each YearRolling Stone Encyclopedia Artists

10

15

20

25

30

35

40

1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Num

ber

of T

kts.

Sol

d (M

illi

ons)

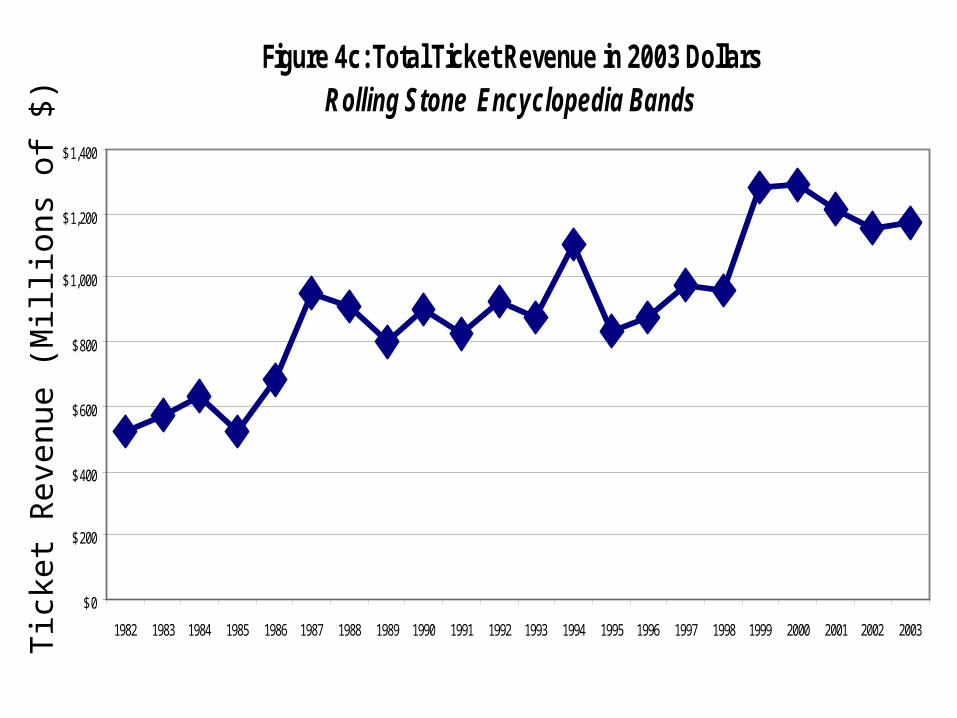

Figure 4c: Total Ticket Revenue in 2003 DollarsRolling Stone Encyclopedia Bands

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Tic

ket R

even

ue (

Mil

lion

s of

$)

Scalping and List Prices• Survey at Springsteen “The Rising” Concert, Oct. 6, 2003 in Philadelphia, PA. Every ticket sold for $75.

• Stratified random cluster sample of seats. Interviewed 858 people in the 15 minutes before the start of the show.

• Short questionnaire on index card. Very high response rate.

• 20-25 percent of tickets scalped. Worst seats more likely to be resold. Average resale price was $300.

• Springsteen gave away $3 million in consumer surplus

Explanations For Two Key Facts Need To Be Found:

• Long run faster growth in concert prices than inflation

• Short-run acceleration in prices the last 5 years

The Economics of Superstars • Sherwin Rosen (AER 1981) • If undergoing heart surgery,

willing to pay a lot more for the best surgeon over the second best surgeon

• Imperfect substitutes Convex reward function

• Plus, size of market Best can reach more customers

• Human capital would not have a linear effect – twice as good paid more than twice as much

• Superstars are known to a broader audience because of technology

• Improved technology differentiates the best from the rest and permits bigger audience (unlike Ms. Billington)

• Demand to hear the very best is higher

• Rewards for the best should rise

Apply to Rock & Roll

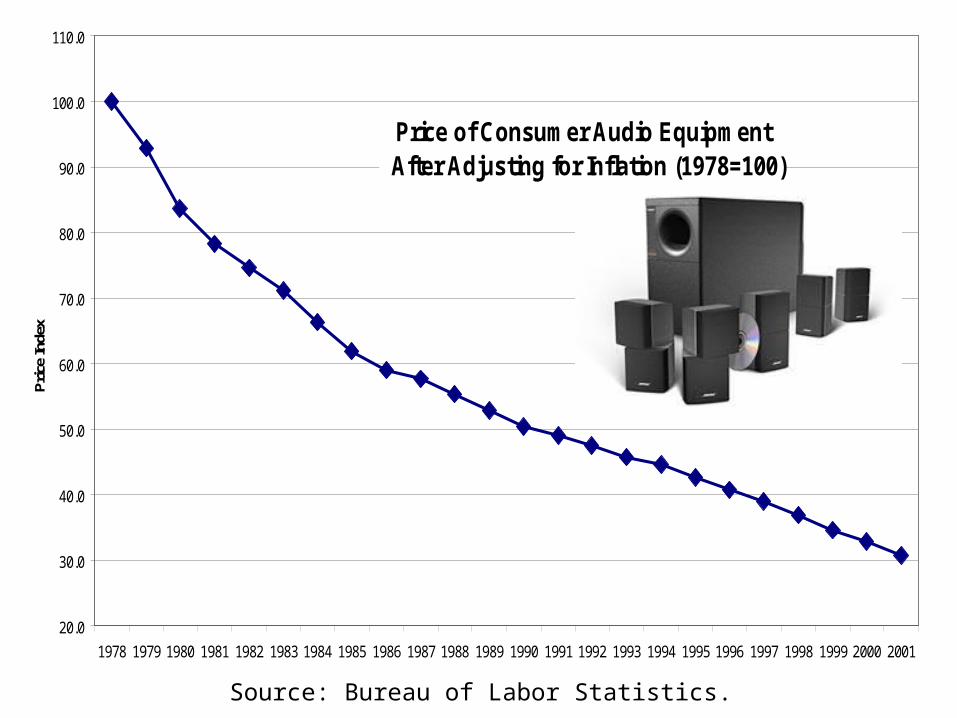

Price of Consumer Audio Equipment After Adjusting for Inflation (1978=100)

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

110.0

1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Pri

ce In

dex

Source: Bureau of Labor Statistics.

0%

20%

40%

60%

80%

100%

1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Year

The Top Artists are Getting a Larger Share of Total Ticket Revenue

Top 1 Percent

Top 2-5 Percent

Everybody Else

84%

Source: Calculated by Alan Krueger based on Pollstar data.

56%

Top 1% 14.6%

26%

62%

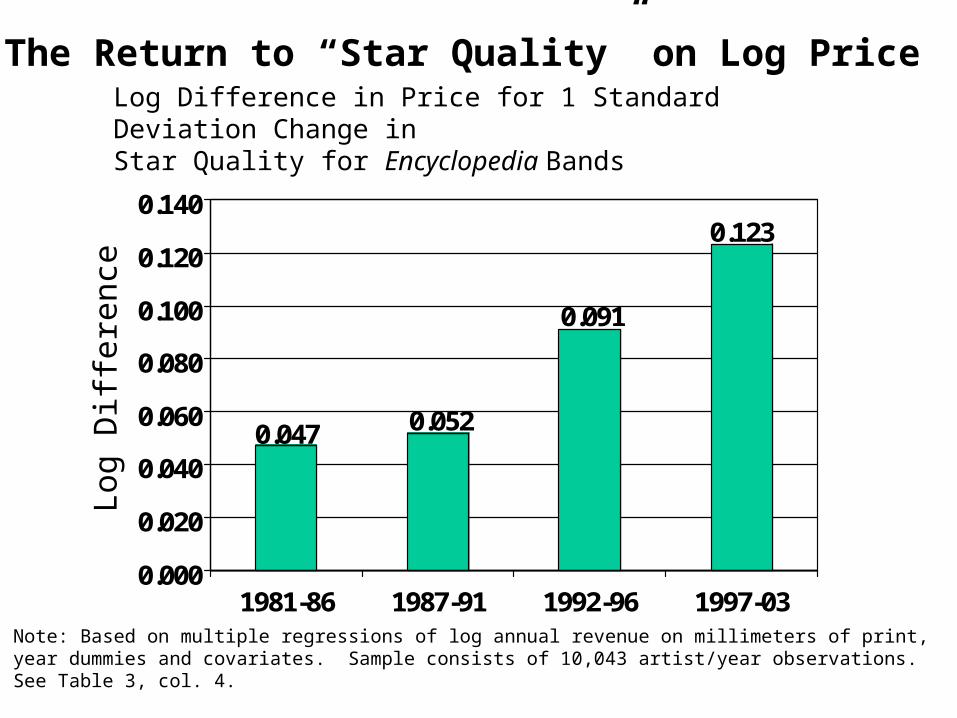

Novel measure of “Star Quality”:

Amount written about artist in Rolling Stone’sEncyclopedia of Rock & Roll

Measured in millimeters to be scientific

399 mm

0.047 0.052

0.091

0.123

0.000

0.020

0.040

0.060

0.080

0.100

0.120

0.140

1981-86 1987-91 1992-96 1997-03

Log Difference in Price for 1 Standard Deviation Change in Star Quality for Encyclopedia Bands

The Return to “Star Quality” on Log PriceL

og D

iffe

renc

e

Note: Based on multiple regressions of log annual revenue on millimeters of print, year dummies and covariates. Sample consists of 10,043 artist/year observations. See Table 3, col. 4.

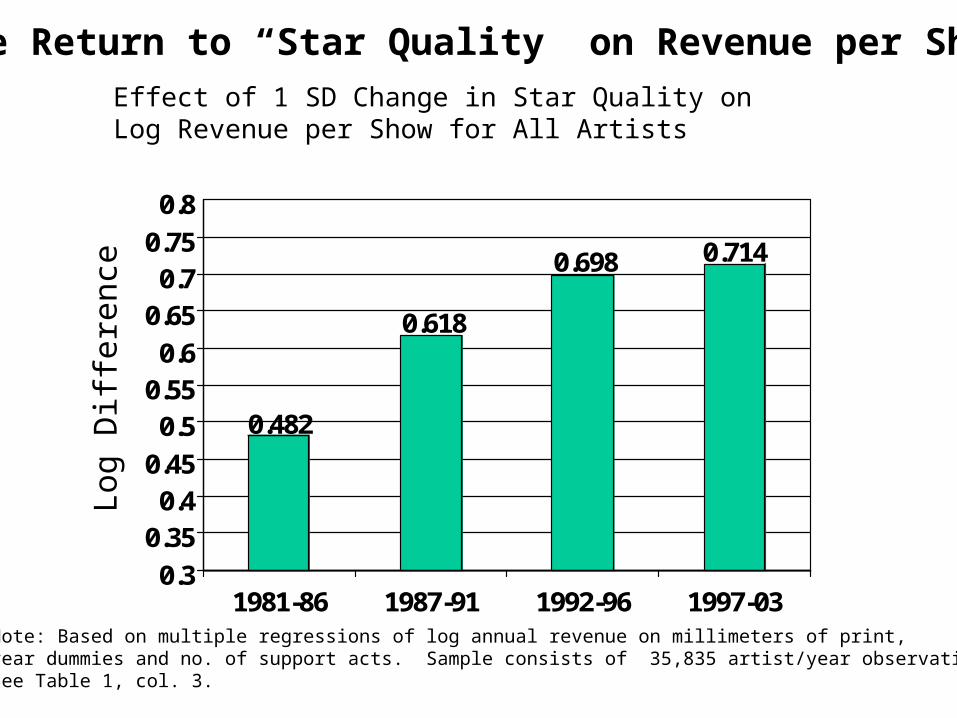

0.482

0.618

0.698 0.714

0.3

0.350.4

0.45

0.50.550.6

0.650.7

0.75

0.8

1981-86 1987-91 1992-96 1997-03

Effect of 1 SD Change in Star Quality on Log Revenue per Show for All Artists

The Return to “Star Quality” on Revenue per Show

Log

Dif

fere

nce

Note: Based on multiple regressions of log annual revenue on millimeters of print, year dummies and no. of support acts. Sample consists of 35,835 artist/year observations. See Table 1, col. 3.

0.492

0.532 0.528

0.440

0.3

0.35

0.4

0.45

0.5

0.55

0.6

1981-86 1987-91 1992-96 1997-03

Effect of 1 SD Change in Star Quality on Log Revenue per Show for Encyclopedia Bands

The Return to “Star Quality” on Revenue per Show

Log

Dif

fere

nce

Note: Based on multiple regressions of log annual revenue on millimeters of print, year dummies and covariates. Sample consists of 10,043 artist/year observations. \See Table 3, col. 6.

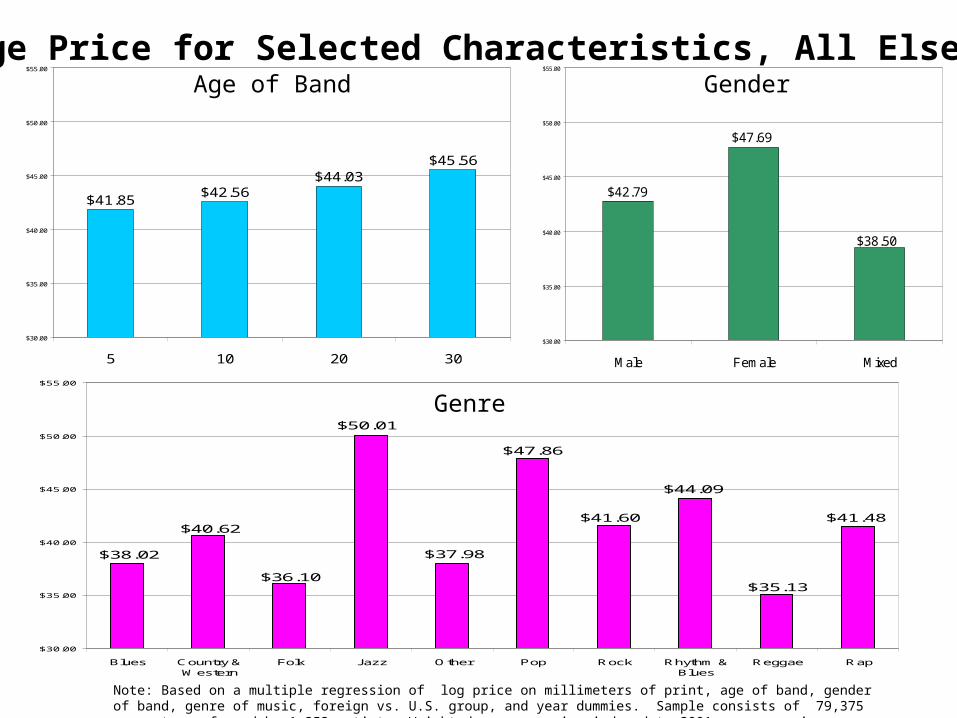

$42.79

$47.69

$38.50

$30.00

$35.00

$40.00

$45.00

$50.00

$55.00

Male Female Mixed

GenderAge of Band

Genre

Note: Based on a multiple regression of log price on millimeters of print, age of band, gender of band, genre of music, foreign vs. U.S. group, and year dummies. Sample consists of 79,375 concerts performed by 1,253 artists. Weighted average price indexed to 2001 average price.

Average Price for Selected Characteristics, All Else Equal

$41.85$42.56

$44.03$45.56

$30.00

$35.00

$40.00

$45.00

$50.00

$55.00

5 10 20 30

$36.10

$40.62

$38.02

$50.01

$37.98

$47.86

$41.60

$44.09

$35.13

$41.48

$30.00

$35.00

$40.00

$45.00

$50.00

$55.00

Blues Country &Western

Folk Jazz Other Pop Rock Rhythm &Blues

Reggae Rap

Tina Turner: What’s Age Got to Do With It?As Artists Age, the High-Low Ticket Price Ratio Rises

Rat

io o

f H

igh

to L

ow

Pric

e

1982 1986 1991 1996 2000

1

1.5

2

2.5

Baumol and Bowen’s Disease• Takes same amount of time

and input to play Free Bird

• Concerts are a low productivity growth sector (modular technological change)

• Would expect prices in low productivity growth sectors to grow relatively quickly

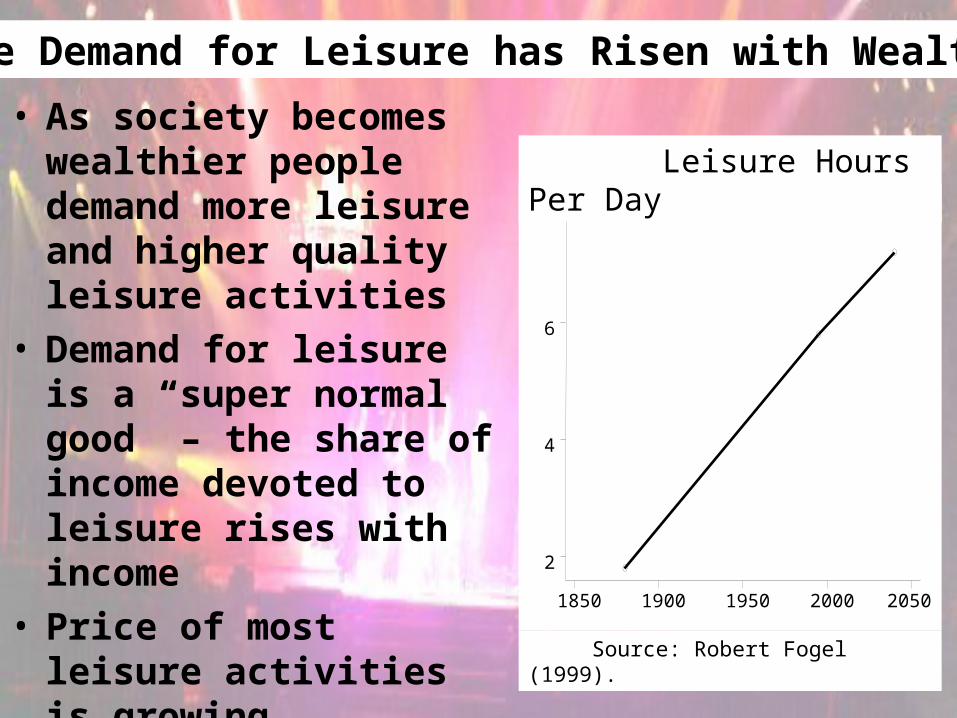

• As society becomes wealthier people demand more leisure and higher quality leisure activities

• Demand for leisure is a “super normal good” – the share of income devoted to leisure rises with income

• Price of most leisure activities is growing relatively fast

• The demand for leisure is likely to continue to grow

The Demand for Leisure has Risen with Wealth

1850 1900 1950 2000 2050

2

4

6

8

Leisure Hours Per Day

Source: Robert Fogel (1999).

Concert Tickets versus Movie, Theater, and Sports TicketsConcert Venue Price Index versus CPI for Movie, Theater and Sports Events

0.427

0.278

0.207

0.546

0.3320.358

0.252 0.241

0.000

0.100

0.200

0.300

0.400

0.500

0.600

1981-86 1986-91 1991-96 1996-01

Per iod

Concerts

Movies, Sports & Theater

Prop

orti

onat

e G

row

th in

Pri

ce

© Alan B. Krueger, 2002.

What Explains Recent Price Growth?

• Production Costs Increased

• Consolidation

• Decline in Complementary Revenue Source: Record Sales

• Undervalued Asset

Industry Consolidation

• Vertical Concentration

- Venues

- Radio

- Marketing, etc.• Horizontal

Concentration - SFX, Clear Channel

ClearChannel

Telecommunications Act of 1996• Signed Feb. 8, 1996• Prior to 1996 Act, radio

stations could own just 40 stations nationally, and 2 in a market

• Cap eliminated nationwide, and raised to 8 in a market

• Since 1996, 10,000 radio station transactions worth $100 billion

• Further legislation could lead to consolidation with TV and newspapers

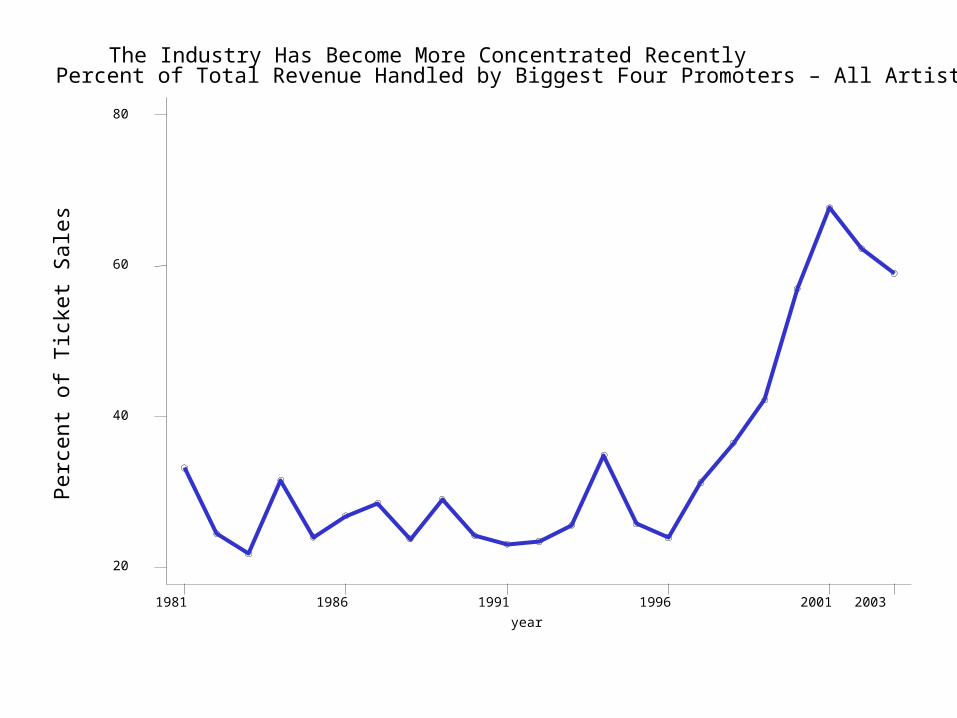

The Industry Has Become More Concentrated RecentlyPercent of Total Revenue Handled by Biggest Four Promoters – All Artists

year

1981 1986 1991 1996 2001 2003

20

40

60

80

Per

cent

of T

icke

t Sal

es

1981 1986 1991 1996 2001 2003

20

40

60

80

Nationally, the Industry Has Become More Concentrated RecentlyPercent of Total Revenue Handled by Biggest Four Promoters - Top Artists

Per

cent

of T

icke

t Sal

es

Source: Calculated by Alan Krueger based on Pollstar data. Only concerts performed in theU.S. are included in the analysis. Sample consists of artists listed in Rolling Stone Encyclopedia.

41%CC

Figure 4a: Number of Shows Each YearRolling Stone Encyclopedia Artists

0

1000

2000

3000

4000

5000

6000

7000

8000

1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Num

ber

of S

how

s

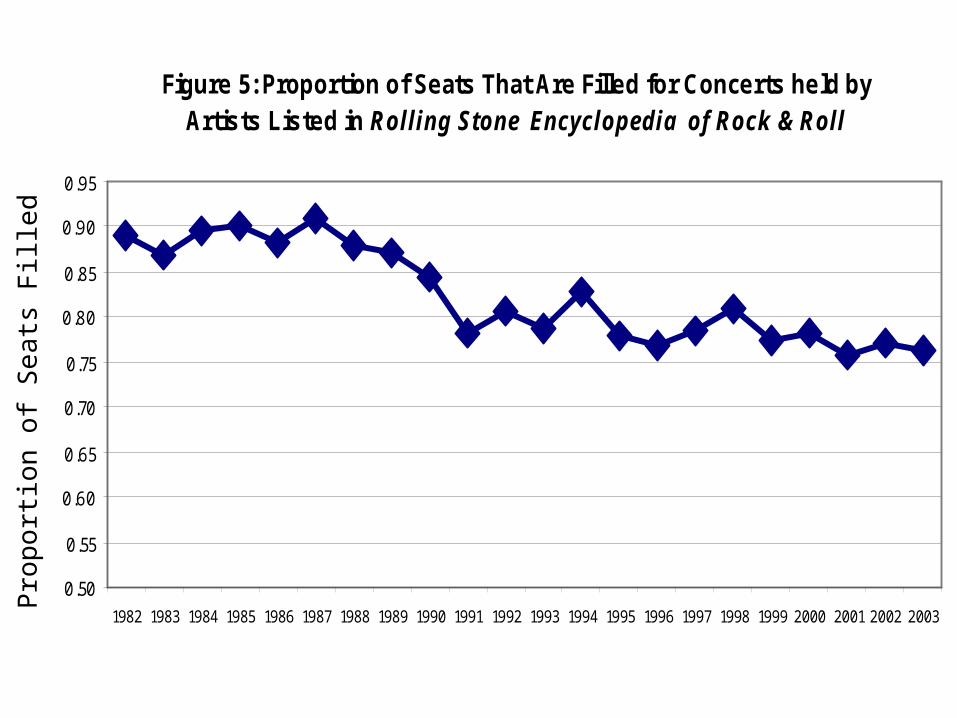

Figure 5: Proportion of Seats That Are Filled for Concerts held byArtists Listed in Rolling Stone Encyclopedia of Rock & Roll

0.50

0.55

0.60

0.65

0.70

0.75

0.80

0.85

0.90

0.95

1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Pro

port

ion

of S

eats

Fill

ed

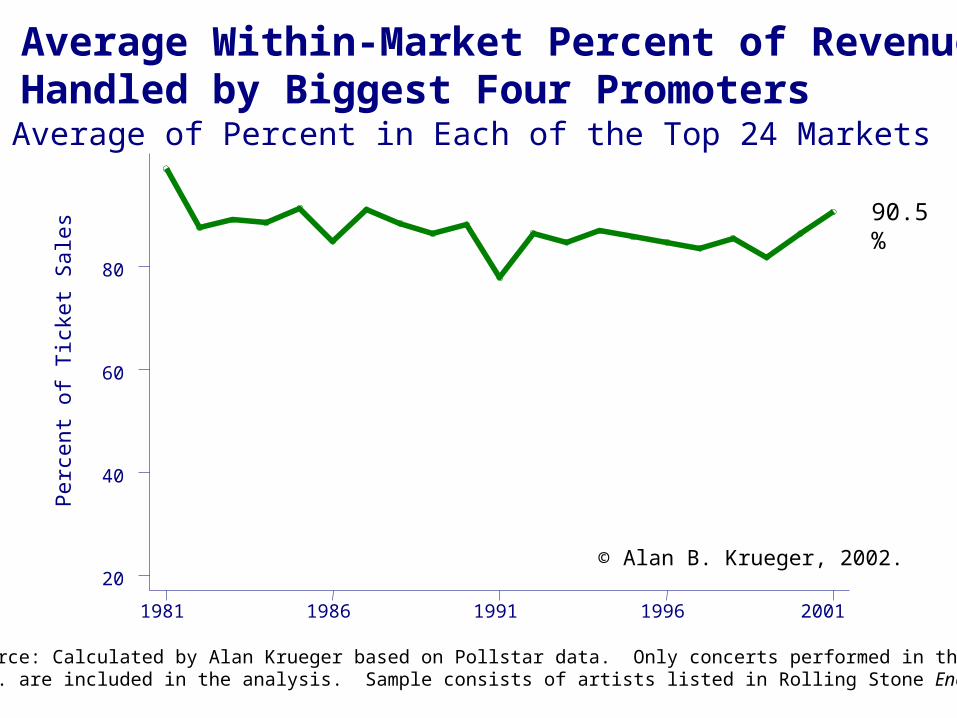

90.5%

Average Within-Market Percent of Revenue Handled by Biggest Four Promoters

Average of Percent in Each of the Top 24 Markets

Per

cent

of

Tic

ket S

ales

1981 1986 1991 1996 2001

20

40

60

80

Source: Calculated by Alan Krueger based on Pollstar data. Only concerts performed in theU.S. are included in the analysis. Sample consists of artists listed in Rolling Stone Encyclopedia.

© Alan B. Krueger, 2002.

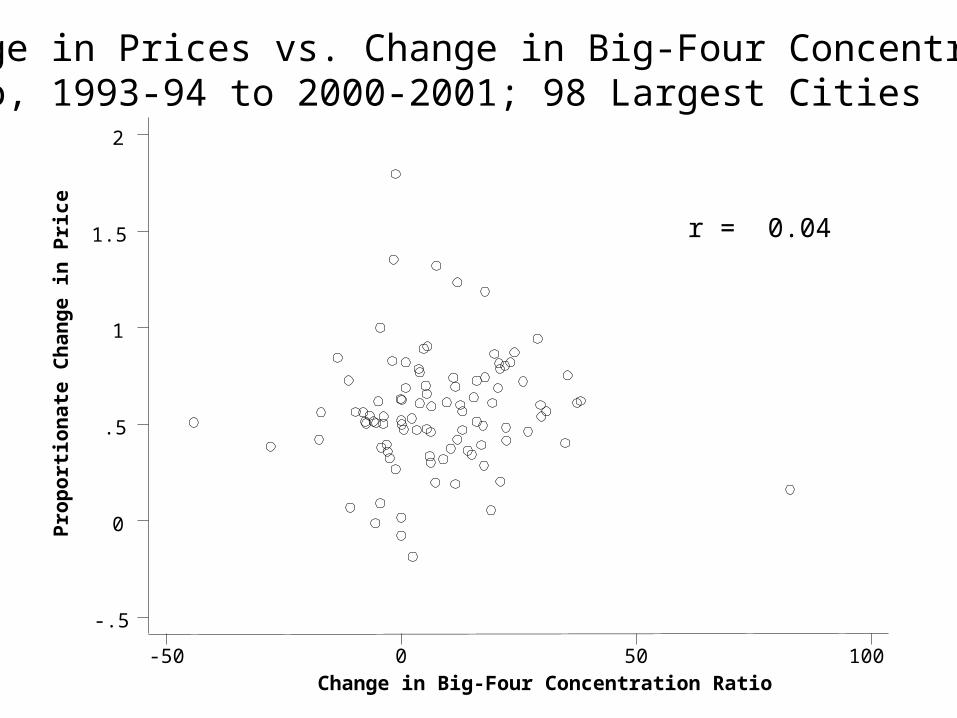

Change in Big-Four Concentration Ratio

-50 0 50 100

-.5

0

.5

1

1.5

2

r = 0.04

Change in Prices vs. Change in Big-Four Concentration Ratio, 1993-94 to 2000-2001; 98 Largest Cities

Pro

po

rtio

na

te C

ha

ng

e i

n P

ric

e

Sh

are

of

Co

nc

ert

Re

ve

nu

e,

20

00

-01

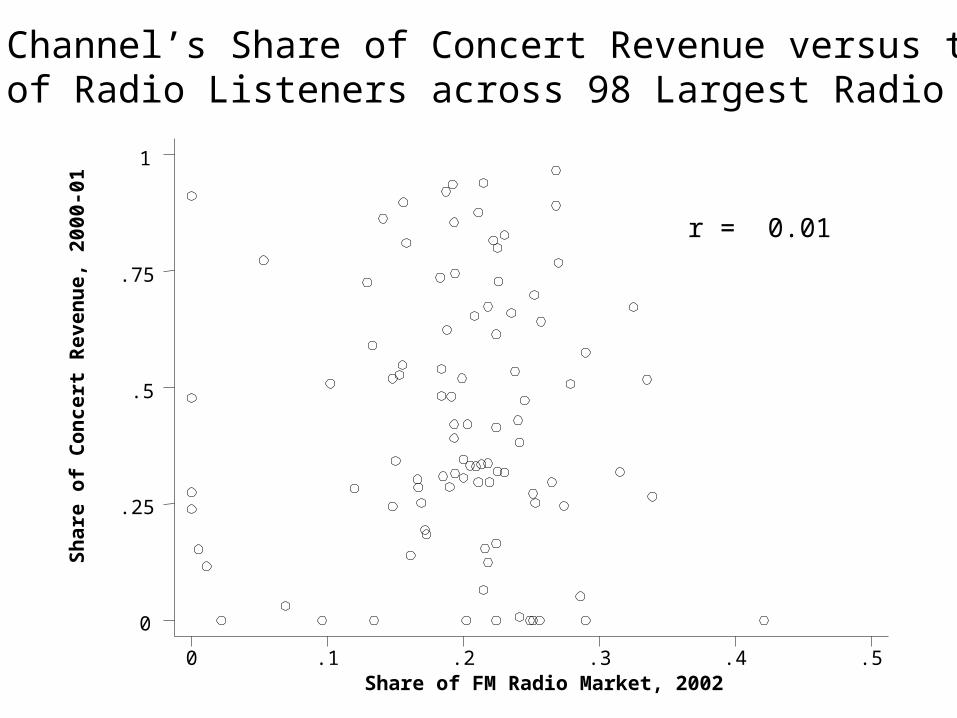

Share of FM Radio Market, 20020 .1 .2 .3 .4 .5

0

.25

.5

.75

1

Clear Channel’s Share of Concert Revenue versus theirShare of Radio Listeners across 98 Largest Radio Markets

r = 0.01

1986 1991 1996 2001

1000

2000

3000

4000

5000

6000

Herfindahl-Hirschman Index for Venues, 1986-2001

Note: Venues that are exclusively used by one promoter in a year in a particular cityare pooled together into one conglomerate. An industry with an HHI above 1,8000is considered highly concentrated according to the Justice Department Merger Guidelines.

Average Across 24 Largest CitiesA

vera

ge H

HI

$0

$10

$20

$30

$40

$50

1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Pric

e (U

S D

olla

rs)

Surge in Average Price Per Concert Ticket in Canada is Similar to that in the United States – 67% Nominal Growth from 1996 to 2001

Grow at U.S. CPI

Avg.Price

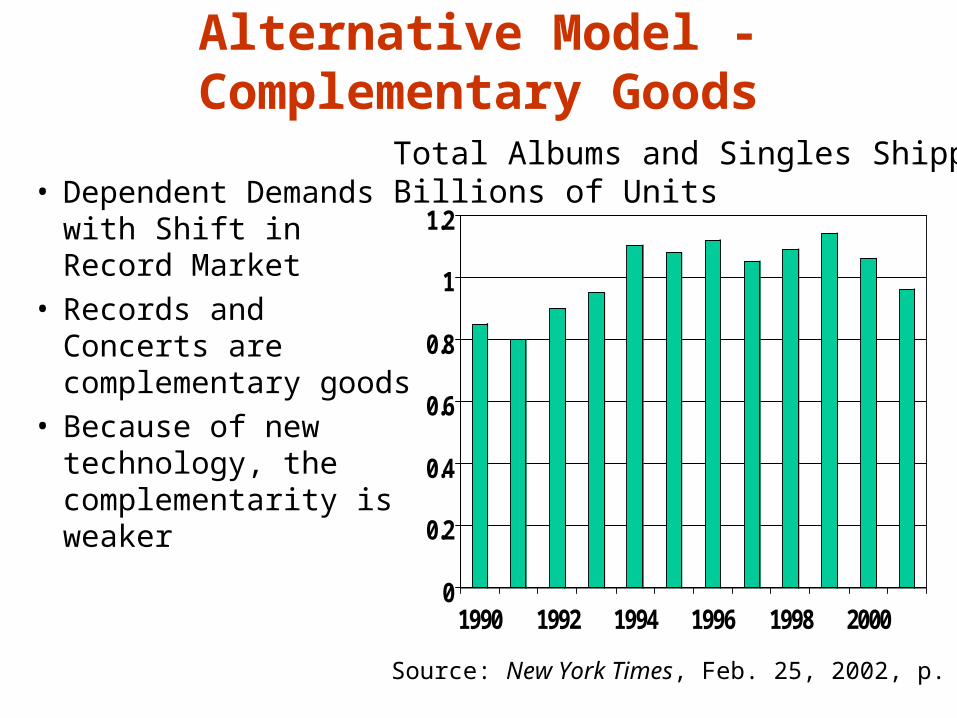

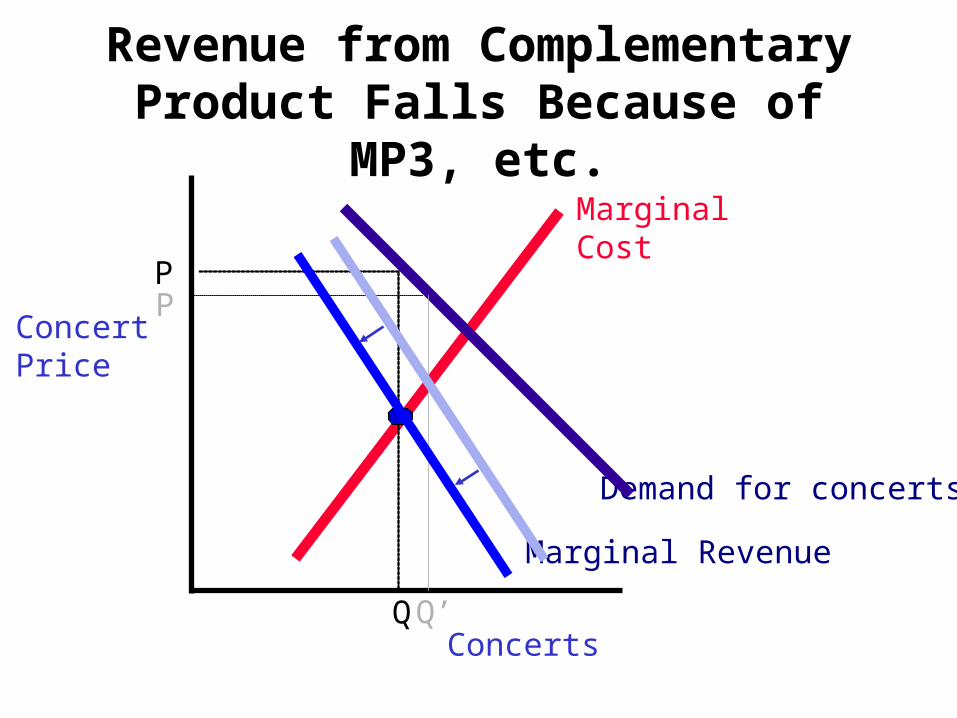

Alternative Model - Complementary Goods

• Dependent Demands with Shift in Record Market

• Records and Concerts are complementary goods

• Because of new technology, the complementarity is weaker 0

0.2

0.4

0.6

0.8

1

1.2

1990 1992 1994 1996 1998 2000

Source: New York Times, Feb. 25, 2002, p. C1.

Total Albums and Singles Shipped Billions of Units

Music shipments were down an estimated 9.6 percent last year, after declining 7 percent in 2000. Sales were flat 1994 to2000.

pDCpDCpDpDp 22112211 pmax

11

122'22

111

'11 1

11 Dp DCp

pCp

Bands Produce 2 Complementary Goods with Market Power

Good 1: Concert TicketsGood 2: Record Sales

“Music itself is going to become like running water or electricity. So it’s like, just take advantage of these lastfew years because none of this is ever going to happen again. You’d better be prepared for doing a lot of touring because that’s really the only unique situation that’s going to be left. It’s terribly exciting. But on the other hand it doesn’t matter if you think it’s exciting or not; it’s what’s going to happen.”

David Bowie The New York Times

June 9, 2002

11

122'22

111

'11 1

11Dp DCp

pCp

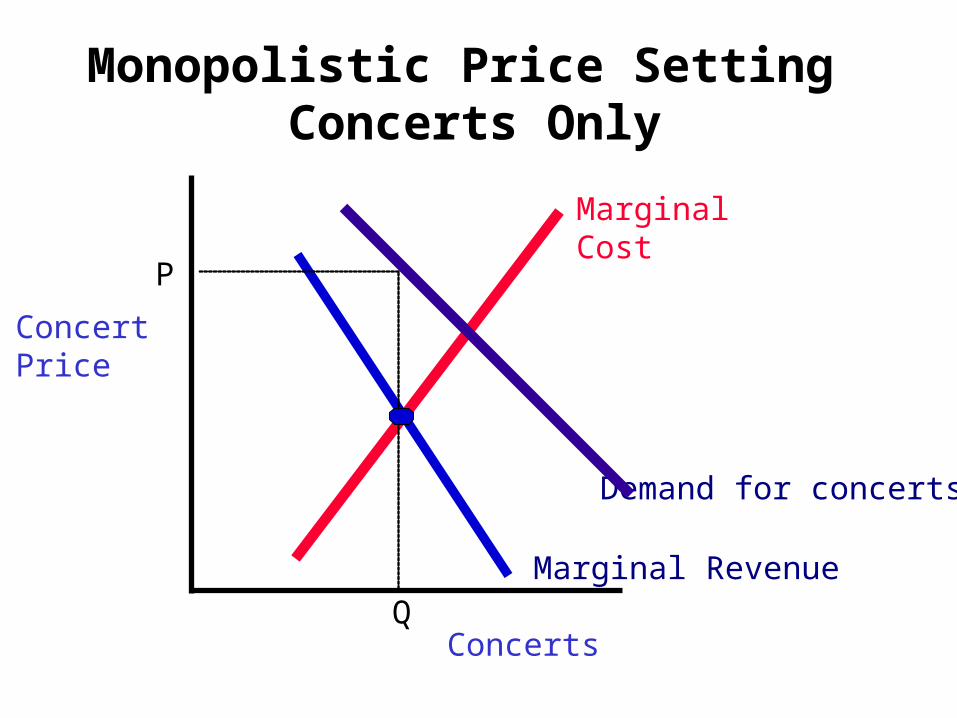

Monopolistic Price Setting Concerts Only

Marginal Cost

Concerts

ConcertPrice

Demand for concerts

Marginal Revenue

P

Q

Marginal Cost

Concerts

ConcertPrice

Demand for concerts

Marginal Revenue

P

Q

P’

Q’

Monopolistic Price Setting with Complementary Product: Records

Marginal Cost

Concerts

ConcertPrice

Demand for concerts

Marginal Revenue

Q

P

Q’

Revenue from Complementary Product Falls Because of MP3, etc.

P

Price Growth by Genre,1996-2001

23.4%

45.0% 47.7%55.6%

74.1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Jazz &Blues

Reggae &Other

Folk &Country

Rap & R&B Pop & Rock

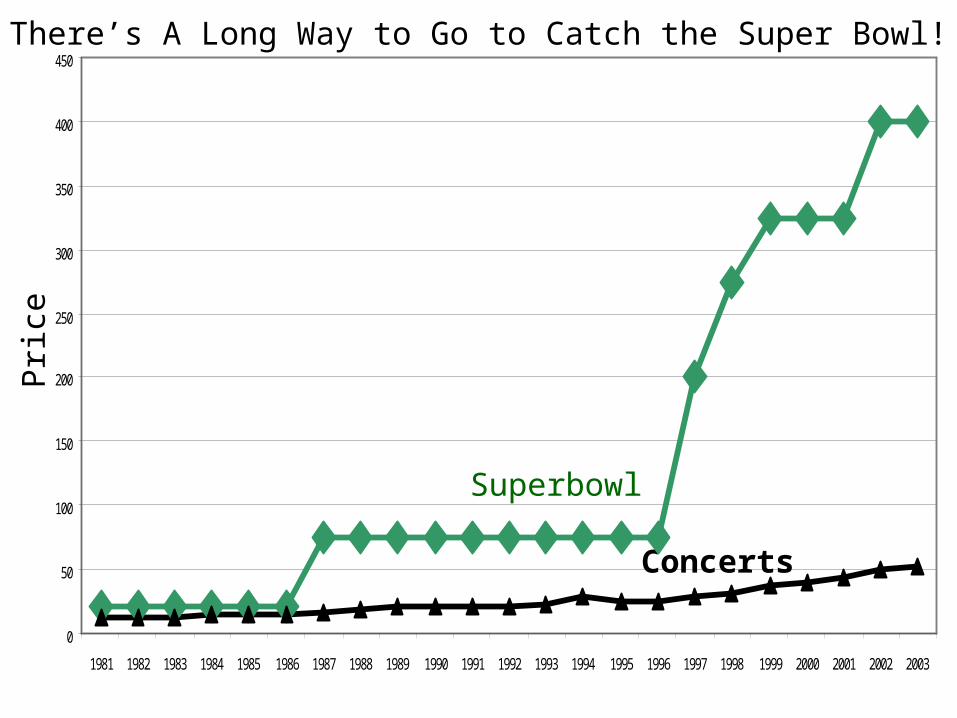

Superbowl

Concerts

There’s A Long Way to Go to Catch the Super Bowl!P

rice

0

50

100

150

200

250

300

350

400

450

1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Conclusions• Rising superstar effects, but

not accelerating

• To understand the market must understand industrial organization and technology

• Legal changes that allowed Clear Channel to dominate industry may be overrated

• Antitrust action in future? Revised Telecom Act?

• Complementarities between concerts and album sales key to market for Rock Stars?