robo advice: revenge of the incumbents (myvest and aite invest session)

TRANSCRIPT

Presented at:

July 12, 2017

ROBO-ADVICE:REVENGE OF THE

INCUMBENTS

Aite (pronounced “eye-tay”) Group is an independent research and advisory firm focused on business, technology, and regulatory issues and their impact on the financial services industry.

A fintech pioneer headquartered in the heart of San Francisco, MyVest combines best practices in wealth management with best-in-class technology. Our cloud-based platform enables holistic, client-centric wealth management across the enterprise in a single, unified system.

Alois PirkerResearch Director,Wealth Management

Anton HonikmanCEO

© 2017 MyVest Corporation. All Rights Reserved.

Type Definition % of Population

Wirehouse Merrill Lynch, UBS, Wells Fargo Advisors, Morgan Stanley 8%

Independent RIAMostly small firms but also have RIA groups working within larger broker-dealer firms

16%

FA with otherself-clearing firm

Large / regional players: e.g., Ameriprise, Edward Jones, Raymond James, LPL, RBC

13%

FA with online broker

Schwab, Fidelity, TD Ameritrade on the retail side (fewer than 2,000 advisors) 10%

FA with insurance BD

e.g. AXA, Northwestern (fewer than 10K advisors, some with more than 5K) 15%

FA with independent BD

e.g. Commonwealth Financial, ING (fewer than 5,000 advisors) 14%

FA with bank BD e.g. PNC, M&T Bank (fewer than 1,000 advisors) 8%

FA with private bank / bank trust

e.g. Northern Trust, US Trust, Bessemer Trust 16%

2 Annual Survey of 400 Advisors1 Qualitative Interviews

In-depth interviews with a variety of industry participants:

• Executives at financial institutions

• Financial advisors

• Executives at fintech firms

• Start-up firms and disruptors

“We take a topic and look at it from both sides, and that gives us a sense of what's happening in the market.”

- Alois Pirker, Aite Group

Aite Group Methodology

© 2017 MyVest Corporation. All Rights Reserved.

How Did We Get Here?

The Evolution of Robo-Advice

Traditional wealth

management is under

pressure

Profitability

Competition

Demographic shifts

Regulatory uncertainty

Legacy technology & business model

1996 Today

Ove

rall

Adop

tion

B2B for Enterprise 1.0

Quick WinsSimplicity, UX

B2B for Enterprise 2.0

Hybrid Human+Tech Multi-Segment

+

+

PioneersEarly Niches

B2C 1.0Retail Disrupters

B2B for Independent

AdvisorsDisrupt RIA Vendors

B2C Pivots to B2B

B2C 2.0Retail Response

Evolution: From robo-advice to digital wealth

© 2017 MyVest Corporation. All Rights Reserved.

1996 Today

Ove

rall

Adop

tion

B2B for Enterprise 1.0

Quick WinsSimplicity, UX

B2B for Enterprise 2.0

Hybrid Human+Tech Multi-Segment

+

+

PioneersEarly Niches

B2C 1.0Retail Disrupters

B2B for Independent

AdvisorsDisrupt RIA Vendors

B2C Pivots to B2B

B2C 2.0Retail Response

Evolution: From robo-advice to digital wealth

© 2017 MyVest Corporation. All Rights Reserved.

“B2B for Enterprise 1.0 is a quick win; B2B for Enterprise 2.0 is about strategic

business transformation.”

- Alois Pirker, Aite Group

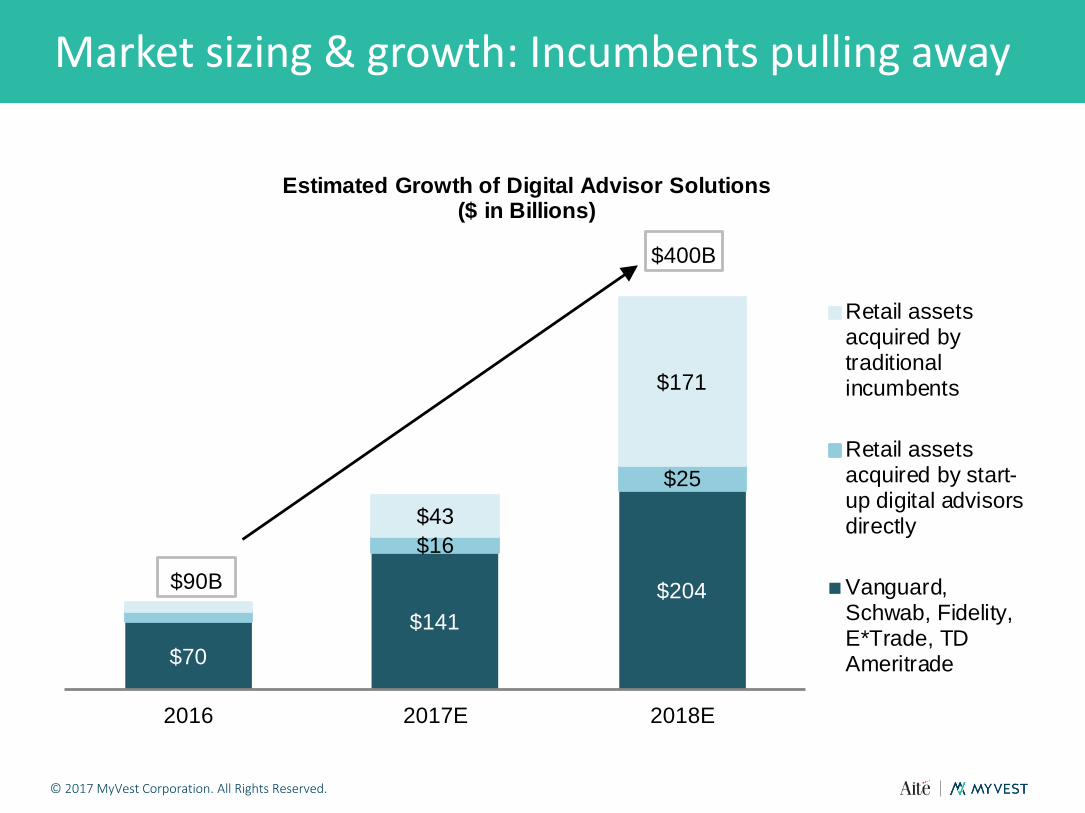

$70$141

$204

$16

$25

$43

$171

2016 2017E 2018E

Estimated Growth of Digital Advisor Solutions ($ in Billions)

Retail assetsacquired bytraditionalincumbents

Retail assetsacquired by start-up digital advisorsdirectly

Vanguard,Schwab, Fidelity,E*Trade, TDAmeritrade

$400B

$90B

Market sizing & growth: Incumbents pulling away

© 2017 MyVest Corporation. All Rights Reserved.

$70$141

$204

$16

$25

$43

$171

2016 2017E 2018E

Estimated Growth of Digital Advisor Solutions ($ in Billions)

Retail assetsacquired bytraditionalincumbents

Retail assetsacquired by start-up digital advisorsdirectly

Vanguard,Schwab, Fidelity,E*Trade, TDAmeritrade

$400B

$90B

Market sizing & growth: Incumbents pulling away

© 2017 MyVest Corporation. All Rights Reserved.

“Banks and insurance firms will challenge this $171 billion growth

segment.”

- Anton Honikman, MyVest

3%

16%

31%

23%

13%15%

5%

15%13%

32%

20%

15%

Practice hasmade the

decision tolaunch a digitaladvisor service

Very interested Interested Somewhatinterested

Not interested We have notdiscussed

this/thoughtabout this

Q2 2017 Q3 2015

50% interested or

ready to adopt

(up from 33%)

Source: Aite Group survey of 369 financial advisors, Q2 2017 and 403 financial advisors, Q3 2015.

Q: How interested is your practice in leveraging new digital advisor technology over the next few years?

Advisor interest in new technology

© 2017 MyVest Corporation. All Rights Reserved.

3%

16%

31%

23%

13%15%

5%

15%13%

32%

20%

15%

Practice hasmade the

decision tolaunch a digitaladvisor service

Very interested Interested Somewhatinterested

Not interested We have notdiscussed

this/thoughtabout this

Q2 2017 Q3 2015

50% interested or

ready to adopt

(up from 33%)

Source: Aite Group survey of 369 financial advisors, Q2 2017 and 403 financial advisors, Q3 2015.

Q: How interested is your practice in leveraging new digital advisor technology over the next few years?

Advisor interest in new technology

© 2017 MyVest Corporation. All Rights Reserved.

“The sands are shifting. The fastest growing advisors see the

opportunity in new technology.”

- Alois Pirker, Aite Group

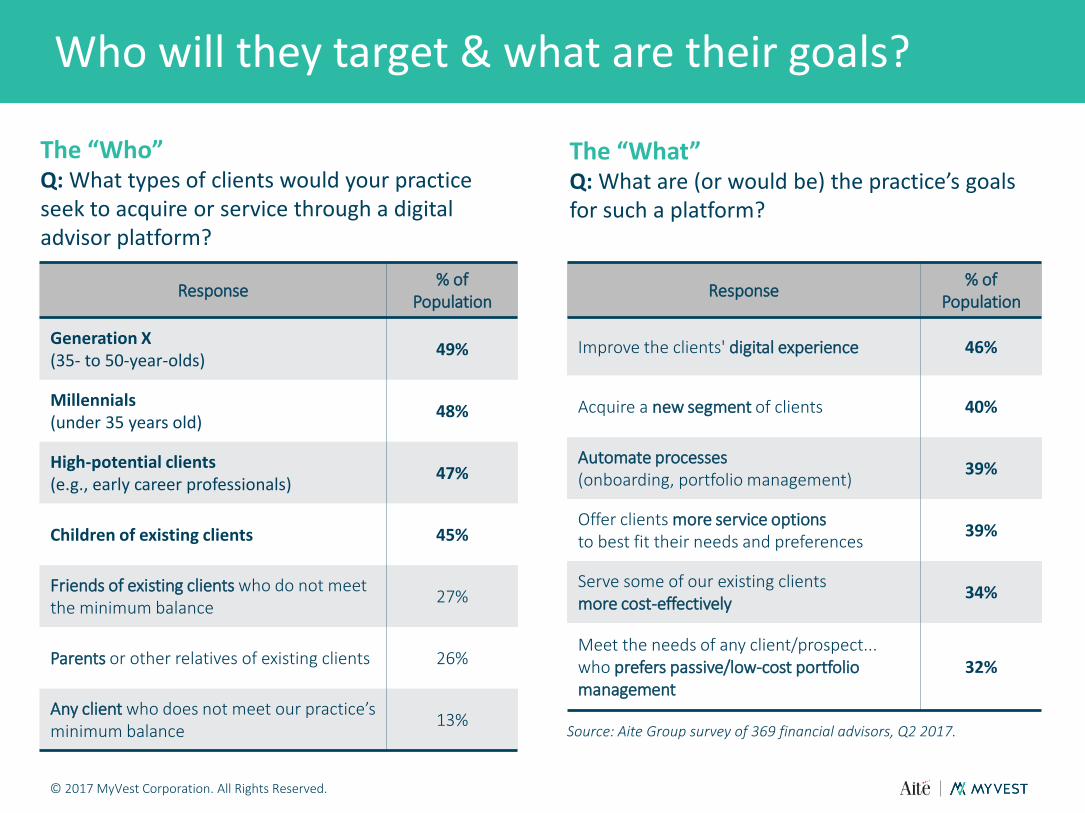

Response % of Population

Improve the clients' digital experience 46%

Acquire a new segment of clients 40%

Automate processes(onboarding, portfolio management) 39%

Offer clients more service options to best fit their needs and preferences 39%

Serve some of our existing clients more cost-effectively 34%

Meet the needs of any client/prospect... who prefers passive/low-cost portfolio management

32%

The “What”Q: What are (or would be) the practice’s goals for such a platform?

Response % of Population

Generation X (35- to 50-year-olds) 49%

Millennials(under 35 years old) 48%

High-potential clients (e.g., early career professionals) 47%

Children of existing clients 45%

Friends of existing clients who do not meet the minimum balance 27%

Parents or other relatives of existing clients 26%

Any client who does not meet our practice’s minimum balance 13%

The “Who”Q: What types of clients would your practice seek to acquire or service through a digital advisor platform?

Source: Aite Group survey of 369 financial advisors, Q2 2017.

Who will they target & what are their goals?

© 2017 MyVest Corporation. All Rights Reserved.

Response % of Population

Improve the clients' digital experience 46%

Acquire a new segment of clients 40%

Automate processes(onboarding, portfolio management) 39%

Offer clients more service options to best fit their needs and preferences 39%

Serve some of our existing clients more cost-effectively 34%

Meet the needs of any client/prospect... who prefers passive/low-cost portfolio management

32%

The “What”Q: What are (or would be) the practice’s goals for such a platform?

Response % of Population

Generation X (35- to 50-year-olds) 49%

Millennials(under 35 years old) 48%

High-potential clients (e.g., early career professionals) 47%

Children of existing clients 45%

Friends of existing clients who do not meet the minimum balance 27%

Parents or other relatives of existing clients 26%

Any client who does not meet our practice’s minimum balance 13%

The “Who”Q: What types of clients would your practice seek to acquire or service through a digital advisor platform?

Source: Aite Group survey of 369 financial advisors, Q2 2017.

Who will they target & what are their goals?

© 2017 MyVest Corporation. All Rights Reserved.

“As you can see, these digital advice platforms service nearly all client

segments and firm goals.”

- Alois Pirker, Aite Group

Where Are We Going?

The Revenge of the Incumbents

Brand

Customer base

Multiple service channels

Existing BD or bank

Client data

Product diversity

Research

Balance sheet

Incumbents’ unique advantages

But incumbents

have their own unique

challenges

Inertia

Lack of digital vision

Fear of cannibalization

Siloed legacy technology

Non-agile development culture

Fintech partnerships

can help bridge the

gap

© 2017 MyVest Corporation. All Rights Reserved.

Fintech partnerships

can help bridge the

gap

© 2017 MyVest Corporation. All Rights Reserved.

“Incumbents will benefit most when they embrace fintech’s culture of change.”

- Anton Honikman, MyVest

Serve multiple segments

Value-added services

Robust client data layer

Incumbents’ new opportunities in digital wealth

© 2017 MyVest Corporation. All Rights Reserved.

Serve multiple segments

Value-added services

Robust client data layer

Incumbents’ new opportunities in digital wealth

© 2017 MyVest Corporation. All Rights Reserved.

“There’s so much opportunity in the amount of data firms have.

Start with the data and use it to hyper-personalize the experience.”

- Anton Honikman, MyVest

1. Invest in great UI/UX (table stakes)

2. Leverage your strengths

3. Seek out smart fintech partnerships

4. Move from simple segmentation to hyper-personalization

Incumbent recipe for

success

1. Invest in great UI/UX (table stakes)

2. Leverage your strengths

3. Seek out smart fintech partnerships

4. Move from simple segmentation to hyper-personalization

Incumbent recipe for

success

“Incumbents, now is your time.”

- Anton Honikman, MyVest

Learnmore

aitegroup.com

myvest.com

© 2017 MyVest Corporation. All Rights Reserved.