richard yamarone director of economic research argus research corp

DESCRIPTION

“What We’re Watching to Identify the Economic Recovery”. June 3, 2009. Richard Yamarone Director of Economic Research Argus Research Corp. Hoping for a “V”-Shaped Recovery. Leading Indicators Signal Some Degree of Recovery. The Most Convincing Argument of Recovery. - PowerPoint PPT PresentationTRANSCRIPT

Richard YamaroneDirector of Economic Research

Argus Research Corp.

“What We’re Watching to Identify the Economic Recovery”

June 3, 2009

Hoping for a “V”-Shaped Recovery

Real GDP (%)

-8

-6

-4

-2

0

2

4

6

8

10

'95 '97 '99 '01 '03 '05 '07 '09 F

Source: Bureau of Economic Analysis

Leading Indicators Signal Some Degree of Recovery

Leading Economic Indicators vs. Real GDP Growth (Y/Y%)

-4

-2

0

2

4

6

8

10

'85 '95 '05

-4

-2

0

2

4

6

8

10GDP

LEI

-3.0%

-2.5%

Source: Bureau of Economic Analysis, The Conference Board, Argus Research Corp.

The Most Convincing Argument of Recovery

ECRI Weekly Leading Index

-30

-25

-20

-15

-10

-5

0

5

10

15

'99 '01 '03 '05 '07 '09

Source: Bloomberg, ECRI

Fed Indices Point to More Prosperous Times

Chicago Fed National Activity Index

-4.00

-3.50

-3.00

-2.50

-2.00

-1.50

-1.00

-0.50

0.00

0.50

1.00

'90 '93 '96 '99 '02 '05 '08

Source: Federal Reserve Bank of Chicago

Three Month Moving Average

A-D-S Business Conditions Index Improving

Source: Federal Reserve Bank of Philadelphia

Anecdotal Reports Starting to Improve

U.S. Average Daily Package Volume UPSvs. Real GDP

-5

-3

-1

1

3

5

7

2000 2002 2004 2006 2008

-3

-2

-1

0

1

2

3

4

5

6

UPS Volume

Real GDP

Real GDPUPS Volume

Source: United Parcel Service, Bureau of Economic Analysis, Argus Research

Fiscal Policy Arriving at the Spigots

Direct Outlays, Stimulus Package ($Blns)

-50

0

50

100

150

200

250

2009 '10 '11 '12 '13 '14 '15 '16 '17 '18 2019

Source: CBO

Monetary Policy…

Source: Federal Reserve Bank of St. Louis

Business Investment has Collapsed

Capital Spending (%)

-40

-30

-20

-10

0

10

20

30

'88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08

Non-Residential Investment

Source: Bureau of Economic Research

Little Reason for Hope in New Orders Data

New OrdersNonDefense Capital Goods Ex-Aircraft (Y/Y%)

-40

-32

-24

-16

-8

0

8

16

24

'94 '96 '98 '00 '02 '04 '06 '08

Source: Department of Commerce

Key Index Implying Strong Recovery

ISM New Orders - Inventories vs. Real GDP

-15

-10

-5

0

5

10

15

20

25

1983 1988 1993 1998 2003 2008

-3

0

3

6

9

GDP

NO-INV

NO-IGDP Y /Y%

Source: BEA, ISM, Argus Research

Little Need to Build With Glut of Commercial Property

Structures Spending (%)

-45

-30

-15

0

15

30

'94 '96 '98 '00 '02 '04 '06 '08

Source: Bureau of Economic Analysis

Signs of Stabilization

New & Existing Home Sales

300

450

600

750

900

1050

1200

1350

'96 '99 '02 '05 '08

3550

4300

5050

5800

6550

7300

New

Existing

New Existing

Source: US Dept. of Commerce, National Association of Realtors

Home Prices Returning to Pre-Bubble Levels

S&P/Case Shiller Home Price Indices

75

100

125

150

175

200

225

250

275

300

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09

AZ-Phoenix

CA-Los Angeles

CA-San Diego

CA-San Francisco

CO-Denver

DC-Washington

FL-Miami

FL-Tampa

GA-Atlanta

IL-Chicago

MA-Boston

MI-Detroit

MN-Minneapolis

NC-Charlotte

NV-Las Vegas

NY-New York

OH-Cleveland

OR-Portland

TX-Dallas

WA-Seattle

Source: S&P

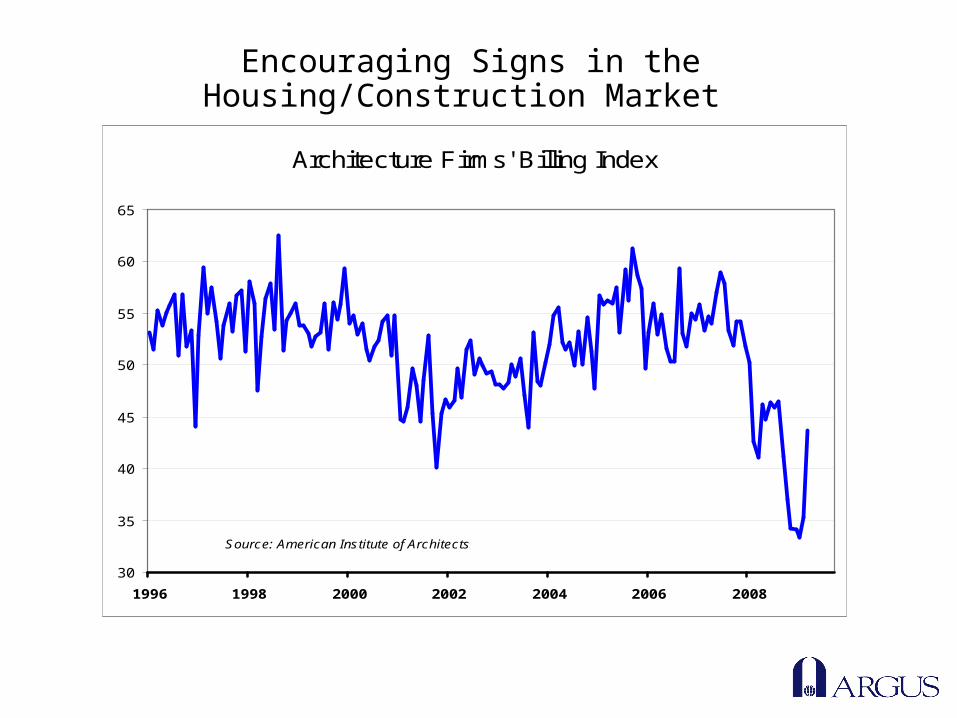

Encouraging Signs in the Housing/Construction Market

Architecture Firms' Billing Index

30

35

40

45

50

55

60

65

1996 1998 2000 2002 2004 2006 2008

Source: American Institute of Architects

“Stimulus” May Help Ailing Construction Sector

Construction Spending (Y/Y%)

-40

-30

-20

-10

0

10

20

30

2003 2005 2007 2009

Non-Residential

Residential

Source: Department of Commerce

Trade, the Unsexy Savior

Contribution to GDPResidential Spending & Trade

-0.23

-1.11-1.4

-1.18-0.91

-0.6

-1.06-1.33

-1.12

-0.52 -0.6-0.8

-1.39

0.09

0.59

-0.12

1.33

-1.2

1.66

2.03

0.940.77

2.93

1.05

-0.15

2.18

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

3

3.5

'06 QI QII QIII QIV '07 QI QII QIII QIV '08 QI QII QIII QIV '09 QI

Residential

Trade

Source: BEA, Argus Research

Some Recovery in Container Traffic

Outbound Container Statistics (TEU)

50,000

70,000

90,000

110,000

130,000

150,000

170,000

'95 '97 '99 '01 '03 '05 '07 '09

Port of Long Beach

Source: Port of Long Beach

Some Signs of Peak in Unemployment

'Jobs Hard-to-Get' &Unemployment Rate

3

4

5

6

7

8

9

10

'90 '92 '94 '96 '98 00 '02 '04 '06 '08

0

10

20

30

40

50

U Rate Jobs Index

Jobs Index

Unemployment Rate

Source: Conference Board, Bureau of Labor Statistics

Unemployment Benefit Claims Point to Economic Trough

Weekly Initial Claims

250,000

300,000

350,000

400,000

450,000

500,000

550,000

600,000

650,000

700,000

'96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09

Source: US Department of Labor

Ever-Resilient Consumer Tossed in Towel

Real Consumer Spending (%)

-5

0

5

10

1992 1995 1998 2001 2004 2007

Source: Bureau of Economic Aanalysis

‘Fab Five’ – Dining Out

Spending: Meals at Other Eating Places (Y/Y%)

-6

-4

-2

0

2

4

6

8

'98 '01 '04 '07

Source: Bureau Economic Analysis, NBER

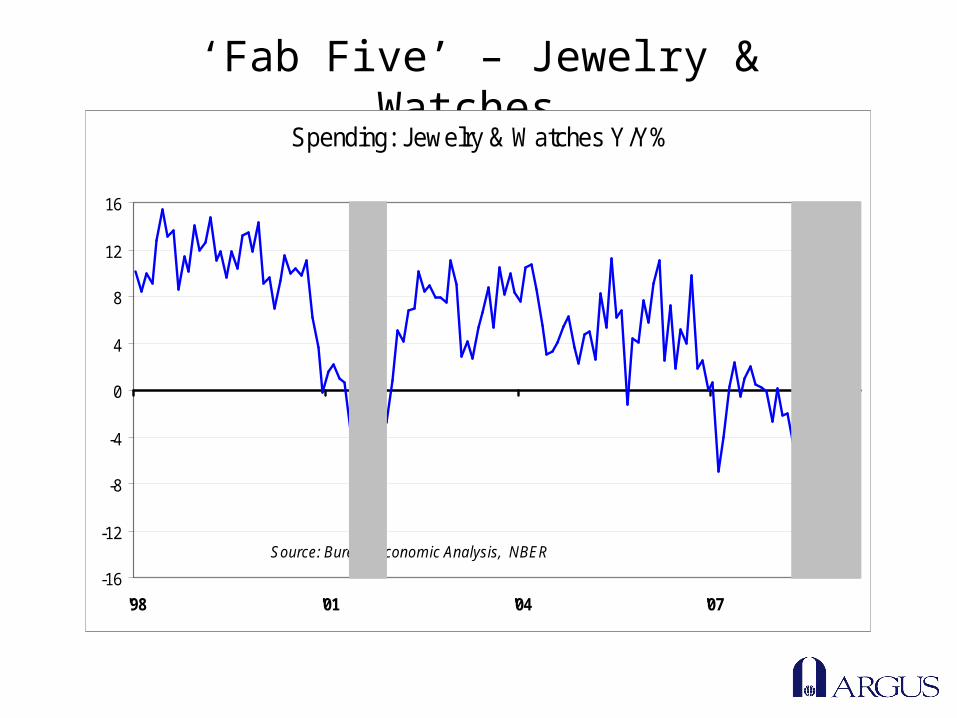

‘Fab Five’ – Jewelry & Watches

Spending: Jewelry & Watches Y/Y%

-16

-12

-8

-4

0

4

8

12

16

'98 '01 '04 '07

Source: Bureau Economic Analysis, NBER

‘Fab Five’ – Cosmetics & Perfumes

Spending: Cosmetics & Perfumes (Y/Y%)

-9

-6

-3

0

3

6

'98 '01 '04 '07

Source: Bureau Economic Analysis, NBER

‘Fab Five’ – Women’s Dresses

Spending: Women's Clothing (Y/Y%)

-8

-6

-4

-2

0

2

4

6

8

10

12

'98 '01 '04 '07

Source: Bureau Economic Analysis, NBER

‘Fab Five’ – Casino GamblingSpending: Casino Gambling Y/Y%

-16

-12

-8

-4

0

4

8

12

16

20

24

'98 '01 '04 '07

Source: Bureau Economic Analysis, NBER

‘Fab Five’ Recovery…

Post Recession, Fab-Five

95

100

105

110

115

120

125

130

135

140

145

Dec-01 Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Dec-07

Dining Out

Perfumes

Women's

Jewelry

Casino

December 2001=100

Bad Signs for Summer Spending

Real Spending: Hotels & Motels (Y/Y%)

-20

-16

-12

-8

-4

0

4

8

12

16

'98 '01 '04 '07

Source: Bureau Economic Analysis, Argus Research, NBER

Auto Industry is the Wildcard

America Still Loves Those Trucks

Total Vehicle Assemblies (Mlns)

3.72 3.34 2.95

1.33 1.66 1.87 1.84

4.123.97

3.72

2.52

3.11 3.05 3.2

0

1

2

3

4

5

6

7

8

9

Oct-08 Nov-08 Dec-08 Jan-09 Feb-09 Mar-09 Apr-09

Trucks

Autos

Source: Federal Reserve System

Prices Aren’t ‘Collapsing’

The Economist Commodity Price Index

110

125

140

155

170

185

200

215

230

245

260

275

2/14/2001 2/13/2002 2/12/2003 2/11/2004 2/9/2005

All Items

Industrials

Food

2005=100

Source: The Economist

Market Inflation Expectations Rising

5-Year Treasury Note - Five Year TIPS Spread

-2.50

-2.00

-1.50

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

2003 2004 2005 2006 2007 2008 2009

Source: Federal Reserve Bank of St. Louis, Argus Research

Consumer Inflation Expectations on the Rise

Reuters/U. Michigan Inflation Expectations (%)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

'03 '04 '05 '06 '07 '08 '09

Source: Bloomberg

Broad Inflation Measures Still Elevated

GDP Deflators (%)

-6

-4

-2

0

2

4

6

2004 2005 2006 2007 2008 2009

PCE Deflator

GDP Deflator

Source: Bureau of Economic Analysis

No ‘Deflation’ in this Respected Measure

Dallas Fed Trimmed-Mean PCE Inflation (Y/Y%)

1.5

1.7

1.9

2.1

2.3

2.5

2.7

2.9

3.1

'95 '97 '99 '01 '03 '05 '07 '09

Source: Federal Reserve Bank of Dallas

Inflation Pressures Appear to be ‘Well-Anchored’… For Now

Core Personal Consumption Expenditure Deflator (Y/Y%)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

'90 '92 '94 '96 '98 '00 '02 '04 '06 '08

Federal Reserve 'Comfort Zone'

Source: Bureau of Economic Analysis, Argus Research

Monetary Policy Getting Easier Every Month

Real Fed Funds RateCore Personal Consumption Deflator (%)

-2.0

0.0

2.0

4.0

6.0

'87 '89 '91 '93 '95 '97 '99 '01 '03 '05 '07 '09

Internal Fed Gauge Implies Fed to Remain on ‘Hold’

Argus Leading Fed Funds Index

0

1

2

3

4

5

6

7

8

9

'90 '92 '94 '96 '98 '00 '02 '04 '06 '08

30

40

50

60

70

80

90

100

110

120

130

FED FUNDS

ALFFI

FF % Index

37.16

Risks to “V”-Shaped Recovery…

Commodity (Food), Energy, Healthcare Inflation

(price pass alongs announced during the quarterly earning season)

Stimulus Fails to Generate Jobs

Jobs Climate Deteriorates Further

Auto Industry Collapse

Consumers Decide to Save

Reasons for Optimism…

Government Has Approved Whopping Fiscal Spending Program

Large Stimulus of Falling Energy Prices

Home Prices Have Returned to Pre-Bubble Levels

Massive Monetary Stimulus in Pipeline

Frozen Credit Markets Have Thawed Considerably