richard a. davis and gabriel rodriguez-yam …rdavis/lectures/unsw_03.pdf · 1 estimation for state...

TRANSCRIPT

1

Estimation for State Space Models: Estimation for State Space Models: an Approximate Likelihood Approachan Approximate Likelihood Approach

Richard A. Davis and Gabriel Rodriguez-YamColorado State University

(http://www.stat.colostate.edu/~rdavis/lectures)

Joint work with:William Dunsmuir, University of New South WalesYing Wang, Dept of Public Health, W. Virginia

2

Example: Daily Asthma Presentations (1990:1993)

Year 1990

••••••••••

•••••

•••••••••••••••••

•••••

•

••••••

••••••••••••

••••

•••••••••••

••••••••

•••••••••

•••

••

••••

••••••

•••••

••

•

•••••••••••••••••••••

••

•

•••••

•

••••

•••••••

••••

•

••••••••••••

•

••••••

•••••

•

•••

•

••••••

•••••••••

•

•••••••

•

•••••••••••••

••••••••••

••••••••••

••••••••••••

••••••

•••••

••••••••

••••••••••••

•••••••

•••••••••••

••••••••••••

•

•••••••••••••

•••••

••••••••••••

••••••••

••••••

••••

06

14

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Year 1991

••••••

••••••••••••

•••••••••

••••••••

•••••

••

•••••

••••••

••••••

••••••

•••••••••

••

•••

••••••

•

•••••••

•

••••••

••••••••

••••••••••••••

•••••

•••••

•

•

•

•••

•••••••••

••••••••

••••••••

••••••••••••

•

•••••••

••••

••••••

•••••••••••

•••••

•••••••

•

••••••••••••

••••

••••••••••

•••••••••••••••••••••••••••

••••••••

•••••

•••••

••••••••••

•••••••

•••••••••••••

•••••

••••••••••

•••••••••••••

••••••••••

•••••••••

06

14

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Year 1992

•

•••••••••

••••••••••••••••••••

••••••••

•

••••••••••

••

•••••

••

••

••••••••••

••

•

••

•••••

•••••

••••••

•••••••

•••

••••

••••••••••

•••

•••••••••

•••••••••

••••••

••

•

••

•

•

••

•

•••••••

•

•••••••

••••

•

•••••

••••••

•••••••••

••••••••••••

••••••

•••••••••

••••

••••••••

•••

••••••••

••••••••

•••••••••••••

•••••

••••••

••••••••••

••••••••

•••••••

•••••••••

•••••••••

•

•••••••

•

••••••••

••••••••••••

••••••••

•••••

•••••••0

614

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Year 1993

••••••••••••

••••••••

•••••

•••••

•••••••••••

•••

••••

••

••••

••••

•

•

•••••••

•

•••••••••••

••

•••••••••

••••

••

••

••••••••

•••••••••

••••••••

•••••••••••

•

•••••••••••

••••

••••••

••

••••••

••

•••••

•••••••••••

•••••••••

•••••••

••••

••••••••••••

•••••••

•••••

••••••••

••••••

•••••••

•••••

•••••••

•••••

•••••

•••••

•••••••••

•

••••••••••••••••••••

••••

••••

•••••••

•••••••••••••••••••••

••••

•••••••••

••••••••••••0

614

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

3

day

log

retu

rns

(exc

hang

e ra

tes)

0 200 400 600 800

-20

24

lag

AC

F

0 10 20 30 40

0.0

0.2

0.4

0.6

0.8

1.0

lag

AC

F of

squ

ares

0 10 20 30 40

0.0

0.2

0.4

0.6

0.8

1.0

lag

AC

F of

abs

val

ues

0 10 20 30 40

0.0

0.2

0.4

0.6

0.8

1.0

Example: Pound-Dollar Exchange Rates (Oct 1, 1981 - June28, 1985; Koopman website)

4

Motivating Examples• Time series of counts• Stochastic volatility

Generalized state-space modelsObservation drivenParameter driven

Model setup and estimationGeneralized linear models (GLM)Estimating equations (Zeger)MCEM (Chan and Ledolter)Importance sampling

- Durbin and KoopmanApproximation to the likelihood (Davis, Dunsmuir, and Wang)

ApplicationTime series of countsStochastic volatility

5

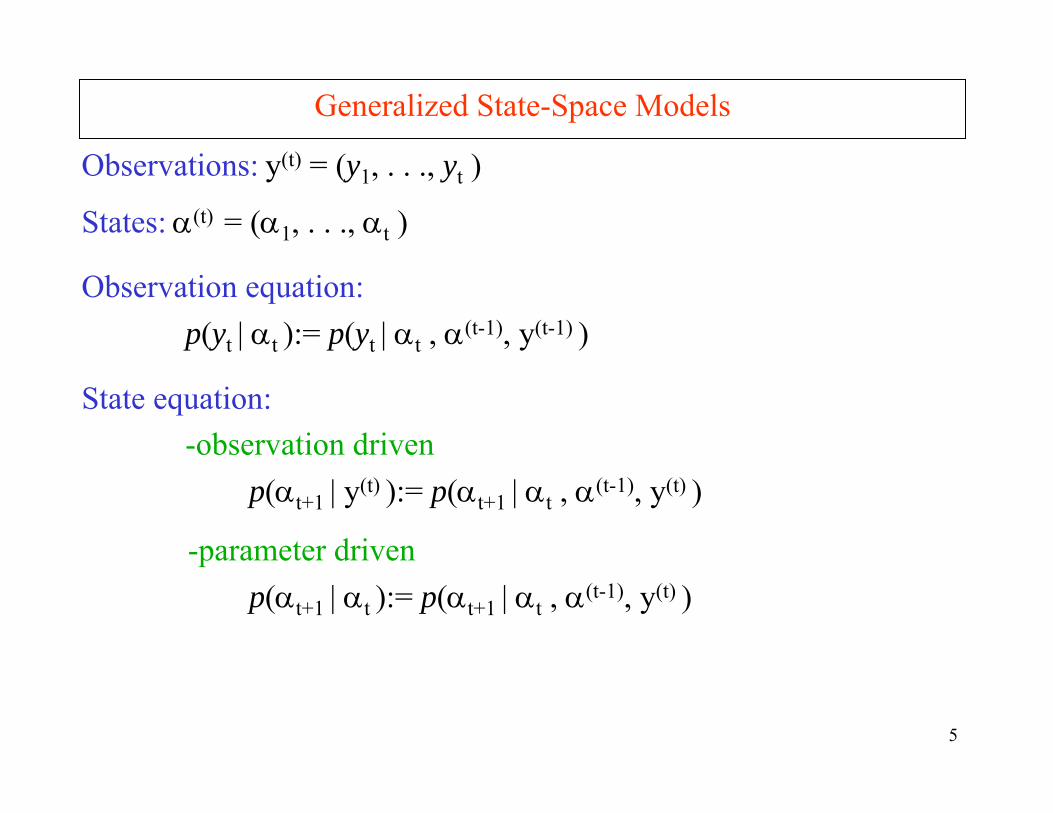

Generalized State-Space Models

Observations: y(t) = (y1, . . ., yt )

States: α(t) = (α1, . . ., αt )

Observation equation:p(yt | αt ):= p(yt | αt , α(t-1), y(t-1) )

State equation:-observation driven

p(αt+1 | y(t) ):= p(αt+1 | αt , α(t-1), y(t) )

-parameter drivenp(αt+1 | αt ):= p(αt+1 | αt , α(t-1), y(t) )

6

..., 1, ,0 ,!

e)|( tt

e

tt

ttt

==αα−−α

yy

ypy

..., 1, ,0 ,!

e)|( tt

e

tt

ttt

==αα−−α

yy

ypy

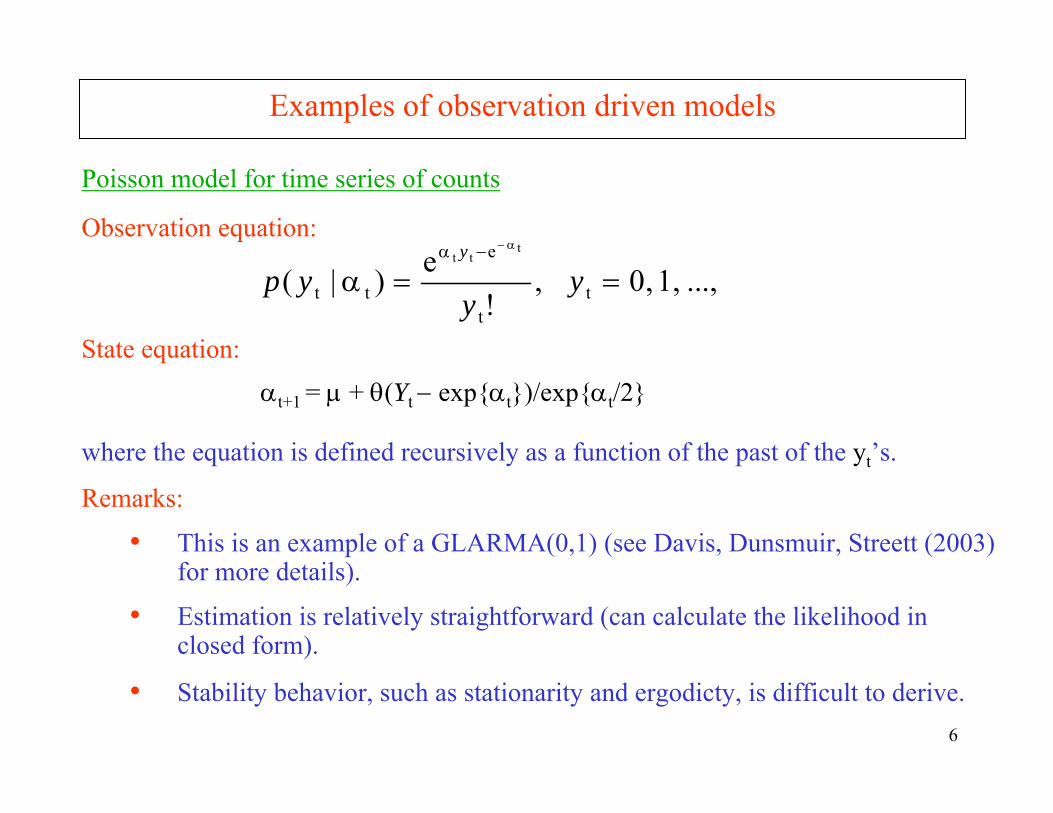

Examples of observation driven models

Poisson model for time series of counts

Observation equation:

State equation:αt+1 = µ + θ(Yt − expαt)/expαt/2

where the equation is defined recursively as a function of the past of the yt’s.

whereRemarks:

• This is an example of a GLARMA(0,1) (see Davis, Dunsmuir, Streett (2003) for more details).

• Estimation is relatively straightforward (can calculate the likelihood in closed form).

• Stability behavior, such as stationarity and ergodicty, is difficult to derive.

7

Examples of observation driven models-cont

An observation driven model for financial data:Model (GARCH(p,q)):

Yt = σt Zt , Zt~IID N(0,1)

Special case (ARCH(1)=GARCH(1,0)): The resulting observation and state transition density/equations are

p(yt| σt) = n(yt ; 0, σ2t )

2211

22110

2qtqtptptt YY −−−− σβ++σβ+α++α+α=σ LL

2110

2−α+α=σ tt Y

Properties:

• Martingale difference sequence.

• Stationary for α1 ∈[0,2eE), E-Euler’s constant.

• Strongly mixing at a geometric rate.

• For general ARCH (GARCH), properties are difficult to establish.

8

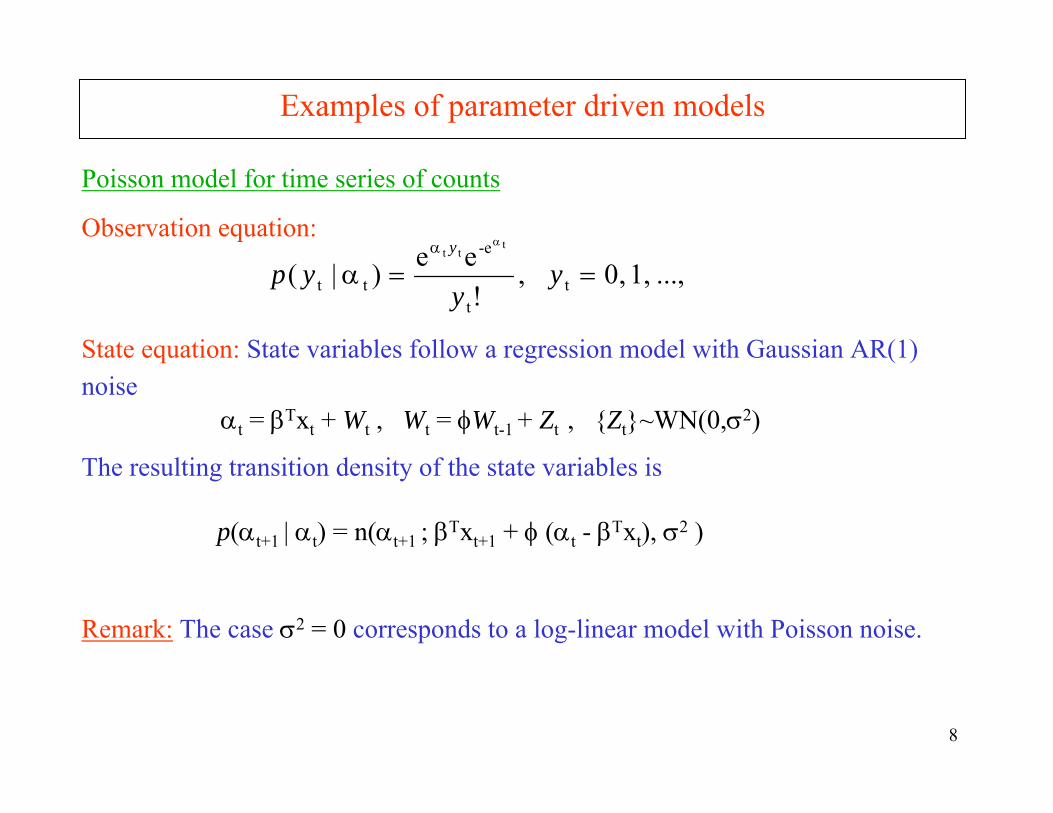

Examples of parameter driven models

Poisson model for time series of counts

Observation equation:

..., 1, ,0 ,!

ee)|( tt

-e

tt

ttt

==ααα

yy

ypy

Remark: The case σ2 = 0 corresponds to a log-linear model with Poisson noise.

State equation: State variables follow a regression model with Gaussian AR(1) noise AR(1) noise:

αt = βΤxt + Wt , Wt = φWt-1 + Zt , Zt~WN(0,σ2)

The resulting transition density of the state variables is

is p(αt+1 | αt) = n(αt+1 ; βΤxt+1 + φ (αt - βΤxt), σ2 )

9

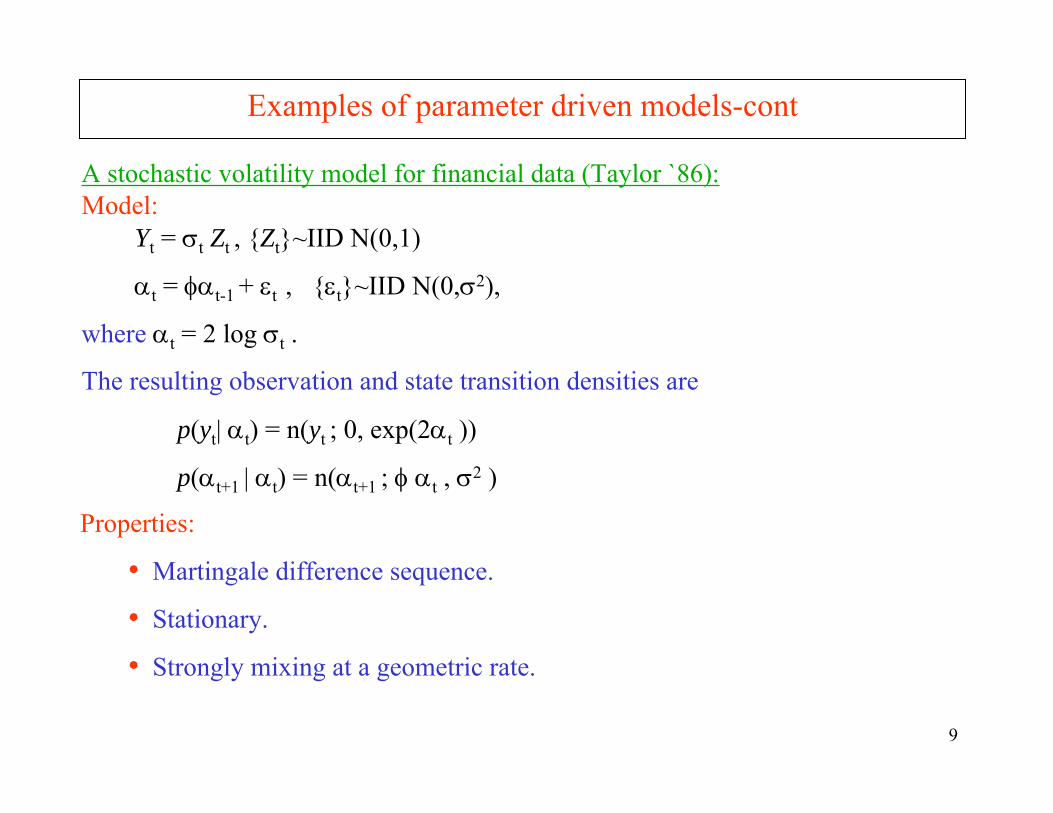

Examples of parameter driven models-cont

A stochastic volatility model for financial data (Taylor `86):Model:

Yt = σt Zt , Zt~IID N(0,1)

αt = φαt-1 + εt , εt~IID N(0,σ2),

where αt = 2 log σt .

The resulting observation and state transition densities are

p(yt| αt) = n(yt ; 0, exp(2αt ))

p(αt+1 | αt) = n(αt+1 ; φ αt , σ2 )

Properties:

• Martingale difference sequence.

• Stationary.

• Strongly mixing at a geometric rate.

10

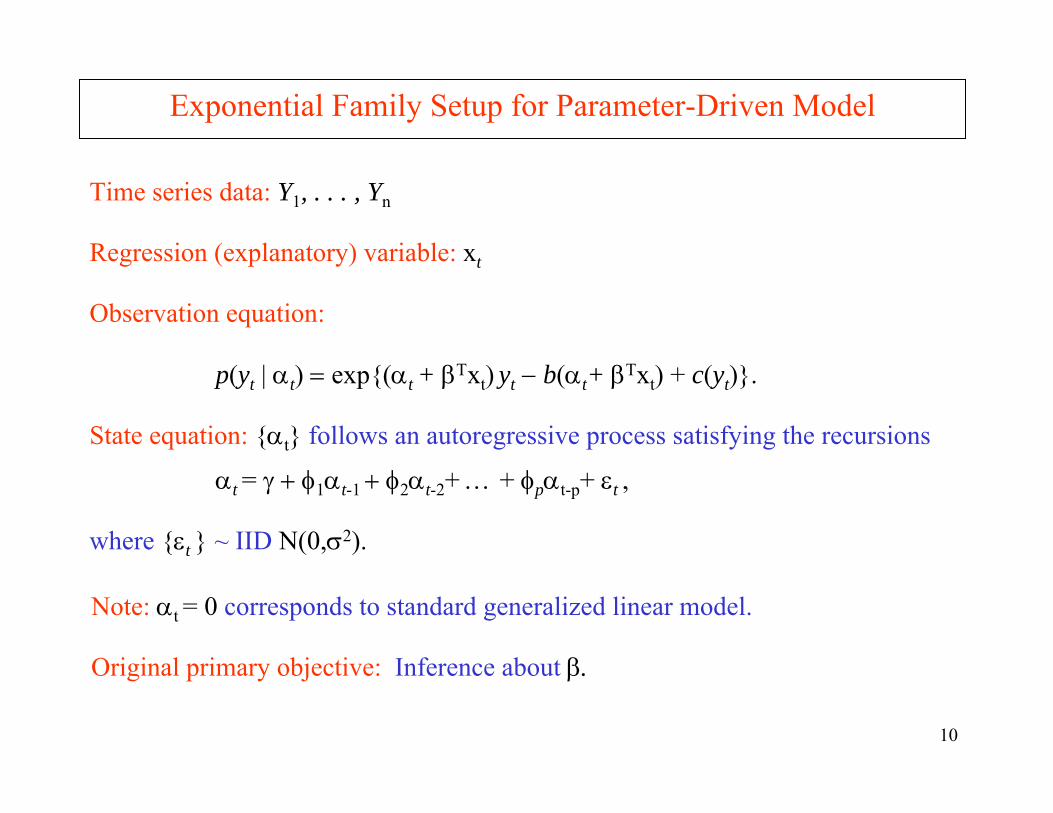

Exponential Family Setup for Parameter-Driven Model

Time series data: Y1, . . . , Yn

Regression (explanatory) variable: xt

Observation equation:

p(yt | αt) = exp(αt + βΤxt) yt − b(αt+ βΤxt) + c(yt).

State equation: αt follows an autoregressive process satisfying the recursions

αt = γ + φ1αt-1 + φ2αt-2+ … + φpαt-p+ εt ,

where εt ~ IID N(0,σ2).

Note: αt = 0 corresponds to standard generalized linear model.

Original primary objective: Inference about β.

11

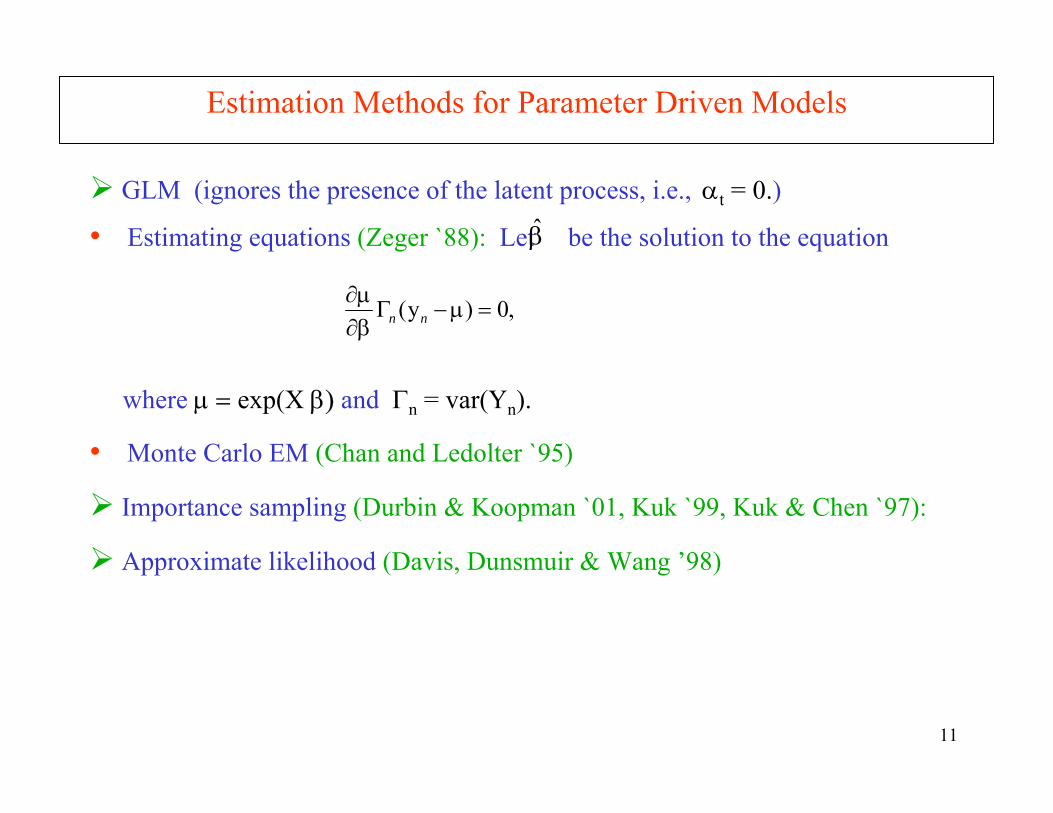

GLM (ignores the presence of the latent process, i.e., αt = 0.)

• Estimating equations (Zeger `88): Let be the solution to the equation

where µ = exp(X β) and Γn = var(Yn).

• Monte Carlo EM (Chan and Ledolter `95)

Importance sampling (Durbin & Koopman `01, Kuk `99, Kuk & Chen `97):

Approximate likelihood (Davis, Dunsmuir & Wang ’98)

Estimation Methods for Parameter Driven Models

,0)y( =µ−Γβ∂µ∂

nn

β

12

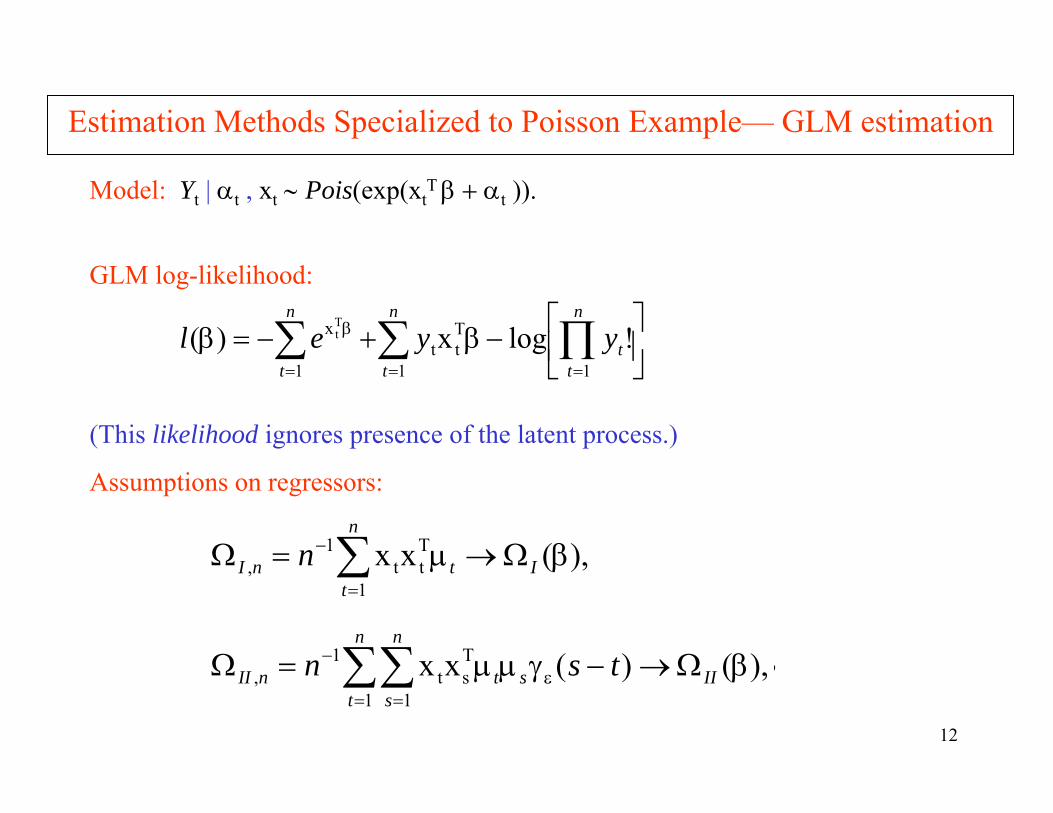

Model: Yt | αt , xt ∼ Pois(exp(xtT β + αt )).

GLM log-likelihood:

(This likelihood ignores presence of the latent process.)

⎥⎦

⎤⎢⎣

⎡−β+−=)β ∏∑∑===

βn

tt

n

t

n

t

yyel11

Ttt

1

x !logx(Tt

Estimation Methods Specialized to Poisson Example— GLM estimation

Assumptions on regressors:

),()(xx

),(xx

1 1

Tst

1,

1

Ttt

1,

βΩ→−γµµ=Ω

βΩ→µ=Ω

∑∑

∑

=ε

=

−

=

−

II

n

ts

n

stnII

I

n

ttnI

tsn

n

),()(xx

),(xx

1 1

Tst

1,

1

Ttt

1,

βΩ→−γµµ=Ω

βΩ→µ=Ω

∑∑

∑

=ε

=

−

=

−

II

n

ts

n

stnII

I

n

ttnI

tsn

n

13

Theorem (Davis, Dunsmuir, Wang `00). Let be the GLM estimate of βobtained by maximizing l(β) for the Poisson regression model with a stationary lognormal latent process. Then

). N(0, )βˆ( 1III

1I

1I

2/1 −−− ΩΩΩ+Ω→−βd

n

Theory of GLM Estimation in Presence of Latent Process

Notes:

1. n-1ΩI-1 is the asymptotic cov matrix from a std GLM analysis.

2. n-1ΩI-1 ΩII ΩI

-1 is the additional contribution due to the presence of the latentprocess.

3. Result also valid for more general latent processes (mixing, etc),

4. The xt can depend on the sample size n.

β

14

Assume the αt follows a log-normal AR(1), where

(αt+σ2/2) = φ(αt-1+ σ2/2) +ηt , ηt~IID N(0, σ2(1−φ2)),

with φ =.82, σ2 = .57.

βZ s.e. βGLM s.e. s.e. βGLM s.d.

Application to Model for Polio Data

Zeger GLM Fit Asym Simulation

Intercept 0.17 0.17 0.13Trend(×10-3) -4.35 2.68cos(2πt/12) -0.11 0.16sin(2πt/12) -.048 0.17cos(2πt/6) 0.20 0.14sin(2πt/6) -0.41 0.14

.207 .075 .205-4.80 1.40 4.12-0.15 .097 .157-0.53 .109 .168.169 .098 .122-.432 .101 .125

.150 .213-4.89 3.94-.145 .144-.531 .168.167 .123-.440 .125

15

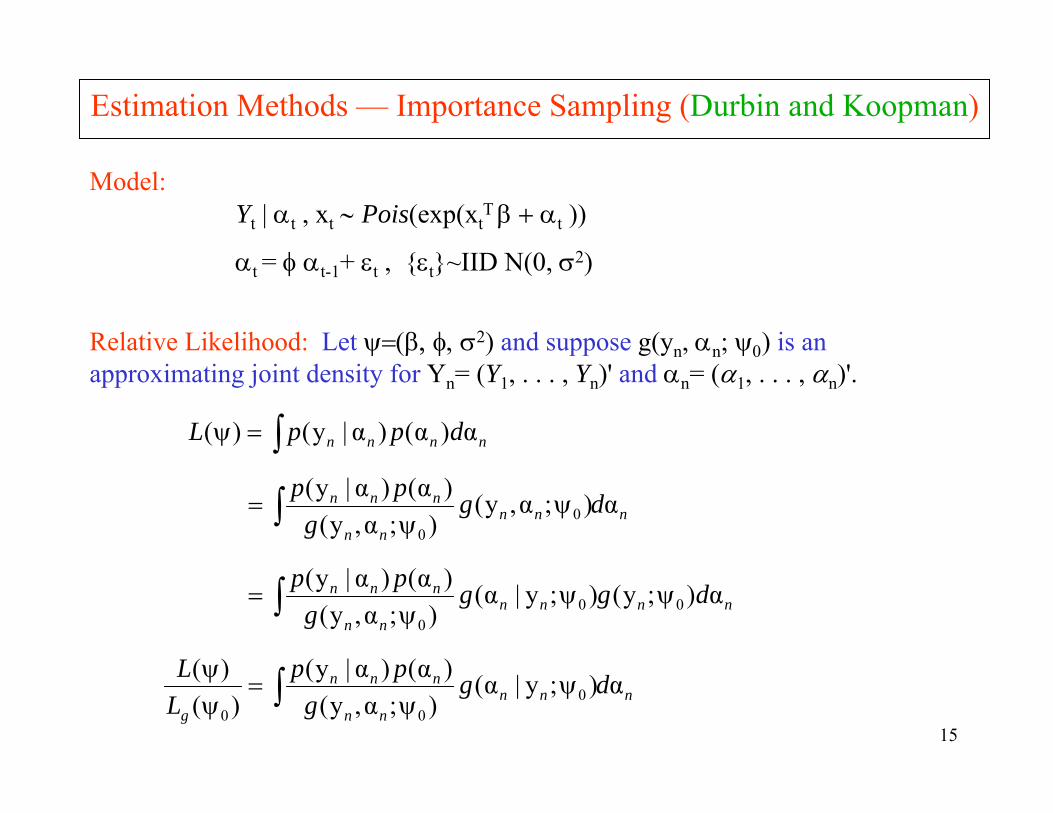

Estimation Methods — Importance Sampling (Durbin and Koopman)

Model: Yt | αt , xt ∼ Pois(exp(xt

T β + αt ))

αt = φ αt-1+ εt , εt~IID N(0, σ2)

Relative Likelihood: Let ψ=(β, φ, σ2) and suppose g(yn, αn; ψ0) is an approximating joint density for Yn= (Y1, . . . , Yn)' and αn= (α1, . . . , αn)'.

nnnn dppL α)α()α|y()( ∫=ψ

nnnnn

nnn

g

nnnnnn

nnn

nnnnn

nnn

dgg

ppLL

dggg

pp

dgg

pp

α);y|α();α,y(

)α()α|y()(

)(

α);y();y|α();α,y(

)α()α|y(

α);α,y();α,y(

)α()α|y(

000

000

00

∫

∫

∫

ψψ

=ψψ

ψψψ

=

ψψ

=

nnnnn

nnn

g

nnnnnn

nnn

nnnnn

nnn

dgg

ppLL

dggg

pp

dgg

pp

α);y|α();α,y(

)α()α|y()(

)(

α);y();y|α();α,y(

)α()α|y(

α);α,y();α,y(

)α()α|y(

000

000

00

∫

∫

∫

ψψ

=ψψ

ψψψ

=

ψψ

=

16

Importance Sampling (cont)

where

,);α,y(

)α()α|y(1~

);y|);α,y(

)α()α|y(

α);y|α();α,y(

)α()α|y()(

)(

1 0)(

)()(

00

000

∑

∫

= ψ

⎥⎦

⎤⎢⎣

⎡ψ

ψ=

ψψ

=ψψ

N

jj

nn

jn

jnn

nnn

nnng

nnnnn

nnn

g

gpp

N

gppE

dgg

ppLL

).;y|g(α iid ~,...,1;α 0)( ψ= nn

jn Nj

.ψ

Notes:

• This is a “one-sample” approximation to the relative likelihood. That is, for one realization of the α’s, we have, in principle, an approximation to the whole likelihood function.

• Approximation is only good in a neighborhood of ψ0. Geyer suggests maximizing ratio wrt ψ and iterate replacing ψ0 with

17phi

log

likel

ihoo

d

0.3 0.4 0.5 0.6 0.7

-416

-415

-414

-413

-412

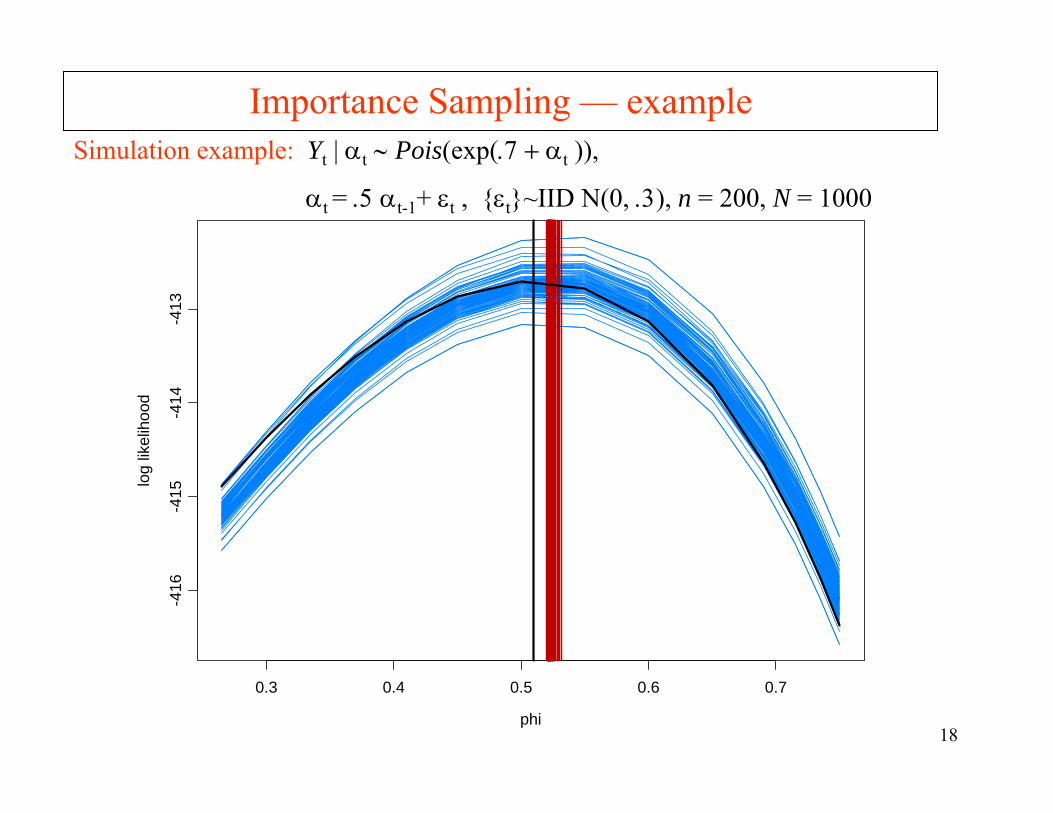

Importance Sampling — exampleSimulation example: Yt | αt ∼ Pois(exp(.7 + αt )),

αt = .5 αt-1+ εt , εt~IID N(0, .3), n = 200, N = 1000

18phi

log

likel

ihoo

d

0.3 0.4 0.5 0.6 0.7

-416

-415

-414

-413

Simulation example: Yt | αt ∼ Pois(exp(.7 + αt )),

αt = .5 αt-1+ εt , εt~IID N(0, .3), n = 200, N = 1000

Importance Sampling — example

19

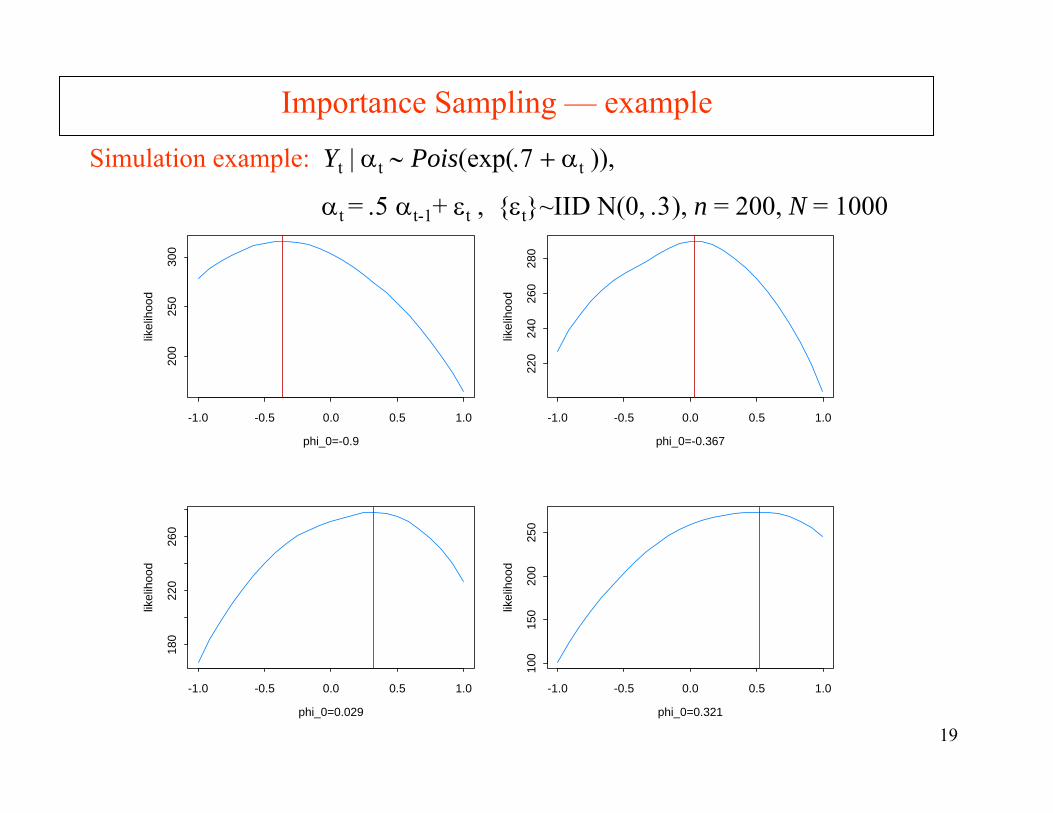

Importance Sampling — example

phi_0=-0.9

likel

ihoo

d

-1.0 -0.5 0.0 0.5 1.0

200

250

300

phi_0=-0.367

likel

ihoo

d

-1.0 -0.5 0.0 0.5 1.0

220

240

260

280

phi_0=0.029

likel

ihoo

d

-1.0 -0.5 0.0 0.5 1.0

180

220

260

phi_0=0.321

likel

ihoo

d

-1.0 -0.5 0.0 0.5 1.0

100

150

200

250

Simulation example: Yt | αt ∼ Pois(exp(.7 + αt )),

αt = .5 αt-1+ εt , εt~IID N(0, .3), n = 200, N = 1000

22

Importance Sampling (cont)

Choice of importance density g:

Durbin and Koopman suggest a linear state-space approximating model

Yt = µt+ xtT β + αt+Zt , Zt~N(0,Ht),

with

where the are calculated recursively under the approximating model until convergence.

),,y~(~);y|g(α 110

−− ΓΓψ nnnnn N

.))'αα(()(diag

,αyy~ 1αXβ

αXβαXβ n

−+

++

+=Γ

+−=

nnn

nnn

Ee

een

n

With this choice of approximating model, it turns out that

where

)y|(ˆ ntgt E α=α,

,1'xˆ

)'xˆ(

)'xˆ(t

β+α−

β+α−

=

+−α−=µ

tt

tt

eH

eyy

t

tttt

,

,1'xˆ

)'xˆ(

)'xˆ(t

β+α−

β+α−

=

+−α−=µ

tt

tt

eH

eyy

t

tttt

23

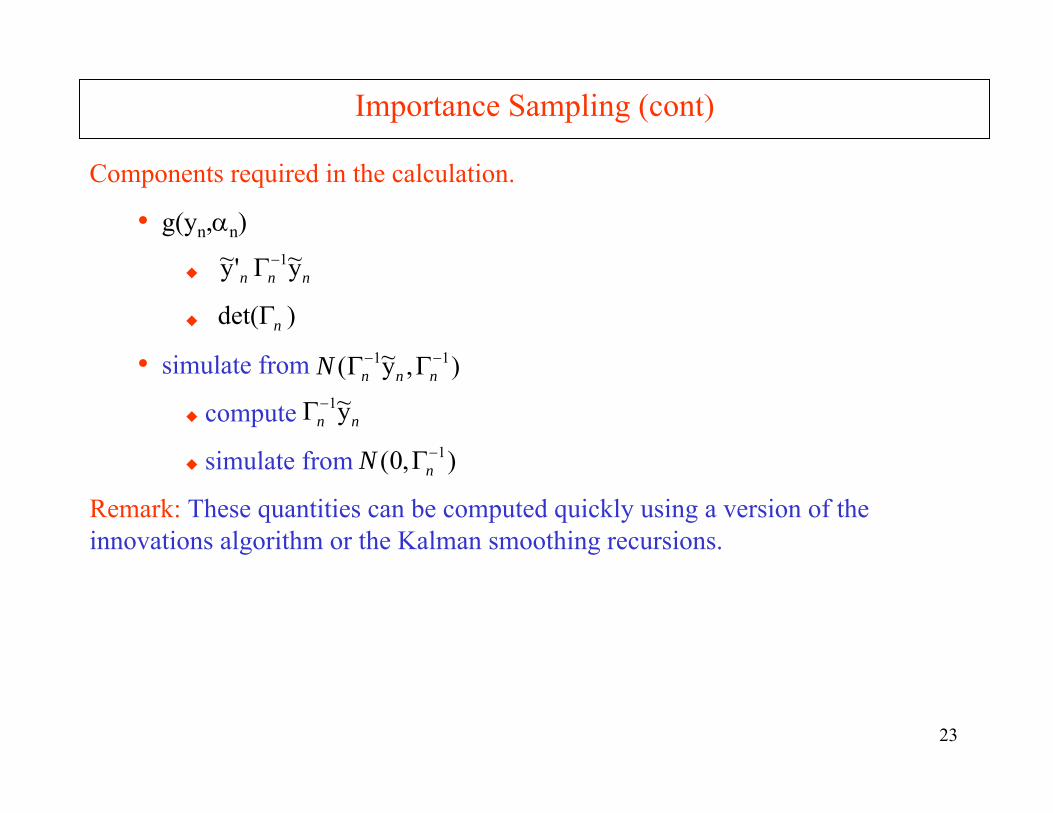

Importance Sampling (cont)

Components required in the calculation.

• g(yn,αn)

• simulate from

compute

simulate from

Remark: These quantities can be computed quickly using a version of the innovations algorithm or the Kalman smoothing recursions.

nnn y~'y~ 1−Γ

)det( nΓ

),y~( 11 −− ΓΓ nnnN

nn y~1−Γ

),0( 1−ΓnN

24

Importance Sampling — example

Simulation example: β = .7, φ = .5, σ2=.3, n = 200, N = 1000, 50 realizations plotted

phi_0=-0.5

likel

ihoo

d

-1.0 -0.5 0.0 0.5 1.0

180

220

260

300

phi_0=-0.25

likel

ihoo

d-1.0 -0.5 0.0 0.5 1.0

200

220

240

260

280

phi_0=0

likel

ihoo

d

-1.0 -0.5 0.0 0.5 1.0

160

180

200

220

240

260

280

phi_0=0.25

likel

ihoo

d

-1.0 -0.5 0.0 0.5 1.0

150

200

250

phi_0=0.5

likel

ihoo

d

-1.0 -0.5 0.0 0.5 1.0

5010

015

020

025

0

phi_0=0.75

likel

ihoo

d

-1.0 -0.5 0.0 0.5 1.050

100

150

200

250

26

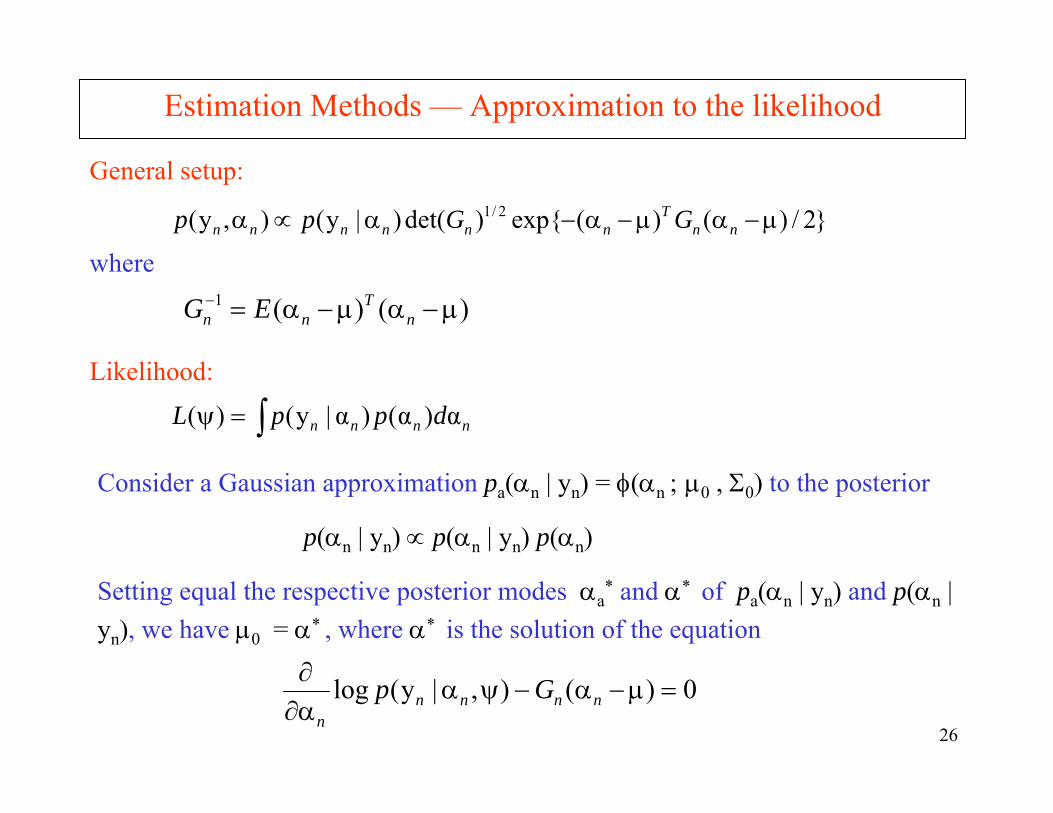

Consider a Gaussian approximation pa(αn | yn) = φ(αn ; µ0 , Σ0) to the posterior

p(αn | yn) ∝ p(αn | yn) p(αn)

Setting equal the respective posterior modes αa* and α* of pa(αn | yn) and p(αn |

yn), we have µ0 = α* , where α* is the solution of the equation

Estimation Methods — Approximation to the likelihood

General setup:

where

Likelihood:

2/)()(exp)det()|y(),y( 2/1 µ−αµ−α−α∝α nnT

nnnnnn GGpp 2/)()(exp)det()|y(),y( 2/1 µ−αµ−α−α∝α nnT

nnnnnn GGpp

)()(1 µ−αµ−α=−n

Tnn EG )()(1 µ−αµ−α=−

nT

nn EG

nnnn dppL α)α()α|y()( ∫=ψ nnnn dppL α)α()α|y()( ∫=ψ

0)(),|y(log =µ−α−ψαα∂∂

nnnnn

Gp 0)(),|y(log =µ−α−ψαα∂∂

nnnnn

Gp

27

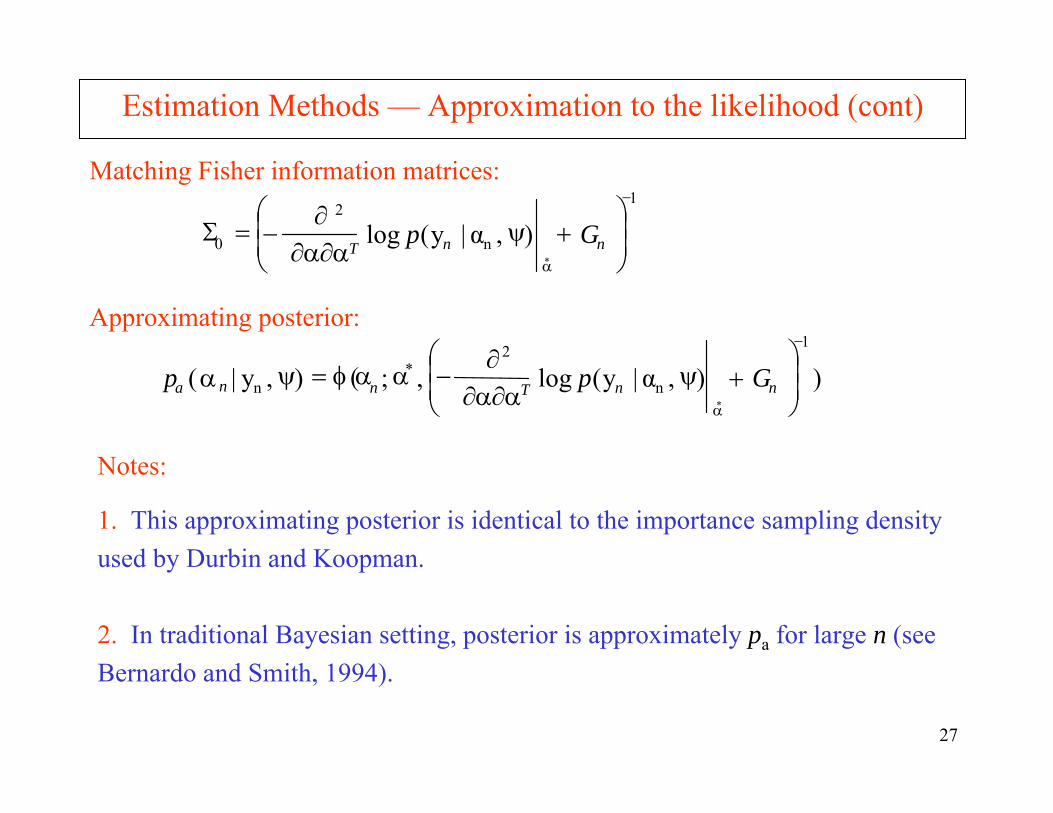

Notes:

1. This approximating posterior is identical to the importance sampling density used by Durbin and Koopman.

Estimation Methods — Approximation to the likelihood (cont)

Matching Fisher information matrices:

Approximating posterior:

2. In traditional Bayesian setting, posterior is approximately pa for large n (see Bernardo and Smith, 1994).

1

n

2

0*

),α|y(log−

α⎟⎟⎠

⎞⎜⎜⎝

⎛+ψ

α∂α∂∂

−=Σ nnTGp

)),α|y(log,;(),y|(1

n

2*

n*

−

α⎟⎟⎠

⎞⎜⎜⎝

⎛+ψ

α∂α∂∂

−ααφ=ψα nnTnna Gpp

28

2/1

n

2

***n

2/1

n***

nn

*

),α|y(logdet

2/)()(exp),|y(||

),y|(/),(),|y()y;(

⎟⎟⎠

⎞⎜⎜⎝

⎛+ψ

α∂α∂∂−

µ−αµ−α−ψα=

ψαψαψα=ψ

αnnT

nT

n

aa

Gp

GpG

pppL

Estimation Methods — Approximation to the likelihood (cont)

Approximate likelihood: Note that

which by solving for L in the expression,

pa(αn* | yn, ψ) = p(αn

* | yn,ψ),

,)y;(

)α()α|y()y|(α n

nnnnn L

pppψ

=

we obtain

,)y;(

)α()α|y()y|(α n

nnnnn L

pppψ

=

2/1

n

2

***n

2/1

n***

nn

*

),α|y(logdet

2/)()(exp),|y(||

),y|(/),(),|y()y;(

⎟⎟⎠

⎞⎜⎜⎝

⎛+ψ

α∂α∂∂−

µ−αµ−α−ψα=

ψαψαψα=ψ

αnnT

nT

n

aa

Gp

GpG

pppL

29

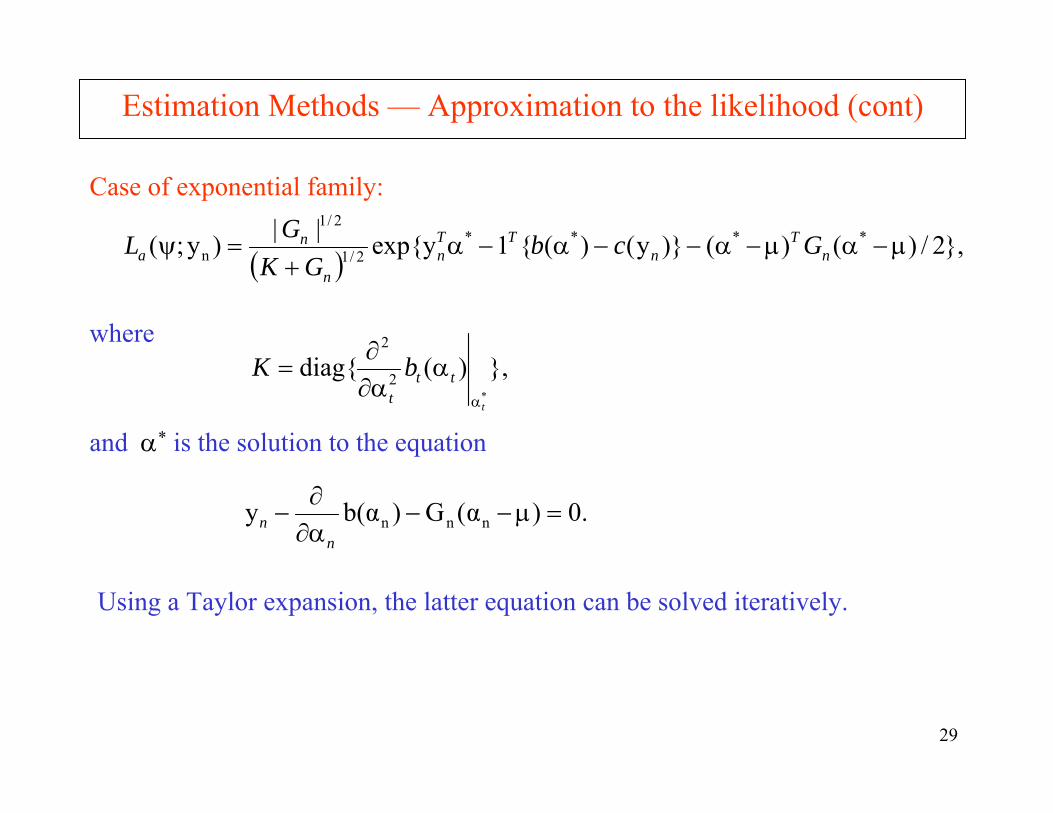

Estimation Methods — Approximation to the likelihood (cont)

Case of exponential family:

where

and α* is the solution to the equation

( ),2/)()()y()(1yexp||)y;( ****

2/1

2/1

n µ−αµ−α−−α−α+

=ψ nT

nTT

nn

na Gcb

GKGL

,)(diag*

2

2

t

ttt

bKα

αα∂∂

=

.0)α(G)b(αy nnn =µ−−α∂∂

−n

n

Using a Taylor expansion, the latter equation can be solved iteratively.

30

Estimation Methods — Approximation to the likelihood

Implementation:

1. Let α∗= α∗(ψ) be the converged value of α(j) (ψ) , where

and

2. Maximize with respect to ψ.

),(y~)b()(α jn

-1j)1( ψ+=ψ+n

j G&&

);y( ψnap

.Gαbbyy~ n(j)jj

njn µ++−= &&&

31

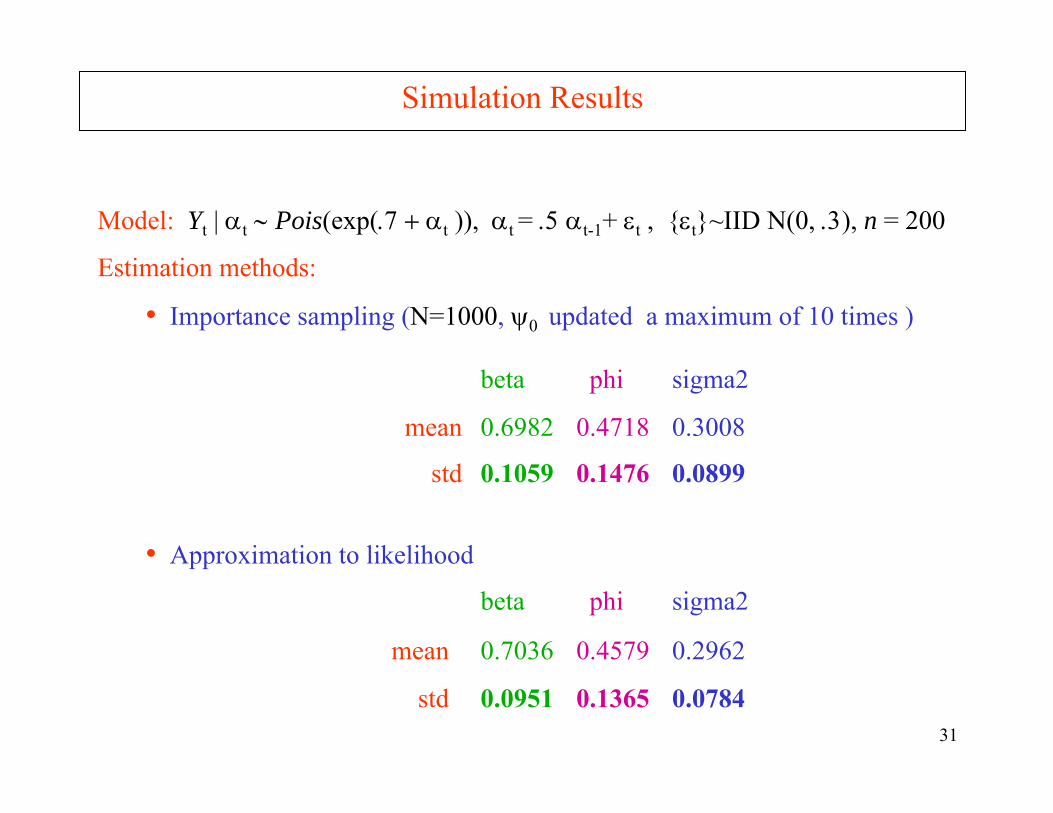

Model: Yt | αt ∼ Pois(exp(.7 + αt )), αt = .5 αt-1+ εt , εt~IID N(0, .3), n = 200

Estimation methods:

• Importance sampling (N=1000, ψ0 updated a maximum of 10 times )

beta phi sigma2

mean 0.6982 0.4718 0.3008

std 0.1059 0.1476 0.0899

Simulation Results

• Approximation to likelihood

beta phi sigma2

mean 0.7036 0.4579 0.2962

std 0.0951 0.1365 0.0784

32

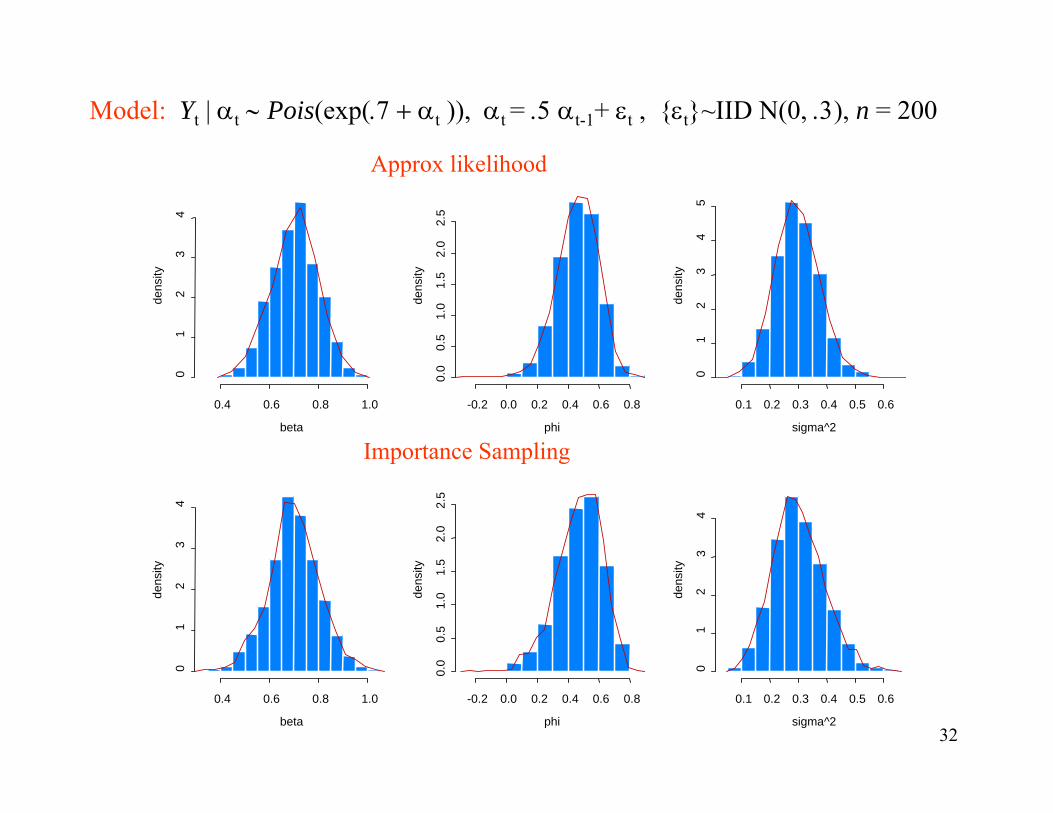

Model: Yt | αt ∼ Pois(exp(.7 + αt )), αt = .5 αt-1+ εt , εt~IID N(0, .3), n = 200

0.4 0.6 0.8 1.0

01

23

4

beta

dens

ity

-0.2 0.0 0.2 0.4 0.6 0.8

0.0

0.5

1.0

1.5

2.0

2.5

phide

nsity

0.1 0.2 0.3 0.4 0.5 0.6

01

23

45

sigma^2

dens

ity

Approx likelihood

0.4 0.6 0.8 1.0

01

23

4

beta

dens

ity

-0.2 0.0 0.2 0.4 0.6 0.8

0.0

0.5

1.0

1.5

2.0

2.5

phi

dens

ity

0.1 0.2 0.3 0.4 0.5 0.60

12

34

sigma^2

dens

ity

Importance Sampling

33

Approx Like Simulation

0.202 0.210 0.343 -2.690 -2.720 3.4150.113 0.111 0.123-0.454 -0.454 0.1430.396 0.400 0.1140.016 0.012 0.1100.845 0.764 0.1650.104 0.114 0.075

ISˆ β Mean SD

Model for αt:αt = φαt-1+εt , εt~IID N(0, σ2).

• Importance sampling ( ψ0 updated 5 times for each N=100, 500, 1000, )• Simulation based on 1000 replications and the fitted AL model.

Application to Model Fitting for the Polio Data

Import Sampling Simulation

Intercept 0.203 0.223 0.381Trend(×10-3) -2.675 -2.778 3.979cos(2πt/12) 0.110 0.103 0.124sin(2πt/12) -0.456 -0.456 0.151cos(2πt/6) 0.399 0.401 0.123sin(2πt/6) 0.015 0.024 0.118 φ 0.865 0.777 0.198 σ2 0.088 0.100 0.068

ALˆ β Mean SD GLM

ˆ β SD

GLM

.207 0.078-4.18 1.400-.152 0.097-.532 0.109.169 0.098-.432 0.101

34

-15 -10 -5 0 5

0.0

0.04

0.08

0.12

beta1

dens

ity

-0.2 0.2 0.4 0.6 0.8 1.00

12

34

phi

dens

ity

0.0 0.1 0.2 0.3 0.4

02

46

sigma^2

dens

ity

Application to Model Fitting for the Polio Data (cont)

Approx Likelihood

-15 -10 -5 0 5

0.0

0.02

0.04

0.06

0.08

0.10

beta1

dens

ity

-0.2 0.2 0.4 0.6 0.8 1.0

01

23

4

phi

dens

ity

0.0 0.1 0.2 0.3 0.4

02

46

simga^2

dens

ity

Importance Sampling

35

Simulation Results

Stochastic volatility model:Yt = σt Zt , Zt~IID N(0,1)

αt = γ + φαt-1 + εt , εt~IID N(0,σ2), where αt = 2 log σt ; n=1000, NR=500

RMSE RMSE

.210 .216

.025 .026

.065 .073

True AL

γ −.411 −.491

φ 0.950 0.940

σ 0.484 0.478

IS

−.490

0.940

0.481

RMSE RMSE

.341 .324

.046 .043

.068 .068

True AL

γ −.368 −.499

φ 0.950 0.932

σ 0.260 0.270

IS

−.485

0.934

0.268

CV=10

CV=1

36

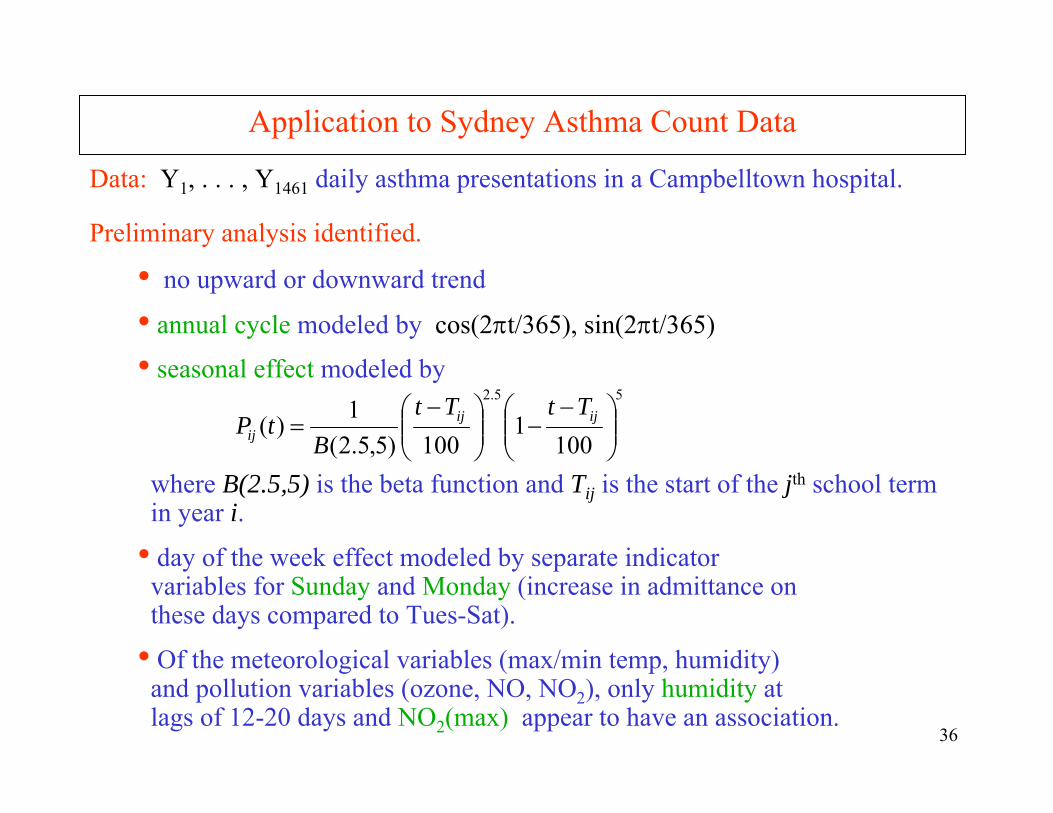

Application to Sydney Asthma Count Data

Data: Y1, . . . , Y1461 daily asthma presentations in a Campbelltown hospital.

Preliminary analysis identified.

• no upward or downward trend

• annual cycle modeled by cos(2πt/365), sin(2πt/365)

• seasonal effect modeled by

where B(2.5,5) is the beta function and Tij is the start of the jth school term in year i.

• day of the week effect modeled by separate indicatorvariables for Sunday and Monday (increase in admittance on these days compared to Tues-Sat).

• Of the meteorological variables (max/min temp, humidity)and pollution variables (ozone, NO, NO2), only humidity at lags of 12-20 days and NO2(max) appear to have an association.

55.2

1001

100)5,5.2(1)( ⎟⎟

⎠

⎞⎜⎜⎝

⎛ −−⎟⎟

⎠

⎞⎜⎜⎝

⎛ −= ijij

ij

TtTtB

tP

37

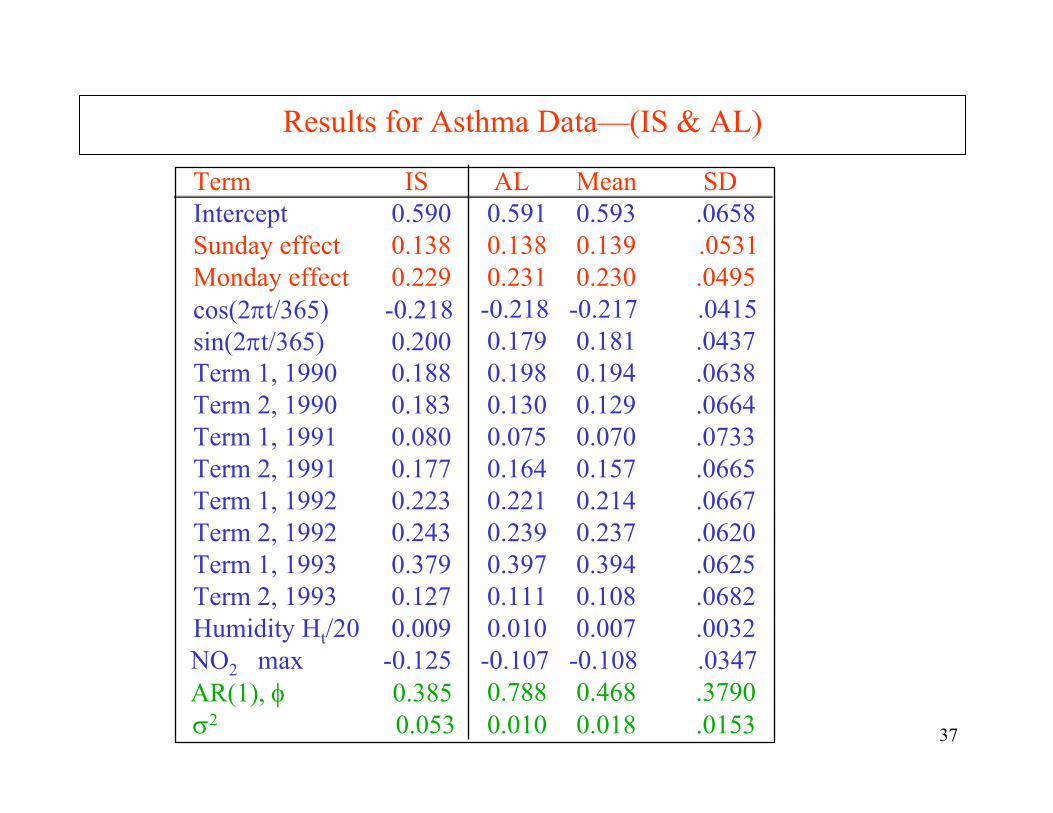

Results for Asthma Data—(IS & AL)

Term IS Intercept 0.590Sunday effect 0.138Monday effect 0.229cos(2πt/365) -0.218 sin(2πt/365) 0.200Term 1, 1990 0.188Term 2, 1990 0.183Term 1, 1991 0.080Term 2, 1991 0.177Term 1, 1992 0.223Term 2, 1992 0.243Term 1, 1993 0.379Term 2, 1993 0.127Humidity Ht/20 0.009NO2 max -0.125 AR(1), φ 0.385σ2 0.053

AL Mean SD0.591 0.593 .06580.138 0.139 .05310.231 0.230 .0495-0.218 -0.217 .04150.179 0.181 .04370.198 0.194 .06380.130 0.129 .06640.075 0.070 .07330.164 0.157 .06650.221 0.214 .06670.239 0.237 .06200.397 0.394 .06250.111 0.108 .06820.010 0.007 .0032-0.107 -0.108 .03470.788 0.468 .37900.010 0.018 .0153

38

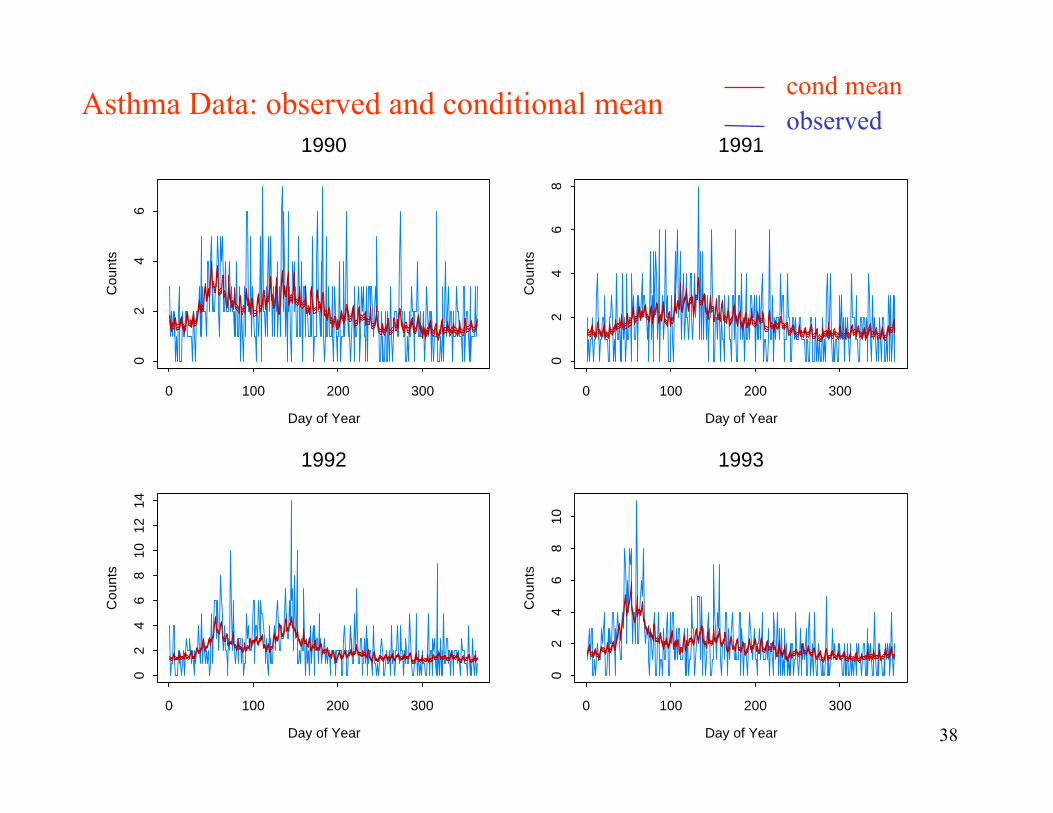

Asthma Data: observed and conditional mean cond meanobserved

1990

Day of Year

Cou

nts

0 100 200 300

02

46

1991

Day of Year

Cou

nts

0 100 200 300

02

46

8

1992

Day of Year

Cou

nts

0 100 200 300

02

46

810

1214

1993

Day of Year

Cou

nts

0 100 200 300

02

46

810

39

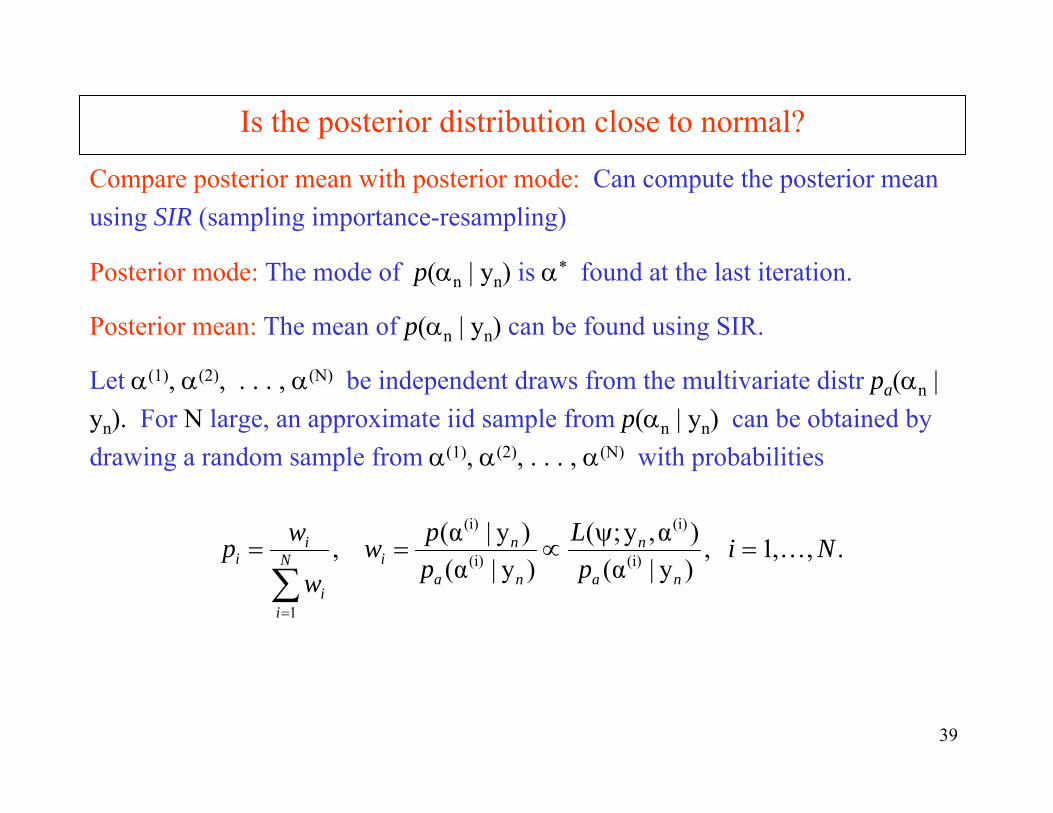

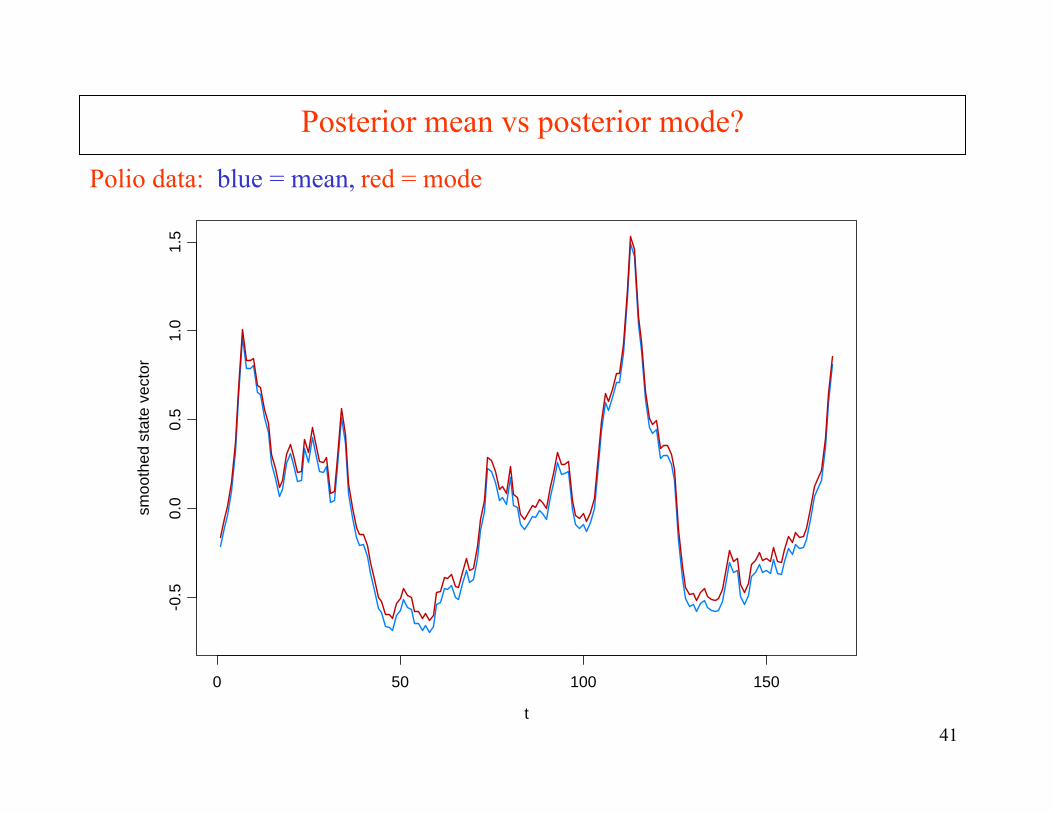

Is the posterior distribution close to normal?

Compare posterior mean with posterior mode: Can compute the posterior mean using SIR (sampling importance-resampling)

Posterior mode: The mode of p(αn | yn) is α* found at the last iteration.

Posterior mean: The mean of p(αn | yn) can be found using SIR.

Let α(1), α(2), . . . , α(N) be independent draws from the multivariate distr pa(αn | yn). For N large, an approximate iid sample from p(αn | yn) can be obtained bydrawing a random sample from α(1), α(2), . . . , α(N) with probabilities

.,,1 ,)y|(α)α,y;(

)y|(α)y|(α , (i)

(i)

(i)

(i)

1

Nip

Lppw

w

wpna

n

na

niN

ii

ii K=

ψ∝==

∑=

41

Posterior mean vs posterior mode?

Polio data: blue = mean, red = mode

t

smoo

thed

sta

te v

ecto

r

0 50 100 150

-0.5

0.0

0.5

1.0

1.5

44

Summary Remarks

1. Importance sampling offers a nice clean method for estimation in parameter driven models.

2. The innovations algorithm allows for quick implementation of importance sampling. Extends easily to higher-order AR structure.

3. Relative likelihood approach is a one-sample based procedure.

4. Approximation to the likelihood is a non-simulation based procedure which may have great potential especially with large sample sizes and/or large number of explanatory variables.

5. Approximation likelihood approach is amenable to boostrapping procedures for bias correction.