revised fiscal note h.b. 235 2015 general session ...le.utah.gov/lfa/fnotes/2015/hb0235.fn.pdf ·...

TRANSCRIPT

H.B

. 235

2015/02/26 10:43, Lead Analyst: Andrea Wilko Attorney: PLA

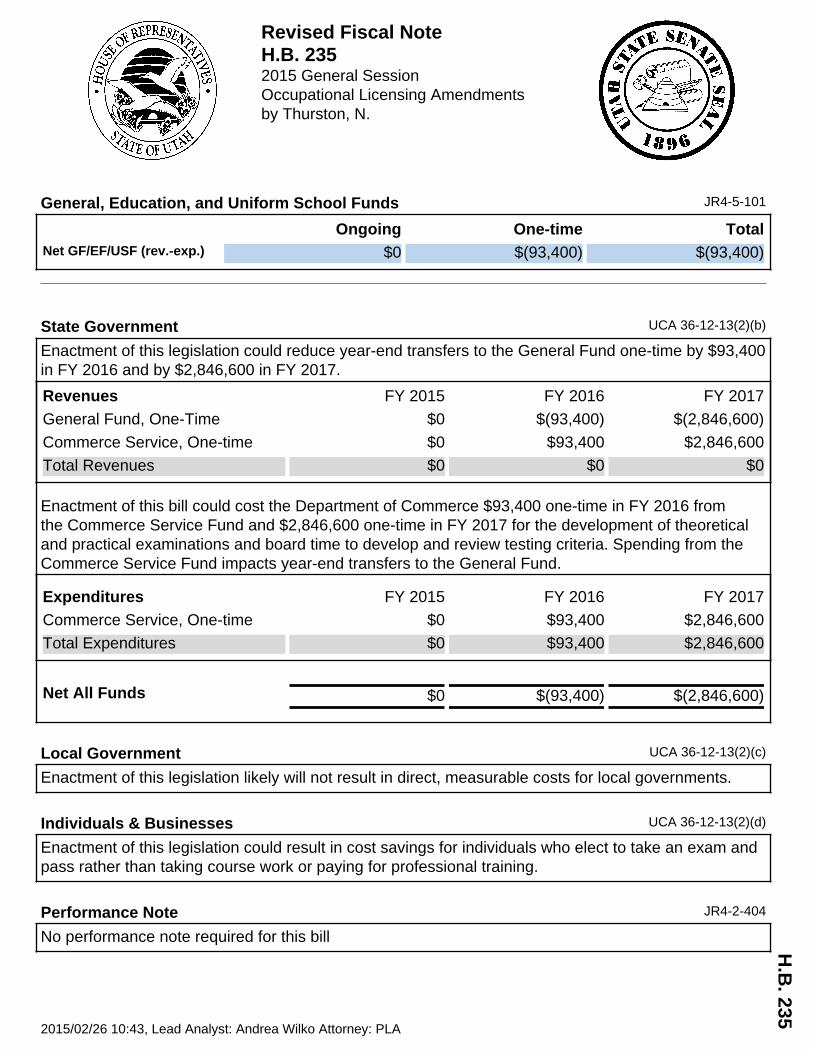

Revised Fiscal NoteH.B. 2352015 General SessionOccupational Licensing Amendmentsby Thurston, N.

General, Education, and Uniform School Funds JR4-5-101

Ongoing One-time TotalNet GF/EF/USF (rev.-exp.) $0 $(93,400) $(93,400)

State Government UCA 36-12-13(2)(b)

Enactment of this legislation could reduce year-end transfers to the General Fund one-time by $93,400in FY 2016 and by $2,846,600 in FY 2017.

Revenues FY 2015 FY 2016 FY 2017

General Fund, One-Time $0 $(93,400) $(2,846,600)

Commerce Service, One-time $0 $93,400 $2,846,600

Total Revenues $0 $0 $0

Enactment of this bill could cost the Department of Commerce $93,400 one-time in FY 2016 fromthe Commerce Service Fund and $2,846,600 one-time in FY 2017 for the development of theoreticaland practical examinations and board time to develop and review testing criteria. Spending from theCommerce Service Fund impacts year-end transfers to the General Fund.

Expenditures FY 2015 FY 2016 FY 2017

Commerce Service, One-time $0 $93,400 $2,846,600

Total Expenditures $0 $93,400 $2,846,600

Net All Funds $0 $(93,400) $(2,846,600)

Local Government UCA 36-12-13(2)(c)

Enactment of this legislation likely will not result in direct, measurable costs for local governments.

Individuals & Businesses UCA 36-12-13(2)(d)

Enactment of this legislation could result in cost savings for individuals who elect to take an exam andpass rather than taking course work or paying for professional training.

Performance Note JR4-2-404

No performance note required for this bill

H.B

. 235

2015/02/26 10:43, Lead Analyst: Andrea Wilko Attorney: PLA

Notes on NotesFiscal notes estimate the direct costs or revenues of enacting a bill. The Legislature uses them to balance the budget. They do not measure a bill'sbenefits or non-fiscal impacts like opportunity costs, wait times, or inconvenience. A fiscal note is not an appropriation. The Legislature decidesappropriations separately.