retirement & pension planning slides

DESCRIPTION

How to planning your retirementTRANSCRIPT

RETIREMENT & PENSION

PLANNING

What is Retirement?

Retirement is the beginning of a new stage of life after

working.

Planning your retirement is a very personal process, not

simply following a one-size-fits-all plan.

Retirement plan should be based on your vision of the life

you hope to lead, and must also take your financial picture

into account.

The best time to start planning your retirement is while

you're still working.

Some questions to ask yourself:

•Do I want to retire?

•How do I want to spend my time

in retirement?

•How will I handle not having to go

to work?

•How much income will I need in

retirement?

•Am I psychologically ready to

retire?

•What impact will my retirement

have on my family?

•What if I don't retire and instead

keep on working like I am now?

EPF / KUMPULAN WANG SIMPANAN

PEKERJA

www.kwsp.gov.my

KUMPULAN WANG PERSARAAN

www.kwap.gov.my

PLANNING FOR YOUR

RETIREMENT

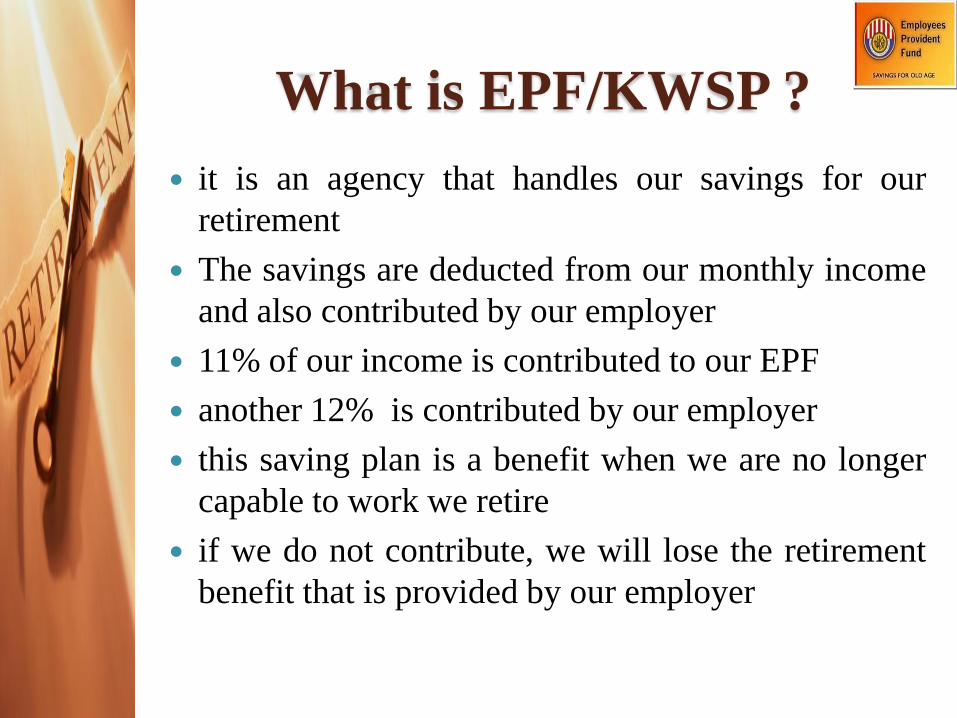

What is EPF/KWSP ?

it is an agency that handles our savings for our

retirement

The savings are deducted from our monthly income

and also contributed by our employer

11% of our income is contributed to our EPF

another 12% is contributed by our employer

this saving plan is a benefit when we are no longer

capable to work we retire

if we do not contribute, we will lose the retirement

benefit that is provided by our employer

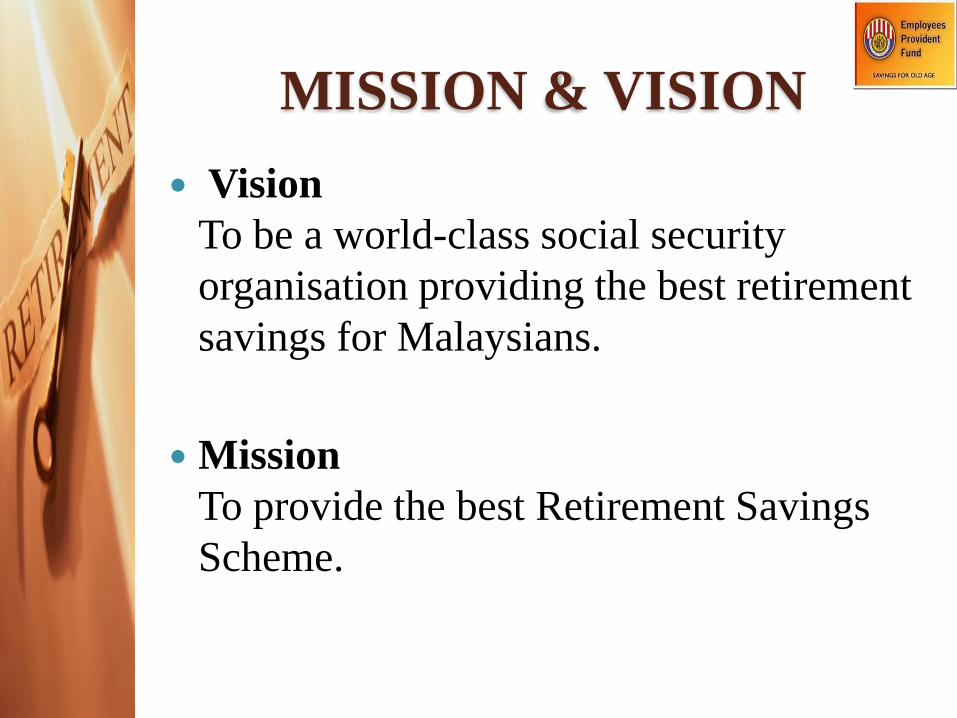

MISSION & VISION

Vision

To be a world-class social security

organisation providing the best retirement

savings for Malaysians.

Mission

To provide the best Retirement Savings

Scheme.

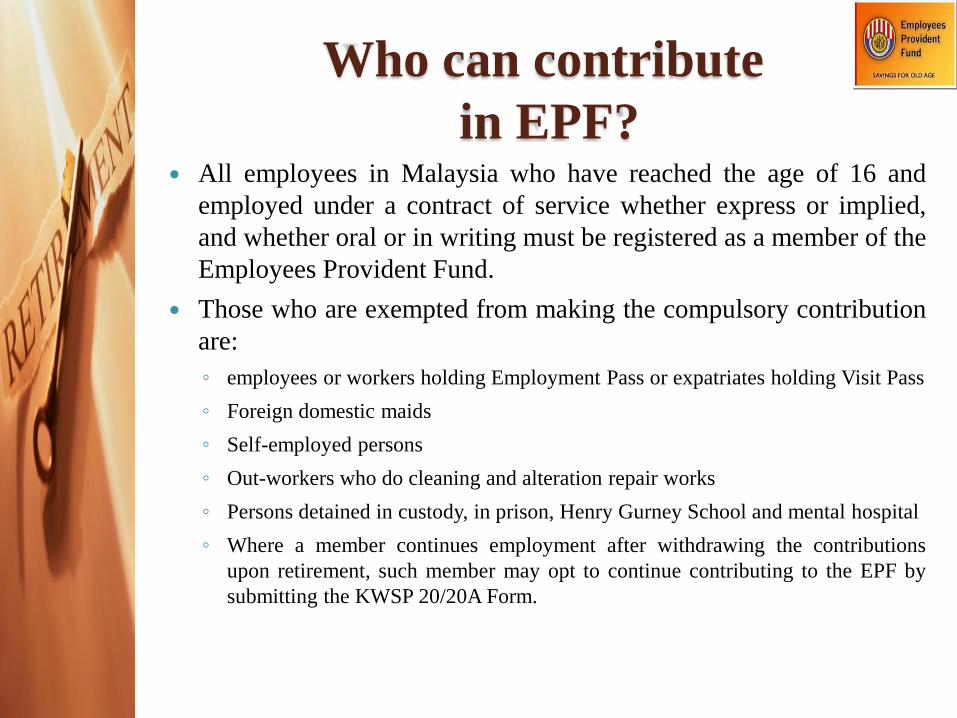

Who can contribute

in EPF? All employees in Malaysia who have reached the age of 16 and

employed under a contract of service whether express or implied,

and whether oral or in writing must be registered as a member of the

Employees Provident Fund.

Those who are exempted from making the compulsory contribution

are:

◦ employees or workers holding Employment Pass or expatriates holding Visit Pass

◦ Foreign domestic maids

◦ Self-employed persons

◦ Out-workers who do cleaning and alteration repair works

◦ Persons detained in custody, in prison, Henry Gurney School and mental hospital

◦ Where a member continues employment after withdrawing the contributions

upon retirement, such member may opt to continue contributing to the EPF by

submitting the KWSP 20/20A Form.

Benefits of EPF

Gain more than just an assured savings that will be

available to you upon your retirement.

Other benefits of EPF :

◦ Dividen

◦ Tax Incentive

◦ Retirement Benefits

◦ Death and Incapacitation Benefits

◦ Saving

◦ Investment

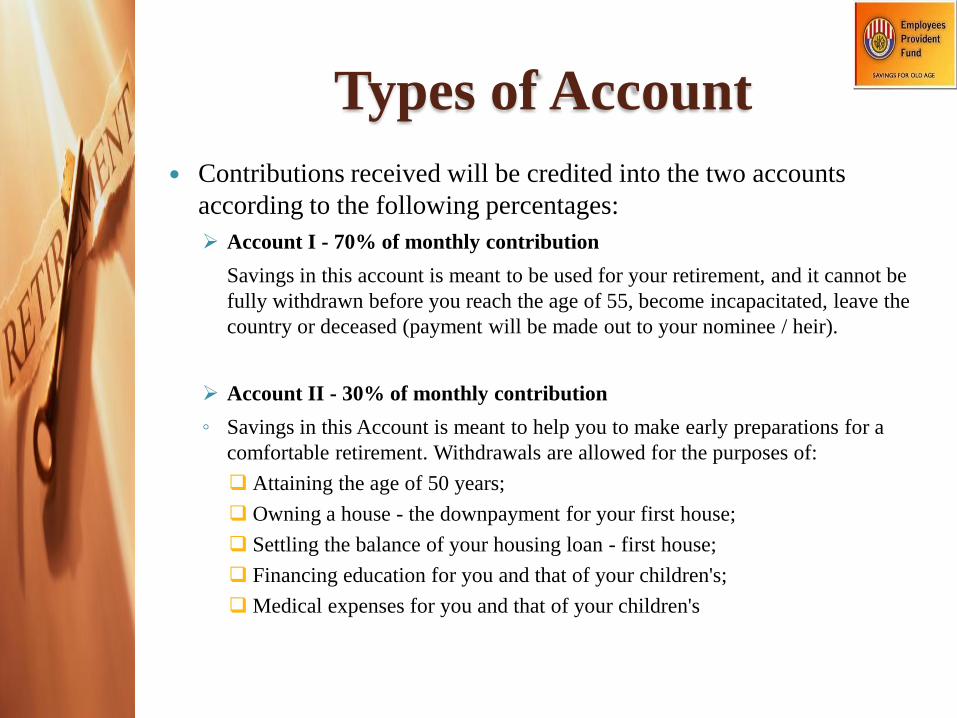

Types of Account

Contributions received will be credited into the two accounts

according to the following percentages:

Account I - 70% of monthly contribution

Savings in this account is meant to be used for your retirement, and it cannot be

fully withdrawn before you reach the age of 55, become incapacitated, leave the

country or deceased (payment will be made out to your nominee / heir).

Account II - 30% of monthly contribution

◦ Savings in this Account is meant to help you to make early preparations for a

comfortable retirement. Withdrawals are allowed for the purposes of:

Attaining the age of 50 years;

Owning a house - the downpayment for your first house;

Settling the balance of your housing loan - first house;

Financing education for you and that of your children's;

Medical expenses for you and that of your children's

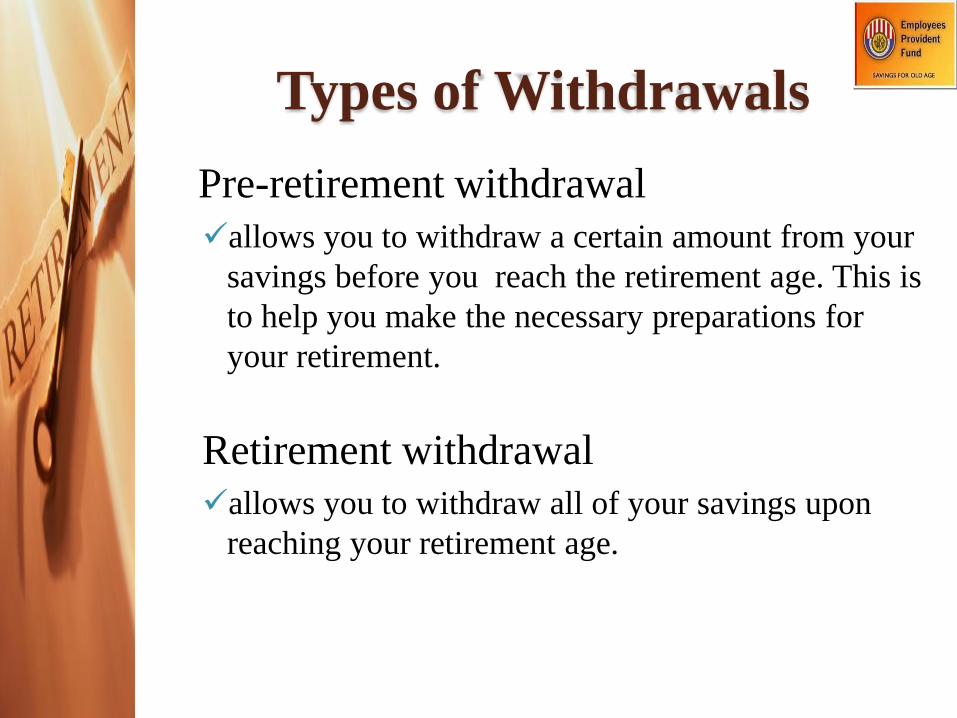

Types of Withdrawals

Pre-retirement withdrawal

allows you to withdraw a certain amount from your

savings before you reach the retirement age. This is

to help you make the necessary preparations for

your retirement.

Retirement withdrawal

allows you to withdraw all of your savings upon

reaching your retirement age.

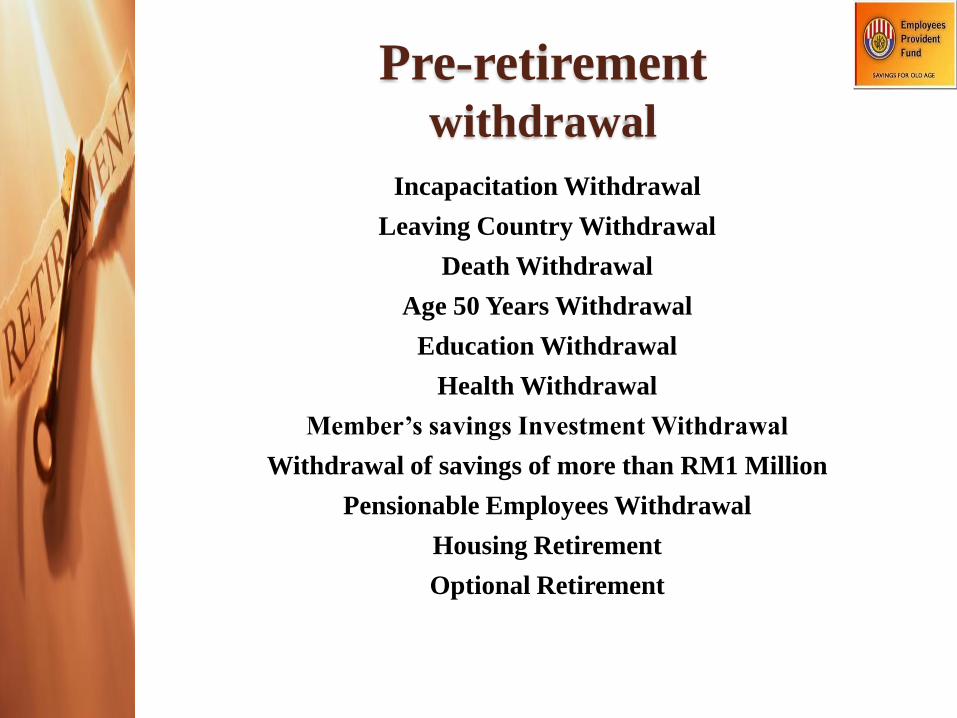

Pre-retirement withdrawal

Incapacitation Withdrawal

Leaving Country Withdrawal

Death Withdrawal

Age 50 Years Withdrawal

Education Withdrawal

Health Withdrawal

Member’s savings Investment Withdrawal

Withdrawal of savings of more than RM1 Million

Pensionable Employees Withdrawal

Housing Retirement

Optional Retirement

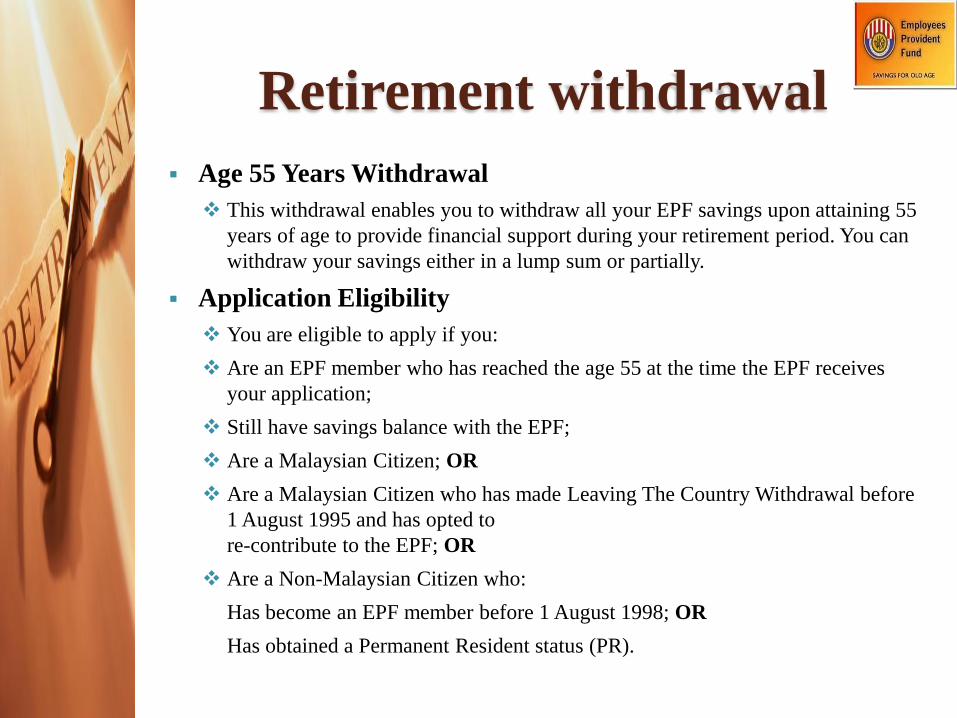

Retirement withdrawal

Age 55 Years Withdrawal

This withdrawal enables you to withdraw all your EPF savings upon attaining 55

years of age to provide financial support during your retirement period. You can

withdraw your savings either in a lump sum or partially.

Application Eligibility

You are eligible to apply if you:

Are an EPF member who has reached the age 55 at the time the EPF receives

your application;

Still have savings balance with the EPF;

Are a Malaysian Citizen; OR

Are a Malaysian Citizen who has made Leaving The Country Withdrawal before

1 August 1995 and has opted to

re-contribute to the EPF; OR

Are a Non-Malaysian Citizen who:

Has become an EPF member before 1 August 1998; OR

Has obtained a Permanent Resident status (PR).

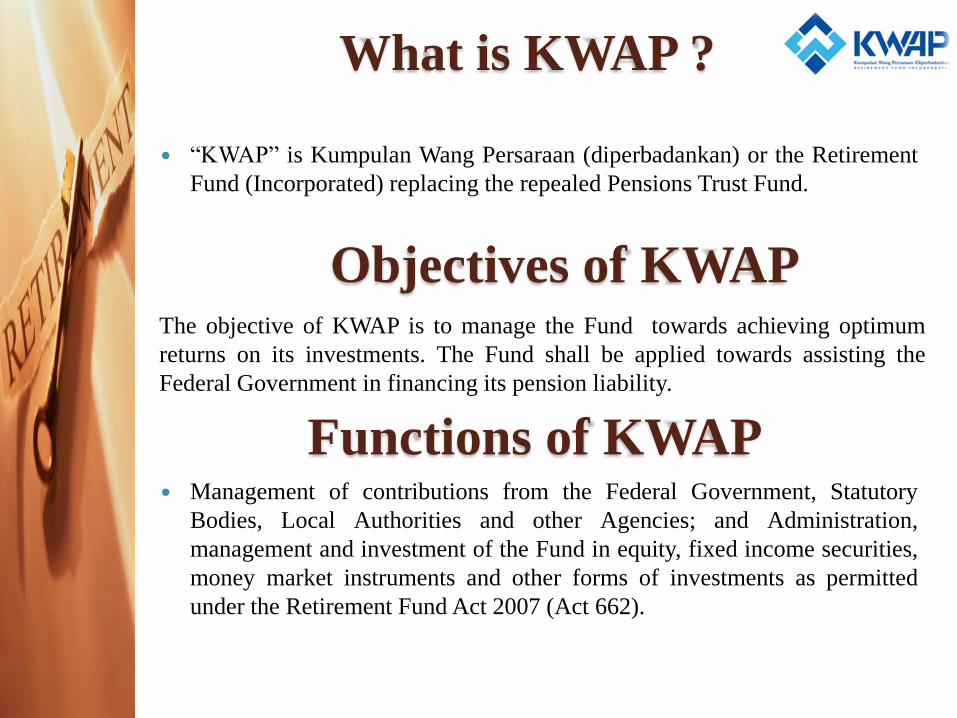

What is KWAP ?

“KWAP” is Kumpulan Wang Persaraan (diperbadankan) or the Retirement

Fund (Incorporated) replacing the repealed Pensions Trust Fund.

Objectives of KWAPThe objective of KWAP is to manage the Fund towards achieving optimum

returns on its investments. The Fund shall be applied towards assisting the

Federal Government in financing its pension liability.

Functions of KWAP Management of contributions from the Federal Government, Statutory

Bodies, Local Authorities and other Agencies; and Administration,

management and investment of the Fund in equity, fixed income securities,

money market instruments and other forms of investments as permitted

under the Retirement Fund Act 2007 (Act 662).

About KWAP

Main responsibilities is to manage pension contributions which are

remitted to KWAP by contributing employers in accordance to the

Statutory and Local Authorities Pensions Acts 1980 (Act 239) and

Service Circular No 12/2008 on the Policy and Procedure of

Appointment of Secondment, Temporary and Permanent Transfer.

As stipulated by the Act, contributing employers comprising of

statutory bodies, local authorities and agencies shall remit to KWAP

the pension contributions for employees who are granted

pensionable status by the Public Service Department

Mission & Vision

Mission

Maximising returns through benchmarking,

dynamic investment framework and sound

risk management.

Vision

A high performing fund assuring sustainable

pension benefits.

Malaysia Provident/

Pension Fund Value Chain

The diagram below illustrates Malaysia's provident/ pension fund value

chain with KWAP's role in the context of pensionable civil service.

RegistrationEmployer’s :

An organization, statutory body and local authority is under a

duty to register with KWAP as an employer under the following

circumstances :

A statutory bodies or local authority has been formed or

established.

Employees of the organization, statutory body and local

authority are conferred pensionable status by Public Service

Department.

The following documents must be submitted for registration

purposes:

Application letter by the employer.

A copy of the Act gazetting the establishment of the

organization as statutory body or local authority

Member’s Registration

It is the duty of the employer to register its pensionable employees

with KWAP upon the grant of the pensionable status by Public

Service Department.

Employers are required to submit the following documents for the

registration of its employees:

An application letter by the employer

Member's Registration Form (CP1)

A copy of approval letter by the Public Service Department on

the grant of pensionable status

Pension Contributions

Rate of Contribution

The rate of contribution is 17.5% of the pensionable employee's

basic salaries.

Payment Date

Payment of pension contribution shall be remitted to KWAP no later

than end of the following month

Late Payment

Late payment of pension contributions shall be subject to a penalty

at a rate of 0.5% of the unpaid amount

Penalties

Employers who fail to remit pension contributions within the

prescribed time shall be charged penalties under Section 8(4) of the

Statutory and Local Authorities Pensions Act 1980 (Act 239).

Penalties are charged at the rate 0.5% in respect of each month

default in payment for the amount remains unpaid.

Who can contribute?

KWSP

Private and non-

pensionable Public

Sector employees

KWAP

All statutory

bodies, local authorities

and agencies with

employees

of pensionable status

shall contribute to

KWAP

Difference between

KWSP & KWAP

KWSP manages contributions from private

sector employees and government employees

who opted to contribute to the EPF.

KWSP will send the annual Statement of

Account to members by post. Normally, the

statement will be sent to members to their

correspondence address that has been updated in

the EPF record.

Difference between

KWSP & KWAP

KWAP only manages contributions from

permanent government staff with pensionable

status and who are in service with Regulatory

Body and Local Authorities .

KWAP does not send out annual statements to

its contributors