restructuring crocs, inc. - turnaround...

TRANSCRIPT

RESTRUCTURING CROCS, INC.

Turnaround Management Columbia Business School

Advisor: Professor Laura Resnikoff April 26, 2010

Molly Bennard Kevin Sayles Ron Schulhof Julie Thaler John Wolff

1

TABLE OF CONTENTS

EXECUTIVE SUMMARY............................................................................................................ 2 INDUSTRY.....................................................................................................................................3 COMPANY...................................................................................................................................11 HISTORICAL FINANCIAL OVERVIEW...................................................................................22 DISCUSSION OF VALUATION ................................................................................................35 TURNAROUND PLAN ...............................................................................................................47 RECOMMENDATION.................................................................................................................51 EXHIBITS.....................................................................................................................................55 MARKETING MATERIAL……..................................................................................................65

2

EXECUTIVE SUMMARY

Crocs, Inc. is a designer, manufacturer and retailer of footwear for men, women and children. Crocs uses

its proprietary closed cell-resin, Croslite, to make shoes that are comfortable, lightweight and odor-

resistant. Since its introduction in 2002, Crocs has sold more than 120 million pairs of shoes in over 125

countries.

During the past two years, Crocs experienced a rapid decline in revenue, from a peak of $847.4 million in

2007 to a trough of $645.8 million in 2009. This decline proliferated throughout all regions in which the

Company operates, with the exception of Asia. Management attributes the deterioration in operating and

financial performance to a combination of macroeconomic factors (the global economic crisis resulted in

a reduction in consumer spending and decreased volume in malls and retail establishments) and difficulty

in executing Crocs’ long-term business strategy (significant challenges in merchandising an expanded

product line through existing wholesale channels, and both the declining demand for mature products and

the increasing competition from imitation products).

In response to these threats, the Company began a restructuring program and other downsizing activities

during FY08 and FY09. The combination of declining revenues, restructuring costs and other one-time

expenses resulted in the Company recording a loss of $185.1 million and $42.1 million during FY08 and

FY09, respectively.

We have reviewed trends in the footwear and apparel industry, closely examined the Company’s strategic,

operational and financial situation, and diagnosed the reasons for its distress. Despite recent

improvements in sales, margins, and the Company stock price, we believe that Crocs is in danger of

returning to the distress of 2008-2009. We recommend that Crocs implement a turnaround strategy with

the following key features:

Realign the distribution model in U.S. Crocs should forgo its retail expansion and instead

focus on a small number of profitable flagship stores and its wholesale and internet channels

Focus on the shoes and key customer segments. Crocs should refocus its entire organization

(design, manufacturing, marketing) on the unique appeal of its shoes

Management Information Systems and Supply Chain Logistics. Systems and supply chain

improvements should occupy a significant portion of management’s time until the issues are

satisfactorily resolved.

3

INDUSTRY

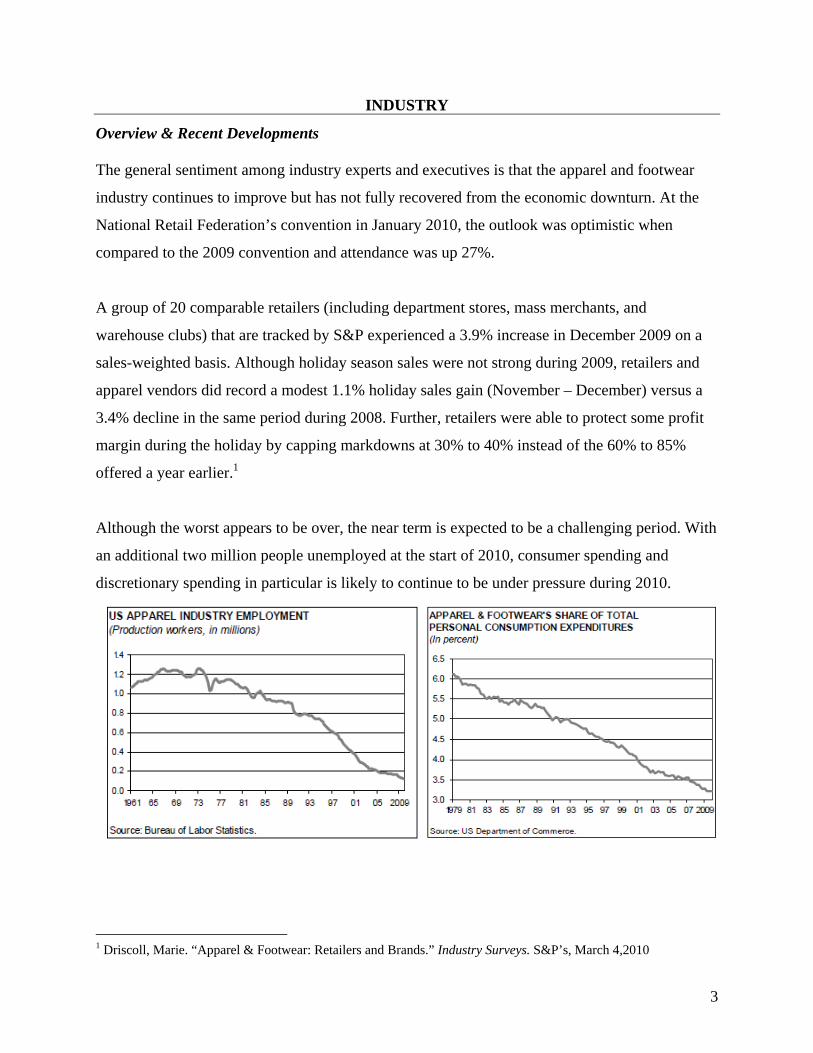

Overview & Recent Developments The general sentiment among industry experts and executives is that the apparel and footwear

industry continues to improve but has not fully recovered from the economic downturn. At the

National Retail Federation’s convention in January 2010, the outlook was optimistic when

compared to the 2009 convention and attendance was up 27%.

A group of 20 comparable retailers (including department stores, mass merchants, and

warehouse clubs) that are tracked by S&P experienced a 3.9% increase in December 2009 on a

sales-weighted basis. Although holiday season sales were not strong during 2009, retailers and

apparel vendors did record a modest 1.1% holiday sales gain (November – December) versus a

3.4% decline in the same period during 2008. Further, retailers were able to protect some profit

margin during the holiday by capping markdowns at 30% to 40% instead of the 60% to 85%

offered a year earlier.1

Although the worst appears to be over, the near term is expected to be a challenging period. With

an additional two million people unemployed at the start of 2010, consumer spending and

discretionary spending in particular is likely to continue to be under pressure during 2010.

1 Driscoll, Marie. “Apparel & Footwear: Retailers and Brands.” Industry Surveys. S&P’s, March 4,2010

4

Experts are predicting a sluggish consumer recovery with slow growth in 2010 and 2011. Due to

the high unemployment rate, S&P predicts that consumers cautiously manage purchases and

continue saving. Despite the negative outlook, there are two positive attributes to highlight:

Revenue has stabilized as inventories are no longer declining sharply. Because

inventory levels have been reduced to meet consumer demand, retailers now require

fewer markdowns to sell excess goods.

Markdowns are easing, resulting in recovering margins. As previously mentioned,

markdown expenses will be minimal when compared to 2008. Gross margins have

therefore recovered, and the current inventory/demand balance suggests footwear

companies should be able to maintain recent gains.2

S&P NetAdvantage suggests that because the majority of the possible cost initiatives have

already been completed, any additional initiatives will likely affect the direct to consumer parts

of the business and could further erode demand. S&P anticipates that companies will experience

increased general and administrative expenses.

Retailers have been implementing various aggressive strategies to contact and market to the

customer. In particular, despite decreased inventory levels, retailers have tried to maintain a

selective set of inventory on hand to cater to customer needs and support product differentiation.

Further, retailers are expected to increase efforts to market new products faster and to

incorporate current demand and fashion trends into new products.

Market Segments

Within the specialty retail industry, the footwear sub-industry segment can be divided into

several market segments including athletic wear, urban apparel, outdoor gear and casual shoes.

Additionally, the market can be subdivided into footwear and accessories. Based on recent

research distributed by S&P NetAdvantage and the Business & Company resource center, the

specialty retailing landscape remains fragmented (despite the proliferation of large chains and

superstore format), with thousands of small- to medium-sized businesses, often catering to local

tastes and preferences.

2 Driscoll, Marie. “Apparel & Footwear: Retailers and Brands.” Industry Surveys. S&P’s, March 4, 2010.

5

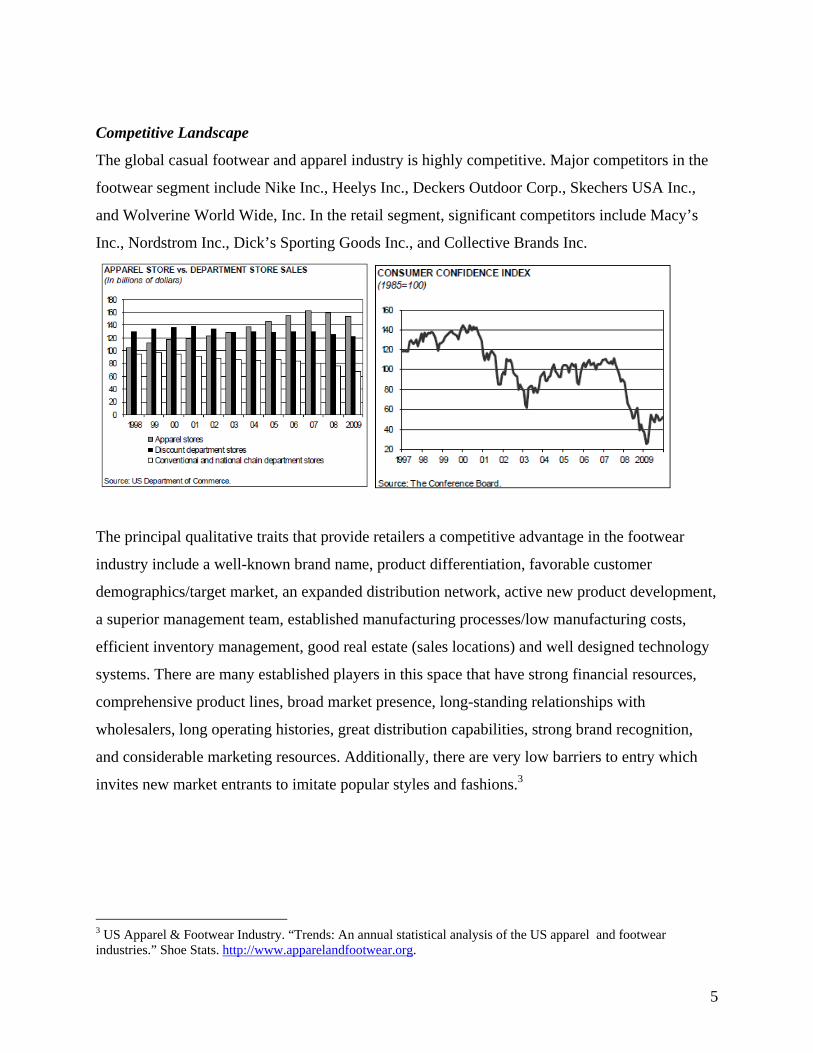

Competitive Landscape

The global casual footwear and apparel industry is highly competitive. Major competitors in the

footwear segment include Nike Inc., Heelys Inc., Deckers Outdoor Corp., Skechers USA Inc.,

and Wolverine World Wide, Inc. In the retail segment, significant competitors include Macy’s

Inc., Nordstrom Inc., Dick’s Sporting Goods Inc., and Collective Brands Inc.

The principal qualitative traits that provide retailers a competitive advantage in the footwear

industry include a well-known brand name, product differentiation, favorable customer

demographics/target market, an expanded distribution network, active new product development,

a superior management team, established manufacturing processes/low manufacturing costs,

efficient inventory management, good real estate (sales locations) and well designed technology

systems. There are many established players in this space that have strong financial resources,

comprehensive product lines, broad market presence, long-standing relationships with

wholesalers, long operating histories, great distribution capabilities, strong brand recognition,

and considerable marketing resources. Additionally, there are very low barriers to entry which

invites new market entrants to imitate popular styles and fashions.3

3 US Apparel & Footwear Industry. “Trends: An annual statistical analysis of the US apparel and footwear industries.” Shoe Stats. http://www.apparelandfootwear.org.

6

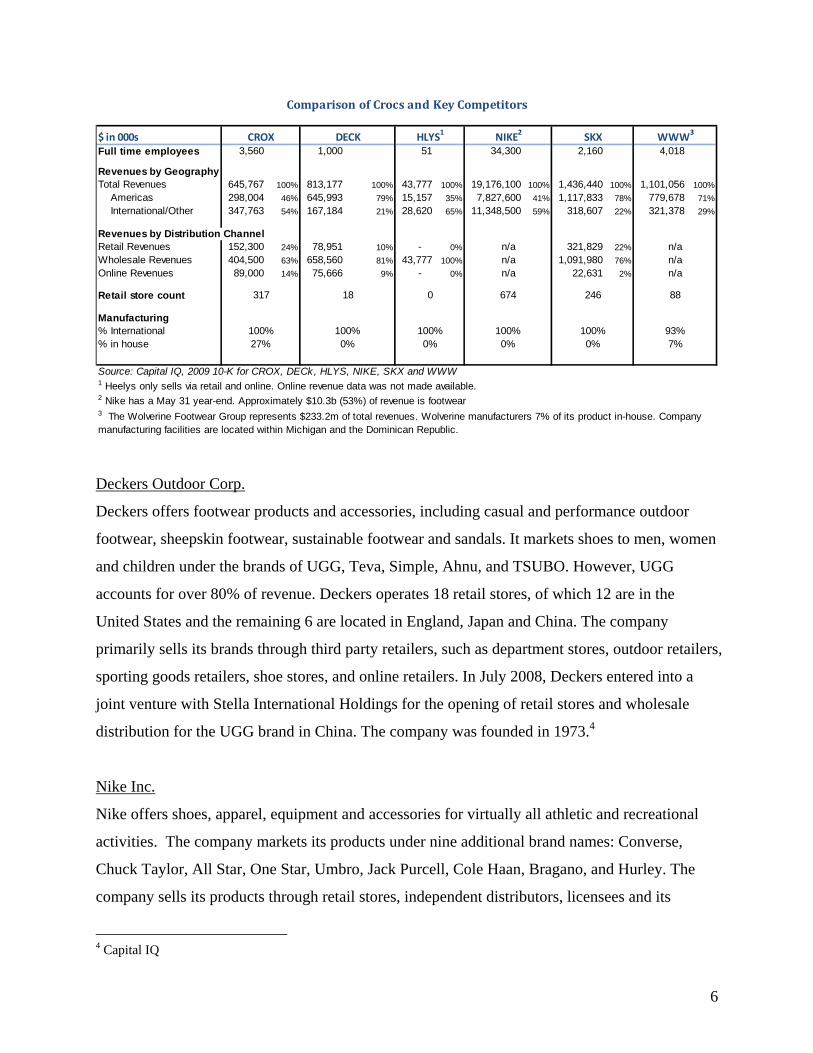

$ in 000sFull time employees 3,560 1,000 51 34,300 2,160 4,018

Revenues by GeographyTotal Revenues 645,767 100% 813,177 100% 43,777 100% 19,176,100 100% 1,436,440 100% 1,101,056 100%

Americas 298,004 46% 645,993 79% 15,157 35% 7,827,600 41% 1,117,833 78% 779,678 71%

International/Other 347,763 54% 167,184 21% 28,620 65% 11,348,500 59% 318,607 22% 321,378 29%

Revenues by Distribution ChannelRetail Revenues 152,300 24% 78,951 10% - 0% 321,829 22%

Wholesale Revenues 404,500 63% 658,560 81% 43,777 100% 1,091,980 76%

Online Revenues 89,000 14% 75,666 9% - 0% 22,631 2%

Retail store count

Manufacturing% International% in house

Source: Capital IQ, 2009 10-K for CROX, DECk, HLYS, NIKE, SKX and WWW1 Heelys only sells via retail and online. Online revenue data was not made available.2 Nike has a May 31 year-end. Approximately $10.3b (53%) of revenue is footwear

Comparison of Crocs and Key Competitors

3 The Wolverine Footwear Group represents $233.2m of total revenues. Wolverine manufacturers 7% of its product in-house. Company manufacturing facilities are located within Michigan and the Dominican Republic.

n/an/an/an/a

n/an/a

100%27%

93%7%0%

100%100%0%

317 18 0 674 246

0%100%0%

100%

88

CROX DECK HLYS1

NIKE2

SKX WWW3

Deckers Outdoor Corp.

Deckers offers footwear products and accessories, including casual and performance outdoor

footwear, sheepskin footwear, sustainable footwear and sandals. It markets shoes to men, women

and children under the brands of UGG, Teva, Simple, Ahnu, and TSUBO. However, UGG

accounts for over 80% of revenue. Deckers operates 18 retail stores, of which 12 are in the

United States and the remaining 6 are located in England, Japan and China. The company

primarily sells its brands through third party retailers, such as department stores, outdoor retailers,

sporting goods retailers, shoe stores, and online retailers. In July 2008, Deckers entered into a

joint venture with Stella International Holdings for the opening of retail stores and wholesale

distribution for the UGG brand in China. The company was founded in 1973.4

Nike Inc.

Nike offers shoes, apparel, equipment and accessories for virtually all athletic and recreational

activities. The company markets its products under nine additional brand names: Converse,

Chuck Taylor, All Star, One Star, Umbro, Jack Purcell, Cole Haan, Bragano, and Hurley. The

company sells its products through retail stores, independent distributors, licensees and its

4 Capital IQ

7

website. Nike has a significant presence abroad and a majority of their 2009 sales were

international. In addition, footwear revenues of $10.3 billion accounted for approximately 55%

of total revenues. Nike operates 338 retail stores in the United States and 336 retail stores

internationally. The company was founded in 1964.5

Heelys, Inc.

Heelys primarily offers their own branded wheeled shoes that allow wearers to easily transition

from walking or running to rolling (by shifting weight to the heel). The company also markets

non-wheeled footwear and accessories. Heelys sells its products to sporting goods retailers,

specialty apparel and footwear retailers, department stores, family footwear stores and online

retailers. The company was founded in 2000.6

Skechers USA, Inc.

Skechers offers a large variety of footwear products for men, women and kids. The company

markets its own brands, including Skechers Sport, Skechers Cali, Skechers Work and Skechers

Kids. The company sells its products at its own retail stores and website as well as through

department stores, specialty stores, athletic retailers, boutiques and catalog and internet retailers.

Skechers operates 219 retail stores in the United States, as well as 27 internationally. The

company was founded in 1992.7

Wolverine World Wide, Inc.

Wolverine World Wide offers footwear, apparel, and accessories in approximately 180 countries.

The company markets its products under the brands of Bates, Harley-Davidson Footwear, Hush

Puppies, Merrell, Patagonia Footwear and Wolverine. The company sells its products at

department stores, national chains, catalogs, specialty retailers, mass merchants, internet retailers

and governments and municipalities in the United States. Wolverine also operates 83 retail stores

in North America and 5 in the United Kingdom. The company was founded in 1883.8

5 Capital IQ, Company annual reports 6 Capital IQ 7 Ibid 8 Ibid

8

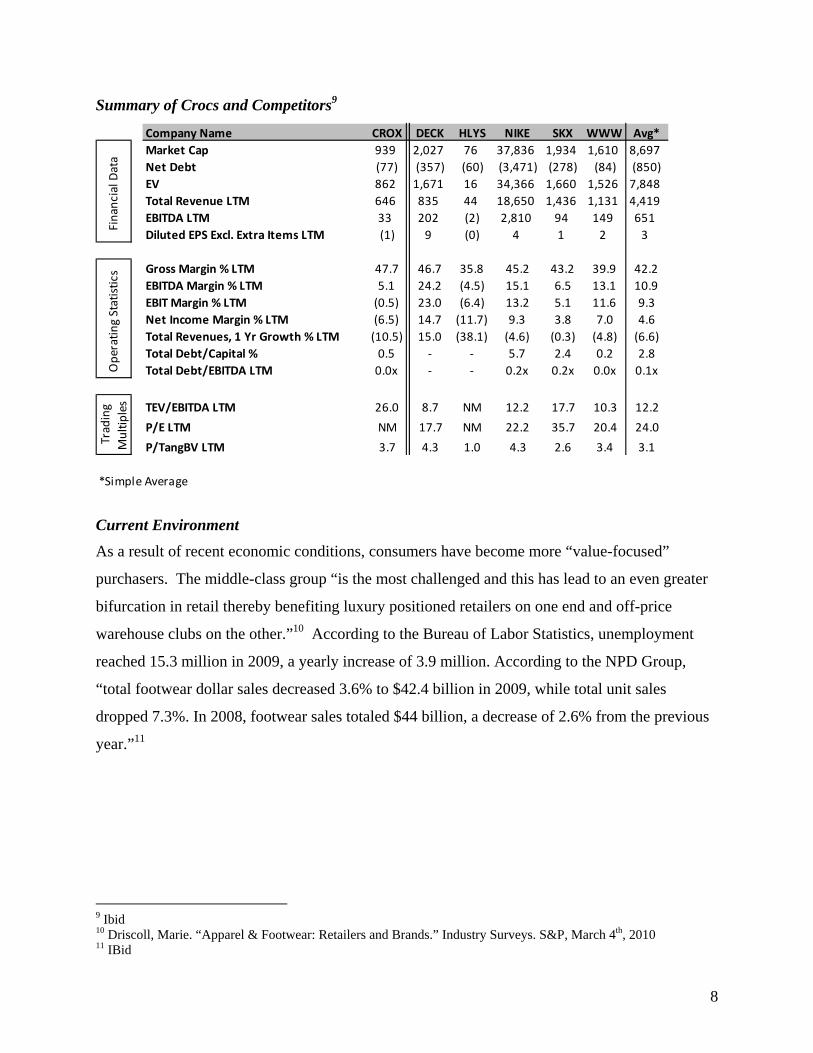

Summary of Crocs and Competitors9

Company Name CROX DECK HLYS NIKE SKX WWW Avg*

Market Cap 939 2,027 76 37,836 1,934 1,610 8,697

Net Debt (77) (357) (60) (3,471) (278) (84) (850)

EV 862 1,671 16 34,366 1,660 1,526 7,848

Total Revenue LTM 646 835 44 18,650 1,436 1,131 4,419

EBITDA LTM 33 202 (2) 2,810 94 149 651

Diluted EPS Excl. Extra Items LTM (1) 9 (0) 4 1 2 3

Gross Margin % LTM 47.7 46.7 35.8 45.2 43.2 39.9 42.2

EBITDA Margin % LTM 5.1 24.2 (4.5) 15.1 6.5 13.1 10.9

EBIT Margin % LTM (0.5) 23.0 (6.4) 13.2 5.1 11.6 9.3

Net Income Margin % LTM (6.5) 14.7 (11.7) 9.3 3.8 7.0 4.6

Total Revenues, 1 Yr Growth % LTM (10.5) 15.0 (38.1) (4.6) (0.3) (4.8) (6.6)

Total Debt/Capital % 0.5 ‐ ‐ 5.7 2.4 0.2 2.8

Total Debt/EBITDA LTM 0.0x ‐ ‐ 0.2x 0.2x 0.0x 0.1x

TEV/EBITDA LTM 26.0 8.7 NM 12.2 17.7 10.3 12.2

P/E LTM NM 17.7 NM 22.2 35.7 20.4 24.0

P/TangBV LTM 3.7 4.3 1.0 4.3 2.6 3.4 3.1

*Simple Average

Operating Statistics

Trading

Multiples

Financial Data

Current Environment

As a result of recent economic conditions, consumers have become more “value-focused”

purchasers. The middle-class group “is the most challenged and this has lead to an even greater

bifurcation in retail thereby benefiting luxury positioned retailers on one end and off-price

warehouse clubs on the other.”10 According to the Bureau of Labor Statistics, unemployment

reached 15.3 million in 2009, a yearly increase of 3.9 million. According to the NPD Group,

“total footwear dollar sales decreased 3.6% to $42.4 billion in 2009, while total unit sales

dropped 7.3%. In 2008, footwear sales totaled $44 billion, a decrease of 2.6% from the previous

year.”11

9 Ibid 10 Driscoll, Marie. “Apparel & Footwear: Retailers and Brands.” Industry Surveys. S&P, March 4th, 2010 11 IBid

9

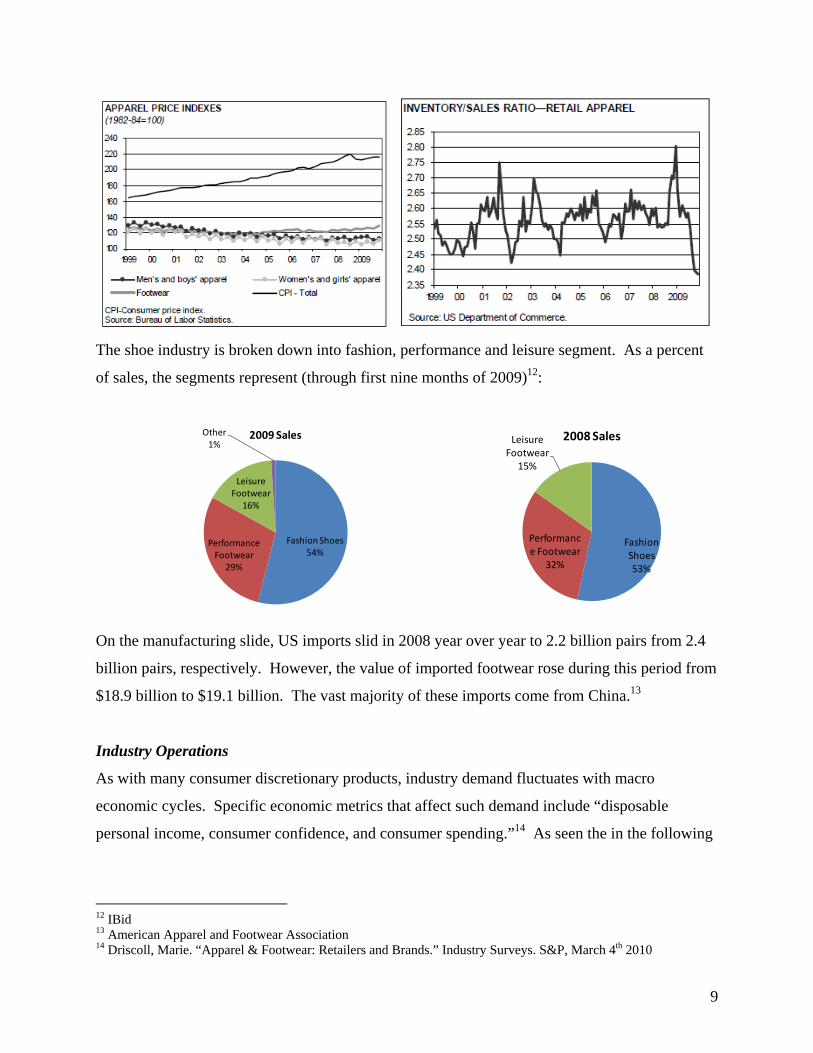

The shoe industry is broken down into fashion, performance and leisure segment. As a percent

of sales, the segments represent (through first nine months of 2009)12:

Fashion Shoes54%

Performance Footwear

29%

Leisure Footwear

16%

Other1%

2009 Sales

Fashion Shoes53%

Performance Footwear

32%

Leisure Footwear

15%

2008 Sales

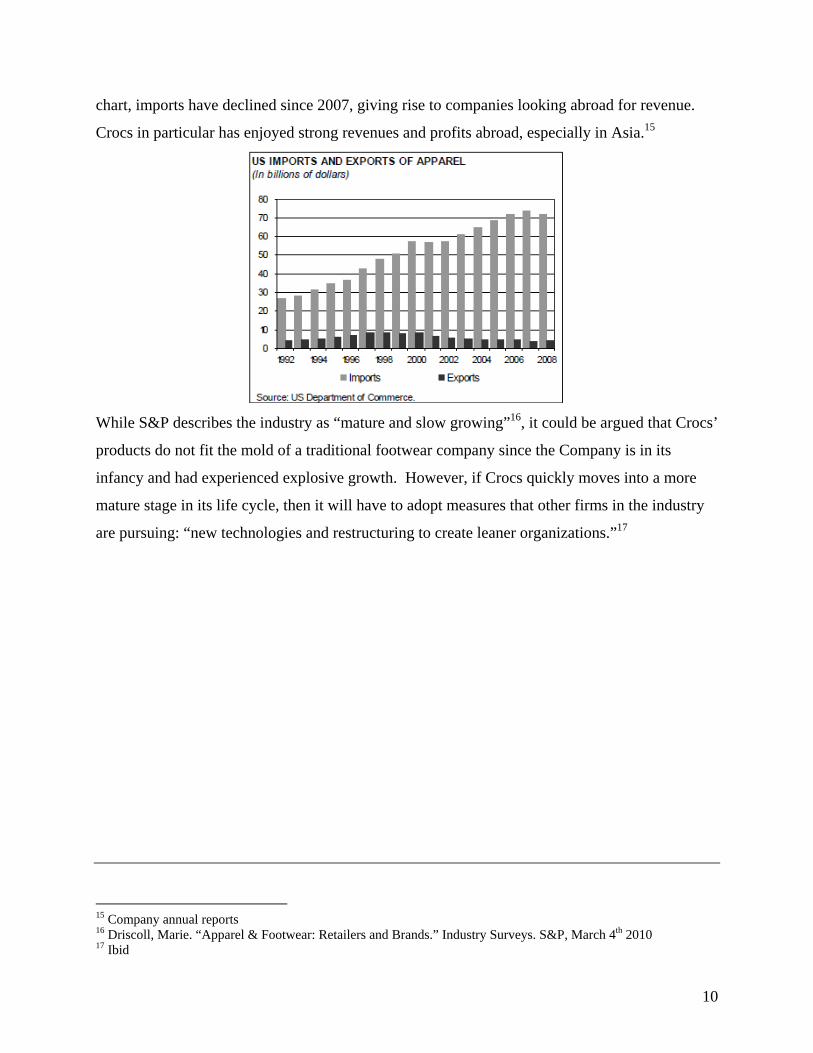

On the manufacturing slide, US imports slid in 2008 year over year to 2.2 billion pairs from 2.4

billion pairs, respectively. However, the value of imported footwear rose during this period from

$18.9 billion to $19.1 billion. The vast majority of these imports come from China.13

Industry Operations

As with many consumer discretionary products, industry demand fluctuates with macro

economic cycles. Specific economic metrics that affect such demand include “disposable

personal income, consumer confidence, and consumer spending.”14 As seen the in the following

12 IBid 13 American Apparel and Footwear Association 14 Driscoll, Marie. “Apparel & Footwear: Retailers and Brands.” Industry Surveys. S&P, March 4th 2010

10

chart, imports have declined since 2007, giving rise to companies looking abroad for revenue.

Crocs in particular has enjoyed strong revenues and profits abroad, especially in Asia.15

While S&P describes the industry as “mature and slow growing”16, it could be argued that Crocs’

products do not fit the mold of a traditional footwear company since the Company is in its

infancy and had experienced explosive growth. However, if Crocs quickly moves into a more

mature stage in its life cycle, then it will have to adopt measures that other firms in the industry

are pursuing: “new technologies and restructuring to create leaner organizations.”17

15 Company annual reports 16 Driscoll, Marie. “Apparel & Footwear: Retailers and Brands.” Industry Surveys. S&P, March 4th 2010 17 Ibid

11

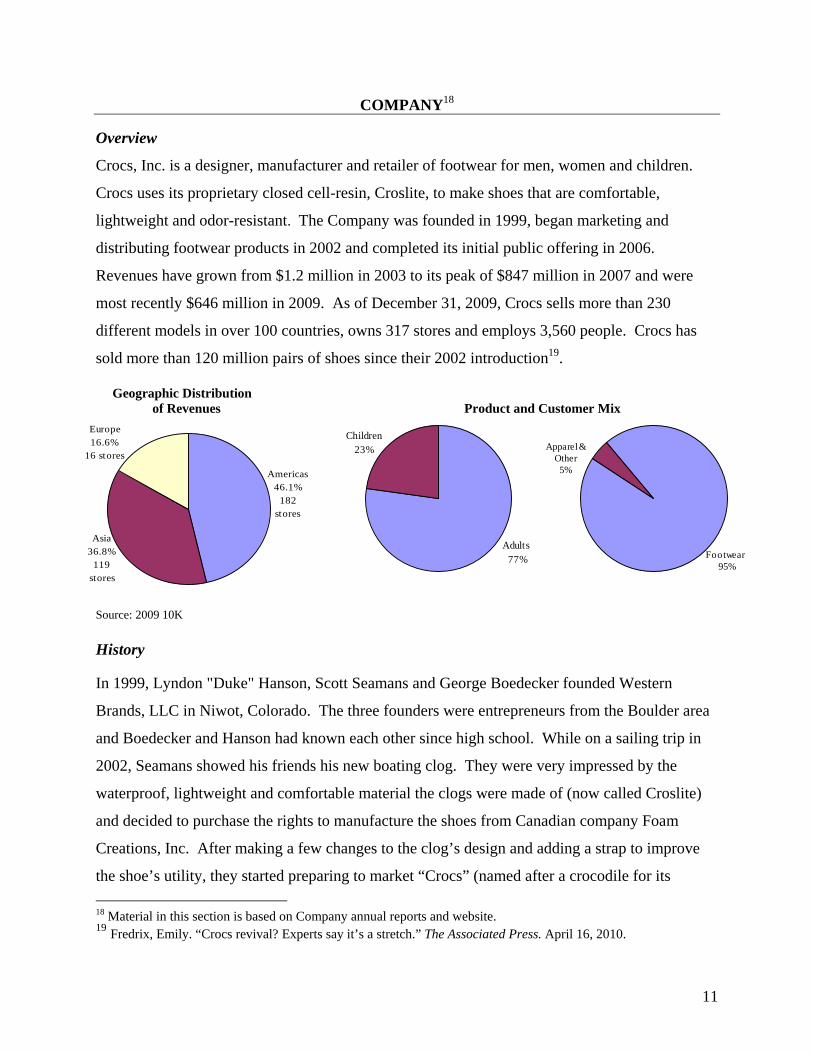

COMPANY18

Overview

Crocs, Inc. is a designer, manufacturer and retailer of footwear for men, women and children.

Crocs uses its proprietary closed cell-resin, Croslite, to make shoes that are comfortable,

lightweight and odor-resistant. The Company was founded in 1999, began marketing and

distributing footwear products in 2002 and completed its initial public offering in 2006.

Revenues have grown from $1.2 million in 2003 to its peak of $847 million in 2007 and were

most recently $646 million in 2009. As of December 31, 2009, Crocs sells more than 230

different models in over 100 countries, owns 317 stores and employs 3,560 people. Crocs has

sold more than 120 million pairs of shoes since their 2002 introduction19.

Geographic Distribution of Revenues Product and Customer Mix

Americas46.1%

182 stores

Asia36.8%

119 stores

Europe16.6%

16 stores

Adults 77%

Children23%

Footwear 95%

Apparel & Other5%

Source: 2009 10K

History In 1999, Lyndon "Duke" Hanson, Scott Seamans and George Boedecker founded Western

Brands, LLC in Niwot, Colorado. The three founders were entrepreneurs from the Boulder area

and Boedecker and Hanson had known each other since high school. While on a sailing trip in

2002, Seamans showed his friends his new boating clog. They were very impressed by the

waterproof, lightweight and comfortable material the clogs were made of (now called Croslite)

and decided to purchase the rights to manufacture the shoes from Canadian company Foam

Creations, Inc. After making a few changes to the clog’s design and adding a strap to improve

the shoe’s utility, they started preparing to market “Crocs” (named after a crocodile for its

18 Material in this section is based on Company annual reports and website. 19 Fredrix, Emily. “Crocs revival? Experts say it’s a stretch.” The Associated Press. April 16, 2010.

12

durability and comfort both on land and in water).20 The founders opened a warehouse in Miami,

Florida and received their first shipment of shoes in August 2002. Boedecker became CEO of

the eight person start-up and they released the “Crocs” clog at an international boat show in Ft.

Lauderdale in October. The clogs were very well received and 1,000 pairs were sold at their

next trade show (at the retail cost of $30 per pair). In fact, sales were quickly forecast to

outnumber supply, due to manufacturing capacity of 8,000 pairs per month.21

Due to their initial success, the founders purchased additional molds from Italy and began

introducing new models to the market. By the middle of 2003, they were selling the original

“Beach” model (now called “Crocs Classic”), the “Highland” model which was marketed for

colder climates because it did not have ventilation holes and the “Nile” model which was a

summer sandal marketed to females. They opened another assembly warehouse in Colorado and

also introduced the website (www.crocs.com). By the end of 2003, Crocs had more than

doubled its production and put a software system into operation to help them manage inventory,

accounting and sales. The founders raised additional capital, increased the number of models

sold and achieved over $1.2 million in revenues in the fiscal year.22

Ron Snyder (who had been consulting for the Company since October 2003) became an

important member of the management team in 2004. Snyder believed that Crocs could continue

its impressive growth if they could provide retailers with a faster turnaround time. By taking

control of their manufacturing and distribution process, Crocs allowed retailers to order as few as

24 pairs at a time and only weeks in advance. This replenishment system also prevented

markdowns of Crocs because stores could base their orders on more accurate demand estimates.

As Synder said, “we decided to base our business model on this - to deliver styles and colors

customers want, and deliver them right away.”23 Crocs was able to achieve this operational

improvement because in June 2004 they purchased Foam Creations Inc. (formerly known as

Finproject NA and now called Crocs Canada). By acquiring their upstream counterpart, Crocs

20 http://www.referenceforbusiness.com/history2/25/Crocs-Inc.html 21 http://www.refreshagency.com/cases/crocs/crocs_media.pdf 22 http://www.refreshagency.com/cases/crocs/crocs_media.pdf 23 Anderson, Diane. “When Crocs attack, an ugly shoe tale.” Business 2.0 Magazine. November 3 2006.

13

gained the manufacturing facilities as well as rights to the proprietary resin-based Croslite material used

to make Crocs.

Crocs’ growth took off and the Company began preparing to go public in 2005. The Company

officially changed its name from Western Brands to Crocs, Inc. in January 2005 and incorporated

in Delaware later that year. Crocs launched its first national advertising campaign and was

recognized as "Brand of the Year" by Footwear News24. Nine models were available in up to 17

different colors and Crocs were carried at more than 5,000 retailers by the end of the year. Due

to the advertising campaign and increased distribution network, Crocs sold over 6 million pairs

of shoes (accounting for approximately $109 million in revenues) and turned its first annual

profit of $16.7 million25. The Company filed its registration statement on August 15, 2005 and

went public on February 8, 2006. While early pricing guidance was at $13 to $15 per share,

Crocs completed its IPO of 9.9 million shares on February 8, 2006 at $21 per share. Crocs raised

$207.9 million in the largest IPO of a footwear manufacturer up to that time.26

In 2006 and 2007, Crocs expanded exponentially - fueled by organic growth as well as numerous

acquisitions. They acquired new brands, such as Jibbitz and Ocean Minded, added a clothing

line made with Croslite and began selling children’s shoes. Due to growing demand, they

increased production capacity through their own manufacturing facilities in Canada, Mexico and

Brazil and also employed contract manufacturers in China, Italy and Romania. Crocs’ product

offering expanded from 25 models in 2006 to over 250 in 2007. The retail expansion continued,

with the first US store openings in Santa Monica, Boston and New York in November 2007. By

the end of 2007, Crocs had 5,300 employees, operated more than 25 company owned retail stores

and sold their products in over 15,000 locations worldwide. They also more than doubled

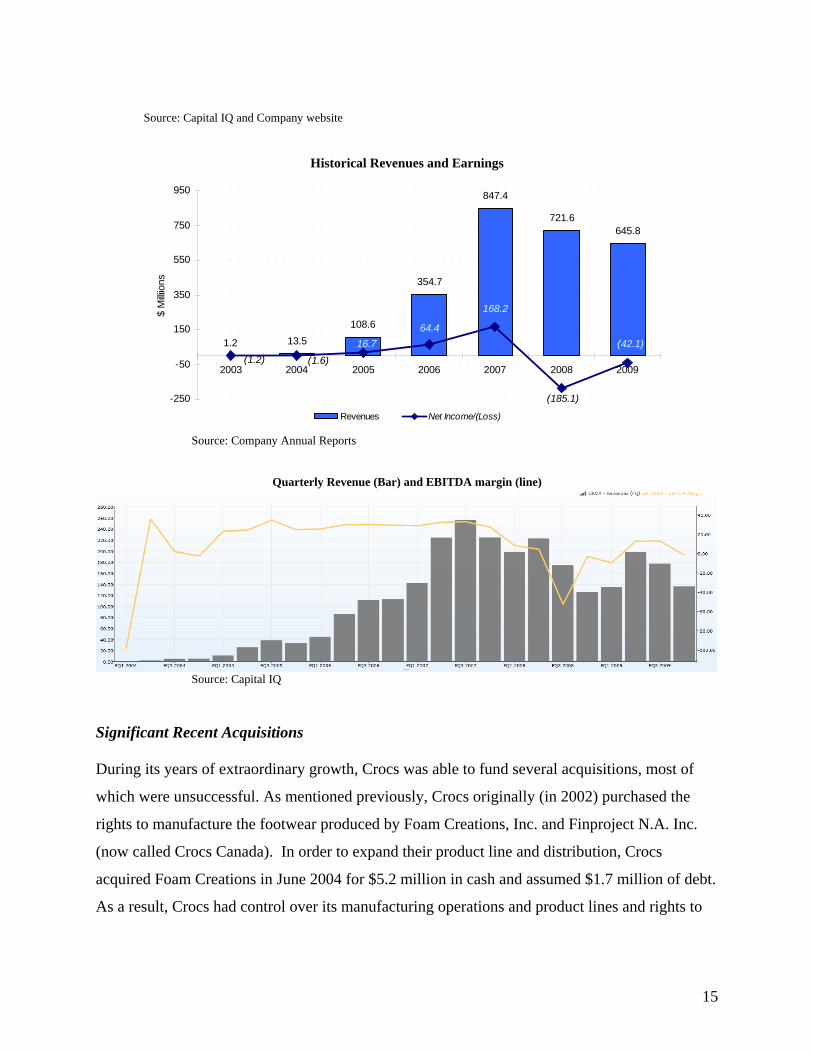

revenues from $354.7 million in 2006 to $847.4 million in 2007.

However, things took a turn for the worse in 2008. Revenue growth slowed in the first quarter

and Crocs experienced a loss of $4.5 million. The decline in growth continued for the rest of the

year and losses mounted. Crocs had grown their manufacturing facilities and inventory in

24 “Brand of the Year.” Company Press Release. Nov. 21, 2005. 25 Alsever, Jennifer. “What a Croc!” Fast Company. June 1, 2006. 26 “Crocs IPO Takes Off.” Denver Business Journal. February 8, 2006.

14

preparation for continued expansion; however the market turned and Crocs was swollen. Crocs

therefore closed their manufacturing facilities in Canada and Brazil and decreased production in

Mexico and China. This resulted in a reduction in force of approximately 1,600 employees. On

the positive side, Crocs attained greater sales from abroad as international sales grew from 32%

of revenues in 2006 to 56% in 2008. Crocs ended the year with a loss of $185.1 million, mostly

due to inventory write-downs and impairments of goodwill and other assets.

In 2009, Crocs continued restructuring and right-sizing the business. They also hired John

Duerden, who previously worked at Reebok to serve as their new CEO in March. Crocs paid

down its outstanding credit facility with UBOC and negotiated a $30 million asset-backed

revolver with PNC in September. Earnings in the second and third quarter beat analyst

expectations. However, Crocs’ demand estimates were too optimistic as growth continued to lag

and the Company reported an annual loss of $42.1 million. In February 2010, Duerden

announced he would be leaving Crocs and John McCarvel was promoted from COO to CEO.

Crocs also recently launched a new advertising campaign called “Feel the Love” to debut new

models for their spring/summer collection and highlight the benefits of Croslite. Lastly, the

Company has provided guidance that they expect revenues to be approximately $160 million in

the first quarter of 2010.

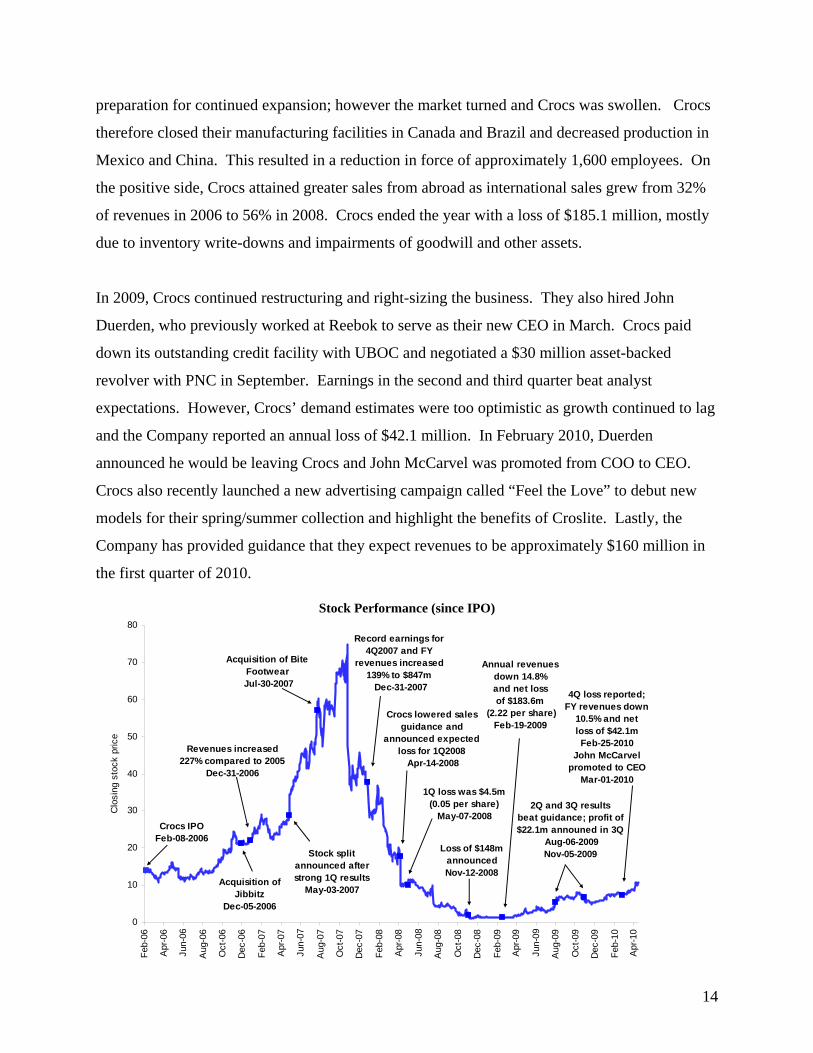

Stock Performance (since IPO)

Crocs IPOFeb-08-2006

4Q loss reported;FY revenues down

10.5% and net loss of $42.1mFeb-25-2010

John McCarvel promoted to CEO

Mar-01-2010

Acquisition of Jibbitz

Dec-05-2006

Revenues increased 227% compared to 2005

Dec-31-2006

Stock split announced after strong 1Q results

May-03-2007

Acquisition of BiteFootwear

Jul-30-2007

Record earnings for 4Q2007 and FY

revenues increased 139% to $847m Dec-31-2007

Crocs lowered sales guidance and

announced expected loss for 1Q2008

Apr-14-2008

1Q loss was $4.5m (0.05 per share)

May-07-2008

Loss of $148mannouncedNov-12-2008

Annual revenues down 14.8% and net loss of $183.6m

(2.22 per share)Feb-19-2009

2Q and 3Q results beat guidance; profit of $22.1m announed in 3Q

Aug-06-2009Nov-05-2009

0

10

20

30

40

50

60

70

80

Feb

-06

Apr

-06

Jun-

06

Aug

-06

Oct

-06

Dec

-06

Feb

-07

Apr

-07

Jun-

07

Aug

-07

Oct

-07

Dec

-07

Feb

-08

Apr

-08

Jun-

08

Aug

-08

Oct

-08

Dec

-08

Feb

-09

Apr

-09

Jun-

09

Aug

-09

Oct

-09

Dec

-09

Feb

-10

Apr

-10

Clo

sing

sto

ck p

rice

15

Source: Capital IQ and Company website

Historical Revenues and Earnings

1.2 13.5

108.6

354.7

847.4

721.6645.8

(1.2) (1.6)

16.7

64.4

168.2

(185.1)

(42.1)

-250

-50

150

350

550

750

950

2003 2004 2005 2006 2007 2008 2009

$ M

illiio

ns

Revenues Net Income/(Loss)

Source: Company Annual Reports

Quarterly Revenue (Bar) and EBITDA margin (line)

Source: Capital IQ

Significant Recent Acquisitions During its years of extraordinary growth, Crocs was able to fund several acquisitions, most of

which were unsuccessful. As mentioned previously, Crocs originally (in 2002) purchased the

rights to manufacture the footwear produced by Foam Creations, Inc. and Finproject N.A. Inc.

(now called Crocs Canada). In order to expand their product line and distribution, Crocs

acquired Foam Creations in June 2004 for $5.2 million in cash and assumed $1.7 million of debt.

As a result, Crocs had control over its manufacturing operations and product lines and rights to

16

the proprietary Croslite material. In October 2008, Crocs divested some of the manufacturing,

inventory and finished products to the original founder of Foam Creations.

Next, Crocs hit a home run with its December 2006 purchase of Jibbitz, a producer of decorative

charms designed to fit into Crocs footwear, for $10 million in cash and an additional $10 million

earn-out based on Jibbitz’s EBIT over the next three years. Jibbitz was the perfect complement

to Crocs, and sales were $67.5 million in 2007 alone, representing nearly 8% of the Company’s

total sales. As of December 31, 2009 Crocs sells 1,200 different Jibbitz charms SKUs, many of

which are based on licensed entertainment characters. Earlier that year, Crocs also acquired Fury

Hockey for $1.5 million and EXO Italia for €6.0 million in October They purchased Fury to

expand into sporting equipment and EXO to have an in-house designer of ethylene vinyl acetate

products. Fury was discontinued in June 2008, resulting in an impairment of $1.3 million for the

brand’s goodwill and trade name.

Crocs made two additional acquisitions of footwear manufacturers in 2007. They purchased

Ocean Minded for their leather and EVA-based sandals in January and they purchased Bite for

their performance shoes and sandals in July. Ocean Minded was acquired for $1.75 million in

cash and milestone payments worth an additional $3.75 million over three years. Bite was

purchased for $1.75 million in cash (plus the assumption of their debt of $1.3 million) and

milestone payments worth an additional $1.75 million over three years. Crocs discontinued Bite

in 2009 and incurred a restructuring charge of $1.1 million to terminate their obligations related

to the Bite agreement.

In April 2008, Crocs acquired Tidal Trade for $4.6 million and Tagger International for $2.0

million. While the purchase of Tidal Trade, the distributor of Crocs in South Africa, included

$1.4 million in customer relationships, it also resulted in reduced revenues of $2.1 million from

previously sold inventory. Crocs discontinued Tagger International, a manufacturer of

messenger bags, in 2009 and recognized an impairment charge for its trademark (valued at $1.9

million at acquisition). Given Crocs’ financial situation in 2008, it is surprising that these

acquisitions were executed. That being said, Crocs has not acquired any additional brands since

April 2008 and has focused on liquidating non-performing assets during the last two years.

17

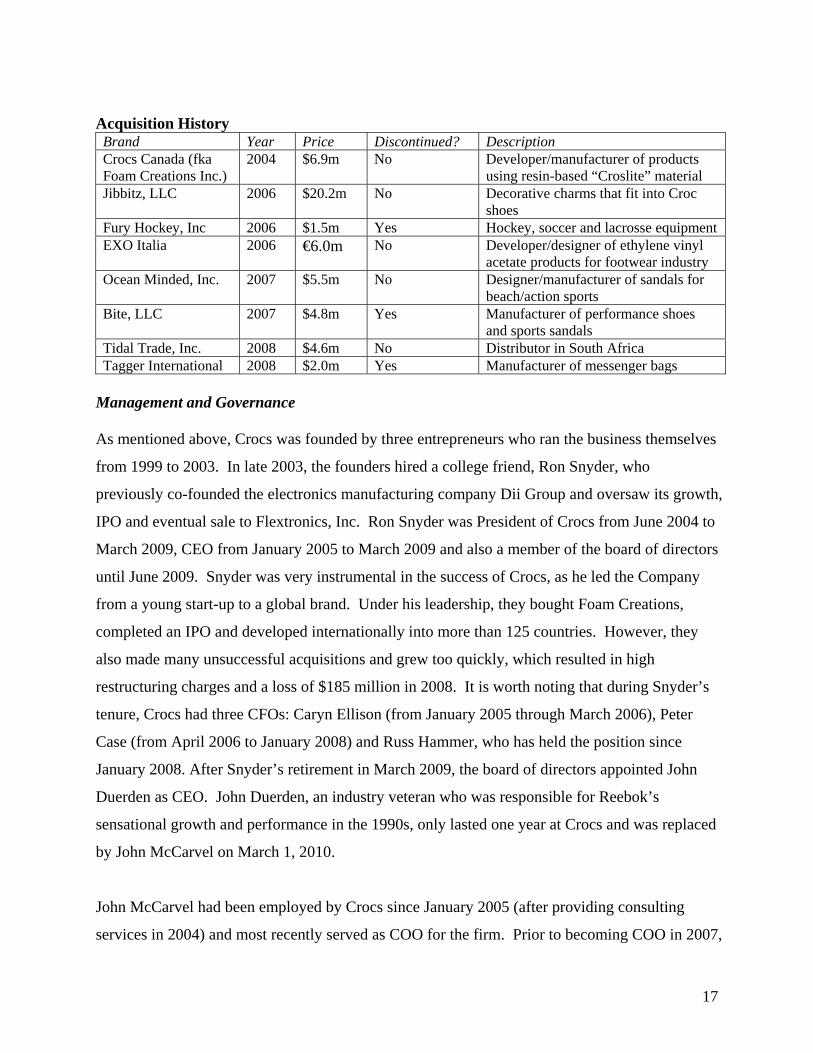

Acquisition History Brand Year Price Discontinued? Description Crocs Canada (fka Foam Creations Inc.)

2004 $6.9m No Developer/manufacturer of products using resin-based “Croslite” material

Jibbitz, LLC 2006 $20.2m No Decorative charms that fit into Croc shoes

Fury Hockey, Inc 2006 $1.5m Yes Hockey, soccer and lacrosse equipment EXO Italia 2006 €6.0m No Developer/designer of ethylene vinyl

acetate products for footwear industry Ocean Minded, Inc. 2007 $5.5m No Designer/manufacturer of sandals for

beach/action sports Bite, LLC 2007 $4.8m Yes Manufacturer of performance shoes

and sports sandals Tidal Trade, Inc. 2008 $4.6m No Distributor in South Africa Tagger International 2008 $2.0m Yes Manufacturer of messenger bags

Management and Governance As mentioned above, Crocs was founded by three entrepreneurs who ran the business themselves

from 1999 to 2003. In late 2003, the founders hired a college friend, Ron Snyder, who

previously co-founded the electronics manufacturing company Dii Group and oversaw its growth,

IPO and eventual sale to Flextronics, Inc. Ron Snyder was President of Crocs from June 2004 to

March 2009, CEO from January 2005 to March 2009 and also a member of the board of directors

until June 2009. Snyder was very instrumental in the success of Crocs, as he led the Company

from a young start-up to a global brand. Under his leadership, they bought Foam Creations,

completed an IPO and developed internationally into more than 125 countries. However, they

also made many unsuccessful acquisitions and grew too quickly, which resulted in high

restructuring charges and a loss of $185 million in 2008. It is worth noting that during Snyder’s

tenure, Crocs had three CFOs: Caryn Ellison (from January 2005 through March 2006), Peter

Case (from April 2006 to January 2008) and Russ Hammer, who has held the position since

January 2008. After Snyder’s retirement in March 2009, the board of directors appointed John

Duerden as CEO. John Duerden, an industry veteran who was responsible for Reebok’s

sensational growth and performance in the 1990s, only lasted one year at Crocs and was replaced

by John McCarvel on March 1, 2010.

John McCarvel had been employed by Crocs since January 2005 (after providing consulting

services in 2004) and most recently served as COO for the firm. Prior to becoming COO in 2007,

18

McCarvel was senior vice president for global operations (from October 2005 to February 2007)

and vice president for Asia. McCarvel successfully moved up the ranks at Crocs, proving

himself on projects such as the expansion of Crocs’ direct channel business, consolidation of

their global warehouse capacity and investments in customer systems. McCarvel is taking

charge of Crocs after a very difficult period of substantial losses and overall economic distress;

however, he already knows the Company inside and out and is hopeful that they will be able to

turn the business around. As he said, “We’ve spent the last 18 months stabilizing the Company

while reinvigorating our product line and brand, and realigning our cost structure. I look forward

to guiding the Company back to profitable growth, with the help of our talented management

team and employees around the world and the support of our board.”27

Of the three founders, Hanson and Seamans are still involved in the firm’s operations. Lyndon

Hanson is currently VP of Customer Relations and Scott Seamans serves as Vice President of

Product Development. George Boedecker was CEO of Crocs from July 2002 through December

2004 and subsequently resigned from Board in May 2006 amid personal issues.

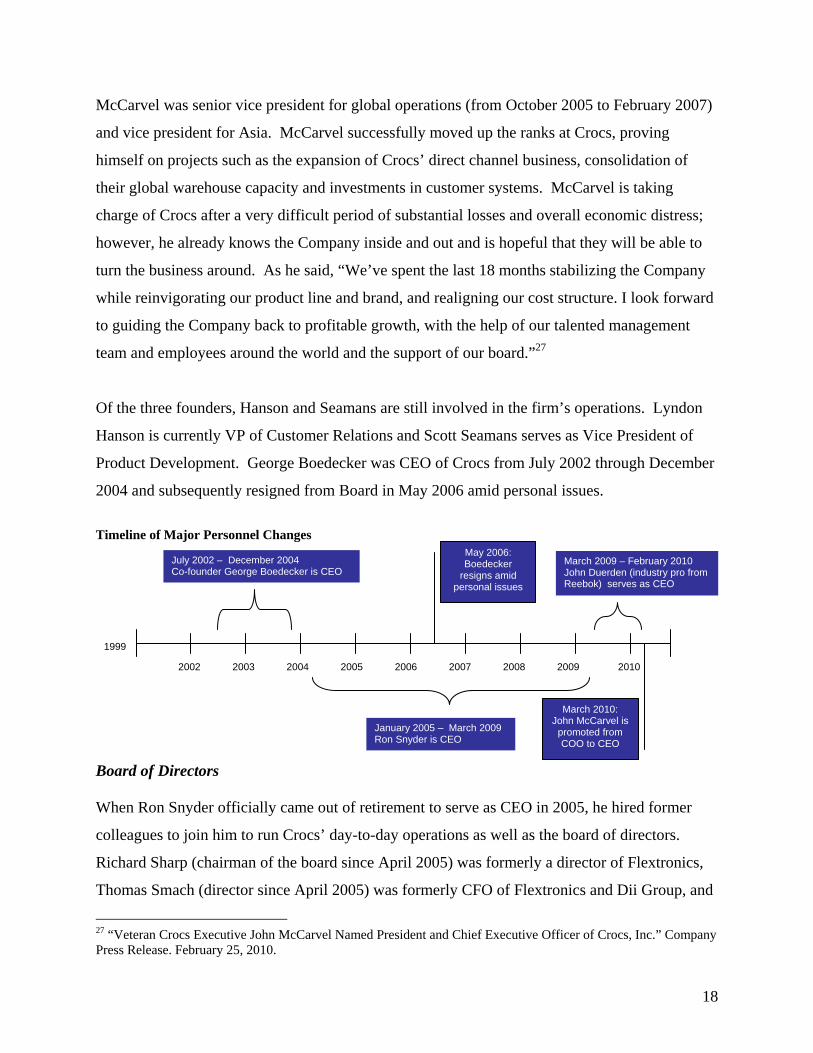

Timeline of Major Personnel Changes

Board of Directors When Ron Snyder officially came out of retirement to serve as CEO in 2005, he hired former

colleagues to join him to run Crocs’ day-to-day operations as well as the board of directors.

Richard Sharp (chairman of the board since April 2005) was formerly a director of Flextronics,

Thomas Smach (director since April 2005) was formerly CFO of Flextronics and Dii Group, and

27 “Veteran Crocs Executive John McCarvel Named President and Chief Executive Officer of Crocs, Inc.” Company Press Release. February 25, 2010.

2002

1999

2003 2004 2005 2006 2007 2008 2009 2010

May 2006: Boedecker

resigns amid personal issues

July 2002 – December 2004 Co-founder George Boedecker is CEO

January 2005 – March 2009 Ron Snyder is CEO

March 2009 – February 2010 John Duerden (industry pro from Reebok) serves as CEO

March 2010: John McCarvel is

promoted from COO to CEO

19

John McCarvel (Crocs’ current CEO) was formerly Vice President of the design, test and

semiconductor division at Flextronics. Over the past five years, the board has experienced some

turnover. In addition to the CEO, two new directors Peter Jacobi and Stephen Cannon (Richard

Sharp’s former General Counsel at Circuit City) have been appointed to the board in the past two

years.

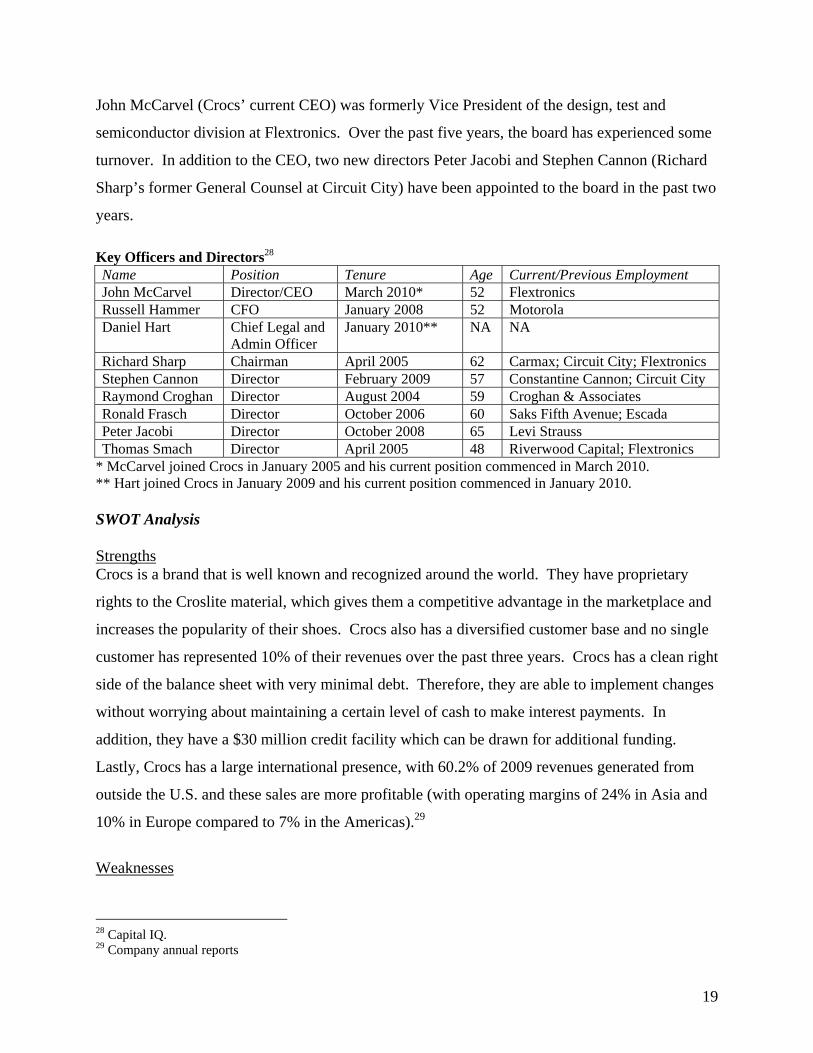

Key Officers and Directors28 Name Position Tenure Age Current/Previous Employment John McCarvel Director/CEO March 2010* 52 Flextronics Russell Hammer CFO January 2008 52 Motorola Daniel Hart Chief Legal and

Admin Officer January 2010** NA NA

Richard Sharp Chairman April 2005 62 Carmax; Circuit City; Flextronics Stephen Cannon Director February 2009 57 Constantine Cannon; Circuit City Raymond Croghan Director August 2004 59 Croghan & Associates Ronald Frasch Director October 2006 60 Saks Fifth Avenue; Escada Peter Jacobi Director October 2008 65 Levi Strauss Thomas Smach Director April 2005 48 Riverwood Capital; Flextronics

* McCarvel joined Crocs in January 2005 and his current position commenced in March 2010. ** Hart joined Crocs in January 2009 and his current position commenced in January 2010. SWOT Analysis Strengths Crocs is a brand that is well known and recognized around the world. They have proprietary

rights to the Croslite material, which gives them a competitive advantage in the marketplace and

increases the popularity of their shoes. Crocs also has a diversified customer base and no single

customer has represented 10% of their revenues over the past three years. Crocs has a clean right

side of the balance sheet with very minimal debt. Therefore, they are able to implement changes

without worrying about maintaining a certain level of cash to make interest payments. In

addition, they have a $30 million credit facility which can be drawn for additional funding.

Lastly, Crocs has a large international presence, with 60.2% of 2009 revenues generated from

outside the U.S. and these sales are more profitable (with operating margins of 24% in Asia and

10% in Europe compared to 7% in the Americas).29

Weaknesses

28 Capital IQ. 29 Company annual reports

20

Crocs does not have a diversified product offering beyond footwear, which causes revenues to be

seasonal (since most of their footwear is worn in summer) and also very cyclical (dependent on

consumer spending and performance of the retail sector). Demand for “Crocs Classic” shoes has

been declining over time (from 30% of total sales in 2007 to 16% in 2009) as they transition to a

mature product and therefore, revenues are contingent upon the success of new models and fads.

Crocs also relies too heavily on key suppliers and manufacturers. In 2009, Crocs only produced

27% of footwear products at company-owned facilities in Mexico and Italy. Another 36% of

2009’s footwear products were produced by their largest third-party supplier in China and Crocs

does not have written supply agreements with their primary third-party manufacturers in China.

Crocs has poor IT systems and depends on manual processes which are not efficient or scalable

as the Company grows. Another weakness is Crocs’ capital markets valuation, as their stock is

currently trading at $10.96, down from a high of $74.75 in October 2007. Lastly, Crocs has also

experienced management turnover in the past year; their CEO John Duerden retired in February

2010, they promoted John McCarvel from COO to CEO (leaving the COO position unfilled) and

their general counsel resigned in December 2009.30

Opportunities Crocs has the ability to expand through growth in direct to consumer sales and internet sales.

Given Crocs’ success internationally, they can continue expanding abroad by reaching untapped

markets. In addition, it’s possible that the Crocs “fad” is in a different part of the fashion trend

cycle abroad and Crocs can even take advantage of further growth in countries where it already

has a presence. Lastly, there is an industry movement towards more comfortable and casual

shoes, so Crocs has the opportunity to attract new consumers by highlighting the benefits of

Croslite.

Threats Given that Crocs does not have patent protection on its proprietary Croslite material, other

companies have been replicating the material or creating close substitutes, which eliminates

Crocs’ competitive advantage. In addition, there are limited barriers to entry and many knock-

offs have been created. While Crocs has filed suits against numerous copycats, this process is

costly and takes time (and important executives) away from their core business. Due to the lack

30 IBid

21

of advanced IT systems, Crocs is more susceptible to human error or fraud. Also, Crocs does not

hedge its exposure to foreign exchange and could therefore face significant losses if the US

dollar strengthens. Crocs likely has over-capacity from its rapid growth pre-2008 which may

add additional difficulty as they come out of the recent economic crisis. Another threat is their

unknown ability to tap the capital markets, given that Crocs may need additional capital if there

are losses in 2010. The revolver with PNC pledges their assets as collateral, therefore the

Company would need to find an unsecured lender. Lastly, there is anti-Crocs sentiment in the

market, as evidenced by the website “I Hate Crocs.com”31 which could reduce demand for its

products.32

31 http://ihatecrocs.com/ 32 IBid

22

HISTORICAL FINANCIAL OVERVIEW Crocs experienced rapid revenue growth and had difficulty meeting the demand for its footwear

products from the Company’s inception to the year ended December 31, 2007. In fact, many

people ‘felt the love’ for the brand when the shoes were introduced in 2002. Revenue reached

$354.7 million in 2006, the year the Company went public. A year later, that figure had more

than doubled to $847.4 million. During this period, the Company significantly increased

production capacity, warehouse space and inventory in an effort to meet demand. This trend

rapidly ended in 2008. But by 2009, sales had fallen nearly a quarter to $645.8 million.

2005A 2006A 2007A 2008A 2009A

Sales growth rate 703.1% 226.7% 138.9% (14.8%) (10.5%)

COGS / Sales 44.0% 43.5% 41.3% 67.5% 52.3%

Gross margin 56.0% 56.5% 58.7% 32.4% 46.6%

SG&A / Sales 31.2% 29.7% 31.7% 47.3% 48.3%

FX transaction losses (gains), net / Sales 0.0% 0.0% ‐1.2% 3.5% ‐0.1%

Net profit margin 15.6% 18.2% 19.9% ‐25.6% ‐6.5%

Capex / PP&E, net (Prev Yr) 309.5% 161.4% 164.7% 63.0% 20.9%

Fiscal Year Ended

Key Financial Ratios, 2005 ‐ 2009

Management believes that both the large decline in revenues in the Americas and Europe, and

the moderation of revenue growth in Asia, are largely attributable to the following factors:

a. The global economic crisis, which impacted the United States, Europe and Asia, causing

a reduction in consumer spending and decreased foot traffic at shopping malls. This

resulted in the Company’s inability to execute its long-term growth strategy or maintain

current revenue levels.

b. A less successful than anticipated attempt to face the following challenges:

a. Merchandising expanded product lines in existing wholesale channels while

responding to lessening demand for mature products.

b. Effectively responding to competitors entering the market with imitation products

that are sold at substantially lower prices.

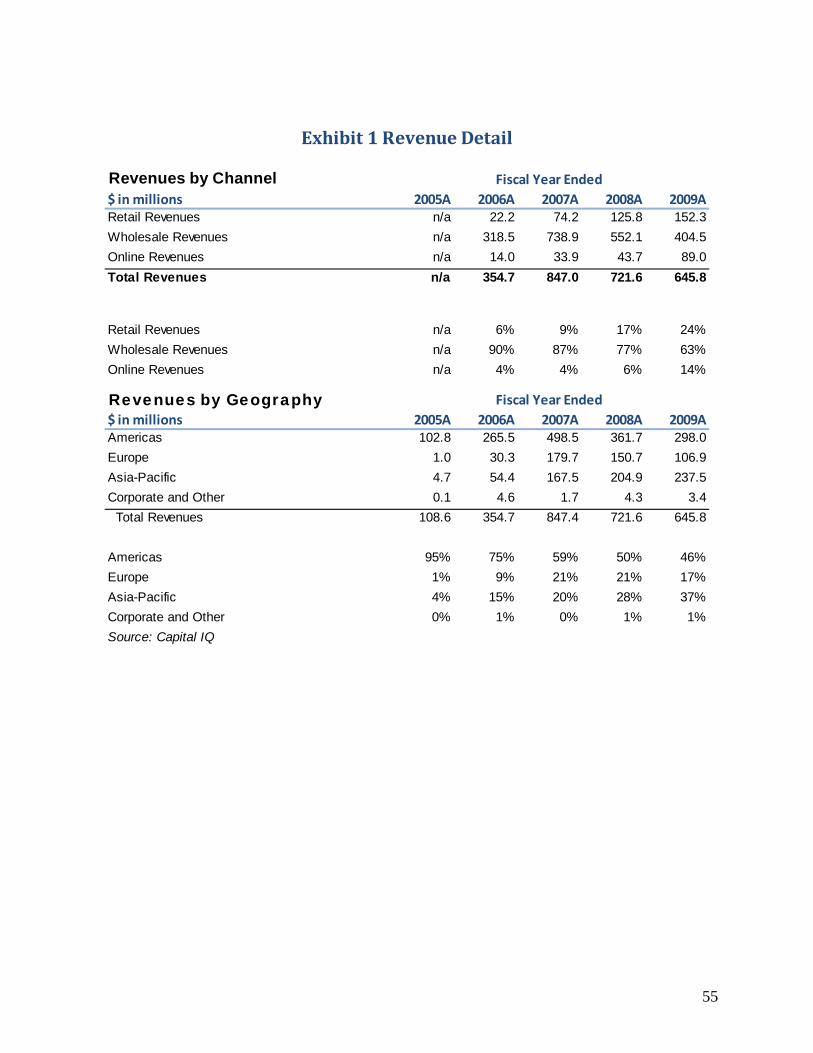

Revenue – Trends and Drivers

23

Over the last five years, Crocs’ revenues, influenced by distribution channel, product mix and

geography have varied significantly and resulted in changes to profitability. As shown in

Exhibits 1 and 2, the following trends are evident:

Increasing revenues in the Asia-Pacific region, from 4% to 37% of total revenues in

FY08 and FY09, respectively, offset by declining revenues in the Americas and Europe

during the same period. The Company expects that growth in Asian markets will continue

to fuel Company revenue growth going forward. Note that revenues earned in Asia (and

Europe) generate significantly larger operating profit margins than those earned in the

Americas. As revenue growth in Asia continues to outpace that of the Americas/Europe,

one would expect the Company’s operating profit margin to improve.

2007 2008 2009Americas 33.3% -12.0% 7.1%Europe 42.9% 0.7% 10.3%Asia-Pacif ic 44.9% 8.1% 24.4%Corporate and Other -4852.9% -3808.6% -4204.1%

Total 28% ‐26% ‐8%

2007 2008 2009Americas 259% -15% 8%Europe 623% 2% 16%Asia-Pacif ic 965% 13% 38%Corporate and Other nm nm nm

Total 270% ‐41% ‐12%Source: Capital IQ, Crocs 10-K, f inancial analysisnm= not meaningful

Operating Profit Margin before Tax by GeographyFiscal year ended

Operating Return on Assets by Geography

Growing retail and online revenues, offset by recent declines in wholesale revenue. It is

part of the Company’s long-term strategy to continue increasing retail and online sales

growth, as these distribution channels earn higher sales prices which is accretive to gross

profit margins and also allow the Company to maintain control over brand

recognition/awareness. Decreasing wholesale revenues are driven by lower unit

sales/Jibbitz sales due to the economic downtown and during FY08, increased sales

return allowances (discussed below). The continued global economic downturn in FY09,

lessened consumer demand and leaner inventory levels further contributed to declining

wholesale revenues. Also, the Company took measures to reduce the number of

24

wholesalers selling its product in order to be in a better position to brand the product in

the marketplace.

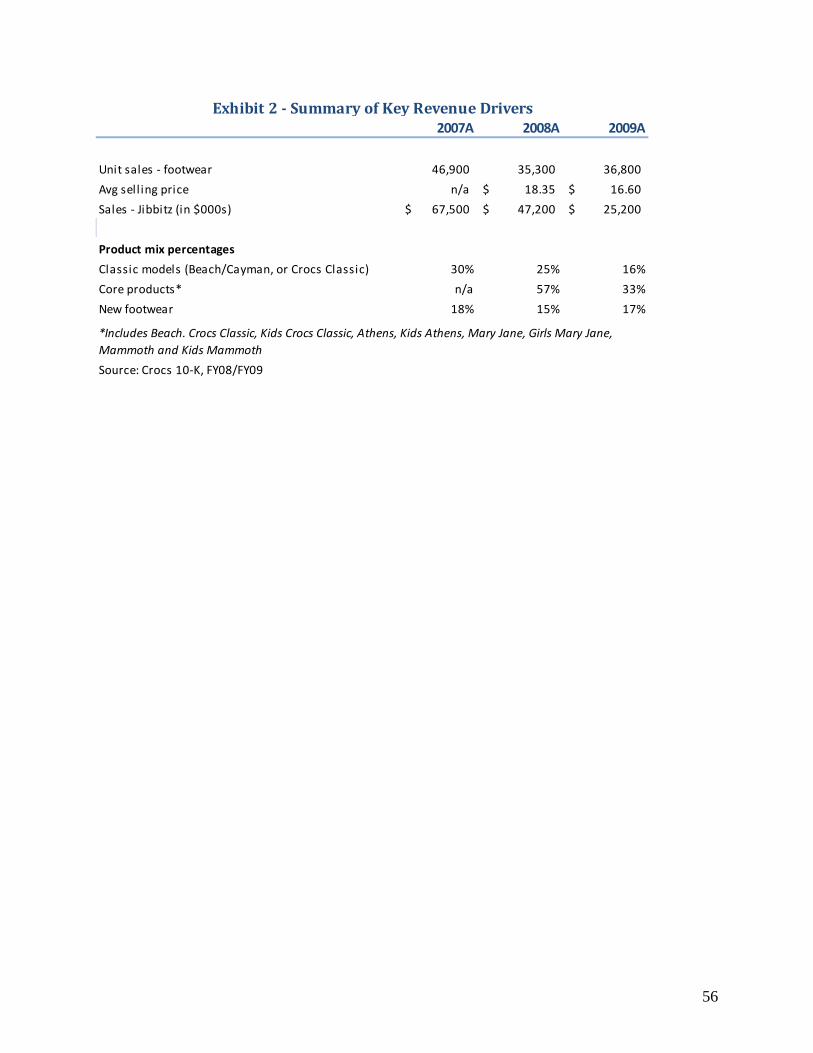

Change in sales mix, from primarily the classic/core Crocs products to newly introduced

shoe models. Per management, a wider range of products requires additional materials

(such as canvas, cloth, lining and suede) and additional processes (such as stitching) to

manufacture. This results in a higher cost of sales and decreased gross margins.

Expenses33

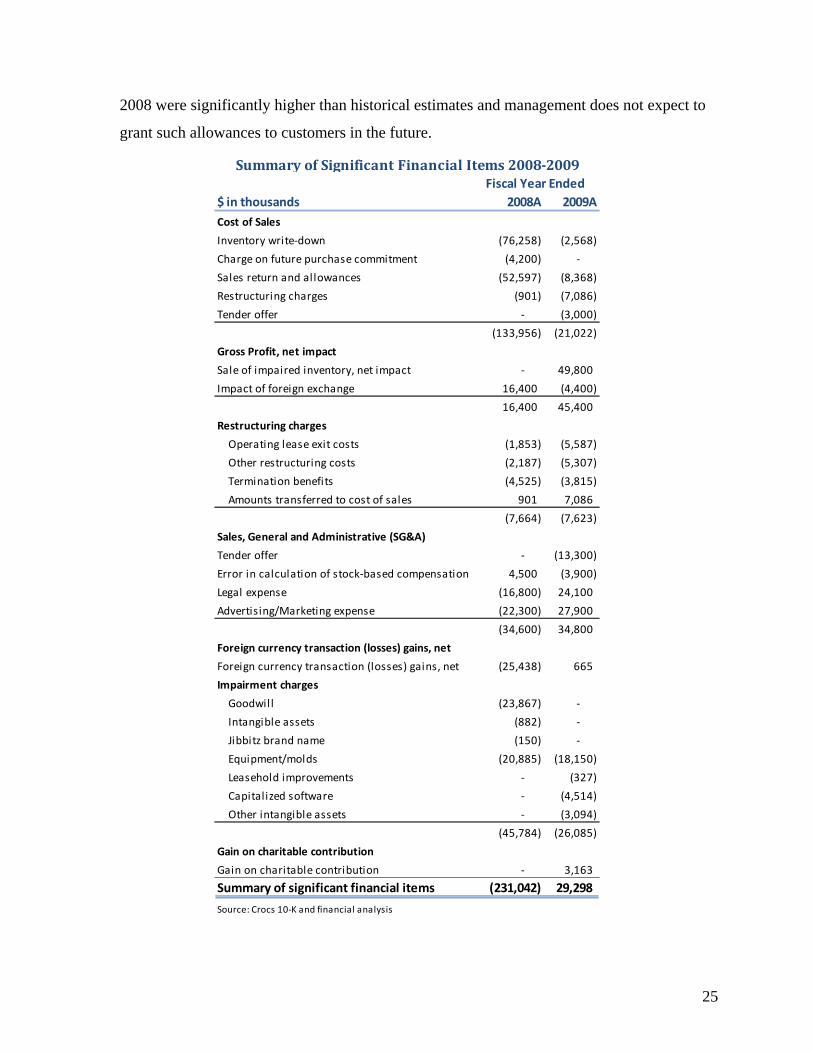

As shown within the Company’s income statement contained within Exhibit 3, the Company

experienced significant changes to both cost of sales and operating expenses during FY08 and

FY09. Given the sharp decline in sales, the Company commenced restructuring efforts and other

downsizing activities during FY08, which resulted in various material non-recurring items being

recorded in the Crocs’ financial statements.

Cost of Sales

Inventory write-down/charge on future purchase commitment: During FY08, Crocs inventory

included certain styles and colors with substantially diminished demand. Based on decreased

demand for these products, the Company discontinued them and implemented a plan for the

disposal of the discontinued product inventories. This plan included structured sales to

established discount retailers, sales through Company-operated outlet stores, warehouse sales

and other disposition activities as well as charitable product donations. In connection with

these efforts, the Company recorded approximately $76.3 m of inventory write-down charges

and an additional $4.2 m in charges related to losses on future purchase commitments for

inventory with a market value lower than cost.

Sales returns and allowances: In light of then-prevailing economic conditions, the Company

granted certain return requests and allowances to a number of customers it believed were

strategically important to the Company’s ongoing business; this resulted in an increase in

sales returns and allowances. The expense recorded for the reserve for sales returns and

allowances increased from $7,168,000 in FY07 to $52,597,000 in FY08 and went back to

$8,368,000 in FY09. Per the MD&A within the Company’s 10-K filing, amounts recorded in

33 Company annual reports

25

2008 were significantly higher than historical estimates and management does not expect to

grant such allowances to customers in the future.

$ in thousands 2008A 2009A

Cost of Sales

Inventory write‐down (76,258) (2,568)

Charge on future purchase commitment (4,200) ‐

Sales return and allowances (52,597) (8,368)

Restructuring charges (901) (7,086)

Tender offer ‐ (3,000)

(133,956) (21,022)

Gross Profit, net impact

Sale of impaired inventory, net impact ‐ 49,800

Impact of foreign exchange 16,400 (4,400)

16,400 45,400

Restructuring charges

Operating lease exit costs (1,853) (5,587)

Other restructuring costs (2,187) (5,307)

Termination benefits (4,525) (3,815)

Amounts transferred to cost of sales 901 7,086

(7,664) (7,623)

Sales, General and Administrative (SG&A)

Tender offer ‐ (13,300)

Error in calculation of stock‐based compensation 4,500 (3,900)

Legal expense (16,800) 24,100

Advertising/Marketing expense (22,300) 27,900

(34,600) 34,800

Foreign currency transaction (losses) gains, net

Foreign currency transaction (losses) gains, net (25,438) 665

Impairment charges

Goodwill (23,867) ‐

Intangible assets (882) ‐

Jibbitz brand name (150) ‐

Equipment/molds (20,885) (18,150)

Leasehold improvements ‐ (327)

Capitalized software ‐ (4,514)

Other intangible assets ‐ (3,094)

(45,784) (26,085)

Gain on charitable contribution

Gain on charitable contribution ‐ 3,163

Summary of significant financial items (231,042) 29,298

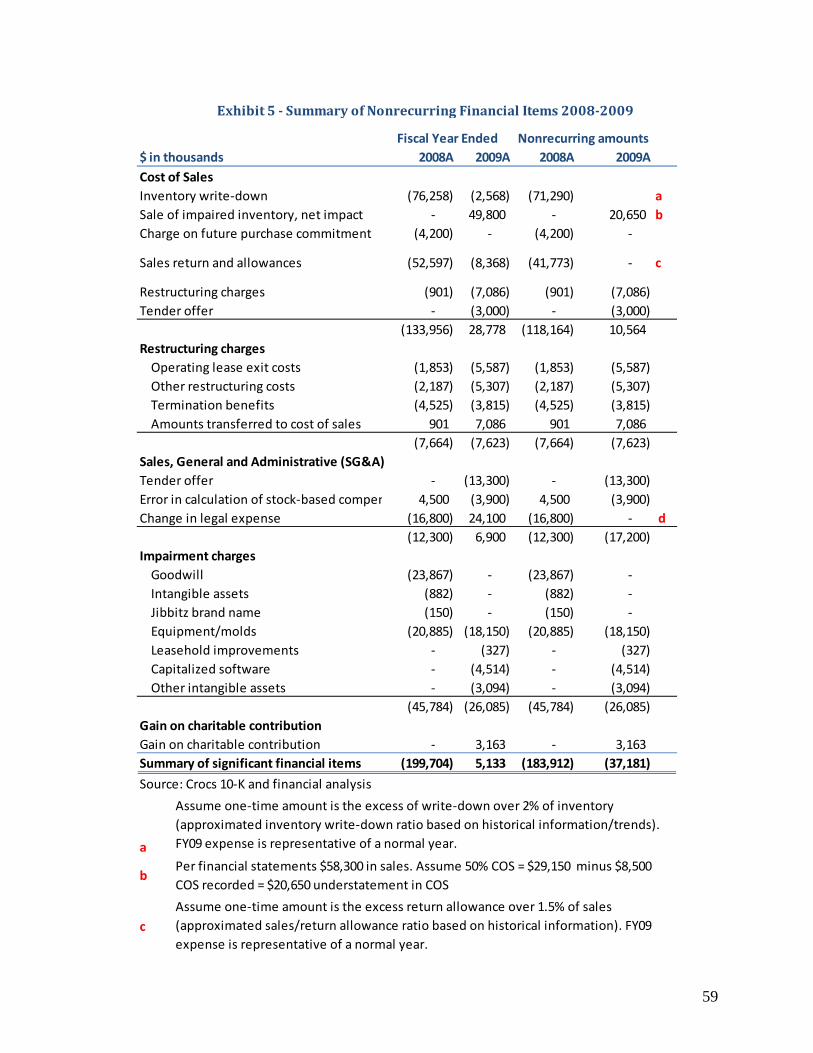

Source: Crocs 10‐K and financial analysis

Fiscal Year Ended

Summary of Significant Financial Items 2008‐2009

26

Gross Profit, net impact

Sale of impaired inventory: Related to the inventory write-down described above, the

Company was able to sell $58.3m of impaired product at substantially higher prices than

what management had previously estimated. The gross profit related to these units was

accretive to gross margin in the amount of $49.8m.

Impact of foreign exchange: According to the Company’s MD&A, changes in foreign

currency exchange rates year-on-year impact gross margin. Management expects that sales at

subsidiary companies with functional currencies other than the US dollar will continue to

generate a substantial portion of overall gross profit. Changes in foreign currency exchange

rates can impact gross margins and/or comparability of gross margins from period to period.

Restructuring Charges

Given declines in revenue, the Company evaluated its production capacity and operations

structure and recorded the restructuring costs outlined below. Of total amounts recorded, the

Company recorded $7.6 million recorded in restructuring charges and $7.1 million in cost of

sales during FY09 and $7.6 million in restructuring charges and $0.9 million in cost of sales

during FY08.

Operating lease exit costs: Includes costs related to the restructuring/discontinuation of

operations in Canada and Brazil during FY08 and the consolidation of warehouse and

distribution facilities in FY09.

Other restructuring costs: Other restructuring costs for FY08 includes the cancellation of

purchase obligations and freight and duty charges related to transferring inventory and

equipment to its United States and Mexico facilities. FY09 amounts include costs related to

the termination of a manufacturing agreement with third party in Bosnia and the termination

of the Company’s sponsorship agreement with the Association of Volleyball Professionals, a

$1.1 million charge to release the Company from obligations under an earn-out agreement

with Bite, LLC, and $0.5 million in charges related to the termination of consulting

agreements with former key employees.

Termination benefits: Represents employee termination costs related to headcount reductions.

27

SG&A costs

Tender offer: During FY09, the Company offered to purchase stock options with exercise

prices equal to or greater than $10.50 per share in order to restore the incentive value of its

long-term performance award programs and in response to the fact that the exercise prices of

a substantial number of outstanding options were under water. Of the $16.3 million charge,

$13.3 million was recorded to SG&A and $3 million was recorded to cost of sales.

Error in calculation of stock-based compensation: During FY09, management identified an

error in the calculation of stock-based compensation for prior periods. The error resulted in a

$4.5 million understatement of stock-based compensation in FY08. Amounts were corrected

during FY09 through both the tender offer expense described above and a direct adjustment

to the financial statements.

Legal expense: During FY08, the Company experienced an increase in legal expense of

$16.8 million due to ongoing litigation and intellectual property enforcement. During FY09,

legal expense decreased $24.1 million when compared to FY08.

Advertising/Marketing expense: The Company’s advertising/marketing expenses fluctuated

significantly during FY08/FY09. Expense increases in FY08 include $5.4m related to

corporate sponsorships and $12m related to advertising expense. During FY09, expenses

decreased $27.9m, due to an $11.1m expense decrease related to corporate sponsorship and a

$16.8m decrease in advertising as the Company exited corporate sponsorships.

Foreign currency transaction gains and losses

Expenses related to recording transactions denominated and settled in a currency other than the

functional currency (USD) have resulted in significant swings in the Company’s income

statement, including a gain of $10.1 million, a loss of $25.4 million and a gain of $665, 000 in

F07, FY08 and FY09, respectively. Per the Company’s 10-K, management intends to engage in

foreign exchange hedging contracts to reduce economic exposure in the future.

Impairment Charges

In conjunction with the restructuring activities described above, the Company recorded various

charges during FY08 and FY09 related to equipment and molds that represented excess capacity,

28

goodwill, intangibles assets including trade names and patents, and other assets/equipment used

in manufacturing, distribution and sales that were considered impaired.

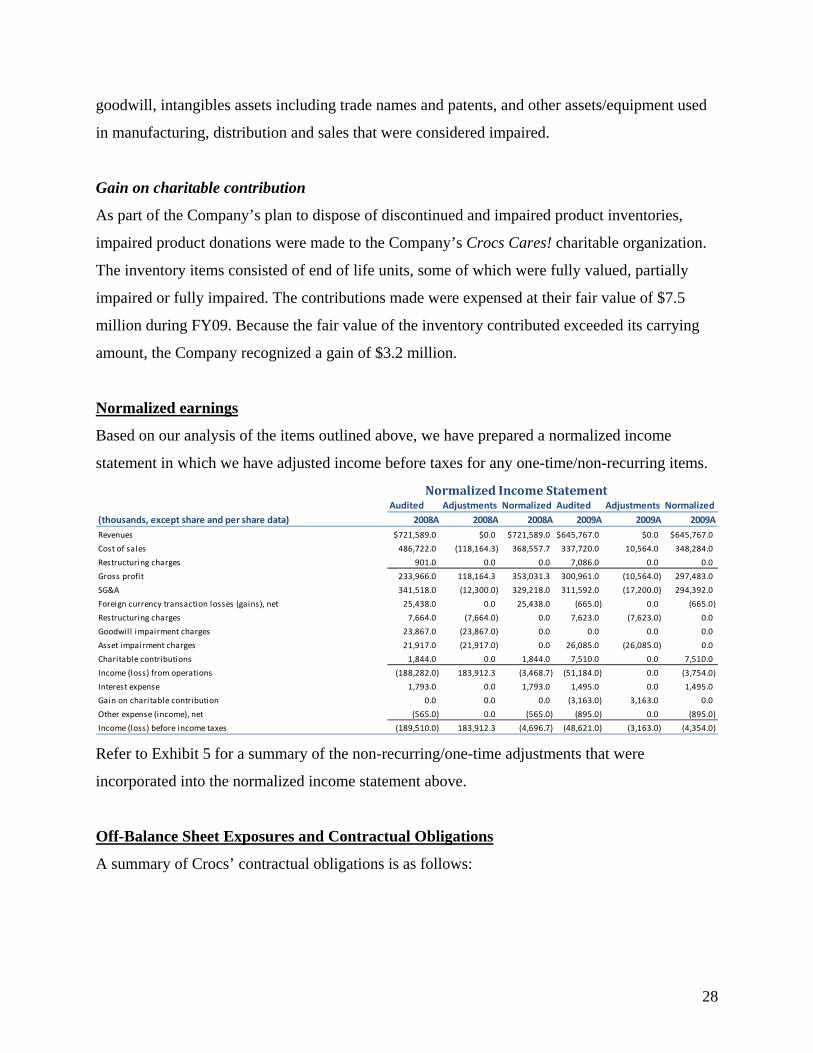

Gain on charitable contribution

As part of the Company’s plan to dispose of discontinued and impaired product inventories,

impaired product donations were made to the Company’s Crocs Cares! charitable organization.

The inventory items consisted of end of life units, some of which were fully valued, partially

impaired or fully impaired. The contributions made were expensed at their fair value of $7.5

million during FY09. Because the fair value of the inventory contributed exceeded its carrying

amount, the Company recognized a gain of $3.2 million.

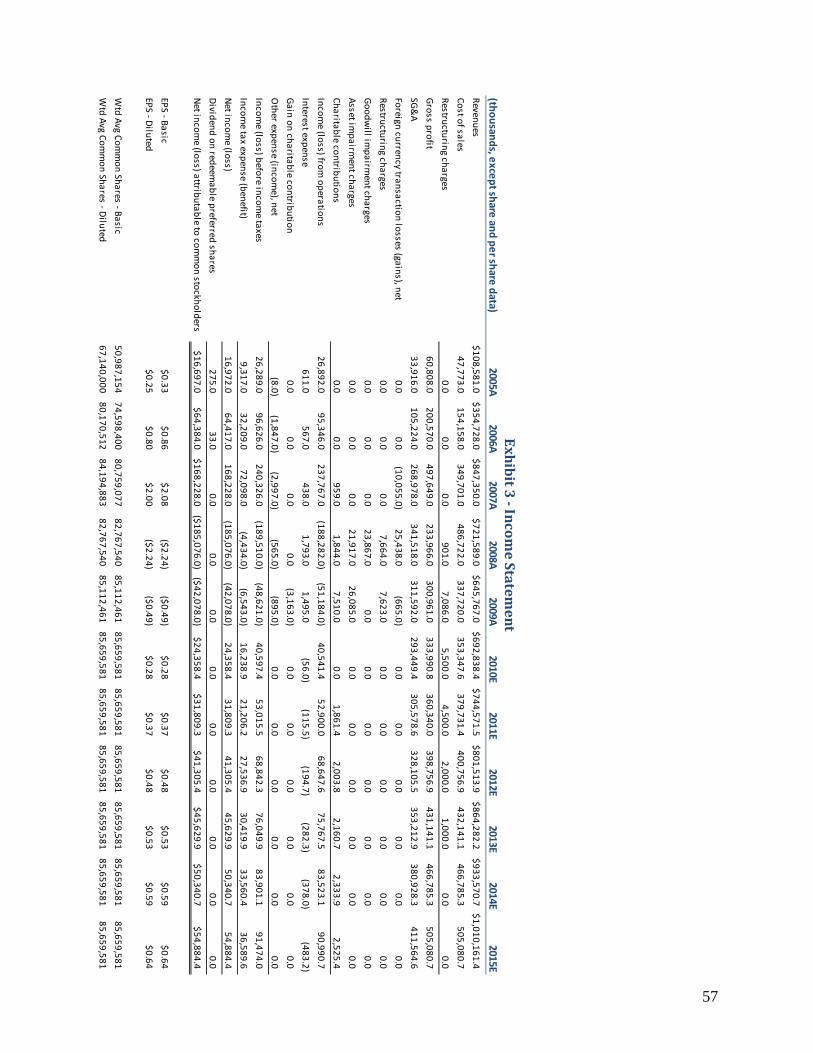

Normalized earnings

Based on our analysis of the items outlined above, we have prepared a normalized income

statement in which we have adjusted income before taxes for any one-time/non-recurring items.

Exhibit 3 ‐ Income Statement Normalized Income StatementAudited Adjustments Normalized Audited Adjustments Normalized

(thousands, except share and per share data) 2008A 2008A 2008A 2009A 2009A 2009A

Revenues $721,589.0 $0.0 $721,589.0 $645,767.0 $0.0 $645,767.0

Cost of sales 486,722.0 (118,164.3) 368,557.7 337,720.0 10,564.0 348,284.0

Restructuring charges 901.0 0.0 0.0 7,086.0 0.0 0.0

Gross profit 233,966.0 118,164.3 353,031.3 300,961.0 (10,564.0) 297,483.0

SG&A 341,518.0 (12,300.0) 329,218.0 311,592.0 (17,200.0) 294,392.0

Foreign currency transaction losses (gains), net 25,438.0 0.0 25,438.0 (665.0) 0.0 (665.0)

Restructuring charges 7,664.0 (7,664.0) 0.0 7,623.0 (7,623.0) 0.0

Goodwill impairment charges 23,867.0 (23,867.0) 0.0 0.0 0.0 0.0

Asset impairment charges 21,917.0 (21,917.0) 0.0 26,085.0 (26,085.0) 0.0

Charitable contributions 1,844.0 0.0 1,844.0 7,510.0 0.0 7,510.0

Income (loss) from operations (188,282.0) 183,912.3 (3,468.7) (51,184.0) 0.0 (3,754.0)

Interest expense 1,793.0 0.0 1,793.0 1,495.0 0.0 1,495.0

Gain on charitable contribution 0.0 0.0 0.0 (3,163.0) 3,163.0 0.0

Other expense (income), net (565.0) 0.0 (565.0) (895.0) 0.0 (895.0)

Income (loss) before income taxes (189,510.0) 183,912.3 (4,696.7) (48,621.0) (3,163.0) (4,354.0)

Refer to Exhibit 5 for a summary of the non-recurring/one-time adjustments that were

incorporated into the normalized income statement above.

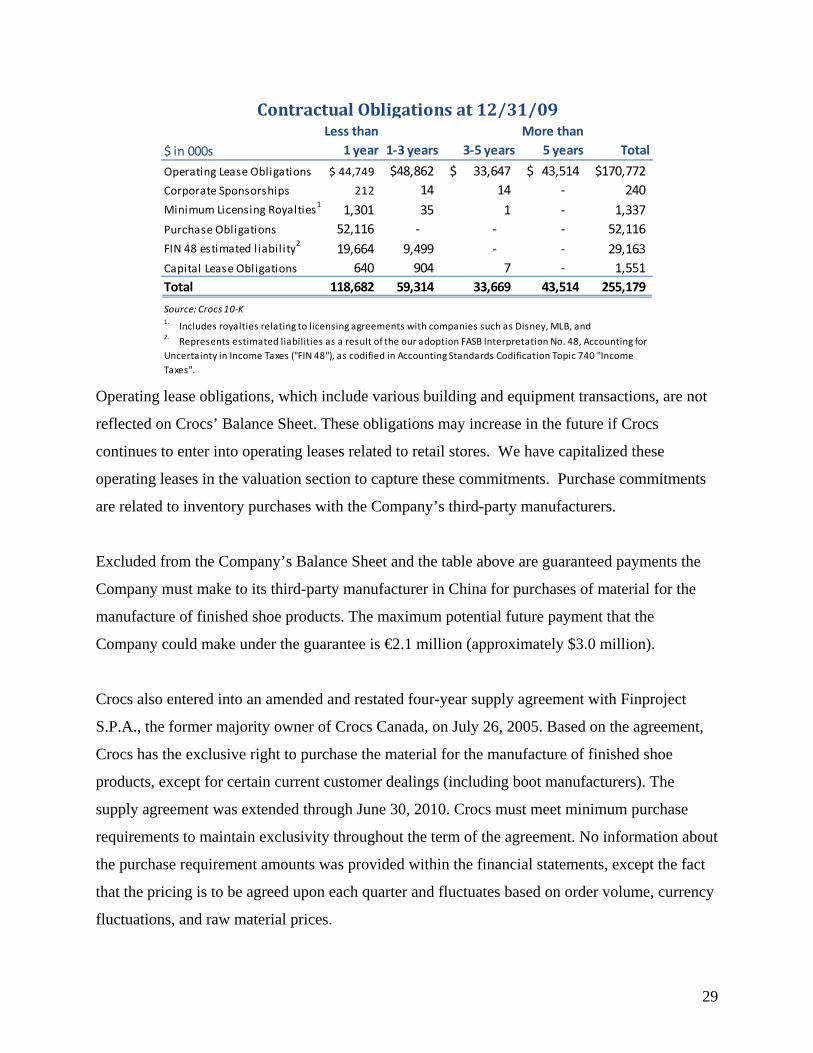

Off-Balance Sheet Exposures and Contractual Obligations

A summary of Crocs’ contractual obligations is as follows:

29

$ in 000s

Less than

1 year 1‐3 years 3‐5 years

More than

5 years Total

Operating Lease Obligations 44,749$ 48,862$ 33,647$ 43,514$ 170,772$

Corporate Sponsorships 212 14 14 ‐ 240

Minimum Licensing Royalties1

1,301 35 1 ‐ 1,337

Purchase Obligations 52,116 ‐ ‐ ‐ 52,116

FIN 48 estimated l iabil ity2

19,664 9,499 ‐ ‐ 29,163

Capital Lease Obligations 640 904 7 ‐ 1,551

Total 118,682 59,314 33,669 43,514 255,179

Source: Crocs 10‐K

Contractual Obligations at 12/31/09

2. Represents estimated liabilities as a result of the our adoption FASB Interpretation No. 48, Accounting for

Uncertainty in Income Taxes ("FIN 48"), as codified in Accounting Standards Codification Topic 740 "Income

Taxes".

1. Includes royalties relating to licensing agreements with companies such as Disney, MLB, and

Operating lease obligations, which include various building and equipment transactions, are not

reflected on Crocs’ Balance Sheet. These obligations may increase in the future if Crocs

continues to enter into operating leases related to retail stores. We have capitalized these

operating leases in the valuation section to capture these commitments. Purchase commitments

are related to inventory purchases with the Company’s third-party manufacturers.

Excluded from the Company’s Balance Sheet and the table above are guaranteed payments the

Company must make to its third-party manufacturer in China for purchases of material for the

manufacture of finished shoe products. The maximum potential future payment that the

Company could make under the guarantee is €2.1 million (approximately $3.0 million).

Crocs also entered into an amended and restated four-year supply agreement with Finproject

S.P.A., the former majority owner of Crocs Canada, on July 26, 2005. Based on the agreement,

Crocs has the exclusive right to purchase the material for the manufacture of finished shoe

products, except for certain current customer dealings (including boot manufacturers). The

supply agreement was extended through June 30, 2010. Crocs must meet minimum purchase

requirements to maintain exclusivity throughout the term of the agreement. No information about

the purchase requirement amounts was provided within the financial statements, except the fact

that the pricing is to be agreed upon each quarter and fluctuates based on order volume, currency

fluctuations, and raw material prices.

30

Liquidity and Capital Resources

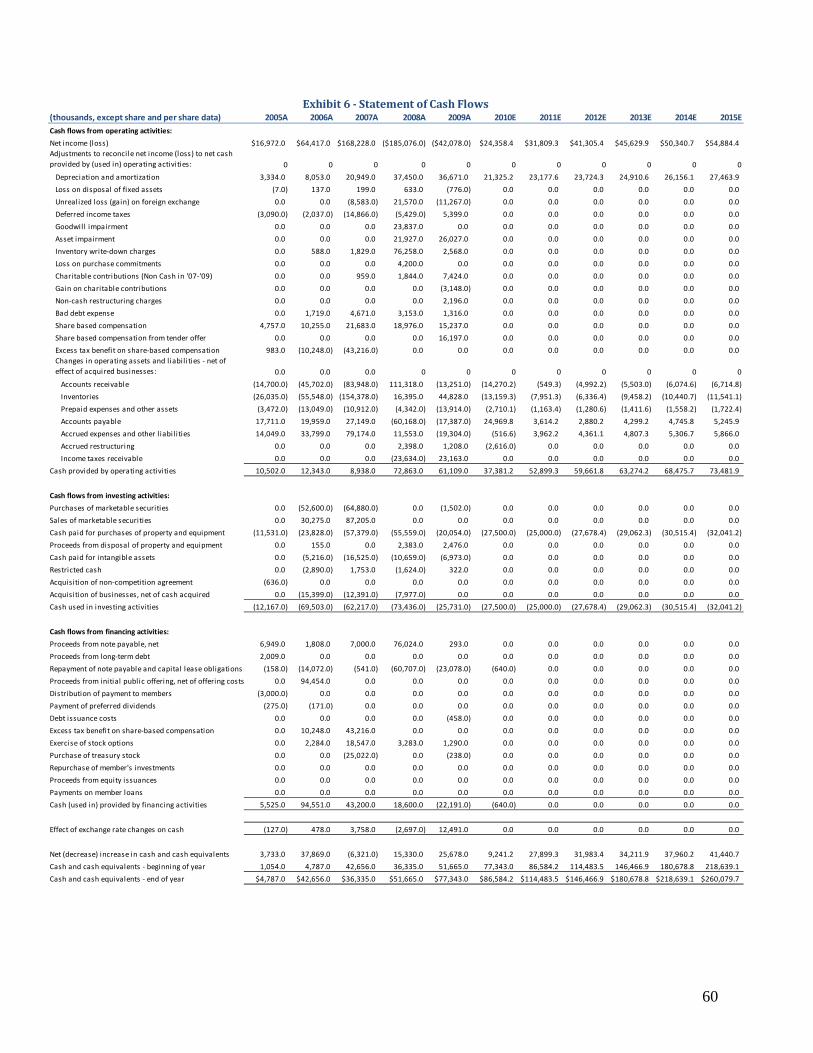

At December 31, 2009, Crocs had $77.3 million in cash and cash equivalents. Refer to Exhibit 6

for the Company’s historical Statement of Cash Flows.

During FY09, the Company fully repaid its Revolving Credit Facility with Union Bank of

California, N.A. (approximately $23 million). In order to secure additional liquidity for the

future, on September 25, 2009, the Company entered into a Revolving Credit and Security

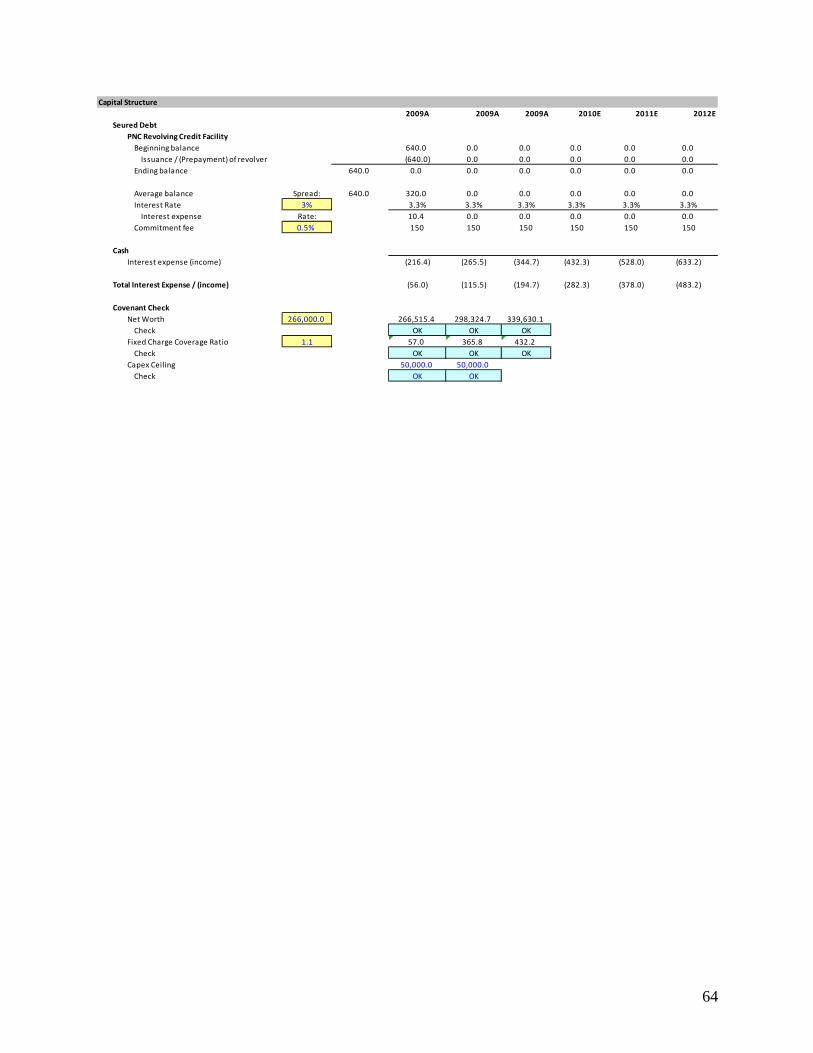

Agreement with PNC Bank, N.A, which matures on September 25, 2012. As outlined within the

Company’s 10-K, this agreement provides for an asset-backed revolving credit facility of up to

$30 million in total, and contains the following sublimits:

$17.5 million sublimit for borrowings against eligible inventory

$2 million sublimit for borrowings against the Company’s eligible inventory in-transit

$4 million sublimit for letters of credit asset-backed revolving lines of credit.

The total borrowings available under the Credit Agreement are also subject to customary

reserves and reductions to the extent the Company’s asset borrowing base changes. Borrowings

are secured by all Company assets, including all receivables, equipment, general intangibles,

inventory, investment property, subsidiary stock and leasehold interests. The Company must

prepay borrowings under the agreement in the event of certain dispositions of property.

Per the Company’s financial statements, interest due on domestic principal amounts outstanding

is charged as a 2% premium over the rate that is the greater than either:

(i) PNC's published reference rate,

(ii) The Federal Funds Open Rate in effect on such day plus 0.5% , or

(iii) The sum of the daily LIBOR rate and 1.0%, with respect to domestic rate loans.

Eurodollar denominated principal amounts (Eurodollar loans) outstanding bear interest of 3.50%

premium over a rate that is the greater of:

i. The Eurodollar rate, or

ii. 1.50%.

31

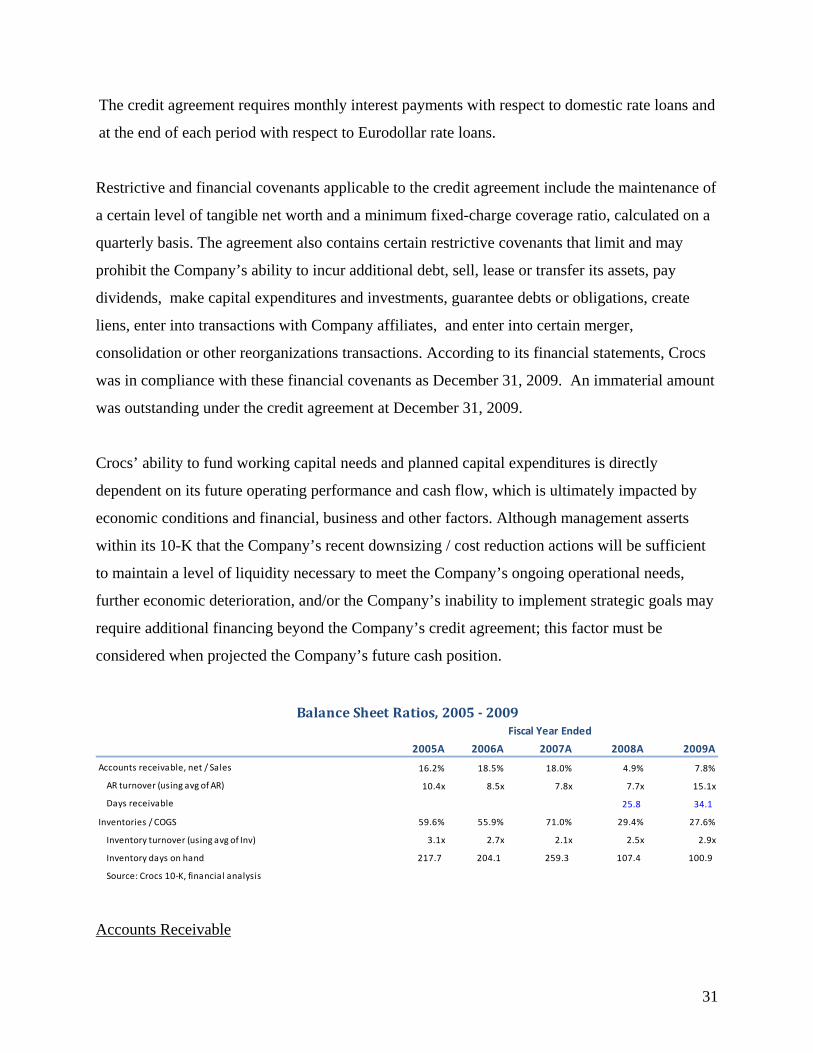

The credit agreement requires monthly interest payments with respect to domestic rate loans and

at the end of each period with respect to Eurodollar rate loans.

Restrictive and financial covenants applicable to the credit agreement include the maintenance of

a certain level of tangible net worth and a minimum fixed-charge coverage ratio, calculated on a

quarterly basis. The agreement also contains certain restrictive covenants that limit and may

prohibit the Company’s ability to incur additional debt, sell, lease or transfer its assets, pay

dividends, make capital expenditures and investments, guarantee debts or obligations, create

liens, enter into transactions with Company affiliates, and enter into certain merger,

consolidation or other reorganizations transactions. According to its financial statements, Crocs

was in compliance with these financial covenants as December 31, 2009. An immaterial amount

was outstanding under the credit agreement at December 31, 2009.

Crocs’ ability to fund working capital needs and planned capital expenditures is directly

dependent on its future operating performance and cash flow, which is ultimately impacted by

economic conditions and financial, business and other factors. Although management asserts

within its 10-K that the Company’s recent downsizing / cost reduction actions will be sufficient

to maintain a level of liquidity necessary to meet the Company’s ongoing operational needs,

further economic deterioration, and/or the Company’s inability to implement strategic goals may

require additional financing beyond the Company’s credit agreement; this factor must be

considered when projected the Company’s future cash position.

2005A 2006A 2007A 2008A 2009A

Accounts receivable, net / Sales 16.2% 18.5% 18.0% 4.9% 7.8%

AR turnover (using avg of AR) 10.4x 8.5x 7.8x 7.7x 15.1x

Days receivable 25.8 34.1

Inventories / COGS 59.6% 55.9% 71.0% 29.4% 27.6%

Inventory turnover (using avg of Inv) 3.1x 2.7x 2.1x 2.5x 2.9x

Inventory days on hand 217.7 204.1 259.3 107.4 100.9

Source: Crocs 10‐K, financial analysis

Fiscal Year Ended

Balance Sheet Ratios, 2005 ‐ 2009

Accounts Receivable

32

One item important to consider when analyzing Croc’s cash flows is that seasonal variations in

product demand and the associated changes in operating assets and liabilities may impact cash

flows from operations. Further, changes in macroeconomic conditions can affect customers’

liquidity and ability to pay amounts due. If the Company were to have difficultly collecting its

accounts receivable, its cash flows and capital resources could be negatively impacted.

Per Croc’s 10-K, the Company monitors its accounts receivable aging and records reserves as

applicable. The accounts receivable balance as of December 31, 2009 was $50.5 million, an

increase of $15.2 million compared to the balance as of December 31, 2008. The increase in

accounts receivable was largely the result of higher sales during Q409 compared to Q408. Days

sales outstanding increased from 25.8 days at December 31, 2008 to 34.1 days at December 31,

2009. This increase was driven by the previously described granting of return request and

allowances to customers in the fourth quarter of 2008. This action caused a lower net accounts

receivable balance for 2008. The combination of these factors artificially lowered the days sales

outstanding for 2008 by approximately 10 days, and therefore 34.1 days is a realistic estimate of

the Company’s days sales outstanding.

Inventory

Crocs inventory balance decreased to $93.3 million at December 31, 2009, from $143.2 million

as of December 31, 2008. As previously described, the Company began an active inventory

management program in 2008, including decreased production and actively selling existing

inventory. This has allowed the Company to increase its inventory turnover ratio and decrease

days on hand. Note that new product introductions, limitations on production capacities and

seasonal variations require that the Company adjust to meet changing market conditions and may

result in material fluctuations in the inventory balance.

Cash Management and Risks

Crocs operates in many different countries, which requires that cash be held in various different

currencies. The global market has recently experienced many fluctuations in foreign currency

exchange rates, and as discussed above, the Company’s results of operations and cash positions

have been significantly impacted. In conjunction with the previously mentioned impact to

33

earnings, foreign exchange fluctuations impacted Croc’s cash balance in the amounts of

$3,758,000, ($2,697,000), and $12,491,000 during FY07, FY08 and FY09, respectively. Any

future fluctuation in foreign currencies may have a material impact on Crocs’ cash flows and

capital resources.

Although Crocs has substantial cash requirements in the U.S., the majority of its cash is

generated and maintained abroad. Management considers unremitted earnings of subsidiaries

operating outside of the U.S. to be indefinitely reinvested, and to be used for the ongoing

operations of the international location of business. Although management does not intend to

change this position, most of the cash held outside of the U.S. could be repatriated to the U.S. but

would be subject to U.S. federal and state income taxes, less applicable foreign tax credits. To

further complicate matters, repatriation of certain foreign balances is restricted by local laws and

could have adverse tax consequences if the Company were to move cash from one country to

another.

At December 31, 2009, $64.8 million of the total $77.3 million in cash was held in international

locations. Of the $64.8 million, $16.0 million could potentially be restricted, as described above.

If the remaining $48.8 million were repatriated to the U.S., the Company would be required to

pay approximately $1.7 million in international withholding taxes with no offsetting foreign tax

credit.

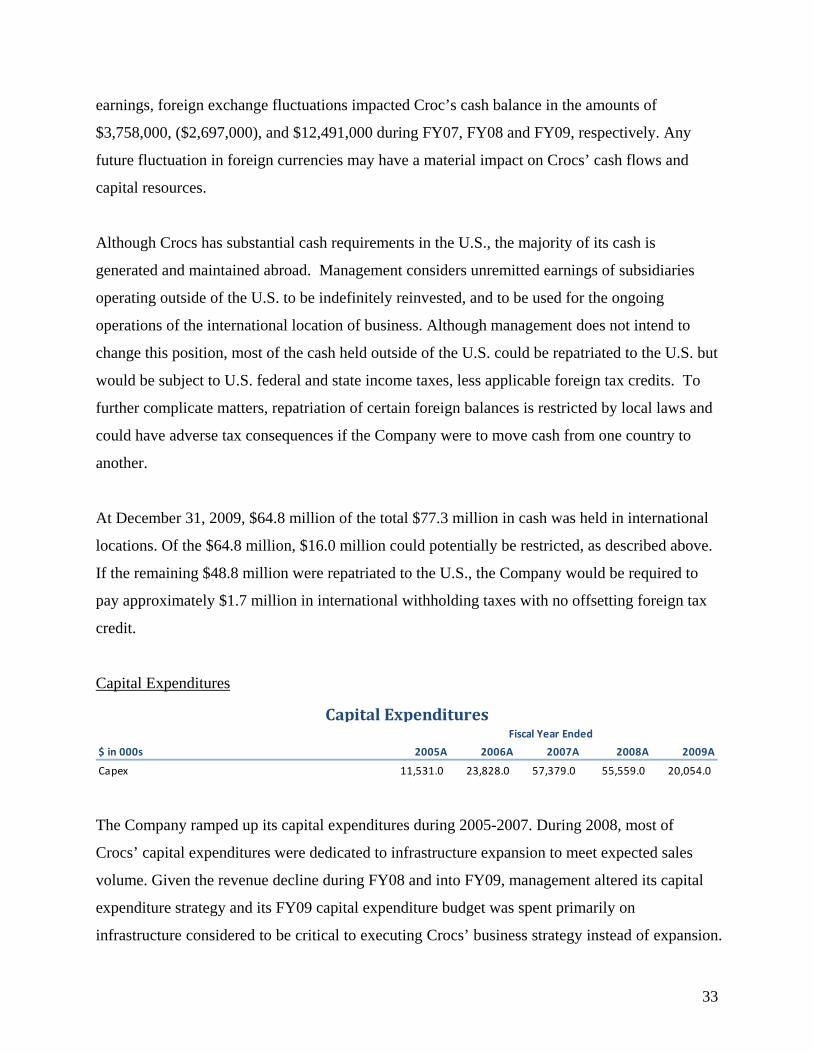

Capital Expenditures

$ in 000s 2005A 2006A 2007A 2008A 2009A

Capex 11,531.0 23,828.0 57,379.0 55,559.0 20,054.0

Fiscal Year Ended

Capital Expenditures

The Company ramped up its capital expenditures during 2005-2007. During 2008, most of

Crocs’ capital expenditures were dedicated to infrastructure expansion to meet expected sales

volume. Given the revenue decline during FY08 and into FY09, management altered its capital

expenditure strategy and its FY09 capital expenditure budget was spent primarily on

infrastructure considered to be critical to executing Crocs’ business strategy instead of expansion.

34

Management plans to continue to make ongoing capital investments in molds and other tooling

equipment related to manufacturing new products and footwear styles as well as those related to

opening additional retail stores. Management also plans to continue to invest in its global

information systems infrastructure to further strengthen its management information and

financial reporting capabilities. Note, however, that the Company:

Has slowed the pace at which it is opening new retail stores

Plans to reduce expenditures in its distribution and manufacturing activities due to a

reduction in revenues, and

Is currently in the process of implementing new software systems which management

hopes to bring greater efficiencies to the Company’s distribution strategy in the long

term.

These capital expenditures also do not capture implied Capex the company would need if they

owned the stores instead of using operating leases. In the following valuation section, we have

capitalized these operating leases and therefore included an estimated amount of Capex needed

for these stores.

35

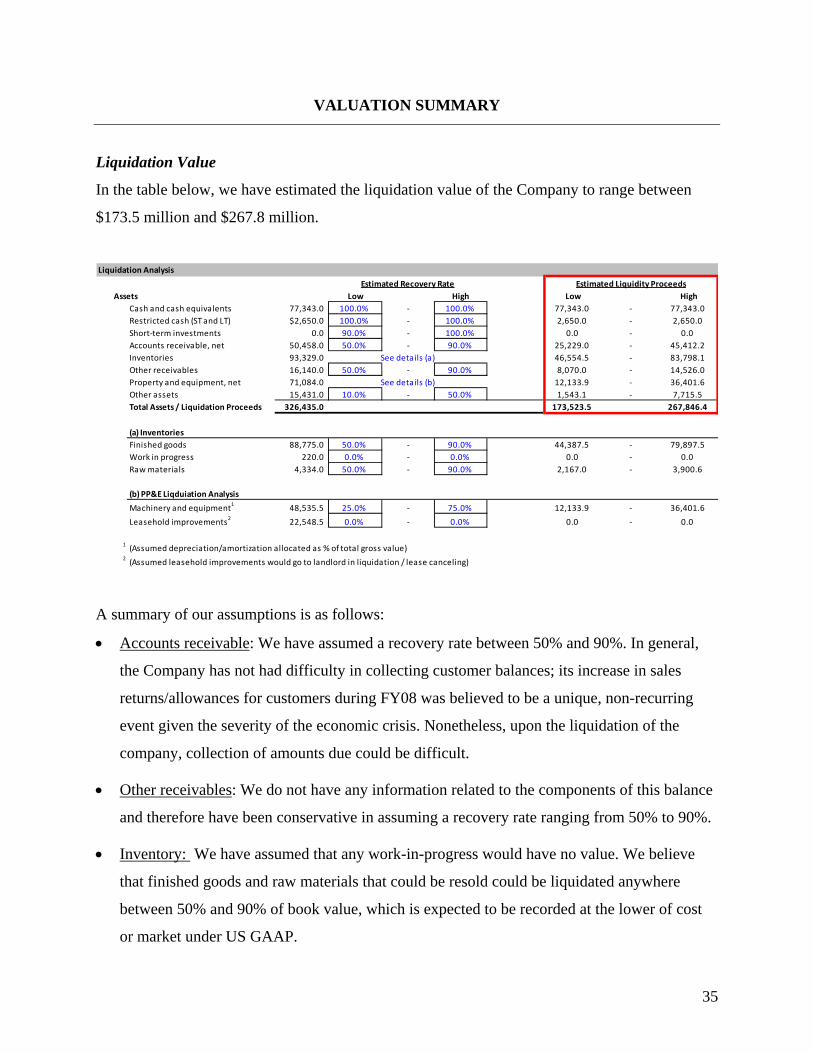

VALUATION SUMMARY

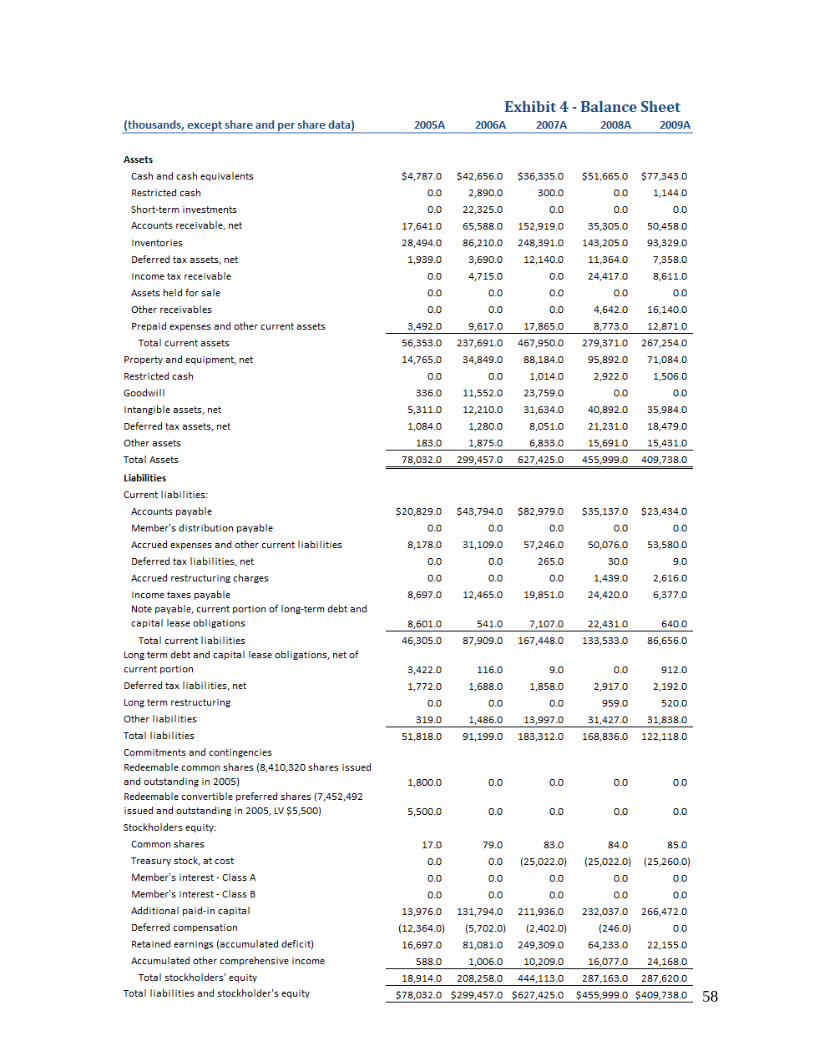

Liquidation Value

In the table below, we have estimated the liquidation value of the Company to range between

$173.5 million and $267.8 million.

Liquidation Analysis

Estimated Recovery Rate

Assets Low High Low High

Cash and cash equivalents 77,343.0 100.0% ‐ 100.0% 77,343.0 ‐ 77,343.0

Restricted cash (ST and LT) $2,650.0 100.0% ‐ 100.0% 2,650.0 ‐ 2,650.0

Short‐term investments 0.0 90.0% ‐ 100.0% 0.0 ‐ 0.0

Accounts receivable, net 50,458.0 50.0% ‐ 90.0% 25,229.0 ‐ 45,412.2

Inventories 93,329.0 See details (a) 46,554.5 ‐ 83,798.1

Other receivables 16,140.0 50.0% ‐ 90.0% 8,070.0 ‐ 14,526.0

Property and equipment, net 71,084.0 See details (b) 12,133.9 ‐ 36,401.6

Other assets 15,431.0 10.0% ‐ 50.0% 1,543.1 ‐ 7,715.5

Total Assets / Liquidation Proceeds 326,435.0 173,523.5 267,846.4

(a) Inventories

Finished goods 88,775.0 50.0% ‐ 90.0% 44,387.5 ‐ 79,897.5

Work in progress 220.0 0.0% ‐ 0.0% 0.0 ‐ 0.0

Raw materials 4,334.0 50.0% ‐ 90.0% 2,167.0 ‐ 3,900.6

(b) PP&E Liqduiation Analysis

Machinery and equipment1

48,535.5 25.0% ‐ 75.0% 12,133.9 ‐ 36,401.6

Leasehold improvements2

22,548.5 0.0% ‐ 0.0% 0.0 ‐ 0.0

1(Assumed depreciation/amortization allocated as % of total gross value)

2(Assumed leasehold improvements would go to landlord in liquidation / lease canceling)

Estimated Liquidity Proceeds

A summary of our assumptions is as follows:

Accounts receivable: We have assumed a recovery rate between 50% and 90%. In general,

the Company has not had difficulty in collecting customer balances; its increase in sales

returns/allowances for customers during FY08 was believed to be a unique, non-recurring

event given the severity of the economic crisis. Nonetheless, upon the liquidation of the

company, collection of amounts due could be difficult.

Other receivables: We do not have any information related to the components of this balance

and therefore have been conservative in assuming a recovery rate ranging from 50% to 90%.

Inventory: We have assumed that any work-in-progress would have no value. We believe

that finished goods and raw materials that could be resold could be liquidated anywhere

between 50% and 90% of book value, which is expected to be recorded at the lower of cost

or market under US GAAP.

36

Property, Plant and Equipment: We have assumed that all leasehold improvements would

have no recovery value, as the improvements are likely connected to the leased property and

would therefore be returned to the landlord upon liquidation/lease termination. We allocated

the total depreciation/amortization on PP&E to each leasehold improvements and machinery

& equipment based on relative gross values. As it pertains to machinery & equipment, we

assumed a low recovery value, somewhere between 25% and 75%.

Other assets: Similar to the other receivables balance, we do not know the components of

this balance. Given the nature of other assets accounts, we have assumed that the recovery

rate would be extremely low, somewhere between 10% and 50%.

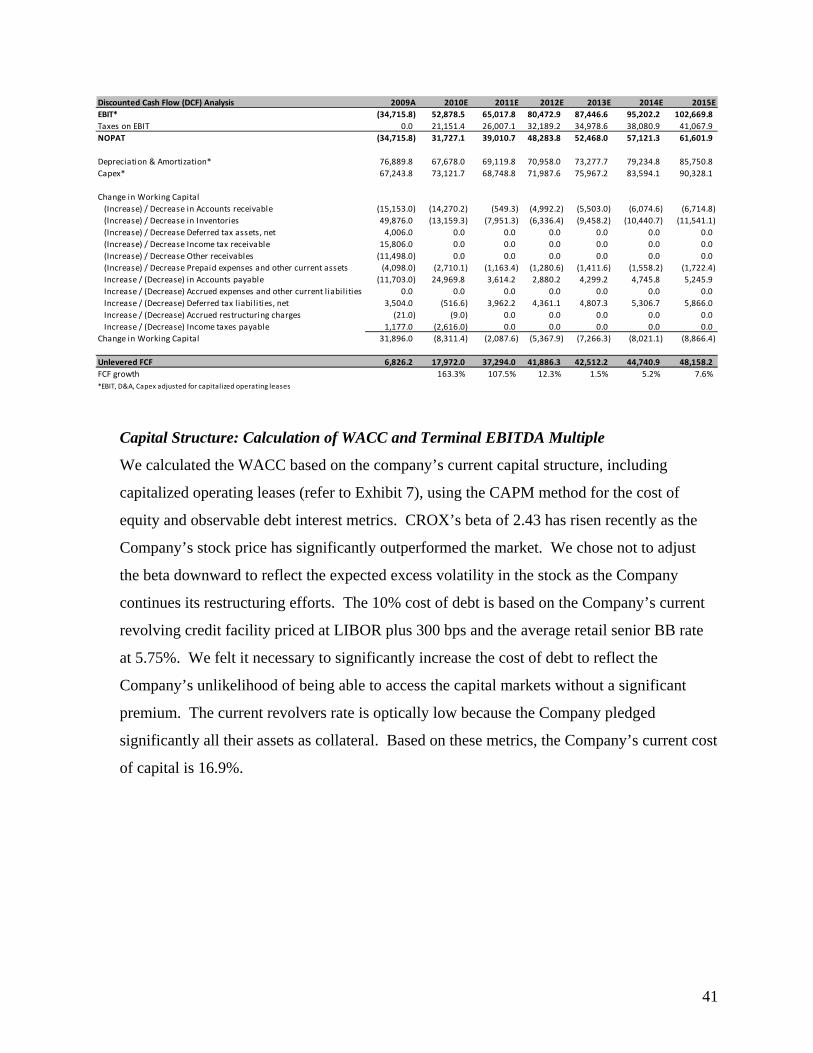

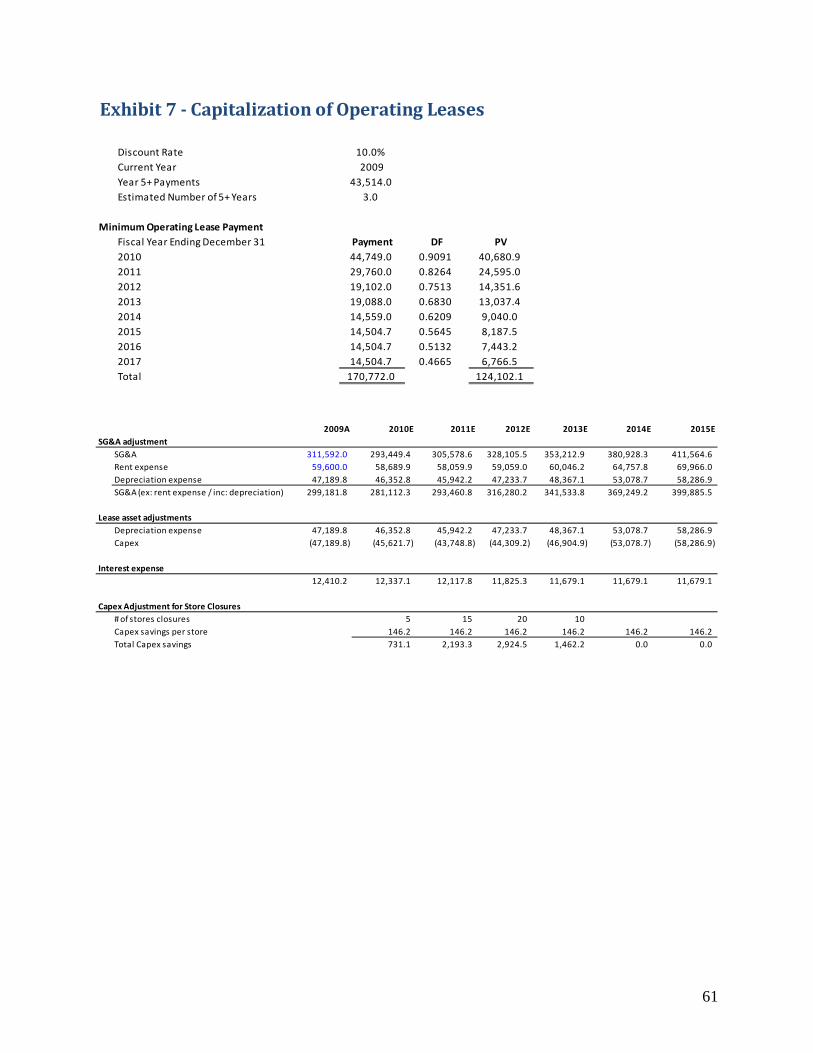

Valuation – Turnaround Strategy, No Liquidation

We have utilized a discounted cash flow model to determine the value of Crocs. Refer to Exhibit

3 for financial statement projections.

Note that prior to projecting the FY10-FY15 financial statements, we normalized FY08 and

FY09 earnings as described in the Financial Overview section so that we had a more realistic

base year upon which we could perform our projections. Refer to Exhibit 5 and the Financial

Overview section of this report for additional information on the items we considered as non-

recurring that have been incorporated into our model. We have also capitalized the operating

leases and restated rent expense as interest expense and depreciation.

Key assumptions included in our free cash flow calculation are as follows:

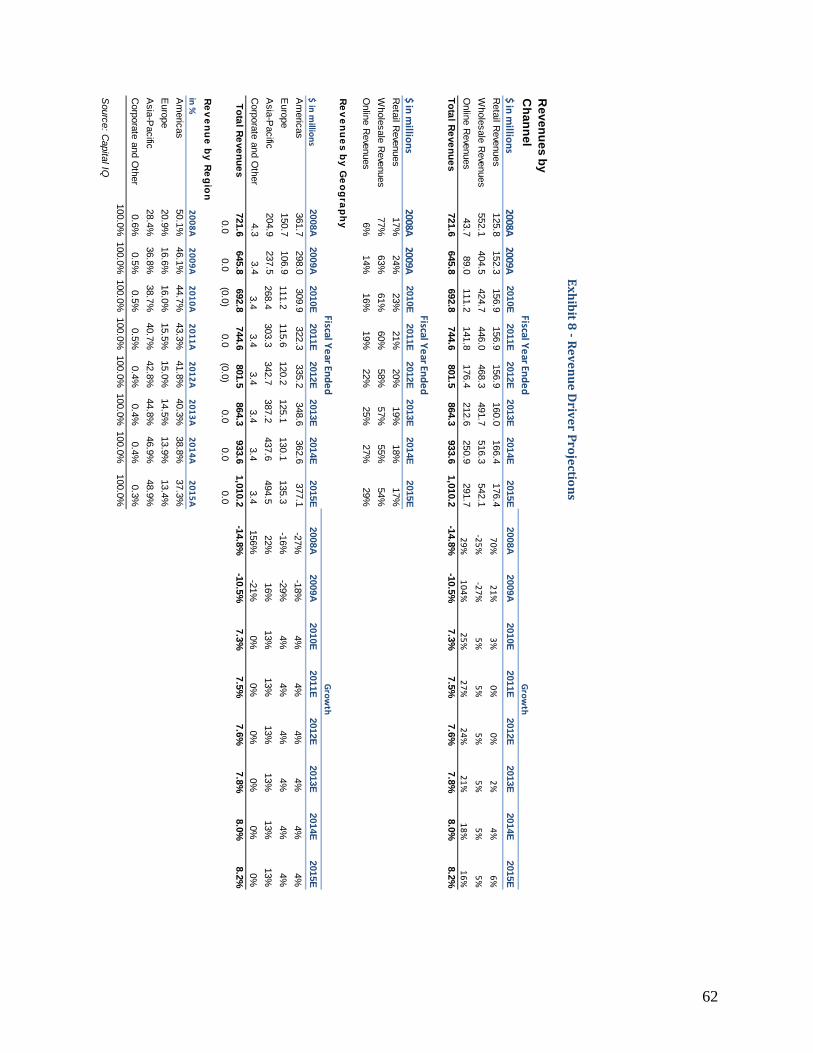

Revenues: We have analyzed and projected revenue growth both by geography and

distribution channel. Refer Exhibit 8 for projected revenue drivers. We have assumed

revenue growth based on various factors:

o GDP growth by geography: We have utilized 2010/2011 GDP growth estimates

recently published by the World Bank34 as our base for growth projections by

geography as we believe GDP growth will fuel the trend in shoe purchases (volume).

Based on expert estimates, GDP growth will continue to be slow within the US and

34 http://siteresources.worldbank.org/INTGEP2010/Resources/GEP2010-Full-Report.pdf

37

Europe over the next two to five years. We have therefore assumed a growth rate of

4% in both regions over the next 5 years. We have assumed a significantly higher

growth rate of 13% for China over the same period; this is slightly more optimistic

than GDP growth expectation for the country but we believe the Crocs product is still

within its growth phase in this region and therefore expect continued significant

revenue growth in this region. We expect the Americas and Europe revenue

contribution to decline while Asia-Pacific revenue contribution increases. Ultimately,

we envision revenues to be comprised of 37.3%, 13.4% and 48.9% associated with

the Americas, Europe and Asia-Pacific, respectively. Also note that our growth

projections are above GDP growth estimates due to our expectation that revenues will

continue to grow in the retail and online space (as described below), where the

Company is able to charge higher sales prices; total retail and online revenues are

expected to represent 49% of total revenues in 2015, compared to 37% in 2009.

o Distribution channel mix: Given our turnaround strategy, detailed in a later section, of

renewing focus on wholesale relationships, continuing growth in retail kiosks, closing

various retail locations in the Americas and maintaining retail stores internationally,

we have assumed retail growth of 6% and wholesale growth of 4% throughout the

projected period. We anticipate continued online revenue growth given the constant

increase in ecommerce and the use of the internet. We do, however, expect growth to

slightly taper over the 5 year period. Ultimately, we project revenues to be comprised

of 21.4%, 50.7% and 28.0% associated with Retail, Wholesale and Online revenues,

respectively

Cost of Sales: Over the last three years, Crocs’ cost of sales has increased significantly, from

41.3% to 50.9% to 55.1% of FY07, FY08 normalized and FY09 normalized revenue,

respectively. This increase reflects increased salaries related to retail business growth and

increased component costs related to a greater variety of product lines. Although we expect

further decreases in product variety, we do not anticipate reaching historical cost of sale %

levels. We also expect cost of sales to slightly decline with an increase in online sales as

online distribution is a low cost form of distribution. We have therefore selected a COS/Sales

ratio of 52% for FY10 and 50% for FY11-FY15. Also note that we anticipate the closure of

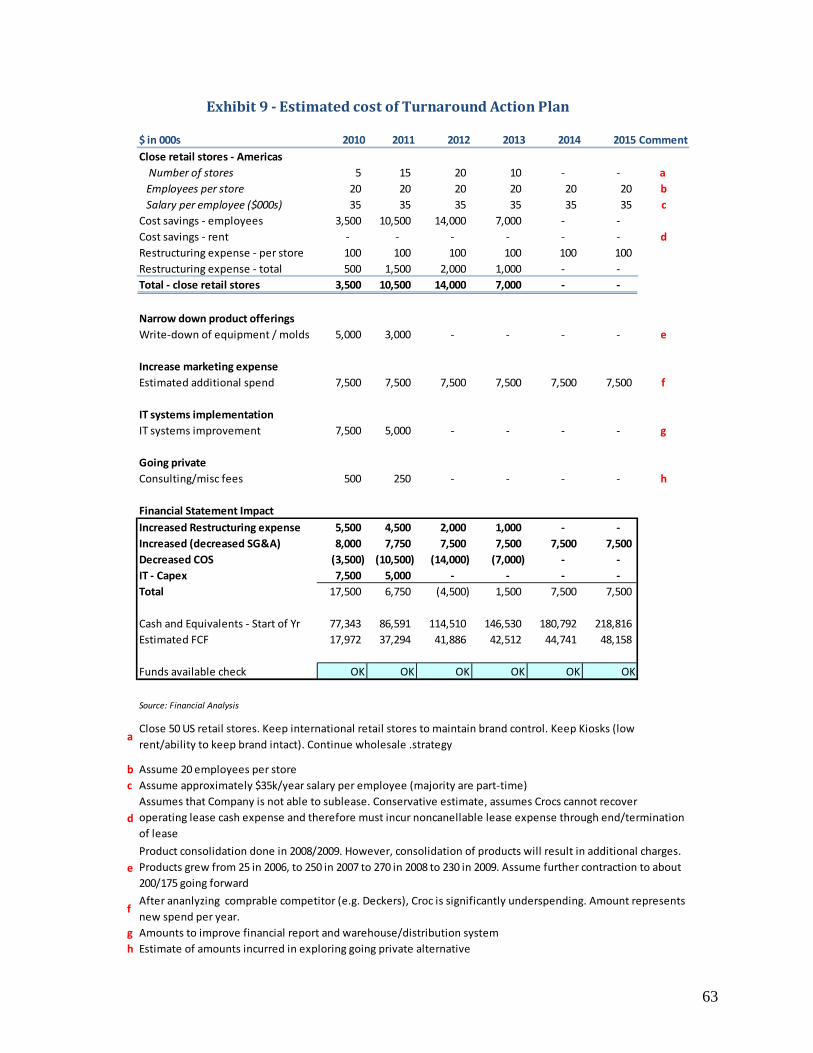

50 retail stores in conjunction with our turnaround plan and have calculated the net impact to

38

the cost of sales; this impact has been incorporated into projected cost of sales. Refer to

Exhibit 9 for a summary of the financial impact of our turnaround plan actions.