research paper-harshil shah 317

TRANSCRIPT

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 1/22

wuiopasdfghjklzxcvbnmqwerty

opasdfghjklzxcbnmqwertyuiopa

fghjklzxcvbnmqwertyuiopasdfg

klzxcvbnmqwertyuiopasdfghjklz

vbnmqwertyuiopasdfghjklzxcvb

mqwertyuiopasdfghjklzxcvbnm

wertyuiopasdfghjklzxcvbnmqweuiopasdfghjklzxcvbnmqwertyu

asdfghjklzxcvbnmqwertyuiopa

fghjklzxcvbnmqwertyuiopasdfgklzxcvbnmqwertyuiopasdfghjklz

vbnmqwertyuiopasdfghjklzxcvb

mqwertyuiopasdfghjklzxcvbnmwertyuiopasdfghjklzxcvbnmqwe

uiopasdfghjklzxcvbnmqwertyu

asdfghjklzxcvbnmrtyuiopasdfg

RISK MANAGEMENT & COMPLIANCE:CURRENT STATE & ITS FUTURE OUTLOOK

RESEARCH PAPER TRIMESTER XV

SUBMITTED BY:HARSHIL SHAHROLL NO. 317

MBA TECHMANUFACTURING / FINANCE

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 2/22

Table of Contents

Table of Contents ........................................................................................................ 2

THE INDIAN ECONOMY ................................................................................................ 3

INDIAN FINANCIAL SYSTEM ......................................................................................... 4

RISK MANAGEMENT ..................................................................................................... 5

INTRODUCTION ....................................................................................................... 5

RISK MANAGEMENT: AN INSIGHT ............................................................................. 6

CURRENT TRENDS & TECHNIQUES .............................................................................. 7

Liquidity risk: ........................................................................................................... 7

Capital Buffers: ........................................................................................................ 8

Supply chain risk ..................................................................................................... 8

Information risk ....................................................................................................... 8

Environmental compliance ..................................................................................... 9

Technology ............................................................................................................. 9

FUTURE OUTLOOK: TRENDS & TECHNIQUES ............................................................... 9

GAME CHANGERS ...................................................................................................... 18

CONCLUSION ............................................................................................................ 21

2 | P a g e

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 3/22

Risk Management & Compliance:

Current State & Its Future Outlook

THE INDIAN ECONOMY

Before the dawn of the liberalization era, India had pawned 67 tons of gold to

the Bank of England and Union bank of Switzerland to improve upon its

dwindling ForEx reserves thereby increasing the demand for USD in the

global markets. Two decades later, with the Indian economy reformed and

booming, the odds have shifted in India’s favor. Indian Government on the

back-run of a strong GDP figures, robust growth and persistent future outlook

had bought 200 tons of gold from International Monetary Fund (IMF). The

country’s sound Banking structure and rising economy aided in improving

the ForEx reserves to $295 billion as against a mere $2billion in 1991. 1

These are the signs for upbeat Indian economy dominance in 2010 and years

to come. Also, the Indian economy is booming in the wake of strong

economic policy decisions, legal framework and a healthy regulatory regime

under the able guidance of regulatory bodies’ viz. RBI, IRDA, SEBI.

The strong growth potential and robust structure of the banking setup in the

country will define the roadmap in the future and its effects will be far

fetching enabling the country to achieve its ultimate goal of high growth

rates. The strong framework will enable the Indian economy to achieve its

potential and reach its farfetched goal of dominance and supremacy.

1 http://www.forbes.com/2010/01/07/india-economy-inflation-entrepreneurs-wharton.html

3 | P a g e

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 4/22

Another major factor contributing to the growth is the Banking Sector which

is the nucleus of the nation’s robust development reforms. The BASEL II

norm which has been accorded from the Bank of International Settlements is

an attempt to implement a sound framework to quantify and measure the

various risks associated with the Banking sector.

INDIAN FINANCIAL SYSTEM

A decade of strong financial reforms and robust framework, the success of

the Indian financial framework is unprecedented. The Indian economy is

surging to its peak and has gathered the critical mass to make a force to

reckon with in the global financial markets. Today, the Indian economy and

its financial system are amongst the leading financial markets and have

created a niche for themselves. The regulatory framework and structural

reforms have ignited the spirit of growth and has improved the profitability of

banks and its assets quality. 2

With the advent of globalization and the Internet era, the dream of an

integrated global markets and economies is becoming a living reality. The

increasing penetration of the internet technology in the banking arena haswidened the global banking frontiers and making it possible for financial

firms to market and trade their products & services on a global platform

thereby increasing their presence & reach across varied cultures, countries

and classes of people. With the opening up of the financial services arena

under the WTO, the spread of internet banking will be astronomical. Thus,

the Indian financial services sector will get the impetus and the opportunity

to expand on a QUID PRO QUO BASIS.

As is the case with all the sectors & industries, the banking unit is also facing

tough competition as per the Porter’s five force model from “Rivalry among

the competitors.” This intense competitive war is enhancing & driving the

2 http://www.coolavenues.com/mba-journal/finance/future-risk-management-indian-banking-industry?page=0,0

4 | P a g e

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 5/22

growth in the banking sector. As per the international requirements, RBI is

thus enforcing a standardized approach of BASEL II accord for all the banks.

This will enable all the banks to enforce a robust structure and account the

various risks associated with their operations thereby creating a better

framework for risk management within the industry.

RISK MANAGEMENT

INTRODUCTIONRisk management in banks has come to fore with the increase in the bank’s

activities. With the advent of the globalization era and rising prowess of the

Indian economy, the Indian banking sector has witnessed rampant increase

in their deposits and borrowings. The per capita income of an average Indian

has increased ten folds, thereby increasing their spending ability and also

increasing their deposits & investments. Thus, various steps have been

undertaken by RBI to regulate and monitor the increase in these activities

and also to formulate a robust risk management framework in order to

reduce the risks and the losses incurred thru the associated risks involved.

With the advent of globalization, liberalization and privatization of the

economy, the risk management scenario in the country needs to be further

strengthened, regulated and integrated at par levels with its global

counterparts. The risk management is needed to be carried out in a more

proactive & mature manner to improve the quality of credit & a strongerrobust financial system.

The current Asset Liability Management (ALM) system is the key focus area.

As we have seen in the past twelve months, the interest rates have been

revised 7times resulting in asset liability mismatches and their frequent re-

5 | P a g e

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 6/22

pricing. This indicates the importance of a strong risk management system.

The calculation of the various risks need to be undertaken thru the use of

advanced credit scoring models such as Merton’s model and Altzman’s credit

scoring model. These models are needed to be used in a more sophisticated

and developed manner to minimize the effects of the various risks associated

with the banking activities.

The implementation of the BASEL II accord will be important for the savings

to be mobilized in the right direction and enable better control and reduction

of the risks associated to create a sound Risk management system.

Also, BASEL III accord will be implemented by 2012 which adds to the risks

associated and will enable a better system to be set up in the future of Risk

management systems.

RISK MANAGEMENT: AN INSIGHT

The global markets are now recovering from the recession that it faced due

to the credit crunch. The recession was also a result of the non recovery of

the funds and poor risk management systems implementation in the

financial system. The main reason for the recession was the lack of clarity

and transparency in the system which led to the massive downfall of the US

Financial markets.

With the aid of the fiscal stimulus provided by the government to the

financial bodies the markets have entered the path of recovery again but

with a caution step. The financial institutions have started taking

precautionary measures and have set forth financial norms across all levels

in the form of BASEL II and BASEL III norms and common financial reporting

guidelines for all sectors and industries through the adaptation of IFRS

Guidelines.

The global dynamics will continue to be challenging post the recession period

through rapidly evolving risk management and regulatory framework. With

6 | P a g e

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 7/22

India now on the global map and a hot destination for parking foreign funds,

Indian Financial Institutions are also implementing BASEL II norms across all

the banks and are being continuously monitored and governed by RBI to

maintain the standards in the industry and regulate it. With more FDI and FII

investments in the country, risk and compliance functions have become even

more critical and complex thereby, enforcing companies to review their

current and future risk management systems and compliance blue-prints.

Various consultancy bodies such as PRMIA are making continuous efforts to

influence the regulatory directions of the financial institutions by conducting

global surveys and seminars with the top brass of various financial

institutions.

Thus, Risk management has become a requirement rather than a need for

the financial institutions in order to influence the profitability and account for

the various risks associated in the system and minimize them.

CURRENT TRENDS & TECHNIQUES

Today, the finance domain faces broader and deeper regulatory issues viz.

Liquidity risk:

It is defined as “It is the risk that a given security or asset cannot

be traded quickly enough in the market to prevent a loss (or

make the required profit).”3

Liquidity risk can arise from both the asset as well as liabilities side. Some

of the reasons for it can be widening of the bid/ask spread, lengthening of

the holding period for VAR, non favorable economic conditions, credit

defaults, inconsistent cash flows, supply-demand gap, explicit liquidity

3 http://en.wikipedia.org/wiki/Liquidity_risk

7 | P a g e

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 8/22

requirement, etc. This was one of the major reasons for the recession of

2008 in USA. The liquidity crunch in the financial system was a result of

the lack of tradability of the assets in-hand due to drop in asset prices.

Capital Buffers:It is a risk management technique used by banks to protect and hedge

itself against the future losses, maintain growth and reduce the volatility

in the marketplace against the rising interest rates.

Banks maintain certain capital adequacy with itself to hedge against the

risk exposure of interest rates, liquidity crunch, counter-cycles, etc.

Banks are being encouraged as per the BASEL II norms to build up capitalbuffers in good times to be drawn upon in periods of stress to reduce pro-

cyclicality in the system. In times of distress, banks can use upon its

capital buffers to protect itself from the stressful situations and come out

unharmed.

Supply chain risk

The entire financial system is based upon the demand-supply dynamics. It

refers to the availability of funds in times of distress. It is co-related to the

liquidity in the system. If the liquidity in the system is less, then it will lead

to non-availability to funds which in turn influences the interest rates in

the system. Thus, banks run the risk of non availability of funds and its

supply. In India, banks borrow funds from RBI at Repo rate and parks

excess funds with RBI at a Reverse-Repo rate. Thus, RBI maintains the

supply of funds to banks and maintains liquidity thru Open market

operations and printing of currency.

Information risk

Banks generate huge volumes of data from its day-to-day operations. Thus, the

MIS systems have to create, distribute, store, copy, transform, encrypt, and

decrypt the data it gets. Thus, banks stand the risk of non availability of data and

8 | P a g e

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 9/22

distribution of the available information to every source and corner if its network.

It’s important to design the MIS of the banks in a way to avail clarity, precision

and accuracy of the data it has stored for usage.

Environmental complianceWith rapid advancement in technology and introduction of cleaner

greener technology, environmental compliance is becoming a

requirement and banks stand a risk if it doesn’t comply with the

environmental standards enforced.

Technology

In addition to how technology has completely changed the banking

industry, technology also impacts the way the risk and compliance in the

system is managed. For example, with the usage of social media tools

such as blogs, wikis and face book the legal and reputation risk needs to

be factored in.

Some of the other factor also contributing to the risk management is the

HUMAN element . Risk and Compliance management is becoming more

people centric. The quant models are going to continue as a vital part of the

risk analysis but the balance needs to be maintained. The focus should be

shifted to more employee ownership in the risk management an d make it

everyone’s responsibility to manage and maintain the risk in the system.

Given the enhanced regulatory requirement, risk and compliance roles are

under immense pressure to perform and deliver as its impacts the

company’s performance and corporate governance.

FUTURE OUTLOOK: TRENDS & TECHNIQUES

Risk management activities will be the front runner in the operation activities

undertaken by banks. It shall become more pronounced in the future with the

added impetus of de-regularization, liberalization and global integration of

9 | P a g e

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 10/22

the financial markets. This will add up to the depth and dimension of the

banking industry and its risks. All risks associated are co-related to each

other and act as a domino effect in case the exposure on one of the risks

increases rapidly. Thus, the success of the banks is dependent on the

effective, efficient, pro-active and integrated manner by which they manage

their risks.

With the implementation of a standardized approach, the collection of data in

the future for the calculation of various risk & compliance parameters such

as Exposure at default (EAD), Probability of default (PD) and Loss given

default (LGD). The banks will be required to hold such data for a minimum

period of 5years to avoid the risk of the spread of the data.

Based on the growth trends as projected by the Indian government and its

expected GDP rate to be in double digits, the usage of Internet is going to be

the key focus area with special emphasis on Management Information

Systems (MIS) and more recent developments in the form of Enterprise Risk

Management systems (ERM). ERM will continue to be the top focus area in

the future with integration on a global platform as the key impact indicator of

the success of the system.

With the dawn of the internet era, the savings in the field of risk &

compliance management in terms of time and effort will become invaluable

with the focus on productivity and efficiency. The consistency in these areas

is being reflected thru enhanced work pressures and real time turnaround

with the best possible results with minimum time & effort.

Liquidity risk and capital adequacy are going to be the main focus areas in

terms of future outlook of the financial services industry. Based on a survey

undertaken by Professional Risk Manager’s International Association (PRMIA)

in august 2010, the top five risk management trends which will be important

to the future industry strategy are:

10 | P a g e

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 11/22

1. Liquidity Risk buffers

2. Enterprise Risk Management

3. Stress Testing

4. Managing Systematic risk

5. Banking book credit risk model4

The above bar chart on a scale of 0-4 shows the result of the survey

undertaken by PRMIA to identify the top trends in risk management

important for future for financial services firm indicating the various trends

important for the future outlook of banks.

Some of the trends important for non-financial services also included the

following viz.

1. Cash Flow at Risk (CFAR)

2. Productivity & efficiency in risk5

4 Future of Risk Management & Compliance: Global Trends & Perspectives: Report by PRMIA-August 20105Future of Risk Management & Compliance: Global Trends & Perspectives: Report by PRMIA-August 2010

11 | P a g e

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 12/22

As stated above, the Human element in the risk & compliance management

shall play a very important role in the success of the Risk management

systems in the future. With the rapid advancements in systematic usage of

the risk management tools, organizations should start focusing more onemployee buy-ins to enable risk controls at all levels thereby enabling risk

management at even the grass root levels. This will promote the feeling that

“Risk is really the job of everyone.” The future workplace is a vision where

employee will pro-actively be able to spend more time on strategic &

effective risk mitigation activities rather than undertake time consuming

activities such as data aggregation & analysis.

Thus, the workplace & controls need to become more people centric through

cross company collaborations becoming a strong pillar for the success of the

risk & compliance management systems in the future.

Some of the perspectives into the risk management systems are of the

opinion that:

1.The analysis to be undertaken will become more visual & systematic

2.Collaboration will be the key

3.Open access to all employees to business analytics & insights

4.Use of web enabled documents & spread sheets.

12 | P a g e

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 13/22

The above chart shows the respondents views on the important changes that

will be made in the future risk & compliance management systems.

The GenX are going to be the drivers of the future risk managementsystems. The special skill sets that will be required to effectively undertake

the role will be deeper business understanding & knowledge, effective

communication skills & grip over the quantitative methods used in risk

management. Also, the increasing popularity of the DIY (Do-It-Yourself)

analytical tools, micro blogging sites, and social media platforms is a sign of

a generational shift towards more tech savvy methods.

These special skill sets & tools will enhance the workflow efficiency &

effectiveness through unlocking of the business data and automating the

workflows & processes.

The graph below shows the role of tools in risk & compliance management

functions:

13 | P a g e

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 14/22

With the onset of the risk management tools & deeper business

understanding, the managers of the future are expected to focus more on

strategic decisions than data collection activities as undertaken by their past

subordinates. The risk management professionals have to define the

dynamic balance between strategic decision making and tactical work such

as data collection & assimilation. Based on the survey undertaken by PRMIA,

62% risk managers spend their time on undertaking data aggregation

activities with a desire to focus their efforts towards more proactive &

strategic risk mitigation activities.

Certainly, depending upon the maturity of the system the balance between

the two can be improved & made better.

With organizations predominantly facing budget constraints and viewed

against the backdrop of Doing more with Less, firms are constrained in

their risk management initiatives. On an average, the organizations expect

their baseline budget needs at roughly about 6-8% of the operational costs

to be allocated to risk management activities. These funds apart from the

core functionality are invested in future projects to improve the efficiency,

productivity and self servicing needs of the organization.

With firms increasingly focusing on improving the employee buy-in at all

levels, technology is the key pillar to the success of the risk managers. The

14 | P a g e

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 15/22

right selection of the technology enables the risk managers to make

effective, efficient and well informed decisions. Thus, it is increasingly

important for the risk managers to undertake a thorough due diligence of the

technology to be implemented and decide the future direction of their risk

management activities and technology synchronization into the system.

Some of the key factors deemed important for the technology to be

implemented are:

1.Improve the productivity of the employees through savings in terms of

time, effort and money.

2.Maximize the investment capabilities – existing & future

3.Empowering the employees to embed solutions into their daily

activities

4.Ability to self service their needs in terms of right information, right

time in the right format

5.Improving the efficiency of the workflows & processes through

integrated offerings

15 | P a g e

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 16/22

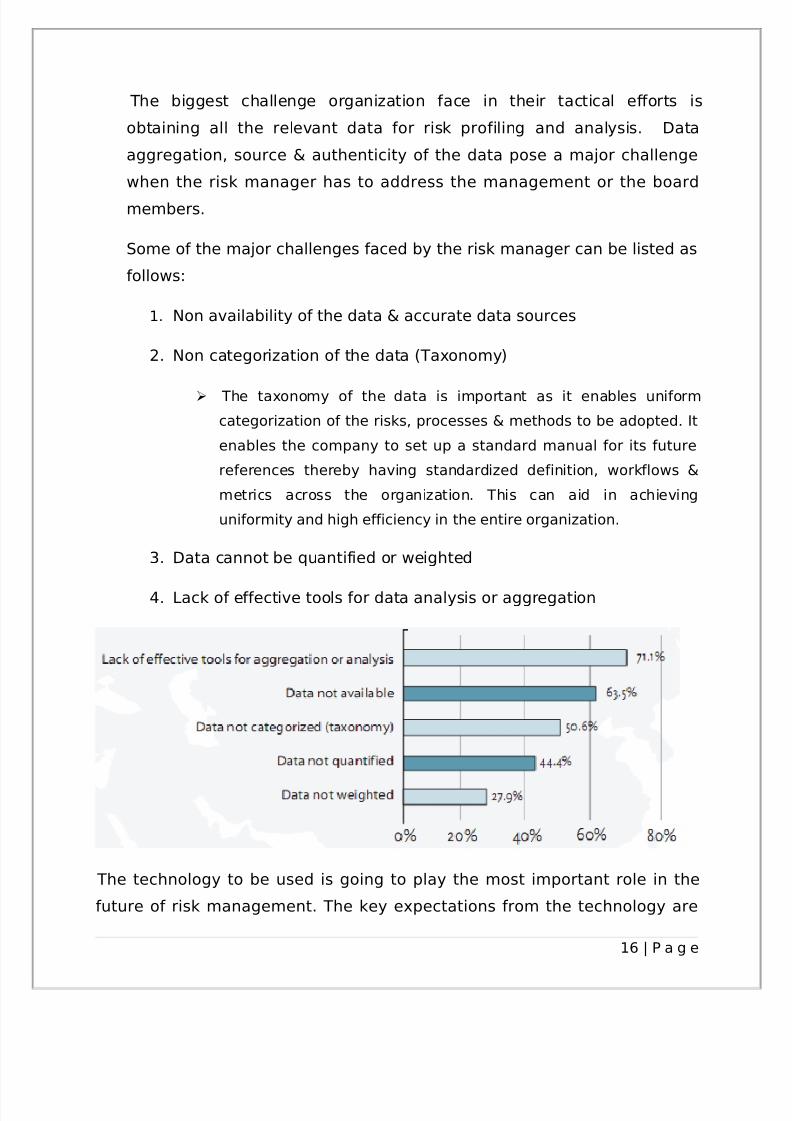

The biggest challenge organization face in their tactical efforts is

obtaining all the relevant data for risk profiling and analysis. Data

aggregation, source & authenticity of the data pose a major challenge

when the risk manager has to address the management or the board

members.

Some of the major challenges faced by the risk manager can be listed as

follows:

1. Non availability of the data & accurate data sources

2. Non categorization of the data (Taxonomy)

The taxonomy of the data is important as it enables uniform

categorization of the risks, processes & methods to be adopted. It

enables the company to set up a standard manual for its future

references thereby having standardized definition, workflows &

metrics across the organization. This can aid in achieving

uniformity and high efficiency in the entire organization.

3. Data cannot be quantified or weighted

4. Lack of effective tools for data analysis or aggregation

The technology to be used is going to play the most important role in the

future of risk management. The key expectations from the technology are

16 | P a g e

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 17/22

flexibility, self service, ease of use and wide spread integration with the

current systems, along with predictive analysis, delivery of high performance

and decision support systems (DSS).

The ultimate objective of improved efficiency & productivity at the workplacewill not be farfetched if the technology enablers are integrated into the

system effectively.

Currently, almost 50% of the risk managers are of the opinion that the

current levels of risk systems are integrated with each other on a common

platform. The advent of technology in the future will help improve the

systems integration on a bigger platform on a mass level.

The technology to be installed is going to be the backbone of the system.

Risk managers opine it to play more discrete roles such as Decision support

systems & artificial intelligence rather than more tactical roles such as data

aggregation. It is deemed to be the Strategic decision enabler rather than a

data analyzer.

Thus, the future technology integration will be a holistic approach for

organizations to invest in for ERM and compliance. The technology will bedeployed in the future with a view to improve the following:

1. Connectivity with the existing systems

2. Lower cost of deployment & maintenance

3. Ease of use & flexibility6

6 Future of Risk Management & Compliance: Global Trends & Perspectives: Report by PRMIA-August 2010

17 | P a g e

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 18/22

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 19/22

These are the main game changers for risk management system in the

future which will define the future outlook and enable it to effectively &

efficiently monitor, control & regulate the financial services domain.

Shown below are the top clusters of the technology clusters that will enablethe rise of Risk management systems in the future to the fore.

19 | P a g e

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 20/22

20 | P a g e

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 21/22

CONCLUSION

The rise of the third world nations such as India, China, Brazil, and Indonesia

is a result of the rapidly changing global economic frontier. With the increase

in the business endeavors and investment activities, risk management in the

financial services sector will come to the fore.

With the new WTO regulations and opening up of the trade agreements

between the developing nations & the western economy, financial

organizations are now in a position to market & trade their products &

services on a global platform. The world is constantly becoming smaller thru

rapid advancements in tele-communication technology & information

management systems. Internet now plays a key role in defining the successof any business endeavor. Internet has in true sense become the “GAME

CHANGER” for the financial services industry. With India on the Investment

radar, risk management has become of great importance to the Banking

sector with the business risks increasing due to several micro & macro

economic factors such as Liquidity, Capital Adequacy, Per capita income

levels, Demand-supply dynamics, information risk, Technology obsolescence

and many others. The entire system is in a state of revamp to be at par with

its global counterparts.

The Indian banking unit under the guidance of Reserve Bank of India (RBI)

has already started the process of re-organization of the system thru

implementation of BASEL II & BASEL III accord and also encouraging

organizations to follow the IFRS guidelines while preparing the financial

statements. This will help improve the uniformity in the system and define a

standardized process & workflow in the system. This is important for thesuccess of the financial sector as a whole.

The current state of systems is in distress and disarray, and under severe

threat of operational and financial risks. Also there is lack of clarity and

integration in the system which is hindering the progress of the system.

21 | P a g e

8/6/2019 Research Paper-Harshil Shah 317

http://slidepdf.com/reader/full/research-paper-harshil-shah-317 22/22

The future of the system is with the added clarity & more definite purpose to

improve the risk management & compliance.

22 | P a g e