reputation in the western world - saïd business … · reputation in the western world stories...

TRANSCRIPT

Reputation in the Western World

Stories about the Blood and Soil

of Business

These slides are from from published and unpublished works. All rights are reserved (© Ronald S. Burt 2011). Materials can be

downloaded from http://faculty.chicagobooth.edu/ronald.burt/research.

15-‐17/09/2011

15/04/2011

Reputation in the Western World The Data Conceptual Foundations Distinguishing Regional Clusters Digging into Significant Bridges Digging into Significant Closure

Appendix Materials

The Data

This is a proposal to build a research platform on a large scale that would encourage analysts to study people, organizations, communities and markets embedded in one another. The platform creates an intimate link between case studies, comparative analysis, and quantitative research to allow more general conclusions from better grounded analyses. It is, in short, a proposal to bring into state-of-the-art research more of the blood and soil of business. This is not a project for an individual or local team. It is an exercise of leadership fittingly performed in collaboration through a reputable Centre.

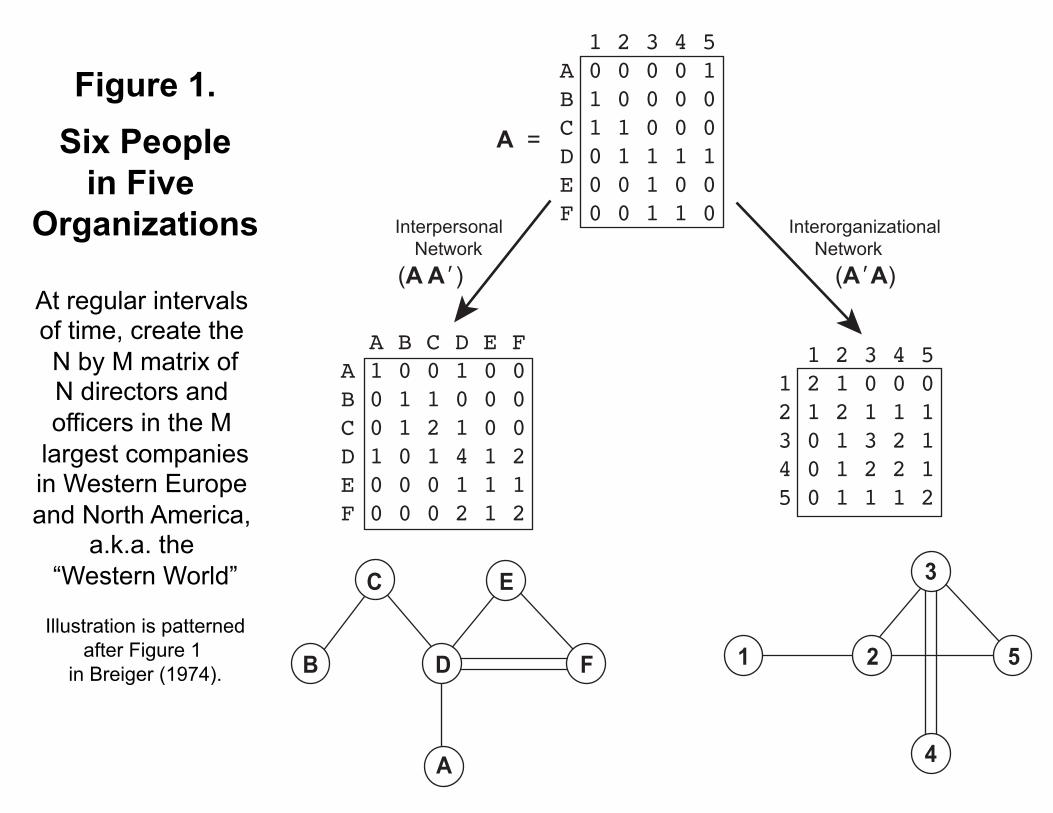

Figure 1. Six People

in Five Organizations

At regular intervals of time, create the N by M matrix of N directors and officers in the M

largest companies in Western Europe and North America,

a.k.a. the “Western World”

Illustration is patterned

after Figure 1 in Breiger (1974).

1 2 3 4 5A 0 0 0 0 1B 1 0 0 0 0C 1 1 0 0 0D 0 1 1 1 1E 0 0 1 0 0F 0 0 1 1 0

1 2 3 4 51 2 1 0 0 02 1 2 1 1 13 0 1 3 2 14 0 1 2 2 15 0 1 1 1 2

A =

A B C D E FA 1 0 0 1 0 0B 0 1 1 0 0 0C 0 1 2 1 0 0D 1 0 1 4 1 2E 0 0 0 1 1 1F 0 0 0 2 1 2

InterpersonalNetwork (A A’)

Interorganizational Network (A’A)

A

C E

B D F 1 2 5

3

4

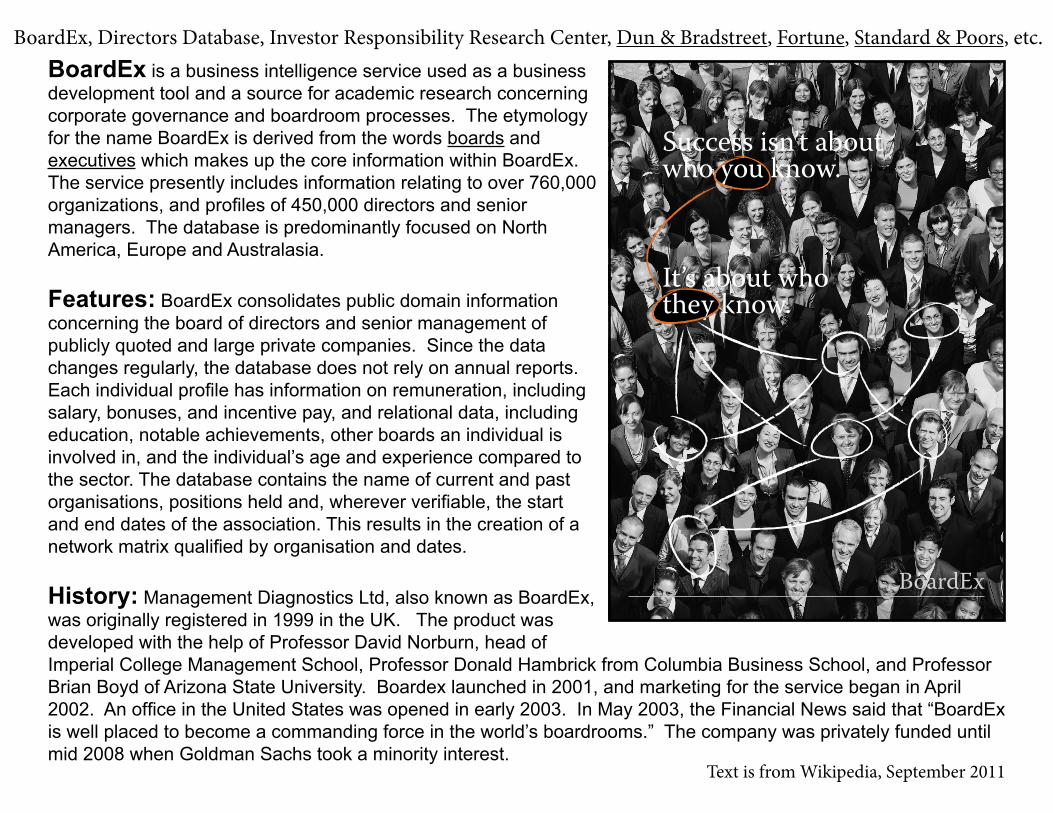

BoardEx is a business intelligence service used as a business development tool and a source for academic research concerning corporate governance and boardroom processes. The etymology for the name BoardEx is derived from the words boards and executives which makes up the core information within BoardEx. The service presently includes information relating to over 760,000 organizations, and profiles of 450,000 directors and senior managers. The database is predominantly focused on North America, Europe and Australasia.

Features: BoardEx consolidates public domain information concerning the board of directors and senior management of publicly quoted and large private companies. Since the data changes regularly, the database does not rely on annual reports. Each individual profile has information on remuneration, including salary, bonuses, and incentive pay, and relational data, including education, notable achievements, other boards an individual is involved in, and the individual’s age and experience compared to the sector. The database contains the name of current and past organisations, positions held and, wherever verifiable, the start and end dates of the association. This results in the creation of a network matrix qualified by organisation and dates.

History: Management Diagnostics Ltd, also known as BoardEx, was originally registered in 1999 in the UK. The product was developed with the help of Professor David Norburn, head of Imperial College Management School, Professor Donald Hambrick from Columbia Business School, and Professor Brian Boyd of Arizona State University. Boardex launched in 2001, and marketing for the service began in April 2002. An office in the United States was opened in early 2003. In May 2003, the Financial News said that “BoardEx is well placed to become a commanding force in the world’s boardrooms.” The company was privately funded until mid 2008 when Goldman Sachs took a minority interest.

Text is from Wikipedia, September 2011

Success isn’t about who you know.

It’s about who they know.

BoardEx

BoardEx, Directors Database, Investor Responsibility Research Center, Dun & Bradstreet, Fortune, Standard & Poors, etc.

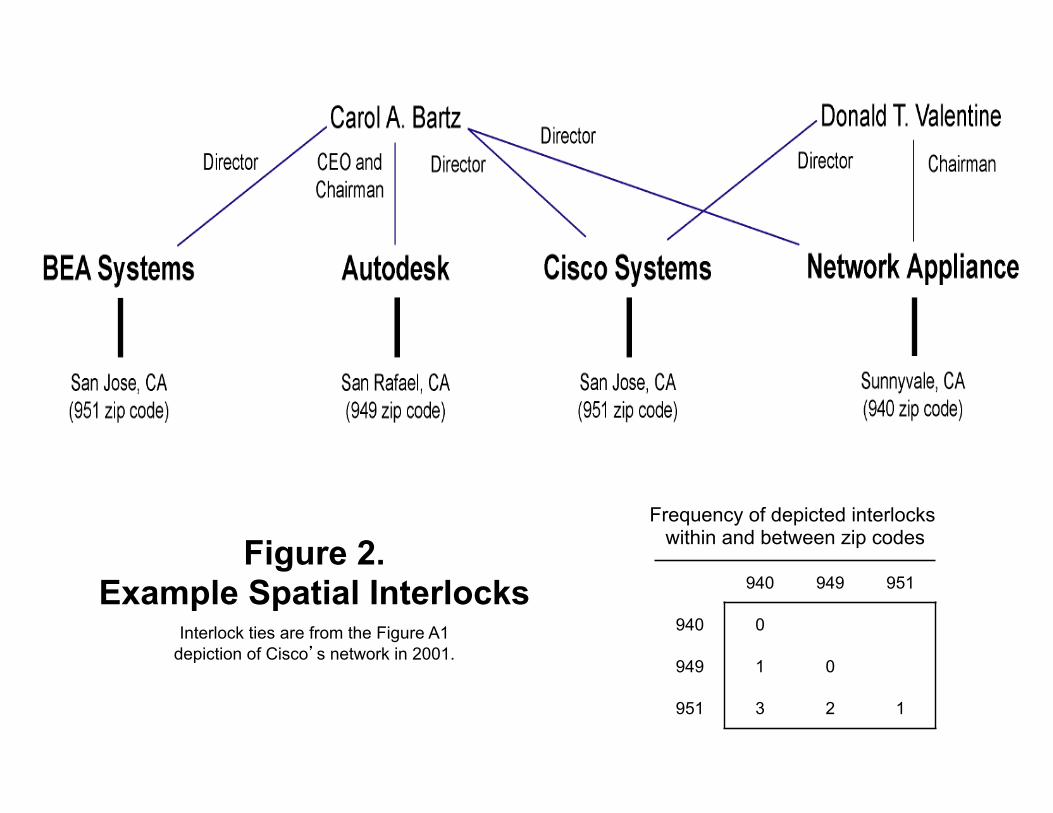

Figure 2. Example Spatial Interlocks

Interlock ties are from the Figure A1 depiction of Cisco’s network in 2001.

940 949 951

940 0

949 1 0

951 3 2 1

Frequency of depicted interlocks within and between zip codes

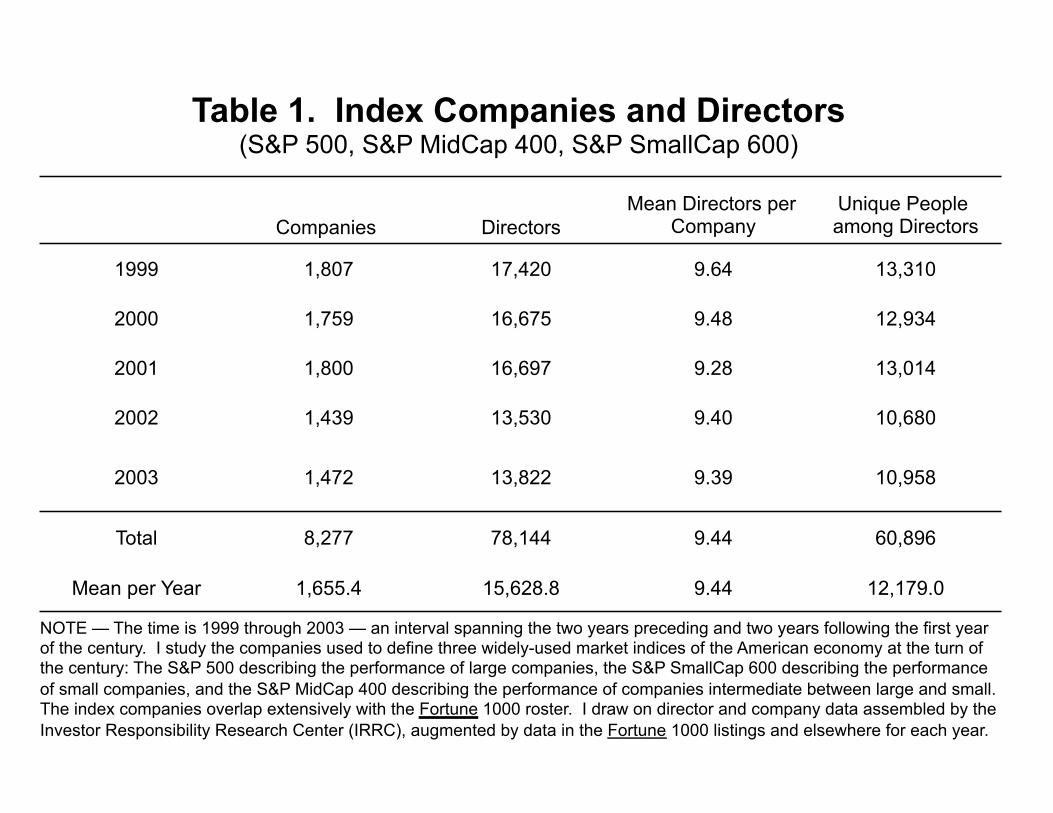

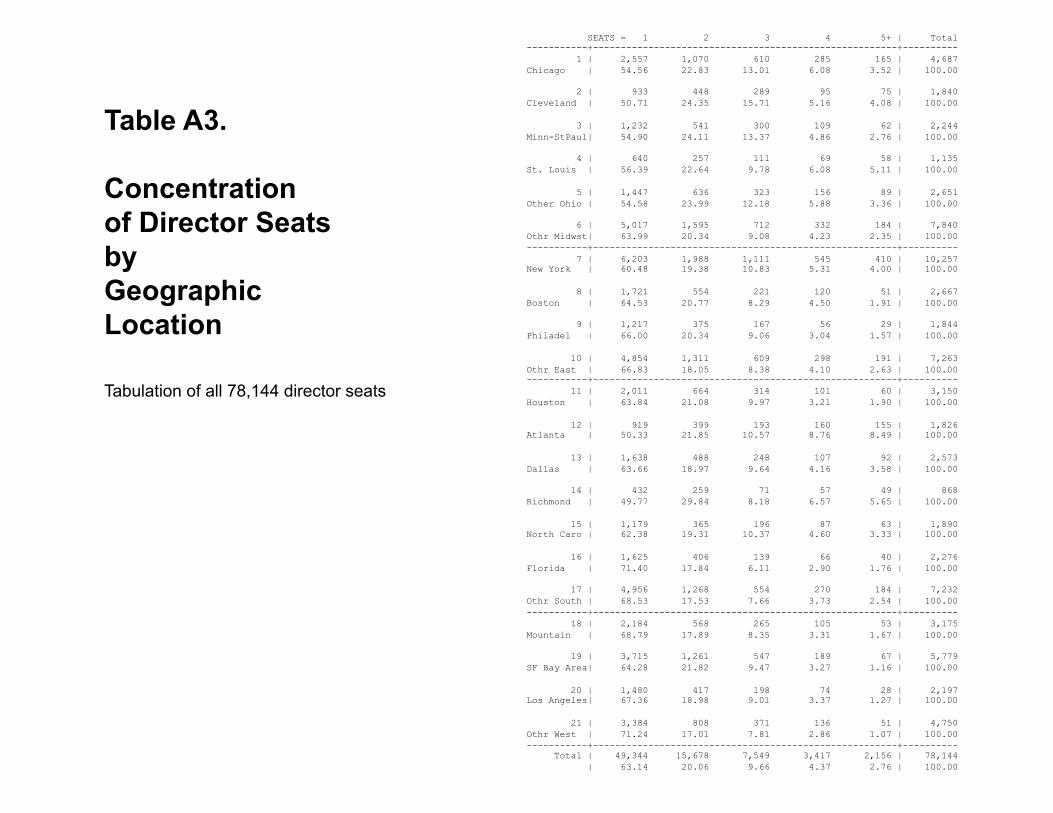

Table 1. Index Companies and Directors (S&P 500, S&P MidCap 400, S&P SmallCap 600)

Companies Directors Mean Directors per

Company Unique People among Directors

1999 1,807 17,420 9.64 13,310

2000 1,759 16,675 9.48 12,934

2001 1,800 16,697 9.28 13,014

2002 1,439 13,530 9.40 10,680

2003 1,472 13,822 9.39 10,958

Total 8,277 78,144 9.44 60,896

Mean per Year 1,655.4 15,628.8 9.44 12,179.0

NOTE — The time is 1999 through 2003 — an interval spanning the two years preceding and two years following the first year of the century. I study the companies used to define three widely-used market indices of the American economy at the turn of the century: The S&P 500 describing the performance of large companies, the S&P SmallCap 600 describing the performance of small companies, and the S&P MidCap 400 describing the performance of companies intermediate between large and small. The index companies overlap extensively with the Fortune 1000 roster. I draw on director and company data assembled by the Investor Responsibility Research Center (IRRC), augmented by data in the Fortune 1000 listings and elsewhere for each year.

15/04/2011

Reputation in the Western World The Data Conceptual Foundations Distinguishing Regional Clusters Digging into Significant Bridges Digging into Significant Closure

Appendix Materials

Conceptual Foundations

Networks Embedded in Networks

Stra

tegi

c Lea

ders

hip

Crea

ting

Valu

e: T

he S

ocial

Cap

ital o

f Bro

kera

ge (p

age 7

)

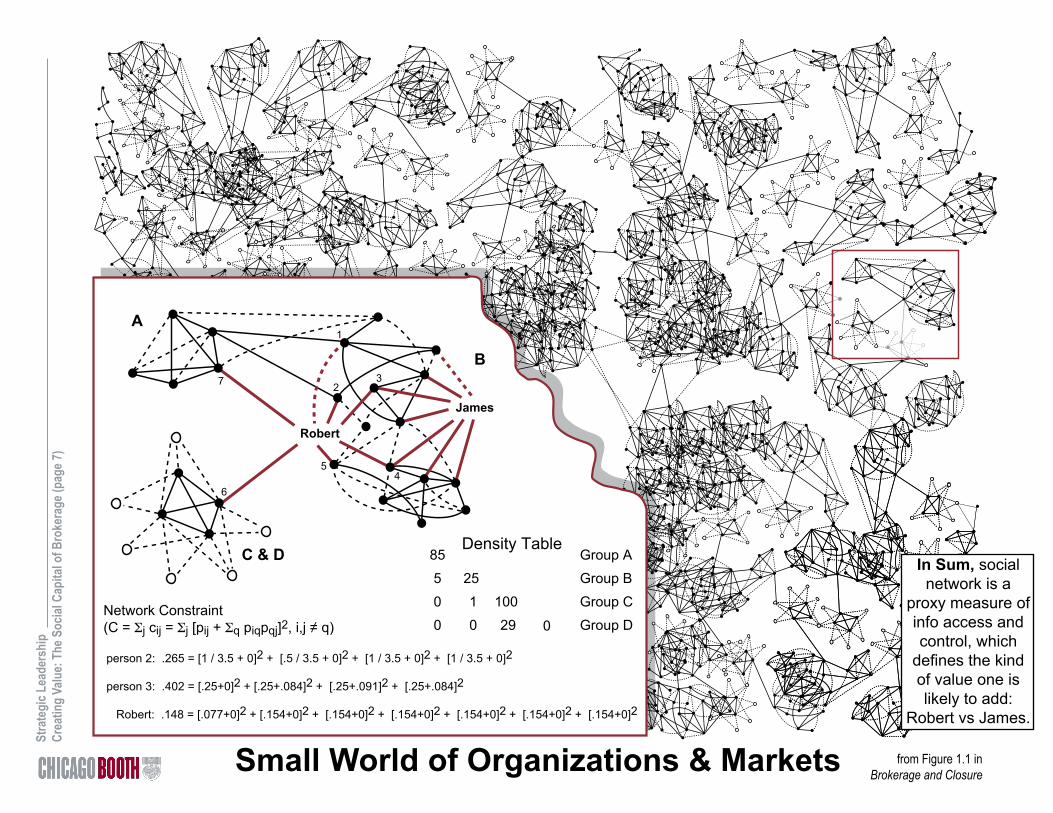

from Figure 1.1 inBrokerage and ClosureSmall World of Organizations & Markets

James

Robert

1

23

54

6

7

A

B

C & D 25

1

0

100

29

Group A

Group B

Group C

Group D

Density Table

0

85

5

0

0Network Constraint(C = Σj cij = Σj [pij + Σq piqpqj]2, i,j ≠ q)

person 2: .265 = [1 / 3.5 + 0]2 + [.5 / 3.5 + 0]2 + [1 / 3.5 + 0]2 + [1 / 3.5 + 0]2

person 3: .402 = [.25+0]2 + [.25+.084]2 + [.25+.091]2 + [.25+.084]2

Robert: .148 = [.077+0]2 + [.154+0]2 + [.154+0]2 + [.154+0]2 + [.154+0]2 + [.154+0]2 + [.154+0]2

In Sum, social network is a

proxy measure of info access and control, which

defines the kind of value one is likely to add:

Robert vs James.

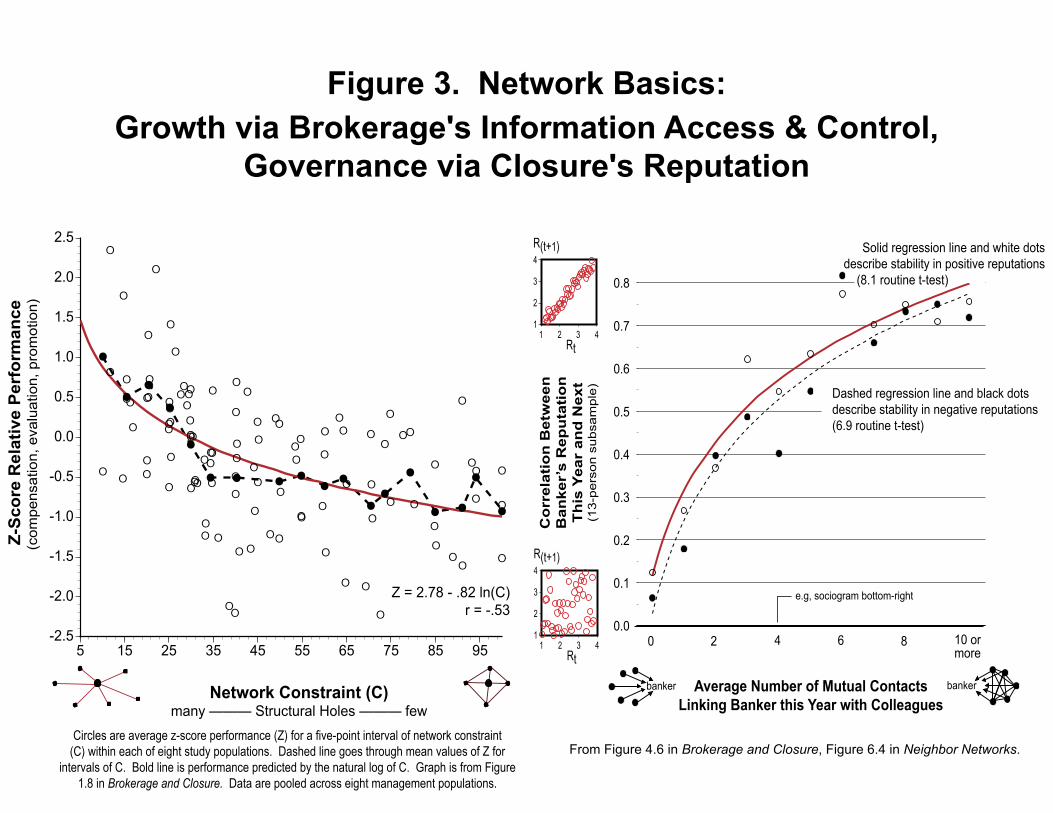

Figure 3. Network Basics:Growth via Brokerage's Information Access & Control,

Governance via Closure's Reputation

E

E

E

E

E

E

E

E

E

E

E

E

E

EEE

E

EE

E

EE

E

E

E

E

EE

EE

E

E

EE

E

E

EEE

E

EE

EE

E

E

E

E

EE

E

E

E

E

E

E

E

E

E

E

E

E

E

E

E

E

E

E

E

EE

E

EEE

E

E

E

EE

E

E

E

E

E

E

E

E

E

E

EE

E

E

E

EE

E

E

E

E

E

E

E

E

J

JJ

J

J

J J JJJJ

JJ

J

J J

J

J

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

5 15 25 35 45 55 65 75 85 95

Z = 2.78 - .82 ln(C)r = -.53

Network Constraint (C)many ——— Structural Holes ——— few

Z-S

core

Rel

ativ

e P

erfo

rman

ce(c

ompe

nsat

ion,

eva

luat

ion,

pro

mot

ion)

Circles are average z-score performance (Z) for a five-point interval of network constraint (C) within each of eight study populations. Dashed line goes through mean values of Z for

intervals of C. Bold line is performance predicted by the natural log of C. Graph is from Figure 1.8 in Brokerage and Closure. Data are pooled across eight management populations.

From Figure 4.6 in Brokerage and Closure, Figure 6.4 in Neighbor Networks.

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0 2 4 6 8 10 ormore

Co

rrel

atio

n B

etw

een

Ban

ker’

s R

epu

tati

on

Th

is Y

ear

and

Nex

t(1

3-pe

rson

sub

sam

ple)

1

2

3

4

1 2 3 4Rt

R(t+1)

1

2

3

4

1 2 3 4Rt

R(t+1)

Average Number of Mutual ContactsLinking Banker this Year with Colleagues

banker banker

e.g, sociogram bottom-right

Solid regression line and white dotsdescribe stability in positive reputations

(8.1 routine t-test)

Dashed regression line and black dotsdescribe stability in negative reputations(6.9 routine t-test)

Stra

tegi

c Lea

ders

hip

Deliv

erin

g Va

lue:

The

Soc

ial C

apita

l of C

losu

re (p

age 2

)

from Figure 3.1 in Brokerage and Closure (for discussion, see pages 105-111)

Robert Jessica Robert Jessica Robert Jessica

Situation ARobert New Acquaintance

(no embedding)

Situation BRobert Long-Time Colleague

("relational" embedding)

Situation CRobert Co-Member Group

("structural" embedding)

More connections allow more rapid communication, so poor behavior can be more readily detected and punished. Bureaucratic authority was the traditional engine for coordination in organizations (budget, head count). The new engine is reputation (e.g., eBay). In flattened-down organizations, leader roles are often ambiguous, so people need help knowing who to trust, and the boss needs help supervising her direct reports. Multi-point evaluation systems, often discussed as 360° evaluation systems, gather evaluative data from the people who work with an employee. These are "reputational" systems in that evaluations are the same data that define an employee's reputation in the company.

Trust is essential to exercising social capital. Organizations depend on able employees using social capital to search out and implement ways to add value, but too much puts the enterprise at risk. Company chains of command broken in service of company interests can just as easily be broken in service of personal interests, or in service of well-intentioned but strategy-eroding interests. Zaffaroni in Affymax, Clendenin at Xerox, and Beers in WPP illustrate the importance of reputation for overcoming the suspicions with which brokers are viewed. In essence, reputation is the governance mechanism in social networks.

Closure Creates a Reputation Cost for Misbehavior,Which Facilitates Trust and Collaboration

Figure 4. Brokerage and Closure Are Two Sides of the Same Coin, Operating by Mechanisms Local and Interdependent

Brokerage and closure operate by local, personal mechanisms — skill in recombinant knowledge and sharing stories — and as we get closer to individual people, we find the people with brokerage advantages in access

to structural holes are the same people who have closure advantages in status and reputation.

A Global Organizationof Bankers

A BalkanizedAsia-Pacific

Product-LaunchOrganization

0.0

1.0

2.0

3.0

4.0

5.00.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5

Net

owrk

Cen

tral

ity/P

ower

/Sta

tus

(eig

enve

ctor

sco

re /

mea

n sc

ore)

Network Brokerage (-(ln[C]))

r = .94

Circles in US, diamonds elsewhere

0

1

2

3

4

5

6

7

8

90.0 0.5 1.0 1.5 2.0 2.5

Net

wor

k C

entr

ality

/Pow

er/S

tatu

s(e

igen

vect

or s

core

/ m

ean

scor

e)

Network Brokerage (-(ln[C]))

r = .86

Sales Regional OpsProduct SupportAdministration

Regions indexedby color, functions by shape

Banker organization is described in Chapter 4 of Neighbor Networks, product-launch in Chapter 3.

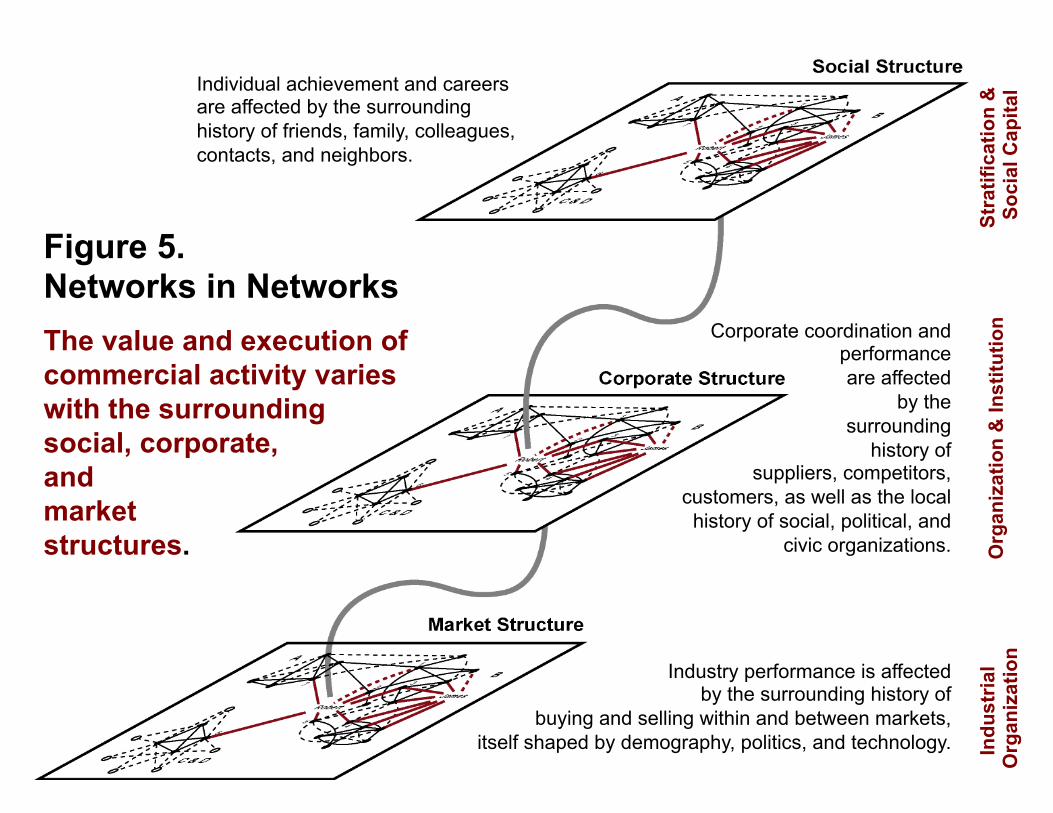

Figure 5. Networks in Networks The value and execution of commercial activity varies with the surrounding social, corporate, and market structures.

Individual achievement and careers are affected by the surrounding history of friends, family, colleagues, contacts, and neighbors.

Corporate coordination and performance are affected

by the surrounding

history of suppliers, competitors,

customers, as well as the local history of social, political, and

civic organizations.

Industry performance is affected by the surrounding history of

buying and selling within and between markets, itself shaped by demography, politics, and technology. In

dust

rial

Org

aniz

atio

n O

rgan

izat

ion

& In

stitu

tion

Stra

tific

atio

n &

So

cial

Cap

ital

15/04/2011

Distinguishing Regional Clusters

Reputation in the Western World The Data Conceptual Foundations Distinguishing Regional Clusters Digging into Significant Bridges Digging into Significant Closure

Appendix Materials

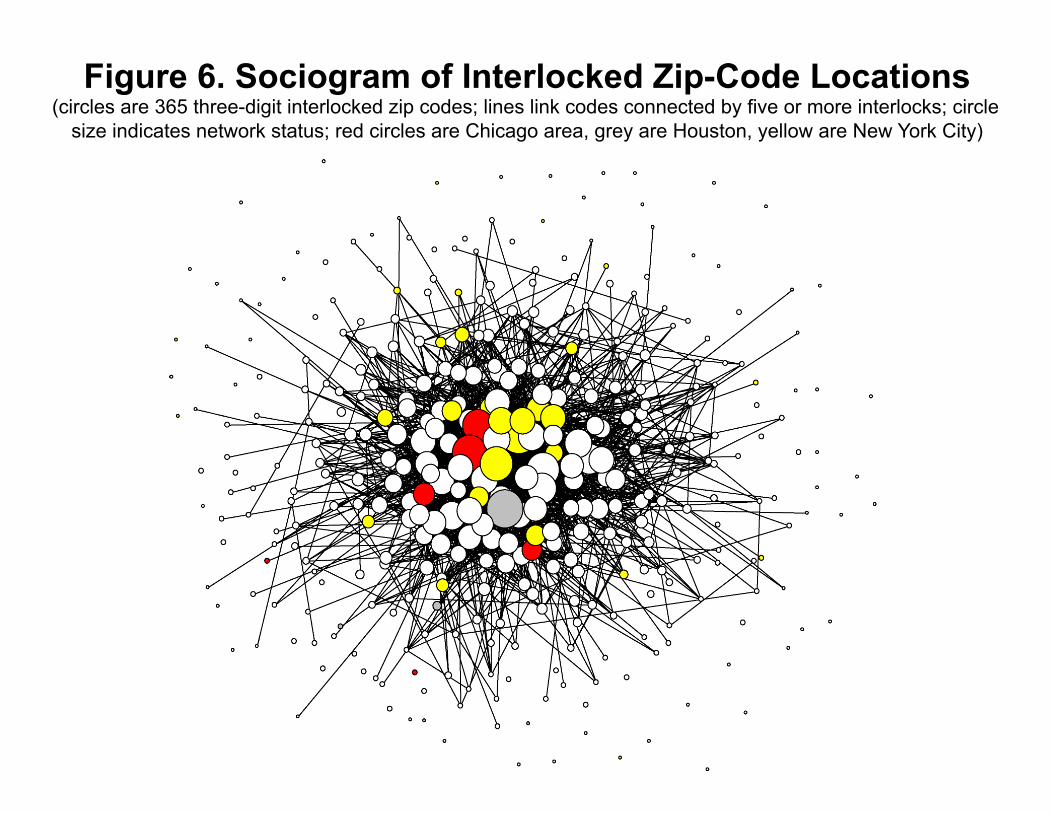

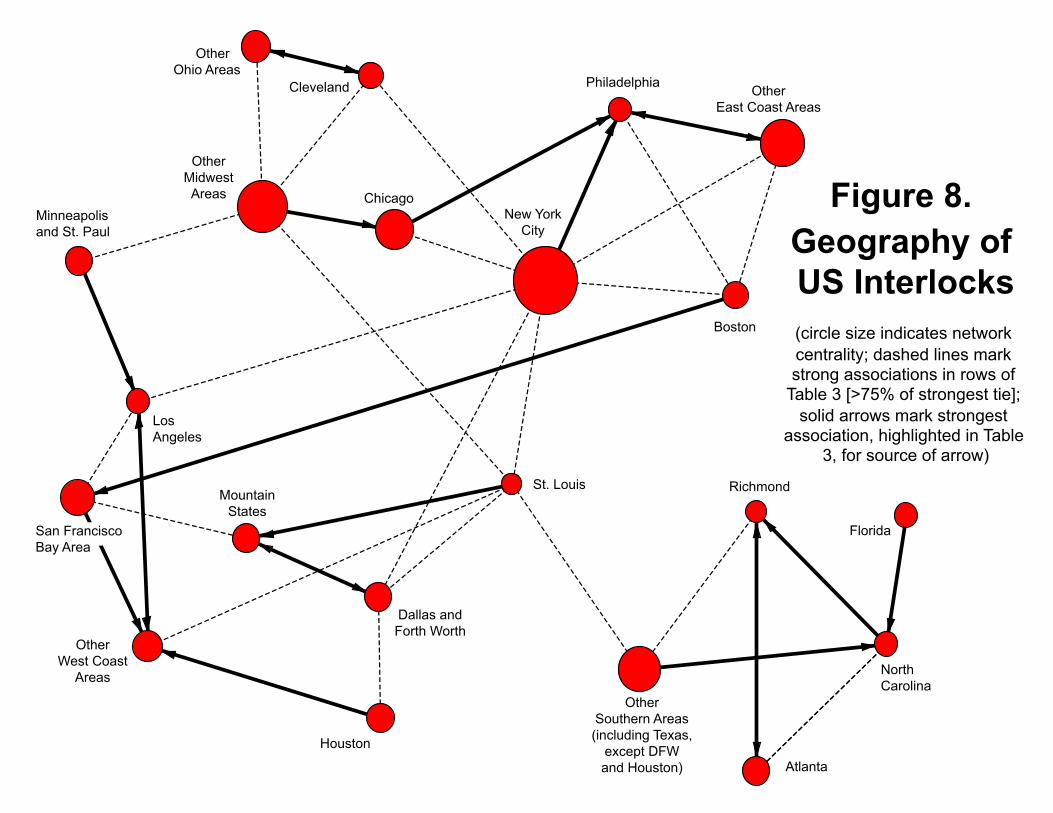

Figure 6. Sociogram of Interlocked Zip-Code Locations (circles are 365 three-digit interlocked zip codes; lines link codes connected by five or more interlocks; circle

size indicates network status; red circles are Chicago area, grey are Houston, yellow are New York City)

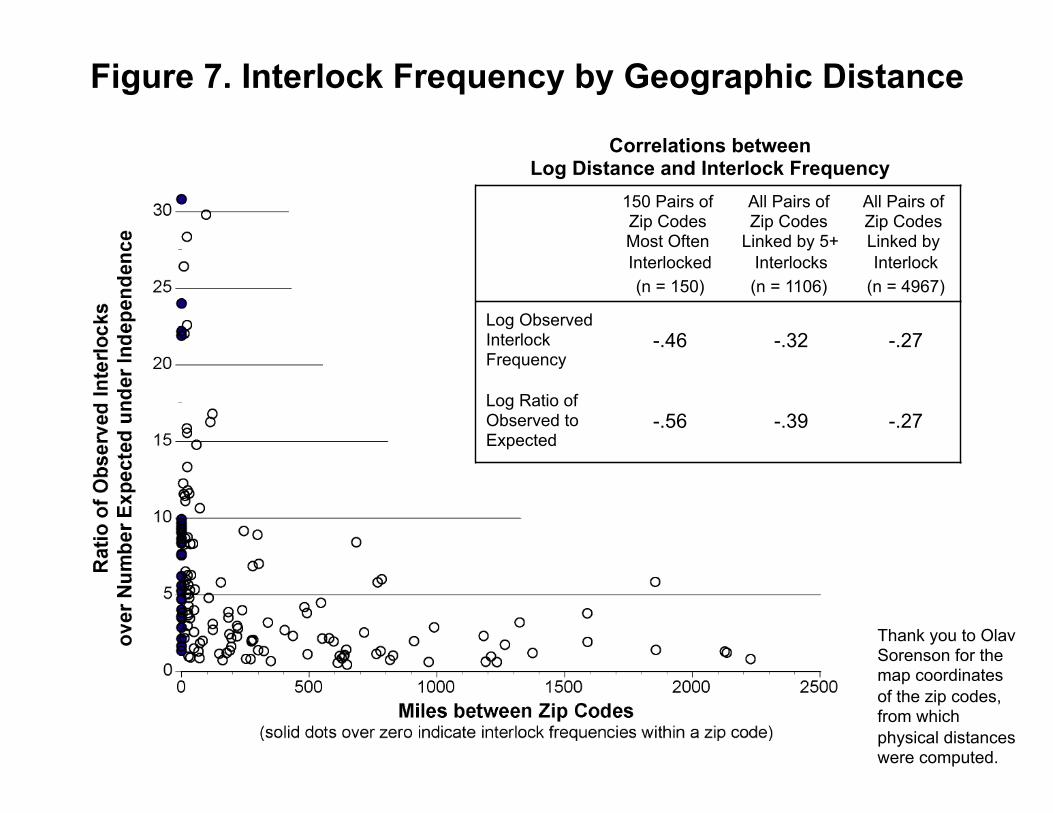

Figure 7. Interlock Frequency by Geographic Distance

Correlations between Log Distance and Interlock Frequency

150 Pairs of Zip Codes Most Often Interlocked (n = 150)

All Pairs of Zip Codes

Linked by 5+ Interlocks (n = 1106)

All Pairs of Zip Codes Linked by Interlock

(n = 4967)

Log Observed Interlock Frequency

-.46 -.32 -.27

Log Ratio of Observed to Expected

-.56 -.39 -.27

Thank you to Olav Sorenson for the map coordinates of the zip codes, from which physical distances were computed.

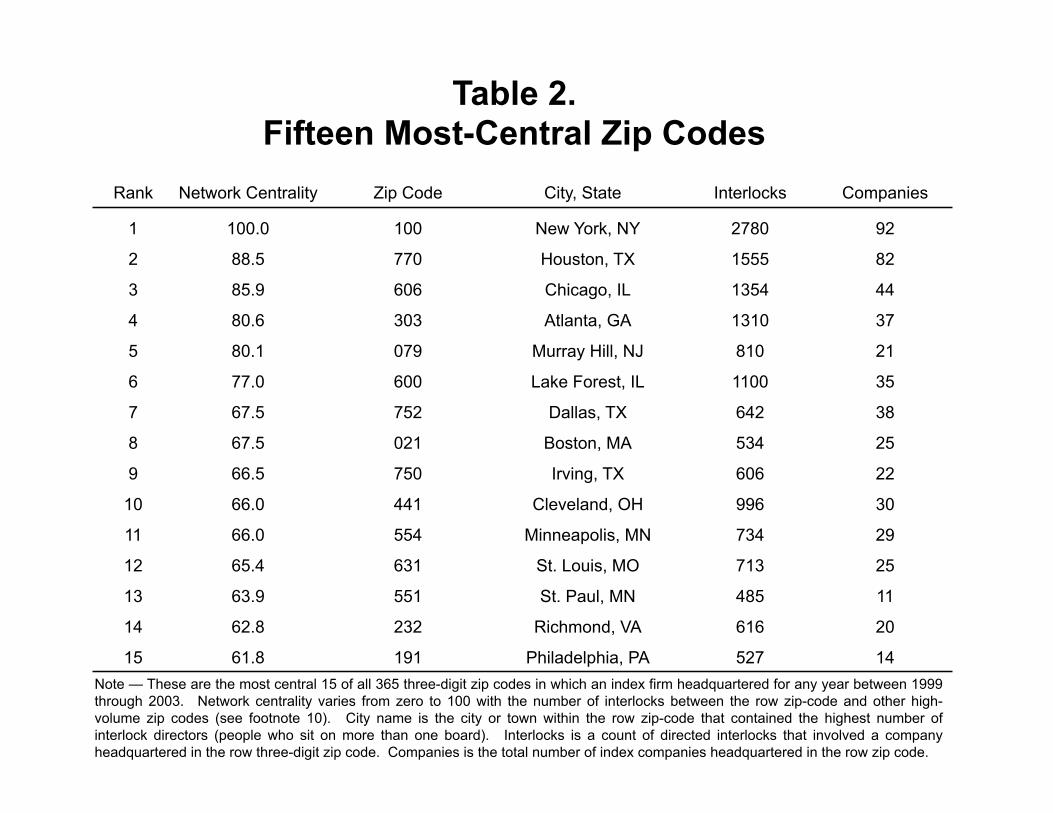

Table 2. Fifteen Most-Central Zip Codes

Rank Network Centrality Zip Code City, State Interlocks Companies

1 100.0 100 New York, NY 2780 92

2 88.5 770 Houston, TX 1555 82

3 85.9 606 Chicago, IL 1354 44

4 80.6 303 Atlanta, GA 1310 37

5 80.1 079 Murray Hill, NJ 810 21

6 77.0 600 Lake Forest, IL 1100 35

7 67.5 752 Dallas, TX 642 38

8 67.5 021 Boston, MA 534 25

9 66.5 750 Irving, TX 606 22

10 66.0 441 Cleveland, OH 996 30

11 66.0 554 Minneapolis, MN 734 29

12 65.4 631 St. Louis, MO 713 25

13 63.9 551 St. Paul, MN 485 11

14 62.8 232 Richmond, VA 616 20

15 61.8 191 Philadelphia, PA 527 14 Note — These are the most central 15 of all 365 three-digit zip codes in which an index firm headquartered for any year between 1999 through 2003. Network centrality varies from zero to 100 with the number of interlocks between the row zip-code and other high-volume zip codes (see footnote 10). City name is the city or town within the row zip-code that contained the highest number of interlock directors (people who sit on more than one board). Interlocks is a count of directed interlocks that involved a company headquartered in the row three-digit zip code. Companies is the total number of index companies headquartered in the row zip code.

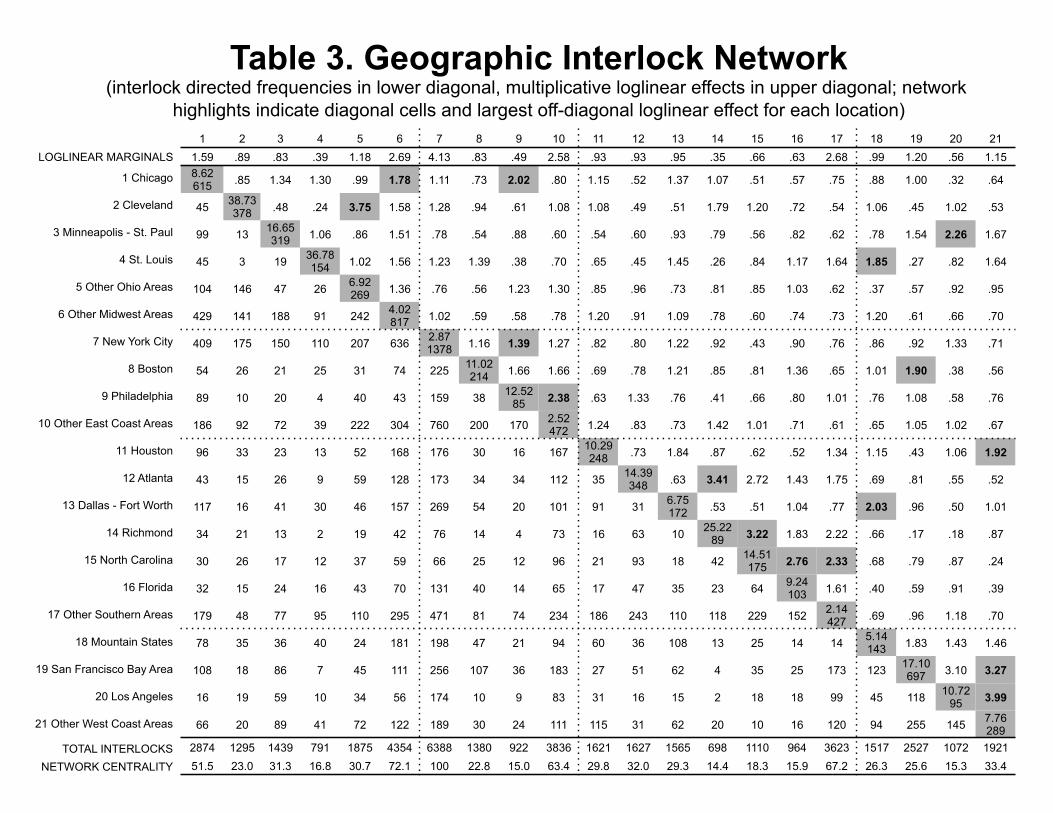

Table 3. Geographic Interlock Network (interlock directed frequencies in lower diagonal, multiplicative loglinear effects in upper diagonal; network

highlights indicate diagonal cells and largest off-diagonal loglinear effect for each location) 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21

1.59 .89 .83 .39 1.18 2.69 4.13 .83 .49 2.58 .93 .93 .95 .35 .66 .63 2.68 .99 1.20 .56 1.15 8.62 615 .85 1.34 1.30 .99 1.78 1.11 .73 2.02 .80 1.15 .52 1.37 1.07 .51 .57 .75 .88 1.00 .32 .64

45 38.73 378 .48 .24 3.75 1.58 1.28 .94 .61 1.08 1.08 .49 .51 1.79 1.20 .72 .54 1.06 .45 1.02 .53

99 13 16.65 319 1.06 .86 1.51 .78 .54 .88 .60 .54 .60 .93 .79 .56 .82 .62 .78 1.54 2.26 1.67

45 3 19 36.78 154 1.02 1.56 1.23 1.39 .38 .70 .65 .45 1.45 .26 .84 1.17 1.64 1.85 .27 .82 1.64

104 146 47 26 6.92 269 1.36 .76 .56 1.23 1.30 .85 .96 .73 .81 .85 1.03 .62 .37 .57 .92 .95

429 141 188 91 242 4.02 817 1.02 .59 .58 .78 1.20 .91 1.09 .78 .60 .74 .73 1.20 .61 .66 .70

409 175 150 110 207 636 2.87 1378 1.16 1.39 1.27 .82 .80 1.22 .92 .43 .90 .76 .86 .92 1.33 .71

54 26 21 25 31 74 225 11.02 214 1.66 1.66 .69 .78 1.21 .85 .81 1.36 .65 1.01 1.90 .38 .56

89 10 20 4 40 43 159 38 12.52 85 2.38 .63 1.33 .76 .41 .66 .80 1.01 .76 1.08 .58 .76

186 92 72 39 222 304 760 200 170 2.52 472 1.24 .83 .73 1.42 1.01 .71 .61 .65 1.05 1.02 .67

96 33 23 13 52 168 176 30 16 167 10.29 248 .73 1.84 .87 .62 .52 1.34 1.15 .43 1.06 1.92

43 15 26 9 59 128 173 34 34 112 35 14.39 348 .63 3.41 2.72 1.43 1.75 .69 .81 .55 .52

117 16 41 30 46 157 269 54 20 101 91 31 6.75 172 .53 .51 1.04 .77 2.03 .96 .50 1.01

34 21 13 2 19 42 76 14 4 73 16 63 10 25.22 89 3.22 1.83 2.22 .66 .17 .18 .87

30 26 17 12 37 59 66 25 12 96 21 93 18 42 14.51 175 2.76 2.33 .68 .79 .87 .24

32 15 24 16 43 70 131 40 14 65 17 47 35 23 64 9.24 103 1.61 .40 .59 .91 .39

179 48 77 95 110 295 471 81 74 234 186 243 110 118 229 152 2.14 427 .69 .96 1.18 .70

78 35 36 40 24 181 198 47 21 94 60 36 108 13 25 14 14 5.14 143 1.83 1.43 1.46

108 18 86 7 45 111 256 107 36 183 27 51 62 4 35 25 173 123 17.10 697 3.10 3.27

16 19 59 10 34 56 174 10 9 83 31 16 15 2 18 18 99 45 118 10.72 95 3.99

66 20 89 41 72 122 189 30 24 111 115 31 62 20 10 16 120 94 255 145 7.76 289

2874 1295 1439 791 1875 4354 6388 1380 922 3836 1621 1627 1565 698 1110 964 3623 1517 2527 1072 1921 51.5 23.0 31.3 16.8 30.7 72.1 100 22.8 15.0 63.4 29.8 32.0 29.3 14.4 18.3 15.9 67.2 26.3 25.6 15.3 33.4

1 Chicago

2 Cleveland

3 Minneapolis - St. Paul

4 St. Louis

5 Other Ohio Areas

6 Other Midwest Areas

7 New York City

8 Boston

9 Philadelphia

10 Other East Coast Areas

11 Houston

12 Atlanta

13 Dallas - Fort Worth

14 Richmond

15 North Carolina

16 Florida

17 Other Southern Areas

18 Mountain States

19 San Francisco Bay Area

20 Los Angeles

21 Other West Coast Areas

TOTAL INTERLOCKS NETWORK CENTRALITY

LOGLINEAR MARGINALS

Figure 8. Geography of US Interlocks (circle size indicates network centrality; dashed lines mark strong associations in rows of

Table 3 [>75% of strongest tie]; solid arrows mark strongest

association, highlighted in Table 3, for source of arrow)

OtherOhio Areas

Cleveland

OtherMidwestAreas

Minneapolisand St. Paul

St. Louis

OtherWest CoastAreas

Boston

OtherSouthern Areas(including Texas,except DFWand Houston)

Richmond

NorthCarolina

Atlanta

Florida

LosAngeles

MountainStates

Chicago

Philadelphia OtherEast Coast Areas

Dallas andForth Worth

Houston

New YorkCity

San FranciscoBay Area

15/04/2011

Digging into Significant Bridges

More cosmopolitan connections More innovation, top-line growth Less emphasis on bottom-line

Less stable reputations

Reputation in the Western World The Data Conceptual Foundations Distinguishing Regional Clusters Digging into Significant Bridges Digging into Significant Closure

Appendix Materials

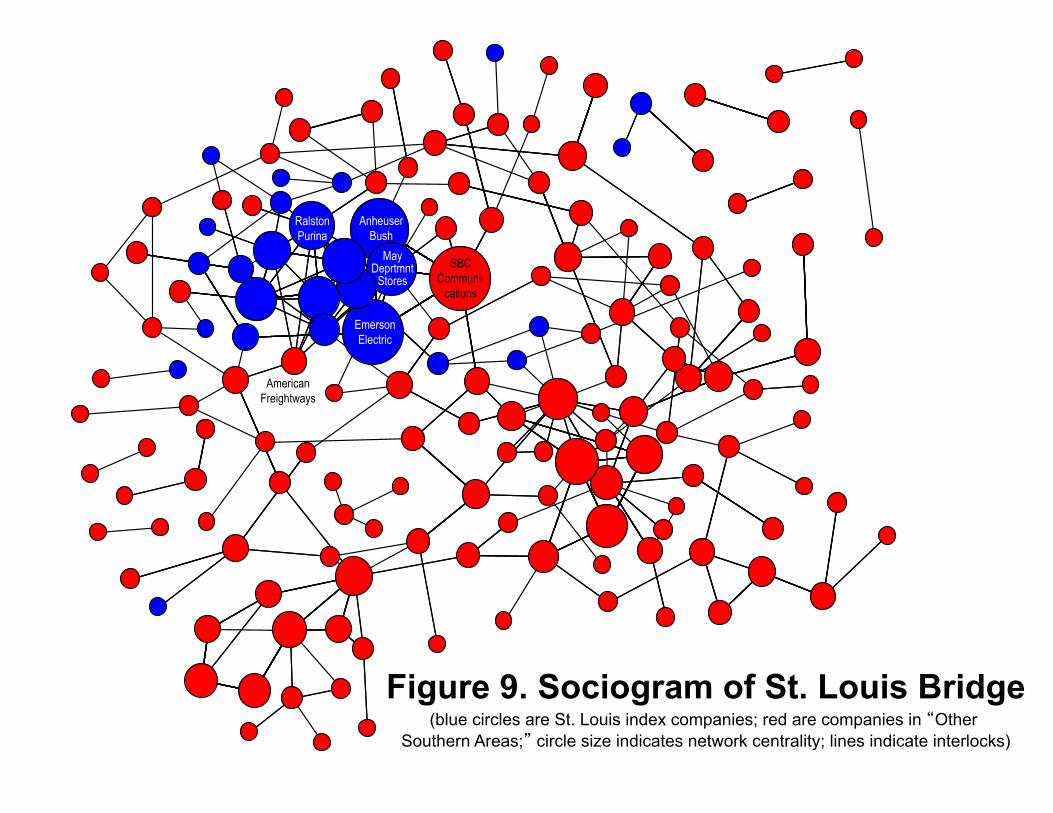

Figure 9. Sociogram of St. Louis Bridge (blue circles are St. Louis index companies; red are companies in “Other

Southern Areas;” circle size indicates network centrality; lines indicate interlocks)

Emerson Electric

SBC Communi-

cations

Anheuser Bush

May Deprtmnt

Stores

Ralston Purina

AmericanFreightways

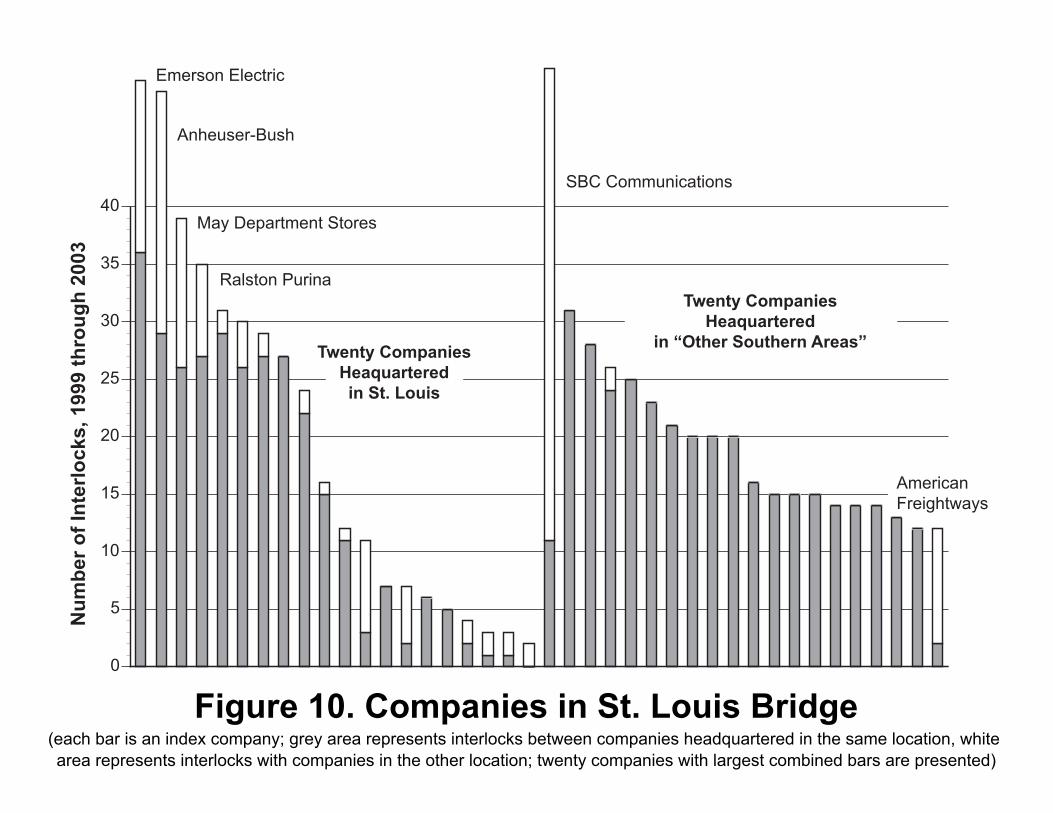

Figure 10. Companies in St. Louis Bridge (each bar is an index company; grey area represents interlocks between companies headquartered in the same location, white area represents interlocks with companies in the other location; twenty companies with largest combined bars are presented)

0

5

10

15

20

25

30

35

40

Num

ber of Interlocks, 1999 through 2003

Emerson Electric

Anheuser-Bush

May Department Stores

Ralston Purina

SBC Communications

Twenty CompaniesHeaquartered

in “Other Southern Areas”Twenty CompaniesHeaquarteredin St. Louis

AmericanFreightways

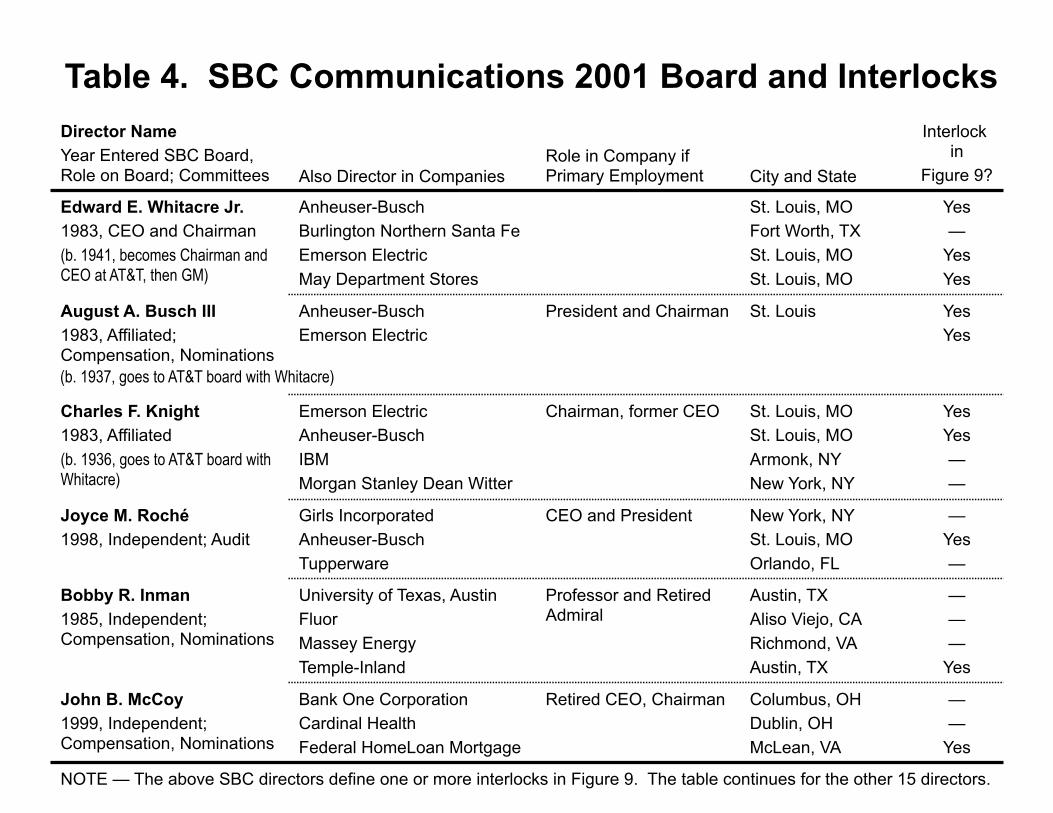

Director Name Year Entered SBC Board, Role on Board; Committees Also Director in Companies

Role in Company if Primary Employment City and State

Interlock in

Figure 9?

Edward E. Whitacre Jr. 1983, CEO and Chairman (b. 1941, becomes Chairman and CEO at AT&T, then GM)

Anheuser-Busch Burlington Northern Santa Fe Emerson Electric May Department Stores

St. Louis, MO Fort Worth, TX St. Louis, MO St. Louis, MO

Yes —

Yes Yes

August A. Busch III 1983, Affiliated; Compensation, Nominations

Anheuser-Busch Emerson Electric

President and Chairman St. Louis Yes Yes

Charles F. Knight 1983, Affiliated (b. 1936, goes to AT&T board with Whitacre)

Emerson Electric Anheuser-Busch IBM Morgan Stanley Dean Witter

Chairman, former CEO St. Louis, MO St. Louis, MO Armonk, NY New York, NY

Yes Yes — —

Joyce M. Roché 1998, Independent; Audit

Girls Incorporated Anheuser-Busch Tupperware

CEO and President New York, NY St. Louis, MO Orlando, FL

— Yes —

Bobby R. Inman 1985, Independent; Compensation, Nominations

University of Texas, Austin Fluor Massey Energy Temple-Inland

Professor and Retired Admiral

Austin, TX Aliso Viejo, CA Richmond, VA Austin, TX

— — —

Yes

John B. McCoy 1999, Independent; Compensation, Nominations

Bank One Corporation Cardinal Health Federal HomeLoan Mortgage

Retired CEO, Chairman Columbus, OH Dublin, OH McLean, VA

— —

Yes

Table 4. SBC Communications 2001 Board and Interlocks

(b. 1937, goes to AT&T board with Whitacre)

NOTE — The above SBC directors define one or more interlocks in Figure 9. The table continues for the other 15 directors.

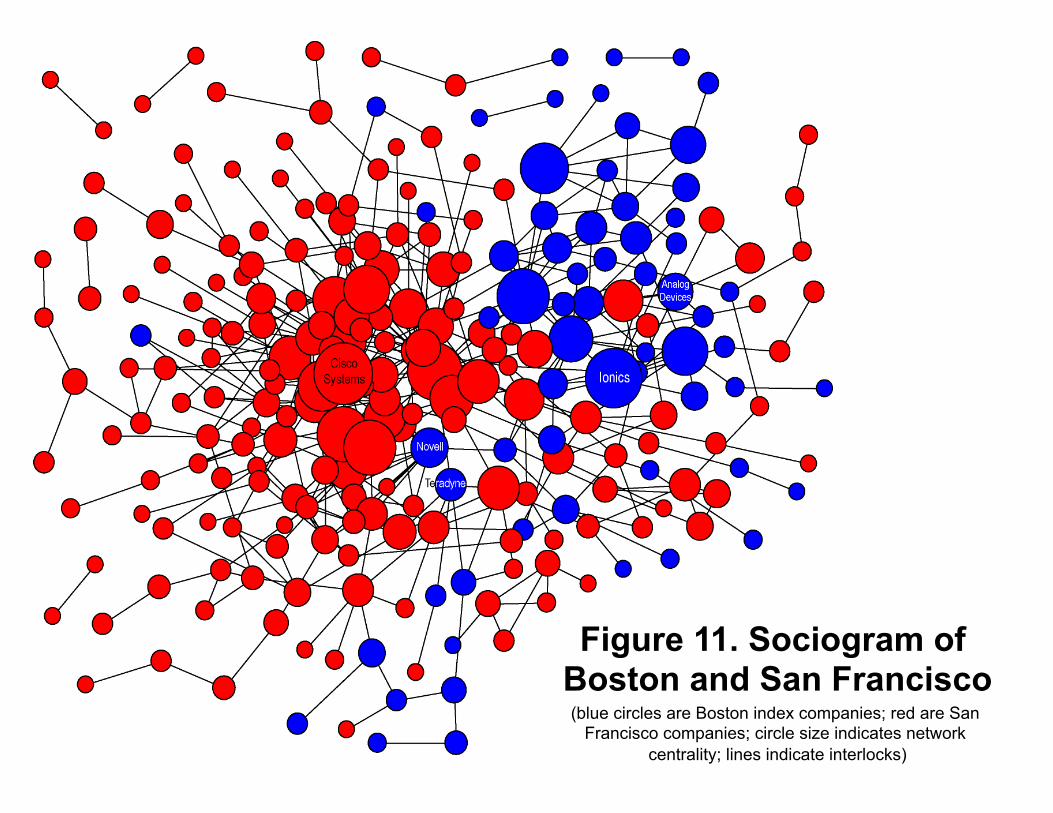

Figure 11. Sociogram of Boston and San Francisco (blue circles are Boston index companies; red are San

Francisco companies; circle size indicates network centrality; lines indicate interlocks)

Figure 12. Companies in Boston Bridge to San Francisco (each bar is an index company; grey area represents interlocks between companies headquartered in the same location, white area represents interlocks with companies in the other location; twenty companies with largest combined bars are presented)

0

5

10

15

20

25

30

35

40

Novell

Number of Interlocks, 1999 through 2003

Lam Research

Knight-RidderXilinx

Ionics

Novellin Figure 11

Teradyne

Cisco SystemsTwenty Companies

Headquartered in

San Francisco Bay Area

Twenty Companies

Headquartered

in Boston

Analog Devices

15/04/2011

Digging into Significant Closure

More community connections More emphasis on bottom line

Less innovation, top-line growth More stable reputations

Reputation in the Western World The Data Conceptual Foundations Distinguishing Regional Clusters Digging into Significant Bridges Digging into Significant Closure

Appendix Materials

Figure 13. Relative to San Francisco, Board Seats in Chicago Are more Concentrated in a Few Individuals

0%

10%

20%

30%

40%

50%

60%

70%

41%

59%

46%

54% 53%

47%

60%

40%

71%

29%

Director

in One

(2557)

[3715]

Director

in Two

(1070)

[1261]

Director

in Three

(610)

[547]

Director

in Four

(285)

[189]

Director

in Five or More

(165)

[67]

Number of Index-Company Board Seats

Occupied by Chicago and San Franscisco Directors

(annual observations summed across 1999 through 2003)

Percent of Directors

Chicago Area

San Fransciso

Bay Area

Figure 14. Local Elites Are more Obvious in Locations more Isolated

Raw Residual

Atlanta 100 98.5

Chicago 49 54.0

Richmond 75 45.6

Twin Cities 38 30.6

Dallas - Ft. Worth -3 23.0

New York City 21 8.2

Houston -21 -8.1

Boston -22 -9.0

Cleveland 68 -15.4

St. Louis 47 -24.0

Philadelphia -38 -25.2

Los Angeles -46 -28.6

San Francisco -31 -52.0

Directorate Concentration

In Local Elite

Note: “Raw” is the Y axis in the graph. Residual is the Y axis minus the concentration expected in a place from isolation (X axis in the graph) and number of interlocks (size).

-80

-60

-40

-20

0

20

40

60

80

100

0 5 10 15 20 25 30 35 40

Location Isolation(diagonal loglinear coefficient in Table 3,

interlocks concentrated inside location)

Directorate Concentration in Local Elite

(seat concentration in few individuals)

Atlanta

Cleveland

St. Louis

Richmond

Minneapolis

St. Paul

San

Francisco

Chicago

New York

City

DFW

Boston

PhiliLA

r = .54

t = 2.8

P = .01

Houston

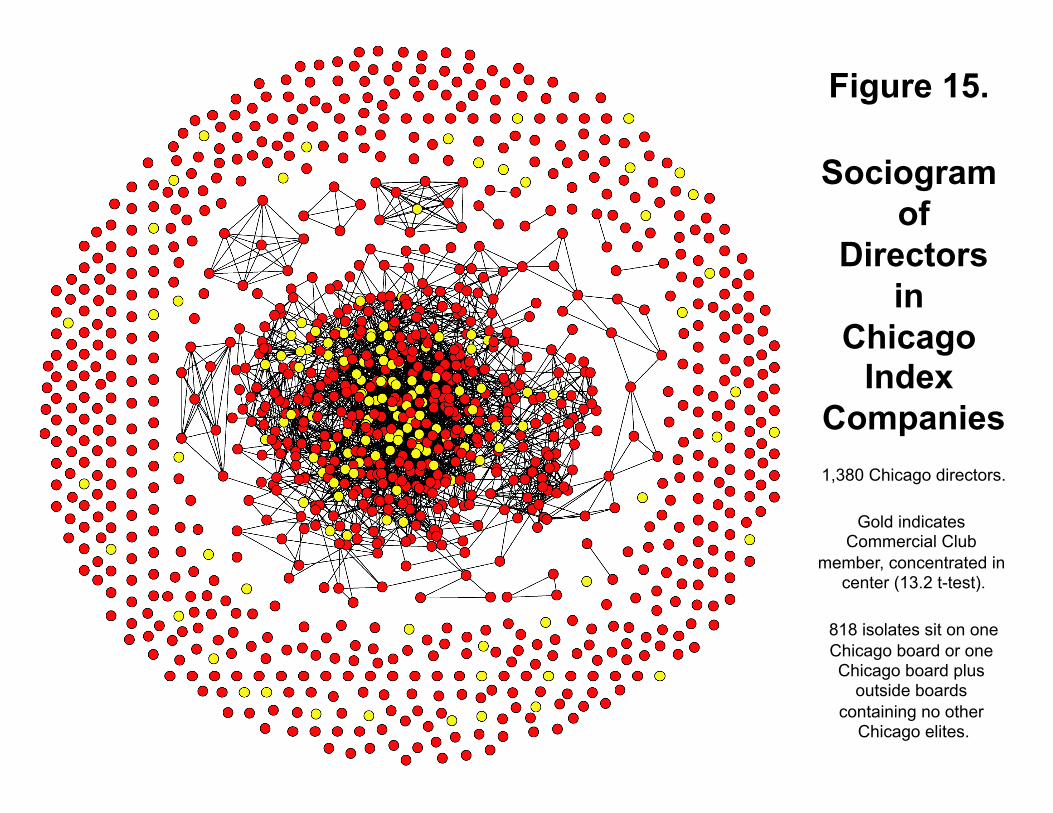

Figure 15.

Sociogram of

Directors in

Chicago Index

Companies

1,380 Chicago directors.

Gold indicates Commercial Club

member, concentrated in center (13.2 t-test).

818 isolates sit on one Chicago board or one Chicago board plus

outside boards containing no other

Chicago elites.

Some Initial Projects

The Chicago Project — Questions to be addressed include how local, social, and historical factors affect access to capital, the circulation of favors, the arrival and departure of companies, the emergence and loss of local markets, as well as the benefits to executive careers that pass through the city.

Comparative analysis to target industries — market profiles compared across cities using Porter cluster data. Set up for Sabel-Saxenian story on why certain industries flourished in the city and others do not.

Comparative network analysis to target firms and individuals — interlocking directorates compared across cities using Fortune 1000 data distinguishing Commercial Club members. Set up for Ansell-Padget story on key people or Saxenian story on key companies.

Institutional story about Commercial Club as closed-network base for reputation in Chicago. The Club as a merchant guild or “business group” in late 19th and early 20th centuries. Set up for Coleman-Granovetter-Grief story.

Here is the founder of PayPal explaining why they moved from Skokie to Palo Alto (underline added):

“We looked around in Chicago, but were told that no one invests in good ideas; you had to ‘know’ somebody.

We moved to Palo Alto, got Nokia to listen (Motorola would not talk to us), and within a year had over $100 million in investment and turned a profit in year two.”

Quoted from p. 12 of Call to Action, June 2003 study by A.T.Kearney for

Chicagoland Chamber of Commerce & Chicagoland Entrepreneurial Center

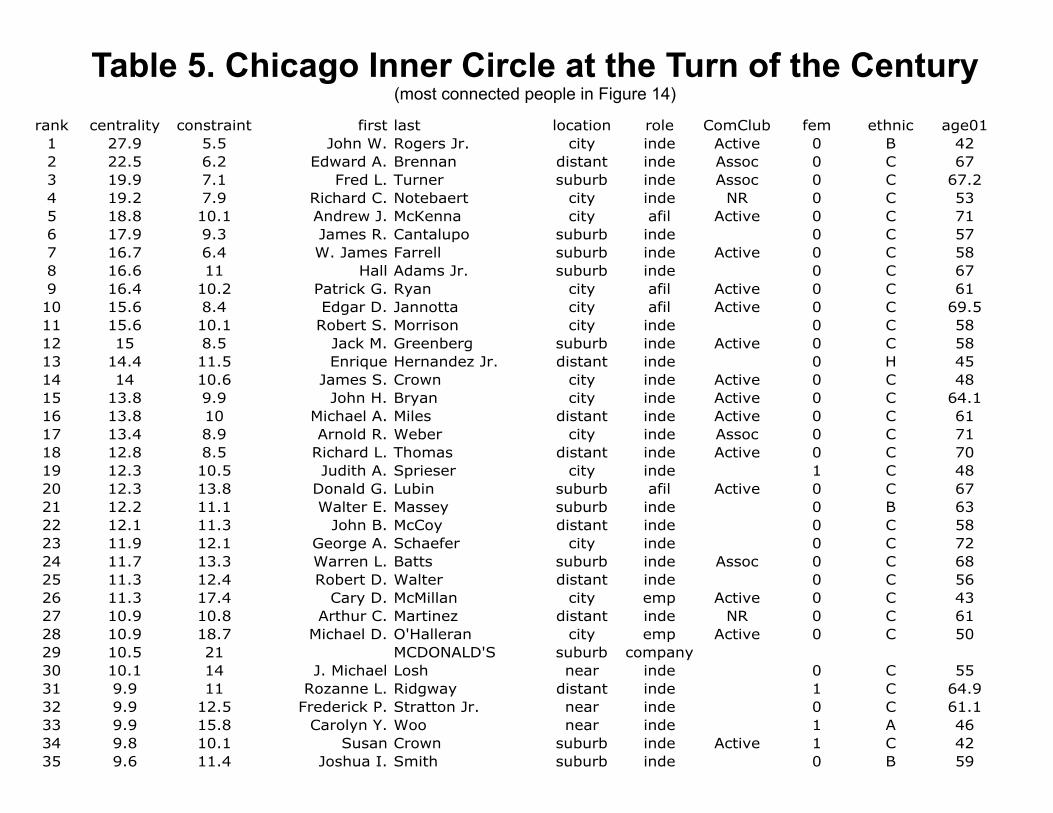

Table 5. Chicago Inner Circle at the Turn of the Century (most connected people in Figure 14)

rank centrality constraint first last location role ComClub fem ethnic age01

1 27.9 5.5 John W. Rogers Jr. city inde Active 0 B 42

2 22.5 6.2 Edward A. Brennan distant inde Assoc 0 C 67

3 19.9 7.1 Fred L. Turner suburb inde Assoc 0 C 67.2

4 19.2 7.9 Richard C. Notebaert city inde NR 0 C 53

5 18.8 10.1 Andrew J. McKenna city afil Active 0 C 71

6 17.9 9.3 James R. Cantalupo suburb inde 0 C 57

7 16.7 6.4 W. James Farrell suburb inde Active 0 C 58

8 16.6 11 Hall Adams Jr. suburb inde 0 C 67

9 16.4 10.2 Patrick G. Ryan city afil Active 0 C 61

10 15.6 8.4 Edgar D. Jannotta city afil Active 0 C 69.5

11 15.6 10.1 Robert S. Morrison city inde 0 C 58

12 15 8.5 Jack M. Greenberg suburb inde Active 0 C 58

13 14.4 11.5 Enrique Hernandez Jr. distant inde 0 H 45

14 14 10.6 James S. Crown city inde Active 0 C 48

15 13.8 9.9 John H. Bryan city inde Active 0 C 64.1

16 13.8 10 Michael A. Miles distant inde Active 0 C 61

17 13.4 8.9 Arnold R. Weber city inde Assoc 0 C 71

18 12.8 8.5 Richard L. Thomas distant inde Active 0 C 70

19 12.3 10.5 Judith A. Sprieser city inde 1 C 48

20 12.3 13.8 Donald G. Lubin suburb afil Active 0 C 67

21 12.2 11.1 Walter E. Massey suburb inde 0 B 63

22 12.1 11.3 John B. McCoy distant inde 0 C 58

23 11.9 12.1 George A. Schaefer city inde 0 C 72

24 11.7 13.3 Warren L. Batts suburb inde Assoc 0 C 68

25 11.3 12.4 Robert D. Walter distant inde 0 C 56

26 11.3 17.4 Cary D. McMillan city emp Active 0 C 43

27 10.9 10.8 Arthur C. Martinez distant inde NR 0 C 61

28 10.9 18.7 Michael D. O'Halleran city emp Active 0 C 50

29 10.5 21 MCDONALD'S suburb company

30 10.1 14 J. Michael Losh near inde 0 C 55

31 9.9 11 Rozanne L. Ridgway distant inde 1 C 64.9

32 9.9 12.5 Frederick P. Stratton Jr. near inde 0 C 61.1

33 9.9 15.8 Carolyn Y. Woo near inde 1 A 46

34 9.8 10.1 Susan Crown suburb inde Active 1 C 42

35 9.6 11.4 Joshua I. Smith suburb inde 0 B 59

15/04/2011

Reputation in the Western World The Data Conceptual Foundations Distinguishing Regional Clusters Digging into Significant Bridges Digging into Significant Closure

Appendix Materials

Appendix Materials

This is a proposal to build a research platform on a large scale that would encourage analysts to study people, organizations, communities and markets embedded in one another. The platform creates an intimate link between case studies, comparative analysis, and quantitative research to allow more general conclusions from better grounded analyses. It is, in short, a proposal to bring into state of the art research more of the blood and soil of business. This is not a project for an individual or local team. It is an exercise of leadership fittingly performed in collaboration through a reputable Centre.

Illustra(ve 3-‐Year Time Line 1a. Begin papers on US data to ini2ate product stream (templates for kinds of reports from Centre), e.g.:

-‐ compara2ve analysis of regions & ci2es – US map & Chicago vs. open city -‐ which companies have the best-‐connected directors & so what? -‐ where is reputa2on more and less persistent – rela2ve to closed network -‐ what is the role of reputa2on in local & industry recogni2on – ascension in Chicago -‐ what is the role of reputa2on in forming key bridges in the economy -‐ SBC

1b. Assemble data on European firms comparable to 1999-‐2002 US data so we have a complete “turn of the century” data set. 2a. Begin papers on European and US firms following up on work in 1a. 2b. Assemble data on US and European firms to create a second data set (lagged to avoid conflict with commercial interests), perhaps a three-‐year interval eight years later? 2008-‐2009-‐2010 3a. Con2nue work crea2ng second data set. 3b. Begin papers crea2ng templates for over-‐2me analysis of European and US firms. Based on results in these papers (much change, liRle), set 2me for next data set.

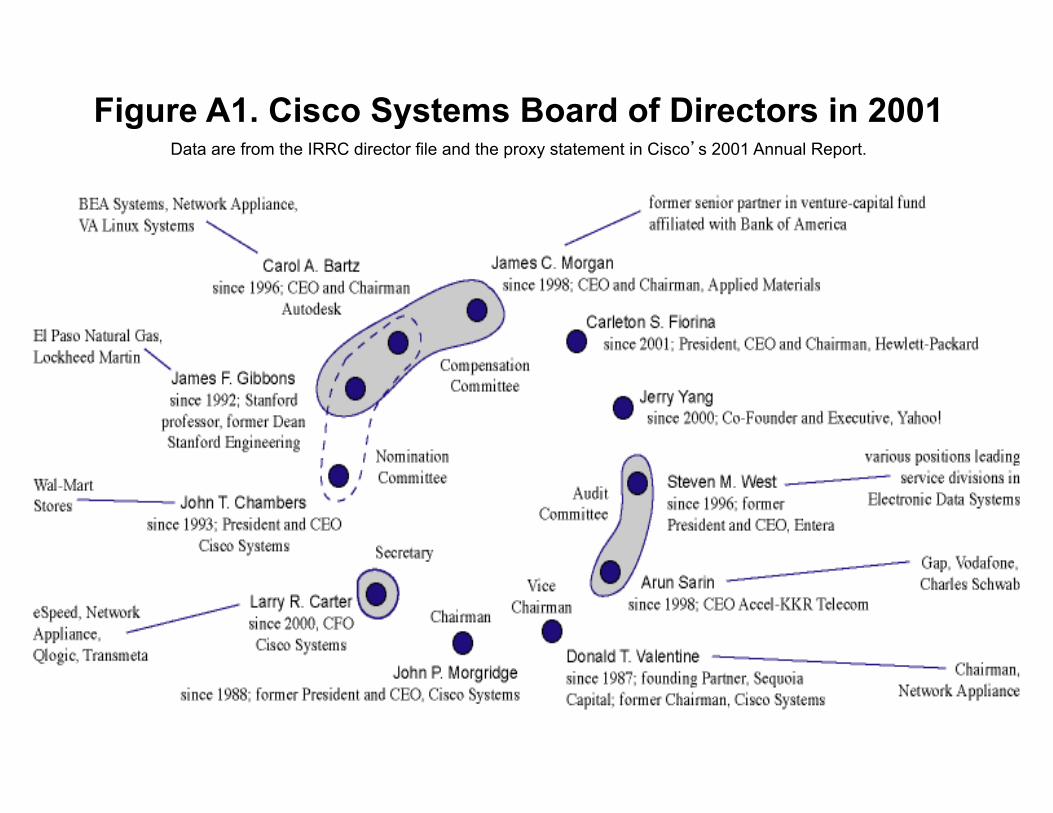

Figure A1. Cisco Systems Board of Directors in 2001 Data are from the IRRC director file and the proxy statement in Cisco’s 2001 Annual Report.

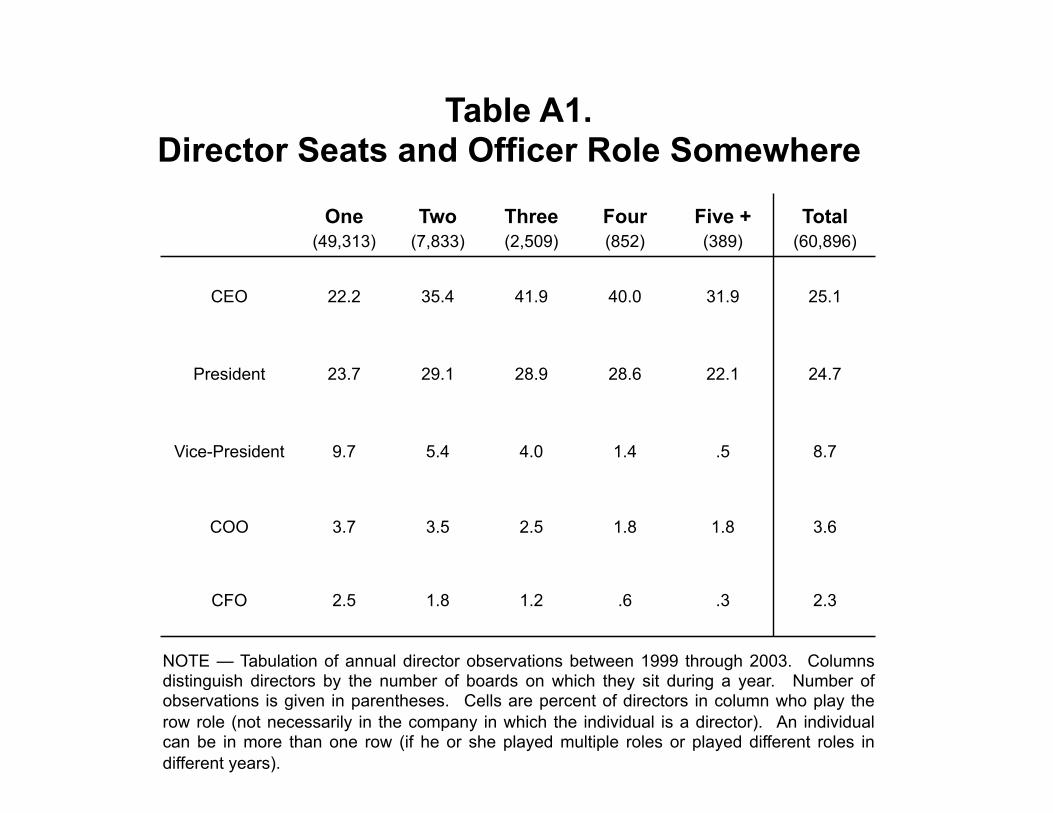

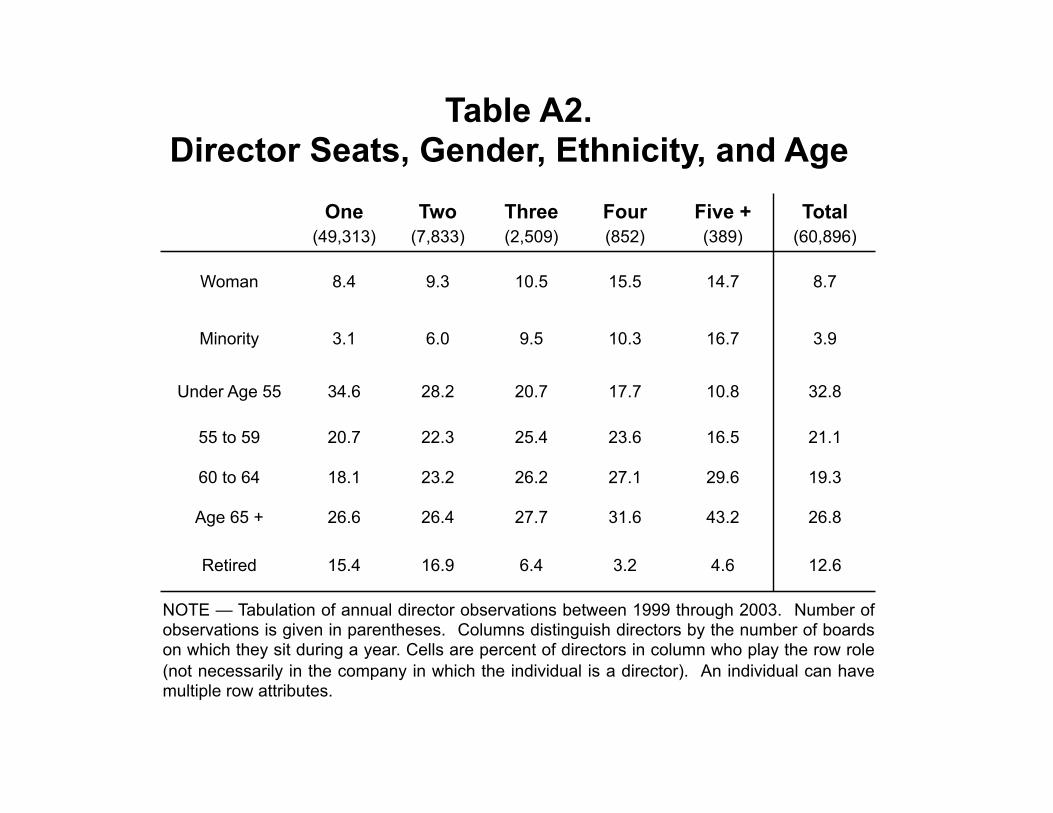

NOTE — Tabulation of annual director observations between 1999 through 2003. Columns distinguish directors by the number of boards on which they sit during a year. Number of observations is given in parentheses. Cells are percent of directors in column who play the row role (not necessarily in the company in which the individual is a director). An individual can be in more than one row (if he or she played multiple roles or played different roles in different years).

Table A1. Director Seats and Officer Role Somewhere

One (49,313)

Two (7,833)

Three (2,509)

Four (852)

Five + (389)

Total (60,896)

CEO 22.2 35.4 41.9 40.0 31.9 25.1

President 23.7 29.1 28.9 28.6 22.1 24.7

Vice-President 9.7 5.4 4.0 1.4 .5 8.7

COO 3.7 3.5 2.5 1.8 1.8 3.6

CFO 2.5 1.8 1.2 .6 .3 2.3

NOTE — Tabulation of annual director observations between 1999 through 2003. Number of observations is given in parentheses. Columns distinguish directors by the number of boards on which they sit during a year. Cells are percent of directors in column who play the row role (not necessarily in the company in which the individual is a director). An individual can have multiple row attributes.

Table A2. Director Seats, Gender, Ethnicity, and Age

One (49,313)

Two (7,833)

Three (2,509)

Four (852)

Five + (389)

Total (60,896)

Woman 8.4 9.3 10.5 15.5 14.7 8.7

Minority 3.1 6.0 9.5 10.3 16.7 3.9

Under Age 55 34.6 28.2 20.7 17.7 10.8 32.8

55 to 59 20.7 22.3 25.4 23.6 16.5 21.1

60 to 64 18.1 23.2 26.2 27.1 29.6 19.3

Age 65 + 26.6 26.4 27.7 31.6 43.2 26.8

Retired 15.4 16.9 6.4 3.2 4.6 12.6

Stra

tegi

c Lea

ders

hip

Deliv

erin

g Va

lue:

The

Soc

ial C

apita

l of C

losu

re (p

age 4

4)

Reputation Stability Predicted by Positive Closure versus Negative Closure

Figure 3 in Burt, "Gossip and reputation" in Management et Réseaux Sociaux, edited by edited by Marc Lecoutre and Pascal Lievre (2008 Hermes-Lavoisier, English language version on my website).

A. Positive Indirect Connections B. Negative Indirect Connections

Colleague Employee Colleague Employee

+++

MutualContactPhilippe

MutualContact

Catherine

+- - -

-

MutualContactEmile

MutualContact

Marc

If bandwidth story true, then: Stability of positive reputation increases with positive indirect, decreases with negative indirect (relations as info pipes) Stability of negative reputation increases with negative indirect, decreaess with positive indirect (relations as info pipes)

If echo story true, then Stability of positive reputation increases with positive or negative indirect (etiquette filter on info transmitted) Stability of negative reputation increases with positive or negative indirect (etiquette filter on info transmitted)

Stra

tegi

c Lea

ders

hip

Deliv

erin

g Va

lue:

The

Soc

ial C

apita

l of C

losu

re (p

age 4

5)

Stability of Positive and Negative ReputationsIncrease with Either Positive or Negative Closure.

Relations Are Balanced in Amplitude, not Direction;Reputations Are Defined by Network Echo, not Bandwidth.

Table 1 in Burt, "Gossip and reputation" in Management et Réseaux Sociaux, edited by edited by Marc Lecoutre and Pascal Lievre (2008 Hermes-Lavoisier, English language version on my website).

NOTE — These are regression models predicting reputation stability from this year to next using network variables measured this year. Stability is measured for an employee by the sub-correlation between reputation in adjacent years (vertical axis in Figure 2 of the source paper cited below, cf. pages 16 and 42 of this handout). Average number of mutual contacts (horizontal axis in Figure 2) are here log scores to capture the nonlinear association illustrated in Figure 2. T-tests in parentheses are adjusted for autocorrelation between repeated observations (using "cluster" option in STATA), but they are only a heuristic since routine statistical inference is not applicable for sub-sample correlations as a criterion variable (footnote 1 in the source paper cited below). * P < .05 ** P < .001

1 2 3 4 5 6

R2 .59 .50 .59 .45 .50 .51

Average Number of Mutual Contacts Linking Employee this Year with Colleagues

Number of Positive .77** (28.1) — .66**

(11.7) .67** (21.2) — .21**

(3.6)

Number of Negative — .71** (23.7)

.12* (2.2) — .70**

(23.3) .52** (8.7)

Predict Positive Reputations

(N = 899)

Predict Negative Reputations

(N = 797)

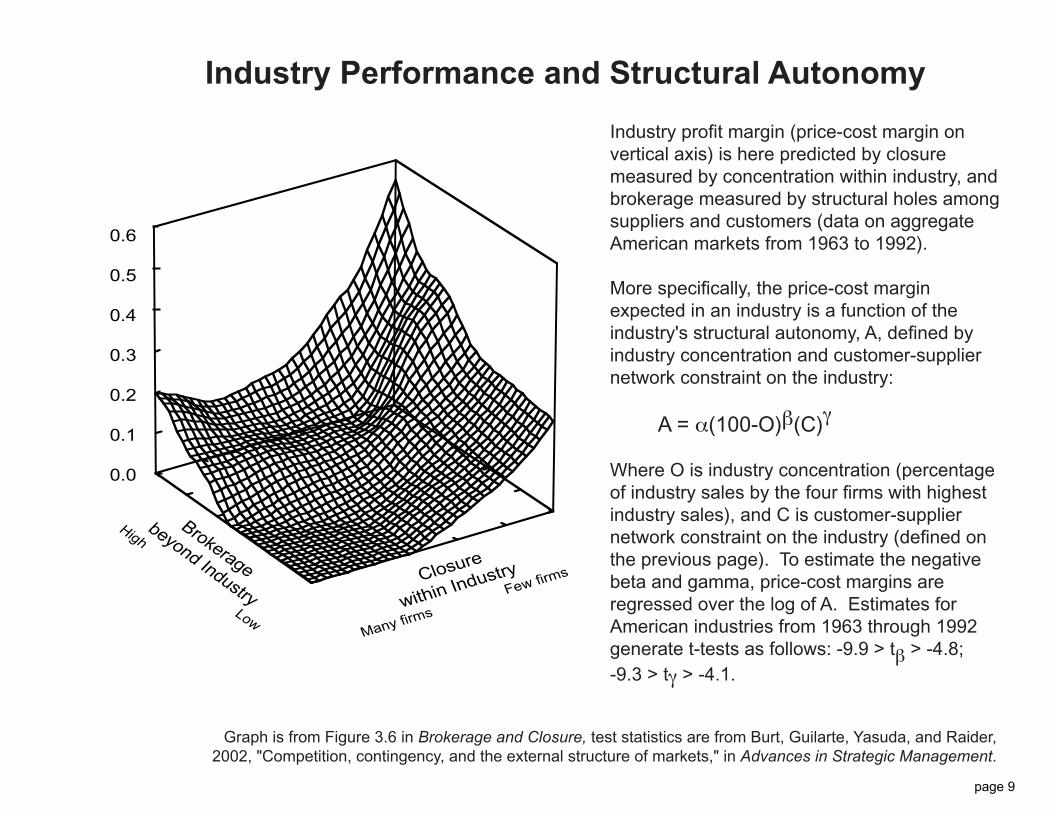

Industry Performance and Structural Autonomy

Industry profit margin (price-cost margin on vertical axis) is here predicted by closure measured by concentration within industry, and brokerage measured by structural holes among suppliers and customers (data on aggregate American markets from 1963 to 1992).

More specifically, the price-cost margin expected in an industry is a function of the industry's structural autonomy, A, defined by industry concentration and customer-supplier network constraint on the industry:

A = a(100-O)b(C)g

Where O is industry concentration (percentage of industry sales by the four firms with highest industry sales), and C is customer-supplier network constraint on the industry (defined on the previous page). To estimate the negative beta and gamma, price-cost margins are regressed over the log of A. Estimates for American industries from 1963 through 1992 generate t-tests as follows: -9.9 > tb > -4.8; -9.3 > tg > -4.1.

Graph is from Figure 3.6 in Brokerage and Closure, test statistics are from Burt, Guilarte, Yasuda, and Raider, 2002, "Competition, contingency, and the external structure of markets," in Advances in Strategic Management.

0.1

0.2

0.3

0.4

0.5

0.6

Internal

Brokerage

beyondIndustry

High

Low

Closure

within Industry

Many firms

Few firms

0.6

0.5

0.4

0.3

0.2

0.1

0.0

page 9

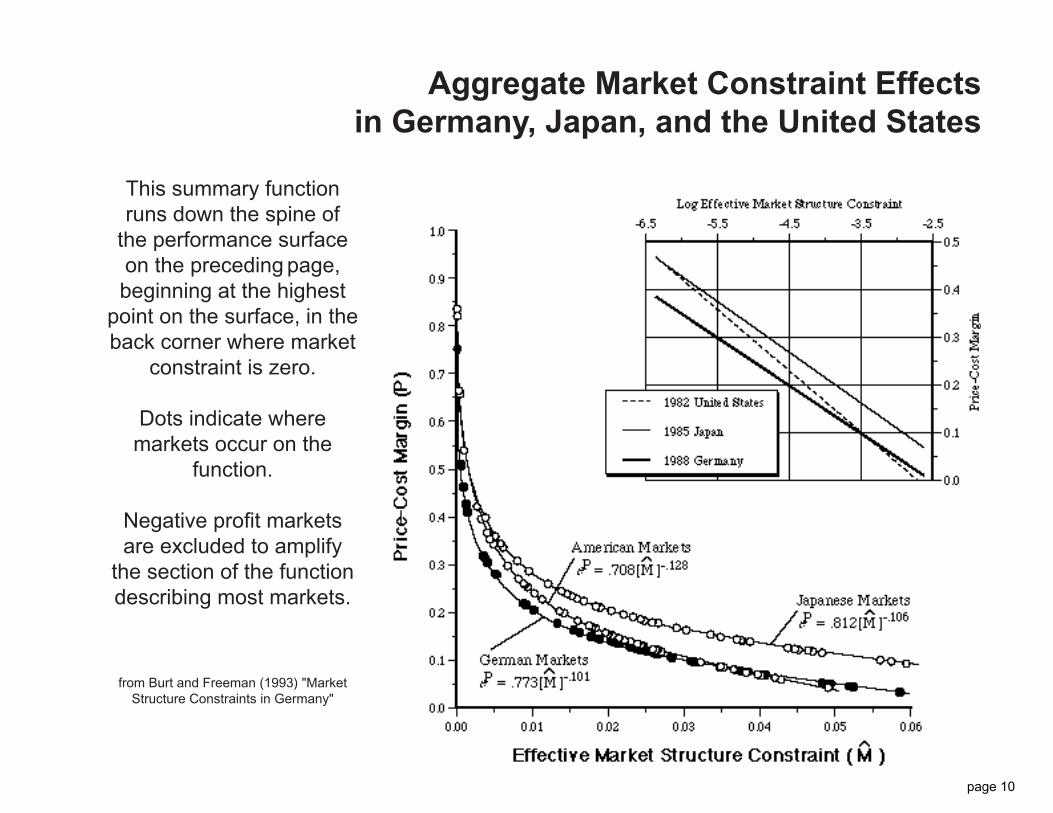

Aggregate Market Constraint Effectsin Germany, Japan, and the United States

This summary function runs down the spine of

the performance surface on the preceding page, beginning at the highest

point on the surface, in the back corner where market

constraint is zero.

Dots indicate where markets occur on the

function.

Negative profit markets are excluded to amplify

the section of the function describing most markets.

from Burt and Freeman (1993) "Market Structure Constraints in Germany"

page 10

Stra

tegi

c Lea

ders

hip

Deliv

erin

g Va

lue:

The

Soc

ial C

apita

l of C

losu

re (p

age 3

7)

Ronald S

. Burt is the

Hobart W

. William

sP

rofessor of Sociology

and Strategy at the

University of C

hicagoG

raduate School of

Business, and the S

hellP

rofessor of Hum

anR

esources at INS

EA

D.

His w

ork describesthe social structure ofcom

petition: network

mechanism

s that ordercareers, organizations,and m

arkets.

When is C

orporate Culture

a Com

petitive Asset?

Sum

mary

-----------------------------------------------------------------------------------A

dvocates speak of corporate culture affecting the bottom line, but

the cited evidence is rarely more than anecdotes, and then

inconclusive. Som

e companies doing w

ell have strong cultures, butother com

panies do well w

ith nothing in the way of shared beliefs

that could be termed a corporate culture. S

o why w

orry about it? Itis to be w

orried about because in certain industries, a strong culturecan be a pow

erful advantage over competitors. T

he complication is

that in other industries, culture is irrelevant to performance. T

hetrick is to know

when culture is a com

petitive asset and when it is

not. Ron B

urt explains with em

pirical evidence how and w

here astrong corporate culture can be a com

petitive asset. Know

ing thecontingent value of culture can be a guide to deciding w

hen to investin the culture of your ow

n organization, when to protect the culture

of an organization merged into your ow

n, and when not to w

orryabout culture.

Culture is to a corporation w

hat it is to any othersocial system

, a selection of beliefs, myths, and

practices shared by people such that they feelinvested in, and part of, one another. P

uttingaside the specific beliefs that em

ployees share,the culture of an organization is strong to theextent that em

ployees are strongly held togetherby their shared belief in the culture. C

ulture isw

eak to the extent that employees hold w

idelydifferent, even contradictory, beliefs so as to feeldistinct from

one another.

Culture effect in theory

In theory, a strong corporate culture can enhancecorporate econom

ic performance by reducing

costs.T

here are lo

wer m

on

itorin

g co

sts. Th

eshared beliefs, m

yths, and practices that definea co

rpo

rate cultu

re are an in

form

al con

trol

mech

anism

that co

ord

inates em

plo

yee effo

rt.E

mployees deviating from

accepted practice canbe detected and adm

onished faster and less vis-ibly by friends than by the boss. T

he firm’s goals

and practices are more clear, w

hich lessens em-

ployee uncertainty about the risk of taking in-ap

pro

priate actio

n so

they

can resp

on

d m

ore

qu

ickly

to ev

ents. N

ew em

plo

yees are m

ore

effectively brought into coordination with es-

tablished employees because they are less likely

to hear conflicting accounts of the firm’s goals

and practices. Moreover, the control of corpo-

rate culture is less imposed on em

ployees thanit is socially constructed by them

, so employee

motivation and m

orale should be higher thanw

hen control is exercised by a superior throughbureaucratic lines of authority.

There are low

er labor costs. For reasons of

social p

ressure fro

m p

eers, the attractio

n o

fpursuing a transcendental goal larger than theday-to-day dem

ands of a job, or the exclusionof em

ployees who do not feel com

fortable with

the corporate culture, employees w

ork harderand for longer hours in an organization w

ith astrong corporate culture. In other w

ords, a strongco

rpo

rate cultu

re extracts u

np

aid lab

or fro

mem

ployees.T

hese savings mean that com

panies with a

stronger corporate culture can expect to enjoyhigher econom

ic performance. W

hatever them

agnitude of the economic enhancem

ent, it isthe "culture effect."

Evidence is m

ixedT

he most authoritative evidence of the culture

effect comes from

a study by Harvard B

usinessS

cho

ol p

rofesso

rs Joh

n K

otter an

d Jam

esH

eskett, based on data published in the appendixo

f their 1

99

2 b

oo

k, C

orp

orate C

ultu

re and

Perfo

rman

ce. Measu

res of p

erform

ance an

dstrong culture are listed for a large sam

ple offirm

s in a variety of broad industries analogousto the industry categories in F

ortune magazine.

To

measu

re relative stren

gth

of cu

lture,

Kotter and H

eskett mailed questionnaires in the

early 1980s to the top six officers in each sample

company, asking them

to rate (on a scale of 1 to5) the strength of culture in other firm

s selectedfor study in their industry. T

hree indicators ofstrong culture w

ere listed: (1) managers in the

firm com

monly speak of their com

pany’s styleor w

ay of doing things, (2) the firm has m

adeits values know

n through a creed or credo andh

as mad

e a seriou

s attemp

t to en

cou

rage

managers to follow

them, and (3) the firm

hasb

een m

anag

ed acco

rdin

g to

lon

g-stan

din

gpolicies and practices other than those of justthe incum

bent CE

O. R

atings were averaged to

define the strength of a firm's corporate culture,

which can be adjusted for the industry average

to make com

parisons across industries.

For exam

ple, Johnson & Johnson is cited as

benefiting from its strong culture in the rapid

recall of Tylenol w

hen poisoned capsules were

discovered on shelves. In the Kotter and H

eskettstudy, Johnson &

Johnson received an averagera

ting

o

f 4

.61

, th

e

hig

he

st g

ive

n

to

ap

harm

aceutical firm

in th

e stud

y, 1.0

7 p

oin

tsabove the 3.51 average for pharm

aceutical firms,

so you see the company to the far right of the

graph below (G

raph 1).R

elative economic perform

ance is plottedon the vertical axis of the graph. K

otter andH

eskett list th

ree measu

res repo

rted to

yield

similar conclusions about the culture effect: net

inco

me g

row

th fro

m 1

97

7 to

19

88

, averag

ereturn on invested capital from

1977 to 1988,and average yearly increases in stock prices from1977 to 1988. F

or illustration here, I use averagereturn on invested capital.

For exam

ple, Johnson & Johnson enjoyed a

17

.89

% rate o

f return

ov

er the d

ecade, b

ut

ph

armaceu

ticals is a hig

h-retu

rn in

du

stry in

which 17.89%

was slightly below

average, soyou see Johnson &

Johnson below zero on the

vertical axis of the graph (17.89 minus 20.21

equals the Johnson & Johnson score of -2.32).

The point is the lack of association betw

eeneconom

ic performance and corporate culture.

Graph 1 contains pharm

aceutical firms, along

with

samp

le firms fro

m b

everag

es, perso

nal

care, and comm

unications — a total of 30 firm

s.N

o extreme cases obscure an association. T

hereis sim

ply no association. The correlation of .06

is almost the .00 you w

ould get if performance

were perfectly independent of culture. K

ottera

nd

He

ske

tt rep

ort a

sligh

tly h

igh

er .3

1co

rrelation

across all o

f their firm

s, bu

t the

correlation was still sufficiently w

eak for themto conclude in their book that: "the statem

ent'stro

ng

cultu

res create excellen

t perfo

rman

ce'appears to be just plain w

rong."

Contingent value of culture

There is a pow

erful culture effect in fact, but itoccurs elsew

here in the economy. G

raph 2, atthe top of the next page, has the sam

e axes asG

raph

1 b

ut p

lots d

ata on

samp

le com

pan

iesfrom

other industries — airlines, apparel, m

otorvehicles, and textiles. T

he 36 sample firm

s fromth

ese ind

ustries sh

ow

a close asso

ciation

between perform

ance and culture; the strongerthe corporate culture, the higher the return oninvested capital.

The key point is illustrated in G

raph 3, which

sho

ws a p

redictab

le shift fro

m cu

lture b

eing

economically irrelevant (G

raph 1) to it being acom

petitive asset (Graph 2). N

ineteen industriesfrom

the Kotter and H

eskett study are orderedon the vertical axis of G

raph 3 by the correlationbetw

een performance and culture. A

pparel isat the top of the graph w

ith its .76 correlationb

etw

ee

n

cu

lture

a

nd

p

erfo

rma

nc

e.

Co

mm

un

ication

s is at the b

otto

m w

ith its

negligible -.15 correlation.T

he horizontal axis of Graph 3 is a m

easureof m

arket competition in each industry. U

singd

ata in th

e pu

blic d

om

ain (p

rimarily

the

benchmark input-output tables published by the

U.S

. Departm

ent of Com

merce; sim

ilar data areav

ailable fo

r agg

regate in

du

stries in m

ost

adv

anced

econ

om

ies), mark

et com

petitio

n is

deriv

ed fro

m th

e netw

ork

effect on

ind

ustry

profit margins of industry buying and selling

with

su

pp

liers

an

d

cu

stom

ers

(thu

s th

e"effective" level of com

petition). The effective

level of market com

petition is high in an industryto the extent that producers show

lower profit

margins than expected from

the network of their

transactions with suppliers and custom

ers (form

easurement details see, under F

urther Reading,

my 1999 paper on com

petition and contingencyw

ith Miguel G

uilarte at the Fielding Institute,

Holly R

aider at INS

EA

D, and Y

uki Yasuda at

Rikkyo U

niversity). G

raph 3 shows that m

arket and culture arecom

plements. T

o the left, where producers face

an effectively low level of m

arket competition,

culture is not a competitive asset. T

hese are the30 sam

ple firms in G

raph 1 taken from the four

Relative C

ulture Strength

(firm score - industry average)

0.0-1.0

-2.01.0

2.0

Y =

.00 + .34 X

r = .06

t = 0.3

Beverages

Pharm

aceuticalsP

ersonal Care

Com

munications

Relative Return on Invested Capital(firm score - industry average)

15%

10%5%0%

-5%

-10%

-15%

Johnson &

Johnson

Graph 1

Scheduled to

appear in anA

utumn, 1999

series in theF

inancial Times

on Mastering

Strategy

from the

Autum

n, 1999Financial Tim

esseries on“M

asteringStrategy”

Appendix III: C

ulture Effect in Brief

Stra

tegi

c Lea

ders

hip

Deliv

erin

g Va

lue:

The

Soc

ial C

apita

l of C

losu

re (p

age 3

8)

Fu

rther read

ing

:

J. P. Kotter and J. L

Heskett (1992)

Corporate C

ulture andP

erformance.

R. S

. Burt, S

. M.

Gabbay, G

. Holt, and

P. Moran (1994)

"Contingent

organization as anetw

ork theory: theculture-perform

ancecontingency function,"A

cta Sociologica

37:345-370.

J. B. S

ørensen (1998)

"The strength of

corporate culture andthe reliability of firmperform

ance," (http://gsbw

ww

.uchicago.edu/fac/jesper.sorensen/research).

R. S

. Burt, M

. Guilarte,

H. J. R

aider and Y.Y

asuda (1999)"C

ompetition,

contingency, and theexternal structure ofm

arkets," (http://gsbw

ww

.uchicago.edu/fac/ronald.burt/research; also here isthe industry appendixfrom

which the results

in the box are taken).

industries en

closed

by a d

otted

line in

the lo

wer-

left of G

raph 3

. These are co

mplex

, dynam

icm

ark

ets su

ch

as th

e c

om

mu

nic

atio

ns a

nd

ph

arm

aceu

tical in

du

stries, in

wh

ich

pro

fitm

argin

s are good, b

ut co

mpan

ies hav

e to stay

nim

ble to

take ad

van

tage o

f the n

ext sh

ift in th

em

arket. T

here is co

mpetitio

n to

be su

re (see the

1999 p

aper), b

ut th

e poin

t here is th

at a strong

co

rpo

rate

cu

lture

is n

ot a

sso

cia

ted

with

econ

om

ic perfo

rman

ce. (My

colleag

ue at th

eU

niv

ersity

of C

hic

ag

o, Je

sper S

øren

sen

, has

studied

these firm

s over tim

e, and d

escribes in

his 1

998 p

aper o

n reliab

le perfo

rman

ce how

the

cultu

re effect is weak

er for firm

s more su

bject

to m

arket ch

ange.)

At th

e oth

er extrem

e, to th

e right in

Grap

h3, w

here p

roducers face an

effectively

hig

h lev

el

of m

ark

et c

om

petitio

n, c

ultu

re is c

lose

lyasso

ciated w

ith eco

nom

ic perfo

rman

ce. These

are the 3

6 sam

ple firm

s in G

raph 2

taken

from

the fo

ur in

dustries en

closed

by a d

otted

line in

the u

pper-rig

ht o

f Grap

h 3

. In th

ese industries

of

effe

ctiv

ely

h

igh

m

ark

et

co

mp

etitio

n,

pro

ducers are easily

substitu

ted fo

r one an

oth

er,su

ppliers, cu

stom

ers or fo

reign p

roducers are

strong, an

d m

argin

s are low

.

Co

ntin

gen

cy fun

ction

Be

twe

en

th

e

two

m

ark

et

ex

trem

es,

the

perfo

rman

ce effect of a stro

ng co

rporate cu

lture

incre

ase

s with

mark

et c

om

petitio

n. T

he

nonlin

ear regressio

n lin

e in G

raph 3

(the so

lidbold

line), can

be u

sed as a co

ntin

gen

cy fu

nctio

nd

esc

ribin

g h

ow

cu

lture

's effe

ct v

arie

s with

mark

et com

petitio

n. F

or an

y sp

ecific level o

fm

arket co

mpetitio

n o

n th

e horizo

ntal ax

is, the

co

ntin

gen

cy

fun

ctio

n d

efin

es a

n e

xp

ecte

dco

rrelation o

n th

e vertical ax

is betw

een cu

lture

strength

and eco

nom

ic perfo

rman

ce.S

ince in

dustry

scores o

n th

e horizo

ntal ax

isare co

mputed

from

data p

ublicly

availab

le on

all in

du

stries, th

e e

xp

ecte

d v

alu

e o

f a stro

ng

co

rpo

rate

cu

lture

in a

ny

ind

ustry

can

be

ex

trap

ola

ted

from

the c

on

ting

en

cy

fun

ctio

n.

Resu

lts for a selectio

n o

f industries are g

iven

inth

e box to

the rig

ht.

Th

e h

igh

co

rrela

tion

for th

e c

on

ting

en

cy

functio

n sh

ow

s that th

e functio

n is an

accurate

desc

riptio

n o

f cu

lture

's effe

ct in

the d

iverse

mark

ets (r = .8

5, fo

r details o

n d

erivin

g, an

dex

trapolatin

g fro

m, th

e contin

gen

cy fu

nctio

n see

my 1

994 article o

n co

ntin

gen

t org

anizatio

n w

ithS

hau

l Gab

bay

at T

ech

nio

n, G

erh

ard

Ho

lt at

INS

EA

D, a

nd

Pete

r Mo

ran

at th

e L

on

do

nB

usin

ess Sch

ool).

At th

e level o

f indiv

idual firm

s, 44%

of th

evarian

ce in co

mpan

y retu

rns to

invested

capital

can b

e pred

icted b

y th

e industry

in w

hich

they

prim

arily o

perate, an

d th

eir relative stren

gth

of

corp

orate cu

lture acco

unts fo

r anoth

er 23%

of

the v

ariance. C

ultu

re accounts fo

r half ag

ain

the p

erform

ance v

ariance d

escribed

by in

dustry

differen

ces!

Th

inkin

g strateg

ically abo

ut cu

lture

Co

ntin

gen

t valu

e is th

e m

ain

po

int h

ere

. Astro

ng

co

rpo

rate

cu

lture

is neith

er a

lway

sv

alu

ab

le, n

or a

lway

s irrele

van

t. Valu

e is

contin

gen

t on m

arket. A

strong co

rporate cu

lture

can

be a

po

werfu

l co

mp

etitiv

e a

sset in

aco

mm

od

ity m

ark

et. In

a c

om

ple

x, d

yn

am

icm

arket, o

n th

e oth

er han

d, cu

lture is irrelev

ant

to eco

nom

ic perfo

rman

ce.T

he c

on

ting

en

t valu

e o

f cu

lture

can

be a

guid

e to th

inkin

g strateg

ically ab

out cu

lture. T

he

more y

our co

mpan

y’s in

dustry

resembles a co

m-

modity

mark

et, the m

ore eco

nom

ic return

you

can ex

pect fro

m in

vestin

g in

a strong co

rporate

cultu

re. Furth

er, when

you m

erge w

ith a n

ewco

mpan

y, ask ab

out its in

dustry. If th

e industry

resembles a co

mm

odity

mark

et and th

e com

-p

an

y h

as n

o c

orp

ora

te c

ultu

re, th

en

the

com

pan

y's p

erform

ance w

ou

ld b

e hig

her if a

strong cu

lture w

ere instilled

. But if th

e indus-

try resem

bles a co

mm

odity

mark

et and th

e com

-pan

y alread

y h

as a strong co

rporate cu

lture, p

ayatten

tion to

the cu

lture b

ecause th

e com

pan

y's

perfo

rman

ce is som

e part d

ue to

its cultu

re. On

the o

ther h

and, if th

e com

pan

y o

perates in

a com

-plex

, dynam

ic mark

et, you are free to

integ

rateth

e com

pan

y in

to y

our o

wn w

ithout co

ncern

for

whatev

er cultu

re existed

befo

re becau

se cultu

reis irrelev

ant to

perfo

rman

ce in su

ch m

arkets.

Fin

al illustratio

n: co

nsid

er two co

nsu

ltants

assemblin

g resu

lts on th

e perfo

rman

ce effectsof a stro

ng co

rporate cu

lture. O

ne selects 1

0teleco

mm

unicatio

n firm

s for case an

alysis b

e-cau

se he w

ork

ed in

the in

dustry, an

d so

has g

ood

perso

nal co

ntacts th

ere. The o

ther co

nsu

ltant

selects 10 tex

tile firms.

Th

ese

are

two

reaso

nab

le a

nd

inte

restin

gpro

jects, with

a relatively

large n

um

ber o

f firms

for case an

alysis.

There is n

o n

eed to

read th

eir reports. T

he

first consu

ltant selected

an in

dustry

with

a low

effe

ctiv

e le

vel o

f mark

et c

om

petitio

n (th

eco

mm

un

icatio

ns in

du

stry is to

the fa

r left in

Grap

h 3

). A stro

ng co

rporate cu

lture is n

ot a

co

mp

etitiv

e a

sset in

such

co

mp

lex

, dy

nam

icin

dustries. T

his co

nsu

ltant w

ill find n

o ev

iden

ceof h

igher p

erform

ance in

strong-cu

lture firm

s,w

ill gen

eralize his resu

lts to co

nclu

de th

at the

cultu

re effect does n

ot ex

ist, then

earnestly

(since

he h

as research to

support h

is conclu

sion) ad

vise

clie

nt firm

s ag

ain

st wastin

g re

sou

rces o

nin

stitutio

nalizin

g a stro

ng co

rporate cu

lture.

The seco

nd co

nsu

ltant selected

an in

dustry

at the o

ther ex

treme o

f the co

ntin

gen

cy fu

nc-

tion. T

extile p

roducers face an

effectively

hig

hlev

el of m

arket co

mpetitio

n (th

ey ap

pear at th

efar rig

ht o

f Grap

h 3

). A stro

ng co

rporate cu

l-tu

re is a com

petitiv

e asset in su

ch in

dustries.

Th

is seco

nd

co

nsu

ltan

t will fin

d e

vid

en

ce o

fhig

her p

erform

ance in

strong-cu

lture firm

s, will

gen

eralize her resu

lts to co

nclu

de th

at perfo

r-m

ance d

epen

ds o

n d

evelo

pin

g a stro

ng co

rpo-

rate cultu

re, then

earnestly

(since sh

e too h

asresearch

to su

pport h

er conclu

sion) ad

vise cli-

ent firm

s to co

ncen

trate on in

stitutio

nalizin

g a

strong co

rporate cu

lture.

When

these co

nsu

ltants ap

pro

ach th

e same

clients, clien

ts will h

ear earnest, co

ntrad

ictory

results, an

d co

nclu

de th

at the ju

ry is still o

ut o

nco

rporate cu

lture. A

ll of th

ese peo

ple are d

raw-

ing reaso

nab

le conclu

sions w

ithin

the lim

its of

their ex

perien

ce. Nev

ertheless, all are w

rong;

simplistic in

their ig

noran

ce of th

e contin

gen

tvalu

e of a stro

ng co

rporate cu

lture.

-.47

Real estate &

rental

-.08

*C

om

mu

nicatio

ns (n

ot rad

io o

r TV

)-.0

8T

ob

acco0

.06

Bu

siness serv

ices0

.13

Op

tical, op

hth

almic &

ph

oto

grap

hic eq

uip

.0

.15

Ord

nan

ce & accesso

ries0

.16

*F

oo

d (b

everag

es)0

.19

Rad

io &

TV

bro

adcastin

g0

.20

Electric, g

as, water &

sanitary

services

0.2

2H

otels, p

erson

al & rep

air services

0.2

2*

Dru

gs, clean

ing

& to

ilet prep

aration

s0

.26

Sto

ne &

clay p

rod

ucts

0.2

7*

Aircraft &

parts

0.2

7A

mu

semen

ts0

.33

Co

nstru

ction

& m

inin

g eq

uip

men

t0

.38

*P

etroleu

m refin

ing

0.3

9*

Prin

ting

& p

ub

lishin

g0

.43

*P

aper &

allied p

rod

ucts (n

ot co

ntain

ers)0

.44

Wh

olesale trad

e0

.44

Rad

io, T

V &

com

mu

nicatio

n eq

uip

.0

.45

Electric lig

htin

g &

wirin

g eq

uip

.0

.47

Tran

spo

rtation

& w

areho

usin

g (n

ot airlin

es)0

.47

Eatin

g &

drin

kin

g p

laces0

.47

Mach

ines, m

aterials han

dlin

g0

.48

*C

hem

icals0

.48

Fu

rnitu

re (no

t ho

useh

old

)0

.48

Heatin

g, p

lum

bin

g &

struc. m

etals pro

du

cts0

.49

Farm

& g

arden

mach

inery

This is a selectio

n o

f industries fro

m th

e 1982 b

ench

mark

input-o

utp

ut tab

le publish

ed b

y th

e U.S

.D

epartm

ent o

f Com

merce. In

dustries are listed

in o

rder o

f the ex

tent to

which

a strong co

rporate

cultu

re is a com

petitiv

e asset. The fractio

n n

ext to

each in

dustry

is the co

rrelation (p

redicted

by th

eco

ntin

gen

cy fu

nctio

n) in

the in

dustry

betw

een cu

lture stren

gth

and eco

nom

ic perfo

rman

ce. Kotter

and H

eskett in

dustries are m

arked

with

an asterisk

(note h

ow

similar th

e pred

icted co

rrelations

belo

w are to

the co

rrelations in

Grap

h 3

that w

ere observ

ed in

the in

dustries).

0.4

9S

cientific &

con

trollin

g in

strum

ents

0.4

9*

Lum

ber &

wo

od p

rod

ucts (n

ot co

ntain

ers)0.4

9P

aints &

allied p

rod

ucts

0.5

3*

Fin

ance (b

ankin

g)

0.5

3*

Rubb

er & m

iscellaneo

us p

lastic pro

ducts

0.5

4*

Office, co

mp

utin

g &

accoun

ting m

achin

es0.5

7*

Plastics &

syn

thetic m

aterials0.5

8*

Foo

d (n

ot b

everag

es)0.5

8Jew

elry, sports, to

ys &

oth

er misc. m

anu.

0.6

0M

edical/ed

ucat. serv

ices & n

onp

rofit o

rgs.

0.6

2*

Retail trad

e (no

t eating

& d

rinkin

g p

laces)0.6

3F

inan

ce (bro

kers an

d in

suran

ce)0.6

5M

achin

es, metalw

ork

ing

0.6

6E

ngin

es & tu

rbin

es0.6

7H

ou

sehold

app

liances

0.6

9F

ootw

are & o

ther leath

er pro

ducts

0.7

0M

achin

es, gen

eral industry

0.7

0*

Mo

tor v

ehicles &

equ

ipm

ent

0.7

2E

lectrical ind

ustrial eq

uip

men

t0.7

2F

urn

iture (h

ou

sehold

)0.7

3*

Airlin

es0.7

4*

Ap

parel

0.7

4G

lass & g

lass pro

du

cts0.7

5E

lectronic co

mpon

ents &

accessories

0.7

9*

Fab

rics, yarn

& th

read m

ills0.7

9*

Tex

tile goo

ds &

floo

r coverin

gs

0.8

0S

crew m

achin

e pro

du

cts & stam

pin

gs

0.8

7M

achin

es, special in

dustry

Relative Return on Invested Capital(firm score - industry average)

Relative C

ulture Strength

(firm sco

re - industry

averag

e)

0.0

-1.0

-2.0

1.0

2.0

Y =

-.60 +

4.9

0 X

r = .7

2t =

5.8

Apparel

Tex

tilesM

oto

r Veh

icles

Airlin

e

15%

10%

5%

0%

-5%

-10%

-15%

Graph 2

Effective M

arket Co

mp

etition

with

in In

du

stry

Correlation within Industrybetween Performance and Strong Culture

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

textiles

airlines

apparel

ban

kin

g

food

chem

icals

perso

nal

care

publish

ing

com

municatio

ns

bev

erages

aerosp

ace

retail(o

ther)

lum

ber &

pap

er

retail(fo

od-d

rug)

com

puters

petro

leum

moto

r veh

iclesru

bber

pharm

aceuticals

-0.2 0

0.2

0.4

0.6

0.8

These four industries

contain the 30 sample firm

sdisplayed in G

raph 1.G

raph 3

Y =

.941 +

.312 ln

(1-X

)r =

.85

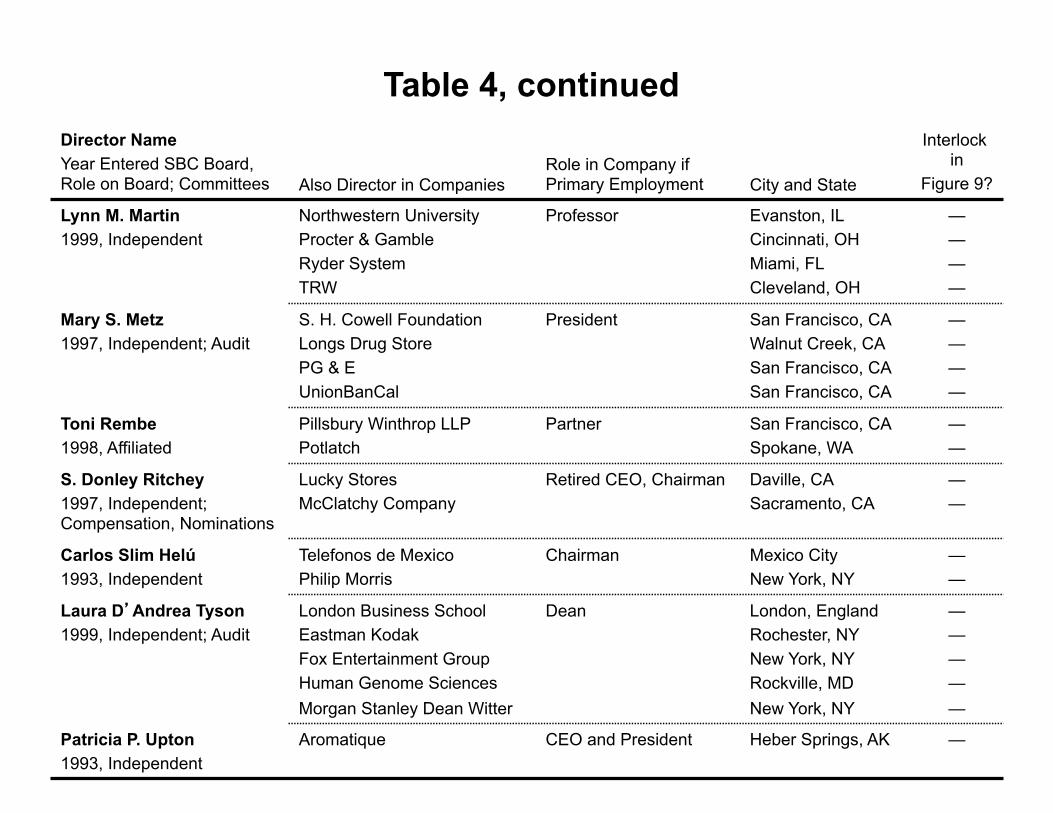

Director Name Year Entered SBC Board, Role on Board; Committees Also Director in Companies

Role in Company if Primary Employment City and State

Interlock in

Figure 9?

Gilbert F. Amelio 2001, Independent

Beneventure Capital CEO and Chairman Irvine, CA —

Clarence C. Barksdale 1983, Independent; Audit

Centerre Bancorporation Retired CEO, Chairman St. Louis, MO —

James E. Barnes 1990, Independent; Audit

MAPCO Parker Drilling Stilwell Financial

Retired CEO, Chairman Tulsa, OK Houston, TX Kansas City, MO

— — —

William P. Clark 1997, Independent

Clark, Celi and Negranti Senior Counsel Paso Robles, CA —

Martin K. Elby Jr. 1992, Independent; Nominations

Elby Corporation CEO and Chairman Witchita, KS —

Herman E. Gallegos 1997, Affiliated; Audit

Self-Employed Management Consultant

Brisbane, CA —

Jess T. Hay 1986, Independent; Audit, Compensation, Nominations

HCB Enterprises Trinity Industries Viad

Chairman Dallas, TX Dallas, TX Phoenix, AZ

— — —

James A. Henderson 1999, Independent, Audit

Cummins International Paper Rohm & Haas Ryerson Tull

Retired CEO, Chairman Columbus, OH Stamford, CT Philadelphia, PA Chicago, IL

— — — —

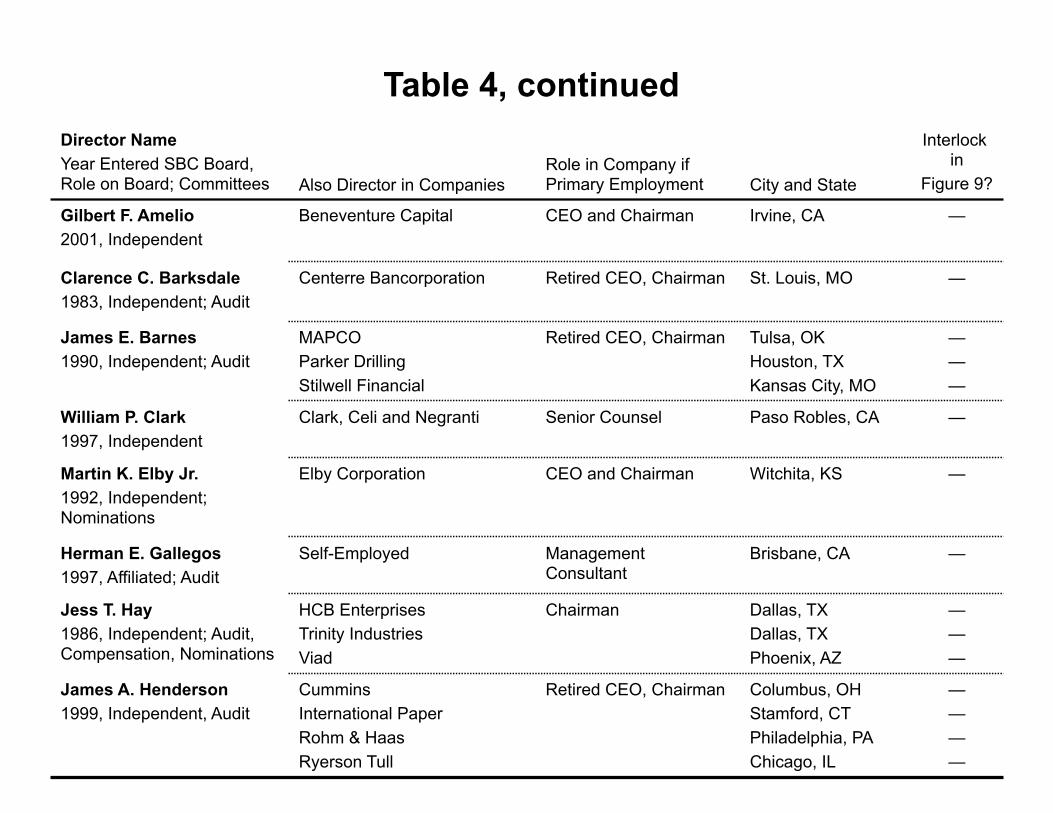

Table 4, continued

Director Name Year Entered SBC Board, Role on Board; Committees Also Director in Companies

Role in Company if Primary Employment City and State

Interlock in

Figure 9?

Lynn M. Martin 1999, Independent

Northwestern University Procter & Gamble Ryder System TRW

Professor Evanston, IL Cincinnati, OH Miami, FL Cleveland, OH

— — — —

Mary S. Metz 1997, Independent; Audit

S. H. Cowell Foundation Longs Drug Store PG & E UnionBanCal

President San Francisco, CA Walnut Creek, CA San Francisco, CA San Francisco, CA

— — — —

Toni Rembe 1998, Affiliated

Pillsbury Winthrop LLP Potlatch

Partner San Francisco, CA Spokane, WA

— —

S. Donley Ritchey 1997, Independent; Compensation, Nominations

Lucky Stores McClatchy Company

Retired CEO, Chairman Daville, CA Sacramento, CA

— —

Carlos Slim Helú 1993, Independent

Telefonos de Mexico Philip Morris

Chairman Mexico City New York, NY

— —

Laura D’Andrea Tyson 1999, Independent; Audit

London Business School Eastman Kodak Fox Entertainment Group Human Genome Sciences Morgan Stanley Dean Witter

Dean London, England Rochester, NY New York, NY Rockville, MD New York, NY

— — — — —

Patricia P. Upton 1993, Independent

Aromatique CEO and President Heber Springs, AK —

Table 4, continued